On November 16, 2018, leading U.S. textile and apparel associations testified before the U.S. International Trade Commission (USITC) to provide industry assessments of the U.S. Mexico Canada Agreement (USMCA, or commonly called “NAFTA2.0”). Below is a summary of these associations’ comments:

First, both the U.S. textile industry and the U.S. apparel industry expressed overall support for USMCA, which is regarded as critical for maintaining the Western-Hemisphere textile and apparel supply chain.

National Council

of Textile Organizations (NCTO): “In an

overarching fashion, the new agreement is an improvement over the original

NAFTA in many areas.”… “The United States, Canada and Mexico have

built a vibrant and prosperous textile production chain over the 24 years

through NAFTA.”

U.S. Fashion

Industry Association (USFIA): “We reviewed the details of the USMCA, and we

were pleased to find much we can support in it.” “USMCA remains a trilateral agreement, and “does no harm”

to existing U.S.-Mexico-Canada supply chains.”

American Apparel and Footwear Association (AAFA): “…state our very strong support of the North American Free Trade Agreement (NAFTA). NAFTA serves as an important anchor for the U.S. textile, apparel, and footwear industry. Much of the textile manufacturing in the United States is tied directly to NAFTA through U.S. exports to NAFTA partners.”…” The USMCA appears to have largely met the goal of “do no harm”. We were pleased to see the USMCA retain this essential trilateral feature.”

Second, not surprisingly, the U.S. textile industry and U.S. fashion brands and apparel retailers hold divided views on the textile and apparel specific rules of origin provision in USMCA—particularly the tariff preference level (TPL). In general, the U.S. textile industry welcomes the changes that limit the usage of-USMCA originating textile inputs, whereas U.S. fashion brands and retailers ask for more flexibilities. Further, even though the agreement seems to be a balanced deal, both the two sides expressed “dissatisfactions” for what they did not get.

Regarding the yarn-forward

rules of origin

NCTO: “We are

pleased that the basic textile origin rules adopted originally in NAFTA were essentially reaffirmed in USMCA. Commend

the creation of a separate textile chapter, which recognized the sensitivities

associated with trade in this sector and allows for unique provisions.”

USFIA: “The

yarn-forward rule of origin already discourages trade in our sector—and some

companies have told us that they don’t claim the duty savings on eligible

products from the region because the compliance requirements are simply too

onerous and expensive.”

Regarding the

tariff preference level (TPL)

NCTO: “While USMCA did reduce the size of some specific TPLs,

the reductions will not cut into existing trade levels. This outcome is

frustrating given the President’s stated goals of increasing benefits for U.S.

manufacturers and eliminating provisions that have helped non-signatory

countries, such as China, taking advantage of tariff preferences intended for

North American producers.”

USFIA: “The

agreement maintains the Tariff Preference Levels (TPLs) for apparel to and from

all three countries. This is one of the

most important elements of the agreement for our industry, and according to

some of our members, the only way they can source textiles and apparel with

these trading partners.”… “We also applaud the elimination of the requirement

that visible linings for tailored clothing come from the NAFTA region. The

maintenance of the TPLs and the elimination of the visible linings

requirement–will help companies continue and expand business with our trading

partners Canada and Mexico.”

AAFA: “we

are discouraged that… the changes made to the rules of origin were to introduce

more restrictive approaches. For example, many tariff preference levels (TPLs) were

lowered…”

“As we argued throughout the talks, the best way to encourage more U.S. content is to weave in more flexibility into the rules. Such flexibilities provide additional opportunities for business to be conducted under the agreement. For example, the USMCA dramatically increases the TPLs that will enable more U.S. apparel and made up goods to be exported to Canada. Even though such articles don’t have to be made with U.S. textiles, the mere presence of their production in the U.S. will mean more customers for U.S. textile firms.”

Sewing thread, pocketing,

narrow elastics and coated fabrics requirements

NCTO: ”We are

very supportive of revisions that will require the use of USMCA-origin sewing

thread, pocketing, narrow elastics and coated fabrics in certain end

items—which will offer a boost for U.S. producers formerly left out of the

origin rules in the original NAFTA ($250 million annual demand for sewing

thread and $70 million for pocketing in the USMCA market).”

USFIA: “the

USMCA creates new technical requirements –for example, the addition of requirements

for originating sewing thread, pocketing and narrow elastic bands—which will

result in higher costs for inputs and higher costs for brands and retailers (as

well as their suppliers in Mexico and Canada) to administer the agreement.”

“We are concerned that the addition of more regulatory

requirements to qualify for duty-free market access may hold back the ability

of some companies to expand their sourcing with Mexico and Canada.”…”There will

be some companies who shift operations out of the Western Hemisphere, or decide

not to move new orders to Canada or Mexico because of these cost increases. The

new regulations WILL make it more expensive and complicated for American brands

and retailers to use the agreement.”

AAFA: “we are

discouraged that – with few exceptions – the changes made to the rules of

origin were to introduce more restrictive approaches. For example, many tariff

preference levels (TPLs) were lowered and the USMCA now includes new requirements

that sewing thread, elastic strips, and pocketing originate. While we

understand U.S. negotiators were attempting to legislate more U.S. content into

North American textile and apparel supply chains, the result, unfortunately,

may be the opposite.”

Additionally, theU.S. textile industry is pleased with the changes to the government procurement provision, which closed a “loophole” regarding the Kissell Amendment.

NCTO: “We are also appreciative of a key change made in the

Government Procurement Chapter of USMCA regarding the Kissell Amendment, which

is a Buy American statute for textiles that applies to the Department of

Homeland Security (DHS). Kissell requires

100% U.S. content, with very limited exceptions, for purchases by the Coast

Guard and Transportation Security Administration (TSA).

Regarding TSA procurement, Kissell has a problematic loophole tied to NAFTA that has allowed Mexico to supply these contracts. As a result, under the terms of NAFTA, Mexico can supply TSA uniforms made from Mexican fiber, yarn, and/or fabric. The TSA Mexico loophole translates to a significant weakening of U.S. Buy American statutes. Noting that DHS spent $34million on clothing and textiles for TSA in FY2017, closing the Kissellloophole was a substantive change from NCTO’s perspective.”

[Note: Not like NAFTA, USMCAwill exclude FSC 83 (Textiles, Leather, Furs, Apparel, Shoe Findings, Tents, and flags) and FSC 84 (Clothing, Individual Equipment, and Insignia and Jewelry)from the procurement list of the Department of Homeland Security (DHS) that opens to Mexico and Canada.]

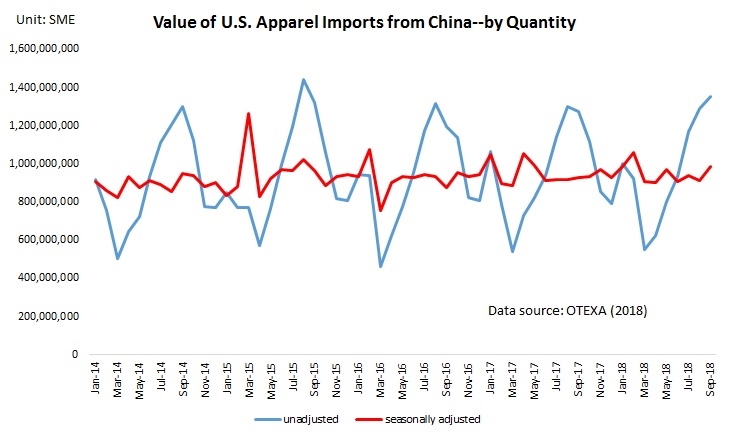

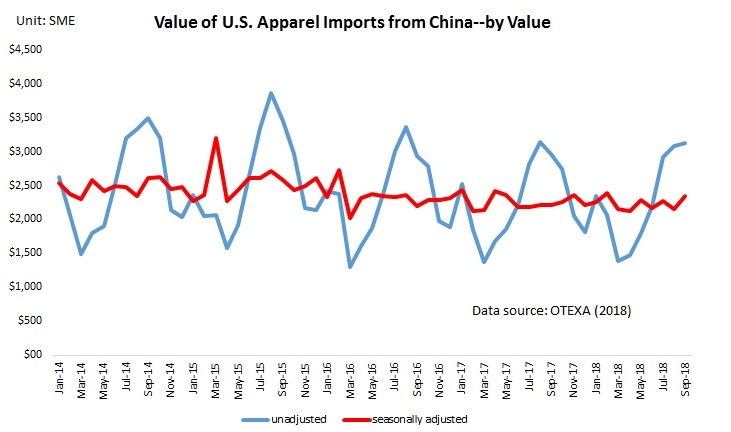

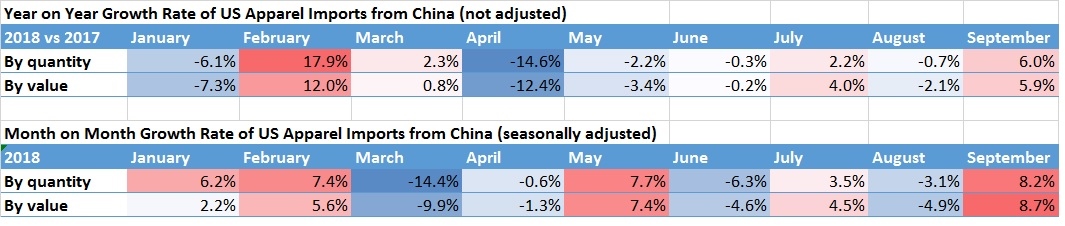

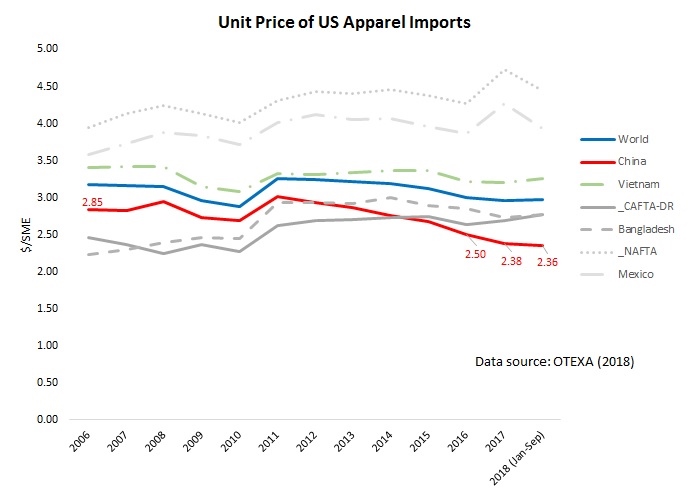

Appendix: