The UK government on March 13, 2019 released the temporary

rates of customs duty on imports if the country leaves the European Union

with no deal. In the case of no-deal Brexit, these tariff rates will take

effect on March 29, 2019 for up to 12

months.

According to the announced plan, around 87% of UK’s imports by value would be eligible for zero-tariff in the no-deal Brexit scenario.

Specifically for apparel products, 113 out of the total 148 tariff lines (8-digit HS code) in Chapter 61 (Knitted apparel) and 145 out of the total 194 tariff lines (8-digit HS code) in Chapter 62 (Woven apparel) will be duty-free. However, other apparel products will be subject to a Most-Favored-Nation (MFN) tariff rate ranging from 6.5% to 12%.

Meanwhile, the UK will offer preferential tariff duty rates for apparel exports from a few countries/programs, including Chile (zero tariff), EAS countries (zero tariff), Faroe Islands (zero tariff), GSP scheme (reduced tariff rate), Israel (zero tariff), Least Developed Countries (LDC) (zero tariff), Palestinian Authority (zero tariff), and Switzerland (zero tariff).

On the other hand, the EU Commission said it would apply the Most-Favored-Nation (MFN) tariff rates on UK’s products in the no-deal Brexit scenario rather than reciprocate.

While U.S. textile manufacturers and the apparel and retail

industries have expressed overall support for the newly reached

US-Mexico-Canada Free Trade Agreement (USMCA or NAFTA2.0), textile producers

and the apparel sector still hold divergent views on certain provisions:

Textile “Yarn-Forward”

Rule of Origin

USMCA vs. NAFTA1.0: The

USMCA will continue to adopt the “yarn-forward” rules of origin. The USMCA will

also newly require sewing thread, coated fabric, narrow elastic strips, and

pocketing fabric used in apparel and other finished products to be made in a

USMCA country to qualify for duty-free access to the United States.

U.S. textile industry: U.S.

textile manufacturers almost always support a strict “yarn-forward” rules of

origin in U.S free trade agreements and

they support eliminating exceptions to the “yarn forward” rule as well. The

National Council of Textile Organization (NCTO) estimates that a yearly USMCA

market for sewing thread and pocketing fabric of more than $300 million.

U.S. apparel and retail

industries: The U.S. apparel industry opposes “yarn forward” and argues

that apparel should be considered of

North American origin under a more flexible regional “cut and sew” standard,

which would provide maximum flexibility for sourcing, including the use of

foreign-made yarns and fabrics.

Tariff Preference

Levels (TPL) for Textiles and Apparel

USMCA vs. NAFTA1.0: With some adjustments, the USMCA would continue a program that allows duty-free access for limited quantities of wool, cotton, and man-made fiber apparel made with yarn or fabric produced or obtained from outside the NAFTA region, including yarns and fabrics from China and other Asian suppliers.

U.S. textile industry: The

textile industry contends China is a major

beneficiary of the current NAFTA TPL mechanism, and it strongly pushed for its

complete elimination in the USMCA.

U.S. apparel and retail

industries: U.S. imports of textiles and apparel covered by the tariff preference level mechanism supply 13% of

total U.S. textile and apparel imports from Canada and Mexico. Apparel

producers assert that these exceptions give regional producers flexibility to

use materials not widely produced in North America.

Viewpoints on other Provisions in USMCA

U.S. textile industry: The

U.S. textile industry also opposes the USMCA newly allows visible lining fabric

for tailored clothing could be sourced

from China or other foreign suppliers, and it would permit up to 10% of a

garment’s content, by weight, to come from outside the USMCA region (up from 7%

in NAFTA1.0). The U.S. textile industry also welcomes that the USMCA would add specific textile verification and

customs procedures aimed at preventing fraud and transshipment. Additionally, the U.S. textile industry is also pleased

that the USMCA would end the Kissell

Amendment. The Kissell Amendment is an exception in NAFTA that allows

manufacturers from Canada and Mexico to qualify as “American” sources when Department

of Homeland Security (DHS) buys textiles, clothing, and footwear using

appropriated funds (about $30 million markets

for textiles, clothing, and shoes altogether).

U.S. apparel and retail

industries: Apparel importers are of

concern that the USMCA continue to incorporate the existing NAFTA short

supply procedure, which is extremely difficult to get a new item approved and

added to the list, limiting their flexibility to source apparel with inputs

from outside North America.

Finally, the report argues that “Regardless of whether the USMCA takes effect, the global competitiveness of U.S. textile producers and U.S.-headquartered apparel firms may depend more on their ability to compete against Asian producers than on the USMCA trade rules.”

Last week in FASH455, we discussed the unique critical role played by textile and apparel trade in generating economic growth in many developing countries. The developed countries also use trade policy tools, such as trade preference programs, to encourage the least developed countries (LDCs) making and exporting more apparel. However, a debate on these trade programs is that they have done little to improve the genuine competitiveness of LDCs’ apparel exports in the world marketplace, but instead have made LDCs rely heavily on these trade programs to continue their apparel exports. Here is one more example:

With growing concerns about “the deterioration of democracy, respect for human rights and the rule of law in Cambodia”, in a statement made on February 12, 2019, the European Union says it has started the process that could lead to a temporary suspension of Cambodia’s eligibility for EU’s Everything But Arms (EBA) program. Specifically, the EU process will include the following three stages:

Stage 1: six

months of intensive monitoring and engagement with the Cambodian government;

Stage 2: another three months for the EU to produce a

report based on the findings in stage 1

Stage 3: after

a total of twelve months in stages 1

& 2, the EU Commission will conclude the procedure with a final decision on

whether or not to withdraw tariff preferences; it is also at this stage that

the Commission will decide the scope and duration of the withdrawal. Any

withdrawal would come into effect after a further six-month period.

However, the EU

Commission also stressed that launching the temporary withdrawal procedure does

not entail an immediate removal of Cambodia’s preferential access to the EU

market, which “would be the option of last resort.”

Developed in 2001, the EBA program establishes duty-free and quota-free

treatment for all Least Developed Countries (LDCs) in the EU market. EBA includes

almost all industries other than arms and armaments. As of February 2019, there

are 49

EBA beneficiary countries.

The EBA program has benefited the apparel sector in particular given clothing accounts for the lion’s share in many LDCs’ total merchandise exports. Because of the preferential duty benefits provided by EBA, many LDCs can compete with other competitive apparel powerhouses such as China. Notably, the EBA program also adopts the “cut and sew” rules of origin for apparel, which is more general than the “double transformation” rules of origin typically required by EU free trade agreement and trade preference programs. Under the “cut and sew” rule, Cambodia’s apparel exports to the EU can enjoy the import duty-free treatment while using yarns and fabrics sourced from anywhere in the world.

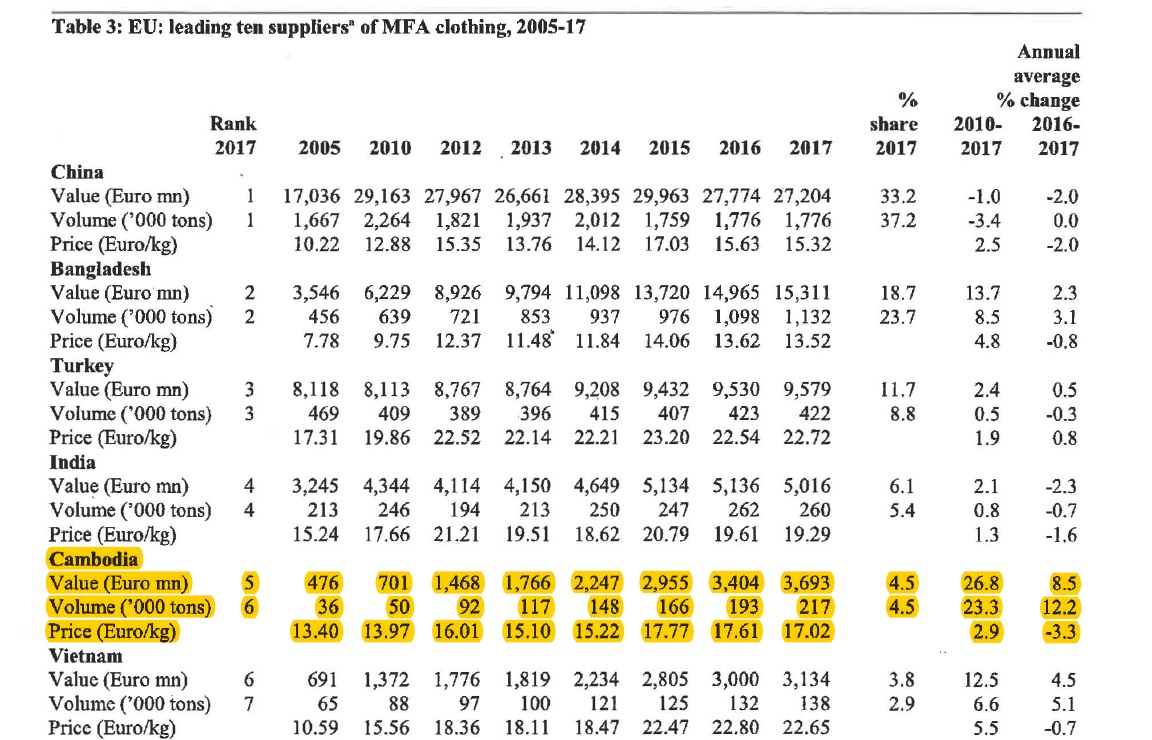

Cambodia is a major apparel supplier for the EU market, accounting for approximately 4% of EU’s

total apparel imports in 2017. Exporting

apparel to EU through the EBA program is also of particular importance to

Cambodia economically. In 2016, the apparel sector created over 500,000

jobs in Cambodia, of whom 86% were female, working in 556 registered factories.

According to Eurostat, of EU’s €4.9bn imports from Cambodia in 2017, around 74.9% were apparel (HS chapters 61 and

62). Meanwhile, of EU’s €3.7bn apparel imports from Cambodia in 2017, as high

as 96.6% claimed the EBA benefits. Understandably,

losing the EBA eligibility could hurt Cambodia’s apparel exports to the EU significantly.