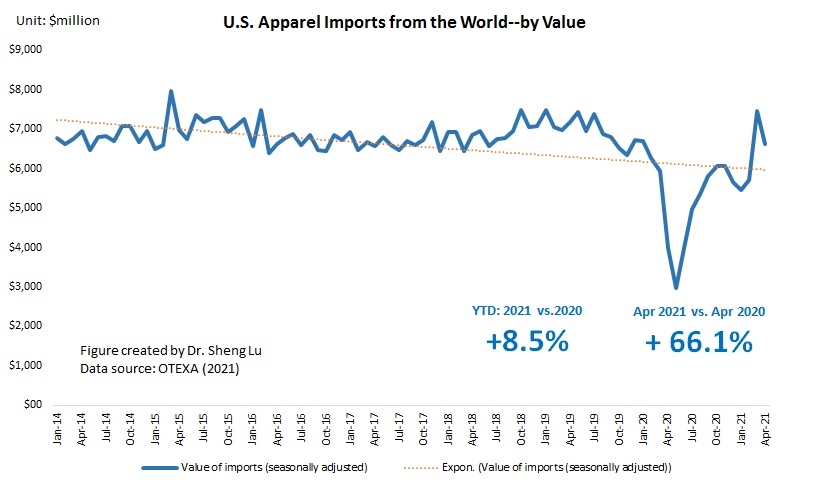

First, thanks to consumers’ resumed demand and a more optimistic outlook for the U.S. economy, U.S. apparel imports continue to rebound. However, uncertainties remain. On the one hand, mirroring retail sales patterns, the value of U.S. apparel imports in April 2021 went up by 66% from a year ago, a new record high since the pandemic. The absolute value of U.S. apparel imports so far in 2021 (January –April) also recovered to around 88% of the pre-Covid level (i.e., January to April 2019). However, the value of U.S. apparel imports in April 2021 was 11.2% lower than in March 2021 (seasonally adjusted), suggesting that the market environment is far from stable yet as the COVID situation in the U.S. and other parts of the world continue to evolve.

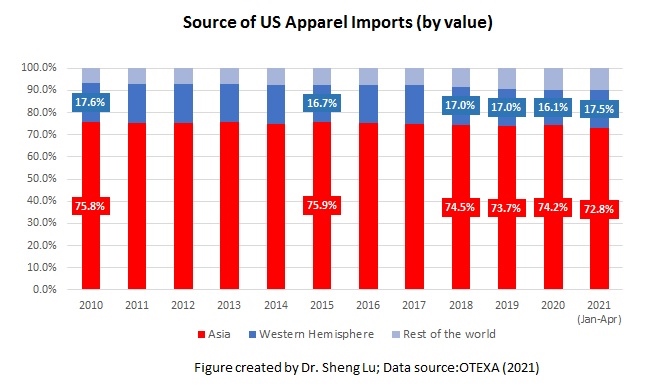

Second, data indicates that Asia as a whole remains the single largest sourcing base for U.S. fashion companies, stably accounting for around 72-75% of the import value. Studies show that two factors, in particular, contribute to Asia’s competitiveness as a preferred apparel sourcing base—price and flexibility & agility. Asia’s highly integrated regional supply chains and its vast production capacity shape its competitiveness in these two aspects.

However, the recent surge of COVID cases in India and its neighboring Southeast Asian countries has raised new worries about the potential sourcing risks and supply chain disruptions for U.S. fashion companies currently sourcing from there.

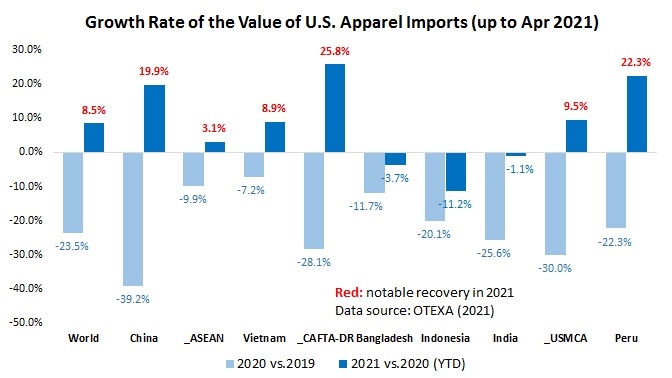

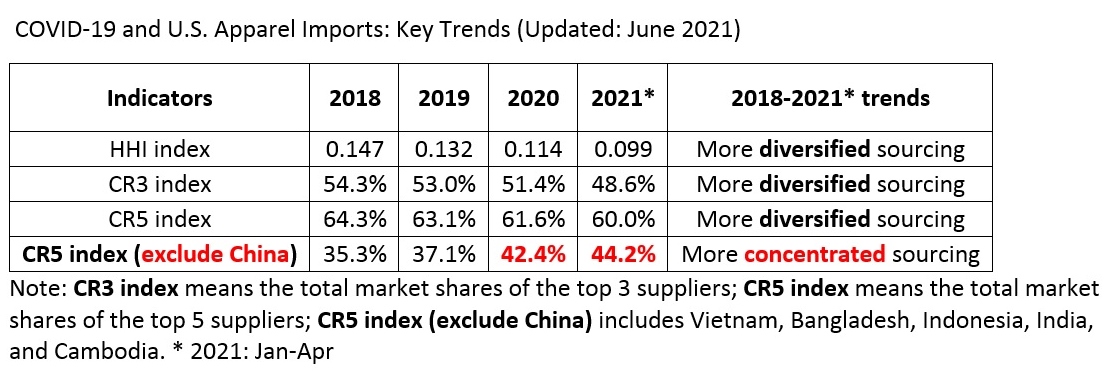

Third, as the direction of the US-China relations becomes ever more concerning, U.S. fashion companies seem to accelerate diversifying sourcing from China. Even China remains the top apparel supplier for the U.S. market, from January to April 2021, China’s market shares fell to 32.1% in quantity (was 36.6% in 2020) and 20.2% in value (was 23.7% in 2020). Also, the HHI index and market concentration ratios (CR3 and CR5) suggest that US fashion companies are increasingly moving their apparel sourcing orders from China to other Asian countries. For example, according to a leading U.S. fashion corporation in its latest annual report, “in response to the recent tariffs imposed by the current US administration, the Company has reduced the amount of goods being produced in China.”

Further, the latest data suggests that the concerns about the alleged forced labor in Xinjiang hurt China’s prospect as an apparel sourcing destination, BOTH for cotton and non-cotton items. Measured by value, only 11.9% of U.S. cotton apparel came from China in April 2021, a new record low since implementing the CBP WROs, which impose a regional ban on any cotton and cotton apparel made in the Xinjiang region. The latest data also suggests that China is quickly losing market shares for non-cotton textile and apparel items.

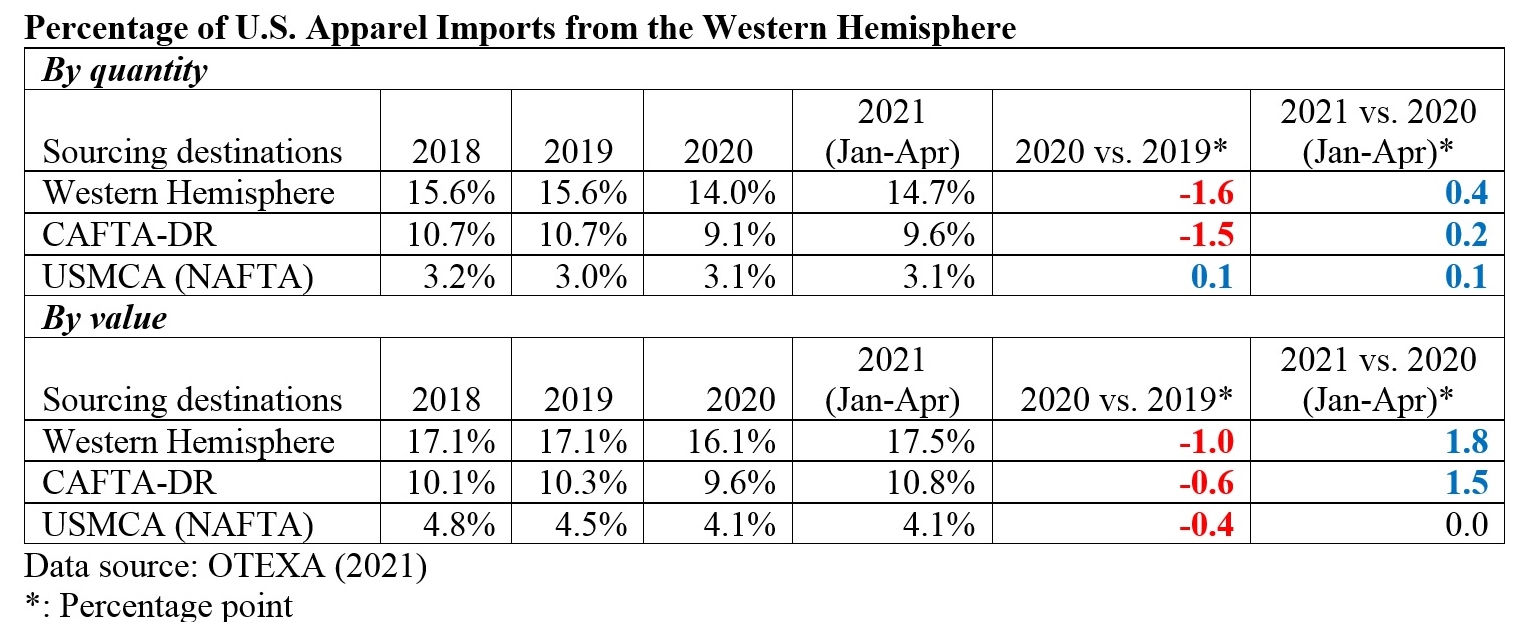

Fourth, U.S. apparel sourcing from CAFTA-DR members gains new momentum, reflecting the strong interest in sourcing more from the region from the business community and policymakers. For example, 17.5% of U.S. apparel imports came from the Western Hemisphere in 2021 (Jan-Apr), higher than 16.1% in 2020 and 17.1% before the pandemic. Notably, CAFTA-DR members’ market shares increased to 10.8% in 2021 (Jan-Apr) from 9.6% in 2020. The value of U.S. apparel imports from CAFTA-DR also enjoyed a 25.8% growth in 2021 (Jan-Apr) from a year ago, one of the highest among all sourcing destinations. The imports from El Salvador (up 29.2%), Honduras (up 28.0%), and Guatemala (27.0%) had grown particularly fast in 2021.

Meanwhile, U.S. apparel imports from USMCA members stayed stable overall. CAFTA-DR and USMCA members currently account for around 60% and 25% of U.S. apparel imports from the Western Hemisphere. They are also the single largest export market for U.S. textile products (around 70%). The Biden administration has signaled its strong interest in strengthening the western hemisphere textile and apparel supply chain by leveraging CAFTA-DR along with other trade policy tools.

by Sheng Lu