Japan has one of the world’s largest apparel consumption markets, with retail sales totaling USD$100bn in 2021, only after the United States (USD$476bn) and China (USD$411bn). Meanwhile, like many other developed economies, most apparel consumed in Japan are imported, making the country a considerable sourcing and market access opportunity for fashion companies and sourcing agents around the globe.

Japanese fashion companies primarily source apparel from Asia. Data shows that Japanese fashion brands and retailers consistently imported more than 90% of clothing from the Asia region, much higher than their peers in the US (about 75%), the EU (50%), and the UK (about 60%). This pattern reflects Japan’s deep involvement in the Asia-based textile and apparel supply chain.

Notably, Japan’s apparel imports from Asia often contain textile raw materials “made in Japan.” Data shows that in 2021, about 65% of Japan’s yarn exports, 75% of woven fabric exports, and 90% of knit fabric exports went to the Asia region, particularly China and ASEAN members. Understandably, in Japan’s apparel retail stores, it is not rare to find clothing labeled “made in China” or “Made in Vietnam” but include phrases like “high-quality luster unique to Japanese fabrics” and “with Japanese yarns” in the product description.

The Global value chain analysis further shows that of Japan’s $5.32 billion gross textile exports in 2017, around 34% (or $1.79 billion) contributed to export production in other economies, mainly China ($496 million), Vietnam ($288 million), South Korea ($98 million), and Taiwan ($92 million).

China remains Japan’s top apparel supplier at the country level. However, Japanese fashion brands and retailers have been diversifying their sourcing base. Since the elimination of the quota system in 2005, China, for a long time, was the single largest apparel supplier for Japan, with an unparalleled market share of more than 80% measured by value. However, as “Made in China” became more expensive, among other factors, China’s market share dropped to 56.4% in 2021. Japanese fashion brands and retailers actively seek China’s alternatives like their US and EU counterparts. Notably, Japan’s apparel imports from Vietnam, Bangladesh, and Indonesia have grown particularly fast, even though their production capacity and market shares are still far behind China’s.

As Japanese fashion companies source from more places, the total market shares of the top 5 apparel suppliers, not surprisingly, had dropped from over 94% back in 2010 to only 82.3% in 2021, measured by value. Similarly, the Herfindahl-Hirschman Index (HHI), commonly used to calculate market concentration, dropped from 0.64 in 2011 to 0.35 in 2021 for Japan’s apparel imports. In other words, Japanese fashion companies’ apparel sourcing bases became ever more diverse.

We can observe the same pattern at the company level. For example, the Fast Retailing Group, the largest Japanese apparel retailer which owns Uniqlo, used to source nearly 100% of its products from China. However, as of 2021, the Fast Retailing Group sourced finished apparel from over 550 factories in more than 20 countries. While about half of these factories were in China, the Fast Retailing Group had strategically developed production capacity in Vietnam, Bangladesh, Indonesia, and India. On the other hand, in April 2021, the Fast Retailing Group opened a 3D-knit factory in Shinonome, allowing the company to re-shoring some production back to Japan.

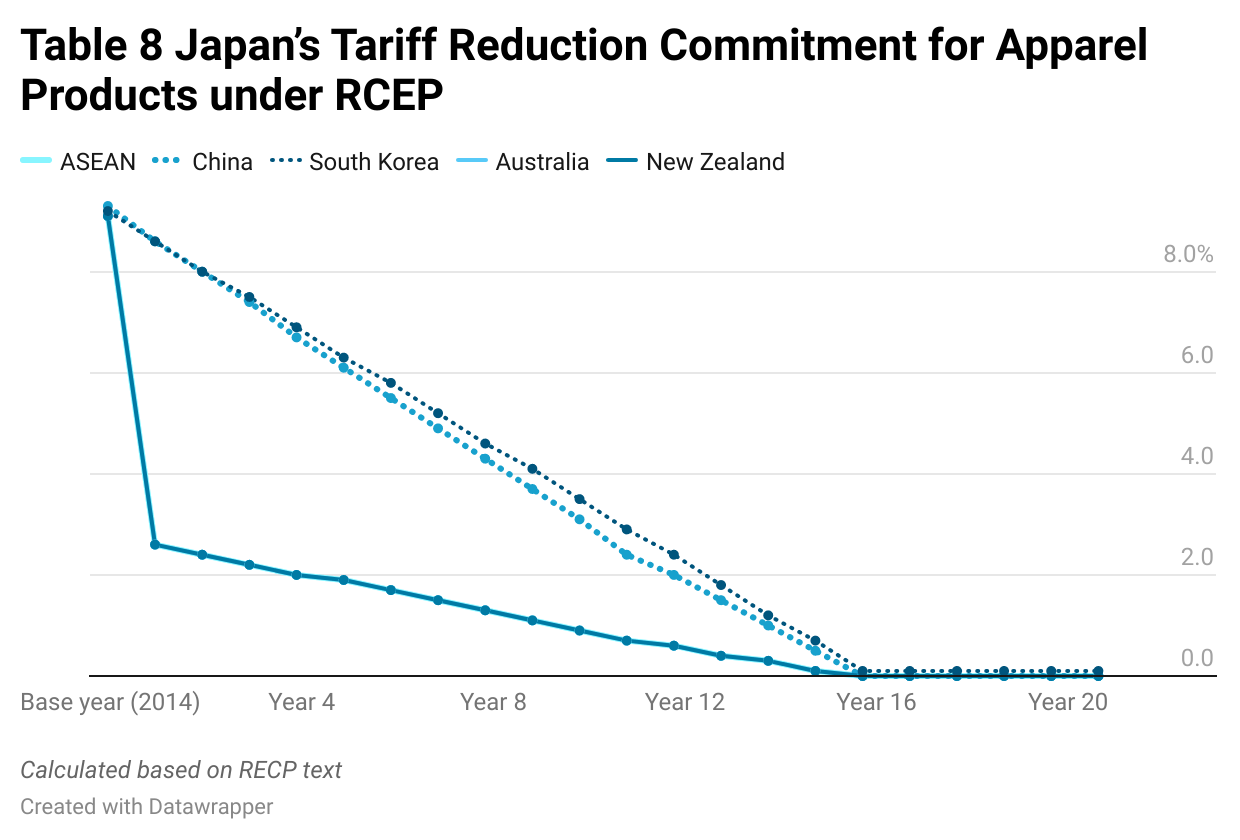

Additionally, Japan is a member of the Regional Comprehensive Economic Partnership (RCEP), the world’s most economically influential free trade agreement. Notably, Japan commits to reducing its apparel import tariffs to zero for RCEP members following a 21-year phaseout schedule. However, as Table 8 shows, Japan’s tariff cut for apparel products is more generous toward ASEAN members and less for China and South Korea due to competition concerns. For example, by 2026, Japan’s average tariff rate will be reduced from 9.1% today to only 1.9% for apparel imports from ASEAN members but will remain above 6% for imports from China. Given the tariff difference, it can be highly expected that ASEAN members such as Vietnam could become more attractive sourcing destinations for Japanese fashion companies.

by Sheng Lu

Further reading: Lu, Sheng (2022). Japan’s apparel market has strong sourcing potential. Just-Style.