In December 2023, Just-Style consulted a panel of industry experts and scholars in its Outlook 2024–what’s next for apparel sourcing briefing. Below is my contribution to the report. Welcome any comments and suggestions!

What’s next for apparel sourcing?

Apparel sourcing is never about abrupt changes. However, fashion companies’ sourcing practices, from their crucial sourcing factors and sourcing destinations to operational priorities, will gradually shift in 2024 in response to the evolving business environment.

First, besides conventional sourcing factors like costs, speed to market, and compliance, fashion companies will increasingly emphasize flexibility and agility in vendor selection. One driving factor is economic uncertainty. For example, according to leading international organizations such as the World Bank and the International Monetary Fund (IMF), the world economy will likely grow relatively slowly at around 2.6%-3% in 2024. However, it is not uncommon that the economy and consumers’ demand for clothing could perform much better than expected. This means companies need to be ready for all occasions. Likewise, geopolitical tensions, from the Russia-Ukraine war and the US-China decoupling to the military conflict in the Middle East, could cause severe supply chain disruptions anytime and anywhere. Thus, fashion companies need to rely on a more flexible and agile supply chain to address market uncertainties and mitigate unpredictable sourcing risks.

Secondly, it will be interesting to watch in 2024 to what extent fashion companies will further reduce their exposure to China. On the one hand, it is no surprise that fashion companies are reducing finished garments sourcing from China as much as possible. However, fashion brands and retailers also admit that it is difficult to find practical alternatives to China in the short to medium terms regarding raw textile materials and orders that require small runs and great variety. Meanwhile, investments from China are flowing into regions considered alternative sourcing destinations, such as the rest of Asia and Central America. These new investments could complicate the efforts to limit exposure to China and potentially strengthen, not weaken, China’s position in the apparel supply chains. And stakeholders’ viewpoints on “investments from China” appear even more subtle and complicated.

Third, regulations “behind the borders” could more significantly affect fashion companies’ sourcing practices in 2024, particularly in sustainability-related areas. While sustainability is already a buzzword, fashion companies must deal with increasingly complex legal requirements to achieve sustainability. Take textile recycling, for example. The enforcement of the Uyghur Forced Labor Prevention Act (UFLPA) on recycled cotton, the US Federal Trade Commission’s expanded Green Guides, the EU’s extended producer responsibility (EPR) program and its strategy for sustainable textiles, and many state-level legislations on textile waste (e.g., California Textile Recycling Legislation) may all affect companies’ production and sourcing practices for such products. Fashion companies’ sourcing, legal, and sustainability teams will need to work ever more closely to ensure “sustainable apparel” can be available to customers.

Apparel industry challenges and opportunities

In 2024, a slow-growing or stagnant world economy will persist as a significant challenge for fashion companies. Without sourcing orders from fashion brands and retailers, many small and medium-sized manufacturers in the developing world may struggle to survive, leaving garment workers in a precarious financial situation. China’s economic slowdown could worsen the situation as many developing countries increasingly treat China as an emerging export market. With shrinking domestic demand, more “Made in China” apparel could enter the international market and intensify the price competition.

Another challenge is the rising geopolitical tensions and political instability in major apparel-producing countries. For example, while a broad base supports the early renewal of the African Growth and Opportunity Act (AGOA), which will expire in 2025, the reported human rights violations in some essential apparel exporting countries in the region could complicate the renewal process in US Congress. Likewise, even though the Biden administration is keen to encourage fashion companies to expand sourcing from Central America, political instability there, from Nicaragua to Haiti, makes fashion companies hesitant to make long-term sourcing commitments and investments. Furthermore, 2024 is the election year for many countries, from the US to Taiwan. We cannot rule out the possibility that unexpected incidents could trigger additional instability or even new conflict.

On the positive side, it is encouraging to see fashion companies continue to invest in new technologies to improve their operational efficiency in apparel sourcing. Digital product passports, 3D product design, PLM, blockchain, Generative AI, and various supply chain traceability tools are among the many technologies fashion companies actively explore. Fashion companies hope to leverage these tools to improve their supply chain transparency, strengthen relationships with key vendors, reduce textile waste, accelerate product development, and achieve financial returns.

It is also a critical time to rethink and reform fashion education. In addition to traditional curricula like apparel design and merchandising, we need more partnerships between the apparel industry and educational institutions to expose students to the real world. More direct engagement with Gen Z will also benefit fashion companies tremendously, allowing them to understand their future core customers and prepare qualified next-generation talents.

The full article is here(Just-Style access required). Below are the key findings:

Based on a content analysis of the annual reports of about 30 largest US fashion brands and retailers from 2018 to 2023, this study aims to identify these companies’ most critical evolving sourcing practices, including their sourcing destination adjustment, primary sourcing factors, and emerging sourcing-related “hot topics.” The findings provide critical market intelligence, informing US fashion companies about their peers’ emerging sourcing trends and popular practices. The results show that:

First, maintaining a relatively diverse sourcing base remains common among US fashion companies. Results show that large-size companies today typically source from more than 20 countries. One critical factor behind fashion companies’ sourcing diversification strategies is that no single supplying country is “perfect,” given the increasingly complex sourcing factors. Sourcing diversification allows fashion companies to balance various sourcing factors. For example, according to company #19, “the (sourcing diversification) approach provides us with the greatest flexibility in identifying the appropriate manufacturers while considering quality, cost, timing of product delivery and other criteria.” On the other hand, sourcing diversification enables companies to adapt quickly to market uncertainties and enjoy supply chain flexibility and resilience.

Second, while US fashion companies are not necessarily leaving any particular countries they source from, many have substantially reduced the number of vendors they work with over the past few years. Specifically, out of the 30 fashion companies the study examined, over 60% explicitly mentioned they consolidated their sourcing base at the vendor level from 2017/2018 to 2022/2023, although the degree varied. For example:

Company #4, a leading sportswear brand, cut its contracted factories from 363 to 291 (or down 19.8%)

Company #6, which owns several jeans and sportswear brands, reduced its contracted factories from 1,000 to around 340 (or down 66%)

Company #9, a well-known specialty clothing store, cut its vendors from 800 to 250 (or down 68.8%)

Company #26, a specialty clothing store targeting the youth, cut its vendors from 150 to around 119 (or down 20.7%)

Company #28, a discount department store, cut its vendors from 3,100 to around 2,800 (or down 9.7%)

Associated with the trend of “country diversification and vendor consolidation,” US fashion companies are increasingly interested in working with “super vendors,” e.g., those with multiple country presence or vertical manufacturing capability. The use of “super vendor” can also be observed in fashion companies’ willingness to give more sourcing orders to their top suppliers. For example, Company #18, a casual and outdoor wear retailer, reduced its vendors from 200 in 2017/2018 to 110 in 2022/2023, but increased the cap of sourcing orders for its top 10 vendors from 40% to 47% over the same period.

Third, regarding the sourcing base, many US fashion companies have intentionally reduced their apparel sourcing from China, given the US-China tariff war, deteriorating bilateral relations, and the forced labor concerns with China’s Xinjiang region (XUAR). Specifically, more than one-third of the examined companies explicitly mentioned their strategy to reduce finished garments sourcing from China. Furthermore, several US fashion companies indicated their “reducing China exposure” strategy would continue, implying China’s market share in the US apparel import market could decrease further.

Nevertheless, even though fewer finished garments are coming from China, US fashion companies admit that China will continue to play a critical role as a textile raw material supplier as no immediate practical alternative is available. For example, Company #20, a specialty clothing chain focusing on trendy and fashionable items, says, “During fiscal 2022, we sourced most of our finished products with partners and suppliers outside the US and we continued to design and purchase fabrics globally, with most coming from China.”

Fourth, in line with trade statistics, US fashion companies consider other Asian suppliers, such as Vietnam, Bangladesh, Cambodia, and Indonesia, as their top choices as China’s alternatives.In comparison, few fashion companies explicitly mentioned moving their sourcing orders from China to Western Hemisphere countries or other regions.

Additionally, regarding emerging “hot topics” related to sourcing:

Geopolitics: the deteriorating US-China relations, escalated trade tensions expanded from tariffs to forced labor, and the potential trade disruptions have concerned US fashion companies significantly. Notably, US fashion companies regard sourcing from China as increasingly risky, with the implementation of the Uyghur Forced Labor Prevention Act (UFLPA) in June 2022. For example, according to Company 2, “The Uyghur Forced Labor Prevention Act and other similar legislation may lead to greater supply chain compliance costs and delays to us and to our vendors.”

Near-shoring: due to the decoupling and de-risking from the China movement, US fashion companies have begun actively exploring near-shoring sourcing opportunities in the Western Hemisphere, particularly from members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR). For example, Company #1, the North American manufacturer, disclosed that “(our) Company relies on a number of preferential trade programs (…) including the Dominican Republic – Central America – United States Free Trade Agreement (CAFTA-DR (…) Collectively, these agreements strengthen US economic relations and expand trade with Central America, the Dominican Republic, and Haiti.”

Sustainability and social responsibility: It is noteworthy that aside from climate change and forced labor, which are typically addressed as risk factors, US fashion companies generally hold an optimistic and forward-looking perspective for sustainability, such as new technologies and endeavors toward more sustainable production and sourcing. Terms such as using preferred or recycled materials, supply chain transparency and traceability, and emerging sustainability technologies have been more frequently mentioned in companies’ annual or ESG reports. For example, Company #17 says, “Increase the usage of environmentally preferred materials to comprise 32.6% of the brand’s global materials footprint.”Company #2 adds, “Our goal is to use preferred materials in 100 percent of our products by 2030.” Company #9 states, “We collaborate with suppliers to increase the supply of preferred raw materials.”

Supply chain transparency: US fashion companies attach great importance to improving supply chain transparency and traceability. Compared to the past, fashion companies are more willing to invest in new technologies and digital tools, allowing them to map supply chains and achieve sustainability goals more effectively. Related to this, US fashion companies have actively engaged with industry associations and other industry communities outside the company to stay informed about sustainability trends and learn best practices.

Students in FASH455 have proposed the following discussion questions based on the videos about the state of textile and apparel in Asia. Everyone is welcome to join the online discussion. For FASH455 students, please address at least two questions and mention the question number (#) in your reply.

#1 We have seen all the improvements and “upgrading” Vietnam has made toward the fashion industry. What can the garment industry in other countries take away from Vietnam’s experiences?

#2 Is Asia’s highly integrated apparel supply chain unique to the region? Can the Western Hemisphere “copy” Asia’s model?

#3 How can Asia’s textile and apparel industry balance the growing demand for sustainability and the need to remain cost-competitive? What innovative strategies can be adopted to achieve this balance?

#4 As Asian textiles and apparel factories continue to improve their efficiency and expand product offers, will it be beneficial for the US to reach a trade agreement with Asian countries? Or do you believe such an agreement might contradict the goals we try to achieve from CAFTA-DR?

#5 Will Vietnam eventually become the next China, or could its labor shortages be a significant barrier preventing its textile and apparel industry from advancing to the next level?

#6 Should textile and garment factories in Asia make more efforts to appeal to the younger generation (e.g., Gen Z)? Or is automation the solution?

#7 To what extent do you think Asian apparel exporting countries (e.g., Bangladesh, Vietnam and Cambodia) will reduce their dependence on textile raw materials supply from China due to the Uyghur Forced Labor Prevention Act (UFLPA)? Or, instead, do you think Asian apparel-exporting countries other than China benefit from UFLPA?

#8 The video shows that Asian countries have begun to invest heavily in new production capacities for textile recycling. Do you believe the region will continue to dominate textile and apparel production in the era of fashion circularity? Or will the emergence of textile recycling shift the world textile and apparel trade patterns in the long run?

Beth Hughes serves as the Vice President of the American Apparel and Footwear Association (AAFA), responsible for supporting the association’s efforts on international trade and customs issues. Beth oversees AAFA’s Trade Policy Committee, as well as AAFA’s Customs Group. Beth is also the spokesperson of the Coalition for Economic Partnership in the Americas (CEPA), a group of prominent American companies, and manufacturers committed to advancing regional trade and employment opportunities in the Western Hemisphere.

Before joining AAFA, Beth served for six years as senior director of international affairs at the International Dairy Foods Association. Beth earned a Bachelor of Arts degree in political science at George Washington University and received a Master of Arts in international affairs from Florida State University.

The interview was conducted by Leah Marsh, a graduate student in the Department of Fashion and Apparel Studies at the University of Delaware. Leah’s research focused on exploring EU retailers’ sourcing strategies for clothing made from recycled textile materials and fashion companies’ supply chain and sourcing strategies.

Julia K. Hughes is President of the United States Fashion Industry Association (USFIA), which represents brands, retailers, importers, and wholesalers based in the United States and doing business globally. She represents the industry in front of the U.S. government as well as international governments and stakeholders, explaining how fashion companies create high quality jobs in the United States and economic opportunities around the world.

An expert on textile and apparel trade issues, Julie has testified before Congress and the Executive Branch. She frequently speaks at international conferences including the China & Asia Textile Forum, Fashion Institute of Technology (FIT), Harvard University’s Bangladesh Development Conference, MAGIC, Prime Source Forum, Vietnam Textile Summit, and others.

Julie served as the first President and is one of the founders of the Washington Chapter of Women in International Trade (WIIT) and is one of the founders of the WIIT Charitable Trust. She also was the first President of the Organization of Women in International Trade (OWIT). In 1992, she received the Outstanding Woman in International Trade award and in 2008, the WIIT Lifetime Achievement Award. She also is a member of the International Women’s Forum.

Julia has an M.A. in International Studies from the Johns Hopkins School of Advanced International Studies and a B.S. in Foreign Service from Georgetown University.

The interview was conducted by Leah Marsh, a graduate student in the Department of Fashion and Apparel Studies at the University of Delaware. Leah’s research focused on exploring EU retailers’ sourcing strategies for clothing made from recycled textile materials and fashion companies’ supply chain and sourcing strategies.

Instructions: In the next few weeks of FASH455, we will learn about many technical aspects of free trade agreements related to apparel sourcing and trade, such as the preferential tariff rates, apparel-specific rules of origin, and trade agreement utilization. However, this presentation takes a different perspective on trade deals– why they are NOT solely about job creation, why trade agreements increasingly focus on “measures behind borders,” and why international institutions like the World Trade Organization (WTO) were established.

Feel free to share your thoughts on the video. You may focus on 1-2 specific points that you find interesting, intriguing, controversial, or debatable and then explain your arguments. You could also propose additional discussion questions for your classmates.

Terminologies mentioned in the video and background notes:

Quota: A quantity restriction on imports. Before 2005, the global textile and apparel trade was subject to 30 years+ quota restrictions. See here for the background information.

Tariff: A tax levied on imports only. Deemed as “import-sensitive,” US still imposes a much higher tariff rate for textile (8.0%) and apparel products (11.6%) than other manufactured goods (2.2%) on average in 2023. See the World Tariff Profile 2023.

Non-tariff barriers (NTB): refers to trade barriers other than tariffs, such as technical barriers of trade (TBT), Sanitary and Phytosanitary (SPS) measures, customs procedures, import licensing, and many others. See more examples here.

GATT and WTO: The General Agreement on Tariffs and Trade (GATT) was a temporary international treaty signed in 1947 by 23 countries (including the United States). GATT aimed to boost trade-led economic recovery after World War II. Since then, GATT members conducted nine major rounds of negotiations to gradually reduce trade barriers, ultimately establishing the World Trade Organization (WTO) in 1995 as the permanent body governing world trade.

Trans-Pacific Partnership (TPP): A trade agreement reached by eleven countries in the Asia-Pacific region (Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, and Vietnam) and the United States in 2016. However, the Trump Administration announced the withdrawal of the United States from TPP in January 2017. Afterward, without the US, the other 11 TPP members reached the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), which officially entered into force in December 2018.

Below are selected comments by US Trade Representative Katharine Tai (Tai) and WTO (World Trade Organization) Director-General Dr. Ngozi Okonjo-Iweala (Ngozi).

What kind of global trade do we want today?

“For decades, the United States has been proud to champion the international rules-based order and the multilateral trading system…But the functioning and fairness of this order are now in question and that is why all of us need to adapt to a more challenging era marked by rapid technological change, increasing extreme climate events, vulnerable supply chains, intensifying geopolitical friction, widening inequality” (Tai)

“The United States is writing a new story on trade. We are pursuing fair competition, addressing the climate crisis, promoting our national security, and ensuring the rules-based system helps all economies, not just the biggest ones.” (Tai)

“how can we harness the effectiveness of our trade tools to be promoting not just efficiency and liberalization, but using those tools to promote what we consider certainly today to be higher goals. And those goals are resilience for our economy and the word economy, sustainability, again, for our economy in the world economy, and inclusivity… we started to see where the concentrations in supply and production started to impact this and spike this economic insecurity on a macro level and also for individuals” (Tai)

Trade and climate change

“trade is necessary to disseminate green technologies and through competition and scale efficiencies to drive down the cost of decarbonization. Another reason is that trade amplifies the impact of environmental policy action. Recent research at the WTO demonstrate that just as countries can reap economic gains by focusing on what they are relatively good at, the world can reap environmental gainsif countries focus on what they are relatively green at” (Ngozi)

Is trade diversification the future?

“A fragmented world economy would not just be bad for already-squeezed household budgets. Without trade, it would become harder, even impossible, to meet the big challenges of our time – resilience, socioeconomic inclusion, and climate change… The problems we encountered in the trading system were less about trade per se and more about excessive concentration for some products and supply relationships. The smart response is to deepen, diverse, and deconcentrate production so there are fewer potential bottlenecks” (Ngozi)

“we believe we can solve the problem by diversifying the supply chains not just to ourselves or to friends but to all over the world where the opportunity exists. Business should look at the possibility of not just doing China+1. It means China plus Vietnam or Indonesia. But they can do Bangladesh. They can do Laos. They can do Rwanda. They can do Senegal. They can do Nigeria. I’m just – Morocco” (Ngozi)

Debate the impact of trade

“Technology was generally a big culprit in job losses…U.S. manufacturing output, the volume of products produced here, is about as high as it has ever been. But the sector employs more machines and fewer people than it used to. Nevertheless, import competition was a significant factor and an easier focus, I think, for political anger.” (Ngozi)

“…between 1995 and 2011, while increased goods import from China did eliminate 2 million jobs in the United States, increased exports to China and elsewhere added 6.6 million jobs to the U.S. economy, 4 million of them from higher-services exports…These numbers illustrate the power of trade for job creation. But as we know, those new jobs were not created in the same places. Neither did they go to the same people. That a backlash would result from those left out was perhaps predictable, but it was not inevitable. There are countries that use domestic-policy levers to translate gains from trade into broadly shared growth by providing people security against income loss and support to seize new opportunities.” (Ngozi)

Renew or update the African Growth and Opportunity Act?

“The world is really different from when AGOA was first created…So I think copy-paste is to really lose an important opportunity…we should be practical. Also, we’re on a timeline…The AfCFTA, the African Continental Free Trade Area, that has been concluded, that has that has been brought into being by the countries on the continent. And those continental integration aspirations should absolutely be reflected in our offer to Africa, and something we should try to figure out how to incorporate” (Tai)

“African countries appreciate AGOA. They would like to see an agreement that is, you know, at least a decade out so that they have some predictability. What they’re hearing from investors is that with this up in the air, they can’t make up their minds whether to invest or not because they don’t know what will happen. So I think if we can reform and get it done, and people can have a predictable time horizon for AGOA, it would really help” (Ngozi)

How to reform the World Trade Organization?

“The United States wants a WTO where dispute settlement is fair and effective, and supports a healthy balance of sovereignty, democracy, and economic integration where all members embrace transparency, where we have better rules and tools to tackle non-market policies and practices, and to confront the climate crisis and other pressing issues.” (Tai)

“We must recognize the diversity of developing members. We should have flexibilities in the rules that reflect actual needs. But we cannot have economic and manufacturing powerhouses gaming the system by claiming the same development status and flexibilities intended for less-advantaged members.” (Tai)

“people ask me all the time, oh, are you worried because there are so many [Free trade agreement, FTA]? I’m not. Like I said, 75 percent of trade still goes on WTO terms [MFN tariff rates]. And we can learn from them.” (Ngozi)

“I don’t have enough time and money to waste resources in Geneva on a process that we don’t actually believe in…When President Biden talks about it from the floor of the United Nations General Assembly, if we still have trading partners who want to question our seriousness, then I think the problem is those partners and it’s not us” (Tai) [note: this comment was mentioned by Politico]

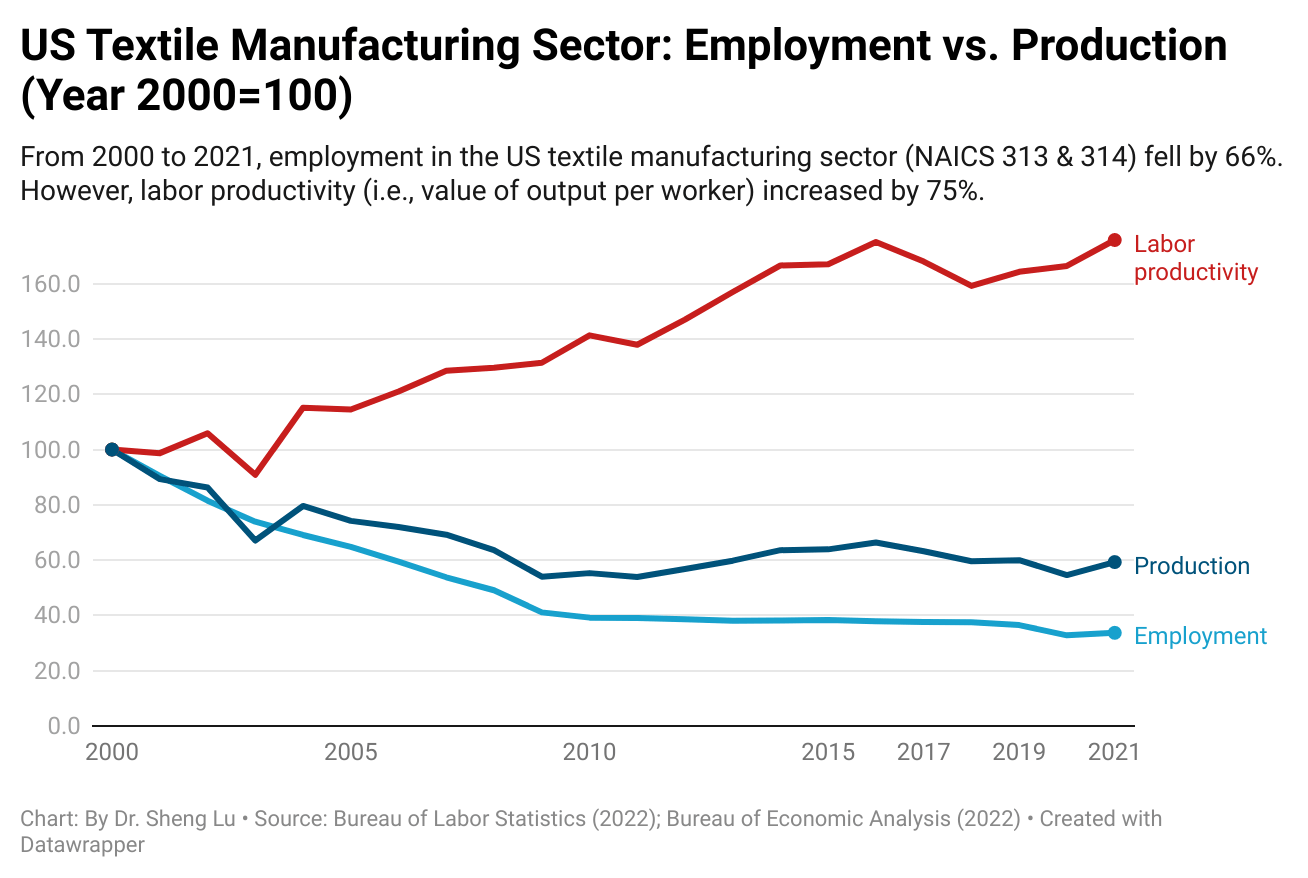

Argument: The U.S. textile manufacturing industry has been a winner of globalization

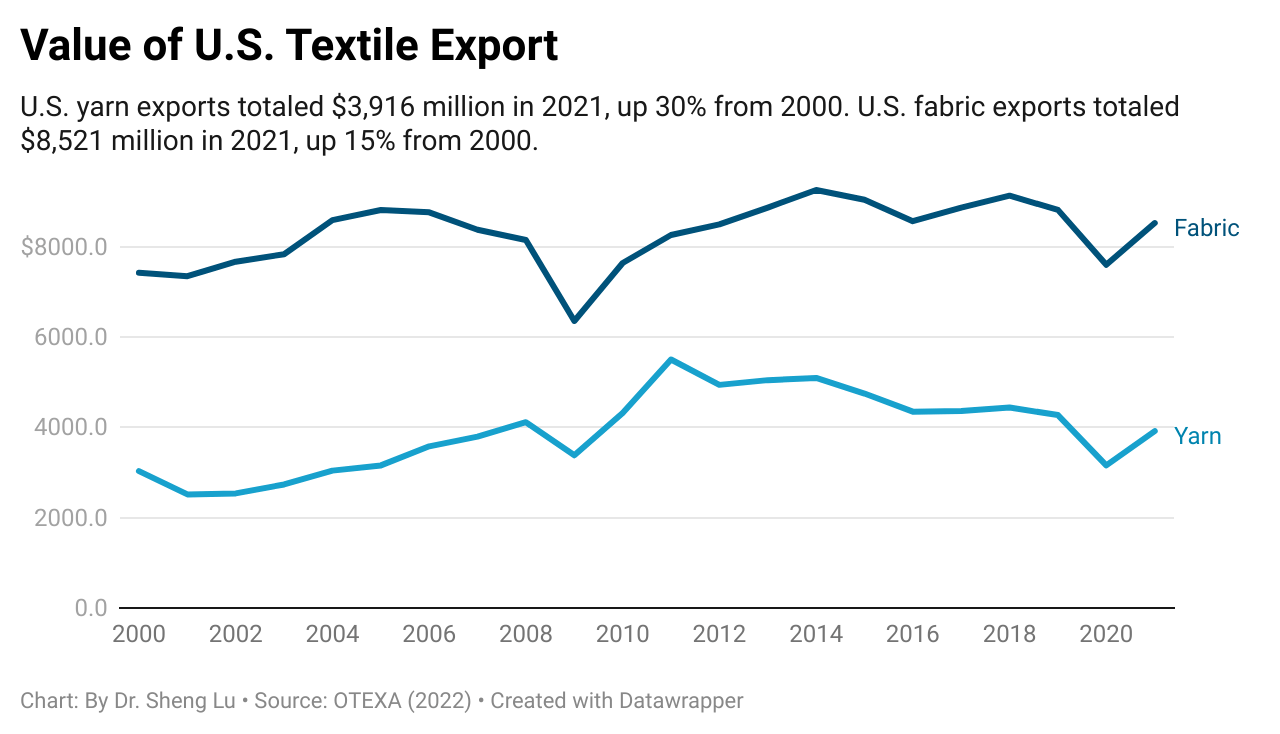

Comment #1: While it is true that many Americans lost their jobs due to the increase in trade, there are more benefits to both importing and exporting rather than the mercantilist view of trade. Increasing trade and globalization, especially during the Clinton administration, was an opportunity to develop strong relationships with other nations. The value of U.S. textile exports since 2000 has risen by 30% for yarn and 15% for fabric, after the establishment of agreements such as NAFTA. Additionally, one of the U.S. apparel manufacturers in the video used machinery for their production from Sweden. Without globalization and trade, they would not be able to use this high-tech equipment. All in all, U.S. textile manufacturing sector benefits from both importing and exporting goods.

Comment #2: Deeper down, the US textile sector seems to be winning in the long run. The squeeze that globalization has placed on them has allowed for innovation within the industry as they fight to stay relevant and compete with overseas goods. Operational slack such as high turnover jobs have been eliminated with automation, and US manufacturers gained a new branding niche that overseas companies do not: a US “personal touch.” Consumers may now be more willing to pay more for a garment just because it says it is made in the USA. USA-made clothing may now be perceived as higher quality and more scarce. The sentiment towards US-made goods and their quality could enact change to reduce overseas reliance, which is a win for US manufacturing in the long run. Additionally, globalization expands the export market for the US textile manufacturing sector.

Comment #3: As discussed in the video, there is a growing trend of reshoring and regionalization in some manufacturing sectors, including textiles. Some U.S. textile manufacturers have seized this opportunity to bring production back to the United States, capitalizing on the advantages of local supply chains, quality control, and speed to market. The video also shows how technology and automation can help streamline production processes and make manufacturing more competitive, even in higher-cost regions like the United States. US textile manufacturers have invested in innovation and automation, making them competitive in producing textiles with advanced features and properties in today’s global economy. It is globalization that is pushing the US textile industry to adopt these new technologies and continue improving its international competitiveness.”

Argument: the U.S. textile manufacturing industry has been a loser of globalization

Comment #4: One of the biggest arguments for globalization is the lower prices & affordability for the consumer. From this perspective, it seemed that the United States was a winner of globalization as a whole. However, when beginning to look at the consequences of moving production overseas, we not only see the textile manufacturing sector being affected, but we also see this impact disperse to the communities in America as well. When brands offshore and outsource production overseas for lower prices & labor, our very own US textile manufacturing industry is losing out on this business. It also forces this industry into a highly competitive environment that does not have equal “playing fields” and does not have insurance/protection in case environmental factors ruin crops. The US has clear labor laws and human rights policies (as well as increasing environmental policies), whereas their cotton-growing competitors, for instance, do not have to follow the same rules. This allows labor exploitation to decrease costs and makes US companies seem unappealing or less competitive.

Comment #5: Over the past few decades, the number of manufacturing jobs in the US textile industry has plummeted after companies began moving production overseas, specifically to countries like China, which have preferential treatment. These foreign facilities can produce things much faster and cheaper because the standards and regulations are completely different than those of the United States. Free trade does not consider these differences in labor and environmental laws, making it much less “free” than it claims. As countries overseas– specifically China and regions like Xinjiang– continue to not play by the rules, the US is forced to keep up by implementing things like the Toyota System…Americans want to be the best in manufacturing and globalization often gets in the way of this. With near-shoring, the US can reclaim high-quality, American-made garments while helping with job security and sustainability.

Comment #6: Overall, I believe that the U.S. textile manufacturing industry is a loser of globalization and international trade, mostly due to the competition from overseas. This competition includes more manufacturers from other countries, but also the competition of pricing since other oversea manufacturers are able to sell their cotton/textile materials at a lower price. Since the U.S. struggles to compete with these lower prices, they are forced to look for another way to have a competitive advantage in the textile manufacturing sector, such as lean manufacturing and technology improvements. At Carolina Cotton Works, Bryan Ashby shares how they have increased efficiency and use high-quality machines (note: imported) for their products. Although this sounds great, this also means that there are fewer workers.

Comment #7: Globalization creates a trade dependence on imports. It’s important we don’t depend on things for when things happen that we can’t predict like the pandemic where we can’t import anymore. Since there was a lack of local textile manufacturing and sourcing in the United States compared to what was being imported, there was less of a chance for technological advances and improvement in the United States textile manufacturing sector. Post Globalization, however, may be the chance for the United States to bring back the textile manufacturing sector momentum. I think this because the United States has seen the result of heavily relying on other countries for their cheap labor/sources, and this could add extra motivation for companies to want to figure out better alternatives in manufacturing in their own country.

Comment #8: I think currently the US is a loser to globalization only because brands want to get the product for cheap. I think brands think that would create more profit that way. However, I do believe we could get to a future where more things would be created in the US and wouldn’t have to pay that much in tariffs and other external prices. I think it would help boost people to work more. I think people are worried about making things in our country because of the relations we have with other countries.

Discussion questions:

Do you agree or disagree with any particular argument above? Any follow-up comments on the impact of globalization on the US textile manufacturing sector? What should government do with trade given the debates? Please feel free to share any additional thoughts.

For FASH455 students: Please share your reflections on the video. For example, how does the video illustrate the global nature of the textile and apparel industry today? How can we understand the impact of globalization on the many stakeholders involved in the textile and apparel supply chains? Do the textile and apparel trade patterns described in the video support or challenge the trade theories we discussed in class? According to the video, what are the debates and controversies related to apparel sourcing and trade? What is your view and proposed solutions?

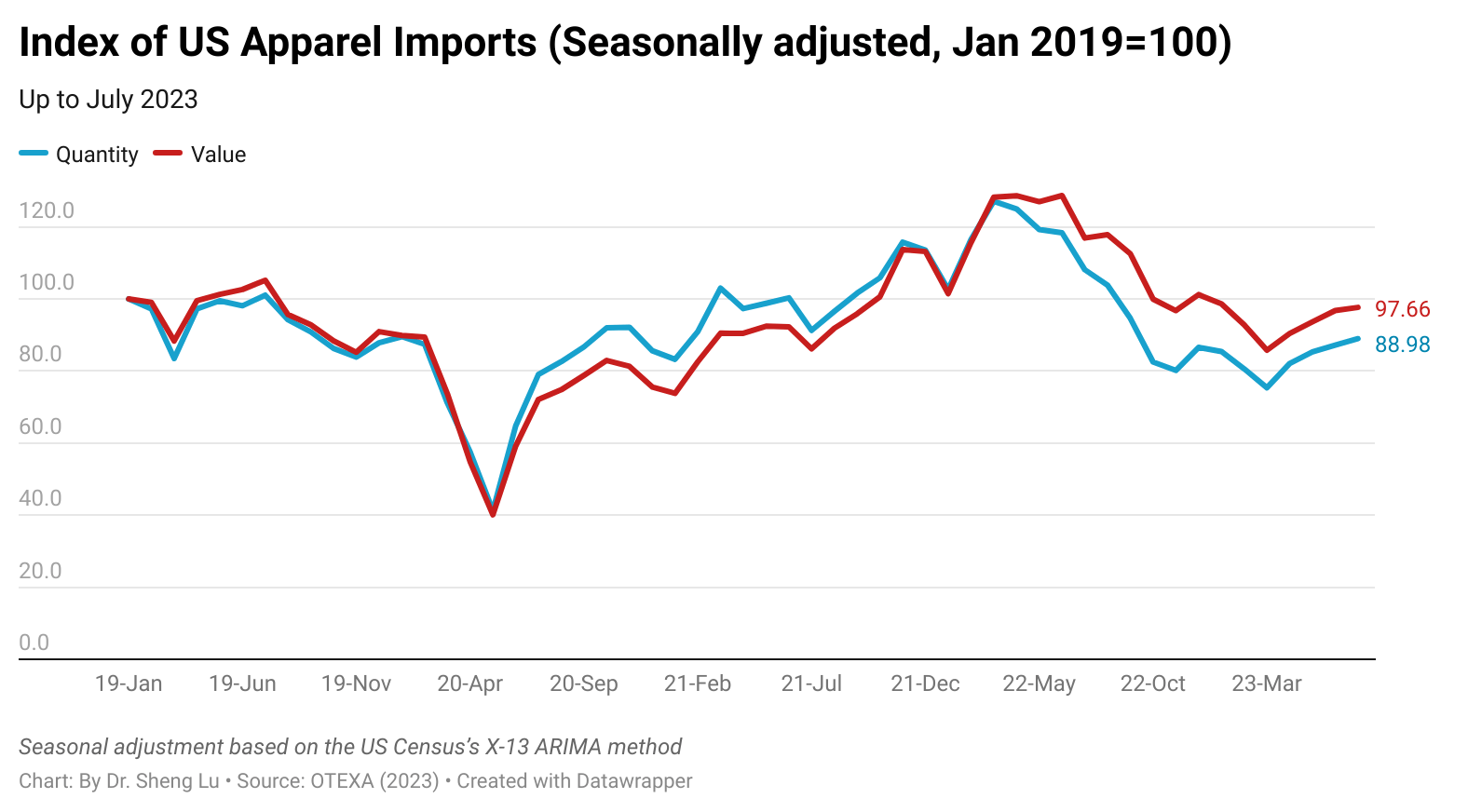

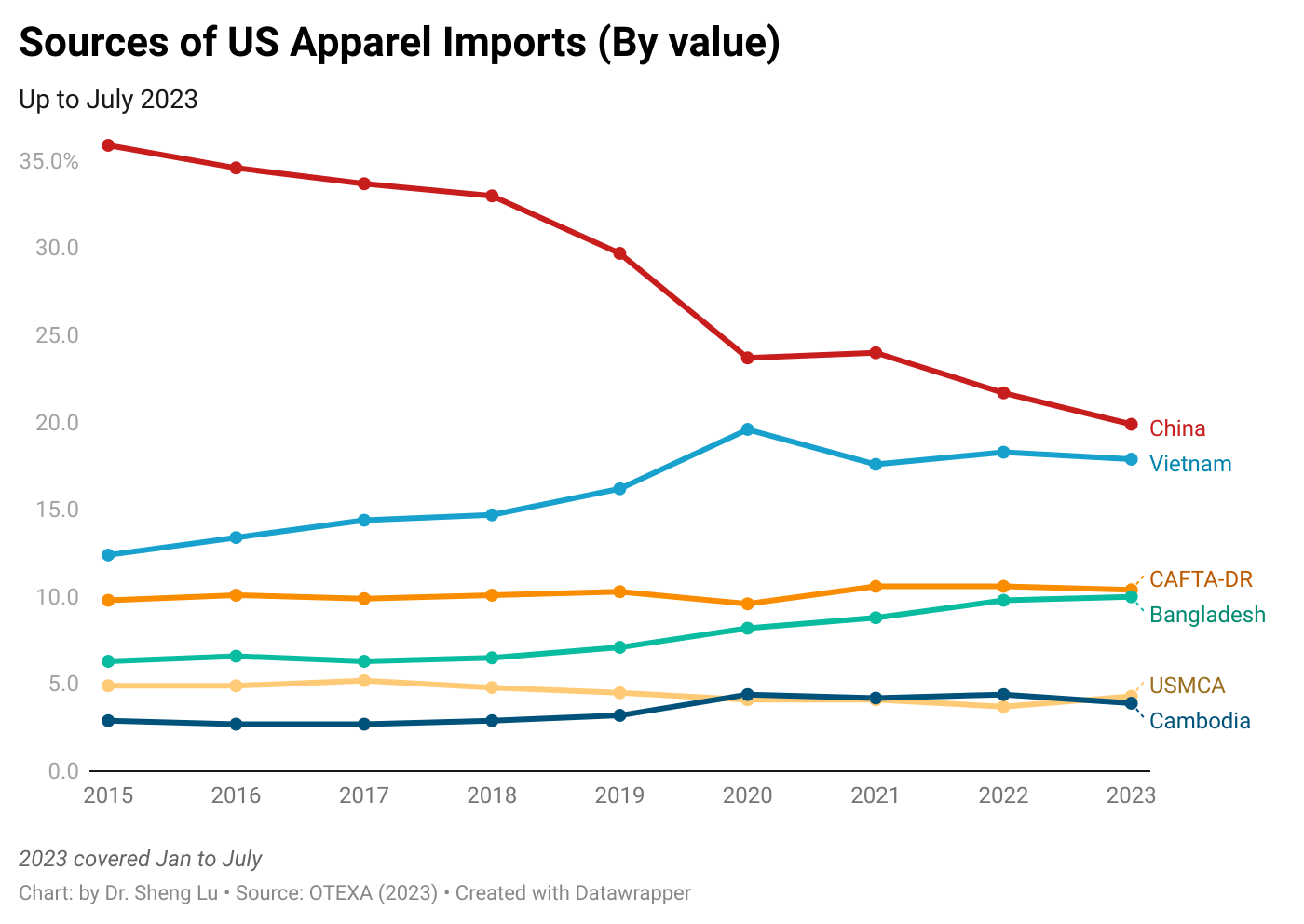

First, while US apparel imports gradually recovered, the import demand remained weak overall. For example, US apparel imports in July 2023 increased by 0.9% in value and 2% in quantity from June (seasonally adjusted). However, the trade volume still experienced a decrease of approximately 17-18% compared to the previous year. Meanwhile, the US consumer confidence index fell again in August 2023, suggesting the economic uncertainties are far from over. Notably, so far in 2023 (January to July), US apparel imports decreased by 22.3% in value and 28% in quantity from the previous year, the worst performance since the pandemic.

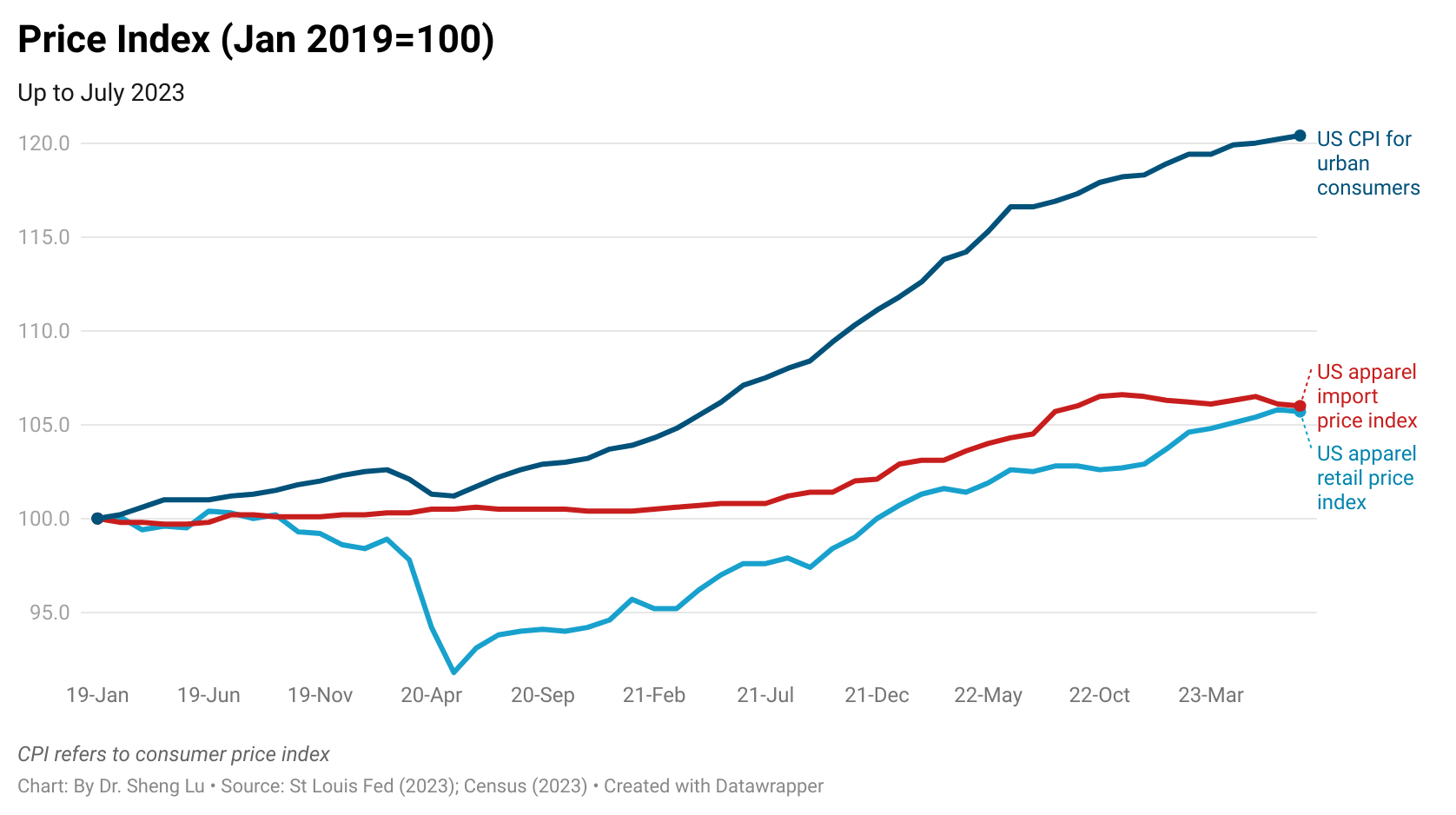

As a silver lining, the price of US apparel imports has stabilized, although inflation remains an issue for the US economy.

Secondly, because of the seasonal pattern, Asian countries were able to capture relatively higher market shares since June. For example, measured in value, China, ASEAN, and Bangladesh accounted for over 64% of total US apparel imports in July 2023, a notable increase from 61% in June and 58% in May 2023.

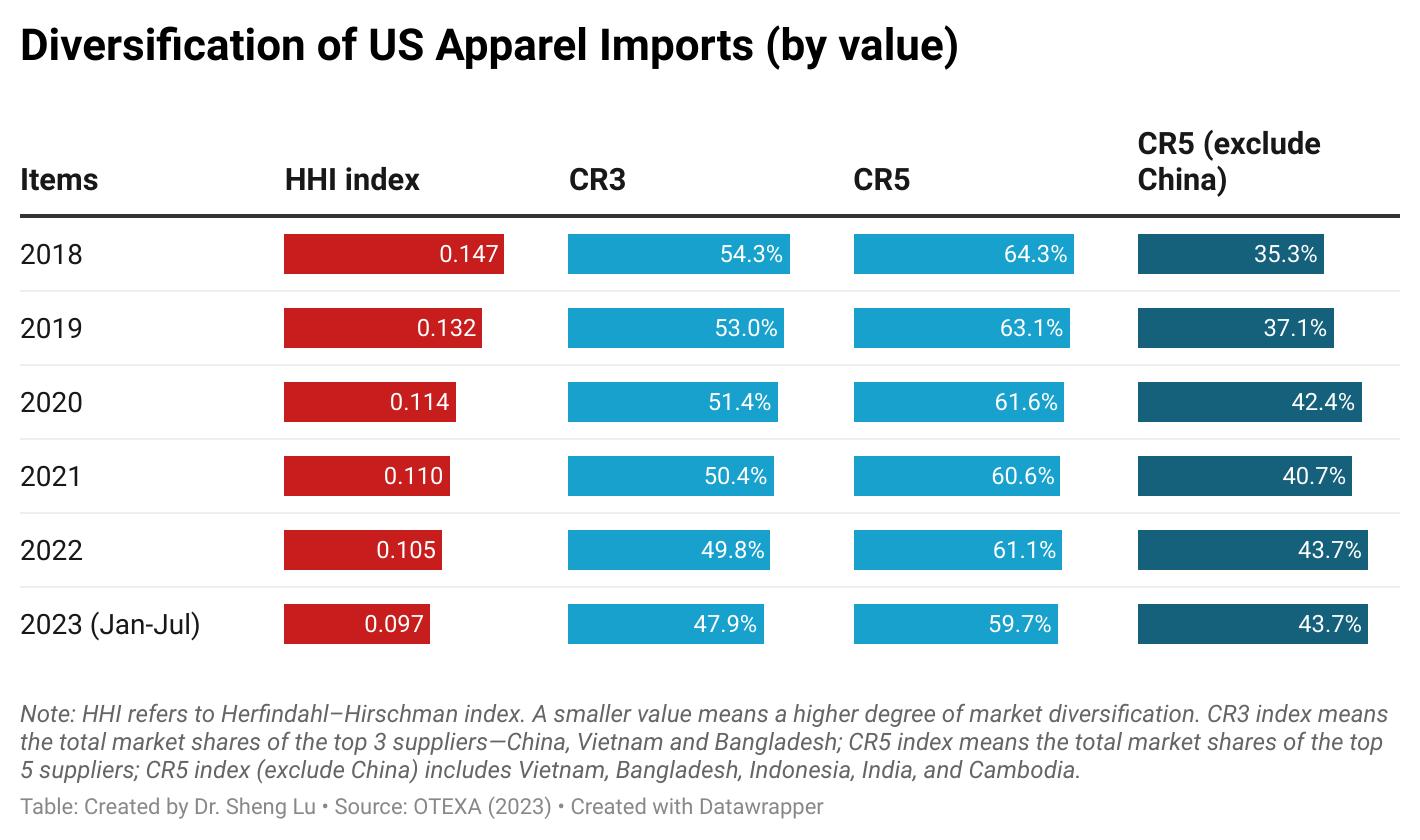

Nevertheless, US fashion companies continue diversifying their sourcing base to mitigate various supply chain risks and rising geopolitical tensions. For example, the HHI Index for US apparel imports dropped to 0.097 in the first seven months of 2023, which is lower than the 0.106 recorded in the same period the previous year (January to July 2022), indicating a greater diversity in the sources of imports.

Third, despite an apparent rebound in exports to the US, China continued to experience a further decline in its market share. For instance, in July 2023, China’s market share was more than 3 percentage points lower in value (27.2% in July 2022 vs. 24.1% in July 2023) and 2.5 percentage points lower in quantity (43.1% in July 2022 vs. 40.6% in July 2023). This marked the worst performance since April 2023. In other words, consistent with recent industry surveys, US fashion companies continue to reduce their China exposure given the adverse business environment.

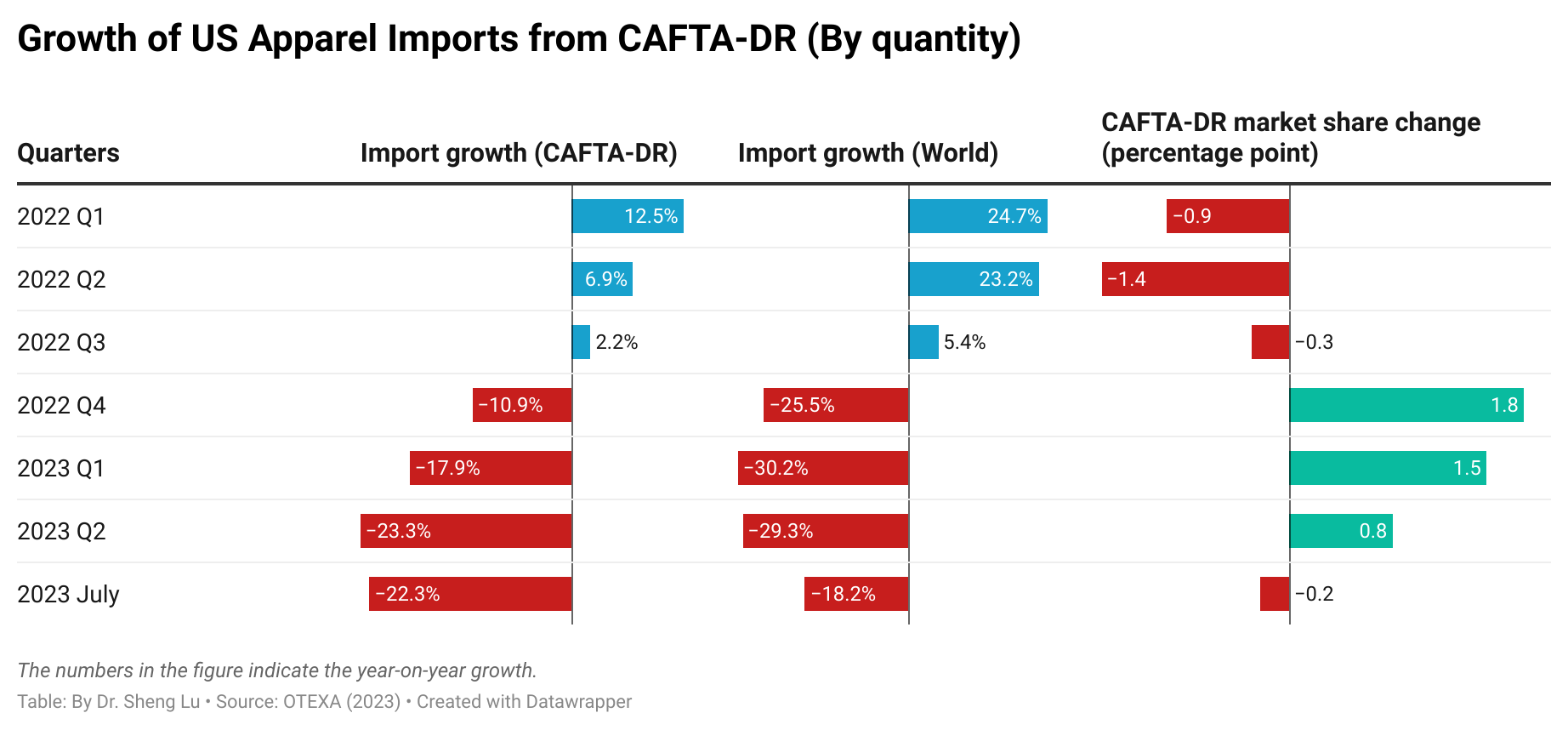

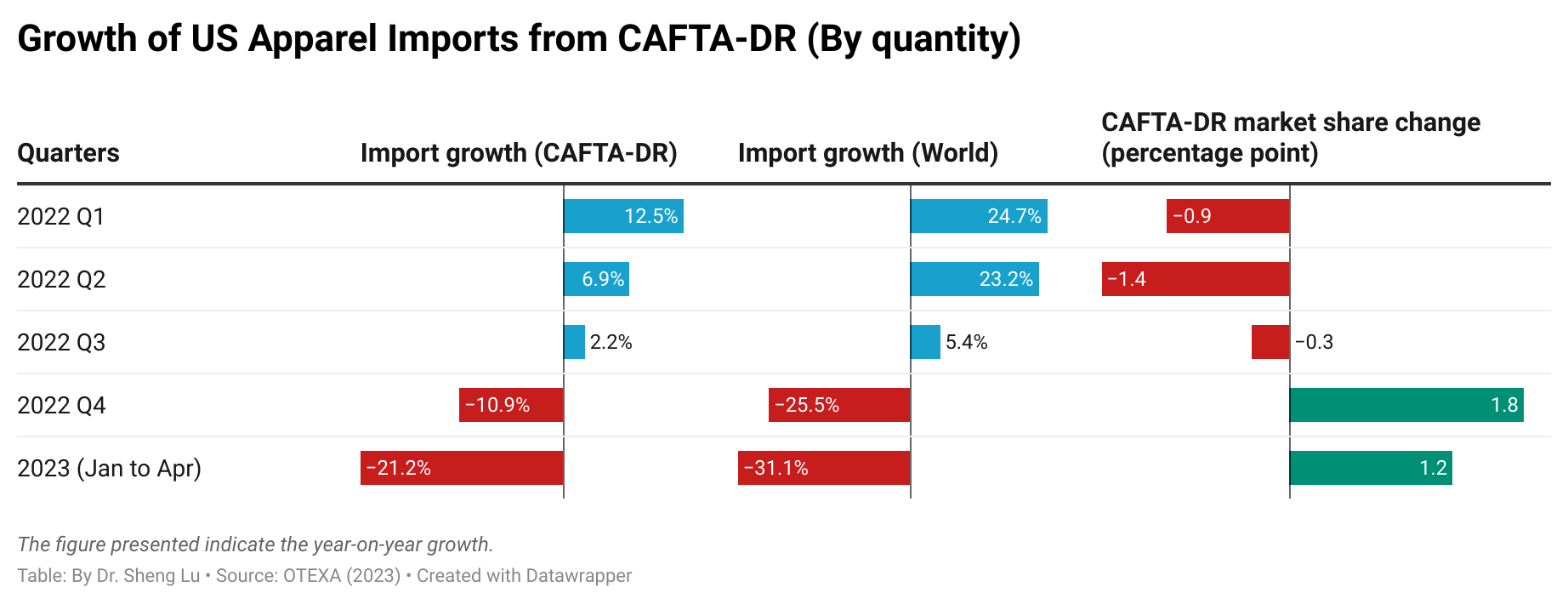

Fourth, the latest data suggests that US apparel imports from CAFTA-DR members remain stagnant, and some critical problems, such as the underutilization of the agreement, even worsened. For example, about 9.5% of US apparel imports in value and 8.5% in quantity came from CAFTA-DR members in July 2023, lower than 10.2% and 9.0% in the previous year (i.e., July 2022). In absolute terms, US apparel imports from CAFTA-DR in 2023 were about 20% lower than in 2022.

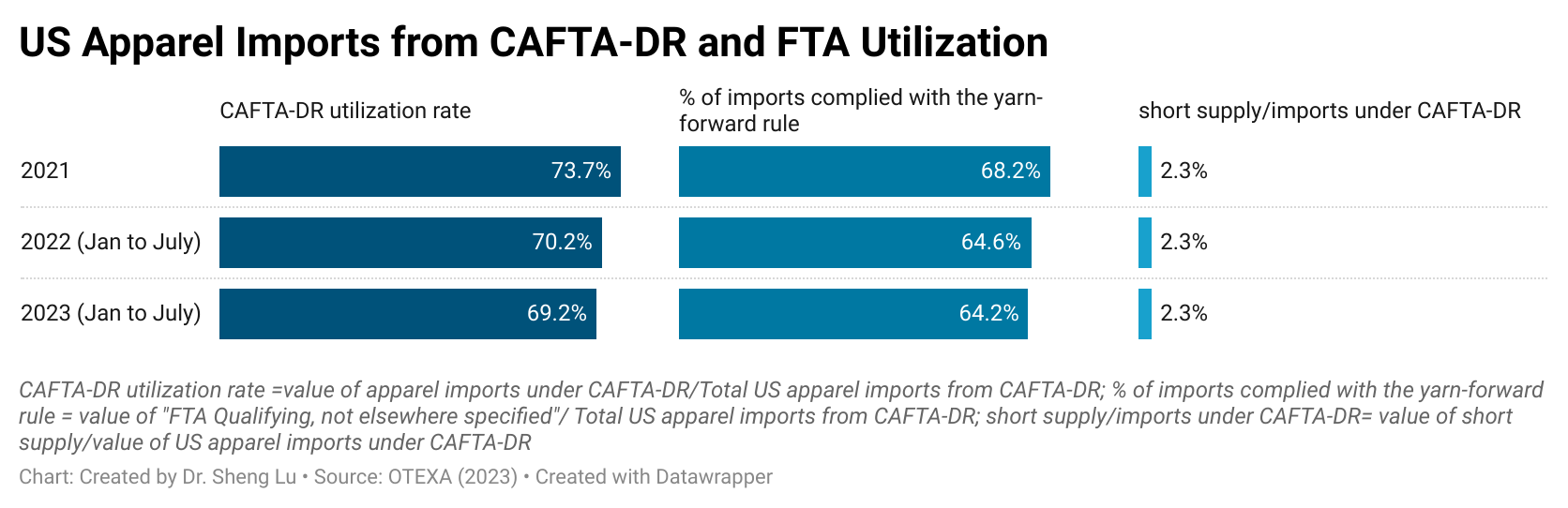

Additionally, CAFTA-DR’s utilization rate (i.e., the value of imports claiming the duty-free benefits under CAFTA-DR divided by the total value of imports from CAFTA-DR) fell from 70.2% in 2022 (Jan to July) to a new low of 69.2% in 2023 (Jan to July). Likewise, the value of imports utilizing CAFTA-DR’s short supply decreased by more than 20%. Thus, how to leverage CAFTA-DR to meaningfully encourage more US apparel imports from the region, particularly in light of US fashion companies’ eagerness to reduce their exposure to China, calls for sustained efforts and probably new strategies.

According to Primark, it does not own any factories but sources all apparel products from contracted factories. Any contracted factory that manufactures products for Primark must meet internationally recognized standards before receiving the first sourcing order.

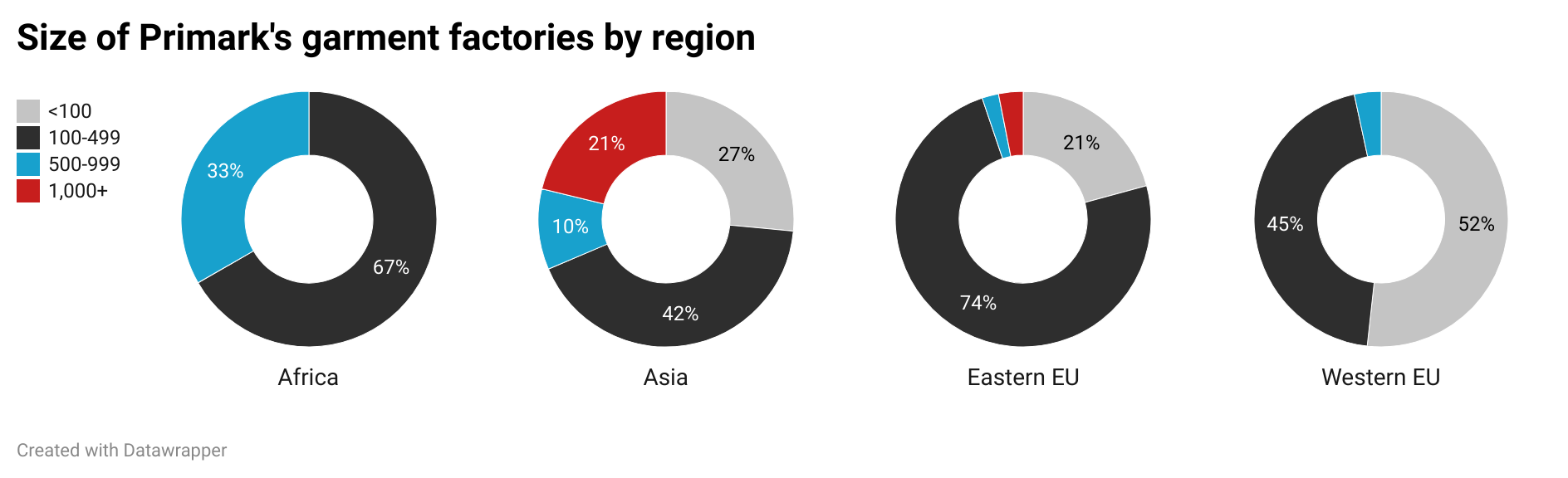

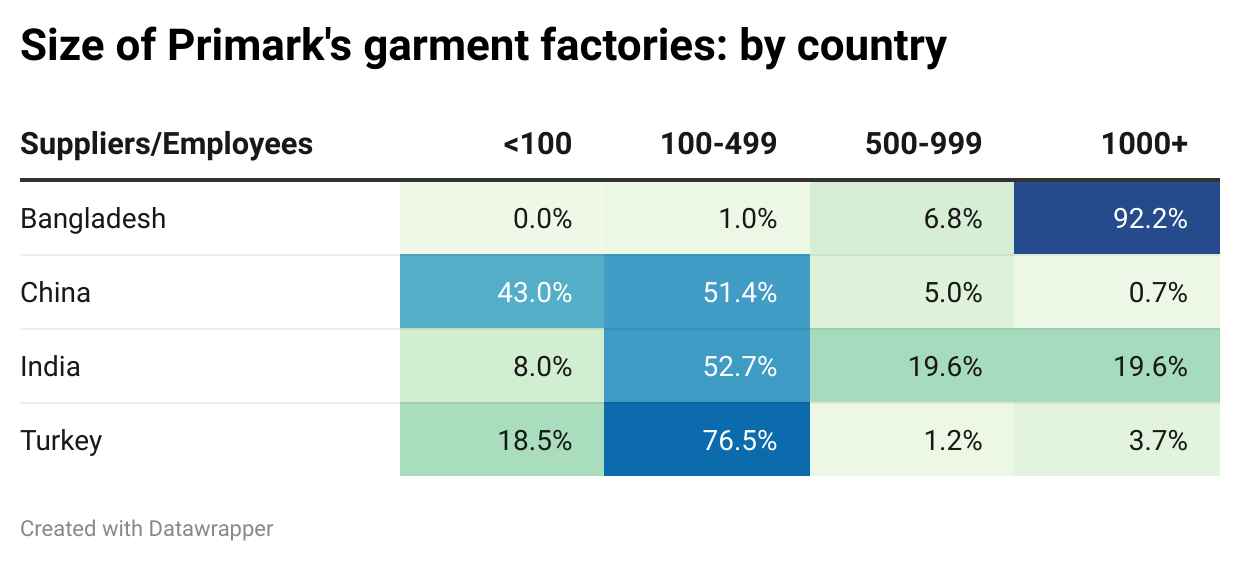

As of October 2022, Primark sourced from 883 contracted factories in 26 countries (note: it was a slight decline from 928 contracted factories in 28 countries as of May 2021). Of these factories, 85.5 percent were Asia-based because of the region’s massive production capacity and a balanced offer of various sourcing factors, from cost, speed to market, and flexibility to compliance risks.

Like many other EU-based fashion companies, near-shoring from within the EU was another critical feature of Primark’s sourcing strategies. About 14 percent of Primark’s contracted garment factories were EU-based (including Turkey).

Measured by the number of workers, Primark’s Asian factories were larger than their counterparts in other parts of the world. For example, while Primark’s factories in Pakistan and Bangladesh typically have more than 2,500+ workers, its factories in Western EU countries like the UK, Germany, Italy, and France, on average, only have 64-200 workers. This pattern suggests that Primark mainly uses Asian factories to fulfill volume sourcing orders, and its EU factories mainly produce replenishment or more time-sensitive fashionable items.

Meanwhile, similar to the case of other retailers like PVH, Primark’s contracted garment factories in China were smaller than their peers in the rest of Asia. For instance, while over 90% of Primark’s garment factories in Bangladesh employ more than 1,000 workers, around 43% of their contracted factories in China have fewer than 100 workers. This pattern suggests Primark could use China as an apparel sourcing base primarily for orders requiring greater flexibility and agility and those involving a wider variety of products but in smaller quantities.

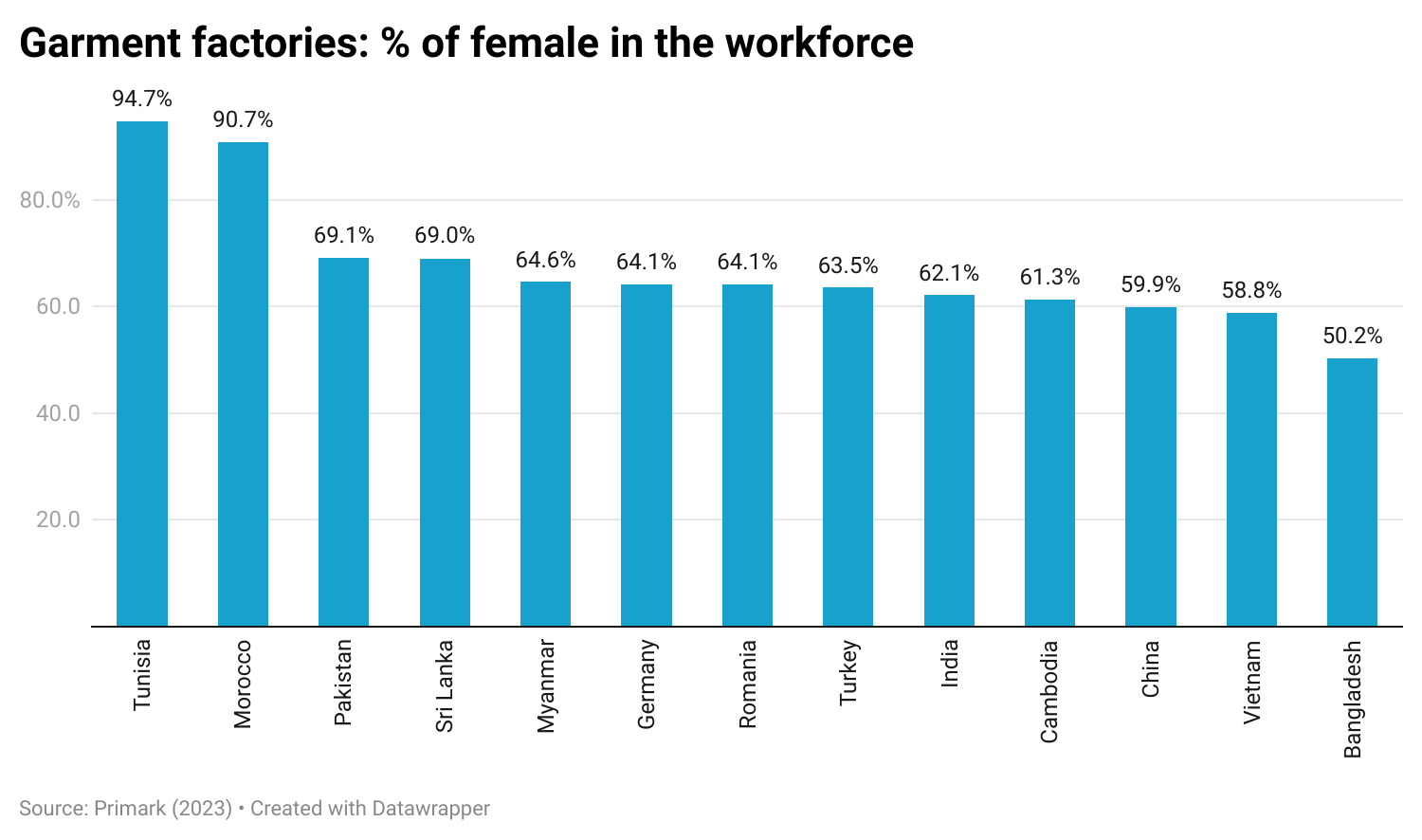

Further, reflecting the unique role of the garment industry in creating economic opportunities for women, females account for more than half of the workforce in most garment factories that make apparel for Primark. The percentage was exceptionally high in developing countries like Tunisia (94%), Morocco (91%), Pakistan (69%), Sri Lanka (69%), Myanmar (64%), India (62%), and Vietnam (59%).

According to Primark (as of September 2023), its Ethical Trade and Environmental Sustainability team comprises over 120 specialists based in key sourcing countries. The team conducts around 3,000 supplier audits a year to monitor compliance (i.e., fair pay, safety, and healthy working conditions.) Additionally, Primark says its factories were in line with the company’s environmental code of conduct, and the company “donated any unsold merchandise to the Newlife Foundation in Europe and KIDS/Fashion Delivers in the US.

by Sheng Lu

Discussion questions:

What are the unique aspects of Primark’s apparel sourcing strategies? What role does sourcing play in supporting Primark’s business success? Any questions or suggestions for Primark regarding its sourcing practices?

Discussion questions: What factors contribute to the complexity of eliminating banned Xinjiang cotton from the apparel supply chain? How can the current efforts be enhanced to better address the situation and by whom? Feel free to share any other reflections on the video and the graphs.

#1 What are the examples of globalization in the above two videos about Temu?

#2 Based on the videos, who are the winners and losers of globalization and why?

#3 What role does international trade play in Temu’s business model?

#4 Some suggest ending the “de minimis rule.” Based on the videos, what is your view and recommendation for US policymakers?

#5 Anything you find interesting/surprising/intriguing in the video and why?

(Note: Anyone is welcome to join the discussion. For students in FASH455, please address at least two questions. Please mention the question number in your response, but there is no need to repeat the question).

Note: About “de minimis rule.”: Under US customs law, specifically the Trade Facilitation and Trade Enforcement Act of 2015, import duties are generally waived for goods valued at $800 or less per person per day. Therefore, Temu’s shipping from China to US consumers is likely to be eligible for the benefits.

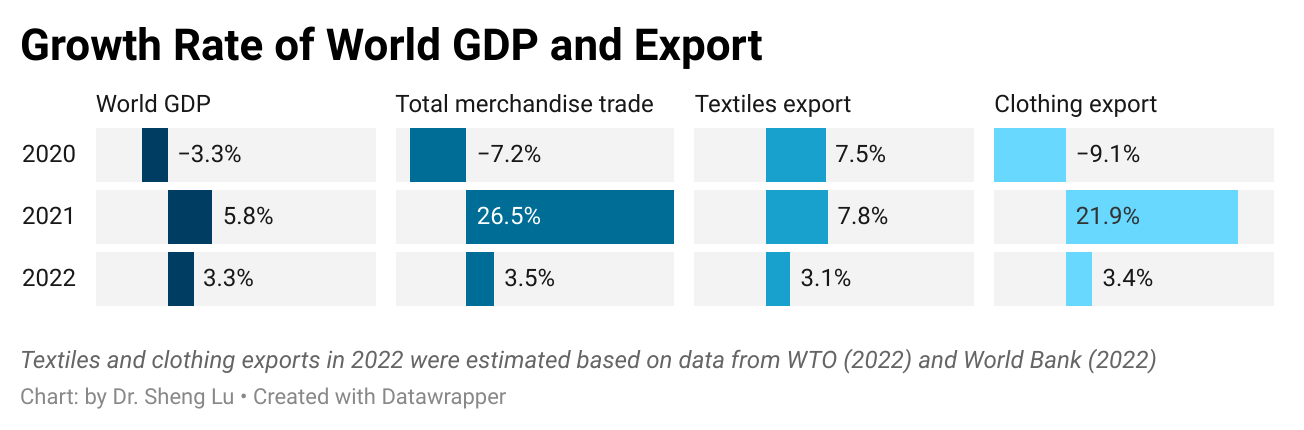

This article comprehensively reviewed the world textiles and clothing trade patterns in 2022 based on the newly released World Trade Organization Statistical Review 2023 and data from the United Nations (UNComtrade). Affected by the slowing world economy and fashion companies’ evolving sourcing strategies in response to the rising geopolitical tensions, mainly linked to China, the world’s textiles and clothing trade in 2022 displayed several notable patterns different from the past.

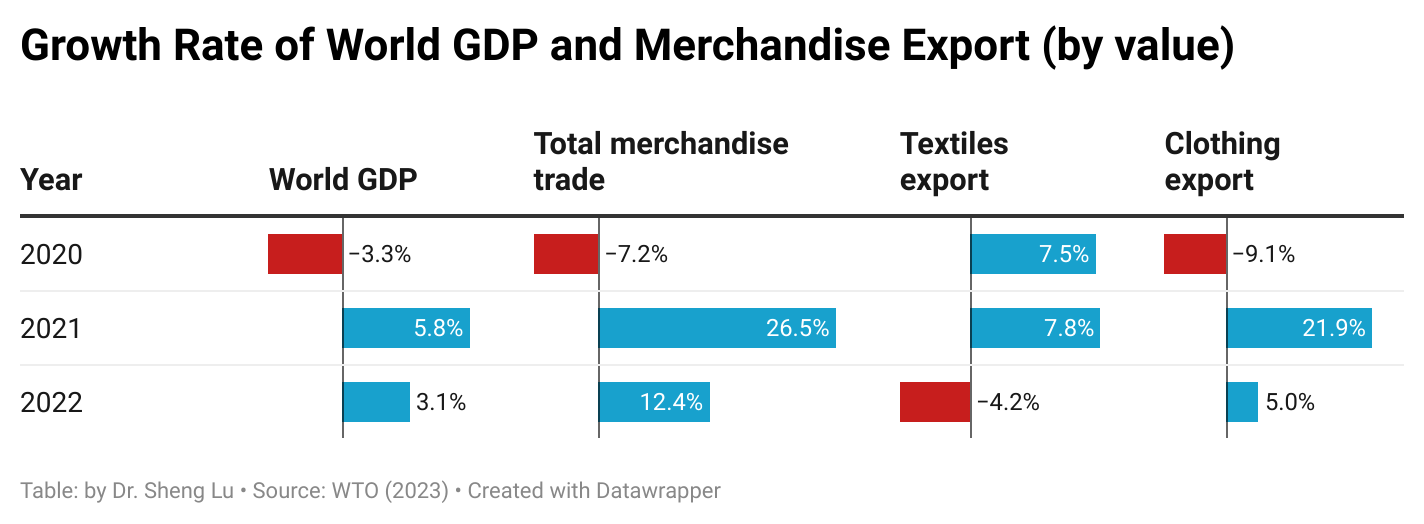

Pattern #1: The expansion of world clothing exports witnessed a notable deceleration in 2022, primarily attributed to the economic downturn. Meanwhile, the world’s textile exports decreased from the previous year, affected by the reduced demand for textile raw materials used to produce personal protective equipment (PPE) as the pandemic waned.

The world’sclothing exports totaled $576 billion in 2022, up 5 percent year over year, much slower than the remarkable 20 percent growth in 2021. The slowed economic growth plus the unprecedented high inflation in major apparel import markets, particularly the United States and Western European countries, adversely affected consumers’ available budget for discretionary expenditures, including clothing purchases.

The world’s textile exports fell by 4.2 percent in 2022, totaling $339 billion, lagging behind most industrial sectors. Such a pattern was understandable as the demand for PPE and related textile raw materials substantially decreased with the pandemic nearing its end.

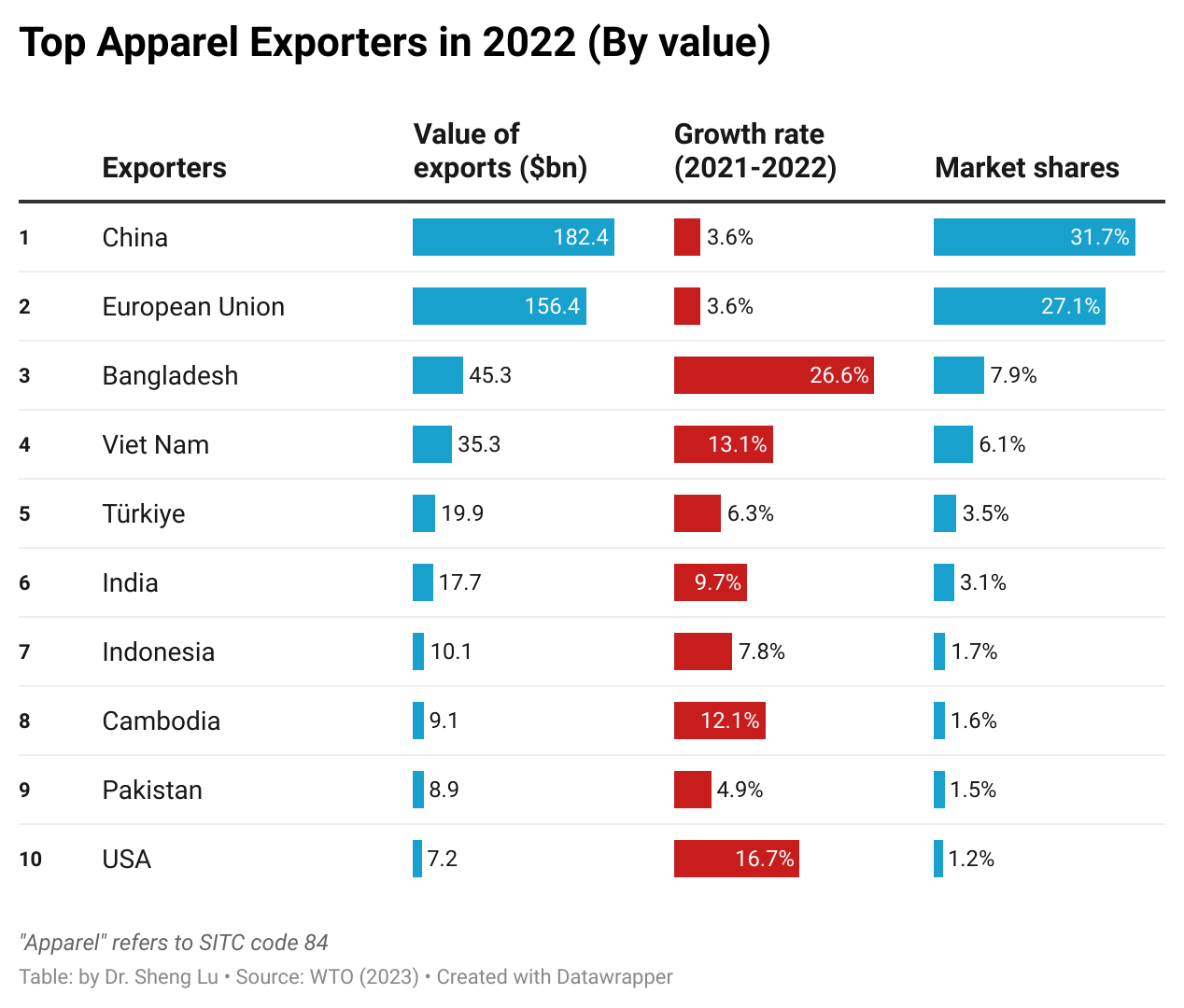

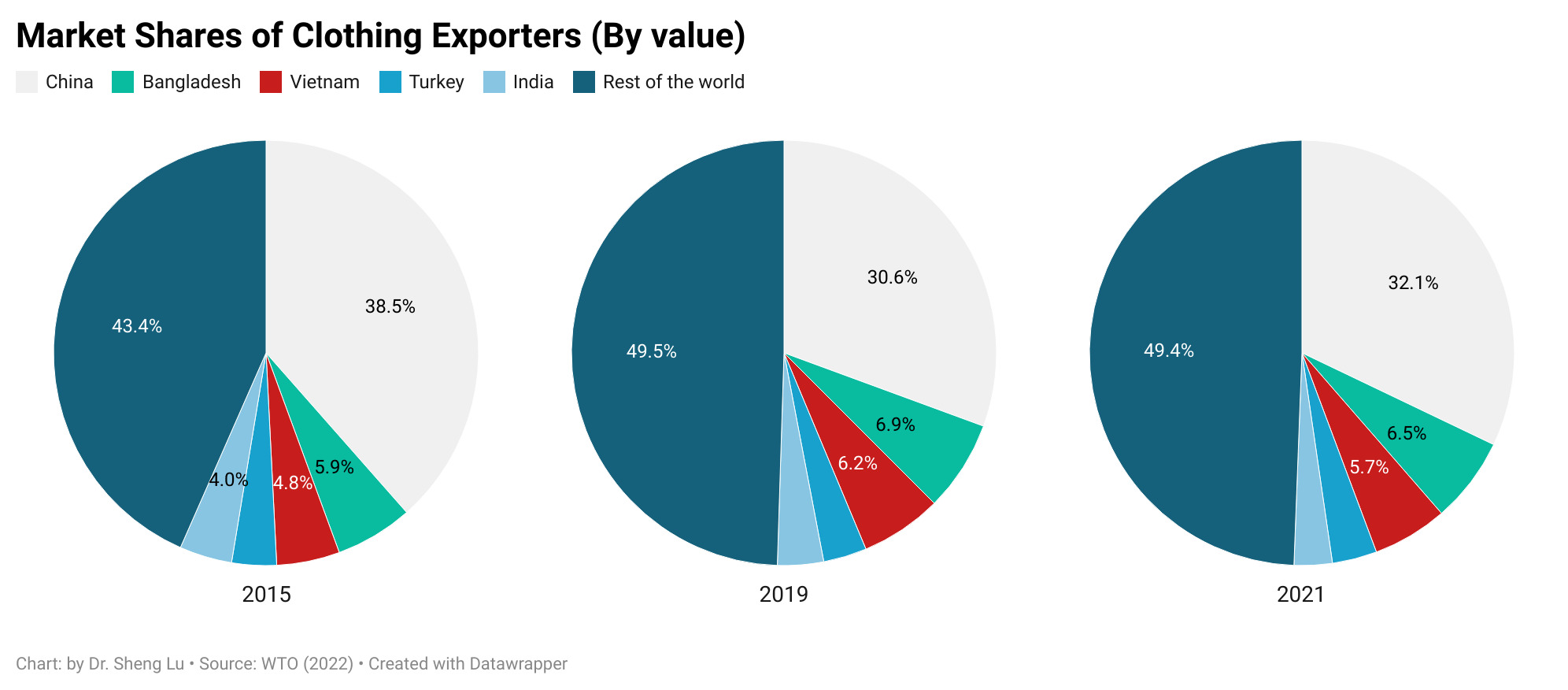

Pattern #2: China continued to lose market share in clothing exports, which benefited other leading apparel exporters in Asia. Notably, for the first time, Bangladesh surpassed Vietnam and ranked as the world’s second-largest apparel exporter in 2022.

In value, China remained the world’s largest apparel exporter in 2022. However, China’s clothing exports experienced a growth of 3.6 percent, below the global average of 5.0 percent, positioning China at the bottom of the top ten exporters.

China’s global market share in clothing exports dropped to 31.7 percent in 2022, marking its lowest point since the pandemic and a significant decrease from the approximate 38 percent recorded from 2015 to 2018. In fact, China lost market share in almost all major clothing import markets, including the US, the EU, Canada, and Japan. The concerns about the risks of forced labor linked to sourcing from China and the deteriorating US-China relations were among the primary factors driving fashion companies’ eagerness to reduce their ‘China exposure” further.

China has been diversifying its clothing exports beyond the traditional Western markets in response to the challenging business environment. For example, from 2021 to 2022, Asian countries, especially members of the Regional Comprehensive Economic Partnership (RCEP), became relatively more important clothing export markets for China. Nevertheless, since RCEP members primarily consist of developing economies with ambitions to enhance their own clothing production, the long-term growth prospects for their import demand of ‘Made in China’ clothing remain uncertain.

Bangladesh achieved a new record high in its market share of world clothing exports, reaching 7.9 percent in 2022, which exceeded Vietnam’s 6.1 percent. Many fashion companies regard Bangladesh as a promising clothing-sourcing destination with growth potential because of its capability to make cotton garments as China’s alternatives, competitive price, and reduced social compliance risks.

Fashion companies’ efforts to “de-risking from China” also resulted in the robust growth of clothing exports from other large-scale Asian clothing producers in 2022, including Vietnam (up 13 percent), Cambodia (up 12 percent), and India (up 10 percent). In other words, despite the concerns about China, fashion companies still treat Asia as their primary sourcing destination.

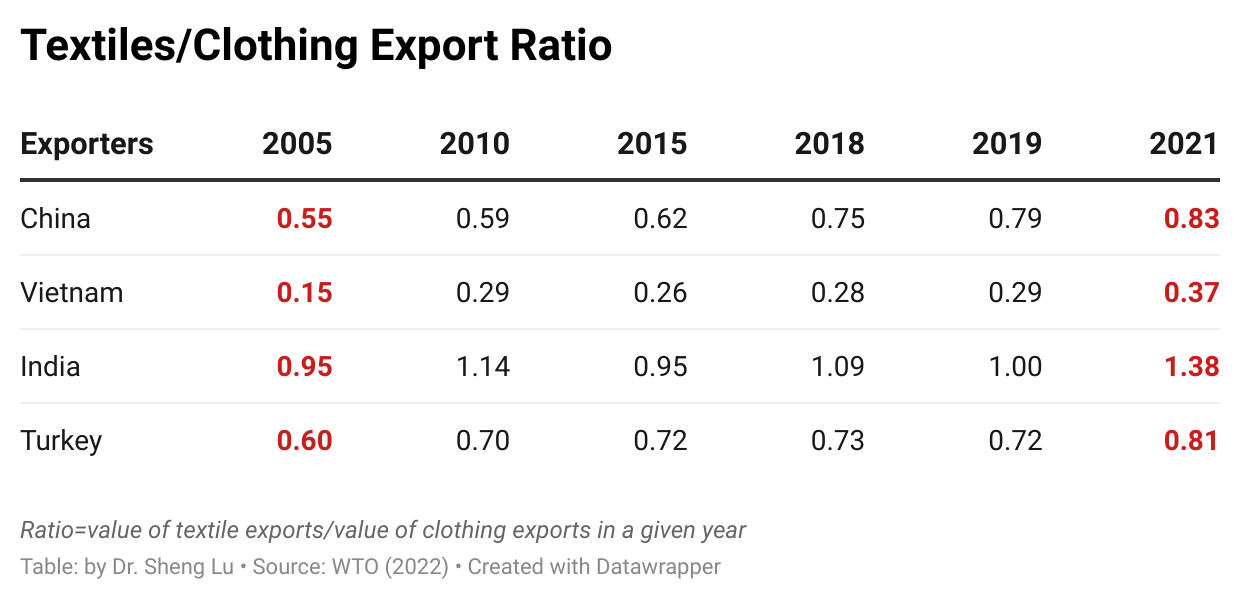

Pattern #3: Developed countries stay critical textile exporters, and middle-income developing countries gradually build new textile production and export capability.

The European Union members and the United States stayed critical textile exporters, accounting for 25.1 percent of the world’s textile exports in 2022, up from 24.5 percent in 2021 and 23.2 percent in 2020. Thanks to the increasing demand from apparel producers in the Western Hemisphere, U.S. textile exports increased by 5 percent in 2022, the highest among the world’s top ten.

As a persistent long-term trend, middle-income developing countries have consistently been strengthening their textile production and export capability. For example, China, Vietnam, Turkey, and India’s market shares in the world’s textile exports have steadily risen. They collectively accounted for 56.8 percent of the world’s clothing exports in 2022, a notable increase from only 40 percent in 2010. Also, over time, these middle-income developing countries have achieved a more balanced textiles-to-clothing export ratio.

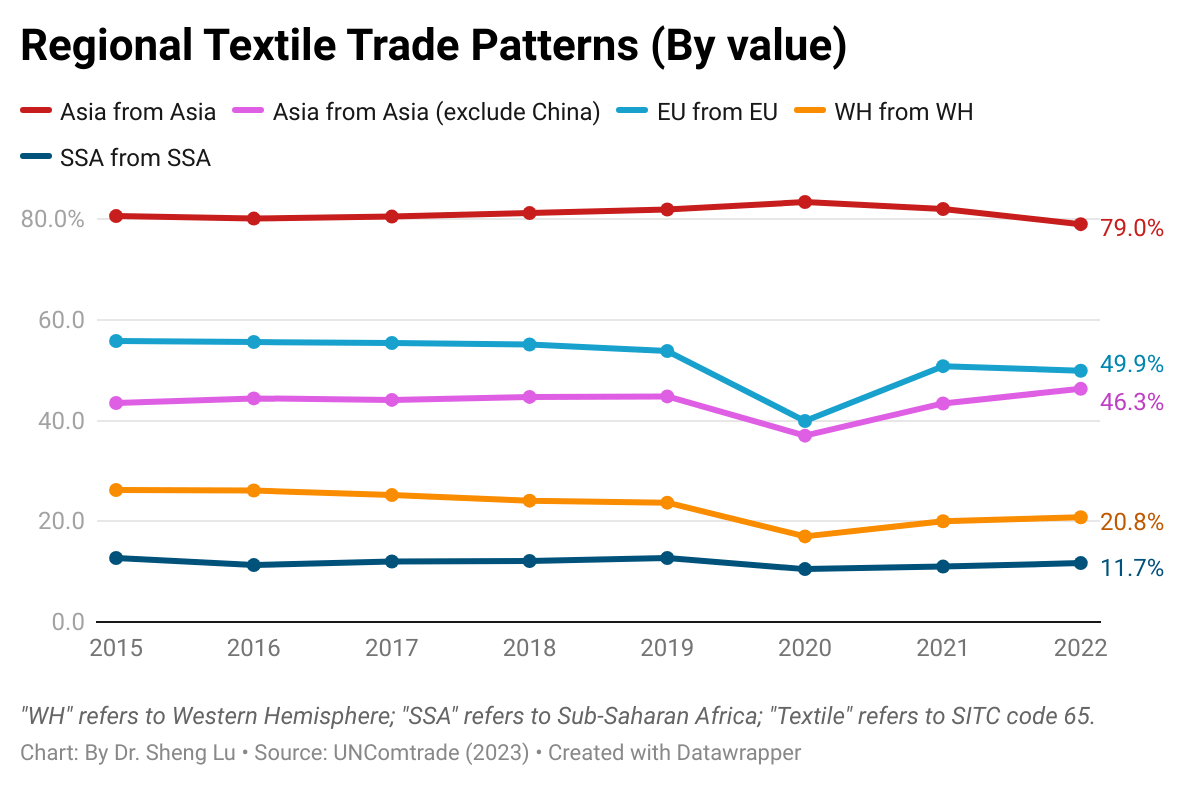

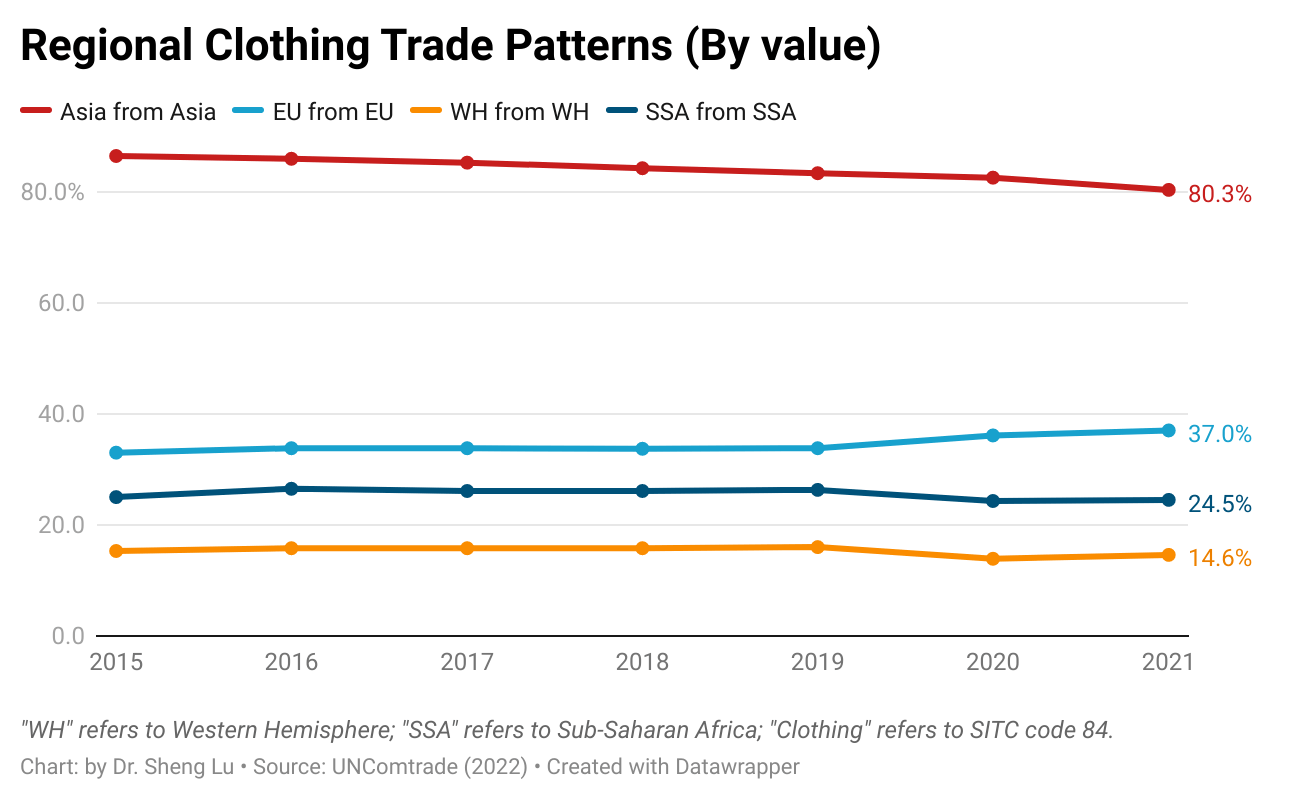

Pattern #4: Regional textile and apparel trade patterns strengthened further with the growing popularity of near-shoring, particularly in the Western Hemisphere. However, an early indication has emerged that Asian countries are diversifying their sources of textile raw materials away from China to mitigate growing risks.

The regional textile and apparel supply chains were in good shape in Asia and Europe. For example, nearly 80 percent of Asian countries’ textile input and apparel imports came from within the region in 2022. Likewise, approximately half of EU countries’ textile imports were intra-region trade in 2022, and one-third were for apparel.

The Western Hemisphere (WH) textile and apparel supply chain became more integrated in 2022 thanks to the booming near-shoring trends. For example, 20.8 percent of WH countries’ textile imports came from within the region in 2022, up from 20.1 percent in the previous year. Likewise, about 15.1 percent of WH countries’ apparel imports came from within the region in 2022, higher than 14.7 percent in 2021 and 13.9 percent in 2022.

Compared with Asia and the EU, SSA clothing producers used much fewer locally-made textiles (i.e., stagnant at around 11% from 2011 to 2022), reflecting the region’s lack of textile manufacturing capability. A more comprehensive examination of strategies for bolstering the textile manufacturing sector in Sub-Saharan Africa, particularly in light of the recently enacted African Continental Free Trade Area (AfCFTA) agreement, might be warranted.

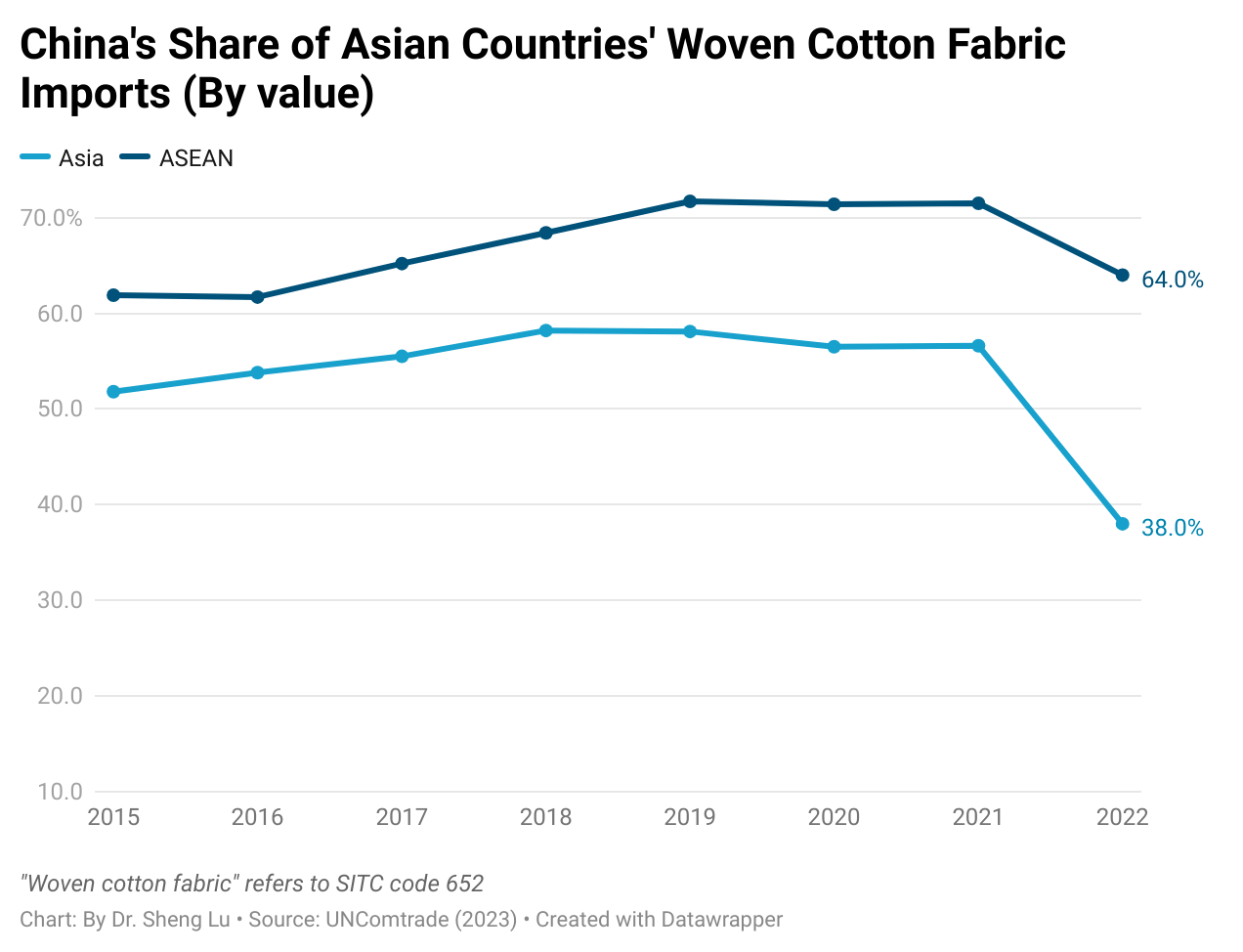

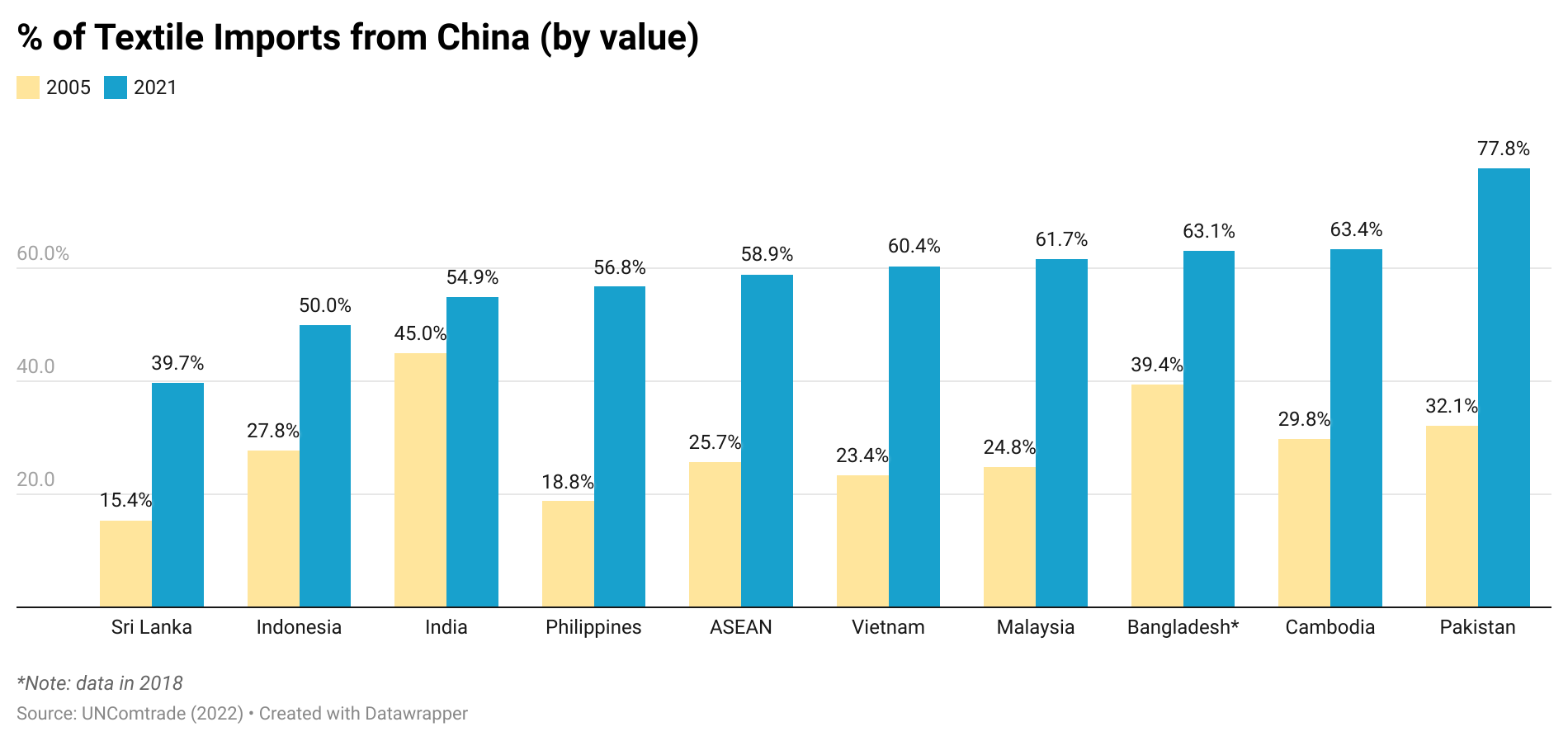

Additionally, data suggests that Asian countries began diversifying their textile imports away from China to mitigate supply chain risks. For example, with the official implementation of anti-forced labor legislation in the US and other primary apparel import markets directly targeting cotton made in China’s Xinjiang region, Asian countries significantly reduced their cotton fabric imports (SITC code 652) from China in 2022. Instead, Asian countries other than China accounted for 46.3 percent of the region’s textile supply in 2022, up from around 42-43 percent between 2019 and 2021.

It is critical to watch how willing, to what extent, and how quickly Asian countries can effectively reduce their dependency on textile supplies from China. The result is also an important reminder that Western fashion companies’ de-risking from China could exert significant and broad impacts across the entire supply chain beyond finished goods.

#1U.S. fashion companies are deeply concerned about the deteriorating U.S.-China bilateral relationship and plan to accelerate “reducing China exposure” to mitigate the risks.

Respondents identified “Finding a new sourcing base other than China” as a more prominent challenge in 2023 than the previous year (i.e., 4th in 2023 vs. 11th in 2022).

This year, over 40 percent of respondents reported sourcing less than 10 percent of their apparel products from China, up from 30 percent of respondents a year ago and a notable surge from only 20 percent in 2019. Similarly, a new record high of 61 percent of respondents no longer use China as their top supplier in 2023, up from 50 percent of respondents in 2022 and much higher than only 25-30 percent before the pandemic.

Nearly 80 percentof respondents plan to reduce apparel sourcing from China over the next two years, with a record high of 15 percent planning to “strongly decrease” sourcing from the country. This strong sentiment was not present in past studies. Notably, large-size U.S. fashion companies (with 1,000+ employees) that currently source more than 10 percent of their apparel products from China are among the most eager to de-risk.

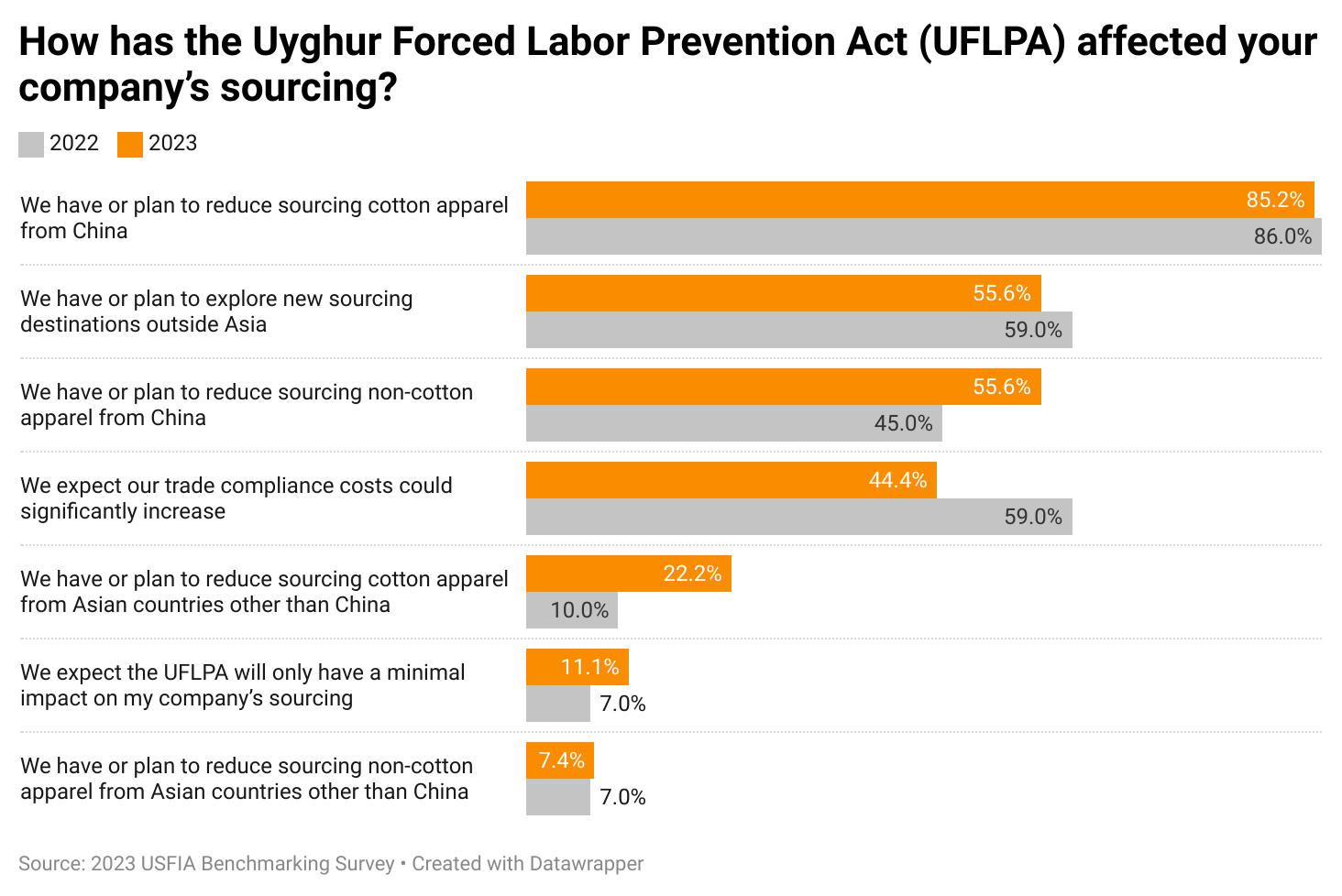

#2 Tackling forced labor risks in the supply chain remains a significant challenge confronting U.S. fashion companies in 2023.

“Managing the forced labor risks in the supply chain” ranks as the 2nd top business challenge in 2023, with 64 percent of respondents rating the issue as one of their top five concerns.

Most surveyed U.S. fashion companies have taken a comprehensive approach to mitigating forced labor risks in the supply chain. Three practices, including “asking vendors to provide more detailed social compliance information,” “attending workshops and other educational events to understand related regulations better,” and “intentionally reducing sourcing from high-risk countries,” are the most commonly adopted by respondents (over 80 percent) in response to forced labor risks and the UFLPA’s implementation.

Since January 1, 2023, U.S. Customs and Border Protection (CBP)’s UFLPA enforcement has affected respondents’ importation of “Cotton apparel products from China,” “Cotton apparel products from Asian countries other than China,” and “Home textiles from China.”

U.S. fashion companies are actively seeking to diversify their sourcing beyond Asia to mitigate the forced labor risks, particularly regarding cotton products.

#3 There is robust excitement about increasing apparel sourcing from members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR).

CAFTA-DR members play a more significant role as an apparel sourcing base this year. Over 80 percent of respondents report sourcing from CAFTA-DR members in 2023, a notable increase from 60 percent in the past few years. Also, nearly 30 percent of respondents placed more than 10 percent of their sourcing orders with CAFTA-DR members this year, a substantial increase from only 19 percent of respondents in 2022 and 10 percent in 2021.

About 40 percent of respondents plan to increase apparel sourcing from CAFTA-DR members over the next two years. Most respondents consider expanding sourcing from CAFTA-DR as part of their overall sourcing diversification strategy.

With U.S. fashion companies actively seeking immediate alternatives to sourcing from China and Asia, respondents emphasize theincreased urgencyof improving textile raw material access to promote further U.S. apparel sourcing from CAFTA-DR members. “Allowing more flexibility in sourcing fabrics and yarns from outside CAFTA-DR” was regarded as the top improvement needed.

#4 US fashion companies demonstrate a solid dedication to expanding their sourcing of clothing made from recycled or other sustainable textile fibers:

Nearly 60 percent of respondents say at least 10 percent of their sourced apparel products already use recycled or other sustainable textile fibers. Another 60 percent of surveyed companies plan to “substantially increase sourcing apparel made from sustainable or recycled textile materials over the next five years.”

Addressing the higher sourcing costs and the low-profit margins are regarded as the top challenge for sourcing clothing using recycled or other sustainable fiber.

About 60 percent of respondents also call for policy support for sourcing clothing using recycled or other sustainable textile materials, such as preferential tariff rates and guidance on sustainability and recycling standards.

#5 Respondents strongly support and emphasize the importance of the early renewal of the African Growth and Opportunity Act (AGOA) and extending the program for at least another ten years.

Respondents sourcing from AGOA members are typically large-scale U.S. fashion brands or retailers (with 1,000+ employees). Generally, these companies treat AGOA as part of their extensive global sourcing network and typically source less than 10 percent of the total sourcing value or volume from the region.

About 40 percent of respondents view AGOA as “essential for my company to source from AGOA members.”

About 60 percent of respondents say the temporary nature of AGOA “has discouraged them from making long-term investments and sourcing commitments in the region.” Many respondents expect to cut sourcing from AGOA members should the agreement is not renewed by June 2024.

About one-third of respondents currently sourcing from AGOA explicitly indicate, “Ethiopia’s loss of AGOA eligibility negatively affects my company’s interest in sourcing from the entire AGOA region.” In comparison, only about 17 percent of respondents say they “have moved sourcing orders from Ethiopia to other AGOA members.

Other topics covered by the report include:

5-year outlook for the U.S. fashion industry, including companies’ hiring plan by key positions

The competitiveness of major apparel sourcing destinations in 2023 regarding sourcing cost, speed to market, flexibility & agility, and compliance risks (assessed by respondents)

Respondents’ qualitative comments on the prospect of sourcing from China and “re-risk”

U.S. fashion companies’ latest social responsibility and sustainability practices related to sourcing

U.S. fashion companies’ trade policy priorities in 2023

Background

This year’s benchmarking study was based on a survey of executives from 30 leading U.S. fashion companies from April to June 2023. The study incorporated a balanced mix of respondents representing various businesses in the U.S. fashion industry. Approximately 73 percent of respondents were self-identified retailers, 60 percent self-identified brands, and 65 percent self-identified importers/wholesalers.

The respondents to the survey included both large U.S. fashion corporations and medium to small companies. Around 77 percent of respondents reported having more than 1,000 employees. And the rest (23 percent) represented medium to small-sized companies with 100-999 employees.

The latest OTEXA trade data suggests several US apparel import patterns:

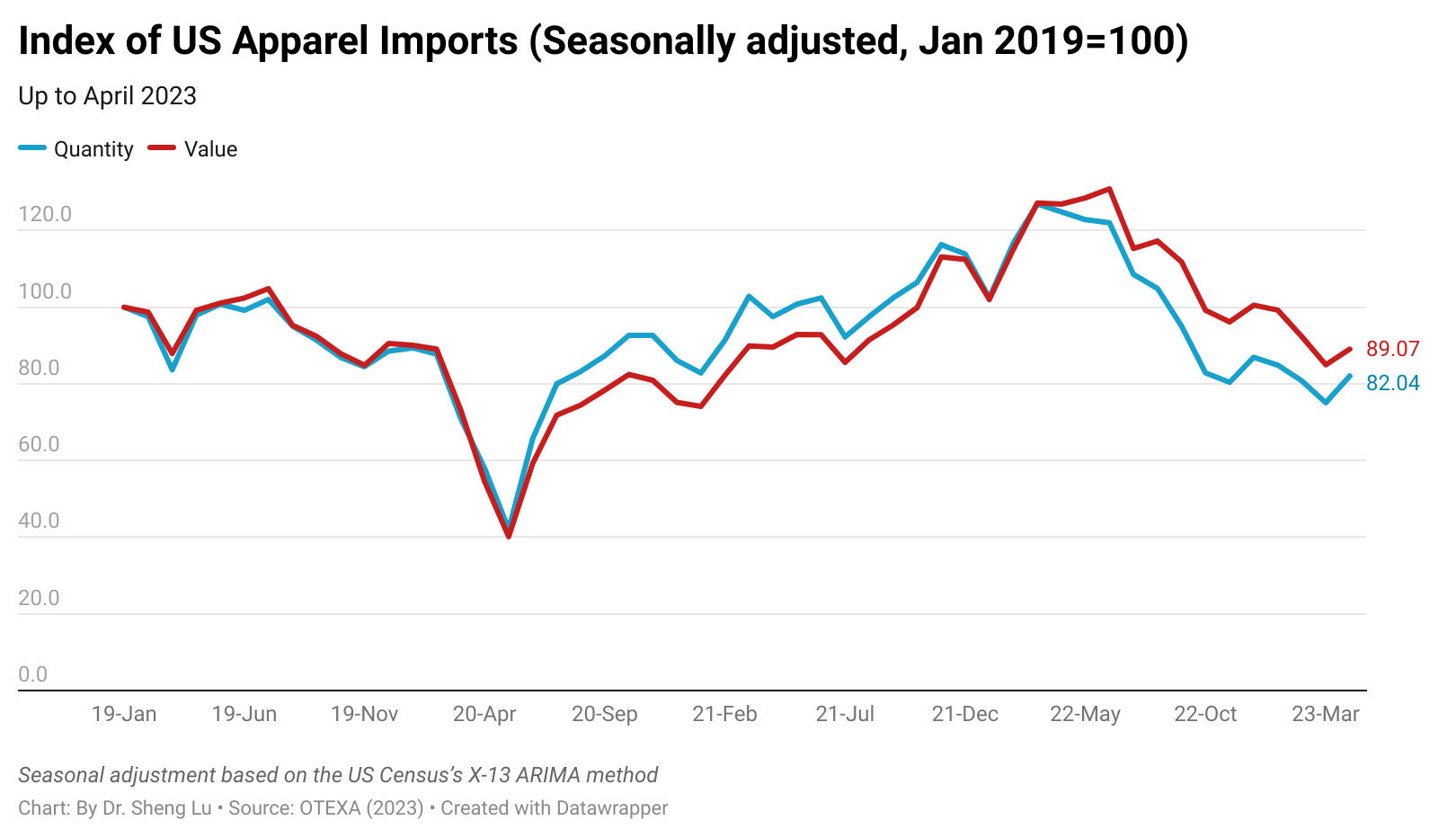

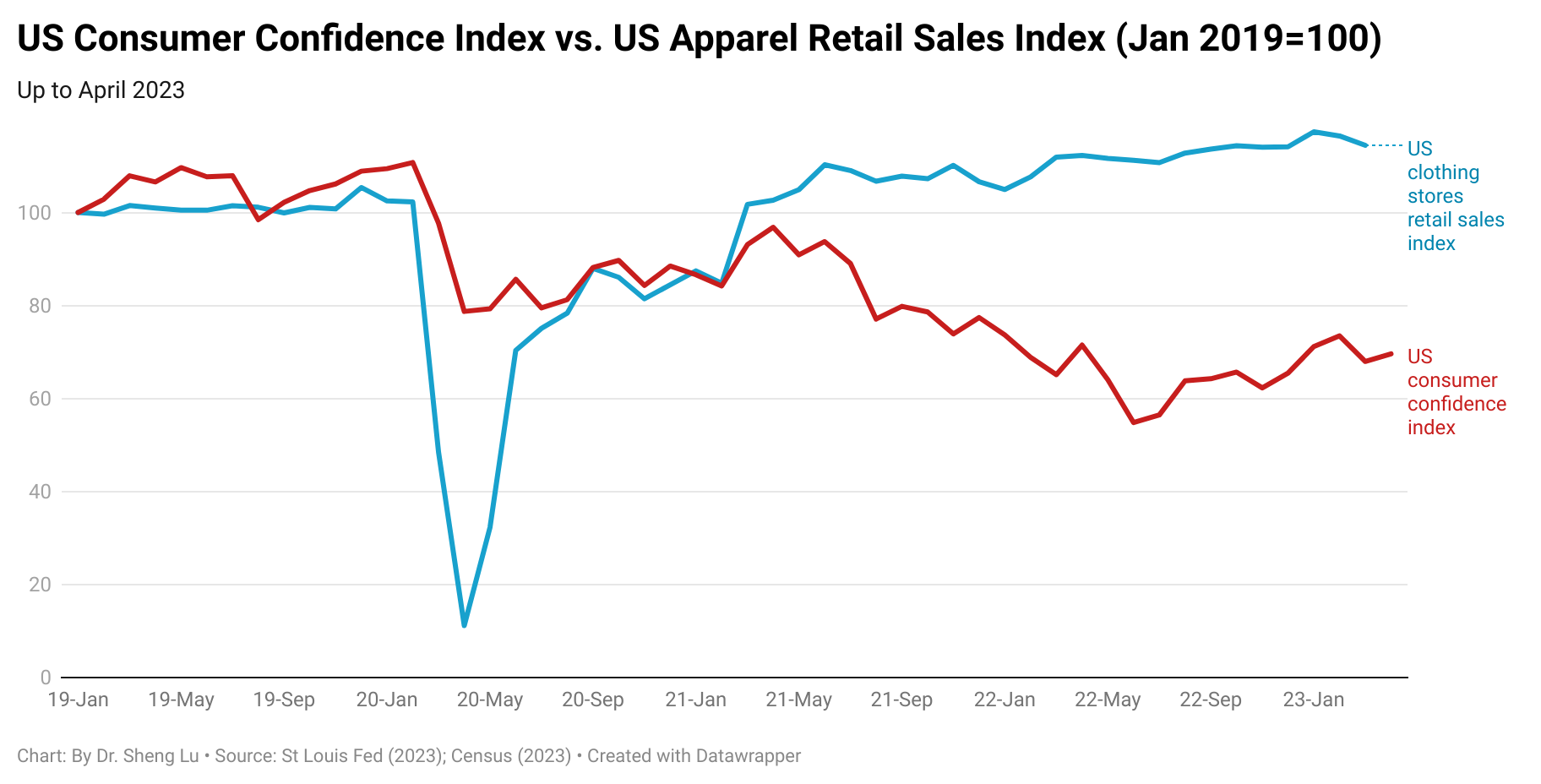

First, US apparel imports indicated a slow improvement in April 2023 but remained weak this year. For example, measured in quantity, US apparel imports fell by 33.9% in April 2023 from a year ago, but it was less significant than in March (i.e., down 40.2% YoY*). Likewise, measured in value, US apparel imports fell by 29.3% YoY in April 2023, which improved from a 32.7% YoY decline in March 2023. (*YoY: Year-over-year)

Overall, the shrinking US apparel import volume reflected the headwinds in the US economy and consumers’ hesitancy to purchase clothing amid financial uncertainties and high inflation. Recent economic indicators also present a mixed picture of the US economy’s growth trajectory. For example, while the US consumer confidence index slightly went up from 68.0 in March to 69.6 in April 2023 (January 2019=100), the advanced clothing store sales index in April fell to 115.6 (Jan 2019=100), the lowest so far in 2023 (e.g., was 120.6 in January 2023). However, since summer is traditionally a peak season for clothing sales, followed by events like back-to-school shopping, there remains hope that US apparel imports may experience a slight recovery at some point in the second half of the year.

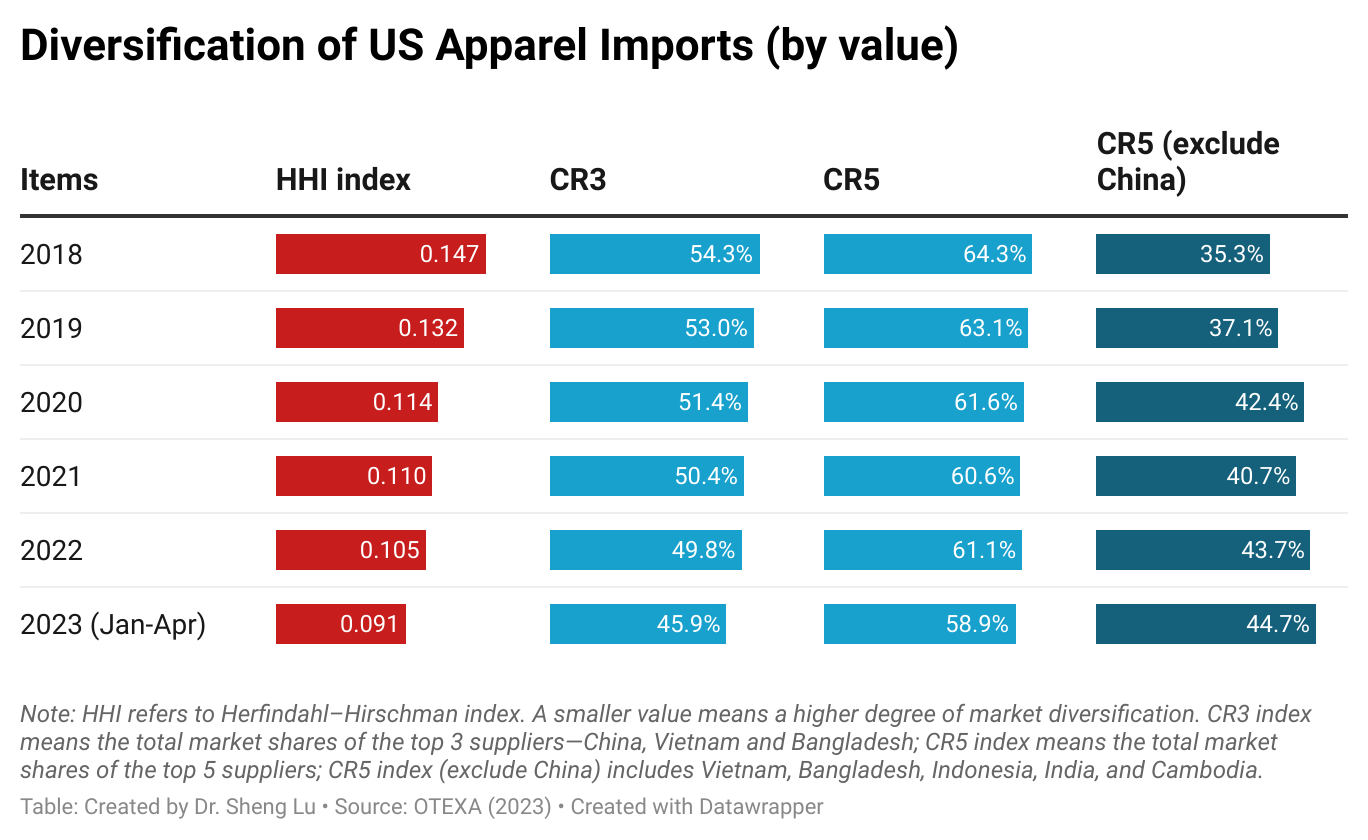

Second, trade data suggested that US apparel imports came from more diverse sources. For example, the Herfindahl–Hirschman index (HHI) fell below 0.1 in the first four months of 2023. Likewise, the market shares of the five largest suppliers (CS5) fell below 60% for the first time since 2018. The result suggested that leveraging sourcing diversification is a prevalent strategy among US fashion companies to mitigate supply chain risks and address market uncertainties.

Third, US fashion companies are serious and eager to further reduce their “China exposure.” Although China remained the top apparel supplier to the US, its market share fell to a new low of 17.9% in value and 30.6% in quantity in the first four months of 2023. Notably, for the first time in decades, less than 10% of US cotton apparel imports came from China in March/April 2023, revealing the significant impact of the Uyghur Forced Labor Prevention Act (UFLPA) on US fashion companies’ China sourcing strategies.

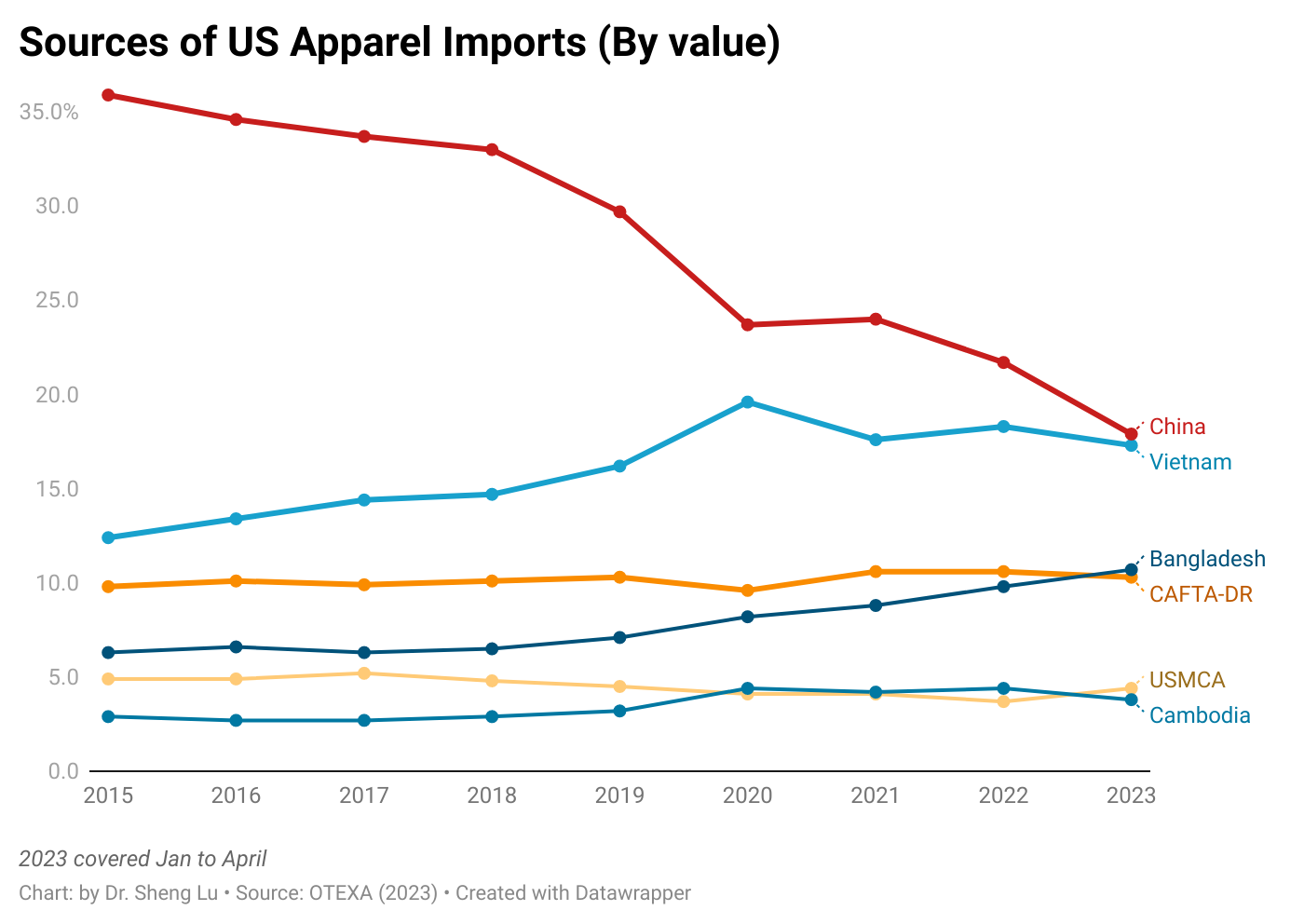

Related, US fashion companies appear to be increasingly cautious about sourcing apparel from Vietnam as its supply chain is too exposed to China, raising concerns about forced labor risks. In value, Vietnam accounted for 17.3% of US apparel imports in the first four months of 2023, down from 18.6% a year ago. Notably, almost the same amount of Vietnam’s textile and apparel products were subject to the CBP’s UFLPA investigation as China in FY2023.

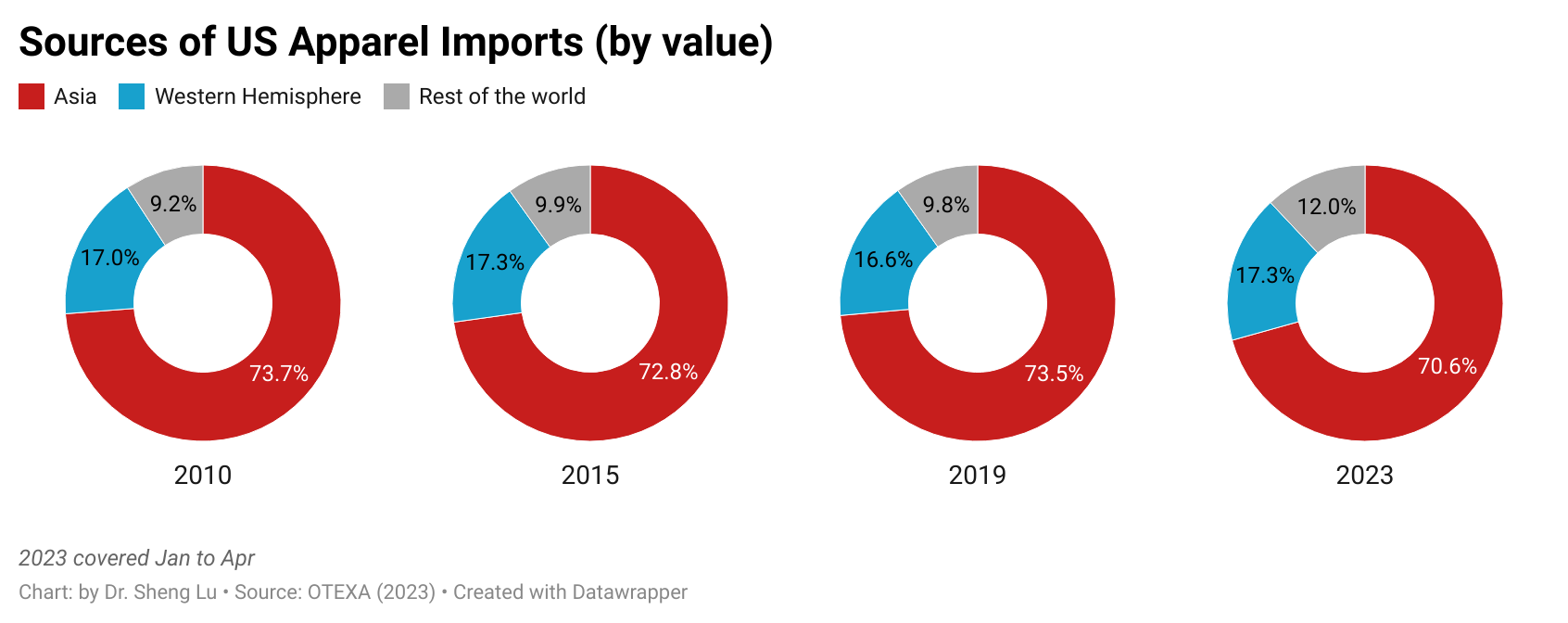

Fourth, large-scale Asian countries benefited the most as US fashion companies looking for China’s alternatives. Specifically, measured in value, about 70.6% of US apparel imports came from Asia in the first four months of 2023, down from 74.9% in 2022. However, the five largest apparel exporting countries in Asia other than China (i.e., Vietnam, Bangladesh, Indonesia, India, and Cambodia) accounted for 44.7% of US apparel imports in the first four months of 2023, a new high since 2018 (i.e., was 35.3%). These countries are among the most popular “alternatives to China” because of their balanced performance regarding production capacity, cost, flexibility, and compliance risks.

Fifth, US fashion companies are also actively exploring new near-shoring opportunities from the Western Hemisphere. For example, about 17.3% of US apparel imports came from Western Hemisphere countries in the first four months of 2023, up from 15.6% in 2023. That being said, measured in quantity, US apparel imports from Mexico and CAFTA-DR members fell by 13.0% and 21.2% in the first four months of 2023 from a year ago due to the struggling US economy. It will be interesting to see whether CAFTA-DR and Mexico can keep or enhance their market shares when the US import demand recovers.

The full paper is HERE. Below are the key findings:

Over the past decade, U.S. fashion brands and retailers have seen Central America as a critical emerging apparel-sourcing destination. Especially since implementing the Dominican-Republic Central America Free Trade Agreement (CAFTA-DR) in 2006, a trade deal among the United States, El Salvador, Guatemala, Honduras, Nicaragua, the Dominican Republic (joined in 2007), and Costa Rica (joined in 2009), apparel sourcing from the region gained consistent interest among U.S. companies.

Nevertheless, U.S. apparel sourcing from CAFTA-DR members is NOT without significant challenges. For example, CAFTA-DR countries’ market shares in the U.S. apparel import market fell from 11.8% in 2005 before the trade agreement entered into force to only 10.6% in 2022, measured by value. Trade data also indicated that U.S. apparel sourcing from CAFTA-DR members concentrated on simple and low-value items, such as T-shirts, and lacked product diversification with no improvement over the years.

Given the high stakes of improving the status quo, this study quantitatively evaluated the impact of textile raw material access on CAFTA-DR’s apparel exports to the United States. Specifically, this study assumed that CAFTA-DR members cut their textile import tariff rates to improve garment producers’ textile raw material access (i.e., to reduce the cost of sourcing textiles from anywhere in the world and beyond the U.S. supply). The computable general equilibrium (CGE) model estimation based on the GTAP9 database shows mixed results:

On the one hand, cutting CAFTA-DR members’ textile import tariffs to improve their garment producers’ textile raw material access would significantly improve CAFTA-DR members’ price competitiveness of their apparel exports to the United States and increase the export volume.

However, cutting CAFTA-DR members’ textile import tariffs to improve their garment producers’ textile raw material access would significantly expand their textile imports from non-U.S. sources. This means that CAFTA-DR members’ dependence on the U.S. textile raw material supply may decline further.

Overall, the study’s findings remind us that the debate on expanding U.S. apparel sourcing from CAFTA-DR members should go beyond CAFTA-DR members’ garment production. Instead, more efforts could be made to enhance CAFTA-DR garment producers’ textile raw material access as an effective way to expand the region’s apparel exports to the United States.

Meanwhile, several leading CAFTA-DR apparel exporting countries, including Honduras and Nicaragua, have been engaged in negotiations for free trade agreements with China, Taiwan, and other Asian economies. As the study’s findings indicate, these new trade deals could incentivize CAFTA-DR apparel manufacturers to increase their textile sourcing from Asia. In other words, inaction on the U.S. side and maintaining the status quo still could have significant implications for the future stability of the Western Hemisphere textile and apparel supply chain.

USITC adopted two methods to estimate Section 301 tariffs’ economic impacts:

Econometric model estimates using monthly trade data (10-digit HS code) from January 2017 to December 2021.

A set of partial equilibrium models that linked section 301 tariffs to domestic prices and production at the four-digit NAICS code level. USITC used data from 2018 to 2021 as the base year.

USITC only considered Section 301 tariffs’ direct impacts, i.e., “how tariffs impacted prices, production, and trade for products subject to section 301 tariffs and domestic sectors that compete directly with those imports.”

Regarding the overall impact of Section 301 actions, USITC found that the tariffs imposed on Chinese goods resulted in a price rise paid by US importers, but the exporter prices received by Chinese firms were mostly unchanged. As a result, “imports from China decreased in quantity, leading to a substantial decline in their import value. These changes, in turn, caused an increase in production and prices in US domestic industries that were competing with Chinese imports.”

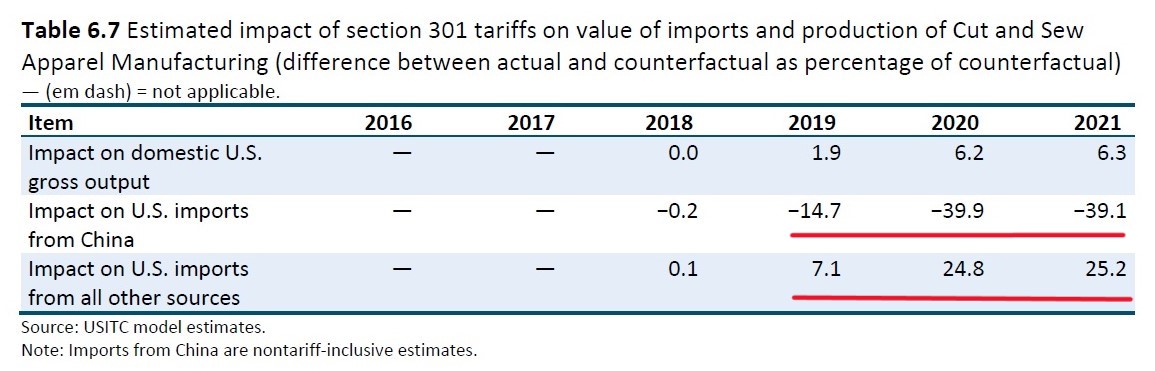

USITC also evaluated the specific impacts of Section 301 tariffs on the Cut and Sew apparel (NAICS 3152) sector. According to USITC:

“nontariff-inclusive value” refers to the change in the value of imports from China excluding the value of the section 301 duties themselves, which provide an indication of the change in import quantities because export prices are mostly unchanged.

First, Section 301 tariffs hurt US apparel imports from China. USITC estimated that US woven apparel (NAICS 3152) imports from China decreased by 14.7% in 2019 but fell nearly 40% in 2020 and 2021 due to Section 301 tariffs. However, USITC didn’t explain why imports from China suddenly worsened, nor if other factors, such as the Uyghur Forced Labor Prevention Act (UFLPA), played a role.

Second, Section 301 tariffs mostly replaced US woven apparel (NAICS3152) imports from China with other sources. However, the direct benefits of Section 301 tariffs to US domestic cut and sew manufacturing seemed limited. Specifically, USITC estimated that US woven apparel imports from sources other than China increased by 7.1% in 2019, 24.8% in 2020, and 25.2% in 2021 due to Section 301 tariffs. In comparison, Section 301 tariffs resulted in modest growth of US domestic woven apparel (NAICS3152) production (up to 6.3%) over the same period.

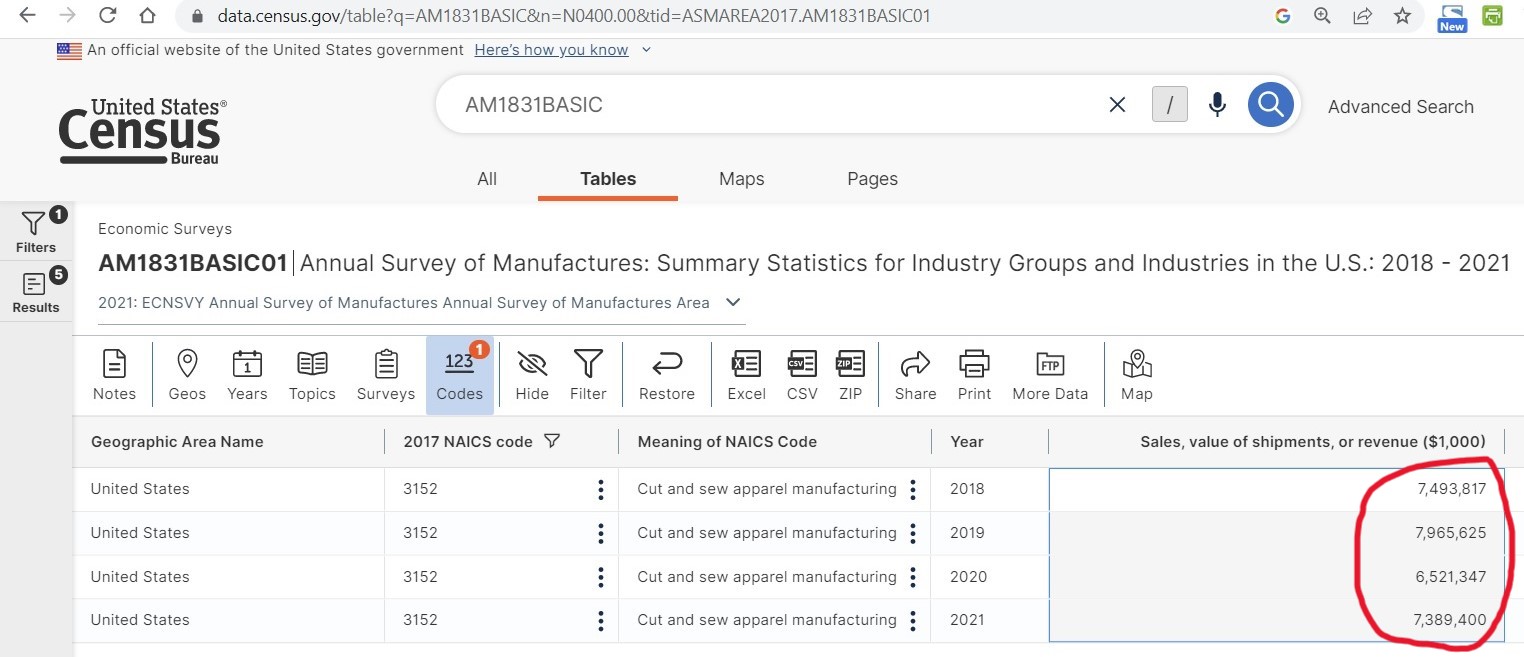

Actual trade and production data further showed that US woven apparel (NAICS 3152) imports from sources other than China increased from $55.3 billion in 2018 to $61.2 billion in 2021 (or up 10.7%). Over the same period, US domestic woven apparel (NAICS 3152) sales & value of shipments declined from $7.49 billion to $7.38 billion (or down 1.4%) (Data source: Census). In other words, no clear evidence suggests that Section 301 tariffs boosted US domestic woven apparel production.

Third, Section 301 tariffs made US woven apparel (NAICS 3152) imports from EVERYWHERE more expensive. On the one hand, USITC found that the price of US woven apparel (NAICS 3152) imports from China increased by 4.4% in 2019, 14.7% in 2020, and 14.5% in 2021 due to the Section 301 tariffs. However, similar to the case of trade volume, USITC didn’t explain why Section 301 tariffs’ price impact suddenly became more significant in 2020 and 2021. (Note: In fact, the Tranche 4A tariffs were 15% since September 1, 2019, but were reduced to 7.5% effective February 14, 2020, because of the US-China Phase One deal.)

Meanwhile, due to limited production capacity outside of China, the Section 301 tariffs caused an increase in the cost of US woven apparel imports from all other countries. Specifically, USITC found that the price of US woven apparel (NACIS 3152) imports from sources other than China increased by 3.2% from 2018 to 2021. (Note: given the hiking sourcing costs in 2022, the price increase could be more significant should USITC include updated 2022 trade data in the estimation.)

Additionally, USITC acknowledged that its estimation may “likely captures the most significant impacts of these tariffs in the short run.” However, some effects of section 301 tariffs would likely be delayed. For example, USITC said, “if importers and domestic producers anticipated the tariffs remaining in place long enough,” they may consider more costly changes, such as adjusting their supply chains and investing in domestic production.

Discussion questions:

Based on USITC’s assessment, should President Biden keep or remove the Section 301 tariffs on imports from China? Why or why not?

Regarding the impact of Section 301, any questions remain unanswered or can be studied further?

Any findings in the USITC report surprised you and why?

Trend 1: US fashion companies continue to diversify their sourcing base in 2022

Numerous studies suggest that US fashion companies leverage sourcing diversification and sourcing from countries with large-scale production capacity in response to the shifting business environment. For example, according to the 2022 fashion industry benchmarking study from the US Fashion Industry Association (USFIA), more than half of surveyed US fashion brands and retailers (53%) reported sourcing apparel from over ten countries in 2022, compared with only 37% in 2021. Nearly 40% of respondents plan to source from even more countries and work with more suppliers over the next two years, up from only 17% in 2021.

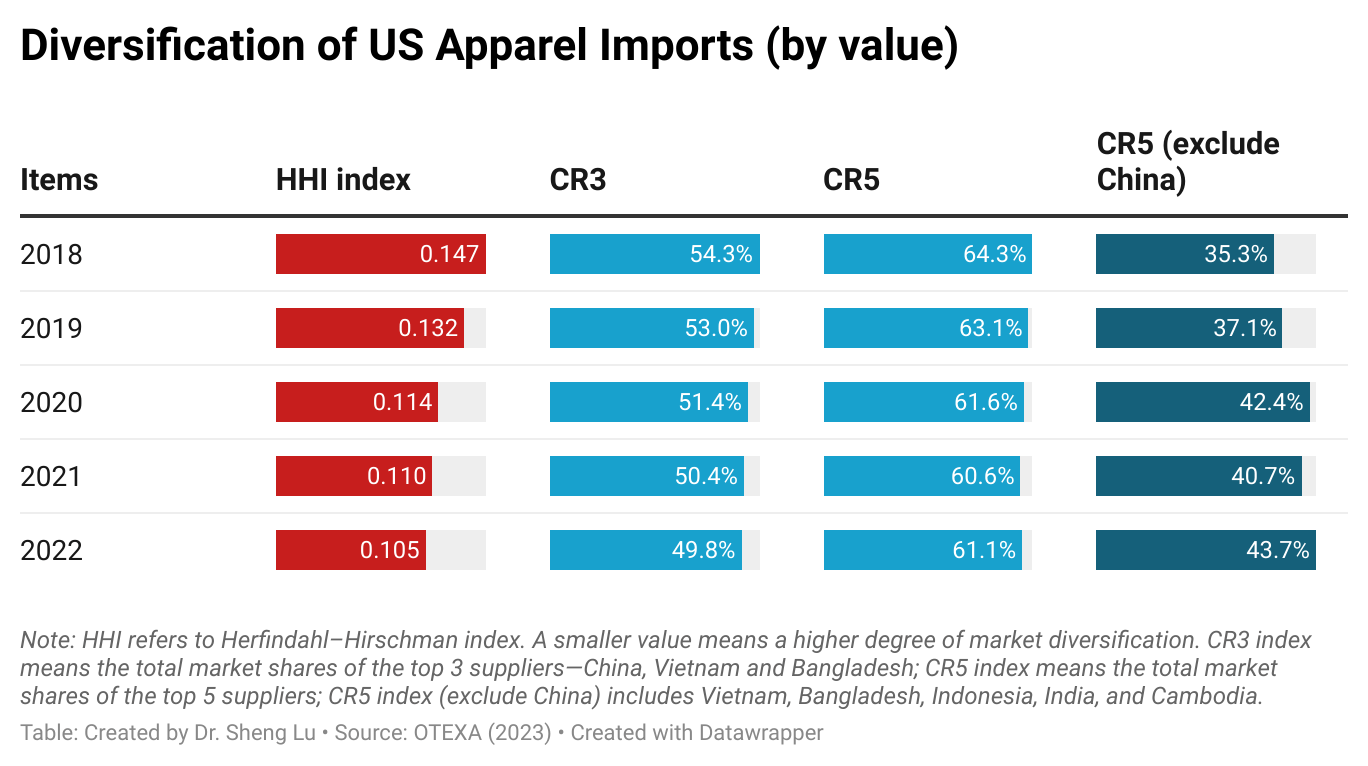

Trade data confirms the trend. For example, the Herfindahl–Hirschman index (HHI), a commonly-used measurement of market concentration, went down from 0.110 in 2021 to 0.105 in 2022, suggesting that US apparel imports came from even more diverse sources.

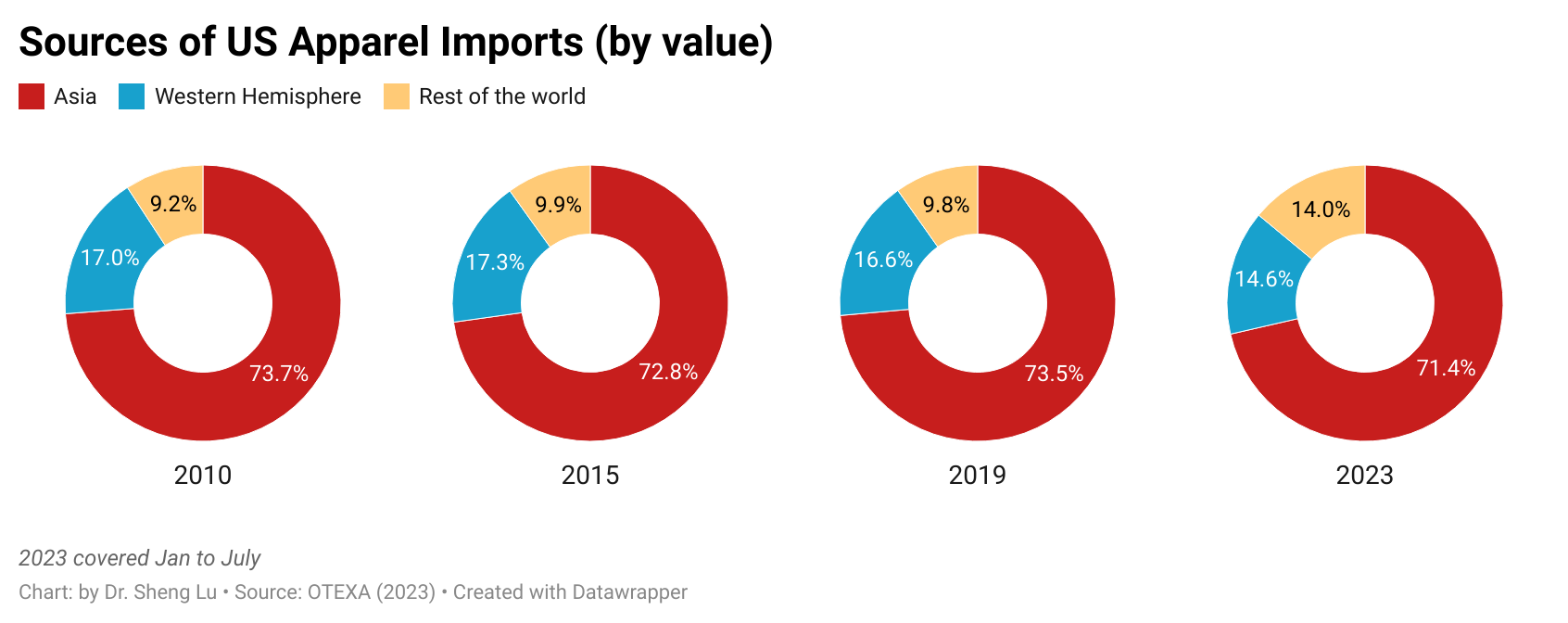

Trend 2: Asia as a whole will remain the dominant source of imports

Measured in value, about 73.5% of US apparel imports came from Asia in 2022, up from 72.8% in 2021. Likewise, the CR5 index, measuring the total market shares of the top five suppliers—all Asia-based, i.e., China, Vietnam, Bangladesh, Indonesia, and India, went up from 60.6% in 2021 to 61.1% in 2022. Notably, the CR5 index without China (i.e., the total market shares of Vietnam, Bangladesh, Indonesia, India, and Cambodia) enjoyed even faster growth, from 40.7% in 2021 to 43.7% in 2022.

Additionally, facing growing market uncertainties and weakened consumer demand amid high inflation pressure, US fashion companies may continue to prioritize costs and flexibility in their vendor selection. Studies consistently show that Asia countries still enjoy notable advantages in both areas thanks to their highly integrated regional supply chain, production scale, and efficiency. Thus, US fashion companies are unlikely to reduce their exposure to Asia in the short to medium term despite some worries about the rising geopolitical risks.

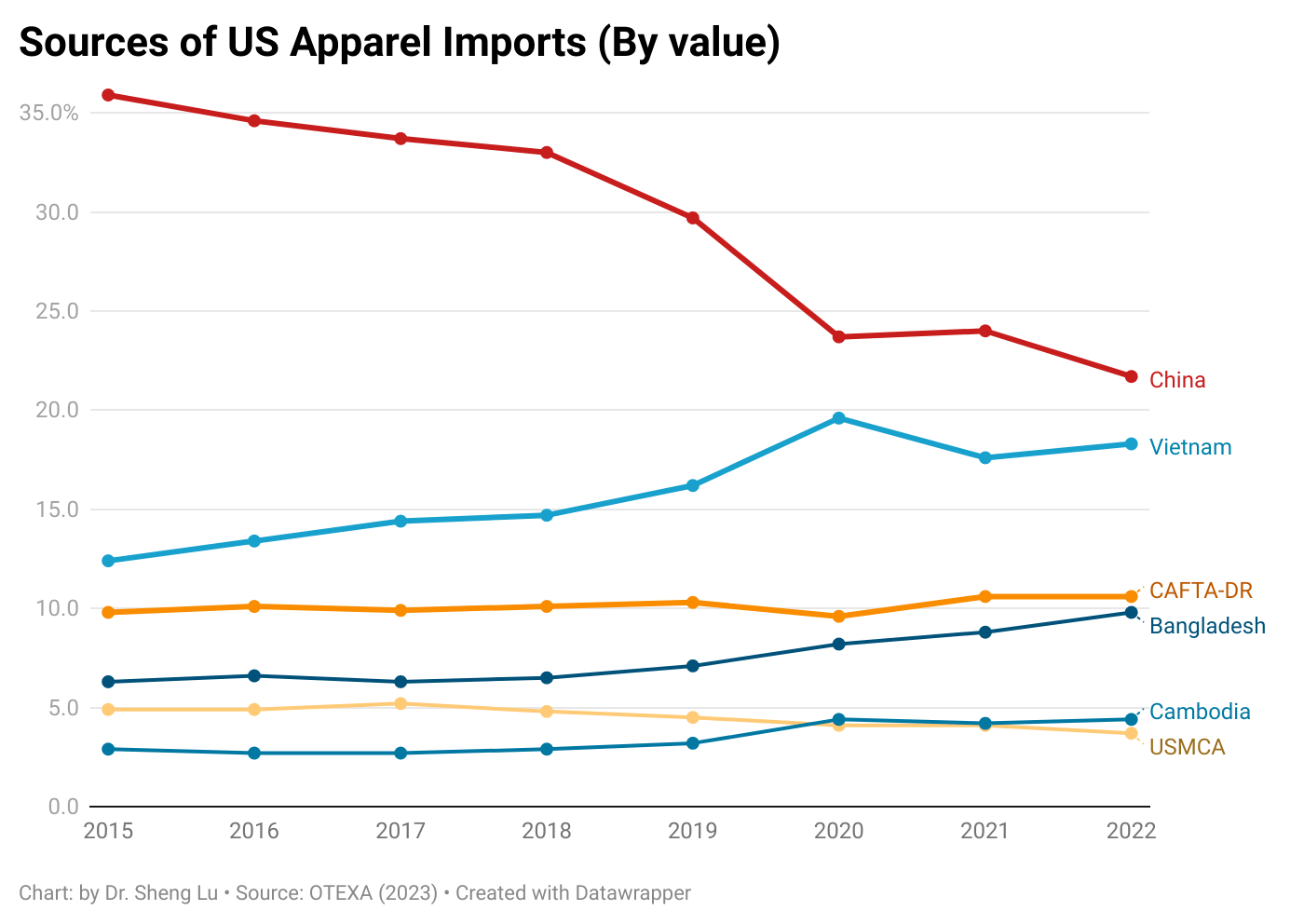

Trend 3: US fashion companies’ China sourcing strategy continues to evolve

Several factors affected US apparel sourcing from China negatively in 2022:

One was China’s stringent zero-COVID policy, which led to severe supply chain disruptions, particularly during the fall. As a result, China’s market shares from September to November 2022 declined by 7-9 percentage points compared to the previous year over the same period.

The second factor was the implementation of the Uyghur Forced Labor Prevention Act (UFLPA) in June 2022, which discouraged US fashion companies from sourcing cotton products from China. For example, only about 10% of US cotton apparel came from China in the fourth quarter of 2022, down from 17% at the beginning of the year and much lower than nearly 27% back in 2018.

The third contributing factor was the US-China trade tensions, including the continuation of Section 301 punitive tariffs. Industry sources indicate that US fashion companies increasingly source from China for relatively higher-value-added items targeting the premium or luxury market segments to offset the additional sourcing costs.

Further, three trends are worth watching regarding China’s future as an apparel sourcing base for US fashion companies:

One is the emergence of the “Made in China for China” strategy, particularly for those companies that view China as a lucrative sales market. Recent studies show that many US fashion companies aim to tailor their product offerings further to meet Chinese consumers’ needs and preferences.

Second is Chinese textile and apparel companies’ growing efforts to invest and build factories overseas. As a result, more and more clothing labeled “Made in Bangladesh” and “Made in Vietnam” could be produced by factories owned by Chinese investors.

Third, China could accelerate its transition from exporting apparel to providing more textile raw materials to other apparel-exporting countries in Asia. Notably, over the past decade, most Asian apparel-exporting countries have become increasingly dependent on China’s textile raw material supply, from yarns and fabrics to various accessories. Moreover, recent regional trade agreements, particularly the Regional Comprehensive Economic Partnership (RCEP), provide new opportunities for supply chain integration in Asia.

Trend 4: US fashion companies demonstrate a new interest in expanding sourcing from the Western Hemisphere, but key bottlenecks need to be solved

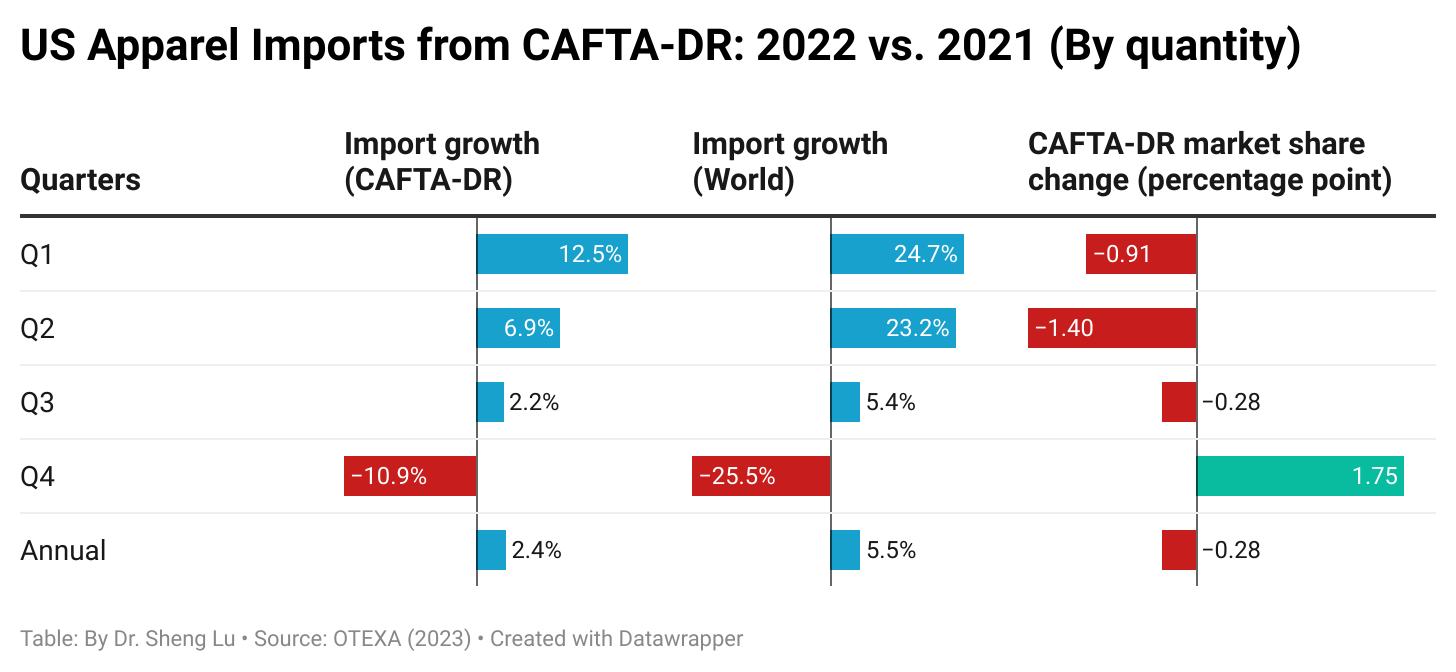

Trade data suggests a mixed picture of near-shoring in 2022. For example, members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) and US-Mexico-Canada Trade Agreement (USMCA) accounted for a declining share of US apparel imports in 2022, measured in quantity and value. While CAFTA-DR and USMCA members showed an increase in their market share of US apparel imports in the fourth quarter of 2022, reaching 10.7% and 3.1%, respectively, this growth was not accompanied by an increase in trade volume. Instead, US apparel imports from these countries decreased by 11% and 15%, respectively, compared to the previous year. CAFTA-DR and USMCA members’ gain in market share was mainly due to a sharper decline in US apparel imports from the rest of the world (i.e., decreased by over 25% in the fourth quarter of 2022).

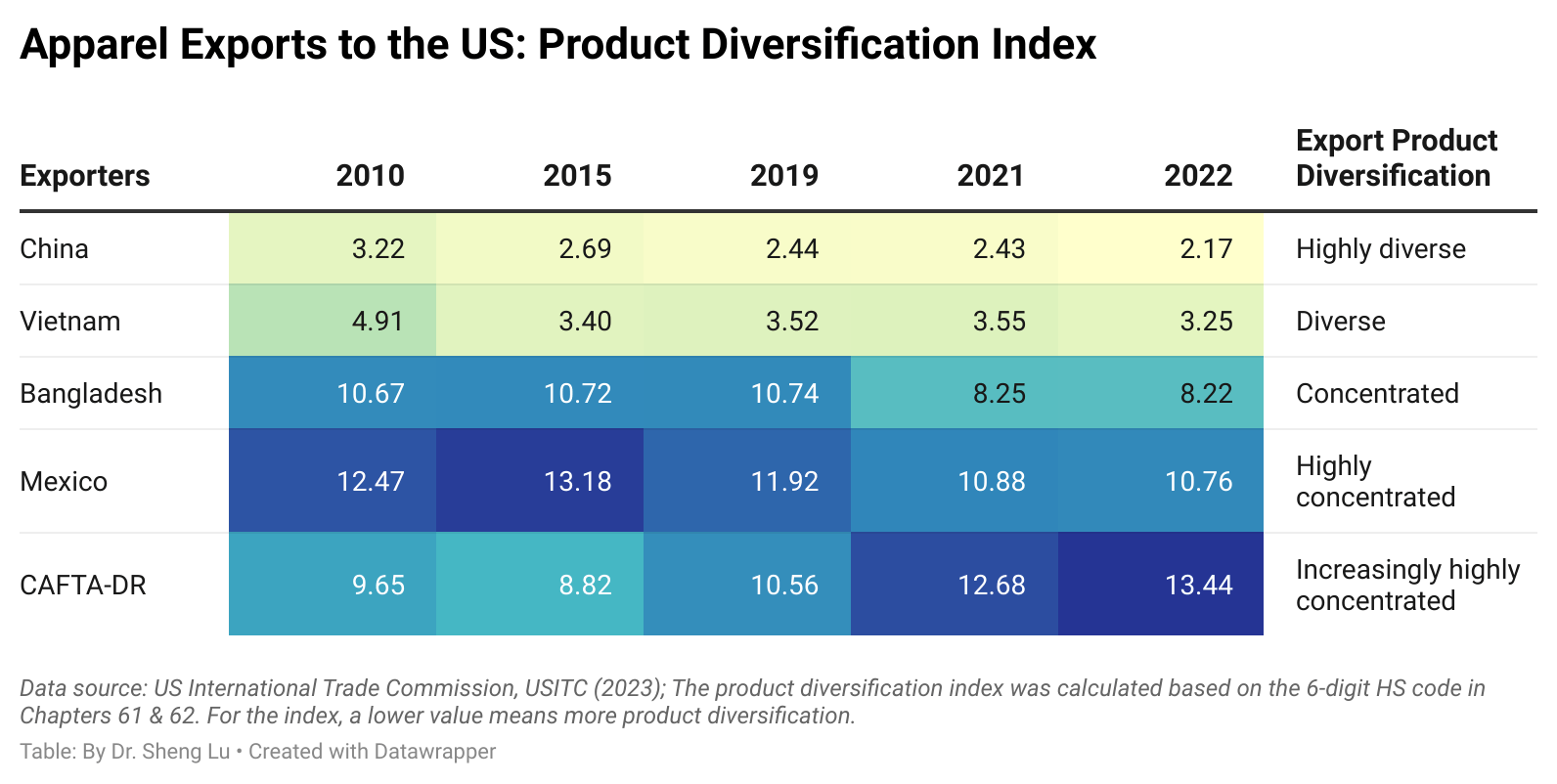

Trade data also suggests two other bottlenecks preventing more US apparel sourcing from CAFTA-DR and USMCA members. One is the lack of product diversity. For example, the product diversification index consistently shows that US apparel imports from CAFTA-DR members and Mexico concentrated on only a limited category of products, and the problem worsened in 2022. The result explained why US fashion companies often couldn’t move souring orders from Asia to CAFTA-DR and USMCA members.

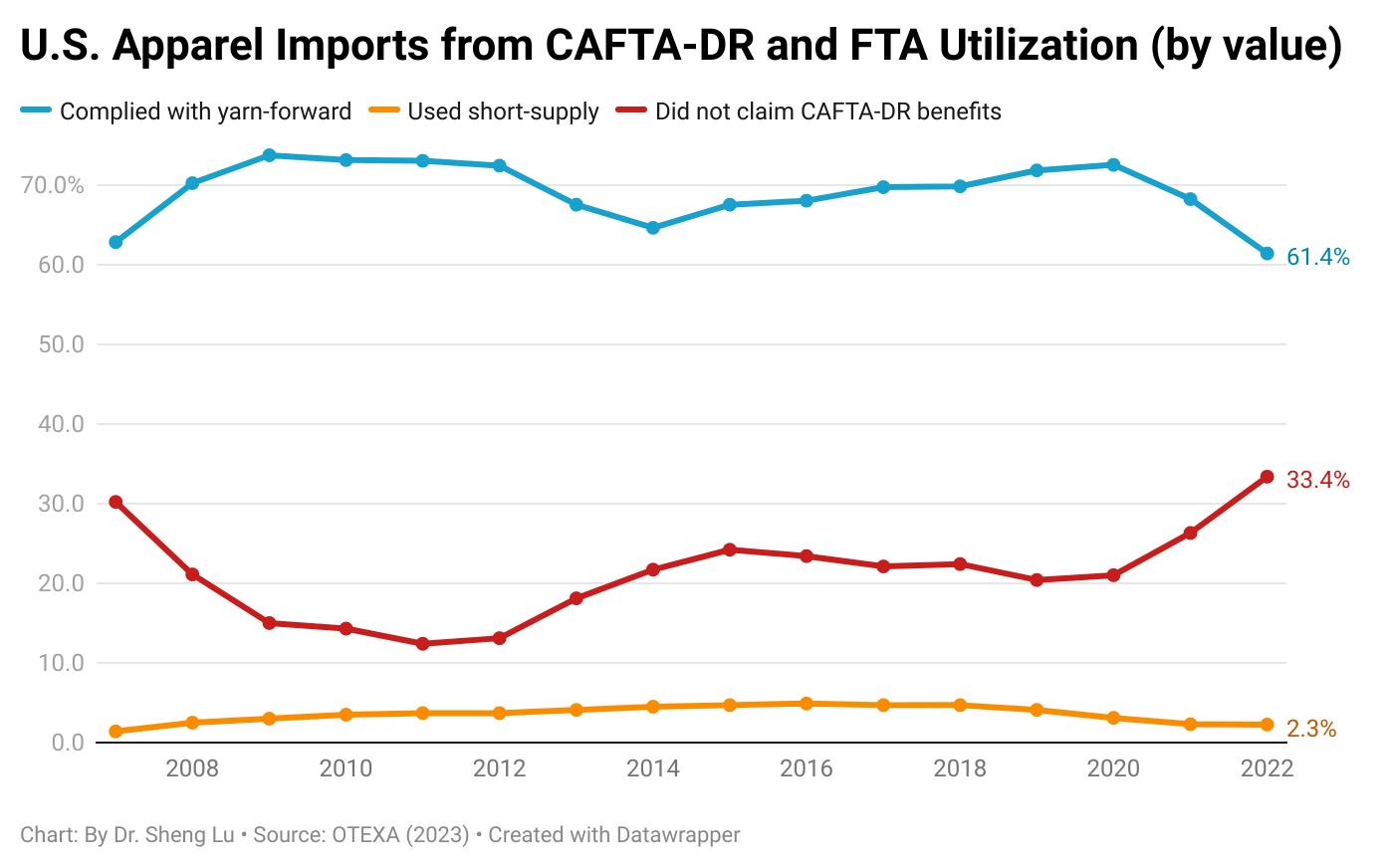

Another problem is the underutilization of the trade agreement. For example, CAFTA-DR’s utilization rate for US apparel imports consistently went down from its peak of 87% in 2011 to only 74% in 2021. The utilization rate fell to 66.6% in 2022, the lowest since CAFTA-DR fully came into force in 2007. This means that as much as one-third of US apparel imports from CAFTA-DR did NOT claim the agreement’s preferential duty benefits. Thus, regarding how to practically grow US fashion companies’ near-shoring, we could expect more public discussions and debates in the new year.

This study aims to understand western fashion brands and retailers’ latest China apparel sourcing strategies against the evolving business environment. We conducted a content analysis of about 30 leading fashion companies’ public corporate filings (i.e., annual or quarterly financial reports and earnings call transcripts) submitted from June 1, 2022 to December 31, 2022.

The results suggest several themes:

First, China remains one of the most frequently used apparel sourcing destinations. For example:

Express says, “The top five countries from which we sourced our merchandise in 2021 were Vietnam, China, Indonesia, Bangladesh and the Philippines, based on total cost of merchandise purchased.”

According to TJX, “a significant amount of merchandise we offer for sale is made in China.”

Children’s Place says, “We source from a diversified network of vendors, purchasing primarily from Vietnam, Cambodia, Indonesia, Ethiopia, Bangladesh, and China.“

Ralph Lauren adds, “In Fiscal 2022, approximately 97% of our products (by dollar value) were produced outside of the US, primarily in Asia, Europe, and Latin America, with approximately 19% of our products sourced from China and another 19% from Vietnam.

However, many fashion companies have significantly cut their apparel sourcing volume from China. More often, China is no longer the No.1 apparel sourcing destination, overtaken by China’s competitors in Asia, such as Vietnam.

According to Lululemon, “During 2021, approximately 40% of our products were manufactured in Vietnam, 17% in Cambodia, 11% in Sri Lanka, 7% in China (PRC), including 2% in Taiwan, and the remainder in other regions… From a sourcing perspective, when looking at finished goods for the upcoming 2022 fall season, Mainland China represents only 4% to 6% of our total unit volume.”

Levi’s says, “The good thing about our supply chain is we’ve got truly a global footprint. We don’t manufacture a whole lot in China anymore. We’ve been slowly divesting manufacturing out of China, if you will, and kind of playing our chips elsewhere on the global map… Less than 1% of what we’re bringing into this country, into the US, less than 1% of it is coming from China.”

Adidas says, “In 2021, we sourced 91% of the total apparel volume from Asia (2020: 93%). Cambodia is the largest sourcing country, representing 21% of the produced volume (2020: 22%), followed by China with 20% (2020: 20%) and Vietnam with 15% (2020: 21%).”

Victoria’s Secret says, “On China, China is a single-digit percentage of our total inflow of merchandise. We’re not particularly dependent on China at all.”

Nike: “As of May 31, 2022, we were supplied by 279 finished goods apparel contract factories located in 33 countries. For fiscal 2022, contract factories in Vietnam, China and Cambodia manufactured approximately 26%, 20% and 16% of total NIKE Brand apparel, respectively“

Meanwhile, fashion companies still heavily use China as a sourcing base for textile raw materials (such as fabrics). For example:

Columbia Sportswear says it sources most of its finished products from Vietnam, but “a large portion of the raw materials used in our products is sourced by our contract manufacturers in China.”

Likewise, Puma says, “90% of our recycled polyester comes from Vietnam, China, Taiwan (China) and Korea.”

Guess says, “During fiscal 2022, we sourced most of our finished products with partners and suppliers outside the U.S. and we continued to design and purchase fabrics globally, with most coming from China.”

Lulumemon says, “Approximately 48% of the fabric used in our products originated from Taiwan, 19% from China Mainland, 11% from Sri Lanka, and the remainder from other regions.”

Second, Western fashion companies unanimously ranked the COVID situation as one of their top concerns for China. Many companies reported significant sales revenue and profits loss due to China’s draconian “zero-COVID” policy and lockdown measures. For example,