Global Apparel Market and Trade—The Modern Cotton Story Podcast

FASH455 Global Apparel & Textile Trade and Sourcing

Copyright© 2012-2026 Dr. Sheng Lu, Professor, Department of Fashion & Apparel Studies, University of Delaware

About TAL Apparel

TAL Apparel is one of the world’s largest apparel companies, with over 70 years of history. Owned by Hong-Kong based TAL group, TAL Apparel employs about 26,000 garment workers in 10 factories globally, producing roughly 50 million pieces of apparel each year, including men’s chinos, polo tees, outerwear, and dress shirts. TAL Apparel claims it makes one in six dress shirts sold in the United States, including for well-known U.S. fashion brands such as Brooks Brothers, Bonobos, and LL Bean.

Other than owning factories in Asian countries such as Vietnam, China, Malaysia, Indonesia, and Thailand, TAL Apparel opened its first garment factory in Ethiopia in 2018 – based at the country’s flagship Hawassa Industrial Park. Among the reasons behind the decision is Ethiopia’s duty-free access to the US under the African Growth and Opportunity Act (AGOA), and to Europe under the Everything But Arms (EBA) initiative.

Discussion questions [Anyone is more than welcome to join our online discussions; For FASH455, please address at least two questions in your comment; please also mention the question number in your comment.]

The size of the U.S. textile and apparel industry has significantly shrunk over the past decades. However, U.S. textile manufacturing is gradually coming back. The output of U.S. textile manufacturing (measured by value added) totaled $18.79 billion in 2019, up 23.8% from 2009. In comparison, U.S. apparel manufacturing dropped to $9.5 billion in 2019, 4.4% lower than ten years ago (Bureau of Economic Analysis, 2020).

Meanwhile, COVID-19 has hit U.S. textile and apparel production significantly. Notably, the value of U.S. textile and apparel output decreased by as much as 21.4% and 14.9% in the second quarter of 2020, respectively, compared with a year ago. This result was worse than a 15% decrease during the 2008-2009 world financial crisis. Further, the decline in U.S. textile exports is an essential factor contributing to the significant drop in U.S. textile manufacturing. In the first seven months of 2020, the value of U.S. yarn and fabric exports went down by 31% and 19%, respectively, year over year (OTEXA, 2020).

Additionally, as the U.S. economy is turning more mature and sophisticated, the share of U.S. textile and apparel manufacturing in the U.S. Gross Domestic Product (GDP) dropped to only 0.13% in 2019 from 0.57% in 1998 (Bureau of Economic Analysis, 2020).

The U.S. textile and apparel manufacturing is also changing in nature. For example, textile products had accounted for over 66% of the total output of the U.S. textile and apparel industry as of 2019, up from 58% in 1998 (Bureau of Economic Analysis, 2020). Textiles and apparel “Made in the USA” are growing particularly fast in some emerging markets that are high-tech driven, such as medical textiles, protective clothing, specialty and industrial fabrics, and non-woven.

