The top challenge facing apparel sourcing and trade in the shadow of Covid-19 has quickly shifted from a lack of textile raw material to order cancellation. In major apparel consumption markets such as the EU and US, clothing stores are locked down, making retailers have no choice but to postpone or even cancel sourcing orders.

Based on the Global Trade Analysis Project Recursive Dynamic (GTAP-RD) Model and its latest database, we estimated the trade impact of Covid-19 in three possible scenarios, as summarized in the table below. All these three scenarios are pretty bad but likely situations we may have to face this year. (Note: Because China, US, and EU are the epic-centers of Covid-19, in the study, we assume these three countries/regions’ economies will be hit harder than the rest of the world.)

There are four preliminary findings:

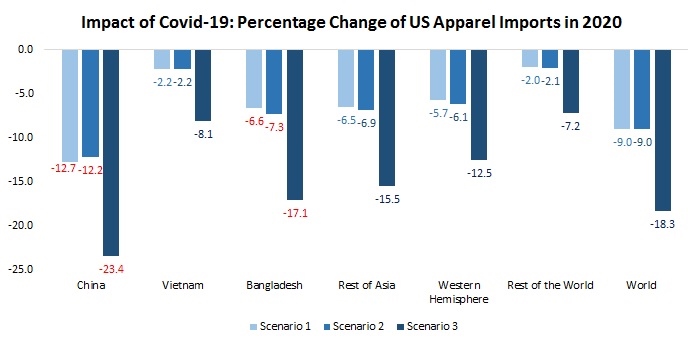

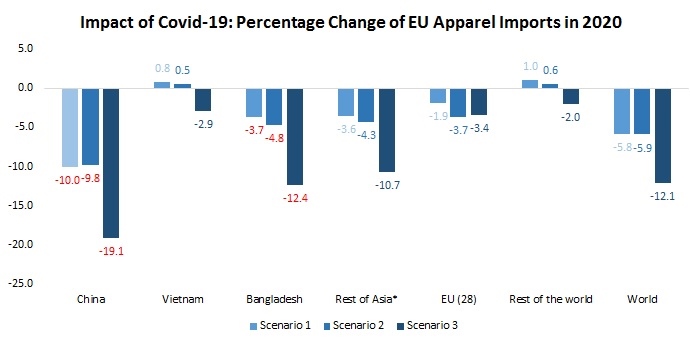

First, the volume of the world apparel trade will be hit hard by Covid-19. As clothing stores are forced to shut down and consumers are losing jobs and struggling financially, the demand for apparel consumption in the EU and US, the world’s top two apparel consumption markets, is expected to drop sharply. As shown in the figures below, every 1% decline in the US and EU Gross Domestic Product (GDP) in 2020 could lead to at least a 2-3% drop in the value of their apparel imports. Notably, during the 2008 financial crisis, the value of world apparel imports also decreased by as much as 11.5% when the EU and US GDP suffered a 2.5-3% negative growth.

Second, with a sharp decline in U.S. and EU apparel imports this year, China could be hit the hardest. In all the three scenarios we estimated, China will suffer the most significant drop in its apparel exports to the US and EU markets. The reasons are threefold: The first factor is the size effect—as the largest source of US and EU apparel imports and with its unparalleled production capacity, China is often used to fulfill large-volume sourcing orders. In the current situation, however, retailers are most likely to cancel these large-quantity orders, resulting in a disproportional loss of China’s apparel exports. Secondly, the US and EU apparel imports from China currently cover almost all major categories, which also makes China the most exposed to order cancellation. Furthermore, jointly affected by last year’s US-China trade war and the outbreak of Covid-19 in China earlier this year, many US and EU fashion brands and retailers have been shifting sourcing orders from China to other Asian countries, such as Bangladesh and Vietnam. To prioritize their limited resources, US and EU retailers are most likely to accelerate this process in the current difficult time.

Other than China, apparel factories in Bangladesh also could suffer severe export decline. Similar to the case of China, Bangladesh serves as a leading apparel supplier for BOTH the EU and US markets, making it more exposed to order cancellation than other countries. Notably, as a beneficiary of the EU Everything But Arms (EBA) program, around 60% of Bangladesh’s apparel currently go to the EU. In comparison, with a more diversified export market, apparel factories in Vietnam are in a better position and have more flexibility to mitigate the impact of a declined import demand from the EU and the US. In 2018, around 40% of Vietnam’s apparel exports went to other markets in the world.

Third, the decreased US and EU apparel imports will have a notable impact on employment in many apparel exporting countries. In history, a 10% change in the value of apparel exports typically results in a 4%-9% change in garment employment. This means, should the US and EU apparel imports drop by 10% in 2020, leading apparel exporting countries such as Bangladesh, Vietnam, Cambodia and India may have to cut 4%-9% of their jobs in the garment sector accordingly. Notably, in developing countries such as Bangladesh and Cambodia, the apparel sector remains the single largest job creator for the local economy, especially for women. The social and economic impact of job losses in the apparel sector due to Covid-19 is very concerning.

Fourth, the economic performance in the US, EU, and China will largely shape the pattern of apparel trade this year. The results in scenarios 1 and 2 overall are pretty close, suggesting the economic cloud of these three countries and regions altogether far exceed the rest of the world.

Last but not least, the global apparel supply chain could continue to face a turbulent time in the next 1-2 years, even if Covid-19 gradually gets under control in the second half of 2020. In history, affected by the 2008 global financial crisis, the value of world apparel exports dropped by 12.8% in 2009. However, the growth rate quickly rebounded to 11.5% the following year. Likewise, should the EU and US apparel imports were able to recover to its normal level in 2021, both importers and garment factories may have to deal with a new round of labor shortage, the price increase of raw material and a lack of production capacity.

by Sheng Lu

Additional reading:

- Retailers Cancel Orders From Asian Factories, Threatening Millions of Jobs (Wall Street Journal)

- Timeline – How coronavirus is impacting the global apparel industry (Just-Style)

Will the COVID-19 pandemic will this drastically change how factories produce garments? Other than having the global economy drastically change, will harsh working conditions like they have in third world countries, such as Bangladesh, change in order to not let something like this happen again, will it help with he overpopulation in the factories, and the cleanliness there?

Other than the economic hardship on factories, I am moderately optimistic about the corporate social responsibility practices in the garment industry: 1) the auditing system is still there and organizations such as WRAP (http://www.wrapcompliance.org/) are working very hard 2) fashion brands and retailers are not changing their sourcing criteria. Instead, sustainability and social responsibility will simply become even more important to the company’s business success. That being said, fashion companies may not be able to allocate as many resources as they would like to the area of corporate social responsibility due to budget restraints.

The fact that so many retailers are having to cancel large orders right now is certainly harmful to their business but also the business of the suppliers that they are buying from. Many people are describing this situation as a “wake-up call for supply chain management.” Because of this, I believe that companies who are focused on sustainability and slow fashion production will be able to recover more easily because they are not placing these extremely large orders that are having to be canceled and their production is done in a more ethical manner. Do you agree with industry reports that sustainable companies will be the ones to survive after this crisis and that even more companies will begin to shift toward more sustainable efforts after this?

these are excellent thoughts and very interesting perspectives! To me, the biggest problem facing the fashion industry right now is that the “music stops…”–stores are forced to close and consumers are asked to stay at home. The unemployment rate is also rising sharply, which implies that consumers’ budget will be tight. Given such a challenging business environment, I am not sure to which extent consumers will shop (or be able to afford) for sustainability–many studies show that “sustainable apparel” are typically priced much higher. That being said, as long as fashion brands and retailers are not downgrading their sourcing criteria and the public still cares about sustainability, at least we won’t see a setback on the issue. Welcome for any further comments and thoughts.

This is a really interesting analysis of everything going on in the T&A industry right now. When I think about sourcing, I immediately consider the retailer’s perspective and how important supplier diversification is in times like these when heavy reliance on one country, like China, has hurt a lot of companies. It is not very often that I stop and think about how factories that did not diversify their exports are being negatively impacted right now as well. Because both manufacturers and retailers across the world are struggling to deal with the aftermath of “putting all of their eggs in one basket,” when we start to get a handle on COVID-19 and industries are restructuring, do you think that globalization will become more prevalent? Who, if any one, do you foresee emerging as the new “go-to” for fulfilling large orders?

excellent comment and thought! a few points to add: 1) The economic impacts of covid19 could go far beyond any financial crisis in history. Notably, not like a purely financial crisis in the past, we are facing a pandemic that has forced nearly all major countries in the world to shut down their economic activities at the same time. As clothing stores are not allowed to open and consumers are asked to stay at home, the challenges facing the apparel industry is represented. 2) The world today is also far more interconnected than decades ago. Not as in the past, garment production has largely turned supply-chain based, which involves multiple countries. Recall when covid-19 hit China at the beginning of the year, the garment industry in Vietnam, Bangladesh, and Cambodia were struggling with a lack of fabric supply from China. 3) Additionally, we have more stakeholders this time. For example, while Cambodia, Vietnam, Myanmar, Indonesia and Bangladesh were all small players in world apparel trade back in the 2009 global financial crisis, they hire hundreds of thousands of garment workers today. As the jobs of these garment workers are under serious threat, the stakes have never been so high.

I think the impact that covid-19 has had so far on the fashion industry as a whole is really eye opening. Thankfully something that we have that is helping some retailers stay afloat is ecommerce. Previous historical events that heavily impacted the fashion industry were during times where e commerce was just beginning. Even though everyone one is suffering during this time, I think fast fashion companies will probably hurt the most. This can definitely be a way to get retailers to understand the negatives to large fast fashion orders. I think during this time something that we should look at is how the virus impacts the way consumers shop after our world starts to recover. Will they continue to be interested in sustainable clothing or are their priorities now shifted to practical necessary clothes due to less disposable income available?

Considering the covid19 circumstances, I was aware that it was going to have negative side effects on the textile and apparel industry, but I never thought about the severity of the effects when combined with the U.S. China trade wars as well. China was already taking an economic and social hit amid the ongoing and increasing trade war, and when then unexpected covi19 hit it took another unimaginable strike. Major countries had already switched most of their sourcing, and covid is only going to speed up that process with possibly other nations joining. I wonder if China will be able to recover, and if not, what other ways they will adapt to make up for lost profit and production? Hopefully they don’t resort to cheaper labor, and as we have seen, poorer work conditions.

good thought and follow-up questions. I think a bigger picture is the trend of “decoupling” of the US-China economic ties, which have been advocated by some US policymakers and scholars for a while. In other words, it may still make sense for US companies to source from China; however, when you also consider other non-economic factors, leaving China became a preferred choice. Here is an interesting article to read: https://www.forbes.com/sites/kenrapoza/2020/04/07/new-data-shows-us-companies-are-definitely-leaving-china/#23c4bd4440fe

The industry survives on consumer demand and with COVID-19 there is no demand for products that are not necessities. I wonder if after the pandemic is over if a globalized structure will still be used as countries will slowly go back to life as it was before the virus? Will countries attempt to produce their own goods as this is a revolutionizing time for the supply chain?

This was a very interesting summary of how the textile apparel industry is affected by COVID-19. It is easy to sympathize with retailers since we hear about their store closures and bankruptcy’s on the news, but there is a ripple affect on the suppliers that these retailers are buying from. A large issue is the cancellations of orders because the repercussions trickle into the next quarters and years. Factories lost so much money on wasted materials and retailers are left scrambling to prepare for next seasons trends. When customers begin to shop again I wonder how the ways they spend money will change. They may be less willing to spend money on quick fashion trends and save their money on essentials. Will fast fashion be able to recover as quickly? Will this be a wake up call that production should be done in smaller batches and should be more diversified?

After reading this blog post at the time of posting and today, a little more than a month later, it is interesting to see what was predicted versus what has come about so far. It was said that EU, The United States and China would see the most drastic impacts in the fashion industry and as of today, the United States and parts of Europe still remain closed as other parts of Europe and China have reopened. I read in an article today from BOF stating that London and NYC remain on lockdown while Milan is on its way to reopen as well as areas of France. With many of the worlds main fashion capitals shut down, what does this mean for factories and suppliers? Will they ever be able to recover from the damages COVID-19 brought upon them? As the stores reopen, it is interesting to think of what the product assortment will be in the stores since the seasons have changed and many orders have been subject to cancellation. The COVID-19 threat will completely redefine the fashion industry and allow us to reshape and evolve the measures put in place.

good thinking! From what I learned, garment factories are hard–they are facing order cancellation AND lockdown measures imposed by their local government. Remember, developing countries are not immune to Covid-19 and in fact, they could be more vulnerable. For example: https://www.business-humanrights.org/en/cambodia-around-400-footwear-workers-protest-to-demand-missing-wages-and-seniority-payments-from-their-employer-while-factory-closes

There is no doubt that this pandemic crisis has affected not only the Textile and Apparel industry, but also global commerce across all industries. That being said, focusing on the Global Trade Analysis model and the three scenarios, all are dire and pessimistic for 2020 and I agree. Scenario 1 and 2 are less pessimistic, with scenario 3 being the most. The truth is nobody knows how quickly global commerce will bounce back. The airline industry does not expect travel demand to the Far East like China and Europe to return to 2019 levels until at least mid 2021. The airlines carry a lot of textile and apparel from exporting countries. As Europe, the US, and the rest of the world come out of lockdown, I feel that scenario 1, the least pessimistic GOP growth model is the most realistic and the economy might even bounce back quicker than even that. The demand for China, Bangladesh, and Vietnamese exports was strong pre covid-19 and after a hopefully 6-month dip, I feel pent up demands will drive exports back to pre covid-19 levels. Sure people and retailers will reevaluate how they buy, sell, and use products, but I think a strong pre covid-19 economy will return quicker than the industry thinks.

This analysis of the textile and apparel industry is such an interesting one. I agree with a comment made above that sustainable companies will potentially be the ones to recover faster. The three main reasons China will have such a hard time recovering make it seem like this could also be a trend for other countries, just on a lesser scale. With China being the country fulfilling most bulk orders, companies will have to search elsewhere to make their garments. Do you think that China will eventually open back up and be able to fulfill those larger scale orders again? Or will all of the companies have moved elsewhere before that can happen.

As the article stated, the steep increase in job loss both in and out of the apparel sector due to Covid-19 is very concerning. On Sunday, the Bureau of Labor Statistics released a statement that reported the unemployment rate is at 14.7%, which is the highest it as been since the Great Depression. This is going to be detrimental to apparel trade and sourcing because consumers aren’t going to have as high of a spending power. People are only going to buy what they need. More specifically, their money is going to go to food, bills, etc. instead of new clothes. It will be interesting to see exactly how the fashion industry is affected in the coming months.

With COVID19, clothing stores were all forced to close down in the mean time while this virus runs its course. In result of this, sourcing orders have been greatly impacted and declined. With china being the largest source of imports for the US and EU, I believe they will take the hit the hardest. The one good thing about this all is that online shopping is still an option. If that were to be wiped out, this whole situation would have been much worse. I wonder how companies are doing with online orders and if they have declined as well. Im interested to see how long this goes on for and what shopping will be like once this is over.

After reading about the affect COVID-19 has on the fashion industry I had never pieced that idea the pressures the industry has especially keeping in mind the trade war that was occurring. As is there was already conflict, to begin with, but now with the pandemic, many parts of both the US and EU have forced retailers to close its stores. With many well-developed countries being economically hit and consumers now in quarantine, the surge in unemployment has caused a tightening in the consumer’s budget. I am curious to see how retailers will handle their sourcing in the months to come. Can the fashion industry prepare to take even larger hits especially in China?

I chose to comment on this post because I find the effects that COVId-19 will cause on the Textile and Apparel Industry to be very interesting. I believe the Pandemic has fundamentally shifted the patterns of world textile and apparel trade. COVID-19 has caused the apparel industry to change tremendously. It has made the production of apparel even harder because the trade industry has been slowed down due to failure to source garment supplies. The slowing down of this process of garment making has cause tons of order cancelations by consumers, causing companies to lose lots of money. I believe that the effects of COVID-19 has escalated into something much bigger than we all might have expected. The way that we have changed our ways of living has become the new norm for some companies. That being said we as students entering the Textile and Apparel Industry in the next couple years, we might not have the opportunity to know experience how the industry functioned before the pandemic. I am interested to see the long term effects of this pandemic.

I very much agree that COVID-19 has had a great impact on employment in many exporting countries, and factories have had to cut jobs in the garment sector during this special period. I would like to know if the clothing imports from the EU and the US can return to normal levels in 2021, and importers and garment factories may have to cope with a new round of labor shortages, then how to reduce work in the clothing sector and cope with the pandemic Then make the most correct choice and decision between labor shortages.