While apparel products are not subject to the Section 301 tariff yet, the trade action nevertheless has created huge market uncertainties for U.S. fashion brands and apparel retailers. Here is how the monthly trade flow of U.S. apparel imports has reflected the impacts of the U.S.-China tariff war:

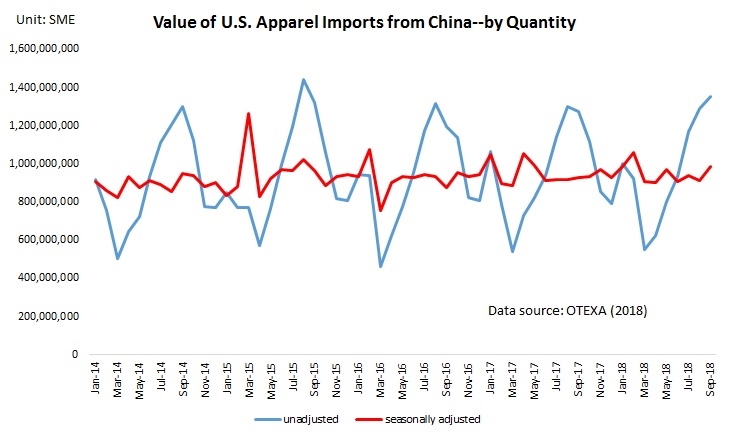

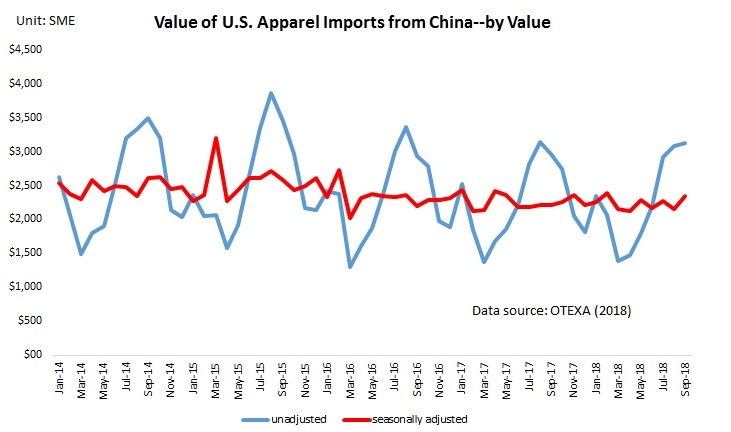

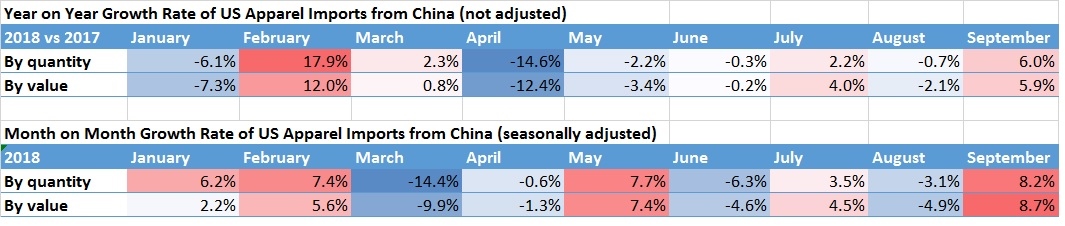

First, U.S. companies did NOT stop importing from China. Seasonally adjusted data shows that between January and September 2018, the value of U.S. apparel imports from China decreased by 0.6 percent in volume and 0.05 percent in value year on year. Despite the decline, China remained the No.1 apparel supplier for the U.S. market in the first nine months of 2018, accounting for 32.3 percent market share in value and 41.3 percent shares in quantity, only marginally dropped by 1 and 0.7 percentage points from a year earlier respectively .

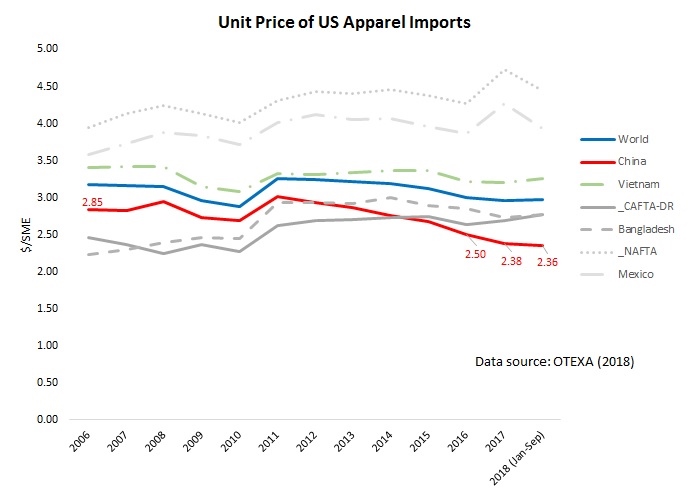

Second, apparel “Made in China” are becoming even cheaper. Notably, the average unit price of U.S. apparel imports from China dropped from $2.5/SME in 2016,$2.38/SME in 2017 to $2.36/SME in the first nine months of 2018. On the one hand, this result suggests that cost concern is not the most influential factor that drives U.S. companies to source less from China. However, it is also likely that Chinese exporters are intentionally reducing their price to keep their orders and overcome the challenges caused by the Section 301.

Third, there is no perfect replacement for “Made in China”. In response to the market uncertainty created by the Section 301 trade action, U.S. apparel importers are diversifying their sourcing base. That being said, it is difficult to identify a single largest beneficiary–notably, the market shares of apparel exports from Vietnam, Bangladesh, NAFTA, and CAFTA regions only marginally increased in the first nine months of 2018 compared with a year ago.

Additionally, it remains unclear whether the section 301 trade action has benefited U.S. textile and apparel manufacturing. Data shows that in the first ten months of 2018, the production index (2012=100) of textile manufacturing in the United States slightly increased from 92.8 in 2017to 94.3. However, over the same period, the index of apparel manufacturing decreased from 73.6 to 72.4.

Looking ahead, the volume of US textile and apparel imports from China is likely to increase in the short run since U.S. importers are eager to complete their sourcing orders before the new tariff hit. Usually, companies place sourcing orders several months ahead of the selling season. However, it will be interesting to see if the trade data in the first half of 2019 will reveal the negative impact of the Section 301 action on China’s apparel exports to the U.S. market.

Data source: Office of Textiles and Apparel (OTEXA), US Department of Commerce

by Sheng Lu