On April 19, 2019, the U.S. International Trade Commission (USITC) released its independent assessment report on the likely economic impact of the U.S.-Mexico-Canada Free Trade Agreement (USMCA or NAFTA2.0). Below are the key findings of the report:

Impact of USMCA on the U.S. economy

USITC found that because of the size of the U.S. economy relative to the size of the Mexican and Canadian economies and the reduction in tariff and nontariff barriers that has already taken place among the three countries under the North American Free Trade Agreement (NAFTA), the overall impact of USMCA on the U.S. economy is likely to be moderate. For example, USITC’s computable general equilibrium (CGE) model suggests that compared to the base year level in 2017, USMCA could increase the U.S. GDP by 0.35% (or $68.2 billion) and create 0.17 million new jobs when other factors held constant.

Impact of USMCA on the textile and apparel sector

First, USITC found that the USMCA overall is a balanced deal for the textile and apparel sector, particularly regarding the rules of origin (RoO) debate. As USITC noted, USMCA eases the requirements for duty-free treatment for certain textile and apparel products, but tighten the requirements for other products. For example, USMCA eliminates the NAFTA requirements that visible linings must be sourced from members of the agreement; however, USMCA adds more restrictive new requirements for narrow elastic fabrics, sewing thread, and pocket bag fabric.

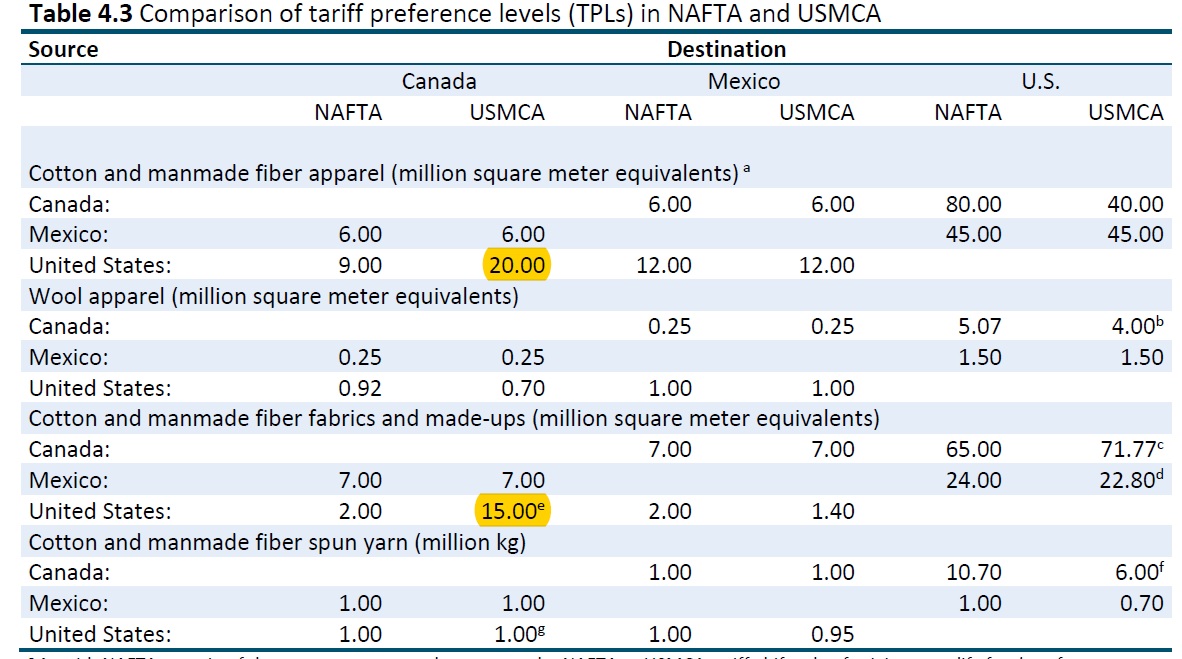

Second, USITC found that the USMCA changes to the Tariff Preference Level (TPLs) would not have much effect on related trade flows. As USITC noted in its report, where USMCA would cut the TPL level on particular U.S. imports from Canada or Mexico, the quantitative limit for these product categories was not fully utilized in the past. Meanwhile, the TPL level for product categories typically fully used would remain unchanged under USMCA. The only trade flow that might enjoy a notable increase is the U.S. cotton and man-made fiber (MMF) apparel exports to Canada—the TPL is increased to 20million SME annually under USMCA from 9 million under NAFTA.

Third, USITC suggested that in aggregate, the changes under USMCA for the textile and apparel sector will more or less balance each other out and USMCA would NOT affect the overall utilization of USMCA’s duty-free provisions significantly. Notably, the under-utilization of free trade agreements (FTAs) by U.S. companies in apparel sourcing has been a long-time issue. Data from the Office of Textiles and Apparel (OTEXA) shows that of the total $4,292.8 million U.S. apparel imports from the NAFTA region in 2018, only $3,756.1 million (or 87.5%) claimed the preferential duty benefits under the agreement. As noted in the U.S. Fashion Industry Benchmarking Study, some U.S. fashion companies do not claim the duty savings largely because of the restrictive RoO and the onerous documentation requirements.

However, interesting enough, the USITC report says little about the potential impact of USMCA on U.S. textile and apparel manufacturing.

Timeline

On 30 September 2018, the United States reached USMCA with Canada and Mexico. On 30 November 2018, USMCA was officially signed by Presidents of the three countries. According to the Bipartisan Congressional Trade Priorities and Accountability Act of 2015 (the picture above), after the release of the USITC economic assessment report on USMCA, the Trump Administration will need to work with U.S. Congress to develop legislation to approve and implement the agreement. However, there remains huge uncertainties over USMCA’s prospect.

Related reading: