Potential impact of the Trans-Pacific Partnership (TPP) remains a hot topic among the U.S. textile and apparel industry. A recent news report suggests that implementation of the agreement will negatively affect clothing manufacturers in LA, where most remaining U.S. apparel manufacturing capacity is located.

According to the news report, “small, independent apparel manufacturers (in LA) did not see big gains from TPP because they did not want to outsource their work, but it put them at a competitive disadvantage.” One local industry estimation quoted in the report claims that “Southern California’s apparel manufacturing will shrink an additional 20 percent if the TPP goes into effect.”

The report further says that “A key question for the apparel industry is whether the agreement includes a yarn-forward provision, which requires material to come from a TPP country in order to be duty-free.” However, the report does not explain why the “yarn-forward” rule could potentially benefit apparel manufacturing in the United States.

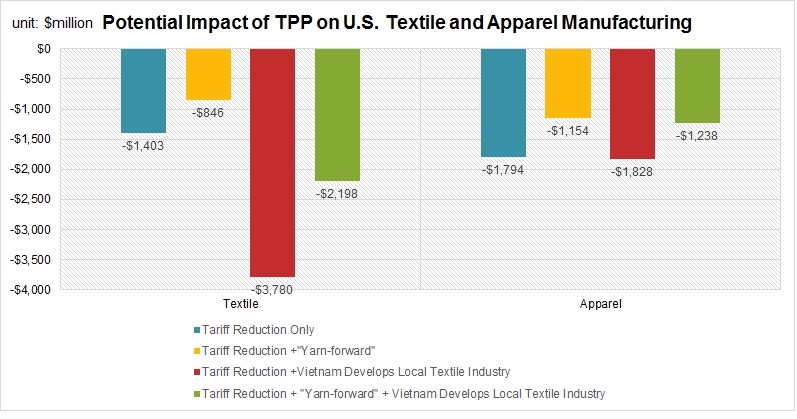

The followings are my personal preliminary estimation* of the potential impact of TPP on U.S. T&A manufacturing. Results show that, compared to the base year level in 2011:

- TPP overall will have a negative impact on U.S. domestic textile and apparel manufacturing. In all simulated scenarios, the annual manufacturing output in the United States will decline by $846 million–$3,780 million for textile and $1,154 million–$1,828 million for apparel than otherwise.

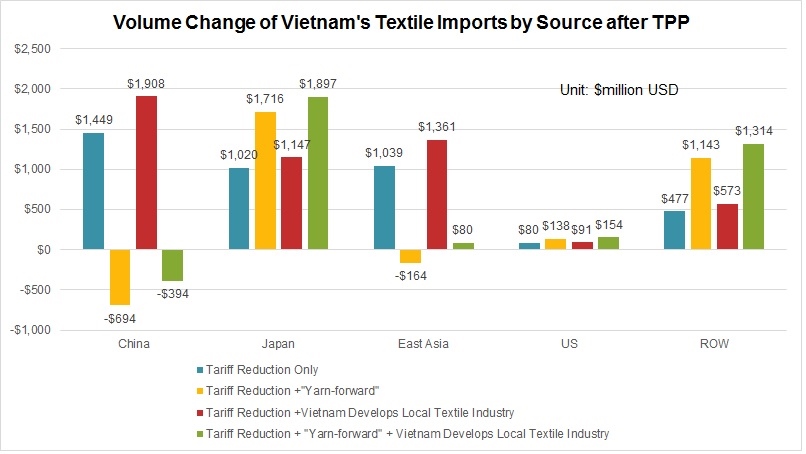

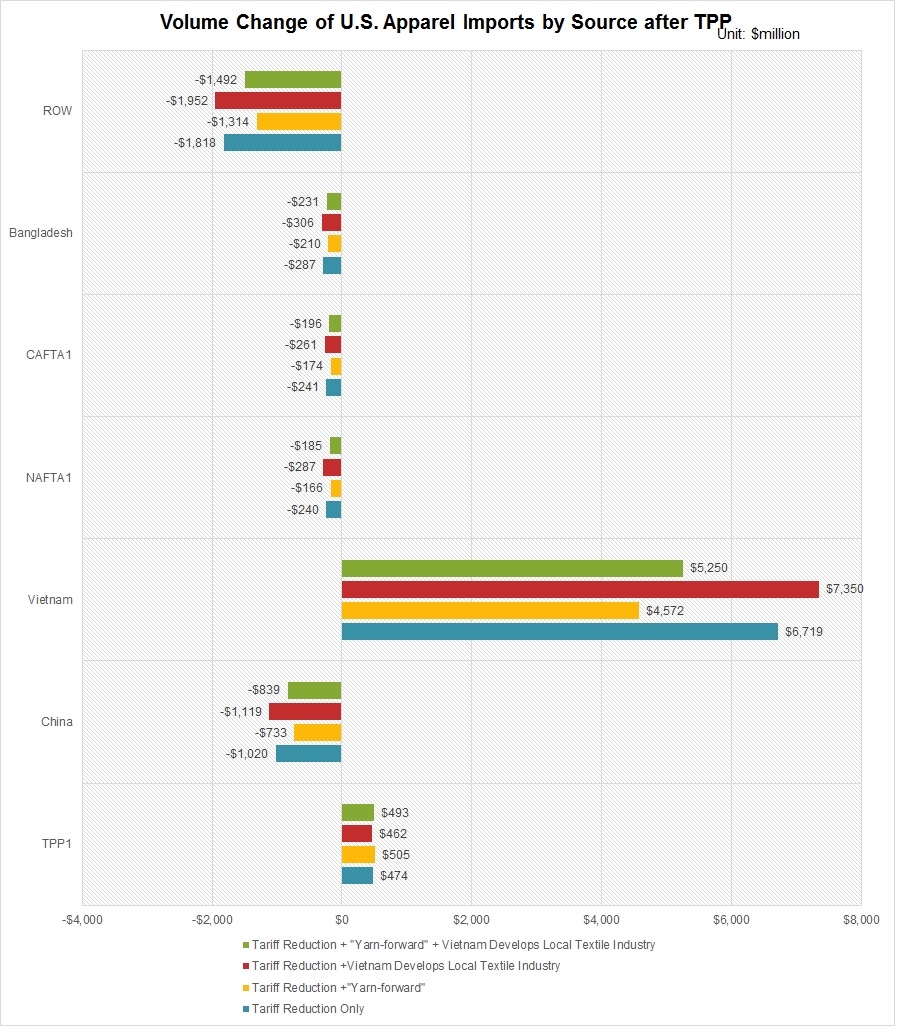

- The “yarn-forward” rule may not substantially benefit U.S. domestic textile and apparel manufacturing as some people had suggested, for two reasons: 1) results show that Vietnam is more likely to use Japanese textiles than U.S. textiles when yarn-forward rule is in place. 2) U.S. apparel imports from Vietnam directly compete with those imported from NAFTA and CAFTA regions, the largest export market for U.S.-made yarns and fabrics. When NAFTA and CAFTA’s market share in the U.S. apparel import market is taken away by Vietnam, U.S. textile exports to NAFTA and CAFTA will decline anyway, regardless of whether Vietnam uses U.S.-made textiles.

- Results suggest that compared with the “yarn-forward” rule, development of Vietnam’s local textile industry will have an even larger impact on the future of U.S. domestic textile and apparel manufacturing. Particularly, when Vietnam becomes more capable of making textile inputs by its own, not only Vietnam’s overall demand for imported textiles will decline, but also Vietnam’s apparel exports will become even more price-competitive in the U.S. as well as the world marketplace.

*Note:1. The estimation is conducted based on the latest Global Trade Analysis Project (GTAP) 9.0 database which includes complete bilateral trade information, transport and protection linkages of 140 countries and 57 sectors. Four scenarios are estimated:

- Scenario 1 (Tariff reduction only): assumes tariff rate for textile and apparel traded between the twelve TPP members are eliminated, whereas tariff rate for other textile and apparel trade flows remain unchanged.

- Scenario 2 (Tariff reduction + yarn forward): assumes that in addition to tariff reduction among TPP members for T&A, Vietnam substantially increases tariff rate by 100 percent for textile imports from its leading suppliers that are non-TPP members (i.e. China, South Korea and Taiwan). This policy shock provides strong financial incentives for Vietnam to import less textile from non-TPP suppliers and instead import more from other TPP members—an equivalent effect as the yarn forward rule.

- Scenario 3(Tariff reduction + Vietnam develops local textile industry): assumes that in addition to tariff reduction among TPP members for T&A, productivity of Vietnam’s textile industry increases by 10 percent whereas productivity of other sectors remain unchanged.

- Scenario 4 (Tariff reduction + yarn forward + Vietnam develops local textile industry): this scenario combines all policy shocks mentioned in scenario 1-3, i.e. tariff rate for textile and apparel traded between the twelve TPP members are eliminated, Vietnam substantially increases its tariff rate by 100 percent for textile imports from its leading suppliers that are non-TPP members (i.e. China, South Korea and Taiwan) and productivity of Vietnam’s textile industry increases by 10 percent.

2. TPP1 includes Australia, New Zealand, Malaysia, Singapore, Burnie, Chile and Peru; NAFTA1 includes Canada and Mexico; CAFTA1 includes all other CAFTA members except the United States.

Sheng Lu

Yarn-forward seemed to me to be the best course of action, but this analysis looks to show otherwise. Although, I think that if an analysis of fabric forward was done, the numbers would be even worse. Are there any policy options where U.S. manufacturing is not negatively affected?

As to the four scenarios: Which scenario do you feel is most likely to happen?

Personally I feel there are misunderstandings about the yarn-forward rule in TPP, especially in the media discussion. TPP presents a much more complicated situation than NAFTA and CAFTA. On the other hand, the commercial interests of the U.S. textile industry have become broader and more diversified. Manufacturing is just part of the industry activity.

It can be seen that the TPP has been a worldwide debate for many years now and brings majors concerns for the Textile and Apparel Industry. I thought the yarn-forward rule might be beneficial in the way that it allows you duty free access for trading if the materials are coming from a TPP country, because this would encourage countries to buy their materials from the U.S After reading this article i can see why people might feel threatened if this agreement is enacted. The reason many of these fashion brands or retailers want to abandon the yarn-forward rule of origin is because of the overall expense of these different yarns and fibers. They do not want to agree or support with anything that is going on if it is going to cost them more money than they are already paying to make these textiles. Many also don’t support it for the reason that some retailers want to be able to import yarns and apparel from other producers even if the textiles are not made in the U.S but unfortunately for them they wont qualify for the duty-free treatment so they feel it is pointless to even support it. It is understandable for these retailers to see the TPP as a threat, they do not want to have a limit on their imports or where they are able to get them from.

I agree with the double transformation rule that the Euratex supports. I feel it is a better and more lenient choice due to the fact that it is equivalent to the fabric forward rule which is less restrictive than the yarn forward rule. I feel people would be more content as well as happy if this rule was in acted because people in the apparel industry would have duty free access to materials and goods from any countries not only the TPP countries. I don’t think that the value added rule will be successful though because it is unrealistic in a way. The reason i believe this is because the value of these products used in spinning or weaving will just make it that much more difficult to calculate the value added at the end. It is also uncontrollable in the way that it can be influenced and or changed by many factors like raw materials which is something that is just out of your hands and makes it harder to deal with.

In addition to a yarn forward rule of origin, I would expect to see extended staging down periods rather than immediate zero-for-zero reductions on day one. This agreement also presents some unique challenges given the number of countries which could include cumulation from fellow trading partners including those with whom the US already has an existing FTA in place.

Agree! There has been discussion on phrase out period and TPL in TPP (https://tmd433.wordpress.com/2015/03/15/tpp-textile-negotiation-updates-march-2015/), but not much information is available to the public. Will see~