This video is a great reminder of the impact of our fashion apparel industry, in particular through trade and sourcing. One key learning objective of FASH455 is to help students get aware of those critical global agendas that are highly relevant to the textile and apparel sector.

Discussion Question: After watching the video, do you have any new thoughts about how you can contribute to the building of a better world as a FASH major?

The latest Just-Style State of Sourcing Survey conducted in December 2016 suggests a few trends of apparel sourcing in 2017:

Exchange rate volatility and rising raw material and labor costs are among the top concerns for apparel sourcing in 2017. Around 69% of survey respondents expect overall sourcing costs to rise in 2017, compared with 54.5% in last year’s survey. The fluctuating exchange rate, buyer’s expectation for higher quality of products and complex compliance requirements are among the major factors driving up the sourcing cost.

Apparel companies expect more uncertainties regarding the political and policy environment in 2017. Specific concerns for apparel companies include trade policy under Trump’s Administration, possible renegotiation of trade agreements such as the North American Free Trade Agreement (NAFTA) and Trump’s threats to impose a 45% punitive tariff on US textile and apparel imports from China. Respondents say the uncertainties make it challenging for companies to do strategic planning in advance

Sourcing will play an increasingly important role helping companies achieve strategic goals. It is highly expected that sourcing can contribute to meeting the fast-evolving demands of omni-channel retailing, consumers’ expectations for a more convenient shopping experience, as well as greater product innovation across all sales channels. A few respondents say they will use process and productivity improvement and closer collaboration with key suppliers to try to achieve these goals and mitigate any sourcing cost increases.

Sourcing destinations may continue to slightly adjust in 2017. Specifically, 72.1% of respondents say they are looking for alternative source of supply in 2017 compared with 69.2% last year. Popular emerging sourcing destinations include Central America and the United States, EU, UK, Vietnam, Bangladesh, Indonesia and Kenya. However, the survey also confirms that China‘s dominance as the top apparel supplier is unlikely to change anytime soon – with a rise in the number of respondents looking to increase orders from the country in the upcoming year.

Respondents of the survey include manufacturers (29%), importers, agents or sourcing office executives (23%), retailers (12%), fiber, yarn, or fabric suppliers (11%), consulting, research, government, trade institute, NGO and university fields (14%) and software suppliers (2.6%).

First, TPP is suggested to have a limited impact on U.S. domestic textile and apparel manufacturing, because:

1) Automation rather than imports is found to be the top factor causing job losses in the U.S. textile industry in the past decade;

2) U.S. is one of the very few TPP members whose textile output mostly went into home textiles, floor coverings and other technical textile products rather than apparel.

3) More than 90% of apparel sold in the United States is already imported. Some companies maintain U.S. manufacturing of high-value products or products requiring quick delivery, which are not likely to be supplied by other TPP members.

4) A quantitative assessment conducted by the U.S. International Trade Commission (USITC) in May also suggests that U.S. imports of textiles will only climb 1.6% by 2032 if TPP enters into force in 2017. Over the same 15-year period, both output and employment in the U.S. textile industry could slightly shrink by 0.4% as a result of the implementation of TPP.

Second, TPP could challenge the Western-Hemisphere supply chain and negatively affect U.S. textile exports to the region:

1) TPP will make apparel manufacturers located in Mexico and Central America lose one important advantage—duty free access to the U.S. market, when competing with Asian TPP members such as Vietnam and Malaysia. The Central American-Dominican Republic Apparel and Textile Council also estimates the CAFTA-DR region could see a contraction of 15%-18% in industrial employment resulting from lost production orders in the first year after the TPP agreement is implemented.

2) The major products sourced by U.S. apparel companies from the Western Hemisphere region include basic, low-value knitwear garments such as shirts, pants, underwear, and nightwear, with a focus on men’s and boys’ wear. However, these products are with low time sensitivity but high price sensitivity, meaning Asian TPP members can easily offer a more competitive price and take away sourcing orders after the implementation of TPP.

3) Because of physical distance and abundance of local supply, leading Asian TPP apparel exporters such as Vietnam seldom use US-made yarns and fabrics. Supported by foreign investments, Vietnam is also quickly building up its own textile manufacturing capacity, which is expected to reach 2 million metric tons for fabrics and 650,000 metric tons for fibers by 2020. This implies that TPP may help little creating new export markets for US textile products, despite the restrictive yarn forward rules of origin.

Additionally, TPP could result in intensified competition in the technical textile area, which is of strategic importance to the future of the U.S. textile industry:

1) If the proposed agreement is implemented, those segments of the U.S. textile industry that supply industrial textiles are likely to face greater competition from rising imports from Japan.

2) TPP will allow Japanese industrial textiles to newly get duty free access to Mexico and Canada, which are the largest export markets for U.S. industrial fabrics in 2015. However, TPP won’t help US companies get more favorable access to China, which is the top export market for Japanese industrial fabrics.

Sourcing is turning from regional to global. In the past, U.S. apparel companies/fashion brands set up regional offices to handle sourcing. Nowadays, companies are building a global infrastructure to develop, source and market their products around world. Global rather than regional sourcing also allows companies to improve sourcing efficiency and reduce total product and distribution cost while maintaining quality of their product and services.

U.S. apparel companies/fashion brands are going with fewer but more capable vendors (“super vendors”). For example, executive from a leading U.S. apparel brand said their company has shrunk their sourcing base by 40% in the past few years. At the same time, they now expect their vendors to be able to supply on a global scale, including having multiple manufacturing facilities around the world and being able to provide value added services such as design and product development.

Related, sourcing is shifting from cut-make-and trim (CMT) to full package. This is consistent with our findings in the latest USFIA benchmarking studywhich suggests that vendors are highly expected to have the capacity of supplying raw material.

U.S. apparel companies/fashion brands are also investing to build a more partnership-based relationship with vendors— help vendors reduce cost, become more innovative and have the same vision looking at the whole picture of the supply chain. At the same time, U.S. apparel companies/fashion brands see vendors as their “ambassadors” and want to know more about them—what they believe, what they can bring to the table and how they treat their workers.

Companies are redefining the role of sourcing in their businesses. Sourcing is no longer treated as a technical function, but an integral part of a company’s overall business strategy.

Made in USA

There is a noticeable interest in sourcing textiles and apparel “Made in USA” at Magic. A dozen U.S.-based apparel companies attended the Magic show and their booths attracted a heavy traffic. According to representatives from these companies, U.S. consumers’ increased demand for apparel “Made in USA” has been a strong support for their business growth in recent years.

Nevertheless, apparel “Made in USA” often contain imported inputs today. I specifically asked a few vendors where their fabrics come from. All but one company said fabrics were imported because it was so hard to find domestic suppliers, especially for woven fabrics. Interesting enough, some companies feel OK to label their apparel “Made in USA” even though they use imported fabrics. According to them, apparel can be labeled “Made in USA” as long as “domestic content exceeds 60% of the value of the finished product.”

At a seminar, some entrepreneurs which make and sell “Made in USA” apparel and accessories said price and production cost remain one of their top business challenges. I asked the panel whether going high-end is the only option for the future of apparel “Made in USA” given the high labor cost in the country. They disagreed—saying technology advancement and design innovation could help reduce production cost. However, all panelists admit they carry some luxury product lines. Additionally, some companies choose to emphasize concepts other than “Made in USA”, such as “hand-made” and “Pride in Seattle”, in order to make their products look more personal to consumers and allow more flexibility in sourcing raw material.

Updates of sourcing destinations

Ethiopia: as I observe, Ethiopia is THE star at this year’s Sourcing at Magic. The country was repeatedly mentioned by panelists at various seminars as a promising and emerging sourcing destination. Several events at the show were also exclusively dedicated to promoting apparel and footwear “Made in Ethiopia”. A couple of reasons why Ethiopia is so “hot”: 1) the ten year extension of AGOA creates a stable market environment encouraging sourcing from Africa and investing in the region (and for sure the duty free access both to the US and EU market). 2) Located in the middle of Africa, Ethiopia is regarded as a hub that has the potential to take a leadership role in integrating the apparel supply chain in the region. 3) It is said that Ethiopian government is very supportive to the development of the local textile industry. 4) Many U.S. fashion companies feel sourcing from Ethiopia involves less risks of trade compliance than sourcing from some Asian countries such as Bangladesh.

China: China unarguably remains the No.1 textile and apparel supplier to the U.S. market—in terms of numbers, around 60% vendors at the Magic show came from China. But I notice that booths of Chinese vendors didn’t have much traffic this time, an interesting signal for sourcing trend in the upcoming season. Nevertheless, while U.S. apparel companies/fashion brands are placing more emphasis on supply chain efficiency, quality of products, speed to market and added value in sourcing, “Made in China” will continue to enjoy many unique advantages over other suppliers. Plus, Chinse factories are actively investing overseas, from Southeast Asian countries to Africa. This makes Chinese factories likely to grow into “super vendors” that western fashion brands/retailers are looking for. To certain extent, macro trade statistics alone may not be able to fully reveal what is going on in apparel sourcing and trade.

Vietnam: Regarding the future of Vietnam as a sourcing destination for U.S. apparel companies/fashion brands, somehow I hear more concerns than excitements at Magic. The uncertainty surrounding the ratification of TPP by the U.S. Congress definitely has made some companies hold back their investment and sourcing plan in Vietnam. Another big concern is Vietnam’s labor shortage and limited manufacturing capacity: apparel factories in Vietnam are already competing with electronic industry for young skilled workers. US companies also have to compete with their EU counterparts for orders in Vietnam. The newly reached EU-Vietnam Free Trade Agreement (EVFTA), which is very likely to be implemented earlier than TPP, provides Vietnam duty free access also to the EU market. And EVFTA adopts a much more flexible rule of origin than TPP, making it easier for Vietnam factories to actually use the agreement.

Sustainability

The awareness of social responsibility and sustainability has much improved: everyone in the industry is talking about them and have a view on them. On a voluntary basis, some companies are making efforts to improve traceability of their products, i.e. to help consumers know exactly where their clothing comes from and what is happening at the upstream of the supply chain. Yet, how to encourage factories to share their information and control tier 2 and tier 3 suppliers remain a challenge.

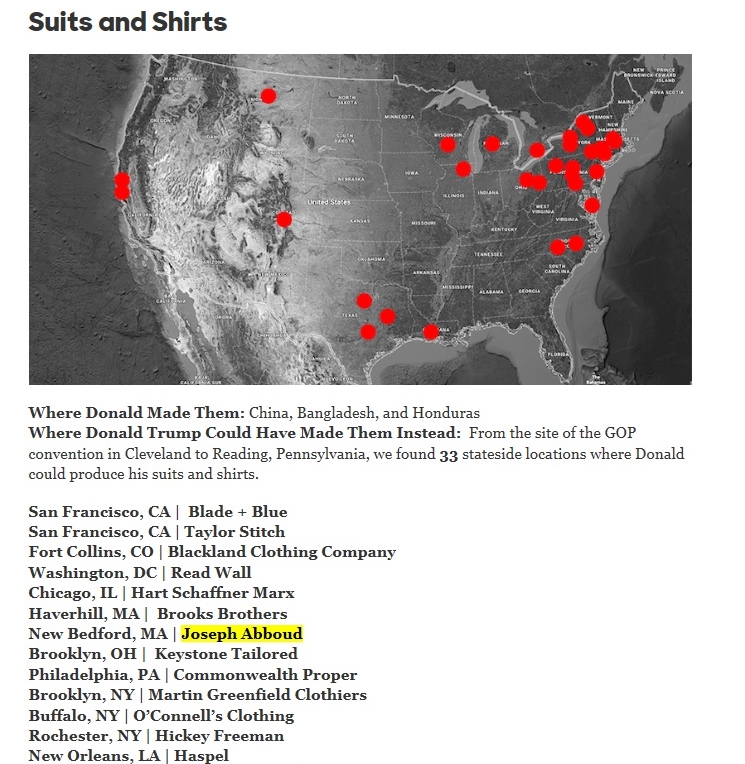

Presidential candidate Hillary Clinton recently launched a new website “Made In America: A Buyer’s Guide for Donald Trump”, which highlighted hundreds of U.S. manufacturers for products ranging from men’s ties, suits to furniture.

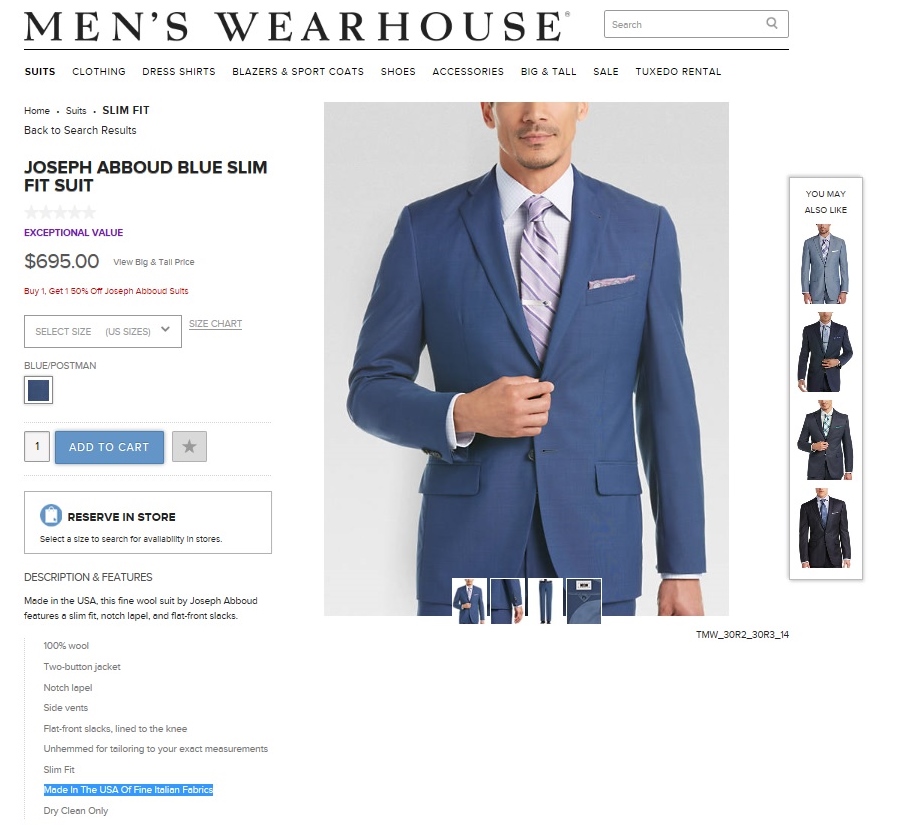

Joseph Abboud is one of the companies highlighted by the website for making “Made in America” suites and shirts. But does “Made in America” mean a Joseph Abboud branded suit or shirt is 100% made in the United States from yarns, fabrics to the cut-and-sew process? Not necessarily!

This is evidenced both by Joseph Abboud’s product label and information provided by some retailers which sell Joseph Abboud’s branded products (See pictures below).

Hamilton Shirts of Houstonis another company highlighted by Clinton’s “Made in USA” website. But similar as the case of Joseph Abboud, a Hamilton branded shirt priced at $215-$245 is typically “Hand cut and sewn in the USA. 100% cotton Italian fabric.”

Actually, Joseph Abboud is a brand owned by JA Holding, Inc., which was acquired by Tailored Brands for $94.9 million on August 6, 2013. As of June 2016, Tailored Brands also owns the Men’s Wearhouse and Jos. A. Bank.

Like most other US apparel companies/fashion brands today, Tailored Brands commits to global sourcing. In fiscal year 2015, the company “sourced approximately 60% of direct sourced merchandise from Asia (36% from China) while 13% was sourced in the U.S., 12% in Mexico, and 15% was sourced in other regions.” (Source: Tailored Brands Annual Report, 2015)

Tailored Brands uses the factory in New Bedford, MA (the one highlighted by Clinton’s website) to make tailored clothing under the Joseph Abboud label, including designer suits, tuxedos, sport coats and slacks which they sell in Men’s Wearhouse stores as well as Joseph Abboud’s flagship store. Tailor Brands also sells Joseph Abboud branded products in Moores stores, which are made in Canada by a third party.

Disclaimer: All blog posts on this site are for FASH455 educational purposes only and they are nonpolitical and nonpartisan in nature. No blog post has the intention to favor or oppose any particular presidential candidate, nor shall be interpreted in that way.

How are Chinese garment factories coping with the challenges of rising labor cost?

Is adopting Taylor’s “scientific management”, i.e. asking skilled workers to do less skilled jobs in a more specialized production line, a smart idea?

What is your view on the growing difficulty of hiring and retaining young skilled workers for the garment industry in China?

Any other thoughts on the video?

Appendix: State of China’s Apparel Exports in 2015

According to the UNComtrade, China remains the world’s largest apparel exporter in 2015 (37.4% world share for knitted apparel, HS61 and 34.9% for woven apparel, HS62).

From 2011 to 2015, “Made in China” continues to acquire more market shares in some key apparel import markets in the world, including the United States and UK (i.e. China’s apparel exports to these markets grew at a faster rate than these countries’ apparel import growth from the world—bubbles in blue in the figures below). Nevertheless, in some other markets (bubbles in yellow in the figures below), notably Japan and Germany, China is losing market shares to other garment exporters such as Vietnam and Bangladesh.

I. Business environment and outlook in the U.S. Fashion Industry

Overall, respondents remain optimistic about the five-year outlook for the U.S. fashion industry. “Market competition in the United States” is ranked the top business challenge this year, which, for the first time since 2014, exceeds the concerns about “increasing production or sourcing cost.”

II. Sourcing practices in the U.S. fashion industry

U.S. fashion companies are more actively seeking alternatives to “Made in China” in 2016, but China’s position as the No.1 sourcing destination seems unlikely to change anytime soon. Meanwhile, sourcing from Vietnam and Bangladesh may continue to grow over the next two years, but at a slower pace.

U.S. fashion companies continue to expand their global reach and maintain truly global supply chains. Respondents’ sourcing bases continue to expand, and more countries are considered potential sourcing destinations. However, some companies plan to consolidate their sourcing bases in the next two years to strengthen key supplier relationships and improve efficiency.

Today, ethical sourcing and sustainability are given more weight in U.S. fashion companies’ sourcing decisions. Respondents also see unmet compliance (factory, social and/or environmental) standards as the top supply chain risk.

III. Trade policy and the U.S. fashion industry

Overall, U.S. fashion companies are very excited about the conclusion of the Trans-Pacific Partnership (TPP) negotiations and they look forward to exploring the benefits after TPP’s implementation.

Thanks to the 10-year extension of the African Growth and Opportunity Act (AGOA), U.S. fashion companies have shown more interest in sourcing from the region. In particular, most respondents see the “third-country fabric” provision a critical necessity for their company to source in the AGOA region.

Free trade agreements (FTAs) and trade preference programs remain underutilized in 2016 and several FTAs, including NAFTA and CAFTA-DR, are utilized even less than in previous years. U.S. fashion companies also call for further removal of trade barriers, including restrictive rules of origin and remaining high tariffs.

The benchmarking study was conducted between March 2016 and April 2016 based on a survey of 30 executives from leading U.S. fashion and apparel brands, retailers, importers, and wholesalers. In terms of business size, 92 percent of respondents report having more than 500 employees in their companies, while 84 percent of respondents report having more than 1,000 employees, suggesting that the findings well reflect the views of the most influential players in the U.S. fashion industry.

I encourage everyone to watch these two short videos, which provide a great summary of FASH455 and remind us the true meaning of our course.

First and foremost, FASH455 is not designed to be a course which just technically talks about textile and apparel (T&A) trade and how to source T&A products. Yes, from various trade theories, evolution pattern of the global T&A industry, T&A regional production and trade network to the flying geese model, we do cover a lot of factual knowledge and theories in FASH455, because this is a highly professional area. But please keep in mind that the vision and perspective set for FASH455 are much higher and critical, that is:

What role can the textile and apparel industry play in building a better world—how to reduce poverty, achieve economic growth, promote human development, enhance sustainability and contribute to world peace and security?

What does it mean as a FASH major (as well as a college graduate)? What can we positively contribute to the world we are living today?

By the same token, I hope students realize that the most meaningful thing you can take away from the course is a fresh new way (perspective) of looking at the world and recognizing the critical 21st century global agendas that are closely connected with our T&A industry. For example:

How to more equally distribute the benefits & cost of globalization among different countries and groups of people?

How to make sure that tragedies like the Rana Plaza building collapse will never happen again?

How to make international trade work better and more effectively lead to economic growth and human development?

How to achieve sustainability while develop the economy? To which extent shall we renovate the conventional growth model?

How to use trade policy as a tool to solve some tough global issues such as labor practices and environmental standard?

For many of these questions, there is no good answer yet. But they are waiting for you, the young professional and new generation of leaders, to find an answer and write the history, based on your knowledge, wisdom, responsibility, courage and creativity!

What do you take away from FASH455? Please feel free to share your thoughts and comments.

(In the video: Gail Strickler, former Assistant US Trade Representative for Textiles, highlights the immense opportunities created by the renewal of AGOA for duty-free access to the massive US market for African textile and apparel producers.)

The African Growth and Opportunity Act (AGOA) is a non-reciprocal trade agreement enacted in 2000 that provides duty-free treatment to U.S. imports of certain products from eligible sub-Saharan African (SSA) countries. AGOA intends to promote market-led economic growth and development in SSA and deepen U.S. trade and investment ties with the region. (note: non-reciprocal means SSA countries do not need to offer equivalent benefits to imports from the United States.)

Because apparel production plays a dominant role in many SSA countries’ economic development, apparel has become one of the top exports for many SSA countries under AGOA. Like many trade agreements and trade preference programs, AGOA also set unique rules of origin for textile and apparel (T&A):

First, to enjoy the duty-free and quota-free treatment in the US market, eligible T&A products made in qualifying AGOA countries need to be one of the following categories:

Apparel made with US yarns and fabrics;

Apparel made with Sub-Saharan African (SSA) regional yarns and fabrics, subject to a cap;

Apparel made with yarns and fabrics not produced in commercial quantities in the United States;

Certain cashmere and merino wool sweaters; and

Eligible hand-loomed, handmade or folklore articles and ethnic printed fabrics.

Second, under a special rule called “third-country fabric” provision, AGOA countries with lesser-developed countries (LDBC) status can further enjoy duty-free access in the US market for apparel made from yarns and fabric originating anywhere in the world (such as China, South Korea, and Taiwan). This special rule is deemed as critical because most SSA countries still have no capacity in producing capital and technology-intensive textile products. [Note: Although the US imports of apparel made with third-country fabric are subject to a cap, the cap has never been reached].

1) Increase exports of apparel. This can be evidenced by the fact that most US apparel imports under AGOA came from those countries that are eligible for the “third-country fabric” provision, such as Lesotho, Kenya, Mauritius, and Swaziland. In comparison, because South Africa is not eligible for the “third-country fabric” provision, its apparel exports to the United States had significantly dropped since 2003 and only accounted for 0.6% among AGOA countries in 2013.

2) Encourage foreign investment. From 2003 to 2013, a total 21 T&A FDI projects were made in SSA, among which 18 projects (or 85.7%) were greenfield FDI. The third-country fabric provision is the main driver for these FDI projects. For example, many Chinese and Taiwanese investors had opened apparel factories in Ghana, Kenya, Lesotho, Madagascar, Malawi, Mauritius, Namibia, Nigeria and Tanzania as a source of exports to the United States and the EU.

3) Enhance trade diversification. Theoretically, relaxing rules of origin (RoO) such as the third-fabric provision can free up companies’ resources and allow them to expand export product lines. As observed by a few empirical studies, AGOA’s third-country fabric provision helped related countries increase the varieties of apparel exports between 39 and 61 percent.

AGOA receives new authorization in 2015, which will last for 10 years until 2025 (including the 3rd country fabric provision). This ten-year renewal of AGOA is regarded as critical and necessary to encourage more long-term investment in the region. As put by Florizelle Liser, Assistant US Trade Representative for Africa “What we know is that African producers of apparel, like producers of apparel all around the world, need to have the flexibility to source their input from wherever of those can be produced most effectively, cost effectively for the products that they are sewing. So we want through the “third country fabric” provision to give the African producers of apparel that flexibility. We do know in terms of establishing textiles business on the ground producing those inputs right there in Africa and that more of that indeed is going to happen. The reason is that as U.S. buyers of apparel and this is an enormous market for apparel… as U.S. buyers of apparel source more of their apparel from Africa, then investors in textile mills, which are very expensive, will be incentivized and are being incentivized to actually establish those fabric mills right there in Africa, and then be able to save time, in terms of getting those inputs that are needed for the clothing that is being produced. So we see that happening already: it’s happening in Kenya, it’s happening in Ethiopia and around the continent. And that is what we need to have more of as we go forward in this ten-year extension of AGOA.”

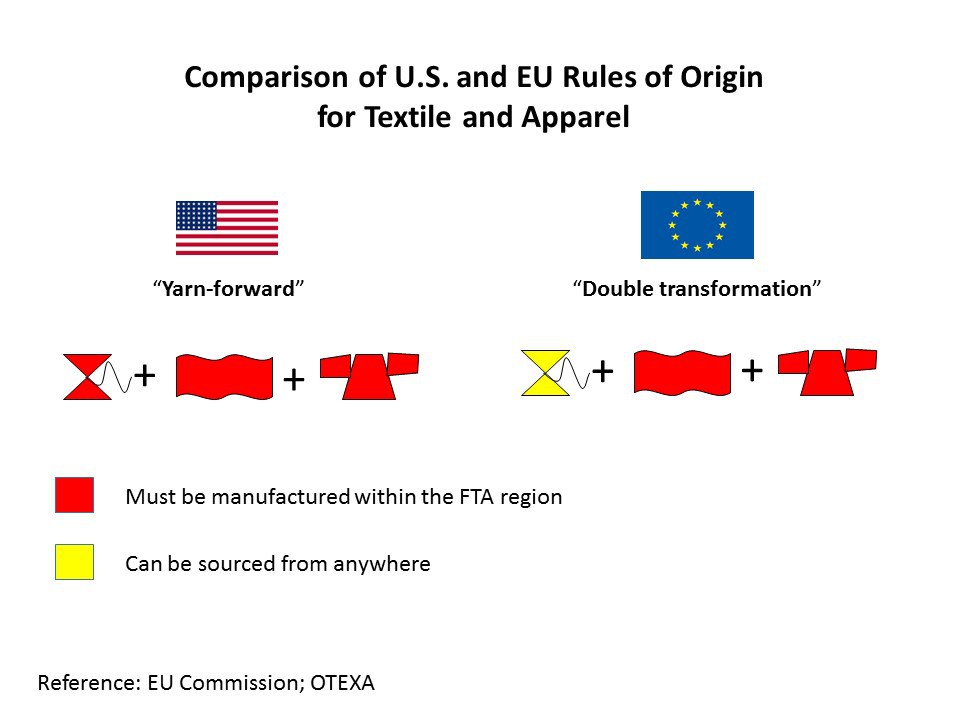

In an April 13 press briefing, the National Council of Textile Organizations (NCTO) which represents the U.S. textile industry, insists the Trans-Atlantic Trade and Investment Partnership (T-TIP) shall adopt the so called “yarn-forward” Rules of origin (RoO). Yarn-forward (or “triple transformation”) in T-TIP means, in order to receive preferential duty treatment provided under the trade agreement, yarns used in textile production in general need to be sourced either from the US or EU. All 14 existing free trade agreements (FTA) in the United States adopt the yarn-forward RoO.

In comparison, in its position paper released in June 2015, the European Apparel and Textile Confederation (Euratex), which represents the EU textile and apparel industry, favors a so called “fabric forward” RoO in T-TIP instead of “yarn-forward”. Fabric-forward (or “double transformation”) in T-TIP means in order to receive preferential duty treatment provided under the trade agreement, fabrics used in apparel production in general need to be sourced either from the US or EU, but yarns used in textile production can be sourced from anywhere in the world.

Exploring data at the 4-digit NAICS code level can find that the United States remains a leading yarn producer. Value of U.S. yarn production (NAICS 3131) even exceeded fabric production (NAICS 3132) in 2014. This means: 1) U.S. has sufficient capacity of yarn production; 2) it will be in the financial interests of the U.S. textile industry to encourage more use of U.S.-made yarns in textile production in the T-TIP region (i.e. pushing the “yarn-forward” RoO).

However, data at the 4-digit NACE R.2 code level suggests that EU(28) was short of €5,643 million local supply of yarns (NACE C1310) for its manufacturing of fabrics (NACE C1320) in 2013 (latest statistics available). This figure well matched with the value of €4,514 million yarns that EU (28) imported from outside the region that year. Among these yarn imports (SITC 651), over half came from China (22%), Turkey (19%) and India (13%), whereas only 5% came from the United States. Should the “yarn-forward” RoO is adopted in T-TIP, EU textile and apparel manufacturers may face a shortage of yarn supply or see an increase of their sourcing & production cost at least in the short run.

The following discussion questions are proposed by students enrolled in FASH455 (Spring 2016). Please feel free to join our online discussion.

#1 Is TPP successful in terms of “creating new market access opportunities” for the U.S. textile and apparel industry? Why or why not?

#2 Should the U.S. textile industry be worried that Vietnam is quickly building its own textile industry because of TPP?

#3 Compared with the case of Vietnam in TPP, why was there little discussion on Mexico and Central American countries developing their local textile industry and becoming less reliant on textile imports from the United States in the context of NAFTA and CAFTA-DR?

#4 If China joins the TPP, do you think they would support a “yarn-forward” rules of origin or a less restrictive one? Why?

#5 Given the grave concerns about the potential impact of TPP on the U.S. textile industry, what is the point of negotiating such a trade deal?

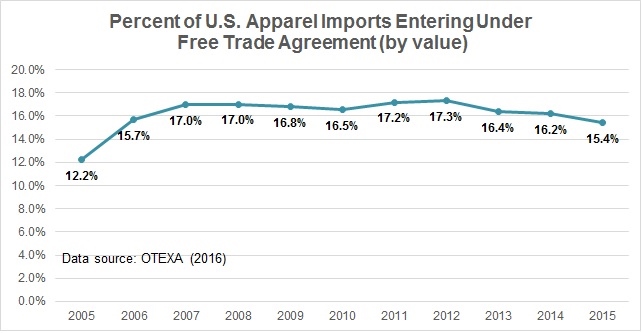

Latest statistics from the Office of Textiles and Apparel (OTEXA) show that the share of U.S. apparel imports entering under free trade agreements (FTAs) fell to a record low level of only 15.4 percent in 2015. This figure was not only lower than 16.2 percent in 2014, but also was THE lowest one since 2006, despite the implementation of a few new FTAs during that period.

Among the major FTAs reached by the United States, the U.S.-Bahrain has the highest utilization rate of 99.7 percent in 2015 (note: utilization rate =value of imports entering under FTA from a particular country/value of imports from a particular country), whereas a couple of FTAs whose utilization rate is below 80 percent, such as CAFTA-DR (75.8 percent), U.S.-Korea FTA (75.2 percent), U.S.-Israel FTA (65.5 percent), U.S.-Australia FTA (53.7 percent) and U.S.-Morocco FTA (34.6 percent). A low utilization rate implies that U.S. companies did not claim the preferential duty benefits while importing apparel from these FTA regions.

On the other hand, CAFTA-DR and NAFTA altogether account for around 76 percent of U.S. apparel imports entering under FTAs in 2015. This result is consistent with the findings in the 2015 U.S. Fashion Industry Benchmarking Study which also finds that CAFTA-DR and NAFTA were the two most frequently utilized FTAs reported by the survey respondents.

As a result of the lower share of apparel imports entering under FTAs, the American Apparel and Footwear Association Apparelstat 2015 released this week found that the effective average U.S. apparel import duty reached 13.54 percent in 2014, which is even higher than 11.97 percent in 2001. In comparison, over the same period, the average U.S. import duty on ALL products dropped from 1.64 percent in 2001 to 1.40 percent in 2014.

The following questions are proposed by students enrolled in FASH455 Spring 2016. Please feel free to leave your comment and engage in our online discussion.

L.L Bean: A Business Model for “Made in USA”?

L.L. Bean has been a strong business for hundreds of years, yet recently their sales of Bean Boots have skyrocketed because they are now seen as trendy. Even though L.L. Bean’s orders and demand has gone up, they still somehow manage to have their products being handmade, sourced locally, and all in the US.

#1: Can L.L. Bean become a model for other businesses looking to manufacture in the US? How has L.L. Bean managed to keep this business model up for so many years and why have they not changed or decided to outsource?

#2: Why doesn’t L.L Bean look into other American cities for manufacturing options so they do not lose productivity by being exclusively made in Maine?

#3: Do you think it would be beneficial for L.L. Bean to outsource to foreign companies for their manufacturing? Would there still be as high of a demand if these boots were manufactured abroad?

Outsourcing v.s. “Made in USA”

#4: It is said that one reason why American brands choose to offshore their manufacturing is because there isn’t as many cutting edge machines readily available in the States as in other countries. Is it realistic for the American manufacturing market to invest in these machines for domestic manufacturing? If so, how can America make sure to stay relevant with these technologies and not fall behind as we have currently?

#5: One aspect commonly mentioned throughout these readings was the lack of skilled labor in the US in the fashion industry. Is the decrease in skilled areas, such as shoemaking and needle trade, due to the increase in skilled labor overseas? Are these professions considered outdated for young Americans to be learning? How can we jumpstart a desire for young people to take up these skills once again?

#6: One major problem the US has been facing regarding keeping production domestic has been the lack of skilled workers to work in factories. Is the cost of providing training to interested workers too high? Should it be required that all fashion majors should take a sewing class? Where does the decision to train apparel workers begin?

#7: Many American manufacturers refrain from manufacturing in the United States because it is too expensive because more people are formally educated and are not willing to work for a low wage, but only 15% of respondents actually are working towards that. Is it realistic to reach out to homeless communities looking to get back onto their feet to see if they would work in factories? Would this help promote American manufacturing and decrease importing?

#8: In today’s fast paced fashion world, trends come and go rather quickly. The striking disadvantage of manufacturing overseas is the slow turnaround time which could be up to 3-5 months. By manufacturing domestically, turnaround can be as quick as 2 weeks. Why do the majority of fashion companies still choose to manufacture overseas when there is a possibility the trend could be over by time they reach store shelves (Thus, a lack in profit)? When will trend pressures become too much for overseas production?

#9: Is it even worth it to bring manufacturing back to America if it is not benefitting the workers and creating jobs? If manufacturing in the US is simply machine based, what is the point of doing so when it could be cheaper elsewhere and benefit countries that need the jobs?

In the recently released 2016 President’s Trade Agenda, the textile and apparel (T&A) sector was mentioned four times (up from only once in 2015*):

1.Trade enforcement

“THE OBAMA ADMINISTRATION has a record of trade enforcement victories that have helped to level the playing field for American workers, businesses, farmers, and ranchers. In 2016, we will continue to aggressively pursue a robust trade enforcement agenda, including by using new and stronger tools under the bipartisan Trade Enforcement Act of 2015 to hold our trading partners accountable.

Ongoing disputes include challenges to:

China’s far-reaching export subsidy program extending across sectors and dozens of sub-sectors, including textiles, industrial and agricultural products.”

2.Trade preference programs

“Haitian Hemispheric Opportunity through Partnership Encouragement Act (HOPE) program, which supports nearly $900 million in garment imports from Haiti, is an essential support for Haiti’s long-term economic growth and industrial development. HOPE supports thousands of jobs in Haiti’s textile and garment sectors, while providing important protections to workers. Early extension of this program will provide the necessary stability and continuity for companies to continue investing in Haiti’s future.”

3.Benefits of trade to the American people

“More recent trends are similar, with families steadily gaining purchasing power as the price of traded goods, such as smart phones, apparel, and toys, falls. While all households benefit, the gains from trade have predominantly benefited lower-income Americans, who spend a greater portion of their incomes on highly-traded staples like food, shoes, and clothing.”

4.Trade and labor

Our engagement has produced an Implementation Plan Related to Working and Living Conditions of Workers that is helping to address concerns about workers’ rights and working conditions in Jordan’s garment sector, particularly with respect to foreign workers. Jordan has issued new standards for dormitory inspections, submitted new labor legislation to its parliament and hired new labor inspectors. USTR and Department of Labor continue to work with Jordan on the issues under the Plan.

Overall, it seems:1) Reflecting the global nature of the sector, T&A is a topic that involves multiple trading parties for the United States; 2) Economic development and foreign aid are important elements in the U.S. trade policy for T&A. 3) Social responsibility and labor practices in the T&A sector remain a grave concern and need further improvement through international collaborations. 4) The T&A sector is involved in some topics with divisive public opinions, such as the impact of imports.

* Textile and apparel mentioned in the 2015 U.S. Trade Policy Agenda:

Our engagement has produced an Implementation Plan Related to Working and Living Conditions of Workers that is helping to address concerns about workers’ rights and working conditions in Jordan’s garment sector, particularly with respect to foreign workers. Jordan has issued new standards for dormitory inspections, submitted new labor legislation to its parliament and hired new labor inspectors.

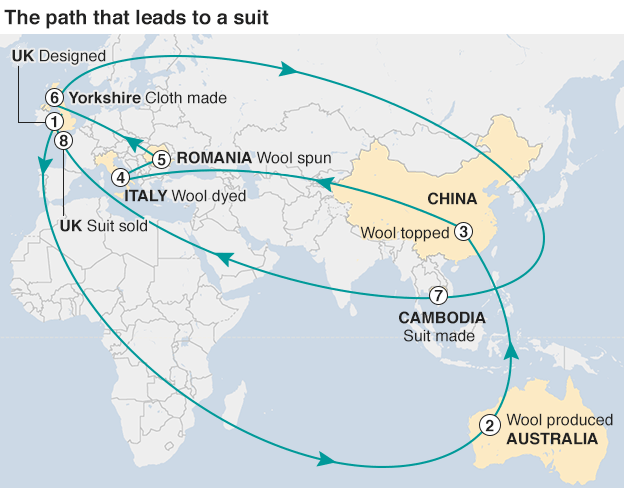

Raw wool was shipped from Australia to China for topping.

Wool top was shipped from China to Italy for dying

Dyed wool was shipped from Italy to Romania to be spun into yarn

Yarn was shipped to Yorkshire, UK to be woven into cloth

Cloth was shipped from Yorkshire, UK to Cambodia to be made into finished suit

Finished suit was shipped back to UK to be sold at M&S retail stores

As noted by the article, such a global-based production model for M&S’s suit is increasingly typical in UK. What makes the issue controversial, however is that, the suit is labeled as “100% British cloth”. As “defined” by M&S, “British cloth means it is woven, dyed and finished in the UK”.

Similar debates also exist in the United States. In the past, even if a garment was cut and sewn in California but made of imported items, the tag still had to say, “Made in USA of imported fabric, zippers, buttons and thread.” But a new law which takes into effect on January 1, 2016 allows California manufacturers to attach the “Made in USA” label as long as no more than 5 percent of the wholesale value of the garment is made of imported materials.

Discussion questions:

What are the driving forces behind apparel companies’ global-based production model?

Is the clothing label “Made in ___” outdated in the 21st century?

Do you support the new law which allows apparel labeled “Made in USA” to contain certain value of imported material? Why? Do we need such a regulation at all? Why or why not?

Apparel producers across Asia may face a more than 5% minimum wage increase in 2016, according to an industry source. India, Malaysia, Thailand and Pakistan may see the biggest increase of minimum wage (up more than 15%) among the leading Asian apparel producers, whereas minimum wage in Bangladesh and Philippine may remain roughly unchanged from last year.

As noted by the industry source, this year’s minimum wage increase comes from various reasons. In Cambodia, the increase is mostly pushed by local labor unions. Indonesian government raises the wage aiming to shorten the gap between minimum and living wage in under-developed regions. Additionally, countries such as India adjust their minimum wages more based on economic factors such as inflation rate, GDP growth rate and consumers’ price index.

Data further shows that the gap in minimum wage between Asian apparel producers somehow is widening. For example, monthly minimum wage in some parts of China has reached $321 USD in 2016, which is $253 USD higher than in Bangladesh ($68 USD/month), up from $225 USD in 2015. A wide gap in minimum wage is also found within some Asian countries. For example, in Philippine, Indonesia and China, the highest minimum wage could be almost twice as high as the lowest minimum wage in the country.

Despite the increase, minimum wage in Asia remains a fraction of the level in the developed countries. For example, minimum wage in the United States was $7.5/hour in 2015, meaning a worker’s monthly minimum wage shall no less than $1,200 (assume working 40 hours/week, 4 weeks/month).

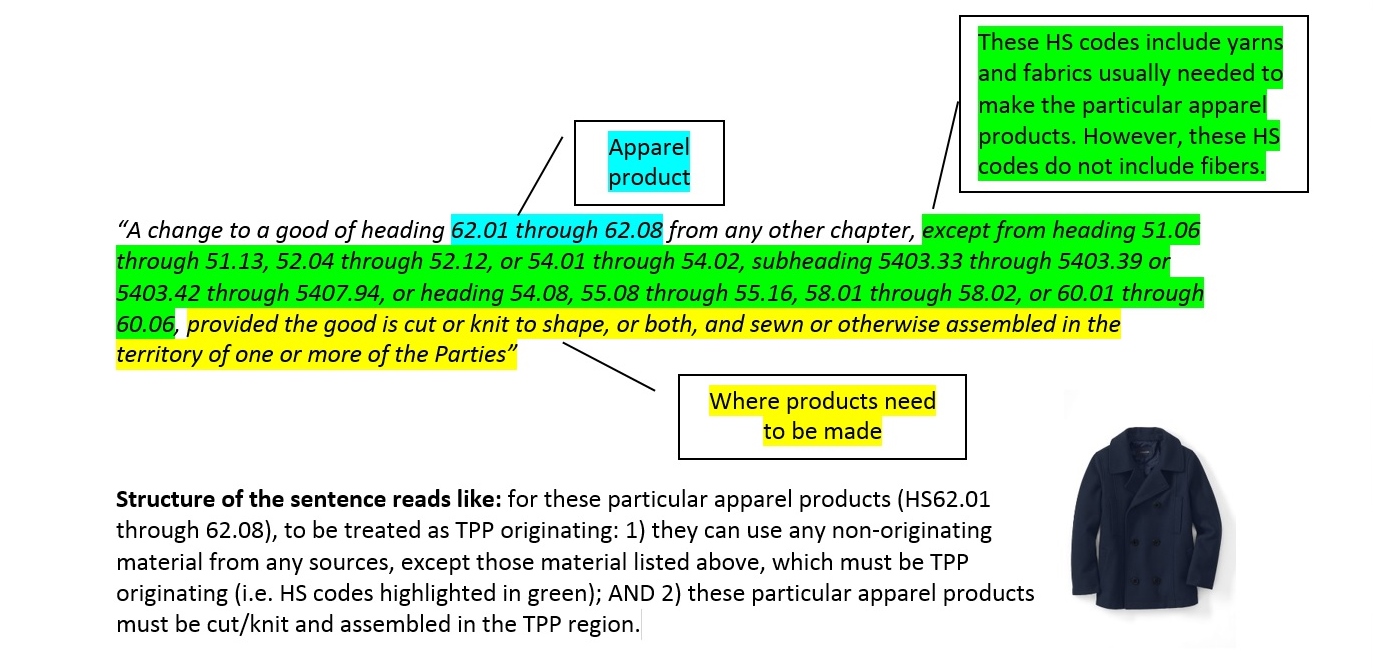

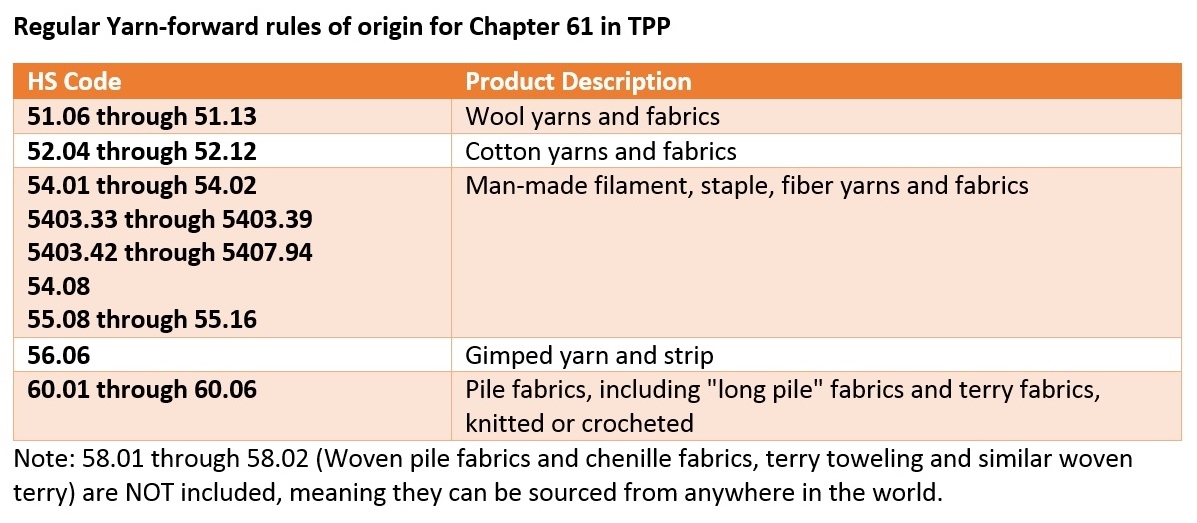

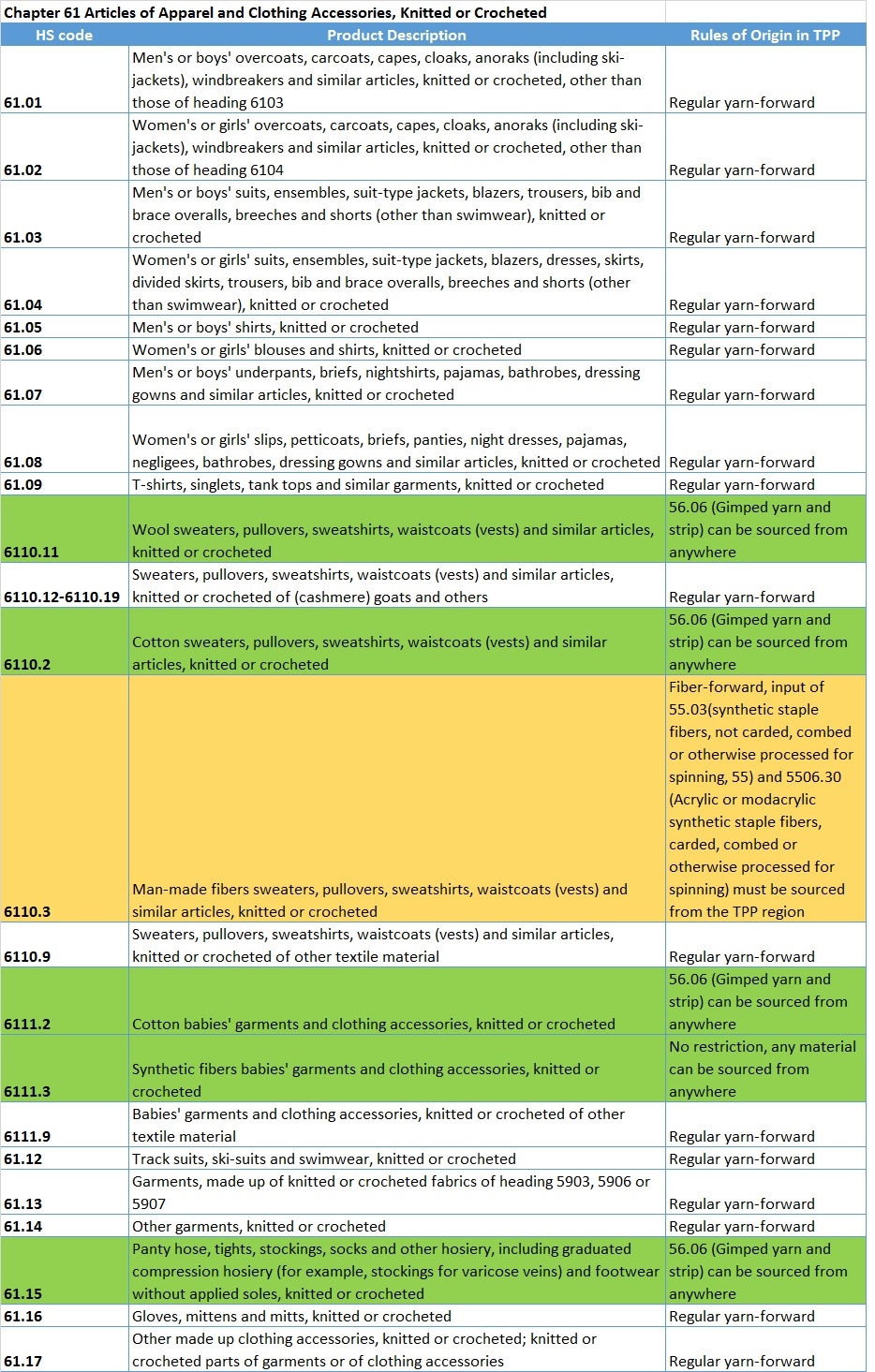

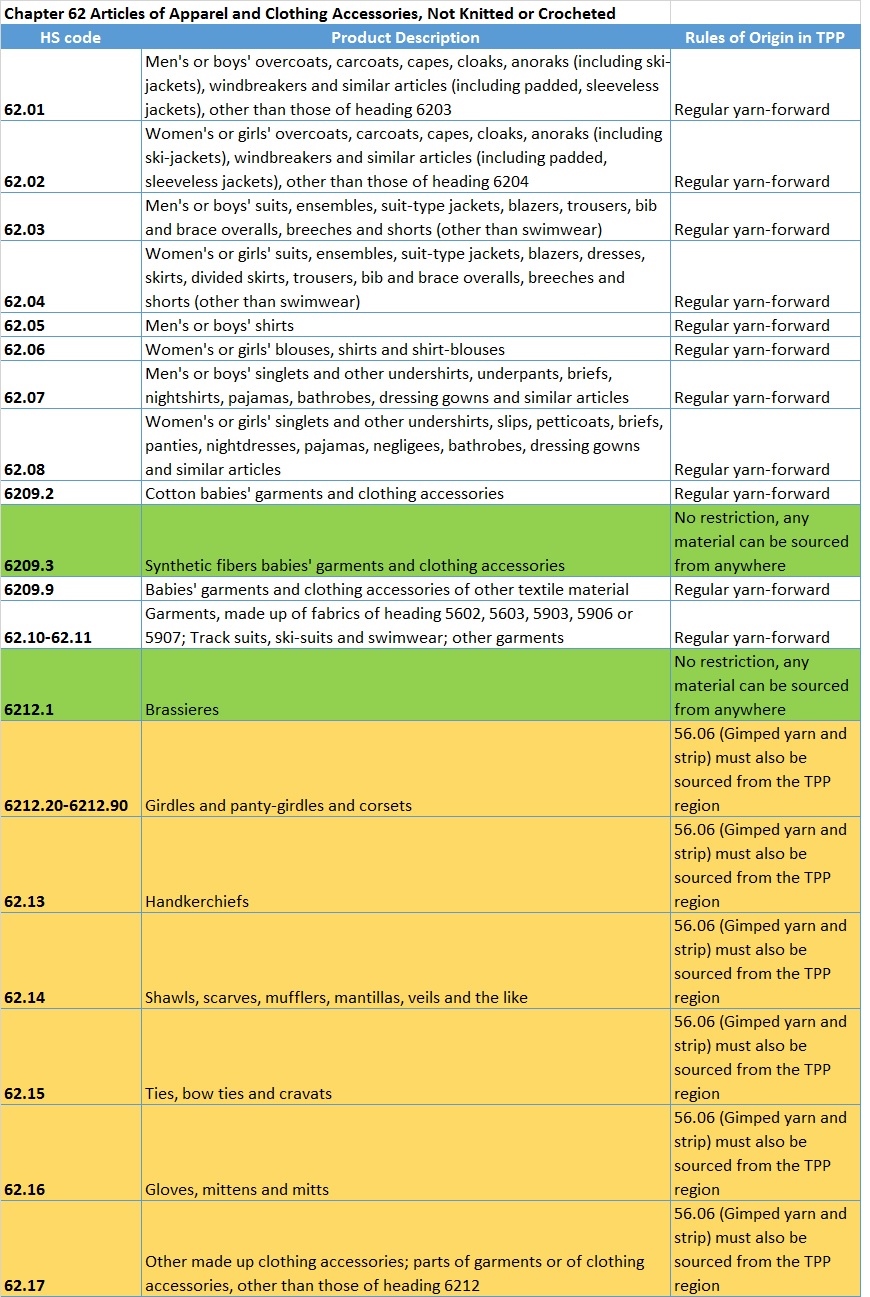

Textile and apparel (T&A)-specific rules of origin (RoO) for most apparel articles under TPP are known as the nickname “yarn forward”. “Yarn-forward “means preferential treatment under TPP will be allowed if the component determining classification meet BOTH the following two criteria:

knit or woven in TPP countries FROM yarn spun or extruded in TPP countries;

apparel is cut or knit to shape or both + sewn or otherwise assembled in TPP countries

In other words, “yarn forward” RoO not only requires the activity of apparel manufacturing must happen in one or more TPP countries, but also requires certain textile material used to make the apparel products must come from the TPP region.

The following is an example of how TPP describes “yarn-forward” rules of origin:

“A good is an originating good if it is produced entirely in one or more TPP countries by one or more producers using non-originating materials and each of the non-originating materials used in the production of the good satisfies any production process requirement, any applicable change in tariff classification requirement or any other requirement specified.”

The followings are details of T&A-specific RoO for apparel products in TPP compiled based on released TPP text. “Regular yarn-forward” means all textile material listed in the table must be TPP originating. Overall, TPP allows much fewer exceptions to “yarn-forward” rules than most existing free trade agreements in the United States (such as NAFTA, CAFTA-DR, and Columbia Free Trade Agreement).

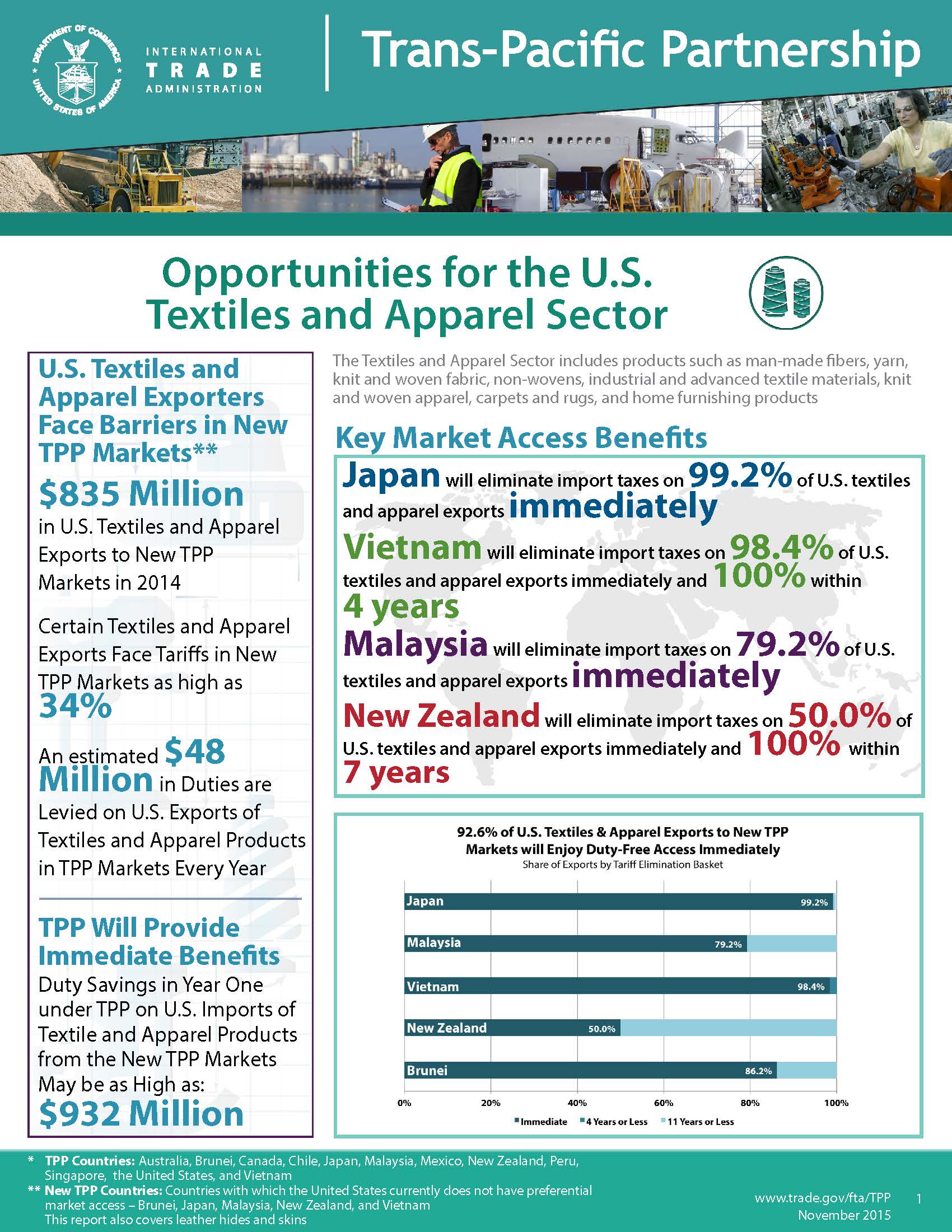

According to the factsheet released by the U.S. Department of Commerce, the Trans-Pacific Partnership (TPP) will create exciting new export opportunities for the U.S. textile and apparel (T&A) industry. The report highlights Vietnam and Japan as two promising markets in TPP for certain T&A products “Made in USA”, including:

Vietnam:

Cotton fiber, yarn, and Cotton woven Fabric (U.S. exported $394 million in 2014 with 16% market share only after China; tariff will be cut from 12% to zero on day one)

Non-woven fabrics (U.S. exported $23million in 2014, up 951% from 2009; tariff will be cut from 12% to zero on day one)

Japan

Synthetic fiber, yarn, and fabric (U.S. exported $61 million in 2014, up 61% from 2009; tariff will be cut from 2.7%-10% to zero on day one)

Industrial and advanced textile fabrics (U.S. exported $91 million in 2014, the fourth largest supplier after China, Taiwan, South Korea; tariff will be cut from 8.2% to zero on day one)

Men’s and boy’s apparel (U.S. exported $32.6milion in 2014, up 30.9% from 2009; tariff will be cut from 9.8% to zero on day one)

The factsheet also argues that TPP is a “balanced” deal for the U.S. T&A industry: long U.S. tariff phaseout schedule, strict “yarn-forward” rules of origin and textile safeguard mechanism in TPP will serve the interests of those stakeholders that seek protection of U.S. domestic T&A manufacturing, whereas duty savings from import tariff cut and the short supply list will create greater market access opportunities for U.S. fashion brands and retailers.

According to the report, the United States is the fourth largest textile exporter in the world. 54% of total U.S. T&A exports went to TPP markets in 2014. The United States is also the single largest importer of T&A in the world. 372,300 T&A manufacturing jobs remained in the United States in 2014.

The following discussion questions are proposed by students enrolled in FASH455 (Global Apparel & Textile Trade and Sourcing) Fall 2015 after learning the unit on textile and apparel industry & market in the Asia-Pacific region. Please feel free to leave your comment and engage in our online discussion.

We’ve heard so much about China’s superior involvement in the textile & apparel sectors globally, but how are these industries contributing to the local economy?

As rules on working conditions and minimum wage have been enforced in Mainland China many business people have moved their operations to Southeast Asia, do you think the Southeast Asia will eventually become like mainland China forcing businessmen to seek low wages elsewhere?

Will Vietnam shift its sourcing of yarns and fabrics from China to US after TPP? What are some setbacks associated with this? What are some potential opportunities?

While Vietnam is currently one of the primary exporters of apparel to the United States, what should be the actions taken by the United States if they continue to “refuse” to cut out Chinese Textiles? Or, should the United States continue their trading patterns with Vietnam despite their reliance on Chinese Textiles?

The Asia pacific region is made up of a variety of countries with different strengths and political infrastructure. How does the variety of policies and governments affect how we do business abroad, and is there a way to set standards that are not individualized to each country?

China and the US can be seen as a threat to one another. However the president of China said the “Pacific Ocean has enough space for the two large countries”. Do you think they are threats to each other, or are they ultimately helping each other’s economies grow?

What will happen as more and more countries that used to produce apparel move into producing more capital intensive production?

What are the advantages or disadvantages of excluding China from international trade agreements such as TPP?

If the T&A industry in China is envisioned by policymakers as beginning to focus more on technical textiles, how will the textile industry in China compete with the industry in the United States?

Why has East Asia become one of the most economically interconnected regions in the world?

What are some of the reasons that China still remains one of most price competitive export markets in the World? Also, does China face challenges in losing their top spot as leader in price competitiveness? If so, what are some of the reasons they are in danger of competition?

How is the discussion about yarn forward rules of origin different in regards to TPP countries than the same discussion between the NAFTA/CAFTA-DR countries?

In an event hosted by the Council on Foreign Relations on October 15, 2015, U.S. Trade Reprehensive Michael Froman left a comment on the textile and apparel chapter (T&A) under TPP. He said that:”

“You know, we worked very hard to find solutions that could address the broad range of stakeholder interests here, even when we had conflicting interests here in the U.S. I’ll take textile as an example. You know, we have a domestic textiles industry that’s been investing in more production in the U.S., growing their employment in the U.S. And obviously we have a strong sector of our economy that brings in apparel from other countries, apparel importers and retailers. We worked very closely with both groups of stakeholders to come up with a solution, to come up with an outcome that we think both will be comfortable with and both will be supportive of. And that’s been very important to us to try and address the broad range of U.S. stakeholder interests, whether it’s labor, environment, importers, exporters, to make sure we’re covering everybody’s interests well.”

In the remarks, Forman also ruled out the possibility that TPP would be renegotiated. He said that:

“So this isn’t one of those agreements where, you know, you can, you know, reopen an issue or renegotiate a provision. This is one where, you know, every issue is tied to every other issue and every country’s outcome is balanced against every other country’s outcome. And so that’s the agreement that we’ll be putting forward under TPA for a vote by Congress.”

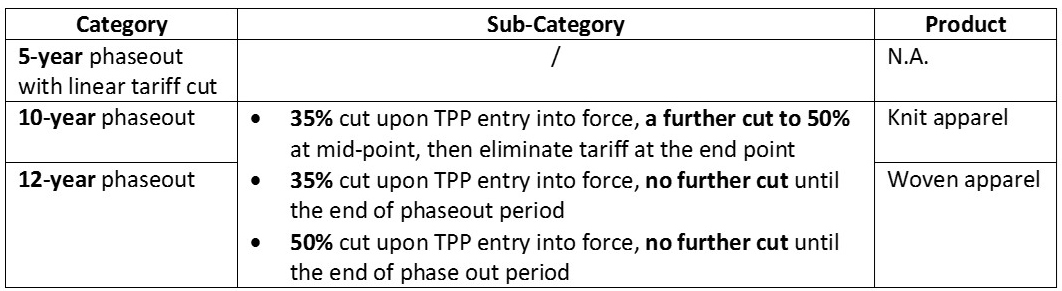

According to Inside U.S. Trade (October 9, 2015), the final TPP reflects some of the key priorities of the U.S. textile industry by allowing limited exceptions from the prevailing yarn-forward rules of origin and by including tariff phaseouts for “sensitive apparel items” of 10 to 12 years.

Besides the basket of goods that will become duty-free upon entry into force (which include cotton shirts and cotton sweaters), TPP sets up three other categories for tariff reductions on apparel:

Major exceptions other than the “short supply list” mechanism under TPP include:

An “earned import allowance“ program for cotton pants made in Vietnam from third-country fabric by importing a specified amount of U.S. cotton pants fabric. This would allow cotton pants from Vietnam would enter the U.S. duty-free as soon as the agreement is implemented. It is said the ratio for the program is “close” to 1:1. However, for men’s cotton pants, there could be a 15 million square meter equivalents (SMEs) annual cap until year 10, after which it will increase to 20 million. There is no quantitative limit for the other types of cotton pants that can be shipped under the program, such as women’s, girls’ and boys’ pants.

A limited list of cut-and-sew items that Vietnam and other TPP countries can ship to the U.S. under the preferential TPP duty rate. These include synthetic baby clothes, travel goods including handbags, and bras.

Regional production-trade network (RPTN) refers to a vertical industry collaboration system between countries that are geographically close to each other. Within a RPTN, each country specialized in certain portions of supply chain activities based on its respective comparative advantages so as to maximize the efficiency of the whole supply chain.

There are three major textile and apparel (T&A) RPTNs in the world today:

Asia: more economically advanced countries/regions such as Japan, South Korea, Taiwan, Hong Kong and China supply textiles to the less economically developed countries such as Vietnam, Bangladesh and Sri Lanka for apparel manufacturing, where the wage level was much lower. On the other hand, Japan is a leading apparel importer and consumption market in Asia.

Europe: among EU members, textile inputs can be supplied by developed countries in Southern and Western Europe such as Italy and Germany. In terms of apparel manufacturing in the European Union, low and medium-priced products can be undertaken by developing countries in Southern and Eastern Europe such as Poland and Romania, whereas high-end luxury products can be produced by Southern and Western European countries such as Italy and France. Furthermore, finished apparel can be shipped to developed EU members such as UK, Germany, France and Italy.

America: within the region, the United States as a developed country supplies textile materials to developing countries in North, Central and South America (such as Mexico and countries in the Caribbean region), which assemble imported textiles into apparel by taking advantage of the local low labor cost. The finished apparel articles are eventually exported to the United States for consumption.

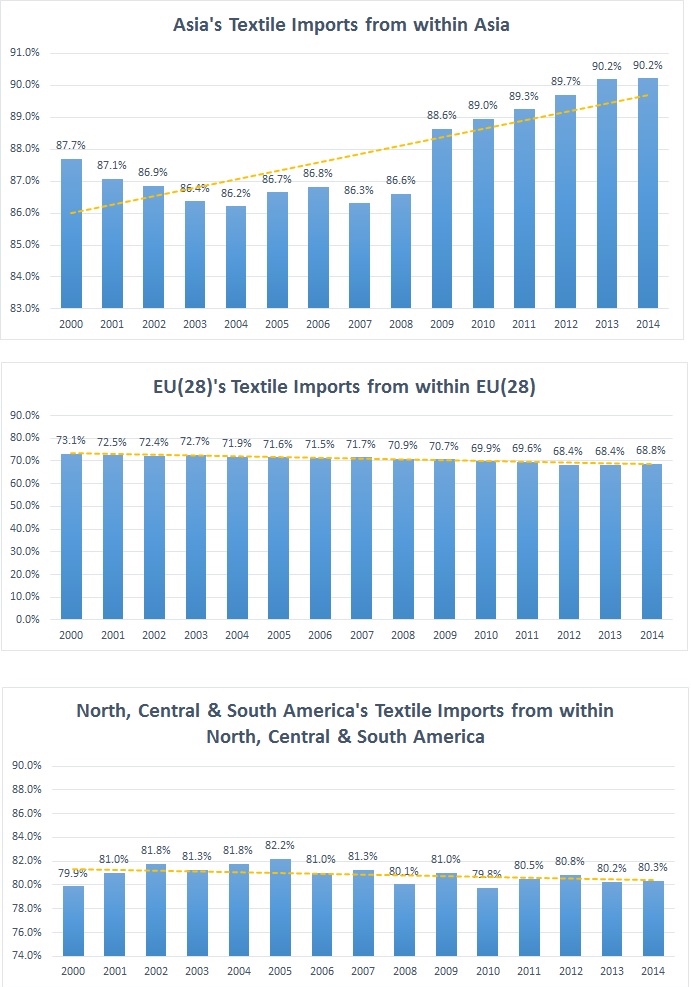

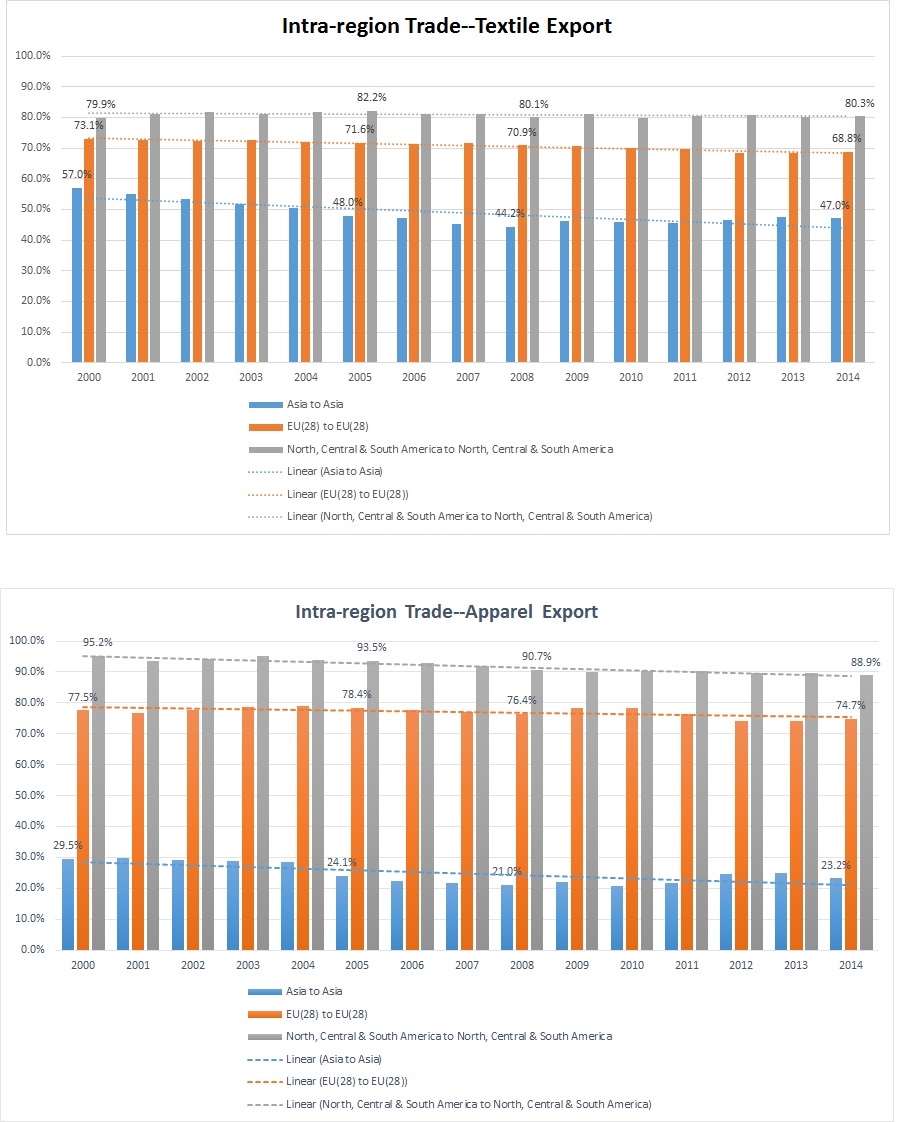

Latest data from the World Trade Organization (WTO) shows that RPTN in the above three regions remain an important feature of today’s global T&A trade as the graphs shown below:

(Note: Data comes from the World Trade Organization)

Particularly, three specific trade flows are worth watching:

One is Asian countries’ growing dependence on textile supply from within the region, which rose to 90.2% in 2014 from 87.7% in 2000. This is a reflection of a growing integrated T&A supply-chain in Asia. As a result, apparel “Made in Asia” is becoming even more price-competitive in the world marketplace today and this has posted pressures on the operation of the T&A RPTNs in EU and America.

Second one is the stable intra-region trade pattern both for textile and apparel in EU. In 2014, 58.8% of EU’s (28 members) textile imports and 46.2% of apparel imports came from other EU members; at the same time, 68.8% of EU’s (28 members) textile exports and 74.7% of apparel exports also went to other EU members.

Additionally, developing countries in North, Central and South America still heavily rely on regional supply of textile inputs; at the same time, their finished apparel are also mostly consumed within the region. Data show that 80.3% of American countries’ textile imports still came from within the region in 2014; at the same time, 88.9% of American countries’ apparel exports were also shipped to the region, mostly the United States and Canada as the final consumption market.

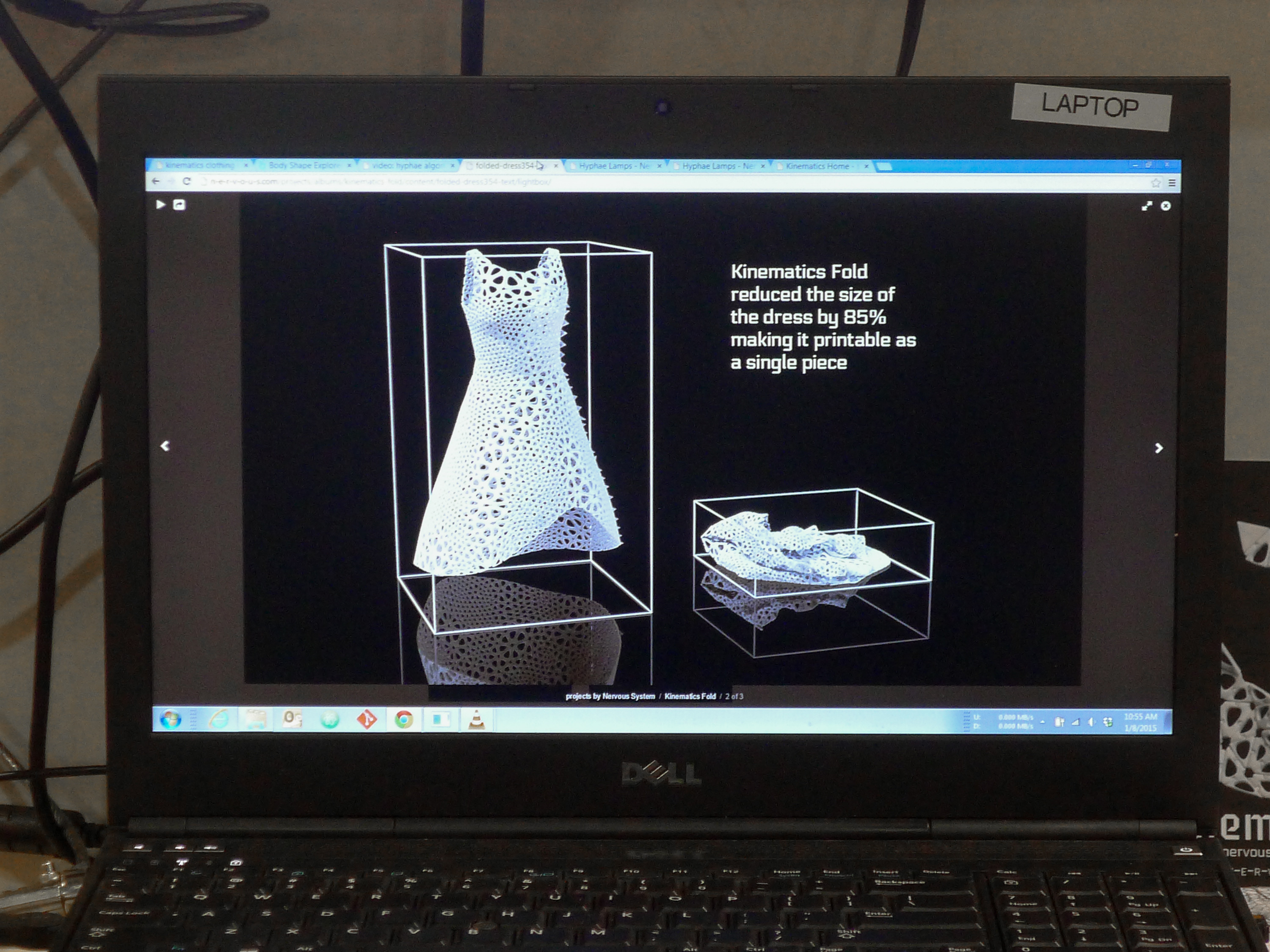

Wearing 3D-printed apparel is no longer a dream (see the pictures above)! But what is the implication of 3D-printing technology on apparel sourcing? Here is my personal vision:

First, 3D printing may create brand new T&A supply chains and business models. 1) Because 3D printing is highly technology and capital intensive with little input from low-skilled labor, it implies that developed countries rather than developing countries may enjoy the comparative advantage in manufacturing 3D-printed apparel. 2) Because apparel will be directly printed by machines, cross-the-border transportation can be largely reduced in the 3D printing era, generating potential cost-saving opportunities both for manufacturers and consumers. 3) 3D printing will empower consumers to more directly involve in the product development process. Yet given consumers’ limited technical knowledge and equipment, many new types of customer services ranging from design assistance to on-site apparel printing may emerge in the 3D printing era.

Second, 3D printing may result in a more sustainable T&A supply chain. 1) Because 3D printing is digital-based, it may help reduce waste during the product development process. 2) Because 3D printing is highly customized and can produce on-demand, it may result in less overproduction in the textile and apparel (T&A) industry. 3) 3D printing has the potential to be made by recycled material. 3D printed apparel itself may be recycled as well, resulting in almost zero carbon emission in the whole product life-cycle.

However, 3D printing my create new challenges for apparel sourcing. 1) When 3D printed apparel substitute traditionally-made apparel among ordinary consumers, demand for apparel sewing workers will be substantially reduced. Millions of unskilled or low-skilled workers currently employed in the T&A sector may have to find new jobs. 2) Workforce in the T&A industry may have to substantially update their knowledge structure in the 3D printing era. The T&A industry may even be short of talents for certain positions such as 3D printing designers and engineers. 3) The application of 3D printing will require an update of the current legal system to better address issues such as intellectual property right protection, consumer privacy protection and data security in a digital-based context.

What is your vision for the future of apparel sourcing in the 3D-printing era?