First, mirroring the trend of aggregate market demand, the value of UK’s apparel imports has only grown marginally over the past decade. Specifically, between 2010 and 2018, the compound annual growth rate of UK’s apparel imports was close to zero, which was notably lower than 1.4% of the world average, the United States (1.9%), Japan (1.5%) and even the European Union as a whole (1.1%).

Second, UK’s fashion brands and retailers are gradually reducing imports from China and diversifying their sourcing base. Similar to other leading apparel import markets in the world, China was the largest apparel-sourcing destination for UK fashion companies, followed by Bangladesh, which enjoys duty-free access to the UK under EU’s Everything But Arms (EBA) program. Because of geographic proximity and the duty-free benefits under the Customs Union with the EU, Turkey was the third-largest apparel supplier to the UK.

Affected by a mix of factors ranging from the increasing cost pressures, intensified competition to serve the needs of speed-to-market better, the market shares of “Made in China” in the UK apparel import market had dropped significantly from its peak of 37.2% in 2010 to a record low of 21.4% in 2018. However, no single country has emerged to become the “next China” in the UK market. Notably, while China’s market shares decreased by 6.3 percentage points between 2015 and 2018, the next top 4 suppliers altogether were only able to gain 0.7 percentage points of additional market shares over the same period.

Third, despite Brexit, the trade and business ties between the UK and the rest of the EU for textile and apparel products are strengthening. Thanks to the regional supply chain, EU countries as a whole remain a critical source of apparel imports for UK fashion brands and apparel retailers. More than 33% of the UK’s apparel imports came from the EU region in 2018, a record high since 2010. On the other hand, the EU region also is the single largest export market for UK fashion companies.

Fourth, the potential impacts of no-deal Brexit on UK fashion companies’ sourcing cost seem to be modest:

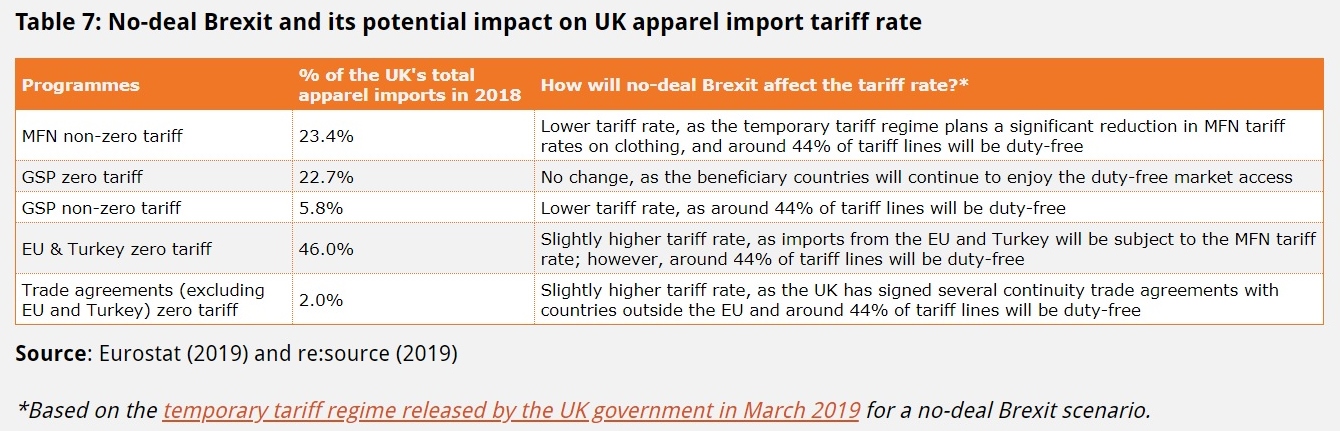

For products currently sourced from countries without a free trade agreement with the EU (such as China) and those Generalized System of Preferences (GSP) beneficiaries that enjoy non-zero preferential duty rates, the tariff rate in the no-deal Brexit scenario will be lower than the current level, as round 44% of tariff lines will be duty-free.

For products currently sourced from countries that enjoy duty-free benefits under the GSP program (such as EBA beneficiary countries), their duty-free market access to the UK will remain unchanged according to the temporary tariff regime.

Products currently sourced from EU countries and Turkey will lose the duty-free benefits and be subject to the MFN tariff rate. However, because around 44% of tariff lines will be duty-free, the magnitude of tariff increase should be modest.

Likewise, products currently sourced from countries that enjoy duty-free benefits under an EU free trade agreement could lose the duty-free treatment and be subject to the MFN tariff rate. However, as around 44% of tariff lines will be duty-free and the UK has signed several continuity trade agreements with some of these countries, the magnitude of tariff increase should be modest overall too. Additionally, these countries are minor sourcing bases for UK fashion companies.

About the authors: Victoria Langro is an Honors student at the University of Delaware; and Dr. Sheng Lu is an Associate Professor in Fashion and Apparel Studies at the University of Delaware.

#1 To which extent should globalization be responsible for Brexit? Does Brexit imply globalization is in retreat? Why or why not?

#2 Why do you think the fashion industry is a stakeholder of “Brexit”? It is said that “some of the world’s poorest countries may end up the victims of Brexit.” Why is that?

#3 The article mentioned the possibility of London losing its reputation as a global fashion capital because of Brexit. What is your evaluation?

#4 Should the UK fashion industry vote for Brexit? Why or why not?

#5 Overall, from the case of Brexit, how do you understand that textile and apparel is a global sector?

[For FASH455: 1) Please mention the question number in your comments; 2) Please address at least TWO questions in your comments]

The UK government on March 13, 2019 released the temporary

rates of customs duty on imports if the country leaves the European Union

with no deal. In the case of no-deal Brexit, these tariff rates will take

effect on March 29, 2019 for up to 12

months.

According to the announced plan, around 87% of UK’s imports by value would be eligible for zero-tariff in the no-deal Brexit scenario.

Specifically for apparel products, 113 out of the total 148 tariff lines (8-digit HS code) in Chapter 61 (Knitted apparel) and 145 out of the total 194 tariff lines (8-digit HS code) in Chapter 62 (Woven apparel) will be duty-free. However, other apparel products will be subject to a Most-Favored-Nation (MFN) tariff rate ranging from 6.5% to 12%.

Meanwhile, the UK will offer preferential tariff duty rates for apparel exports from a few countries/programs, including Chile (zero tariff), EAS countries (zero tariff), Faroe Islands (zero tariff), GSP scheme (reduced tariff rate), Israel (zero tariff), Least Developed Countries (LDC) (zero tariff), Palestinian Authority (zero tariff), and Switzerland (zero tariff).

On the other hand, the EU Commission said it would apply the Most-Favored-Nation (MFN) tariff rates on UK’s products in the no-deal Brexit scenario rather than reciprocate.

On

October 16, 2018, the Trump

Administration notified U.S. Congress its intention to negotiate the

U.S.-EU Free Trade Agreement. Between

2013 and 2016, the United States and EU were also engaged in the negotiation of

a comprehensive free trade agreement– Trans-Atlantic Trade and Investment Partnership

(T-TIP) with the goal to unlock market access opportunities for

businesses on both sides of the Atlantic through the ambitious elimination of

trade and investment barriers as well as enhanced regulatory coherence. The T-TIP

negotiation was stalled since 2017, although

the Trump Administration has never officially announced to withdraw from the

agreement.

II. Negotiating Objectives

On

January 11, 2019, the Office of the U.S. Trade Representative (USTR) released

thenegotiating

objectives of the proposed U.S.-EU Free Trade Agreement after

seeking inputs from the public. Overall, the proposed agreement aims to address

both tariff and non-tariff barriers and to “achieve fairer, more balanced trade”

between the two sides.

Regarding textiles and apparel, USTR says it will secure duty-free access for U.S. textile and

apparel products and seek to improve competitive opportunities for exports of

U.S. textile and apparel products while taking into account U.S. import

sensitivities” during the negotiation. The proposed U.S.-EU free trade

agreement also will “establish origin procedures for the certification and

verification of rules of origin that promote strong enforcement, including with respect to textiles.” T-TIP

had adopted similar negotiating objectives for the textile and apparel sector.

III. Industry viewpoints on the agreement

As of

January 2019, leading trade associations

representing the U.S. apparel industry and the EU textile and apparel industries

have expressed support for the proposed U.S.-EU Free Trade Agreement. In general,

these industry associations recommend the agreement to achieve the following

goals:

First, eliminate import duties. For example:

American

Apparel and Footwear Association (AAFA): “We

support the immediate and reciprocal elimination of the high duties that both

countries maintain on textiles, travel goods, footwear, and apparel.”…” We also

support the immediate elimination of any retaliatory duties imposed by the

E.U., as well as any duties imposed by the U.S. (that led to that retaliation).

The duties impose costs on activities, including manufacturing activities in

the U.S., and undermine markets for U.S. exporters in Europe.”

European

Apparel and Textile Confederation (Euratex):“The

European Textile and Clothing sector faces high tariffs while exporting to the

US market from 11% to up to 32% for some products, namely sewing thread of

man-made filaments, suits, woven fabrics of cotton, trousers and t-shirts. Zero

customs duties while ensuring modern rules of origin will allow EU companies to

boost exports and offer more choice to American consumers and professional

buyers.”

Second, promote regulatory coherence (Harmonization). For example:

AAFA: “The E.U. and the

United States both maintain an extensive array of product safety, chemical management,

and labeling requirements regarding apparel (including legwear), footwear,

textiles, and travel goods.”…” Yet they often contain different requirements,

such as testing or certification, that greatly add compliance costs.”…” We

believe the U.S.‐E.U. trade agreement presents an important opportunity to achieve

harmonization or alignment for these regulations.”

Euratex: “Maintaining high

level of standards while eliminating unnecessary burdens, removing additional

requirements and facilitating customs procedures that impede business are top

priorities. Mutual recognition of the EU and US standards will preserve high

level of consumer protection on both sides of the Atlantic. Convergence on labelling (fibre

names, care symbols and wool labelling),

consumer safety on children products and flammability standards is key for the

T&C sector.” “EURATEX believes the EU and US standardization bodies should

cooperate on setting standards for Smart Textiles taking into account the

industry views for facilitating development and trade of such products of the

future.”

Third, adopt flexible/modern rules of origin. For example:

AAFA: “We should also support higher usage of the agreement by making sure the rules of origin reflect the realities of the industry today…”the yarn forward” rules, although theoretically promote usage of trade partner inputs, in practice they operate as significant barriers that restrict the ability of companies to use a trade agreement in many cases”…” We need to incorporate sufficient flexibilities into the rules of origin so that different supply chains –and the U.S. jobs they support – can take advantage of the agreement.”

Euratex: “Zero customs

duties while ensuring modern rules of

origin will allow EU companies to boost exports and offer more choice to

American consumers and professional buyers.”

The National Council of Textile Organizations (NCTO), which represents the U.S. textile industry, hasn’t publically stated its position on the proposed U.S.-EU Free Trade Agreement. However, NCTO had strongly urged U.S. trade negotiators to adopt a yarn-forward rule of origin in T-TIP. NCTO also opposed opening the U.S. government procurement market protected by the Berry Amendment to EU companies.

IV. Patterns of U.S.-EU textile and apparel trade

The

United States and the EU are mutually important textile and apparel (T&A)

trading partners. For example, the United States is EU’s largest extra-region

export market for textiles, and EU’s fifth largest extra-region supplier of

textiles in 2017 (Euratex, 2018).

Meanwhile,

the EU is one of the leading export markets for U.S.-made technical textiles as

well as an important source of high-end apparel products for U.S. consumers (OTEXA,

2018). Specifically, in 2017, U.S. T&A exports to the European Union

totaled $2,572 million, of which 73.2% were textile products, such as specialty

& industrial fabrics, felts & other non-woven fabrics and filament

yarns. In comparison, EU’s T&A exports to the United States totaled $4,163

million in 2017, among which textiles and apparel evenly accounted for 48.7%

and 51.3% respectively.

V. Potential economic impact of the agreement

By adopting the Global Trade Analysis Project (GTAP) model, Lu (2017) quantitatively evaluated the potential impact of a free trade agreement between the U.S. and EU on the textile and apparel sector. According to the study:

First,

the trade creation effect of the agreement will expand the EU-U.S.

intra-industry trade for textiles. Meanwhile, the agreement is likely to

significantly expand EU’s apparel exports to the United States.

Second,

the trade diversion effect of the U.S.-EU Free Trade Agreement will affect other

T&A exporters negatively, including Asia’s T&A exports to the U.S. market

and EU and Turkey’s T&A exports to the EU market.

Third, the U.S.-EU Textile and Apparel Trade might affect the intra-region T&A trade in the EU region negatively but in a limited way.

Overall, the study suggests that the EU T&A industry will benefit from the additional market access opportunities created by the U.S.-EU Free Trade Agreement.One important factor is that the U.S. and EU T&A industries do not constitute a major competing relationship. For example, the United States is no longer a major apparel producer, and EU’s apparel exports to the United States fulfill U.S. consumers’ demand for high-end luxury products. The U.S.-EU Free Trade Agreement is also likely to create additional export opportunities for EU textile companies in the U.S. market, especially in the technical textiles area, which accounted for approximately 40% of EU’s total textile exports to the United States in 2017 measured in value. Compared with traditional yarns and fabrics for apparel making purposes, technical textiles are with a greater variety in usage, which allows EU companies to be able to differentiate products and find their niche in the U.S. market.

Further, the study suggests that we shall pay more attention to the details of non-tariff barrier removal under the U.S.-EU Free Trade Agreement, which could result in bigger economic impacts than tariff elimination.