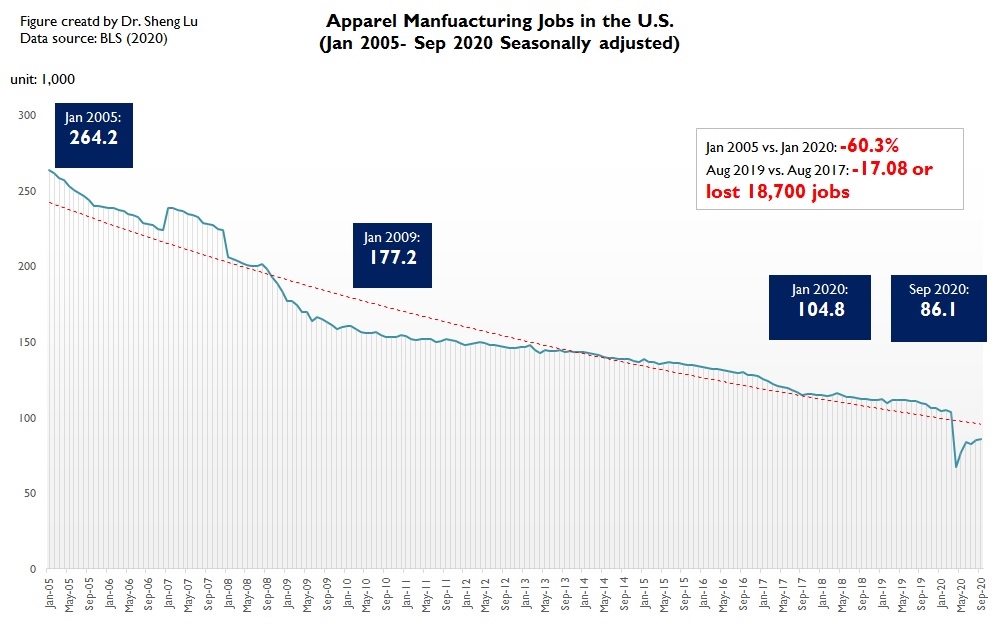

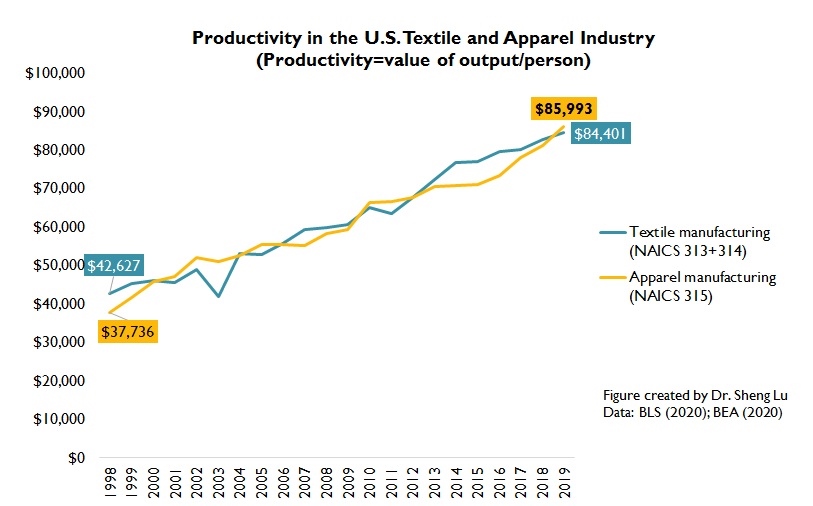

As production turns more automated, the U.S. textile and apparel manufacturing sector is NOT creating more jobs. Even before the pandemic, from January 2005 to January 2020, employment in the U.S. textile manufacturing (NAICS 313 and 314) and apparel manufacturing (NAICS 315) declined by 44.3% and 59.3%, respectively (Bureau of Labor Statistics, 2020). However, improved productivity (i.e., the value of output per employee) could be a critical factor behind the net job losses.

Data further shows that COVID19 has resulted in more than 83,700 job losses in the U.S. textile and apparel manufacturing sector between March-April 2020, of which around 80% have returned as of September 2020. Nevertheless, the downward trend in employment is not changing for the U.S. textile and apparel manufacturing sector.

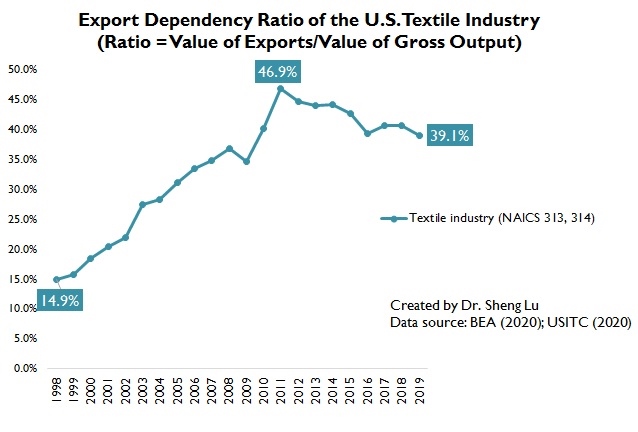

Consistent with the theoretical prediction, U.S. remains a net textile exporter and a net apparel importer. In 2019, the U.S. enjoyed a $1,633million trade surplus in textiles and suffered an $80,637 million trade deficit in apparel (USITC, 2020). Notably, nearly 40% of textiles “Made in the USA” (NAICS 313 and 314) were sold overseas in 2019, up from only 15% in 2000 (OTEXA, 2020). On the other hand, because of the regional supply chain, close to 70% of U.S. textile and apparel export go to the western hemisphere, a pattern that stays stable over the past decade.

by Sheng Lu

Discussion questions:

In January 2019, Just-Style consulted a panel of industry leaders and scholars in its Outlook 2019–Apparel Industry Issues in the Year Ahead management briefing. Below is my contribution to the report. Any comments and suggestions are more than welcome!

1: What do you see as the biggest challenges – and opportunities – facing the apparel industry in 2019, and why?

In my view, uncertainty will remain the single biggest challenge facing the apparel industry in 2019, ranging from a more volatile global economy, the unpredictable outlook of the U.S.-China trade talks to the various possible scenarios of Brexit. While uncertainty creates exciting new research opportunities for scholars like me, it could be a big headache for companies seeking a foreseeable market environment to guide their future business plan and investments.

Meanwhile, the increasing digitalization of the apparel supply chain based on big-data tools and artificial intelligence (AI) technologies means a huge opportunity for fashion companies. Indeed, the apparel industry is quickly changing in nature—becoming ever more globalized, supply-chain based, technology-intensive and data-driven. Take talent recruitment as an example. In the 2018 US Fashion Industry Benchmarking Study, which I conducted in collaboration with the US Fashion Industry Association (USFIA), as much as 68 percent of surveyed leading U.S. fashion brands and apparel retailers say they plan to increase hiring of data scientists in the next five years. Googling “apparel industry” together with terms such as “big data” and “data science” also returns much more results than in the past. It is hopeful that the advancement of digital technologies and the smarter use of data will enable apparel companies to overcome market uncertainties better and improve many aspects of their businesses such as speed to market, operational efficiency and even sustainability.

2: What’s happening with sourcing? How is the sourcing landscape likely to shift in 2019, and what can apparel firms and their suppliers do to stay ahead?

Based on my research, I have three observations regarding apparel companies’ sourcing trends and the overall sourcing landscape in 2019:

First, apparel companies overall will continue to maintain a diverse sourcing base. For example, in a recent study, we examined the detailed sourcing portfolios of the 50 largest U.S.-based apparel companies ranked by the Apparel Magazine. Notably, on average these companies sourced from over 20 different countries or regions using more than 200 vendors in 2017. Similarly, in the 2018 US Fashion Industry Benchmarking Study, which I conducted in collaboration with the US Fashion Industry Association (USFIA), we also found companies with more than 1,000 employees typically source from more than ten different countries and regions. Since no sourcing destination is perfect, maintaining a relatively diverse sourcing base allows apparel companies to strike a balance among various sourcing factors ranging from cost, speed, flexibility, to risk management.

Second, while apparel companies are actively seeking new sourcing bases, many of them are reducing either the number of countries they source from or the number of vendors they work with. According to our study, some apparel companies have been strategically reducing the number of sourcing facilities with the purpose of ensuring closer collaborations with their suppliers on social and environmental compliance issues. Some other companies are consolidating their sourcing base within certain regions to improve efficiency and maximize productivity in the supply chain. Related to this trend, it is interesting to note that approximately half of the 50 largest U.S. apparel companies report allocating more sourcing orders to their largest vendor in 2017 than three years ago.

Third, nearshoring or onshoring will become more visible. Take “Made in the USA” apparel for example. According to the 2018 U.S. Fashion Industry Benchmarking Study, around 46 percent of surveyed U.S. fashion brands and apparel retailers report currently sourcing “Made in the USA” products, even though local sourcing typically only account for less than 10 percent of these companies’ total sourcing value or volume. In a recent study, we find that 94 out of the total 348 retailers (or 27 percent) sold “Made in the USA” apparel in the U.S. market between December 2017 and November 2018. These “Made in the USA” apparel items, in general, focus on fashion-oriented women’s wear, particularly in the categories of bottoms (such as skirts, jeans, and trousers), dresses, all-in-ones (such as playsuits and dungarees), swimwear and suits-sets. The advantage of proximity to the market, which makes speedy replenishment for in-season items possible, also allows retailers to price “Made in the USA” apparel substantially higher than imported ones and avoid offering deep discounts. Looking ahead, thanks to automation technology and consumers’ increasing demand for speed to market, I think nearshoring or onshoring, including ”Made in the USA” apparel, will continue to have its unique role to play in fashion brands and retailers’ merchandising and sourcing strategies.

3: What should apparel firms and their suppliers be doing now if they want to remain competitive further into the future? What will separate the winners from the losers?

2019 will be a year to test apparel companies’ resources, particularly in the sourcing area. For example, winners will be those companies that have built a sophisticated but nimble global sourcing network that can handle market uncertainties effectively. Likewise, companies that understand and leverage the evolving “rules of the game”, such as the apparel-specific rules of origin and tariff phase-out schedules of existing or newly-reached free trade agreements, will be able to control sourcing cost better and achieve higher profit margins. Given the heavy involvement of trade policy in apparel sourcing this year, companies with solid government relations should also enjoy unique competitive advantages.

On the other hand, as apparel business is changing in nature, to stay competitive, apparel companies need to start investing the future. This includes but not limited to exploring new sourcing destinations, studying the changing consumer demographics, recruiting new talents with expertise in emerging areas, and adopting new technologies fitting for the digital age.

4: What keeps you awake at night? Is there anything else you think the apparel industry should be keeping a close eye on in the year ahead? Do you expect 2019 to be better than 2018, and why?

Two things are at the top of my watchlist:

First, what is the future of China as an apparel sourcing base? While external factors such as the U.S.-China tariff war have attracted most of the public attention, the genuine evolution of China’s textile and apparel industry is something even more critical to watch in the long run. From my observation, China is playing an increasingly important role as a textile supplier for apparel-exporting countries in Asia. For example, measured by value, 47 percent of Bangladesh’s textile imports came from China in 2017, up from 39 percent in 2005. Similar trends are seen in Cambodia (up from 30 percent to 65 percent), Vietnam (up from 23 percent to 50 percent), Pakistan (up from 32 percent to 71 percent), Malaysia (up from 25 percent to 54 percent), Indonesia (up from 28 percent to 46 percent), Philippines (up from 19 percent to 41 percent) and Sri Lanka (up from 15 percent to 39 percent) over the same time frame. A key question in my mind is how quickly China’s textile and apparel industry will continue to evolve and upgrade by following the paths of most other advanced economies in history.

Second, how will the implementation of several newly-reached free trade agreements (FTAs) affect the big landscape of apparel sourcing and the existing regional apparel supply chains? For example:

(comment for this post is closed)

Textile Mills

The textile mills market primarily includes yarns and fabrics. The market size is estimated based on the value of domestic production plus imports minus exports, all valued at manufacturer prices.

The value of the global textile mills market totaled $748.1 billion in 2016 (around 83.7% were fabrics and 16.3% were yarns), up 3.5% from a year earlier. The compound annual growth rate of the market was 2.7% between 2012 and 2015. The Asia-Pacific region accounted for 59.6% of the global textile mills market value in 2016 (up from 54.6% in 2015), Europe and the United States accounted for a further 19.1% and 10.8 of the market respectively.

The global textile mills market is forecast to reach $961.0 billion in value in 2021, an increase of 28.5% since 2016. The compound annual growth rate of the market between 2016 and 2021 is forecast to be 5.1%.

Apparel manufacturing market

The apparel manufacturing market covers all clothing except leather, footwear and knitted items as well as other technical, household, and made-up products. The market size is estimated based on the value of domestic production plus imports minus exports, all valued at manufacturer prices.

The value of the global apparel manufacturing market totaled $785.9 billion in 2016, up 3.3% from a year earlier. The compound annual growth rate of the market was 4.4% between 2012 and 2016. The Asia-Pacific region accounted for 61% of the market value in 2016 and Europe accounted for a further 15.2% of the market.

The global apparel manufacturing market is forecast to reach $992 billion in value in 2021, an increase of 26.2% since 2016. The compound annual growth rate of the market during the period of 2016 and 2021 is forecast to be 4.8%.

Apparel retail market

The apparel retail industry consists of the sale of all menswear, womenswear and childrenswear. The market value is calculated at retail selling price (RSP), and includes all taxes and duties.

The value of the global apparel retail market totaled $1,414.1 billion in 2017 (52.6% womenswear, 31.3% menswear and 16.1% childrenswear), up 4.9% from a year earlier. The compound annual growth rate of the market was 4.4% between 2013 and 2017. The Asia-Pacific region accounted for 37.1% of the global apparel retail market in 2017 (up from 36.8% in 2015), followed by followed by Europe (28.5%) and the United States (23.6%).

The global apparel retail market is forecast to reach $1,834 billion in value in 2022, an increase of 29.7% since 2017. The compound annual growth rate of the market between 2017 and 2022 is forecast to be 5.3%.

Data source: MarketLine (2018)

A recent study released by the U.S. International Trade Commission (USITC) provides a comprehensive review and valuable insights into the state of textile and apparel manufacturing in the United States. According to the study:

First, data suggests a mixed picture of the recovery of textile manufacturing in the U.S.

Second, some evidence suggests that reshoring has taken place in recent years in the apparel sector, although on a modest scale.

Third, the advantages of making textiles and apparel in the United States include: