On April 17, 2023, the US International Trade Commission (USITC) released a new report analyzing the trade and economic impact of the African Growth Opportunity Act (AGOA). The report fulfills the investigation request by the US House of Representatives Committee on Ways and Means in January 2022.

The full report is HERE. Below are the key findings regarding the apparel sector:

The African Growth and Opportunity Act (AGOA) matters significantly to Sub-Saharan African countries (SSA)’s apparel exports to the United States

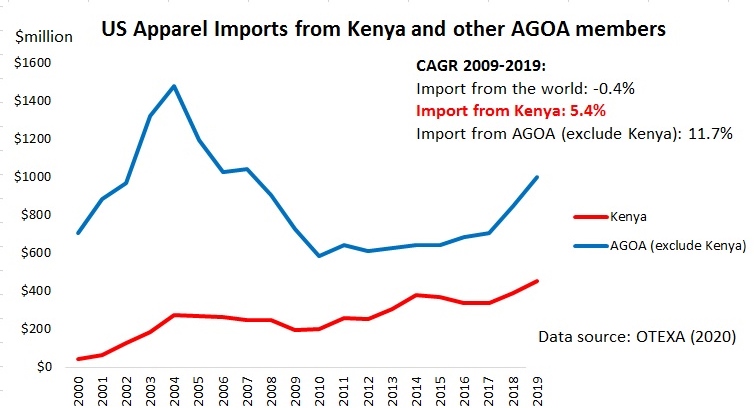

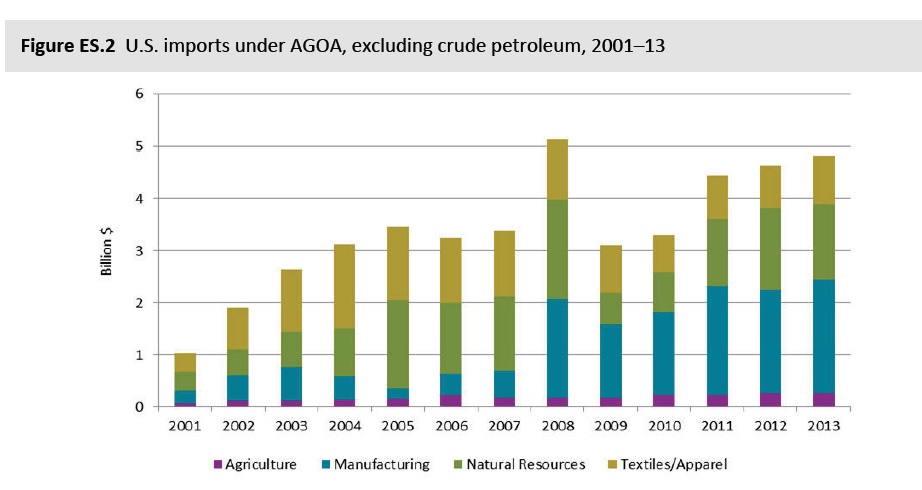

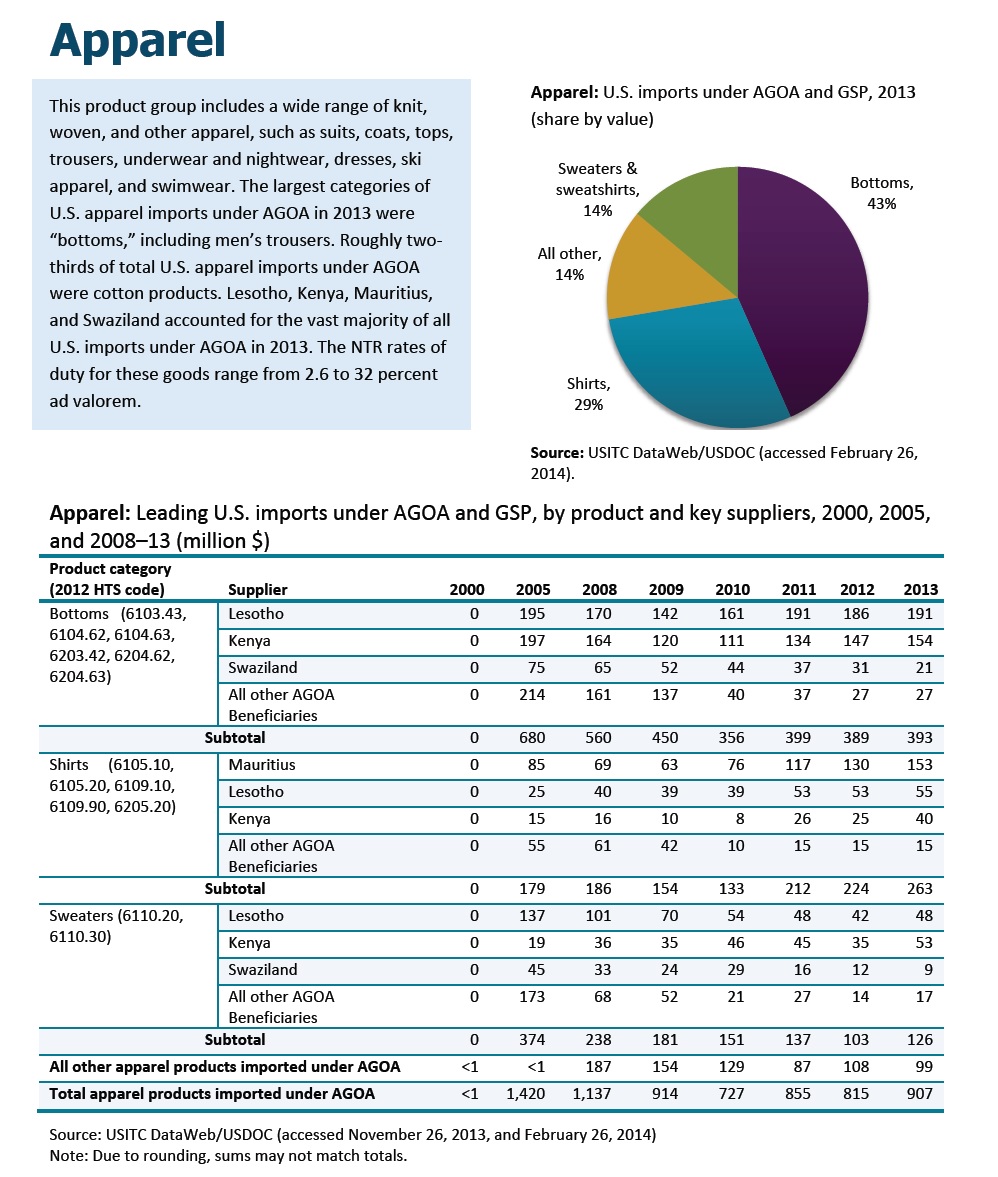

- AGOA has been the primary competitive advantage for SSA’s apparel exports to the United States. For example, US apparel imports from AGOA beneficiaries have risen from $953 million in 2001 to $1.4 billion in 2021 (note: up to $1.76 billion in 2022). More than 96.4% of these imports claimed AGOA’s duty-free benefits, including 98.8% utilized the “third-country fabric” provision.

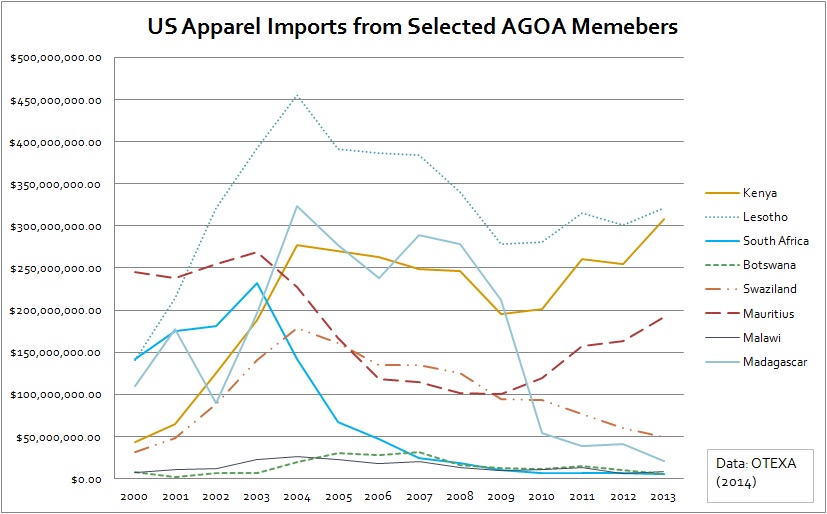

- While twenty countries were eligible for AGOA’s apparel provision, over 90% of US apparel imports from AGOA members in 2021 originated in five SSA countries: Kenya (31.5%), Madagascar (19.9%), Lesotho (20.6%), Ethiopia (18.3%), and Mauritius (5.1%).

- AGOA benefits appear essential for SSA countries to maintain their apparel exports to the United States. USITC noted that in every case when a country lost AGOA eligibility between 2000 and 2021, there was a noticeable decrease in US apparel imports from that country, such as Rwanda and Madagascar. (note: according to OTEXA’s latest trade data, US apparel imports from Ethiopia, which lost its AGOA eligibility in 2022, dropped by 42% in the first two months of 2023 from a year ago, far worse than a 5.8% decrease of AGOA members as a whole.)

