Sub-Saharan Africa (SSA) is widely regarded as a growing apparel-souring destination. Particularly, U.S. Congress established the African Growth and Opportunity Act (AGOA), a non-reciprocal trade preference program, in 2000, to help developing SSA countries grow their economy through expanded exports to the United States. Because apparel production plays a dominant role in many SSA countries’ economic development, apparel has become one of the top exports for many SSA countries under AGOA. Notably, the “third-country fabric provision” under AGOA allows US apparel imports from certain SSA countries to be qualified for duty-free treatment even if the apparel items use yarns and fabrics produced by non-AGOA members, such as China, South Korea, and Taiwan. This special rule is deemed as critical as most SSA countries still have no capacity in producing capital and technology-intensive textile products.

That being said, to play a bigger role as an apparel sourcing base, SSA is not without significant challenges:

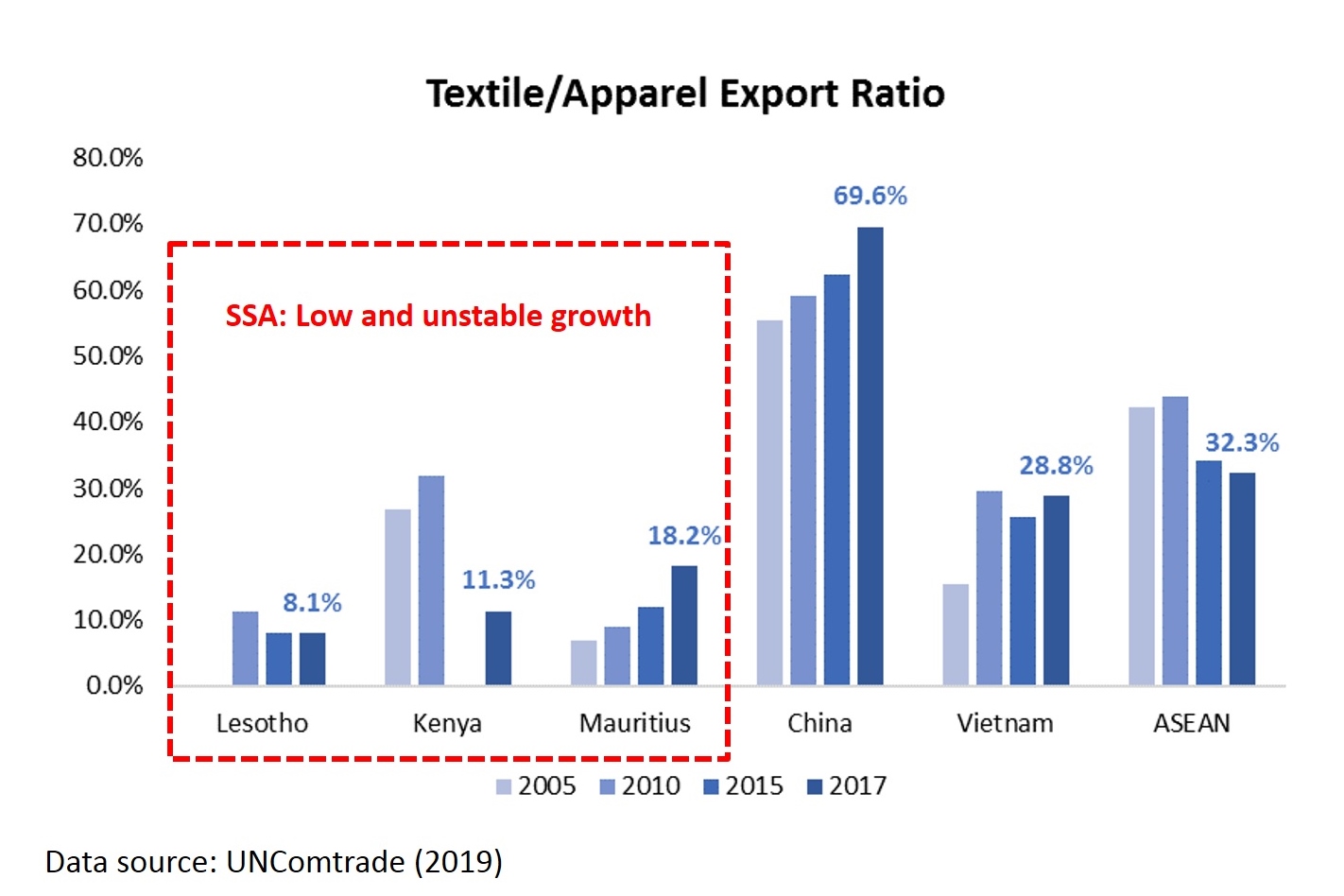

Challenge 1: limited industry upgrading and local textile production capacity

Theoretically, as a country’s economy advances, it should gradually be producing and exporting more capital and technology-intensive textiles versus labor-intensive apparel products. This is the notable trends in many Asian countries (such as China and Vietnam), where the textile/apparel export ratio has been rising steadily between 2005 and 2017. However, as a reflection of the stagnant industry upgrading, the textile/apparel export ratio remains fairly low in SSA, including in Lesotho, Kenya, and Mauritius, the top three largest apparel exporters in the SSA region.

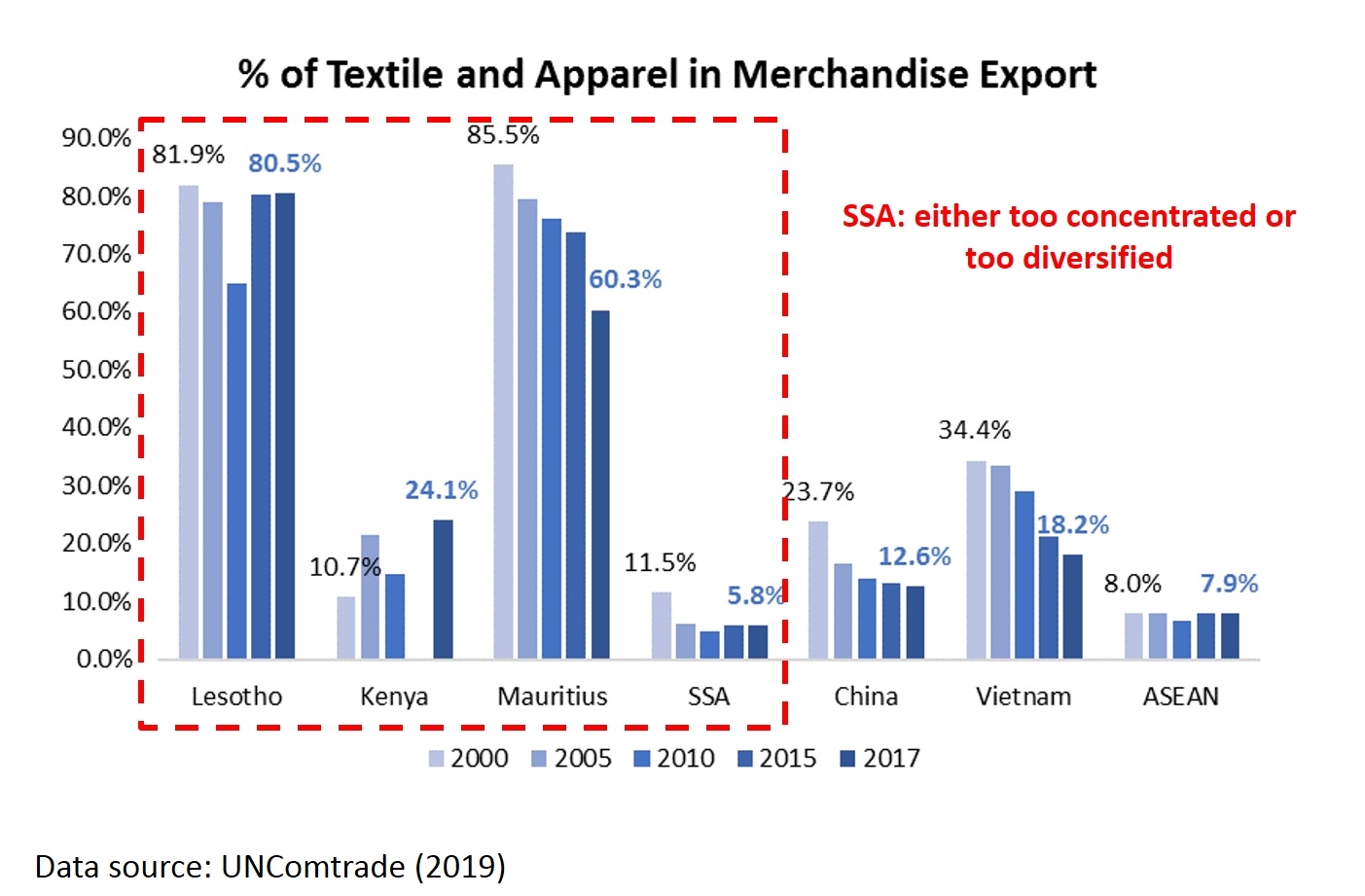

Challenge 2: Slow and no progress in export diversification

Ideally, as the economy becomes more sophisticated, textiles and apparel (T&A) should account for a declining share in a country’s total merchandise exports. Countries such as China, Vietnam, and ASEAN demonstrate perfect examples. However, in some SSA countries (e.g., Lesotho), T&A has stably accounted for over 80% of their total merchandise exports over the past 17 years, a sign of slow or no progress in export diversification. In other SSA countries, T&A accounted for less than 10% of their total merchandise exports, suggesting the sector is not a priority to the local economy.

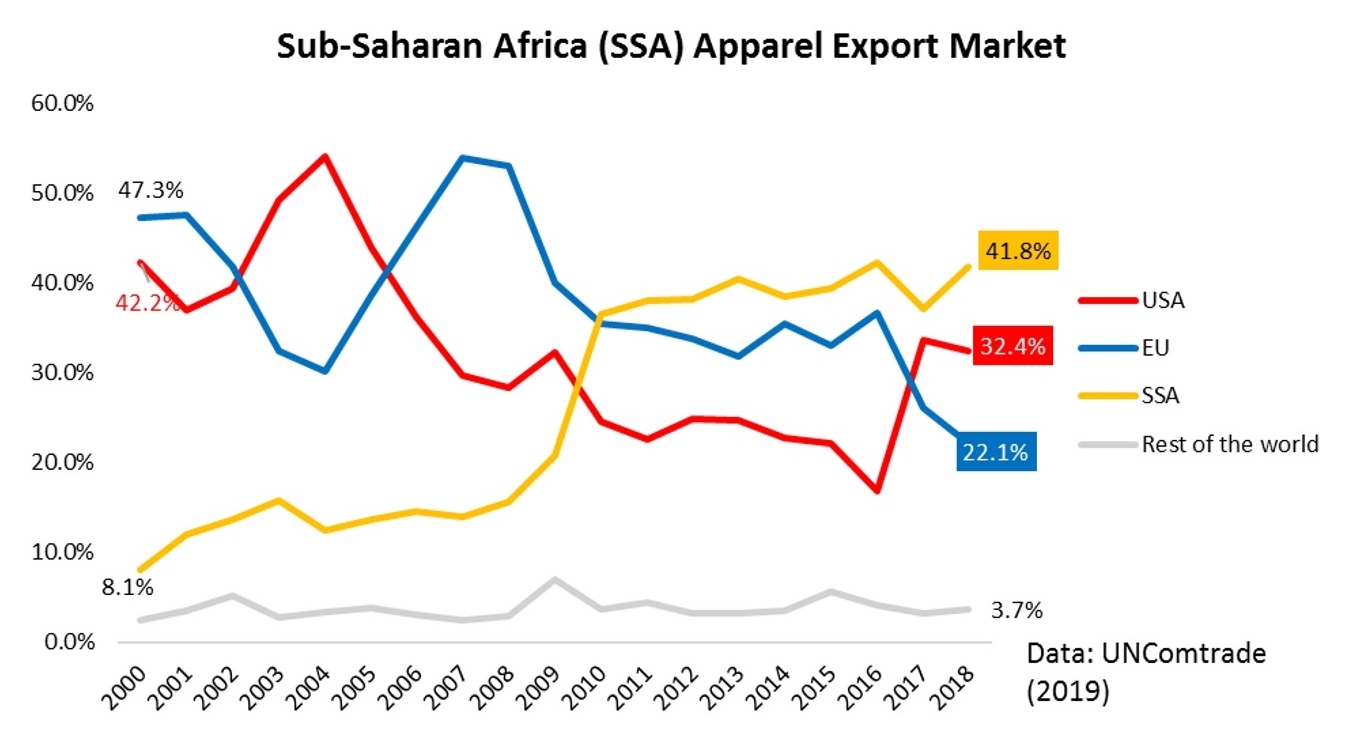

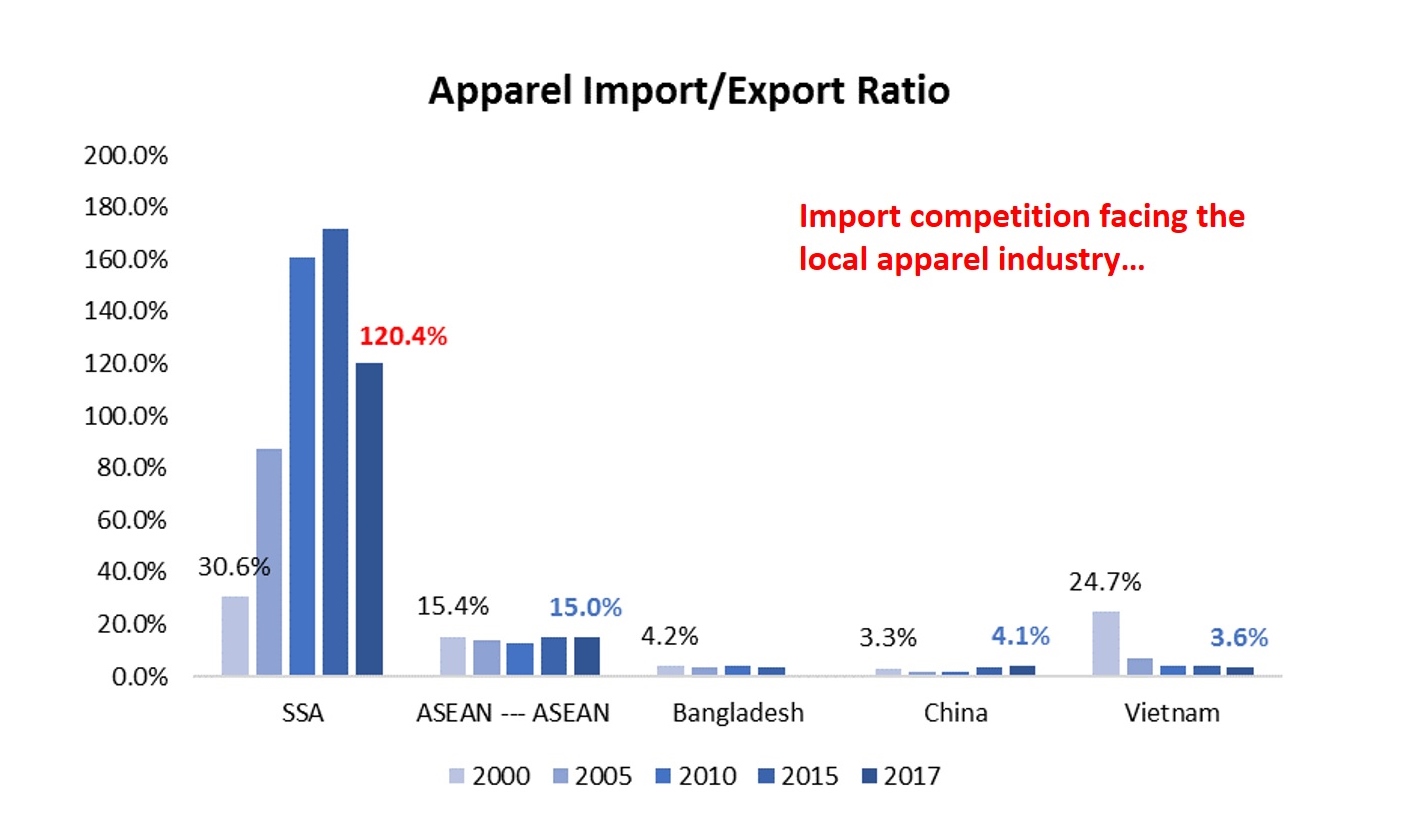

Challenge 3: Intense competition both in key export markets and domestic market

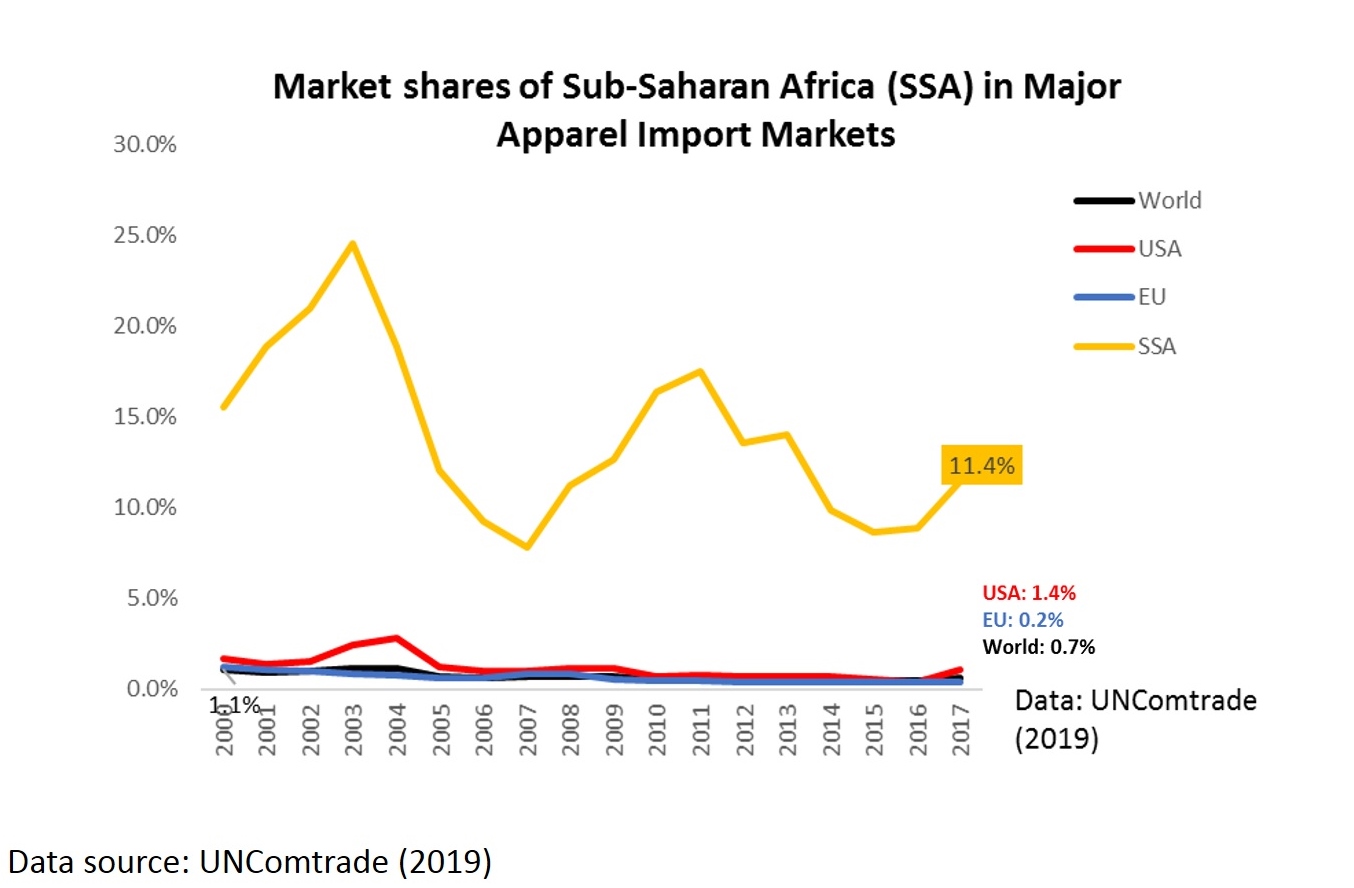

As of 2017, over 96% of SSA countries’ T&A exports went to three markets: the United States, the EU, and other SSA members. However, because of the intense competition, except for the regional SSA market, SSA countries account for merely 1.4% and 0.2% of total U.S. and EU textile and apparel imports in 2017 respectively.

Even more concerning, the T&A industry in SSA countries is facing growing competition in the domestic market with cheap imports, mostly from Asia. Notably, SSA countries import MORE apparel than they export, a phenomenon rarely seen among developing countries in a similar stage of economic development.

Challenge 4: U.S. companies remain low interest in investing in the region directly

According to several recent studies, leading U.S. fashion brands and retailers remain low interest in investing in the SSA region directly, even though companies admit more investments in areas such as infrastructure are critical to the success of SSA countries serving as competitive apparel sourcing bases. Some argue that the “temporary” nature of AGOA make companies hesitant to build factories in SSA. However, should AGOA become a permanent free trade agreement, which follows the principle of reciprocity, SSA countries would have to lower their trade barriers to U.S. products, including eliminating the tariffs and non-tariff barriers, in exchange for the reciprocal market access benefits from the United States. It doesn’t seem most AGOA members are ready for that stage yet.

by Sheng Lu

Further reading: