The EU region as a whole remains one of the world’s leading producers of textile and apparel (T&A). The value of EU’s T&A production totaled EUR137.3 bn in 2019, down around 2% from a year ago (Note: Statistical Classification of Economic Activities or NACE, sectors C13, and C14). The value of EU’s T&A output was divided almost equally between textile manufacturing (EUR68.7bn) and apparel manufacturing (EUR68.6bn).

Regarding textile production, Southern and Western EU, where most developed EU members are located such as Germany, France, and Italy, accounted for nearly 75% of EU’s textile manufacturing in 2019. Further, of EU countries’ total textile output, the share of non-woven and other technical textile products (NACE sectors C1395 and C1396) has increased from 19.2% in 2011 to 23.0% in 2017, which reflects the on-going structural change of the sector.

Apparel manufacturing in the EU includes two primary categories: one is the medium-priced products for consumption in the mass market, which are produced primarily by developing countries in Eastern and Southern Europe, such as Poland, Hungary, and Romania, where cheap labor is relatively abundant. The other category is the high-end luxury apparel produced by developed Western EU countries, such as Italy, UK, France, and Germany.

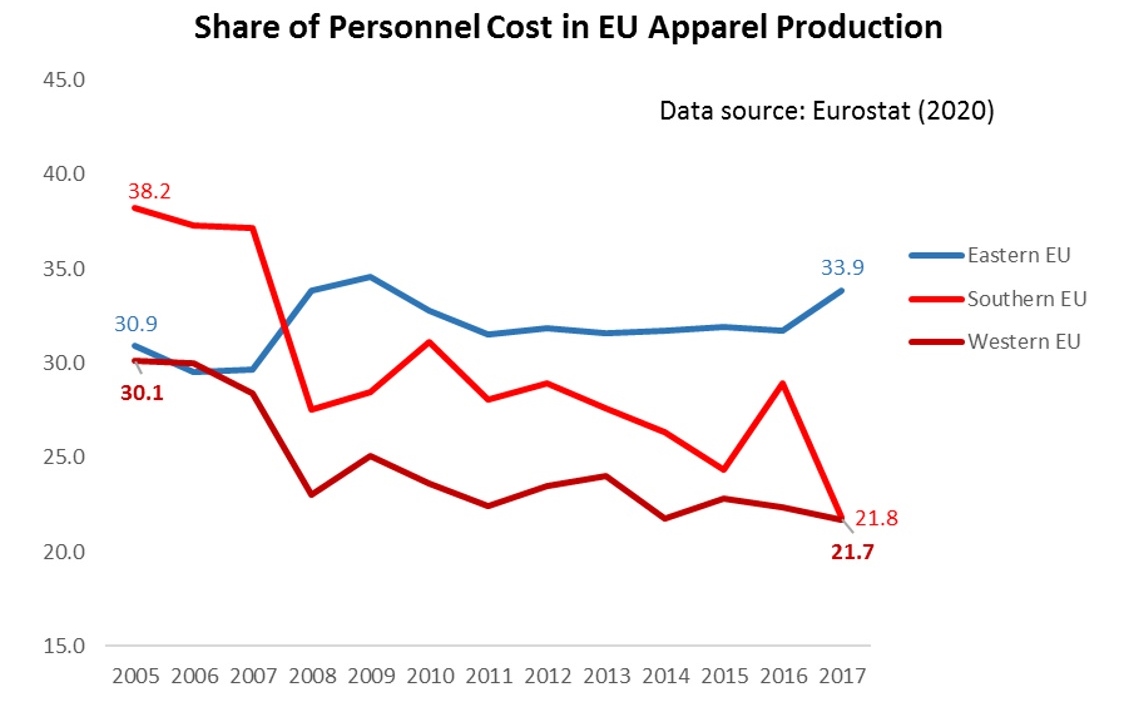

It is also interesting to note that in Western EU countries, labor only accounted for 21.7% of the total apparel production cost in 2017, which was substantially lower than 30.1% back in 2006. This change suggests that apparel manufacturing is becoming capital and technology-intensive in some developed Western EU countries—as companies are actively adopting automation technology in garment production.

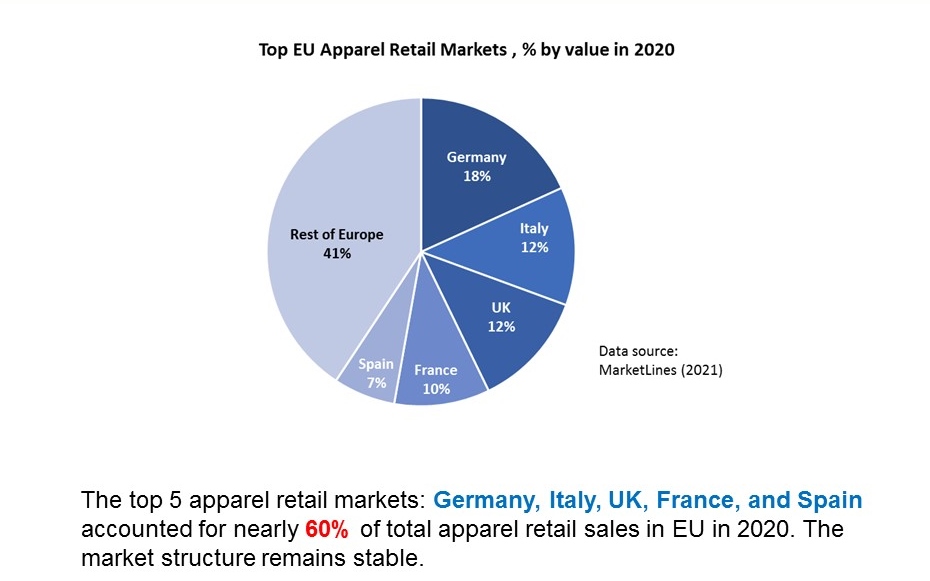

Because of their relatively high GDP per capita and size of the population, Germany, Italy, UK, France, and Spain accounted for nearly 60% of total apparel retail sales in the EU in 2020. Such a market structure has stayed stable over the past decade.

Data source: UNcomtrade (2021)

Intra-region trade is an important feature of the EU’s textile and apparel industry. Despite the increasing pressure from cost-competitive Asian suppliers, statistics from UNComtrade show that of the EU region’s total US$73.8bn textile imports in 2019, as much as 54.6% were in the category of intra-region trade. Similarly, of EU countries’ total US$204.0bn apparel imports in 2019, as much as 37.4% also came from other EU members. In comparison, close to 98% of apparel consumed in the United States are imported in 2019, of which more than 75% came from Asia (Eurostat, 2021; UNComtrade, 2021).

Regarding EU countries’ textile and apparel trade with non-EU members (i.e., extra-region trade), the United States remained one of the EU’s top export markets and a vital textile supplier (mainly for technical and industrial textiles). Meanwhile, Asian countries served as the dominant apparel sourcing base outside the EU region for EU fashion brands and retailers.

The EU textile and apparel industry is not immune to COVID-19. According to the European Apparel and Textile Federation (Euratex), the EU textile and apparel production feel 9.3% and 17.7% respectively in 2020 from a year ago.

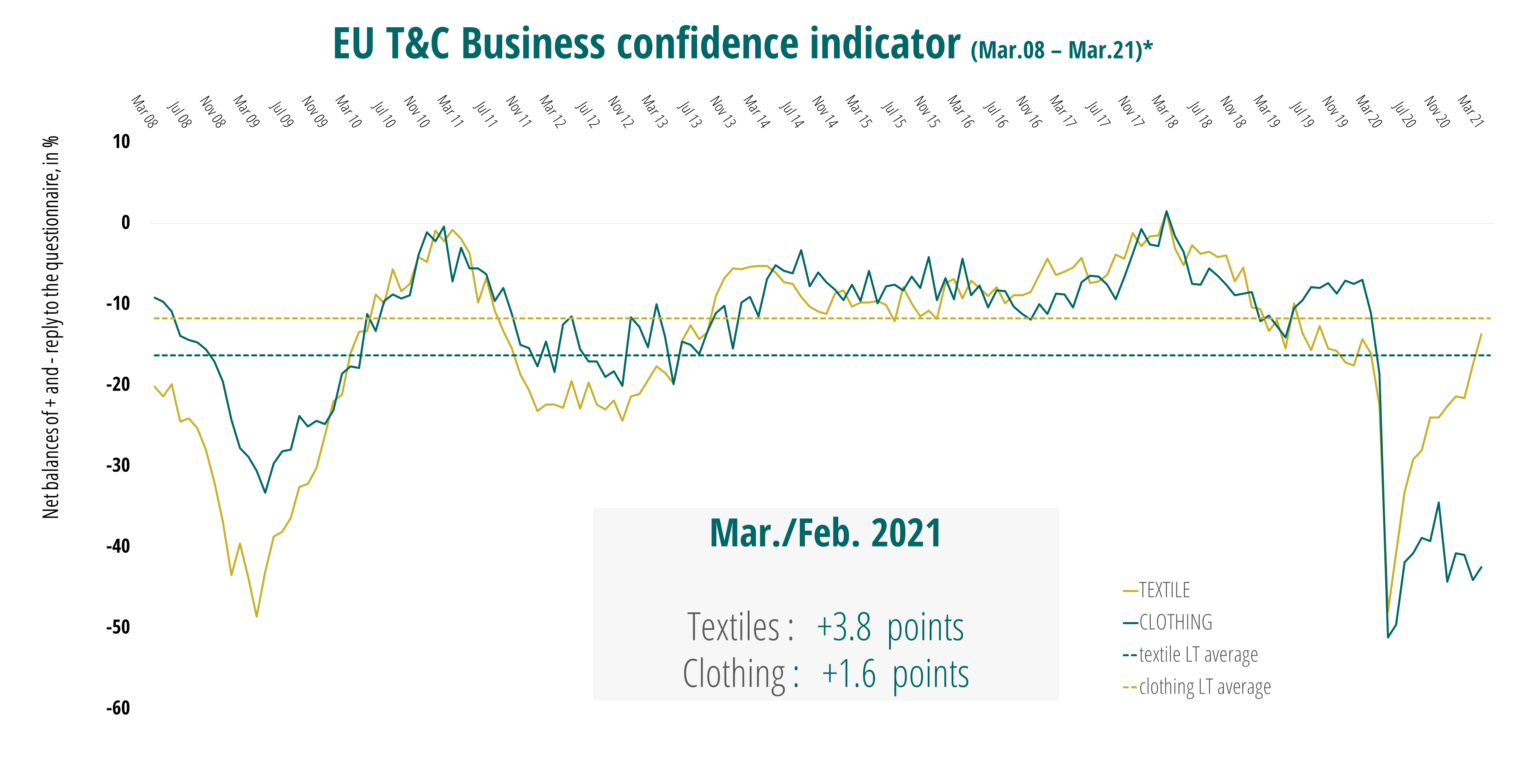

2021 hopefully will be a year of recovery and growth for the EU textile and apparel industry. According to Euratex, the EU Business Confidence indicator of March 2021 gained momentum, with a confirmed upward trend in the textile industry (+3.8 points), and a modest recovery in the clothing industry (+1.6 points). However, Euratex also noted that EU textile and apparel companies still face daunting challenges and uncertainties in 2021, ranging from the rising raw material price, increasing transportation cost, to political instability in some key sourcing destinations (such as China and Myanmar).

by Sheng Lu

I have gathered many takeaways after reading this post. While learning about this in class, I found it very interesting how the EU really likes to only source and trade within EU countries. Although the EU has many more different countries with different resources, I find this an extremely smart tactic. By only trading within the EU it puts less reliance on other parts of the world to manufacture your products and help your business run. This is something I think the U.S. needs to look into. What if we were able to source from different states and set up apparel manufacturing throughout the region? Could this be something to look into? Would this be beneficial? Why or why not? I am also impressed with how involved EU fashion companies are within their supply chain. In one of our readings about Hugo Boss, the company has many requirements and standards that needs to be met by their supply chain. On top of that, they even provided manuals of how things were to be operated. This is another tactic the U.S. needs to jump on board with. If U.S. fashion companies had these set standards within their supply chain, they wouldn’t be involved in issues like Rana Plaza.

April ’21 trade pattern statistics for the EU Textile and Apparel Industry remain consistent with the intra-region theories. The EU divides production between developed, western European countries for roughly 75% of textile production and developing, Eastern and Southern European countries for apparel manufacturing – both of which we see shifting towards capital and technology-intensive processes. Noting the intra-regional trade patterns, the U.S. textile and apparel industry should not push the new Biden administration to conclude the negotiation of a US-UK trade deal. Consumers in the EU prefer locally made textiles and apparel, in which premium products made in the U.S. could compete neither with prices nor quality.

In 2021 how do you think EU textile and apparel industry will grow and recovery from Covid-19. What are some suggested ideas that could help them?

It is interesting to me that the US is the 5th top textile supplier to the EU. Also, our share decreased from 4% in 2019 to to 1.9% in 2020. We are competing directly with China’s textile manufacturing. China’s share of textile imports to the EU increased from 37.5% in 2019 to 64.4% in 2020. These numbers are crazy to me! Why did their share double in just one year? As a developed country in post-maturity, how is the United States being overpowered by China? China is increasingly manufacturing textiles and has the capacity to be world leaders in textiles and apparel.

I think it is interesting to see how heavily the EU relies on one another for trade. It is a good thing that they are all pretty developed and are taking advantage of the fact that they are all so close to one another. I also did not realize that the EU had as much textile manufacturing as it does. Since we have mainly talked about China and the US, I did not realize the other places produce textiles. So are China, the EU, and the US all competing for their textiles to be used? Will the top exporter change in the coming years? Will there ever be a trade agreement between all 3?

I think there are many reasons why the EU only primarily relies on itself for sourcing and trading. There are many benefits to this. One, I am sure that it is much less expensive than it would be from other parts of the world. I remember reading in another article that if the US sourced much closer, for instance Mexico, that it would be much less expensive for them. Along with this, it also increases speed and production, and allows them to have a faster speed to market. I am sure that the EU takes into considerations some of these components within their decisions to source and trade in the EU. Another thing that was not surprising to me was the top retail sales countries within the EU. Germany, Italy, UK, Spain and France account for 60% of EU total apparel retail sales. The reason I am not shocked by this is because of these countries population, and tourism that occurs. These countries do very well in the retail business, and have people coming in and out of their country all of the time.

I think it is interesting how the EU primarily sources and trades within EU countries. I think there are several advantages to this tactic that maybe other countries should start to implement in their own trading and sourcing. By sourcing and trading primarily within EU countries, EU countries do not face the burden of a tariff which can make things more expensive for consumers and retailers. The proximity of sourcing and trading within EU countries allows EU countries to receive items quicker and have a shorter lead time which allows them to be on top of the trends and get items in their store faster than competitors. As we have discussed in class, near-shoring is something that is projected to increase during/after COVID-19 so it appears EU is ahead of other countries for near-shoring. Although it appears intra region trading for textiles and apparel has decreased in EU over the years, I think we will see an increase in the next year due to COVID-19.

The EU’s use of intra-region trade can be an inspiration for the rest of the world for the future. The EU has successfully and consistently depended on itself for textile and apparel production. They have proved the true meaning of near5-shoring and the benefits that can come from it. They do not have to heavily concern themselves with foreign trade policies or tariffs since majority of their relationships in their supply chain are within their own union. One of the most interesting take aways got me was that their labor costs dropped almost 10% in 10 years. This shows how technologically advanced and intensive they are becoming. An increase in better and more efficient technology is only going to help them grow in the textile and apparel industry as they will better be able to compete with Asian countries cheap production prices.

I made a lot of similar points to your response! I agree that the EU’s use of intra-region trade could be an inspiration for the rest of world as it proves to be a successful tactic for them. They also are a great example of a region that takes advantage of near-shoring. Due to Covid-19 I think we will see other regions follow in their footsteps and attempt to near-shore with countries nearby their region for shorter lead times and to stay ahead of competitors.

Suppliers to the EU apparel market come from two main sources: local European textile and apparel producers and non-European producers. By working tirelessly to improve its competitiveness and adjust to the new environment of international trade, the European textile and apparel industry has maintained its vitality and dynamism in the face of the challenges of globalization. The strongest areas of the European textile and apparel industry are luxury goods, ready-to-wear and technical, technical and innovative textiles. The EU is the second largest exporter of textiles in the world. The EU is also the second largest exporter of apparel, after China. 1/4 of the EU apparel industry’s apparel imports are supplied from the periphery (within the EU) and the remaining 3/4 from Asia. 3/4 of apparel sourcing is in CMT form and the remaining 1/4 in FOB form. The proportion of online sales is growing rapidly (Amazon, Zalando, etc.). For apparel manufacturing, European retailers have social responsibility and environmental awareness.

EU has maintained being one of the world’s leading producers of textile and apparel. Apparel manufacturing within EU has two categories that they remain consistent. Medium priced products and high end products are both produced in two different locations. The medium priced products are produced in developing countries while the high end pieces are created in high end fashion countries such as Italy and France. EU does a great job of maintaining trade relationships with areas close by and does not get too involved with trade agreements and tariffs. They are advancing and becoming more dominant as they learn new ways to source and trade with surrounding countries. Like many other countries affected by Covid. EU is trying to rebuild their reputation and technologically advance in all aspects of the industry.

After reading this post, I was able to farther understand the EU’s trading patterns and how they are a leading producer of textiles and apparels. Due to them combining their GDPs per nation, it created a much larger economy closer to the size of the US and other comparative nations. With the EU having a focus on high end fashion, and having nations like Italy and France, it greatly boosts their revenues, according to the graphs. This fact is something that remains unique to the EU. The US, China, India, etc couldn’t match the quality, prices, or designs that the EU produces and that serves to be a major plus point for them.

I found it really interesting while I read the article that the low price products are produced in Eastern and Southern Europe while the high price products are developed by Western Europe. This is because cheap labor is more available in Southern and Eastern Europe. This article helped me a lot to more understand the trade patterns in Europe. For example, something I learned was that Europe’s textile and apparel industry uses intra-region trade. In 2019, when their textile imports were at 73.8 billion, 54.6% of that was in intra-region trade. Europes textile and apparel industry is really strong and independent and other countries should follow in their footsteps.

it is even more interesting to me that despite the high wage level (even higher than in the US), many western EU countries remain leading apparel manufacturers and exporters today. the detailed factors can be explored further.

As someone who has traveled (and shopped) in both eastern and western Europe, I find the statistical breakdown of the t&a industries in these countries extremely interesting. Three years ago I went to Poland and one thing I noticed about the area I was in was that there were a lot of random inexpensive stores selling tourist items and apparel. Other than seeing name brands such as Zara the stores I saw were more for basics rather than high fashion. This goes directly with what the article says about eastern Europe focusing on medium-priced mass-market apparel. Last winter I went to Budapest. One of the first things I noticed about the country was how inexpensive things were compared to the US dollar. Regarding their fashion I saw a lot of small stores that focused on arts and craftsmanship, rather than name brands. This handmade focus didn’t really fit the idea of focusing on clothing for the mass market, but this may have been because the area I was in was different than the rest of Hungary, and there may not be as much cheap labor.

Overall I think it’s so interesting to see the contrast between how Europe trades vs the US. The US is usually much more isolated compared to Europe, but it’s so different when it comes to the t&a industries. Europe is set up in a way that they can support themselves, while the US relies on others. I think it would be amazing if the US could begin to manufacture more so they don’t need to rely so much on other countries.

I found this article interesting for a multitude of reasons. Firstly, I was unaware of just how heavily the EU relies on itself and surrounding countries for trade. That being said, it does make sense, and it’s smart of them to take advantage of how closely located all the countries are. This is a major advantage that the EU enjoys that the US does not. Secondly, I found it interesting that the US was still among the top textile producers for the EU. Given all the options and their location, I would have thought that other countries would provide to the EU more than the US does.

After reading this article, I think we should prioritize the U.S. textile and apparel trade policy to continue to protect the exports of yarn and fabrics to the WH. I also think that it would be a smart move for the US to increase our own production in order to become more self-reliant. While relying on other countries is sometimes necessary, it is smart to be able to provide for yourself in the event that others are no longer providing for you.

This article was very interesting to me because the EU Textile and Apparel Industry seems unique compared to other industries such as the Western Hemisphere Supply Chain and The Flying Geese Model. EU countries primarily source from each other and produce both textiles and apparel, which isn’t very common. Another unique aspect of this supply chain is the luxury market, which no other supply chains have. Countries such as Germany and France are the top producers of luxury apparel, so many western countries focus on this market. The US is one of the main importers of these luxury garments because US citizens have the disposable income to spend on high price items so there is a market for it in the US. In contrast, eastern countries such as Poland, focus on mass production of medium-priced products because they have more abundant cheap labor. In class and from this article, I have really enjoyed learning about the luxury market in the EU and the US, because I like how much thought and consideration is put into the production of these products. So many garments are massed produced, so it is refreshing to learn about products that so much care is put into the production of.

Cheap labor is more available in Southern and Eastern Europe which results in the low price products being produced in Eastern and Southern Europe while the high price products are developed by Western Europe. It is interesting to observe the way trading works like that Europe’s textile and apparel industry uses intra-region trade. It is interesting that despite high wages in the EU, Europes textile and apparel industry is so independent and close-knit which in a way makes them unbreakable.

This article was really eye opening to show that most European countries produce textiles and the apparel. This is usually not very common because developing countries and the ones that usually produce the apparel and the developed countries produce the textiles because they have the supplies to do so. South and Western Europe last year accounted for 75% of EU’s textile manufacturing. this included the countries of Germany, France and Italy. It was also interesting to read that cheap labor is more available in Southern and Eastern Europe. I love that these countries source from each other, this creates a way for the EU countries to not have to worry about the burden of tariffs which are always a constant war between countries arguing over them. These countries don’t have to worry about barriers and customs as well since everything is in the same country. This makes the items get produced faster and more efficiently. The US should start looking into this and making there regulations better so issues don’t occur.

Prior to reading this article and taking this course, I never knew just how heavily the EU relies on itself and surrounding countries for trade. I think the EU is at an advantage compared to the US since they are able to make use of the nearby countries. EU countries are also among the top luxury producers; the US is actually one of the top importers of these luxury brands. The EU focuses heavily on luxury fashion, which according to their graphs, helps boost their revenues.

The EU interests me greatly in that they rely on their own countries for trading and sourcing. This stimulates their industry and helps to reduce cost. NAFTA exists and could potentially seek to do similar. The near shoring production process would reduce lead times and essentially speed up the process. In order to do this, the countries would need to work together and better establish production capabilities. The EU’s apparel market primarily resides in the EU. This helps to keep all of the country’s economies stable. The US on the other hand is experiencing growing pains when it comes to manufacturing. Trading within the region has helped better the EU economic state, and the NAFTA countries are missing out on an opportunity.

The EU is a large producer of textiles and apparel, but they really thrive in the medium and high quality products. Countries in the EU cannot compete with the cheap labor in Asia for cheaper products, so specializing in higher quality products is a good model. I was surprised though about how Europe does their sourcing. Most of their sourcing comes from within Europe. I could also see this as a way to keep costs down although they are making higher quality products. Europe is relatively small and many of their borders are tax free, so this is a way for companies in the EU to increase their profits.

I find it interesting that the US and EU are seen as equally developed regions and yet there is a substantial difference in the success of the T&A in each area. The EU is ranked as one of the largest producers of Textile and Apparel. Meanwhile, the US is struggling with its textile industry and creating deals with other countries in order to stimulate business for American textile companies. It feels as though the US is almost desperate for other counties to use their labor and supplies in the textile industry while it is a more natural flow for the EU to produce T&A. Should the US reevaluate its place in the textile industry?

The thing I found most interesting about this post is how the value of EU textiles and apparel are approximately equal. This was surprising to me because I would have thought EU countries have an edge when it comes to manufacturing textiles, not apparel, which would make textiles total more. It is a good sign for Europe because that means it does not have to rely on other countries for textile or apparel manufacturing. Also, I would imagine that the trade balance in apparel between the EU and Asia (especially China and India) will steadily favor EU because it offers luxury clothing. As wealth increases in large Asian countries, there will be a higher demand for these products which can only come from Europe due to the fact that the location is closely tied to the products.