- SSA garment manufacturers often find supplying the US apparel market a better fit than Europe, primarily because US brands tend to place orders for higher volume bulk basics, which allows workers to focus on a narrower set of skills.

The impact of AGOA on SSA’s apparel production and exports varied at the country level

- Some SSA countries (e.g., Kenya and Lesotho) already had well-established apparel industries when AGOA was implemented in 2000. In contrast, other SSA countries (e.g., Madagascar, Ethiopia, Tanzania, and Ghana) received substantial investments from foreign-owned firms after AGOA was enacted, which helped jumpstart their apparel sectors.

- USITC also identified two “unsuccessful” AGOA cases. For example, Mauritius was the largest AGOA beneficiary apparel supplier to the United States in 2000 but has since fallen to the fifth-largest in 2021, largely due to increased labor costs. Likewise, South Africa’s apparel export to the US was negatively affected by its disqualification from the “third-country fabric” provision under AGOA.

AGOA has had a limited impact on building an integrated regional textile and apparel supply chain in SSA

- Currently, SSA countries primarily participate in the cut-and-sew operations of apparel based on imported textile raw materials from outside the region (mostly from Asia).

- The USITC identified several challenges in building the local textile industry in SSA. For example, building a textile mill typically requires much higher investments (e.g., $200–300 million) than a garment factory (i.e., $25 million). Also, most SSA manufacturers cannot make the various types of yarns and fabrics in demand from U.S. buyers.

- The dilemma is not new: Access to textile inputs from sources outside SSA is essential for garment manufacturers in SSA to meet the specifications of US buyers. However, relying on imported textile inputs reduces the incentives for investing in new textile production capabilities in SSA.

- The USITC report found Mauritius an exception as it has developed a relatively competitive capability in producing cotton fabrics, which are supplied to garment factories in Madagascar. There is also some collaboration between cotton producers in Tanzania and Uganda and Kenya’s textile manufacturers.

US fashion companies generally see SSA as a promising emerging sourcing destination

- Apparel producers in SSA are less established in global apparel value chains than manufacturers in other parts of the world. Therefore, it is not uncommon that fashion brands and retailers “work more directly with SSA apparel manufacturers to ensure product quality, particularly for new or expanding product lines.”

- Most SSA garment factories only have cut, make, and trim (CMT) capability and rely on imported textile materials arranged by fashion brands and retailers.

- USITC found that US companies increasingly import man-made fiber (MMF) apparel from AGOA members to benefit from greater import duty savings. (note: US tariff rates for MMF apparel were typically higher than those made with natural fibers like cotton. On the other hand, however, it’s worth noting that SSA countries generally have more competitive advantages in producing cotton apparel products than in producing MMF apparel).

- SSA countries also have advantages over their Asia competitors. For example, “a shipment takes about 15–18 days to travel from the port in Lomé to the East Coast of the United States. From China or Bangladesh, lead times range from 40–50 days.”

- Many fashion brands “have expressed interest in sourcing from greenfield factories with fewer legacy challenges posed by compliance and environmental impacts.”

- US fashion companies’ sourcing diversification strategy to avoid risk exposure also contributed to the expansion of their apparel imports from AGOA members.

Uncertainty of AGOA renewals hurt US apparel imports from SSA

- Apparel companies typically make sourcing decisions 12–18 months in advance. This practice underscores the importance of renewing AGOA early rather than granting extensions only within two to nine months of expiration, as in the past.

- The USITC report mentioned, “Without the assurance of the “third country fabric” provision, many US apparel companies sourced from AGOA beneficiaries reported holding back orders from the region.”

More can be done to leverage SSA’s cotton production better

- Cotton growing is widespread across about thirty SSA countries. SSA accounts for about 7 percent of the world’s cotton production, the fifth-largest globally.

- However, most SSA cotton is sold to international buyers and exported to Asian mills that process it into yarns and fabrics. In contrast, the consumption of domestic cotton in SSA is limited.

- The SSA cotton industry produces high-quality, “sustainable” cotton that can be used in several high-value end products sold globally. However, because of a lack of mechanization, SSA cotton production struggles to increase supply to meet demand.

- Also, cotton-growing regions in SSA tend to be poorer and less politically stable than other parts of the region.

Discussion questions:

- Based on the blog post and class discussions, how competitive or attractive are AGOA members as apparel-sourcing destinations for US fashion companies, especially compared with suppliers from Asia and the Western Hemisphere?

- Based on the blog post, what improvement can be made to make AGOA or any problems that need to be addressed?

- Any other thoughts related to the patterns of apparel trade and sourcing based on the blog post?