From watching the video (the first 18 minutes):

- What are the key challenges faced by fashion companies nowadays?

- How has the business model of fashion companies evolved?

- What’s your outlook for the U.S. fashion industry?

FASH455 Global Apparel & Textile Trade and Sourcing

Copyright© 2012-2026 Dr. Sheng Lu, Professor, Department of Fashion & Apparel Studies, University of Delaware

From watching the video (the first 18 minutes):

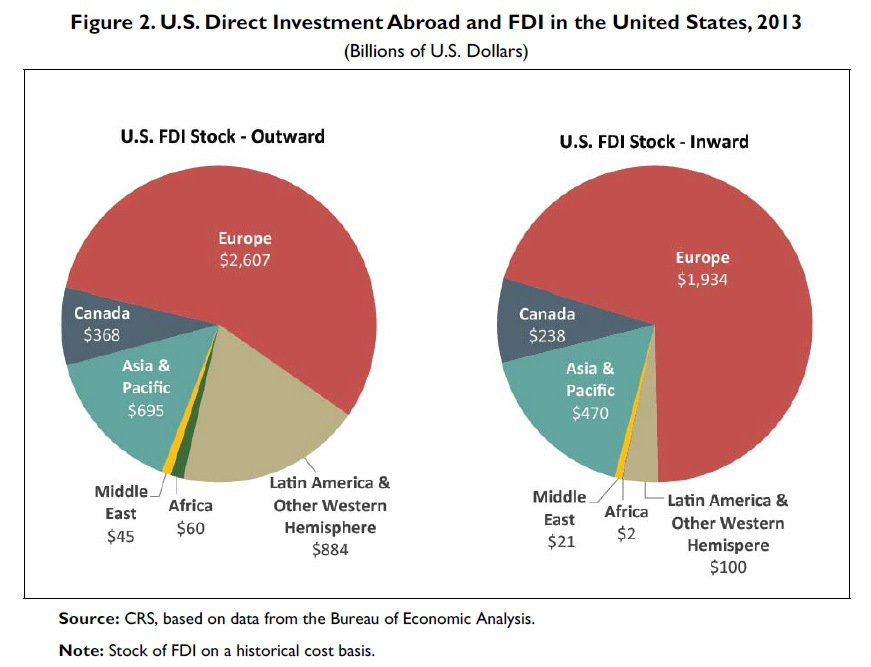

Foreign direct investment (FDI) is a major format of cross-border capital flow. It occurs when a company based in one country invests in physical productive assets in another country and obtains a controlling interest in the operation (Brookings, 2014).

Statistics show that in 2013 the total stock of global FDI exceeded $25 trillion, among which around 18.8% ($4.7 trillion) were made by U.S.-based companies. In the meanwhile, the United States is also a major FDI recipient, with the stock of FDI totaled $2.8 trillion by the end of 2013 (CRS, 2015). Europe is both the top destination of US FDI abroad (55.5%) and the largest source of FDI in the U.S. (70.1%).

Although historically developed countries have been the primary source of global FDI, in recent years, developing countries (especially emerging economies such as China) have played an increasing role in global investment. For example, according to a recent study released by the National Committee on US-China Relations, from 2000 to 2014, Chinese firms spent nearly $46 billion on new establishments and acquisitions in the U.S.. This includes Keer Group, a Chinese textile company, which invested $218 million in South Carolina to produce industrial cotton yarn products specifically for the China market.

It should be noted that in the 21st century FDI is considered to be a major driver of international trade. Particularly, a substantial share of international trade today is between parent firms and their foreign affiliates. For example, Statistics show that in 2012 the affiliates of foreign firms in the U.S. exported $334 billion or 21% of total U.S. exports and imported $671 billion or 29% of total U.S. imports. At the same time, U.S. parent companies (i.e. those companies made FDI overseas) exported $738 billion or 47% of total U.S. exports and imported $949 billion.

The U.S. textile and apparel industry (T&A) has been actively engaged in FDI as well. Data from the Bureau of Economic Analysis (BEA) show that in 2013 U.S. FDI abroad in the T&A industry reached $16.5 billion and FDI inflow reached $13.7 billion. The apparel retail sector (NAICS 448) in particular accounted for 85% of FDI inflow and 51% FDI outflow in the U.S. T&A industry. Interesting enough, data also show that FDI abroad made by the U.S. apparel manufacturers have substantially increased by 85.4% from 2009 to 2013, implying that U.S. apparel manufacturers may accelerate moving factories overseas rather than adding manufacturing capacity in the United States.

Last week, Milliken & Company, one of the largest U.S. textile manufacturers founded in 1865, was featured in a Wall Street Journal article on the changing position of the U.S. textile industry on international trade. As you may remember in our case study, it was Roger Milliken, the chairman of the Milliken & Company, that founded the Crafted with Pride in the U.S.A. campaign in the 1980s. The campaign not only encouraged U.S. consumers to purchase more “Made in USA” products, but also intended to raise the public awareness of “import threat”. However, titled “free trade gains a convert”, the WSJ article argues that Milliken & Company today has “dropped protectionist stance as business went global”.

The article is a great reminder of the changing nature of the U.S. textile industry in the 21st century. One of them is going global. According to the Hoover’s Academics (2015). Milliken & Company today operates about 40 manufacturing plants in the US, Belgium, China, France, and the UK, as well as sales and services offices worldwide. In particular, as mentioned in the WSJ article, China nowadays is seen as Milliken & Company’s future. The company opened an industrial-carpet factory near Shanghai in 2007 and also moved its Asia headquarters from Tokyo to Shanghai in 2012. And rather than using Chinese labor to make goods for export back to the United States, most Milliken & Company’s products made in China target the local market. As estimated by GlobalData, urbanization and an increase in house ownership in developing countries like China, India, Vietnam, Thailand and Indonesia have led to an annual 7.9% growth of carpets and rug sales in the region.

It is also important to recognize that Milliken & Company’s business model is no longer based on manufacturing basic yarn or fabrics used for apparel. Instead, the company mostly produces highly tech-driven and capital intensive industrial textiles as well as chemicals and colorants that offer more than 100 applications including infusing washable markers and liquid laundry detergent, killing bacteria, melting ice, and blocking UV rays. In many industry sources, Milliken & Comopany is even counted as a chemical company that directly competes with industry giants such as DuPont, Dow Chemical and Shaw industries. Overall, it is product and business innovation that drive this hundred-old company moving forward.

Additionally, we shall not misread title of the WSJ article—i.e. the U.S. textile industry 100% supports free trade with no condition. As a matter of fact, the rules regulating global textile and apparel trade are still very complicated and restrictive in nature. For example, the U.S. textile industry still insists strict yarn-forward rules of origin to be adopted in the Trans-Pacific Partnership (TPP) and the Trans-Atlantic Trade and Investment Partnership (T-TIP). However, many U.S. apparel companies and fashion brands see the restrictive yarn-forward rule of origin outdated and incompatible with the 21st century global apparel supply chain.

No matter how, it is a noticeable change that the U.S. textile companies like Milliken start to shift their position on international trade, even just in a subtle way. Globalization has demonstrated its impact on shaping the new landscape of the U.S. textile industry and will continue to do so in the years to come.

[Updated data is available: U.S. Continues to Lose Apparel Manufacturing Jobs in 2016]

It may disappoint those who are hoping a return of apparel “Made in USA”, but according to the latest statistics from the Bureau of Labor Statistics, the U.S. apparel manufacturing sector (NAICS 315) lost another 4.2% jobs from April 2014 to April 2015. From January 2008 to April 2015, about 86,800 jobs (or 39%) in the U.S. apparel manufacturing sector had disappeared.

From the academic perspective, a sizable return of apparel manufacturing job in the United States seems to be extremely unlikely given the nature of the U.S. and global economy in the 21st century.

First, it is all about comparative advantage suggested by classic trade theories. The World Bank data show that from 1980 to 2010, the U.S. GDP increased by 424% (note: world GDP increased by 484% over the same period) whereas the total U.S. population was only 23% higher in 2010 than in 1980 (note: world population increased by 65.21% over the same period). This suggests that the United States actually is becoming more capital & technology abundant with less comparative advantage in manufacturing labor intensive apparel. A sizable return of apparel manufacturing in the United States might only happen in the following two occasions: 1) apparel manufacturing can be automated like textile manufacturing; 2) substantial amount of foreign workers were allowed to work in the United States. Unfortunately, neither of the two occasions seem likely to happen at least in the near future.

Second, it is about US apparel company’s business model in the 21st century. The suggested dominant types of apparel companies in the United States today are “branded manufacturers” and “marketers” whose business models heavily rely on global sourcing and non-manufacturing activities such as branding, marketing and design (Gereffi, 1999). If you carefully read US apparel companies’ annual reports, seldom you’ll see a company still regards “manufacturing” as a key competitive advantage or an area of strategic importance to invest in the future.

Additionally, according to data from the U.S. Bureau of Economic Analysis (BEA), the percentage of compensation of employees in the apparel industry’s total value added has been gradually declining since 2008. Similar trend is also observed in the U.S. economy and the U.S. manufacturing sector as a whole. Does the result imply that labor input is becoming less important to the output of the U.S. apparel industry? Or does the result suggest that U.S. apparel companies are more willing to invest on buying machines than hiring more people? Maybe it is the time that we shall pay more attention to the labor-capital substitution trend in the U.S. apparel industry.