This event is free and open to ALL UD students (undergraduate and graduate), faculty,and prospective students of the UD FASH program, but registration is required (please use .edu email address): https://www.wita.org/events/pathways-careers-behind-the-seams/

Note: Students in FASH455-010 (Tue and Thu) do not need to register for the event. We will attend the workshop and participate in the live Q&A session in the classroom.

Featured speakers (bios here) from JCPenney include:

Amanda Blackman, Director of Planning and Allocation

Michelle Erwin, Sourcing Manager

Hunter Green, Senior Manager of International Transportation

Angela Hofmann, VP, Government Affairs

Wayne Milano, SVP, Global Sourcing and Product Development

Aqsa Tasleem, Senior Manager of Fabric & Sustainability

As the fashion industry grapples with increasing demands for sustainability, transparency, and social responsibility, the next generation of industry professionals—Generation Z—will play a crucial role in shaping the future of apparel sourcing and social responsibility practices in the industry.

This session explores how US college fashion programs equip Gen Z with critical knowledge in due diligence, sustainable sourcing, and supply chain transparency. Including voices from educators, Gen Z students (future professionals), and industry partners, the session will share best education practices, identify educational gaps, and present valuable Gen Z’s vision for improving due diligence and social responsibility in the garment industry. Additionally, the session will emphasize the increasing importance of industry-academic partnerships in curriculum development and talent preparation, illustrating the long-term benefits of such collaboration.

This session is highly relevant to industry professionals, educators, students, international organizations, and policymakers interested in supporting the next generation of fashion leaders and fostering a more socially responsible and sustainable fashion industry.

For FASH455 students: Please share your reflections on the video regarding the free trade debate. You can focus on analyzing 1-2 specific debates raised in the video (e.g., comparing the arguments from both sides) and then share your thoughts. Please do not simply state your “opinion,” but use examples, statistics, or trade theories we learned to support your viewpoint.

In December 2024, Just-Style consulted a panel of industry experts and scholars in its Shape of apparel sourcing in 2025 briefing. Below is my contribution to the report. Welcome any comments and suggestions!

What’s next for apparel sourcing

Although the world economy is predicted to grow at a similar pace in 2025 from 2024, the slowing US and Chinese economies could impose new challenges to apparel sourcing, from weakened demand to intensified price competition.

Regarding the macroeconomic environment in 2025, which “sets the tone” for apparel sourcing, the International Monetary Fund (IMF) and the World Bank estimated that the world economy would grow by approximately 2.7-3.2 percent in 2025, with almost no change from the previous year. Similarly, the World Trade Organization (WTO) projected that world merchandise trade would increase by 3.3 percent in 2025, slightly higher than 2.6 percent in 2024.

Despite this incremental improvement, the world’s two largest economies–the US (with 2.2 percent GDP growth in 2025, down from 2.8 in 2024 and 2.9 in 2023) and China (with 4.5 percent GDP growth in 2025, down from 4.8 in 2024 and 5.2 in 2023) are expected to experience slower economic growth in the new year ahead. This slowdown means that apparel producers around the world, particularly those developing countries making large-volume basic items, will likely continue to struggle with a shortage of souring orders in 2025 due to overall weak import demand.

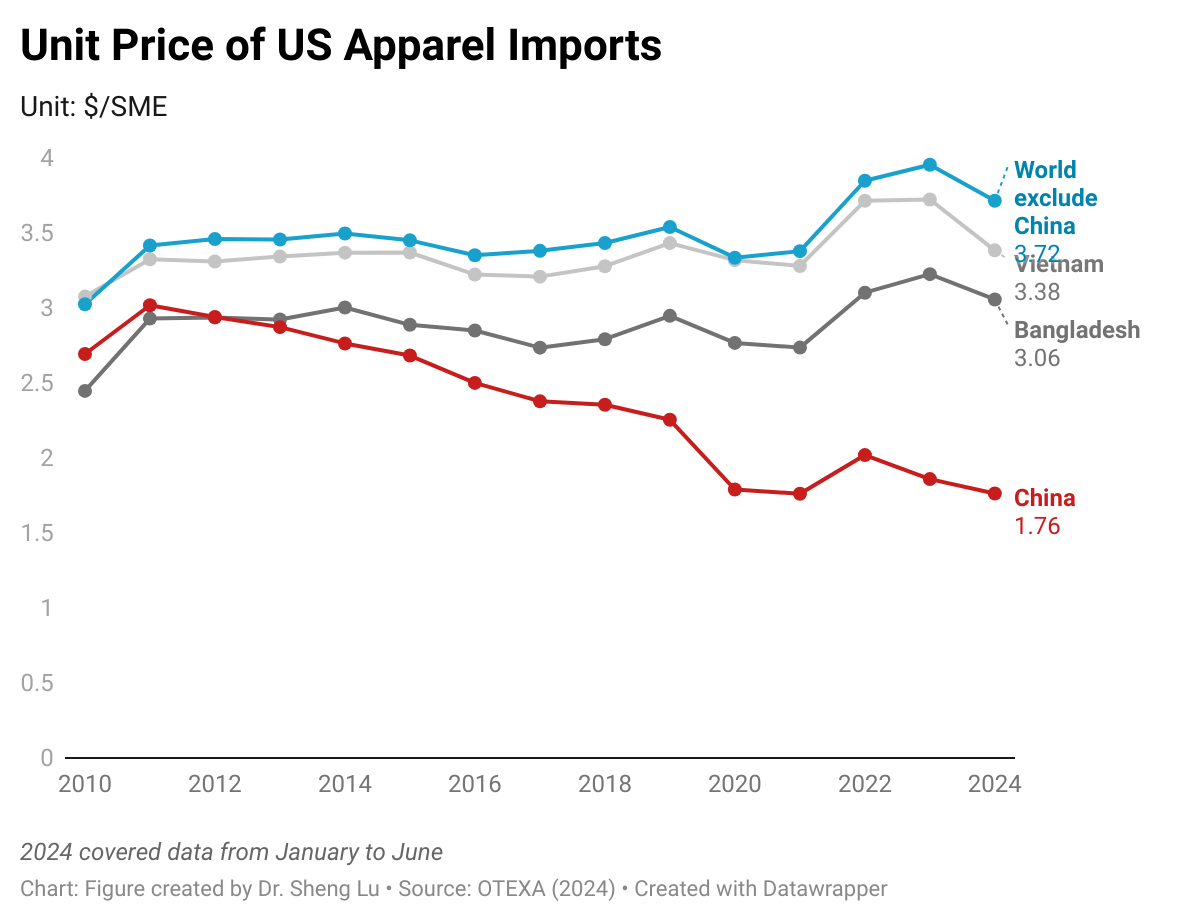

Even more concerning, as China grapples with declining domestic sales, the world clothing market could see an additional influx of low-cost Chinese products, especially through new e-commerce channels. Notably, less than half of China’s clothing production is exported, indicating its significant untapped export capacity. Furthermore, while China’s wage levels are higher than those in many other Asian apparel-producing countries, the unit price of U.S. apparel imports from China measured in dollar per square meter equivalent ($/SME) dropped by more than 21% between 2018 and 2024 (up to October). In contrast, U.S. apparel import prices from the rest of the world increased by 7.8% over the same period. Related to this, what is often overlooked is that even Shein, the “ultra-fast fashion” retailer known for its exceptionally competitive pricing, deliberately opted out of the vast Chinese market due to concerns about the intense price competition there. In other words, disregarding the new Trump tariff, 2025 could see an escalation of trade tensions targeting Chinese products in the US market and beyond.

Meanwhile, due to concerns about rising geopolitical tensions worldwide and trade policy uncertainty during Trump’s second term, fashion companies will likely continue to leverage sourcing diversification to mitigate risks. However, the “reducing China exposure” and sourcing diversification movement has yet to substantially benefit near-shoring or emerging sourcing destinations such as the Western Hemisphere and Sub-Saharan Africa (SSA). This result was mainly because fashion companies utilized China to source a wide range of various products, whereas Western Hemisphere and SSA suppliers can only produce a few basic categories.

For example, my latest studies show that in the first nine months of 2024, even excluding major platforms like Shein, Amazon, and Temu, US fashion companies sourced more than 60K Stock Keeping Units (SKUs) of clothing items from China. In comparison, India and Vietnam each supplied approximately 15K SKUs, Cambodia and Bangladesh each contributed 3,000 SKUs, Mexico provided only 2K SKUs, and CAFTA-DR and AGOA member countries supplied around 200 SKUs each. Therefore, even if fashion companies report sourcing from more countries, they are likely to stay sourcing from more Asian countries with closer export capacity and structure to China. Meanwhile, the total value or volume of trade may not fully capture the whole picture of sourcing diversification. This trend may persist in 2025, even with new tariff escalations.

Apparel industry challenges and opportunities

Today’s fashion business is highly global and relies heavily on the frequent movement of goods and services across borders. Thus, the uncertain and protectionist nature of U.S. trade policy during Trump’s second term could present significant challenges to the fashion industry in 2025. Of particular concern is that Trump’s new tariff actions would raise fashion companies’ sourcing costs, create additional inflationary pressure, reduce US consumers’ purchasing power on clothing, and trigger retaliatory trade measures from U.S. trading partners, ultimately hurting the U.S. economy. Notably, when the 7.5% Section 301 tariff was imposed on selected Chinese clothing products in 2018, the U.S. Consumer Price Index (CPI) growth was relatively low at 1.9%. However, imposing a 20% global tariff, a 60% tariff on Chinese products, and the existing 15%-30% regular tariff on clothing when the CPI is historically high is like “adding fuel to the fire.”

Besides tariffs, in 2025, if not sooner, U.S. fashion companies and many e-commerce suppliers worldwide will closely watch how Congress and the new Trump administration reform the de minimis rule, which currently exempts small-value shipments under $800 from tariffs and most customs procedures. With Trump’s new tariffs looming, some argue that closing the de minimis “loophole” has become even more urgent, as it creates more financial incentives to use the rule to bypass the tariff increase. Meanwhile, proposals under consideration suggest removing textile and apparel products entirely from de minimis, a move that could be an “earthquake” for those fashion companies utilizing the rule heavily.

Trump’s approach and philosophy toward conventional trade agreements and trade preference programs in 2025 also deserve attention. During his first term, Trump launched a few bilateral trade negotiations, from the one with the United Kingdom and Japan to Kenya. Back then, Trump saw a bilateral agreement would give the U.S. more leverage for a better “deal.” Specifically related to apparel sourcing and trade, two flagship U.S. trade preference programs–the African Growth and Opportunity Act (AGOA) and the Haiti HOPE/HELP Act, will expire in September 2025. It remains uncertain whether the new Trump administration will support the early renewal of these two trade preference programs with minimal changes or prefer to renegotiate them and add new bilateral elements.

Additionally, even though the new Trump administration may not prioritize addressing climate change, it is an irreversible trend for fashion companies to allocate more resources to comply with upcoming or newly implemented sustainability and environmental-related legislation, whether from the EU or the US state level. Unlike in the past, when being more sustainable only meant adding operational costs or paying a “one-time fee,” today’s new generation of sustainability-focused regulations—such as Extended Producer Responsibility (EPR)—requires companies to shift their mindset and demonstrate continuous improvement. Interestingly, my recent study tracking apparel products’ sustainability claims shows that vague terms like “sustainable” and “eco-friendly” are gradually being replaced by more neutral, fact-based keywords such as “regenerative,” “textile waste,” and “low impact.”

Meanwhile, offering “sustainable” apparel products and those using “preferred sustainable fibers” could provide fashion companies new opportunities to diversify their sourcing base and expand their vendor networks. For example, studies show that in the U.S. market, China and many other Asian countries are not necessarily the top suppliers of clothing made with recycled materials. Instead, Europe and countries in the Western Hemisphere or even Africa present unique sourcing advantages and capacities due to the unique nature of such products. Therefore, in 2025, we can expect an ever-closer collaboration between design, product development, merchandising, sourcing, and legal teams within fashion companies, working together to meet the growing demand for sustainable apparel and ensure compliance with evolving regulations.

The full article is published in Just-Style and below is the summary:

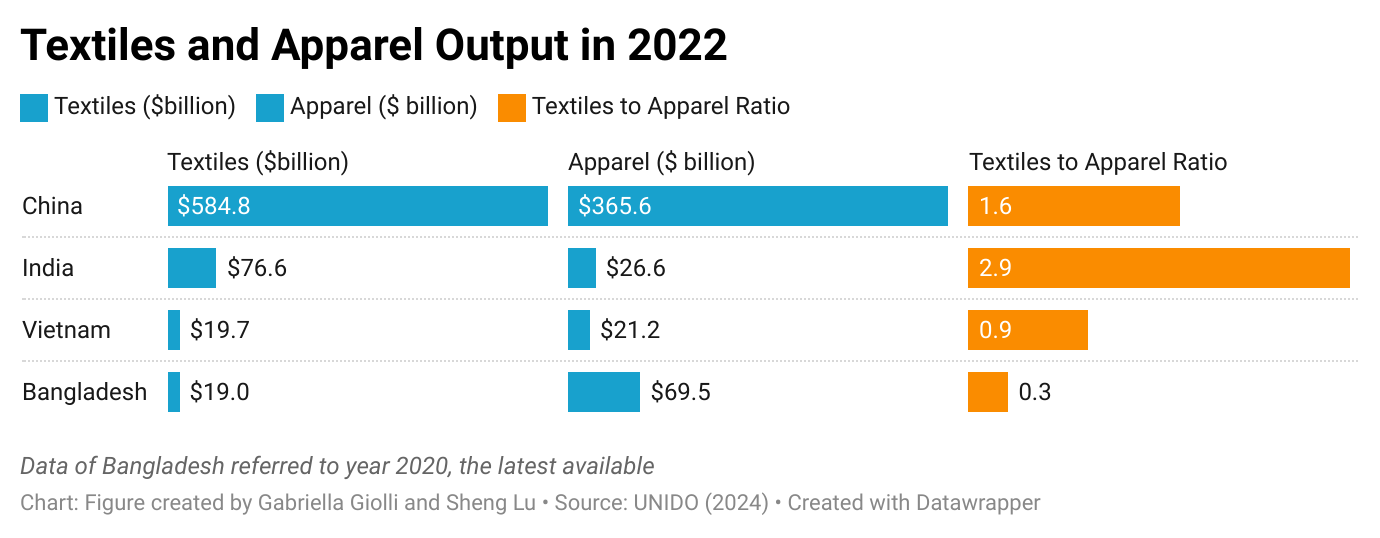

India’s Textiles and Apparel Production

Data from the United Nations Industrial Development Organization (UNIDO) shows that India produced around $76.5 billion in textiles and $26.64 billion in wearing apparel in 2022. Although still smaller than China’s, this production scale has already surpassed that of most other Asian countries, including Vietnam. Behind these numbers were India’s over 4,000 ginning factories, 3,500 textile mills, and around 45 million workers directly employed by the textile and apparel sector.

India is one of the world’s largest textile fiber producers, including regular cotton, organic cotton, silk, polyester, and viscose. India also has more advanced local textile manufacturing capabilities than most other developing apparel-exporting Asian countries, allowing it to benefit from a vertically integrated local textile and apparel supply chain. A recent U.S. International Trade Commission (USITC) study noted that more than 90 percent of India’s textile raw materials needed for its apparel production can be sourced domestically. In comparison, as the World Trade Organization (WTO) global value chain analysis estimated, more than 64 percent of Vietnam’s apparel exports in 2022 contained foreign-made content (i.e., imported yarns and fabrics), 57 percent for Cambodia, 49 percent for Indonesia, and 33 percent for Bangladesh.

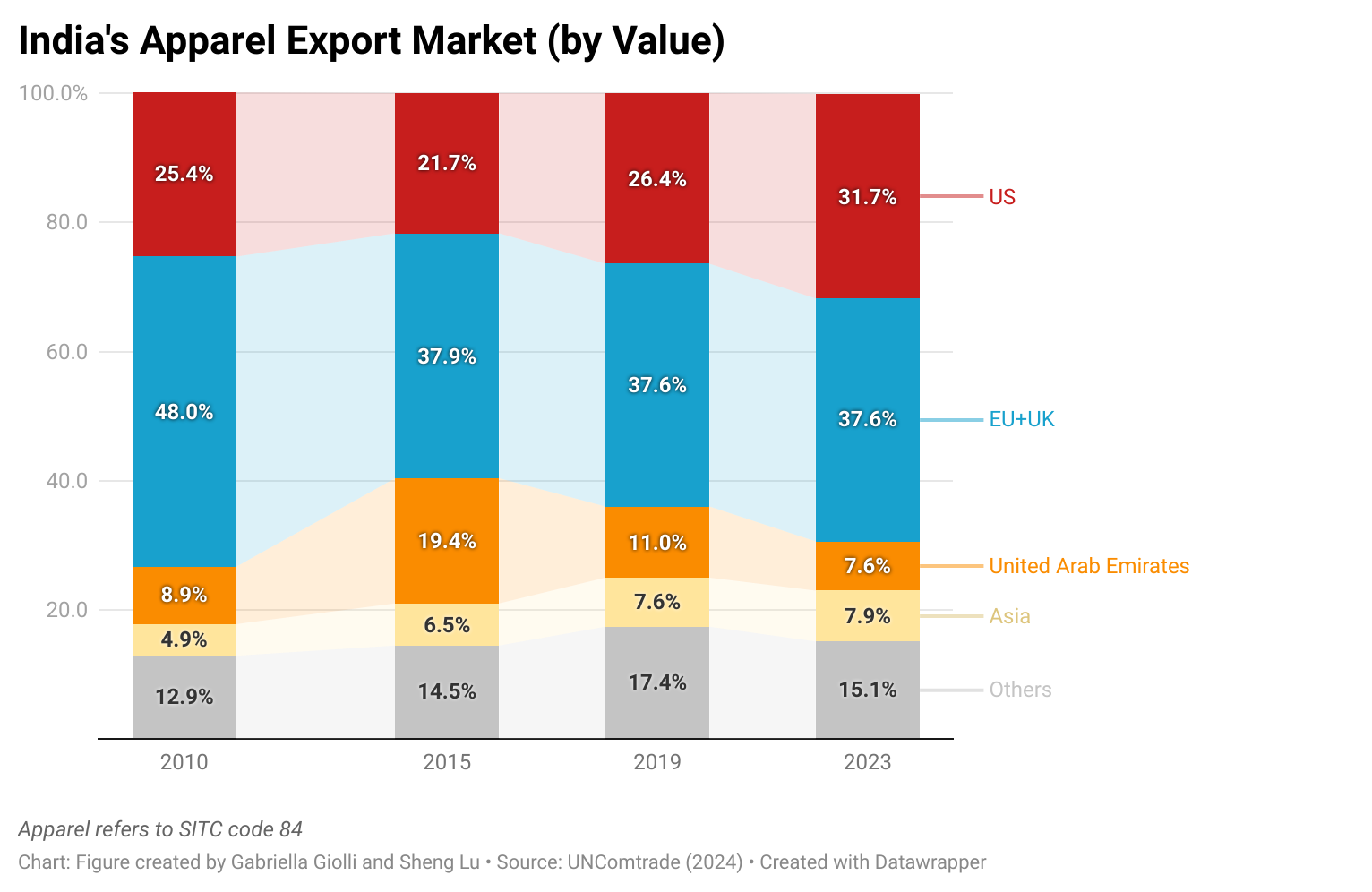

India’s Apparel Export

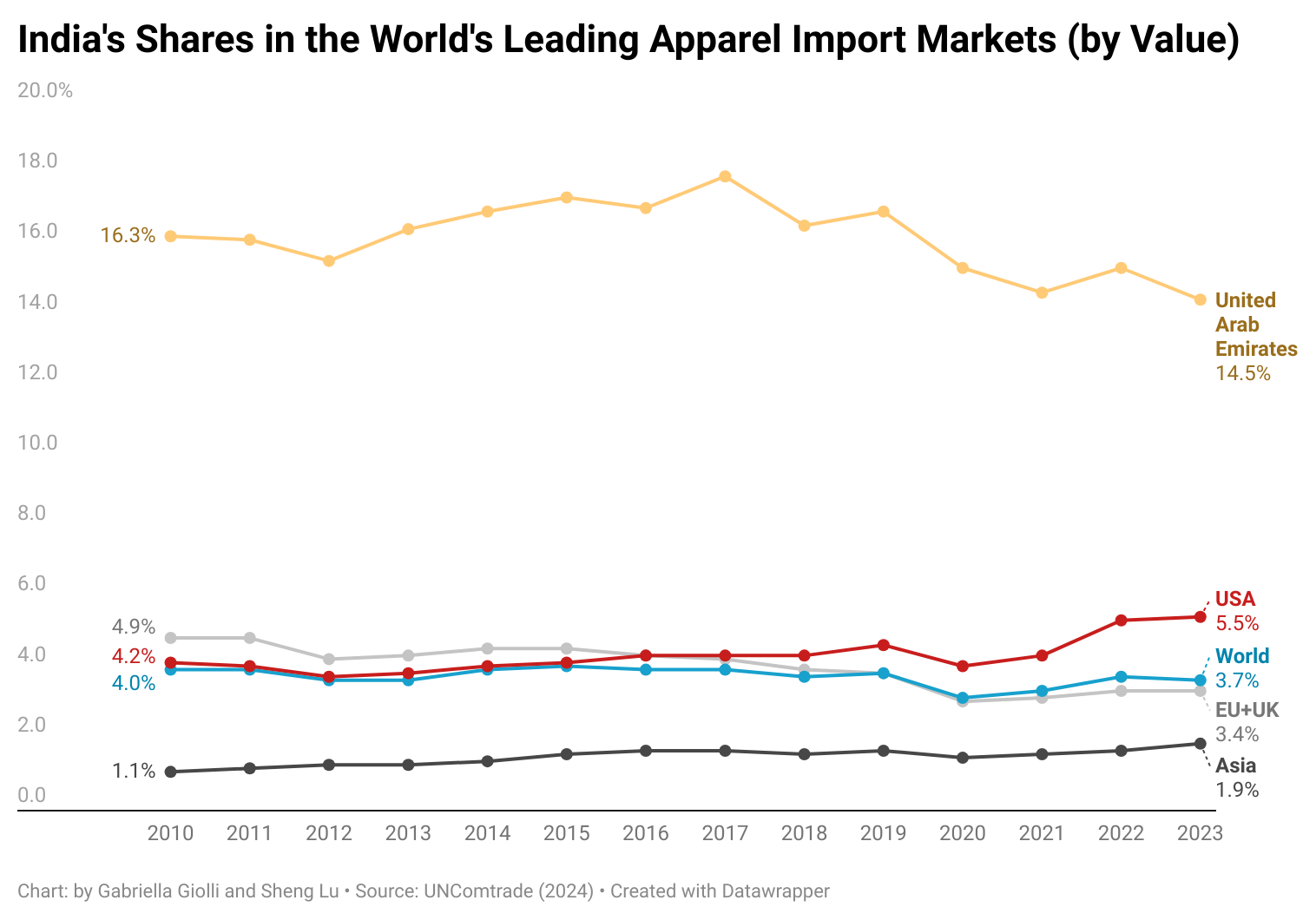

India remained a much smaller apparel exporter than China, Vietnam, and Bangladesh. According to the World Trade Organization (WTO), India exported about $15 billion in apparel in 2023, ranked the world’s sixth largestor 2.8 percent of the global total. Similarly, in 2023, India accounted for 5.5 percent of U.S. apparel imports and 3.5 percent of the EU, showing its position as a significant supplier but not among the largest. However, unlike most other developing Asian countries, India exports less than half of its apparel output due to its massive domestic market with a population of 1.43 billion. This implies that India’s substantial untapped apparel export potential should not be ignored.

Why Sourcing from India?

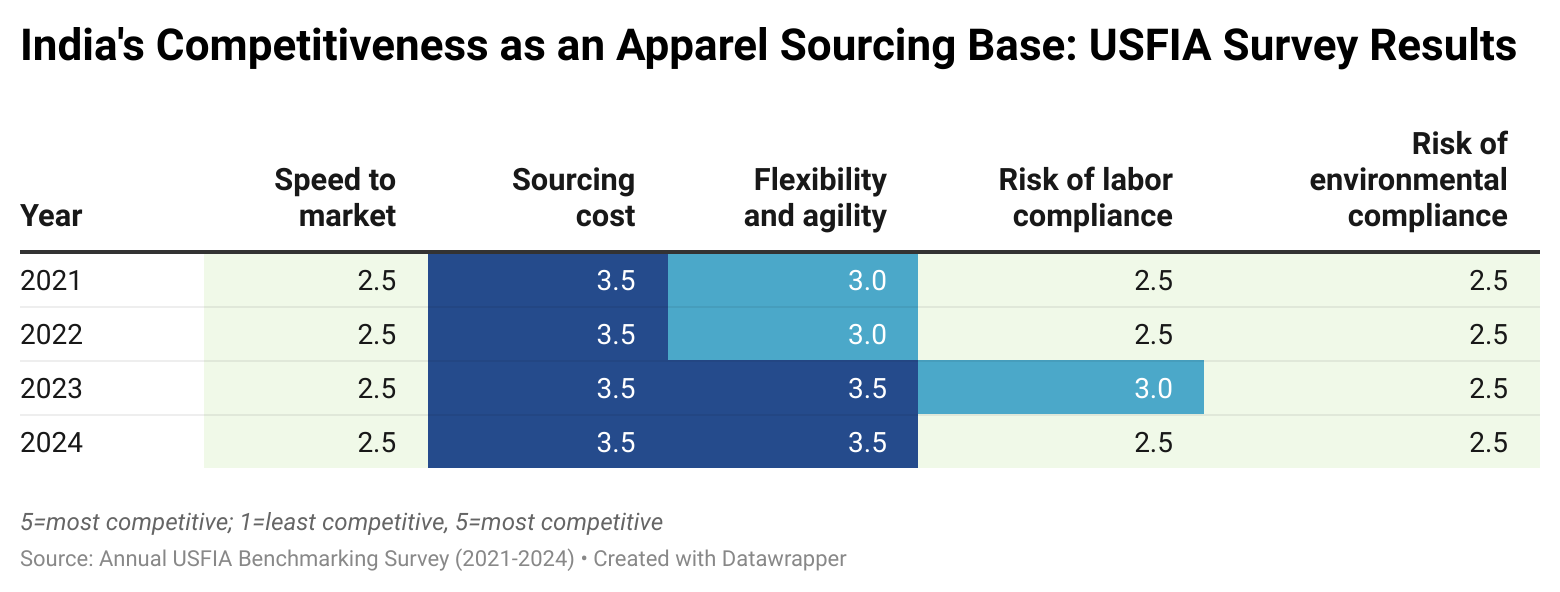

Firstly, aligned with trade statistics, many U.S. fashion companies already source from India, although in a relatively small volume. For example, the USFIA benchmarking survey respondents consistently ranked India as the 3rd or 4th most utilized apparel sourcing base from 2021 to 2024, after China and Vietnam. However, U.S. fashion companies typically place less than 10 percent of their total sourcing value or volume in India. The recent USITC study also raised concerns that India’s apparel factories were primarily small and medium-sized, which could limit their ability to fulfill large-volume sourcing orders.

Secondly, “Made in India” clothing is not necessarily cheap but could be perceived as “worth the value.” Notably, from January to October 2024, clothing labeled “Made in India” sold in the U.S. retail market was, on average, priced much higher than imports from Bangladesh and Vietnam, particularly in the mass market segment. Meanwhile, in the premium market segment, clothing “Made in India” was, on average, priced relatively lower than “Made in China,” such as dresses, tops, and bottoms. These results suggest that U.S. fashion companies do not typically consider India a preferred sourcing base for basic and price-sensitive items. Instead, India may be seen as a more cost-effective alternative to China for high-quality, value-added clothing.

Thirdly, India has been strengthening its competitiveness in export flexibility and agility, enabling its vendors to quickly adjust the delivery, volume, and product of the sourcing order upon customers’ requests. In the latest 2024 USFIA survey, respondents rated India’s sourcing flexibility and agility second only to China, surpassing Bangladesh, Cambodia, and Central American countries. Likewise, India was regarded as one of the few Asian countries that could fulfill apparel sourcing orders with relatively low “minimum order quantity (MOQ)” requirements.

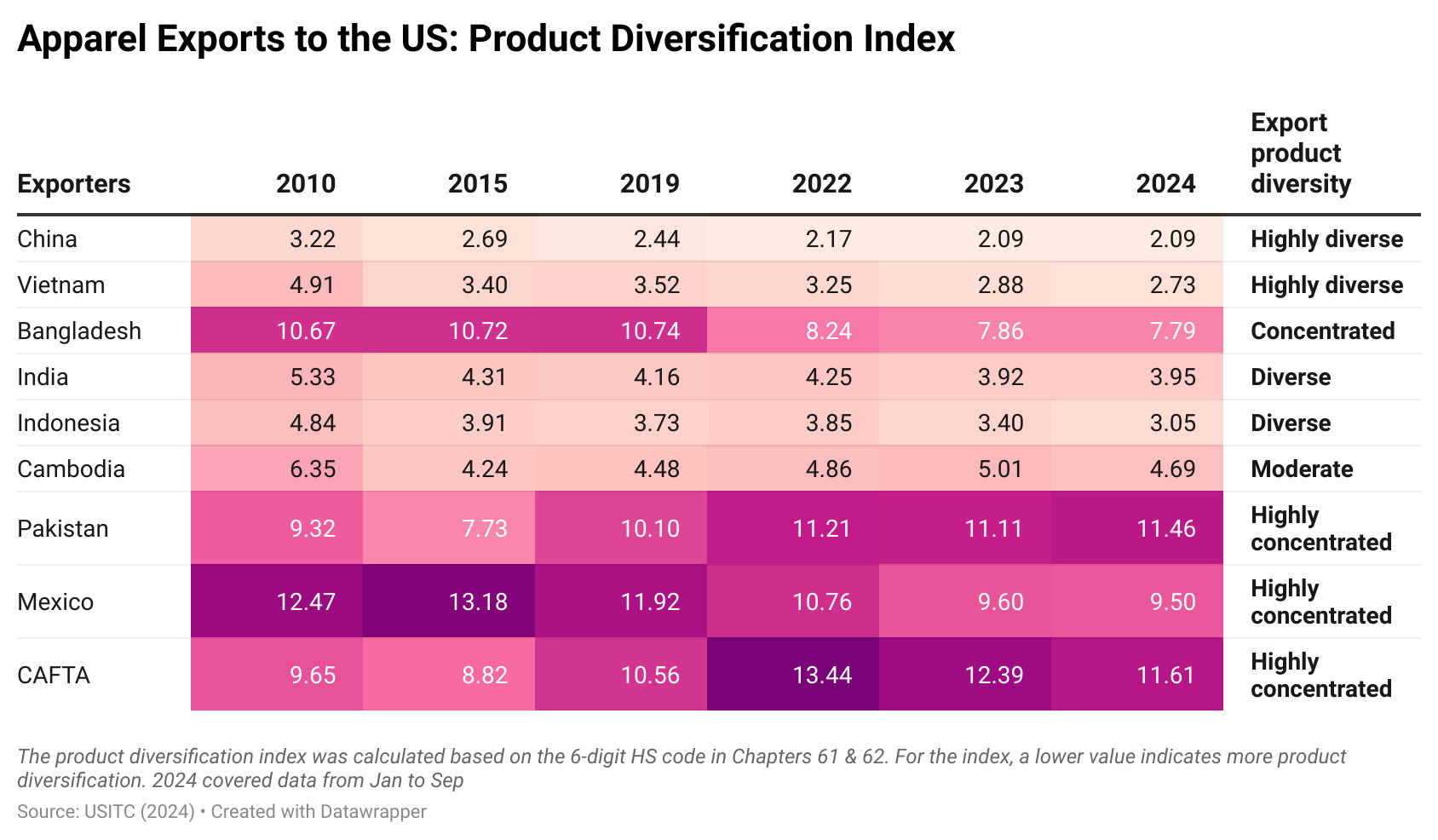

One major factor contributing to India’s perceived advantages in sourcing flexibility and agility is its ability to produce a wide range of apparel products. For example, the Herfindahl-Hirschman Index (HHI) calculated using trade data at the 6-digit HS code level indicates that U.S. apparel imports from India cover more diverse product categories than most Asian countries.

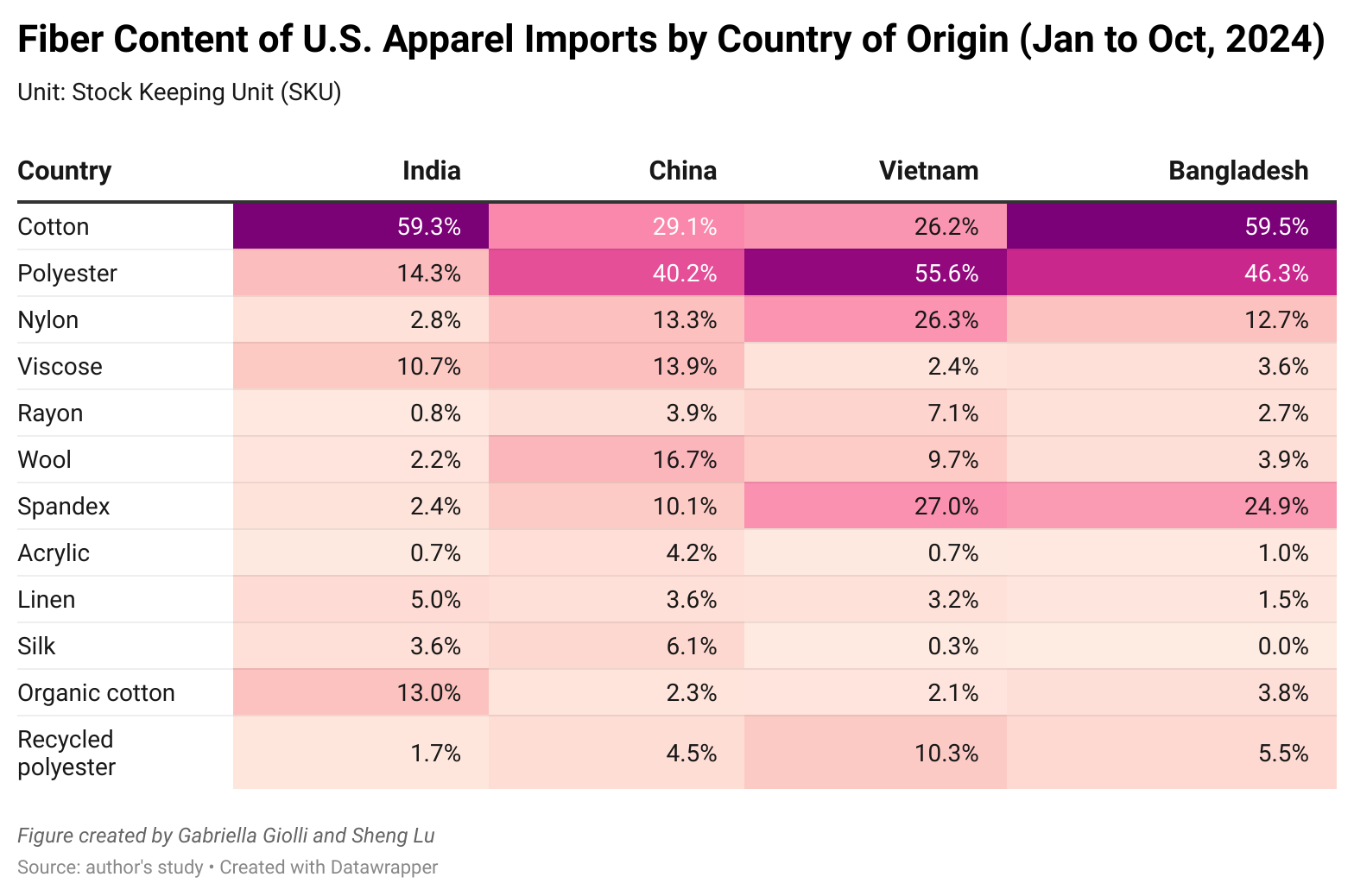

Moreover, due to India’s position as one of the world’s leading cotton producers, in the first ten months of 2024, nearly 60 percent of U.S. apparel imports from India contained cotton fibers, including 13 percent using organic cotton. This percentage was much higher than imports from other Asian suppliers such as China and Vietnam. In comparison, over the same period, U.S. apparel imports from India appear less likely to contain man-made fibers like polyester, nylon, spandex, and recycled polyester. This fiber composition explains why India has yet to become a leading supplier of certain apparel product categories, like outerwear, which more commonly uses man-made fiber than cotton.

Additionally, in the first ten months of 2024, over 45 percent of India’s apparel newly introduced to the U.S. market targeted the luxury and premium segment, closely matching China’s nearly 50 percent and exceeding other Asian suppliers such as Vietnam (20 percent), Bangladesh (13 percent), Cambodia (5 percent), and Indonesia (18 percent). This result explains why U.S. fashion companies increasingly consider India a strategic alternative to sourcing from China, given the similarities in their product offerings.

Reflections

India’s large country size and population, the presence of an already highly integrated and sophisticated textile and apparel supply chain, and its ability to make a great variety of high-quality products suitable for various market segments position it well in the export competition. U.S. fashion companies’ eagerness to reduce sourcing from China due to rising geopolitical concerns and the limited sourcing capacity elsewhere created historical opportunities for India to expand its apparel exports to the U.S. market further.

Nevertheless, it remains a question mark whether India is fully committed to expanding labor-intensive apparel production and exports, given the country’s economy is moving toward more capital and technology-intensive sectors. Notably, in value, apparel only accounted for about 5.6 percent of India’s total merchandise exports in 2023, similar to China’s 5.3 percent but much lower than other lesser-developed Asian countries, including Vietnam (10 percent), Bangladesh (88 percent), and Cambodia (44 percent).

Moreover, while India is not a primary focus for compliance issues like forced labor, sourcing from the country still carries general social and environmental compliance risks similar to those in most developing countries (note: see the 2024 USITC report). It remains to be seen whether India’s textile and apparel mills are technically and financially prepared to meet more stringent social and environmental standards being adopted in the U.S. and can effectively compete in the growing market for “sustainable apparel.”

by Gabriella Giolli (Honors Marketing major & Fashion management minor, University of Delaware) and Sheng Lu

About the interview: Fashion is possible because of international trade. Each year, the global fashion industry generates more than $4 trillion USD and provides families with affordable clothing options. However, as fast fashion continues to grow, so does awareness of pressing issues such as labor standards and environmental sustainability. How are the United States and China involved in the global fashion industry? How can they collaborate on the issues facing the global fast fashion industry, from production to consumption?

Sheng Lu joins the National Committee to discuss how fast fashion is a global phenomenon and how the United States and China can address common areas of concern.

The event was hosted by the Washington International Trade Association on October 9, 2024

Panelists

Ralph Carter, Staff Vice President, Regulatory Affairs, FedEx

Kim Glas, President & CEO, National Council of Textile Organizations; Commissioner, U.S.-China Economic and Security Review Commission

Melissa Irmen, Director of Advocacy, NAFTZ-National Association of Foreign-Trade Zones

John Pickel, Senior Director, International Supply Chain Policy, National Foreign Trade Council

Felicia Pullam, Executive Director, Office of Trade Relations, U.S. Customs and Border Protection

Ana Swanson, Trade and International Economics Reporter, The New York Times (Moderator)

Event summary: Competing views about de minims and its reform

Arguments supporting De Minimis: Proponents like Ralph from FedEx argue that de minimis reduces trade friction, drives international supply chain efficiency, and allows U.S. companies to offer competitive pricing through free returns and streamlined customs processes. Meanwhile, they argue that the de minimis supports low-income U.S. consumers and enables small U.S. businesses to remain competitive.

Criticism of De Minimis: Critics, including Kim Glas from the National Council of Textile Organizations (NCTO), argue that it undercuts U.S. manufacturers, especially in industries like textiles, by allowing cheap imports from countries like China, often bypassing tariffs and safety regulations. They also say that de minimis was unfair to U.S. retailers that pay millions of dollars of tariff duties. Additionally, there are significant concerns about the safety risks posed by counterfeit goods and dangerous products (e.g., fentanyl) entering under de minimis exemptions.

Challenges of dealing with de Minimis: Felicia from the U.S. Customs and Border Protection (CBP) emphasizes the strain on the agency’s resources due to the sheer volume of de minimis shipments—it surged from about 2.8 million shipments per day in fiscal year 2023 to close to 4 million shipments per day in fiscal year 2024. She highlighted challenges such as the often unreliable information the de minimis imports submitted and the outdated authorities that hinder CBP’s enforcement.

Equal treatment for U.S. Foreign Trade Zones: U.S. Foreign Trade Zones (FTZs) are designated areas within the United States that are considered outside U.S. customs territory for import duties. They allow businesses to import, store, assemble, manufacture, or process goods with deferred or reduced customs duties, which are only paid when goods leave the FTZ and enter U.S. commerce. Currently, U.S. FTZs do not benefit from the de minimis exemption, meaning goods imported directly into the U.S. from overseas warehouses can qualify for de minimis, but goods entering through U.S. FTZs do not.

Melissa Irmen from NAFTZ-National Association of Foreign-Trade Zones advocates for U.S. foreign trade zones to be given the same de minimis privileges as foreign warehouses, arguing that this would ensure better oversight and security while maintaining trade efficiency. Critics, however, say that expanding de minimis in this way would exacerbate the problem rather than fix it.

Reforming the De minimis: There is a push for comprehensive reform of the De minimis system, with proposals ranging from raising duties on certain products to eliminating the exemption altogether for specific categories of goods (e.g., textiles, products subject to Section 301 tariffs).

Particularly, in a face sheet released in September 2024, the Biden Administration announced it would address “the significant increased abuse of the de minimis exemption, in particular China-founded e-commerce platforms.” The announcement said the Biden Administration would issue a Notice of Proposed Rulemaking that would exclude from the de minimis exemption all shipments containing products covered by tariffs imposed under Sections 201 or 301 of the Trade Act of 1974, or Section 232 of the Trade Expansion Act of 1962. The announcement also called for Congress to pass new legislation to reform the de minimis rule comprehensively.

FASH455 Learning activity: After watching the two video above, please explore the following topics with the assistance of ChatGPT or other generative AI tools:

The significance and complexity of container shipping for U.S. fashion brands and retailers

Current issues related to container shipping for U.S. fashion brands and retailers

In your response, please include the following elements:

Questions: list at least three questions you asked ChatGPT or other AI tools that helped generate the most information and insights.

Summary and reflections: summarize the key points from the answers you received from the AI tool and share your reflections (e.g., were there any surprising insights? the outlook for the issues discussed)

Further Reading: Suggest 1-2 additional articles from national or international press that offer deeper insights into the topics. The readings need to be published after 2024. Please share the article link and briefly explain why you recommend them.

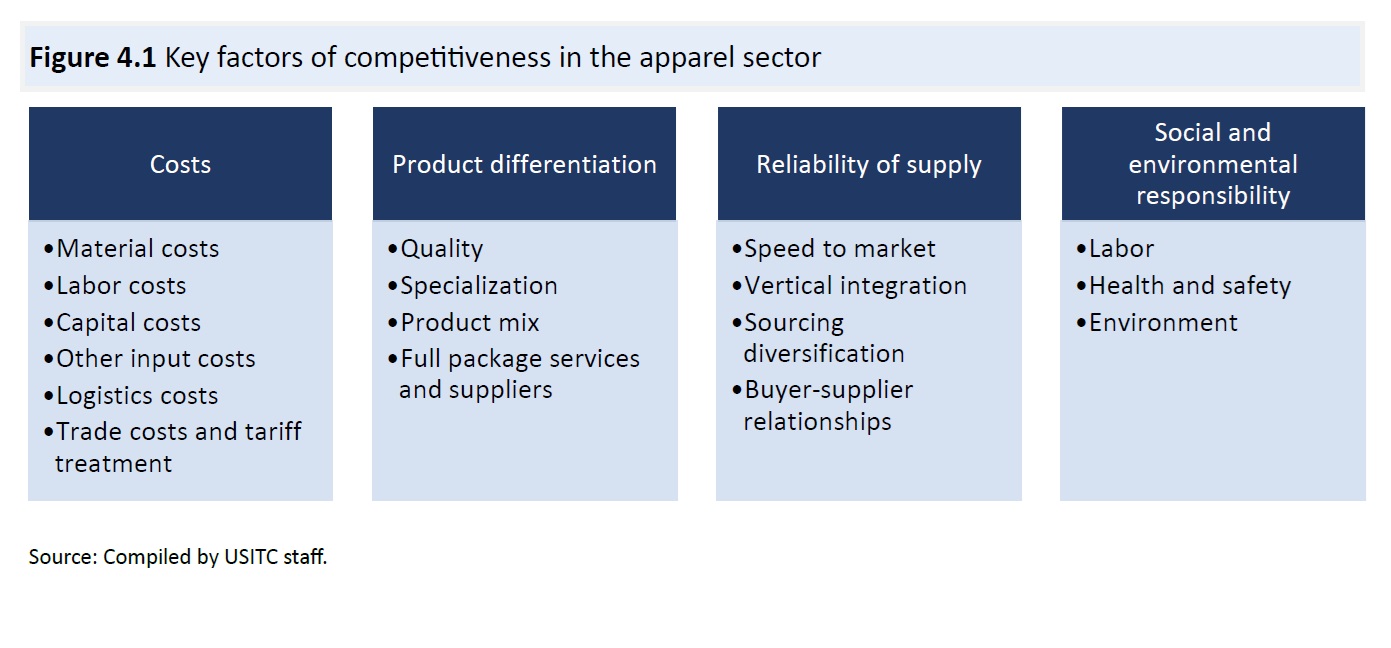

The United States International Trade Commission (USITC) released its new fact-finding report examining the competitiveness of Bangladesh, Cambodia, India, Indonesia, and Pakistan as apparel suppliers to the United States. The study was conducted in 2024 based on input from secondary sources (e.g., trade statistics, public hearings, and desk studies) and fieldwork. Below are summaries of the key findings regarding apparel export competitiveness.

Factors that affect export competitiveness in the global apparel sector

One key issue the study explored is what factors affect a country’s apparel export competitiveness and how to become a preferred apparel sourcing base for U.S. fashion companies.

The studies suggest that four types of factors are most important (see the figure above). However, consistent with existing literature, the USITC report could not determine which factor is decisive in fashion companies’ apparel sourcing decisions. For example, the report found that:

“cost—the price buyers pay their suppliers—plays a key role in sourcing decisions, although opinions vary regarding the importance of cost relative to other factors.”

“Depending on the product, target consumer, and identity of a brand or buyer, apparel buyers will place varying degrees of importance on product differentiation factors such as quality, specialization, product mix, and full package offerings, which include design services, finishing, packaging, and logistics.”

“The emphasis on reliability has particularly grown in response to various recent disruptions to global apparel supply chains such as a global pandemic, geopolitical conflicts, and trade policy.”

“Although emerging research suggests that compliance programs concerning wages, social inclusion, and climate change mitigation may increase competitiveness, buyers and brands remain divided on the topic…the relative importance, or “weight,” of such compliance in sourcing decisions remains a topic of active study and discussion within the industry.”

Cost and export competitiveness

The USITC report highlighted the complex and nuanced relationship between “costs” and a country’s apparel export competitiveness. Several patterns are noteworthy:

Apparel is a buyer-driven industry, meaning “the global apparel supply chain gives buyers the power to negotiate based on price, which can push down prices and transfer greater costs to the supplier.”

The ability to produce textile raw materials locally can provide cost advantages in garment production—“Material inputs are widely recognized as the largest component in the cost of a final apparel product, and these prices are largely determined by the presence of a domestic textile industry or costs of importing textiles.”

It is difficult to compare wages across countries to measure labor competitiveness. In particular, low labor costs “do not reflect the true cost of doing business (e.g., via wage suppression)” in a country and “they can harm a country’s reputation for social compliance and negatively affect labor productivity.”

Buyer-supplier relationships in apparel sourcing

The USITC report revealed some positive developments in the buyer-supplier relationships involving U.S. fashion companies.

Fashion companies increasingly recognize the value of building long-term relationships with their vendors. Buyers emphasize that maintaining these relationships is a key factor in sourcing decisions, largely due to the cost and time involved in finding and establishing relationships with new suppliers.

Fashion companies’ efforts to improve supply chain transparency and traceability also need “suppliers who will act in line with their brand’s values.”

Suppliers benefit from the long-term relationship, too. As the USITC report noted, some fashion companies guarantee suppliers a particular profit margin to ensure their continued operation. Additionally, some buyers gain a deep understanding of their suppliers’ cost structures, enabling them to calculate the costs of compliance with various standards and assist suppliers in reducing costs where possible.

Subcontracting is still regarded as necessary for the garment industry. As noted in the USITC report, apparel orders fluctuate seasonally, making it impractical for suppliers to hire additional permanent workers or invest in machinery for peak demand. To meet buyer expectations during busy periods, manufacturers often subcontract parts of orders and increase overtime or rely on temporary contract workers. This practice is seen as essential for ensuring a reliable supply of apparel.

Social and environmental responsibility and apparel sourcing

The USITC report acknowledged the growing importance of social and environmental compliance to a country’s apparel export competitiveness. However, the relationship remains complex.

The extent to which voluntary social and environmental responsibility programs and their associated auditing practices have influenced outcomes, especially regarding worker rights, remains unclear.

Suppliers report that the increased frequency of flooding and high temperatures due to climate change negatively affect their ability to meet labor and environmental standards.

Increased compliance with social and environmental standards raises supplier costs, negatively impacting their cost competitiveness. Many stakeholders note that while brands and consumers demand greater responsibility, this often does not come with a “price premium” for suppliers, who ultimately absorb these increased costs.

Note: The USITC report also evaluated the export competitiveness of each apparel-exporting country it examined, including their respective competitive advantages and issues to address.

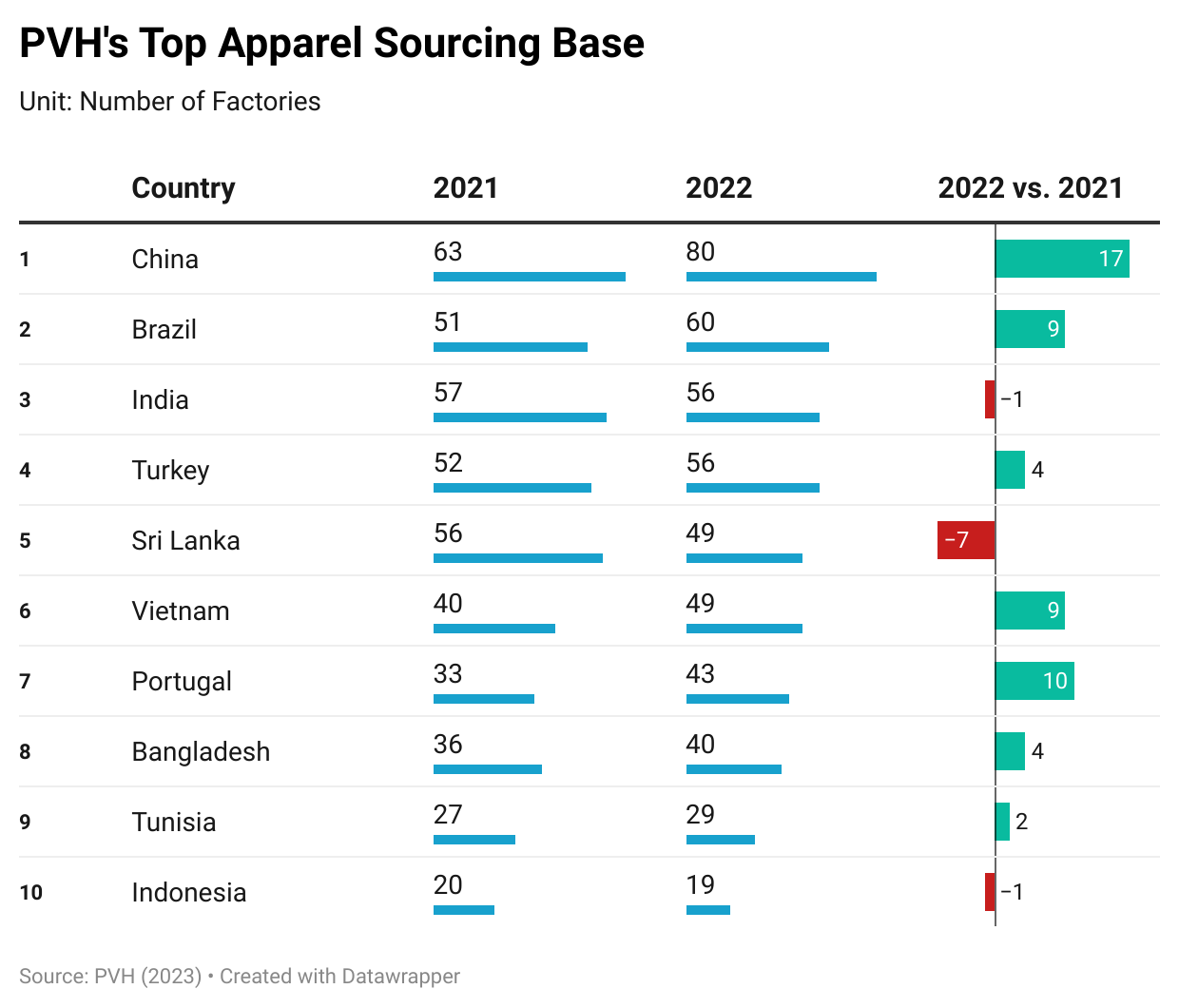

PVH Corporation (PVH), which owns well-known brands including Calvin Klein, Tommy Hilfiger, Van Heusen, Arrow, and Izod, is one of the largest US fashion companies with nearly $9.2 billion in sales revenues in 2022.

By leveraging PVH’s publically released factory lists, this article analyzes the company’s detailed sourcing strategies and changes from 2021 to 2022. Key findings:

Trend 1: PVH adopts a diverse apparel sourcing base and continues to work with more vendors. Specifically, in 2022, PVH sourced apparel from as many as 37 countries in Asia, Europe, America, the Middle East, and Africa, the same as in 2021. Despite not expanding the number of countries it sources from, PVH increased its total number of vendors from 503 in 2021 to 553 in 2022, highlighting the company’s ongoing commitment to diversifying its sourcing base.

Trend 2: Asia is PVH’s dominant sourcing base for finished garments and textile raw materials.

Specifically, about 56.2% of PVH’s apparel suppliers were Asia-based in 2022, followed by the EU (20.3%). Compared with a year ago, PVH even added twenty new Asia-based factories to its supplier list in 2022, suggesting no intention of reducing sourcing from the region. Moreover, From 2021 to 2022, as many as 83% of PVH’s raw material suppliers were Asia-based, far exceeding any other regions.

Trend 3: PVH’s China sourcing strategies are evolving and more complicated than simply “reducing China exposure.”

First, PVH continued to work with MORE Chinese factories. Specifically, between 2021 and 2022, PVH added 17 Chinese factories to its apparel supplier list, more than other countries. However, the expansion could be because of PVH’s growing sales in China.

Second, PVH’s garment factories in China are smaller than their peers in other Asian countries. For example, in 2022, most PVH’s contracted garment factories in top Asian supplying countries, such as Bangladesh (87.5%), Vietnam (63.3%), and Sri Lanka (65.3%), had more than 1,000 workers. In comparison, only 11.3% of PVH’s Chinese vendors had 1,000 workers, and more than 62.5% had fewer than 500 workers. The result suggests that PVH treats China as an apparel sourcing base for flexibility and agility, particularly those orders that may include a greater variety of products in relatively smaller quantities.

Further, PVH often priced apparel “Made in China” higher than those sourced from the rest of Asia.

Trend 4: PVH actively used “emerging” sourcing destinations outside Asia. Other than those top Asian suppliers, PVH’s apparel sourcing base includes several countries in America, the EU, and Africa that deserve more attention, including Portugal, Brazil, Tunisia, and Turkey. Overall, PVH sourced from these countries for various reasons, from serving local consumers, seeking sourcing flexibility, accessing raw materials, and lowering sourcing costs.

Part I: Watch the following two videos on tariffs—one from an economic perspective and the other from a political perspective.

Part II: Check the respective tariff rate for the following products by copying and pasting the HS code into the search box

Product 1 (men’s and boys’ overcoat, cotton): HS code 6101.20.00

Product 2 (cotton): HS code 5201.00.05

Product 3 (smartphone): HS code 8517.13.00

Discussion question: Based on the videos and your findings, how would you explain the differences in tariff rates for these products? Do you think tariffs are still necessary in the 21st century?

Note: The revealed comparative advantage (RCA) index measures a country’s relative export performance of a particular product compared to the world average. It helps identify sectors in which a country holds a competitive edge in international trade. RCA =(Country’s exports of product X/Country’s total exports)/(World exports of product X/World total exports).

RCA > 1: A value greater than 1 indicates that the country has a revealed comparative advantage in the product, meaning the product has a higher export share in the country’s portfolio compared to the global average. This suggests the country is more competitive in exporting that product relative to the rest of the world.

RCA < 1: A value less than 1 means the country has a revealed comparative disadvantage in that product. It indicates that the country is less competitive in exporting that product compared to the global average.

Observe the sectors in which the U.S. enjoyed a revealed comparative advantage (i.e., RCA > 1) in 2023. How does this compare with Bangladesh? What is your explanation for the observed differences?

Firstly, while China remained the world’s largest clothing exporter in 2023, rising geopolitical tensions and Western fashion companies’ ongoing de-risking efforts pose increasing challenges to its export outlook.

To some extent, 2023 wasn’t too bad for clothing “Made in China.” In value, China’s clothing exports totaled $164 billion, accounting for 31.6% of the world—unchanged from 2022. While China’s clothing exports decreased by 9.7 percent in 2023 compared to the previous year due to weaker market demand, this performance was better than most other top ten suppliers, including Bangladesh (down 16 percent), Vietnam (down 12 percent), India (down 13 percent), and Indonesia (down 17 percent).

However, China’s clothing exporters face significant challenges ahead. Despite maintaining its overall market share, China is losing momentum in nearly all key Western clothing markets, including the United States, the European Union, the UK, and Canada. This trend is primarily driven by perceived heightened sourcing risks associated with China, ranging from concerns over forced labor in the Xinjiang region to escalating geopolitical tensions involving the country.

For example, according to the 2024 Fashion Industry Benchmarking Study released by the US Fashion Industry Association (USFIA) in July, a record 43 percent of surveyed leading US fashion companies reported sourcing less than 10 percent of their apparel products from China in 2024, compared to only 18 percent in 2018. Likewise, nearly 60 percent of respondents no longer use China as their top apparel supplier in 2024, much higher than the 25-30 percent range before the pandemic. Additionally, nearly 80 percent of respondents plan to further reduce their apparel sourcing from China over the next two years through 2026, citing perceived high sourcing risks as the primary concern.

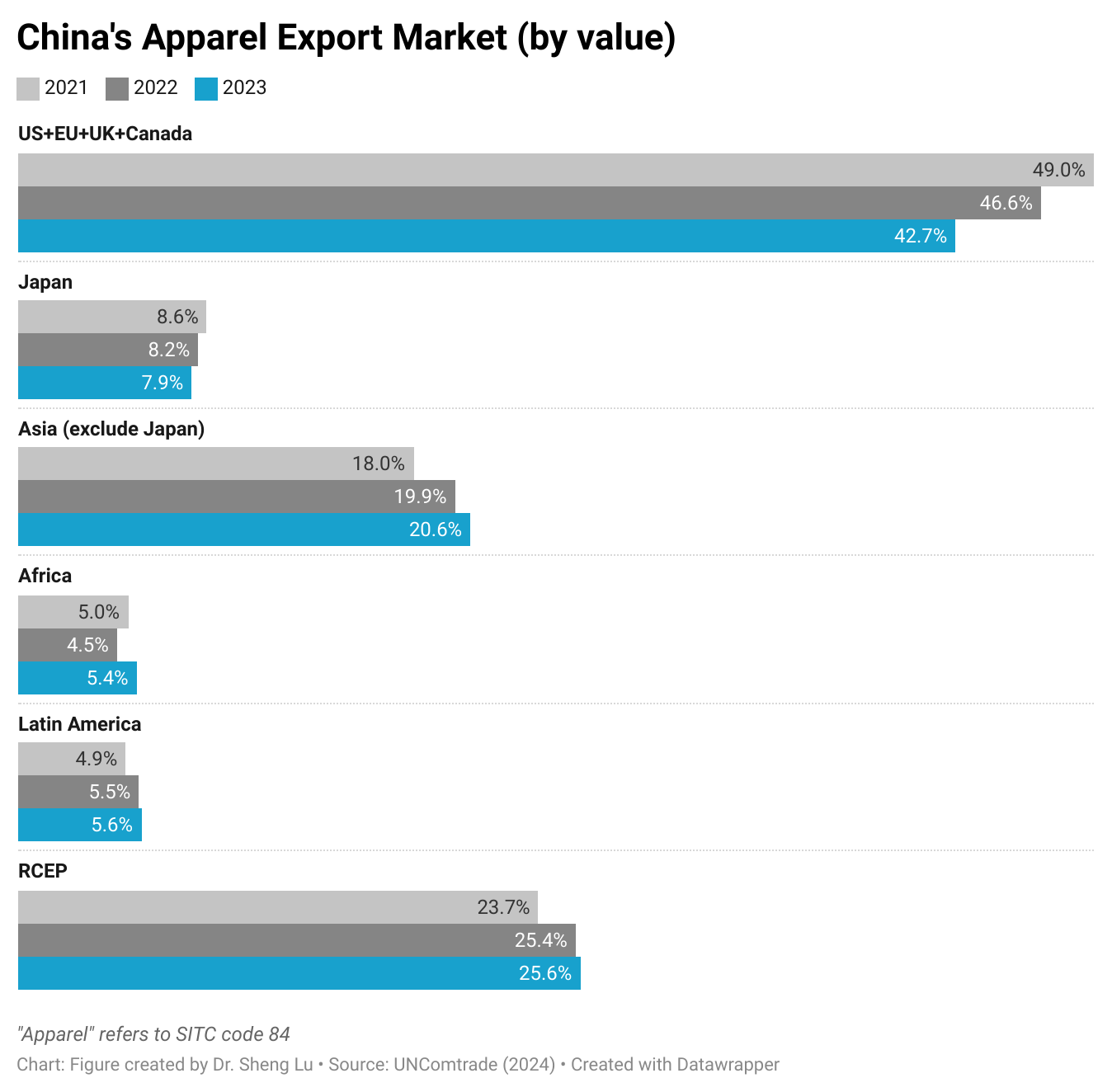

Secondly, China has been diversifying its clothing exports beyond traditional Western markets in response to the “de-risking” movement. For example, the US, EU, UK, and Canada combined accounted for 43-45 percent of China’s clothing exports in 2023, lower than over 50 percent in the past. In comparison, these four Western markets typically accounted for 70 to 90 percent of an Asian country’s clothing exports. Meanwhile, since 2021, Asian economies, especially members of the Regional Comprehensive Economic Partnership (RCEP) and Africa, have become more important export markets for China. Nevertheless, since RCEP members and those in Africa primarily consist of developing economies with ambitions to expand their own clothing production and exports, the long-term growth prospects for their demand for “Made in China” clothing remain uncertain.

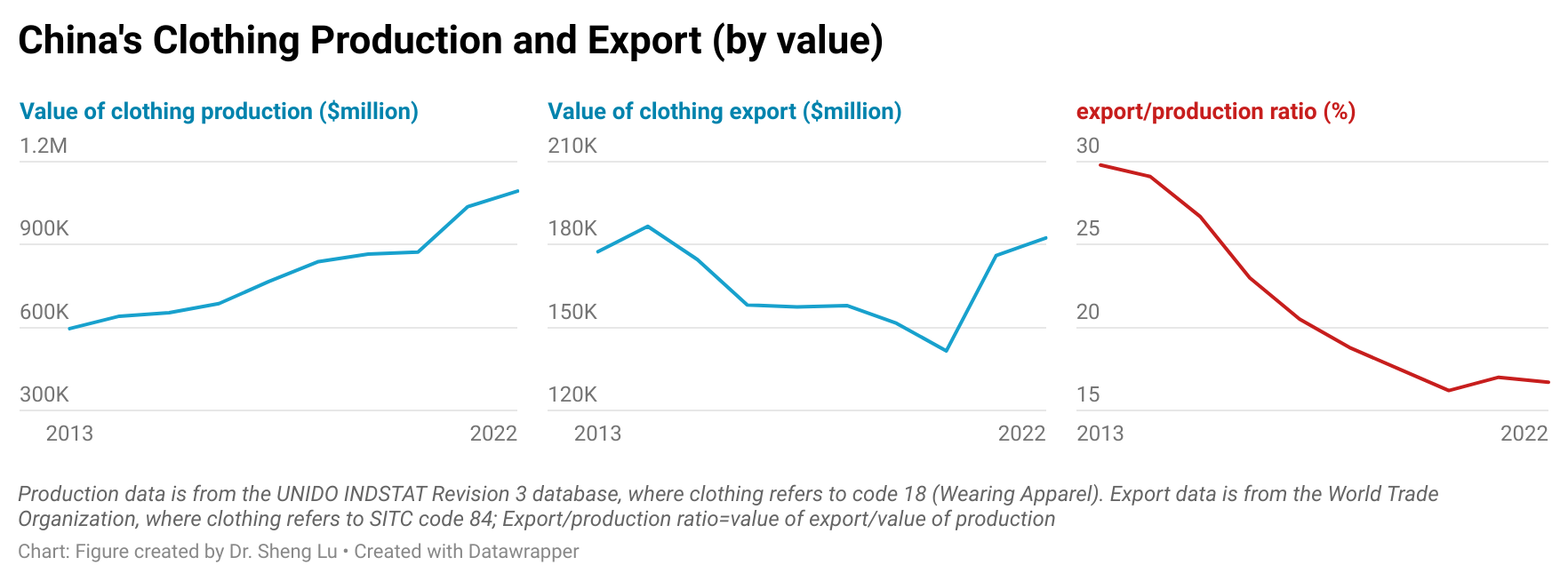

Thirdly, China’s weakened economy could lead to an increased supply of low-cost Chinese clothing in the global market.

Despite being known as the world’s largest clothing exporter, between 2013 and 2022 (the latest available data), over 70%–80% of clothing produced in China was consumed domestically,with only about 20%–30% being exported. However, as China’s economic growth has slowed and consumer spending on clothing has stalled, more clothing made in China could enter the international market and intensify the price competition. Notably, between June 2023 and June 2024, the average unit price of US apparel imports from China decreased unusually by 7.6 percent, signaling that an increased supply of Chinese clothing began to suppress market prices. Likewise, it doesn’t seem reasonable that the unit price of U.S. apparel imports from China was 40% lower than that of imports from Bangladesh in the first half of 2024. Thus, the growing influx of cheap Chinese products raises the risk of market disruptions, potentially leading to additional trade tensions and restrictive measures against Chinese products.

Fourthly, there is an early sign that Asian countries have become more cautious about using Chinese yarns and fabrics. China remained a key supplier of textile raw materials to leading apparel-exporting countries in Asia. However, Asian countries appeared to be sourcing fewer yarns and fabrics from China in 2023, possibly due to the enforcement of anti-forced labor laws, such as the Uyghur Forced Labor Prevention Act (UFLPA), and the perceived risks associated with sourcing Chinese cotton. Instead, more Asian countries’ yarns and fabrics now came from regional suppliers other than China.

Speaker: Dr. Deborah Elms, Founder and Executive Director of the Asian Trade Centre and the President of the Asia Business Trade Association. The clip was part of the webinar “Asia’s Noodle Bowl Of Trade” (March 2023).

Background

The Asia-Pacific region includes several mega free trade agreements:

ASEAN (Association of Southeast Asian Nations) is a regional intergovernmental organization comprising ten countries in Southeast Asia (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam). In 2022, ASEAN members have a combined nominal GDP of $3.6 trillion and a population of 671.6 million.

CPTPP (Comprehensive and Progressive Agreement for Trans-Pacific Partnership) is a free trade agreement signed by 11 countries in the Asia-Pacific region, including Japan, Malaysia, Vietnam, Australia, Singapore, Brunei, New Zealand, Canada, Mexico, Peru, and Chile. The CPTPP covers a market of 495 million people with a combined GDP of $13.5 trillion in 2021. The United States was originally a participant in the Trans-Pacific Partnership (TPP) negotiations, but in January 2017, former US President Trump withdrew the US from the agreement. The Biden administration has indicated no interest in rejoining CPTPP. Additionally, China is actively seeking to join CPTPP (as of March 2024).

RCEP (Regional Comprehensive Economic Partnership) is a free trade agreement signed by 15 countries in the Asia-Pacific region, including China, Japan, South Korea, Australia, New Zealand, Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, Vietnam. In 2021, RCEP members collectively represented a market of 2.3 billion people with a combined GDP of $26.3 trillion. India was an RCEP member but withdrew from the agreement due to concerns about import competition with China.

IPEF (Indo-Pacific Economic Framework for Prosperity) is a US-led economic cooperation framework that aims to “link major economies and emerging ones to tackle 21st-century challenges and promote fair and resilient trade for years to come.” IPEF is NOT a traditional free trade agreement, and it does not address market access issues like tariff cuts. Instead, IPEF includes four pillars: trade, supply chains, clean economy, and fair economy. IPEF members in the Asia-Pacific region include the United States, Japan, Australia, New Zealand, South Korea, India, Fiji, Brunei, Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam. The IPEF is designed to be flexible, meaning that IPEF partners are not required to join all four pillars. For example, India chooses not to join the trade pillar of the framework. In 2021, IPEF countries collectively represented a market of 2.1 billion people with a combined GDP of $23.3 trillion. The potential economic impact of IPEF remains too early to tell.

Notably, ASEAN, CPTPP, RCEP, and IPEF members play significant roles in the world textile and apparel trade. Specifically:

ASEAN and RCEP members have established a highly integrated regional textile and apparel supply chain. For example, a substantial portion of ASEAN and RECP members’ textile imports came from within the region.

ASEAN and RCEP members’ supply chain connection with China has substantially strengthened over the past decade. In contrast, the US barely participated in Asia-based textile and apparel supply chains. For example, other than CPTPP, the US accounted for less than 2% of ASEAN, RCEP, and IPEF members’ textile imports in 2022.

ASEAN and RCEP members also hold significant market shares in the world textile and apparel exports (over 50%). Meanwhile, the US and EU are indispensable export markets for ASEAN and RCEP members.

Because of the inclusion of the United States, IPEF represented one of the world’s largest apparel import markets (i.e., 33.7% in 2021, measured in value). Similarly, in 2022, about 26% of US apparel imports came from current IPEF members. Should IPEF address market access issues, it could offer significant duty-saving opportunities for textile and apparel products.

Additionally, the UK’s membership in CPTPP may have a limited direct impact on the textile and apparel sector, at least in the short to medium terms. For example, current CPTPP members only accounted for about 6% of the UK’s apparel imports in 2022.

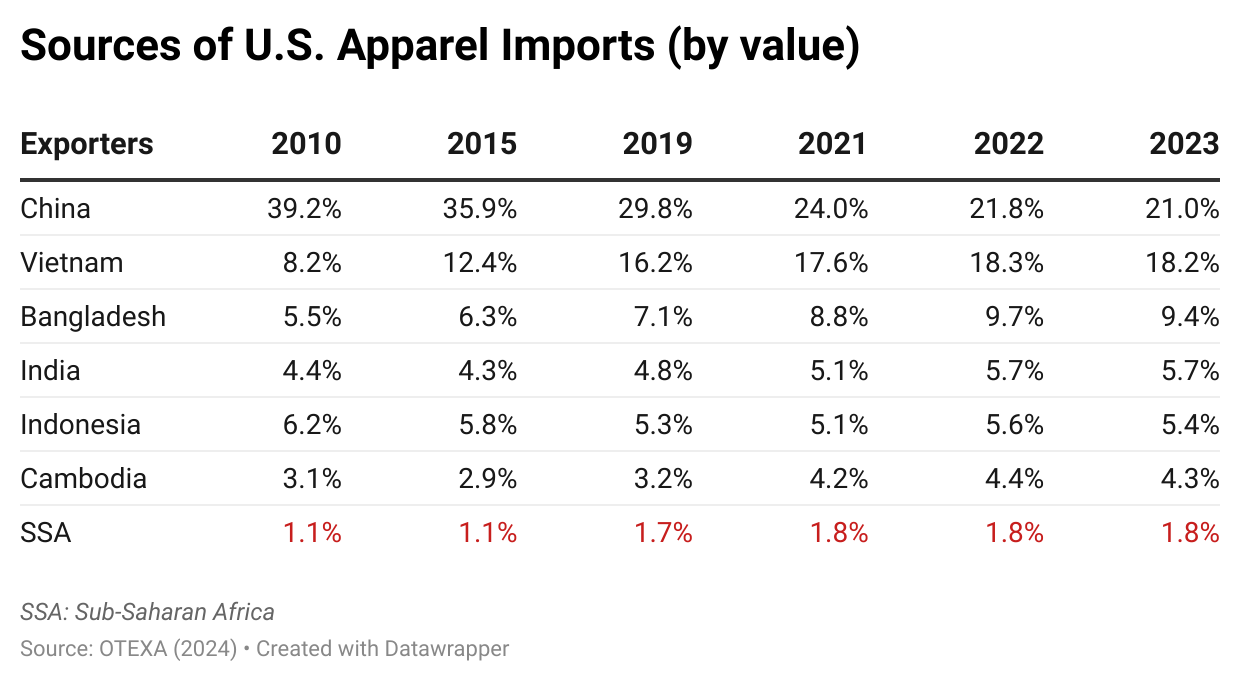

The prospect of Sub-Saharan Africa (SSA) as an apparel-sourcing base for U.S. fashion companies has been a growing heated debate. On the one hand, U.S. fashion companies, driven by increasing geopolitical concerns and other market factors, were eager to diversify apparel sourcing away from Asia. The SSA region was often regarded as one of the most popular alternative sourcing destinations thanks to its large population, relatively low labor costs, and shorter shipping distance to U.S. ports compared to most Asian. The African Growth and Opportunity Act (AGOA), a trade preference program enacted in 2000, in particular, allowed eligible apparel exports from SSA countries to enter the United States import duty-free, creating substantial financial incentives for U.S. fashion companies to source from the SSA region.

However, empirical trade data shows that U.S. apparel imports from SSA members have stagnated over the past decades without evident growth. Notably, with little change from 2010, SSA countries collectively accounted for only 1.8% of U.S. apparel imports in 2023, with no single SSA member achieving a market share of more than 1%. In contrast, over the same period, despite China’s declining market shares, the following five largest Asian suppliers—Vietnam, Bangladesh, India, Indonesia, and Cambodia—jointly accounted for 43.0% of U.S. apparel imports in 2023, a notable increase from 27.4% in 2010.

This study aims to evaluate SSA countries’ capacity to serve as an alternative apparel sourcing destination to Asian suppliers for US fashion companies. Specifically, the study examined the detailed product information of a total of 10,000 stock keeping units (SKUs) of clothing items sold in the U.S. retail market from January 2021 to December 2023. Half of these items were sourced from the six largest apparel-exporting countries in SSA: Lesotho, Kenya, Mauritius, Ethiopia, Madagascar, and Tanzania. Together, these countries accounted for over 96% of the value of U.S. apparel imports from the SSA region between 2021 and 2023. The remaining half came from China, Vietnam, Bangladesh, Cambodia, India, and Indonesia, the six largest Asian apparel exporters, which stably accounted for approximately 90% of U.S. apparel imports from Asia over the past decade.

Key findings:

First, the results revealed that U.S. fashion companies’ sourcing strategies for SSA countries appeared more subtle and complicated than simply treating the region as another low-cost sourcing destination, as suggested by previous studies. Instead, according to the results, U.S. fashion companies seemed to leverage SSA countries as suppliers of “niche products,” such as those relatively simple and basic apparel categories containing African cultural elements and targeting the luxury and premium market segment. Meanwhile, the demand for such products could be much smaller than regular apparel items sold in the value and mass market. This allows SSA countries to fulfill these smaller orders despite their limited production capacity, often family-owned or involving handmade processes.

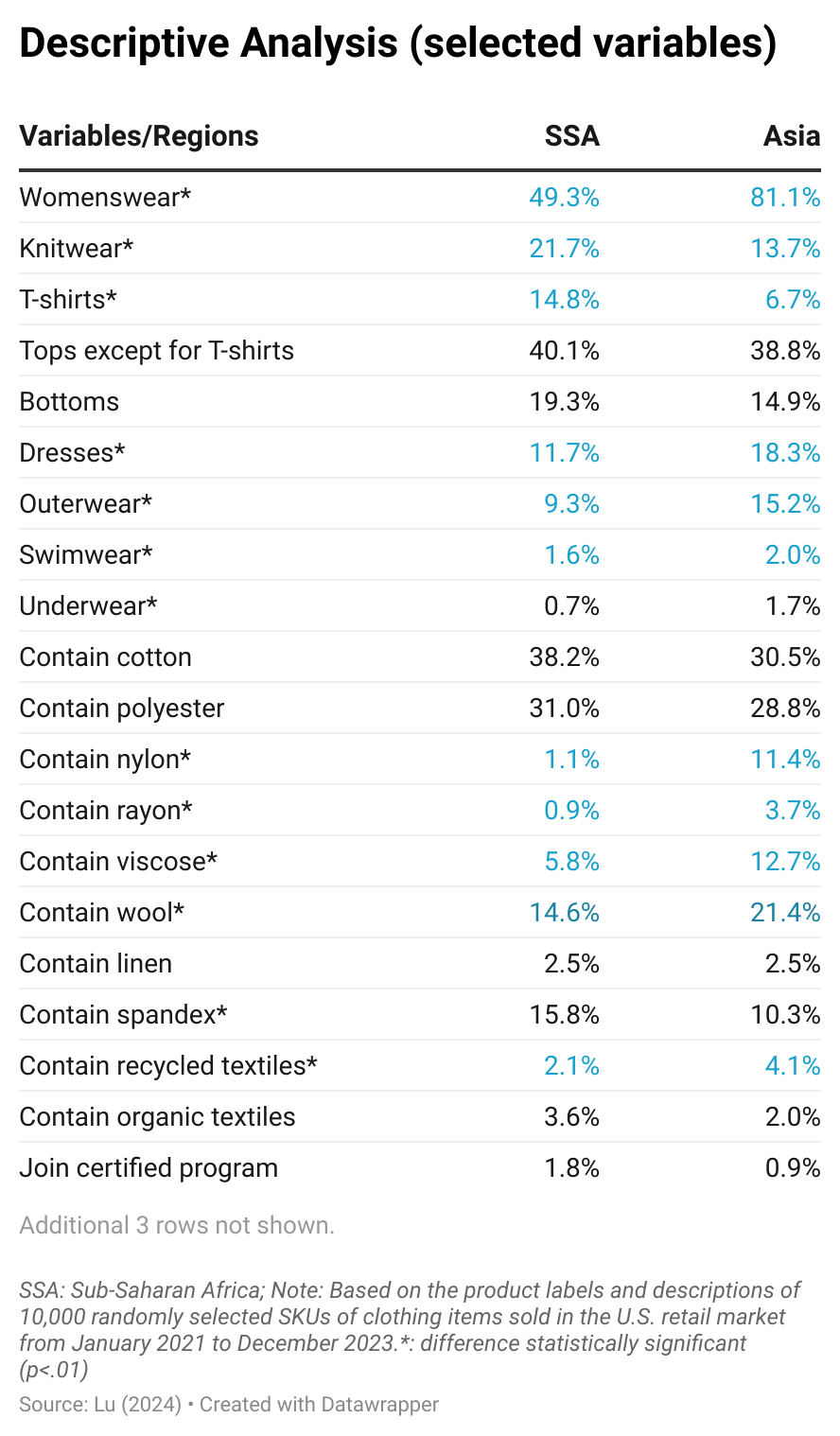

Second, the study’s findings identified significant challenges for SSA countries serving as immediate alternatives to sourcing from Asia for U.S. fashion companies. While SSA countries could offer relatively low sourcing costs, the range of apparel products available for U.S. fashion companies to source from the SSA region remained significantly more limited than those from Asia. For example, results show that U.S. fashion companies preferred sourcing relatively basic and technologically simple categories like knitwear, T-shirts, and bottoms from SSA countries. However, imports from SSA countries offered more limited sizing and color choices and were less likely to include womenswear and relatively more sophisticated or specialized product categories such as outerwear and swimwear. As another example, U.S. apparel imports from SSA countries were primarily made of cotton and polyester, with less use of other fiber types, including nylon, rayon, viscose, wool, and those made from recycled textile materials (see table below).

Third, building on the previous point, the results call for new thinking on strengthening SSA countries’ genuine competitiveness as an apparel-sourcing destination. Over the past decades, trade preference programs such as AGOA have mainly focused on improving the price competitivenessof SSA countries’ apparel exports. However, as this study’s findings illustrate, AGOA and other trade preference programs seemed inadequate in assisting SSA countries in developing capacity beyond basic apparel categories and securing a sufficient variety of textile materials. As U.S. fashion companies have placed greater emphasis on factors beyond price in their sourcing decisions, such as flexibility, agility, sustainability, and vendors’ capability to make a wide variety of products, this could put SSA countries at even more significant disadvantages down the road to being considered alternatives to Asia for apparel sourcing.

The results also reminded us that AGOA’s liberal rules of origin, which allowed least-developed SSA countries to use textile materials from anywhere worldwide, cannot replace the crucial need to develop the local textile manufacturing capacity within the SSA region. Without a robust local textile manufacturing sector, SSA countries would encounter significant challenges in diversifying their product offerings to include more complex and versatile clothing categories, such as outerwear and women’s dresses. These categories typically require a wide variety of raw textile materials and accessories, making it highly impractical and inefficient to rely solely on imports for their supply.

On the other hand, the findings reveal the necessity of creating a stable and foreseeable business environment, such as the long-term renewal of AGOA, to attract more long-term investments in SSA. For example, investing in and strengthening SSA countries’ local supply of sustainable textile materials, such as recycled or organic fibers, could strategically enhance SSA countries’ competitiveness in meeting the increasing demand from U.S. fashion companies for sustainable apparel products.

The full article is available HERE and below is the summary:

With consumers’ growing demand for sustainable apparel products, fashion companies increasingly carry clothing made from recycled textile materials and seek additional supply bases. Recycled cotton has great potential for use in garments because of the wide availability of cotton-made secondhand clothing and the perceived positive environmental impacts of effectively recycling post-consumption cotton waste.

This study explores Egypt, Morocco, and Tunisia’s potential as sourcing bases for clothing made from recycled cotton. North African countries, including Egypt, Morocco, and Tunisia, have a long history of making and exporting cotton and cotton-made finished garments. The “developing country” status and membership in trade agreements or trade preference programs, such as the African Growth and Opportunity Act (AGOA) and the EU-Mediterranean Association Agreement, allow apparel products from these three countries to enjoy preferential duty benefits in the world’s top import markets. Therefore, there is great potential to capitalize on recycled cotton apparel and “green exports” to further promote economic development in the region.

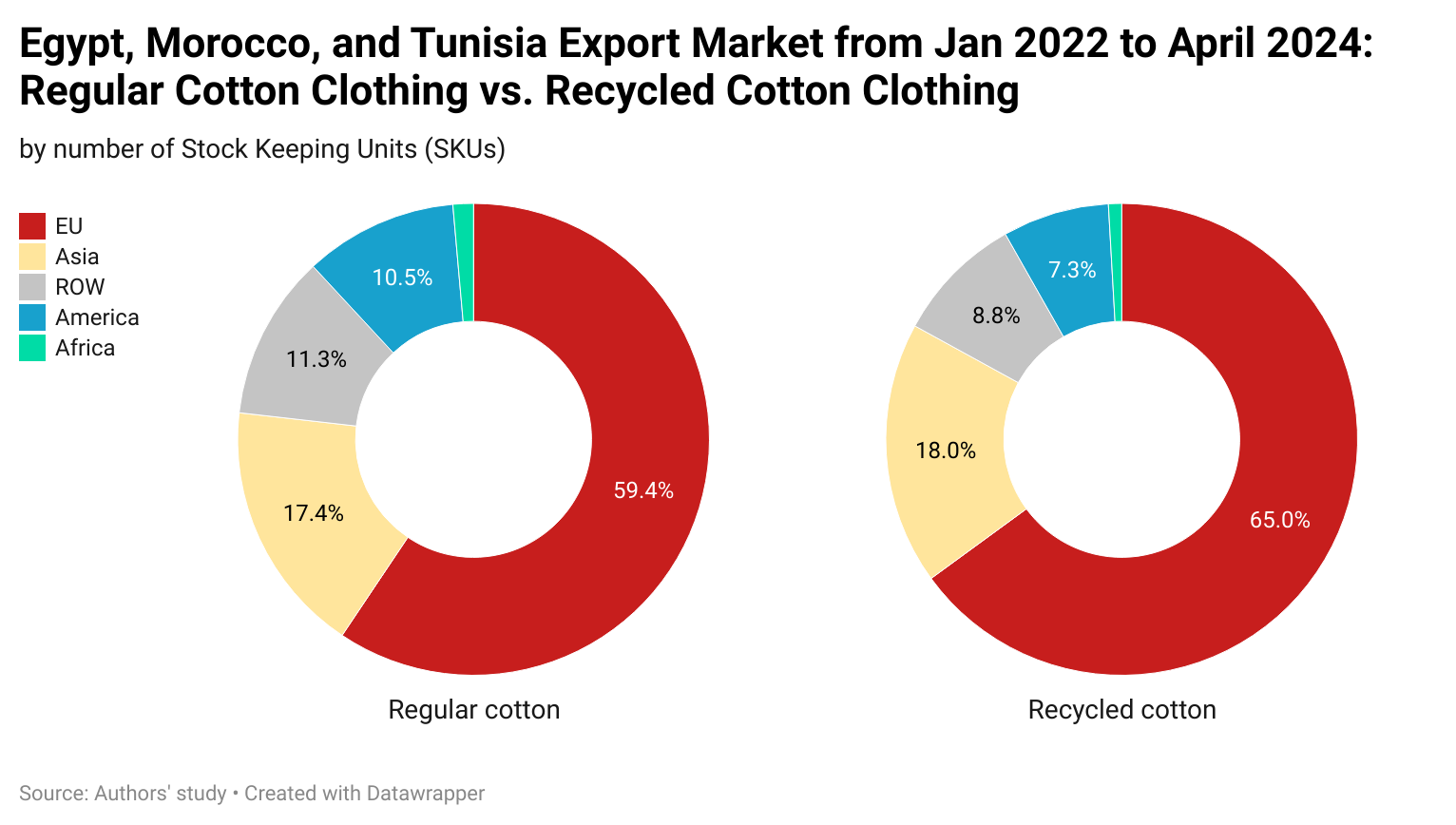

About 13,000 Stock Keeping Units (SKUs) of clothing items made by these three countries newly launched to the world retail market between January 2022 and April 2024 were randomly captured from fashion brands and retailers’ websites. About half of the items were made of regular cotton, and the other half explicitly mentioned using “recycled cotton” in the product label or description. The results show that:

#1: Egypt, Morocco, and Tunisia have gradually expanded their clothing exports made from recycled cotton since 2022. For example, as estimated, about 1,300 SKUs of clothing using recycled cotton from these three countries were newly launched to the US and EU retail markets in 2023, a substantial increase from only 150 SKUs back in 2022 (or a sevenfold increase). Similarly, in the first four months of 2024, clothing using recycled cotton accounted for 10.2% of total cotton apparel from the three countries in the US and EU markets, a substantial increase from only 1.1% in 2022.

#2: Of the collected samples, apparel using recycled cotton from Egypt, Morocco, and Tunisia was destined for as many as 49 countries, reflecting the global demandfor such products. However, possibly restrained by the limited supply, the export market for clothing using recycled cotton remained less diverse than that for clothing made of regular cotton, which spanned 72 countries.

#3: Geographically, the European Union (EU) was the top clothing export market for Egypt, Morocco, and Tunisia, accounting for over 75% of these countries’ export value in 2022, according to UN trade statistics (UNComtrade). This was also the case for recycled cotton products. Specifically, the EU accounted for 65% of these three countries’ total recycled cotton clothing exports measured in SKUs in the collected samples, higher than 59.4% of regular cotton clothing products.

#4: Egypt, Morocco, and Tunisia focused on different product categories for clothing using recycled cotton than those made from regular cotton. Specifically, of the sampled items, clothing using recycled cotton had a notable concentration on bottoms (52.9%), followed by tops other than T-shirts (23.8%). Recycled cotton clothing also was more commonly used for outerwear (7.5%) than those using regular cotton (3.8%). In comparison, only about 7.9% of clothing using recycled cotton were T-shirts, much fewer than nearly 30% of those using regular cotton. Similarly, specific product categories, such as underwear and hosiery, rarely use recycled cotton. Likely, the concerns for quality and durability and the difficulty of absorbing higher production costs make using recycled cotton for these relatively simple categories more challenging.

#5: Even though cotton apparel made in Egypt, Morocco, and Tunisiaalready commonly mentioned their sustainability attributes (86%), phrases such as “sustainability” and “sustainable” appeared even more frequently in clothing using recycled cotton (94.6%). For example, some producers highlighted that they “worked with suppliers, workers, unions and international organizations” to ensure their recycled cotton clothing contributed to “the United Nations Sustainable Development Goals.” Likewise, some labels intentionally remind consumers about the positive environmental impact of using recycled cotton, “The use of recycled cotton helps to limit the consumption of raw materials.” Another added, “The production of recycled cotton recovered cotton, mainly from the production of other garments, thus reducing the production of virgin spring and water consumption, energy and natural resources.”

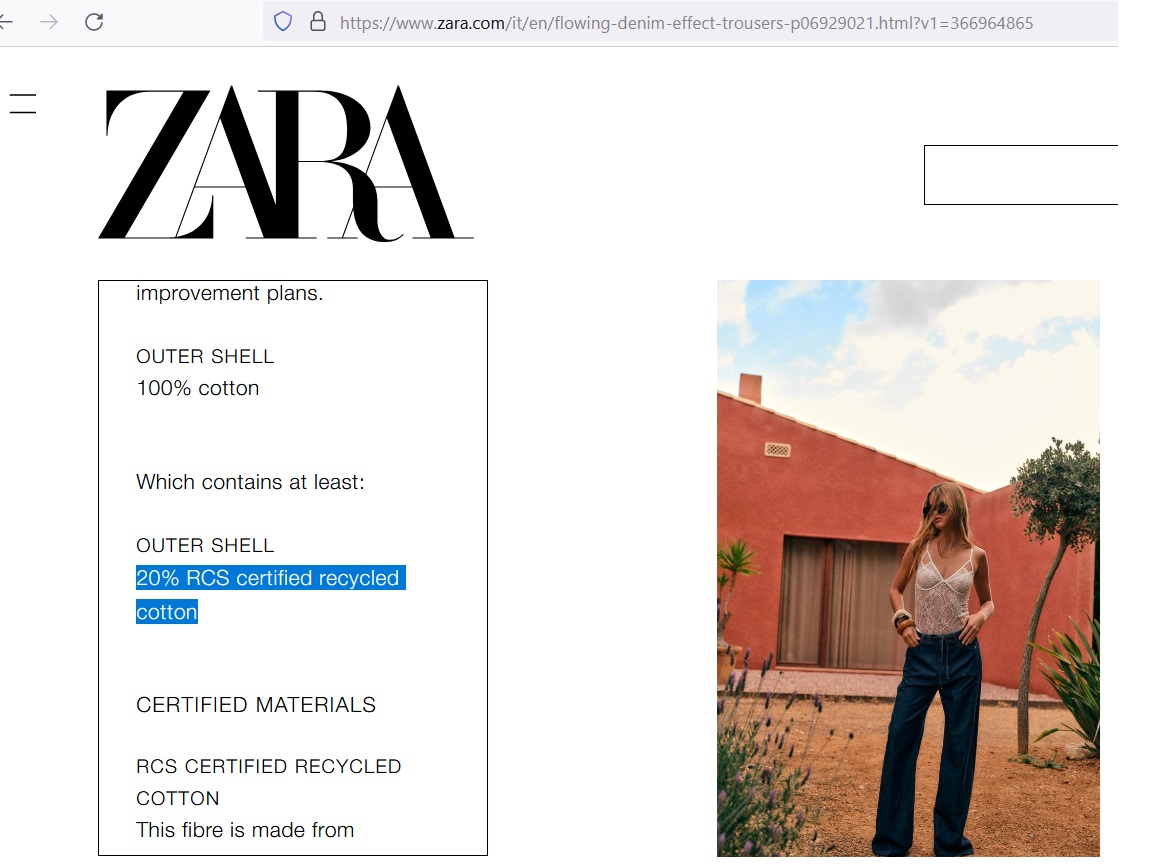

Meanwhile, compared to clothing using regular cotton, those made with recycled cotton in Egypt, Morocco, and Tunisia reported much higher participation incertification programs, such as the Recycled Claim Standard (RCS), which verifies the recycled content and tracks it from source to final product.

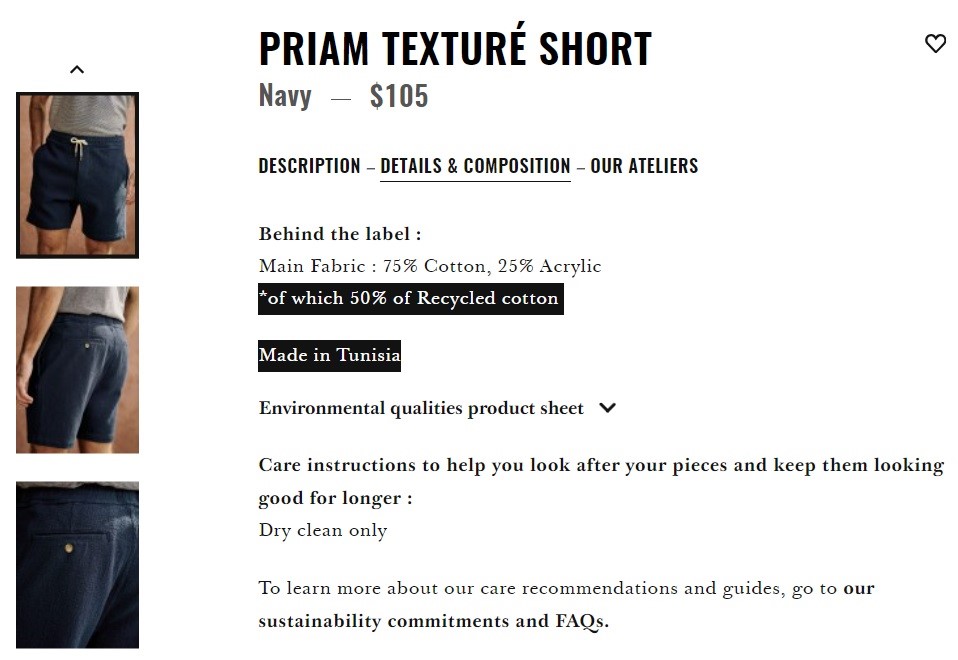

#6: Reflecting the technical limitations of the fiber property, it remains rare to have clothing that is 100% made from recycled cotton. According to industry experts, longer cotton fibers generally indicate higher quality. Since the recycling process shortens cotton fibers, regular virgin cotton or other fibers like polyester are typically used alongside recycled cotton to make fabrics smoother, stronger, and more durable. For example, common labels include descriptions such as “80% virgin cotton, 20% RCS certified recycled cotton” and “55% RCS certified recycled polyester, 45% RCS certified recycled cotton.”

#7: Except for T-shirts, in most cases, clothing made from recycled cotton in Egypt, Morocco, and Tunisia was priced lower than their equivalent using virgin fiber in the market. This is particularly the case for the premium and luxury market segments, where clothing using recycled fiber typically was 20-30% lower priced than regular clothing. The results echo the findings of numerous studies indicating that consumers are generally unwilling to pay higher prices for recycled fiber clothing as they perceive such products as lower quality and less “valuable.” Also, more needs to be done to create more financial incentives for producers in Egypt, Morocco, and Tunisia to expand the production scale and increase the use of recycled cotton in their products.

The new punitive tariffs on Chinese steel and aluminum: The overcapacity problem in the steel industry globally could raise national security concerns. While the Biden Administration is more focused on outreach to allies and partners to address the issue collectively, the Trump Administration took a different approach with the Section 232 tariffs specifically targeting China. However, the impact of China-targeted measures could be muted due to the limited amount of US steel imported from China today. The next administration is expected to face the challenge of addressing global overcapacity in various industries. Like it or not, tariffs seem to be one of the few tools available to the US government to tackle these issues directly.

Currency debate: “Currency manipulation” refers to the deliberate actions taken by a country’s government or central bank to artificially influence the value of its currency in the foreign exchange market. When a foreign government deliberately lowers the value of its currency, it could result in more US imports from that country and hurt the price competitiveness of US exports. While currency manipulation has not been a significant concern in recent years, the recent strength of the US dollar against other currencies, such as the Japanese yen, Chinese yuan, and Vietnamese dong, may reignite debate over the issue. The Biden Administration struggles to fight high inflation using high-interest rates, making it extremely challenging to “devalue the US dollar” in a macro sense. In comparison, the second Trump administration could designate countries of concern as currency manipulators, followed by new retaliatory measures, including tariffs or other trade barriers.

Industrial policy and subsidy: The Biden administration has packaged industrial policy as a core pillar of “Bidenomics,” which has pledged more than $805 billion in new subsidies for semiconductor manufacturing and research, climate and energy investments, and infrastructure spending. In comparison, the Republicans would be more inclined to let market forces determine the outcome of these policies rather than funding them through the government. It is also likely that the second Trump administration will tighten certain rules related to foreign entities taking advantage of US tax credits. However, there could be coordinated investments and supply chain resilience efforts in Biden and Trump’s second term, such as tactical coordination to prevent global subsidy races and disruptions in supply chains.

Trade policy as a tool for other issues: Reviving the Trans-Pacific Partnership (TPP) or similar mid-2010s era trade agreements was slim during the Biden administration. Instead, the Biden administration prioritizes a climate and trade agenda, as evidenced by the launch of a new White House Climate and Trade Task Force. Biden administration will continue to prioritize investments in domestic production capacity while looking outward to use trade to support other non-trade objectives.

In comparison, the Trump administration was more aggressive in pushing back against protectionist trade measures against US products but also less optimistic about the willingness of other countries to engage in good-faith negotiations with the US. Further, Trump 2.0 will likely return to trade policies similar to his first term, including potential tariffs of up to 60% on Chinese imports and an across-the-board tariff of 10% on all imports. Further, there is bipartisan support for increasing tariffs on Chinese goods, considering the deteriorating bilateral relationship. However, a 10% global tariff on imports from countries like Switzerland and Ireland could be more controversial due to potential consumer price impacts and damage to US alliances.

Discussion questions:

Any of the aforementioned issues could potentially impact fashion apparel companies? Why?

In your view, is it preferable for the textile and apparel industry not to be a focus of US trade policy? Why?

What are your top 1-2 takeaways from the panel discussion?

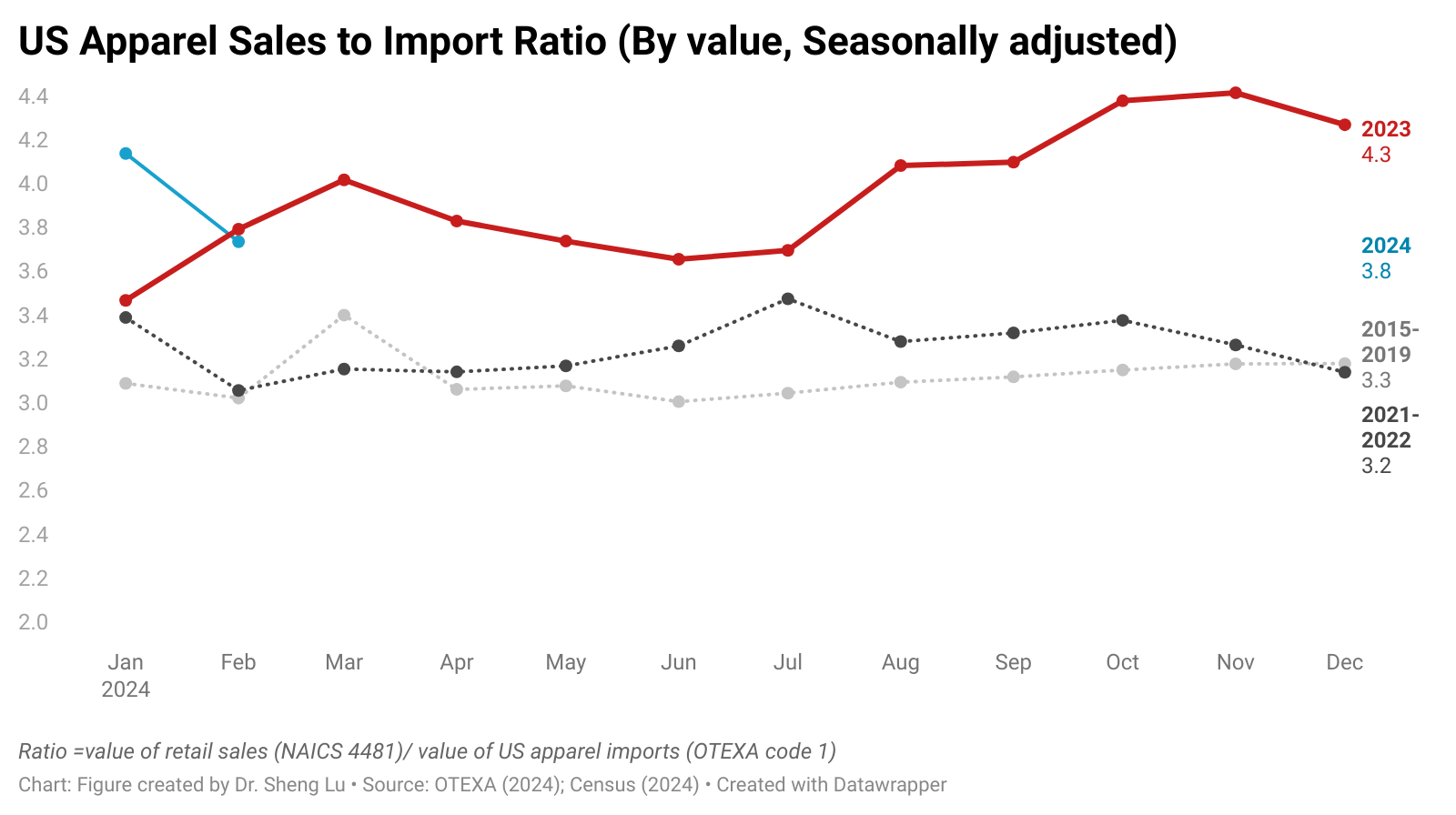

The latest US apparel import data raises several puzzles that deserve to be investigated further.

Question 1: Why did imports suddenly surge, and is this surge sustainable?

Unexpectedly, US apparel imports experienced a significant surge in February 2024. This surge was marked by a 12.9% increase in quantity and a 2.9% increase in value compared to the previous year. Seasonally adjusted US apparel imports in February 2024 were also nearly 10% higher than in January 2024. The import surge was particularly surprising given that the value of US clothing sales in February 2024 was only 1.3% higher than a year ago and even 0.5% lower than in January 2024 (seasonally adjusted).

Therefore, it will be important to watch whether the US apparel trade has indeed reached a turning point and will continue growing in the coming months and throughout the year.

Question 2: Could the volume of US apparel imports in 2023 have been underreported?

With over 98% of clothing sold in the US retail market being imported today, there exists a strong correlation between US apparel retail sales (NAICS code 4481) and the volume of apparel imports. Between 2015 and 2022, the US clothing sales to clothing import ratio remained consistently around 3.0-3.2 (seasonally adjusted). In other words, the value of retail sales was approximately three times the value of apparel imports. However, in 2023, this ratio increased to 4.0-4.5.

One suspicion is that as more apparel imports came into the US through the de minimis, the official US apparel import data in 2023 was somewhat underreported. Notably, according to Euromonitor, about 40% of US apparel retail sales were achieved through e-commerce in 2023, a substantial increase from 9.4% in 2010. Likewise, with US customs tightening controls on “small package shipments” and enhancing UFLPA enforcement, more imports likely began entering through the standard procedure in recent months, which explains why the US apparel sales to import rato fell back to 3.8 in February 2024.

On the other hand, some say the lowered US apparel import volume in 2023 was due to retailers’ efforts to control inventory levels. Data shows that US clothing stores’ stock-to-sales ratio in the last quarter of 2023 averaged 2.34, slightly lower than 2.43 from 2015 to 2019, but was higher than 2.19 back in 2021. In other words, while there was some effort by retailers to control inventory (as seen by the ratio being lower than pre-pandemic levels), it wasn’t a significant enough change to have a large impact on import demand. Also, considering that apparel is a seasonal product, it doesn’t seem too likely that retailers would risk losing sales opportunities during the most critical selling season of the year (i.e., 4th quarter) by promoting outdated items instead of stocking new ones on the shelf.

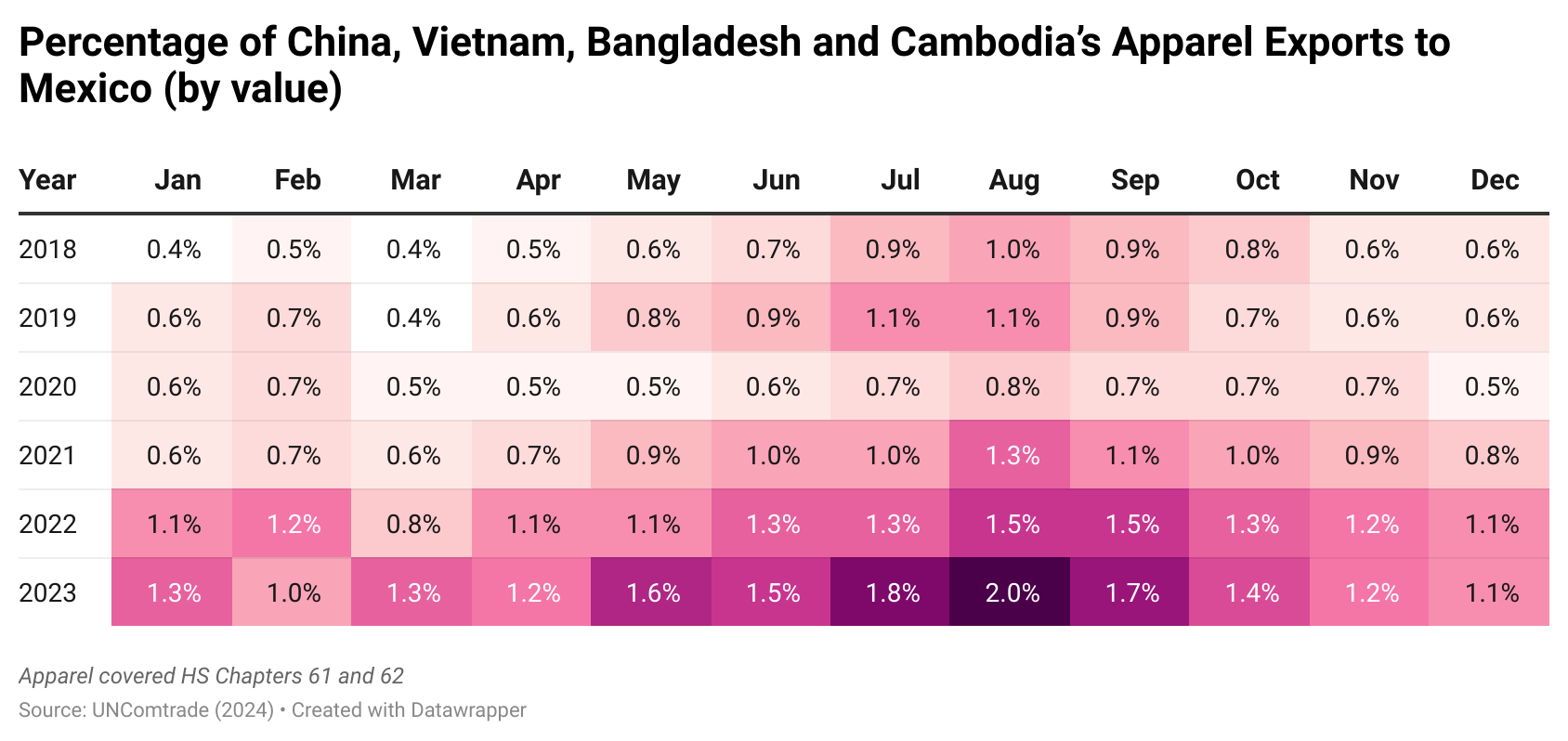

Question 3: Why did Asian countries export more apparel to Mexico?

As a developing country, Mexico is not traditionally a leading apparel import market due to consumers’ limited purchasing power and the sufficient local apparel supply. Take China, Vietnam, Bangladesh, and Cambodia, the four top Asian apparel exporting countries (Asia4), for instance. Between 2018 and 2020, Mexico typically accounted for 0.4%-0.7% of Asia4’s total apparel exports. However, since 2022, Asia4 has almost doubled its apparel exports to Mexico (i.e., increased to 1.5%-2.0%). Moreover, during the same period, the percentage of Asia4’s apparel exports to the United States declined from 27% to below 20%, especially in the last quarter of 2023.

What’s behind the increase in Asian countries’ apparel exports to Mexico needs to be investigated further. As noted earlier, Mexico itself is a leading apparel-producing country. Also, according to Euromonitor, the clothing market in Mexico stayed relatively stable at around 7.6%-7.9% of the size of the US from 2017 to 2023 (in quantity). In other words, Mexico’s increased import demand for Asian clothing doesn’t make much sense.

Others suspect some Asian apparel exports to Mexico eventually entered the US market either by taking advantage of the de minimis rule or the US-Mexico-Canda (USMCA) trade agreement. However, the exact size of this particular trade flow calls for further investigation.

#1: On April 5, 2024, the US Department of Homeland Security (DHS) released its new enhanced strategy to combat illicit trade and level the playing field for the American textile industry and the estimated over 500,000 US textile jobs*. *note: according to the Bureau of Labor Statistics, as of December 2023, the US textile and apparel manufacturing sector employed about 272,400 workers (seasonally adjusted), including 89.3K in NACIS313 textile mills, 95.6K in NAICS314 textile product mills and 87.5K in NAICS315 apparel manufacturing. As of December 2023, NAICS 4482 apparel retail stores employed about 850,000 workers (seasonally adjusted).

According to DHS, the new enforcement plan will focus on the following areas:

Cracking down on small package shipments to prohibit illicit goods from U.S. markets by improving screening of packages claiming the Section 321 de minimis exemption for textile, Uyghur Forced Labor Prevention Act (UFLPA), and other violations, including expanded targeting, laboratory and isotopic testing, and focused enforcement operations.

Conducting joint Customs and Border Protection (CBP)-Homeland Security Investigation (HIS)HSI trade special operations to ensure cargo compliance. This includes physical inspections; country-of-origin, isotopic, and composition testing; and in-depth reviews of documentation. CBP will issue civil penalties for violations of U.S. laws and coordinate with HSI to develop and conduct criminal investigations when warranted.

Better assessing risk by expanding customs audits and increasing foreign verifications. DHS personnel will conduct comprehensive audits and textile production verification team visits to high-risk foreign facilities to ensure that textiles qualify under the U.S.-Mexico-Canada Agreement (USMCA) or the Central America-Dominican Republic Free Trade Agreement (CAFTA-DR). (note: As CBP noted, most US free trade agreements and trade preference programs have complex textiles and apparel-specific rules of origin requirements. CBP is “responsible for ensuring that the trade community complies with all statutory, regulatory, policy, and procedural requirements that pertain to importations under free trade agreements and other trade preference programs.”)

Building stakeholder awareness by engaging in an education campaign to ensure that importers and suppliers in the CAFTA-DR and USMCA region understand compliance requirements and are aware of CBP’s enforcement efforts.

Leveraging U.S. and Central American industry partnerships to improve facilitation for legitimate trade. (note: The Biden Administration aims to leverage textile and apparel trade as part of the solution to address “root causes of migration in Central America. According to the White House Fact Sheet released in March 2024, the Office of the U.S. Trade Representative and Central American Trade Agencies and textiles and apparel industry stakeholders will work together to build a directory with detailed profiles of manufacturing and sourcing companies in the region, including information on business practices and production capabilities, to facilitate transparent sourcing, and bolster the region’s supply chain.)

Expanding the Uyghur Forced Labor Prevention Act (UFLPA) Entity List to identify malign suppliers for the trade community through review of additional entities in the high-priority textile sector for inclusion in the UFLPA Entity List. (note: Once an entity is on this list, in general, it is prohibited from exporting its goods to the United States. Importers are required to ensure the supply chains of their imported products are free from entities on the Entity List).

#2: Several US textile and apparel industry stakeholders have publicly responded to DHS’s new strategy.:

“We strongly commend DHS for the release of a robust textile and apparel enforcement plan today. We also greatly appreciate Secretary Mayorkas’ personal engagement in this urgent effort and believe it’s a strong step forward to addressing pervasive customs fraud that is harming the U.S. textile industry.”

“The essential and vital domestic textile supply chain has lost 14 plants in recent months. The industry is facing severe economic harm due to a combination of factors, exacerbated by customs fraud and predatory trade practices by China and other countries, which has resulted in these devastating layoffs and plant closures. DHS immediately understood the economic harms facing the industry and deployed the development of a critical action plan.”

“The industry requests include

Ramped up textile and apparel enforcement with regard to Western Hemisphere trade partner countries, including onsite visits and other targeted verification measures to enforce rules of origin as well as to address any backdoor Uyghur Forced Labor Prevention Act (UFLPA) violations.

Increased UFLPA enforcement to prevent textile and apparel goods made with forced labor from entering our market, including in the de minimis environment.

Immediate expansion of the UFLPA Entity List, isotopic testing, and other targeting tools. Intensified scrutiny of Section 321 de minimis imports and a review of all existing Executive Branch authorities under current law to institute basic reforms to this outdated tariff waiver mechanism. “

“We appreciate the Department of Homeland Security (DHS)’s announcement today outlining enhanced enforcement activities to prevent illicit trade in textiles. Our members support 55 million (more than one in four) American jobs and invest considerable time and resources in their customs compliance programs. Many of our members are Tier 3 participants in Customs-Trade Partnership Against Terrorism (C-TPAT). They are trusted traders and meet the high standards required to receive that designation by U.S. Customs and Border Protection and DHS. Our members are on the front lines for ensuring that they have safe and secure supply chains.

“While DHS launches this enforcement plan, we urge it to partner with our associations and our associations’ members. A successful enforcement plan must include input from all stakeholders, clear communication with the trade, and coordinated activities with importers, especially if DHS finds illicit activity happening in the supply chain. The results of any illicit activities must be shared so that our members and other importers can act quickly to address the issue. As our members look to diversify their supply chains, especially back to the Western Hemisphere, we must make sure efforts are included to incentivize and not deter new investments.”

#3 Comments: Overall, the new DHS textile enforcement plan suggests several key US textile and apparel trade policy directions: 1) revisit the current de minimis rules that are used by many e-commerce businesses; 2) further strengthen the UFLPA and forced labor enforcement; 3) expand the Western hemisphere textile and apparel supply chain and encourage more US apparel sourcing from CAFTA-DR members; 4) scrutinize US apparel imports from China and imports from other Asian countries that heavily use textile raw material from China.

Discussion questions for FASH455 (please answer them all):

How do the perspectives of the US textile industry and US fashion brands and retailers diverge concerning CBP’s new strategy? What are the areas in which they share common ground?

Building on the previous question, how can the difference between the US textile industry and US fashion brands and retailers be explained regarding their response to DHS’s new enforcement strategy?

As a sourcing manager for a major US apparel brand with global operations, how do you plan to adjust your company’s sourcing practices in light of DHS’s new strategy? You can list 1-2 detailed action plans and provide your analysis.

Background

The U.S. Customs and Border Protection (CBP) is an agency within the Department of Homeland Security (DHS), responsible for “regulating and facilitating international trade, collecting import duties, enforcing U.S. trade laws, and protecting the nation’s borders.”

Homeland Security Investigations (HSI) is also a division within the Department of Homeland Security (DHS), responsible for “investigating transnational crime and threats, specifically those criminal organizations that exploit the global infrastructure through which international trade, travel and finance move.”

Cecilia Malmström, Nonresident Senior Fellow, Peterson Institute for International Economics (PIIE)

Eva Maydell, Member, European Parliament; Rapporteur for the European Union’s AI Act

Joshua P. Meltzer, Senior Fellow, Global Economy and Development Program, Brookings Institution

Key points

AI has the potential to optimize supply chains, analyze shipping routes, forecast demand, and enhance risk assessment and fraud detection.

AI could potentially offer better market intelligence to help businesses make better-informed decisions and improve forecasting accuracy.

AI could reduce barriers to trade in services and technical barriers of trade (TBT) and empower small and medium-sized enterprises (e.g., translation services)

While trade in goods has peaked, services trade continues to grow substantially, even during COVID-19, with digital services and professional services being the main drivers. AI could further facilitate the expansion of service trade.

AI is already affecting the nature of jobs and the services trade.

Policymakers need to focus on creating an environment that supports the development and deployment of AI, particularly by balancing the need to provide regulatory guardrails and the need to encourage business innovation.

AI regulation is currently fragmented worldwide. However, there is significant potential for establishing international standards and regulatory coherence, offering a common approach to regulating AI.

Building more societal trust among the business community, policymakers, and civil society is necessary to address concerns about AI and related challenges.

Students in FASH455 have proposed the following discussion questions based on the readings about the US textile and apparel industry and fashion companies’ sourcing strategies. Everyone is welcome to join the online discussion. For FASH455 students, please address at least two questions and mention the question number (#) in your reply.

#1 As a developed country, should the US prioritize further strengthening highly capital-intensive yarn manufacturing, or should we rebuild a vertically integrated textiles and apparel supply chain (e.g., yarns, fabrics, and garments) at home? What is your recommendation, and why?

#2 In FASH455, we discussed how the US textile industry has experienced a decline in employment despite increasing production volumes, largely due to advancements in technology. However, why is import competition often cited in the media as the single largest threat to the US textile industry?

#3 While studies show that US fashion companies are reducing “China exposure,” measured in quantity, China still accounted for 36.1% of US apparel imports in 2023, even higher than 34.7% in 2022. How can we explain this phenomenon? What factors have made US fashion companies hesitant to move away from China?

#4 How will US fashion companies’ growing interest in carrying more sustainable textiles and apparel affect their sourcing destinations and supply chains? Will developing countries with cheap labor and/or developed countries with the right capital and technology be the winners in the sustainability movement? Please provide your thoughts.

#5 Will the growing demand for supply chain transparency and traceability reduce the incentives or add additional burdens for fashion companies to diversify their supply chain further? What are the benefits of pursuing sourcing diversification other than mitigating the potential sourcing risks?

#6 What is your vision for the use of AI in apparel sourcing? What key sourcing and supply chain problems facing fashion brands and retailers can AI potentially solve?

Speaker: Katherine Tai (U.S. Trade Representative, Office of the U.S. Trade Representative)

Presider: Michael Froman (President, Council on Foreign Relations; Former U.S. Trade Representative, 2013-17)

Excerpt from the conversation

Worker-Centric US trade policy

Question from FROMAN: “Back in the old days, there was a notion that since the U.S. market is relatively open—we don’t have that much protection here, the average applied tariff is about 3 ½ percent—that if we were able to reduce barriers to other countries disproportionately we could export more made by U.S. workers, and that export-related jobs paid more than non-export related jobs, and that we could use access to our market as a way of getting other countries to reform their labor practices and raise their standards, which would create a more level playing field. That theory is sort of out of vogue at the moment. But, tell me, can you envisage what an agreement that is worker-centric looks like that reduces barriers or increases trade?”

Response from TAI: “The percentage of (U.S.) exports to GDP is around 10 percent—maybe 11 or 12 percent. So it’s not very high. Some of our—some of our trading partners have very, very high exports as a proportion of GDP (e.g., 25 percent)…So you just have to put that (trade liberalization) into context. I think you also have to think about the fact of the balance of exports and imports…”

“We’re trying to create and maintain jobs, and good jobs, at home… so then the question becomes not what do I have to pay you to do X, Y, or Z, but how can we put the forces of our cooperation together? What does the deal look like where we are building our middle classes together? And I think that the worker pieces then come in, along with the environment pieces, as something that I shouldn’t have to pay you to do, but as something that you should want to do…”

“Traditionally we’ve kept our scorecard by, you know, how many trade agreements you finished and how many you’ve gotten across the finish line… Our progress lies very much in how the conversation has fundamentally shifted. That the conversation now is very much focused on supply chain resilience, on equity, and how not to leave those within our economies behind further, how not to leave those developing countries behind further.”

Digital trade

Question from FROMAN: “For a long time, the U.S. had a position around the free flow of data across borders, not taxing digital products across borders… given the fact that the U.S. economy is probably—certainly the leader in all things digital, what does it mean for us to move away from defending these principles that have been so core to what we’ve tried to do before?”