A recent survey of 294 apparel companies and 20 apparel industry clusters* in China was conducted by the China Garment Association between February 19 and 20, 2020, aiming to understand the impact of the coronavirus (2019-nCoV) on China’s garment industry and production. The respondents of the survey include both garment factories (63.3%) and apparel brands (36.7%). Around 83.4% surveyed companies reported over RMB20 million (or $2.85million) sales revenues. Below are the key findings:

State of Production

- 68.4% of surveyed companies say they have gradually resumed production. Of these companies, about 45.6% of their workers in need have returned. The surveyed companies also expect their production output to reach 50% of its normal level by March and could fully recover by April, should the situation stabilized.

- However, still, as many as 31.6% of surveyed companies say they have not resumed production because of a mix of factors ranging from the need to prevent coronavirus, government restrictions, to the difficulty in recruiting workers. Further, for apparel companies from areas most affected by the coronavirus, they report no plan for reopening anytime soon.

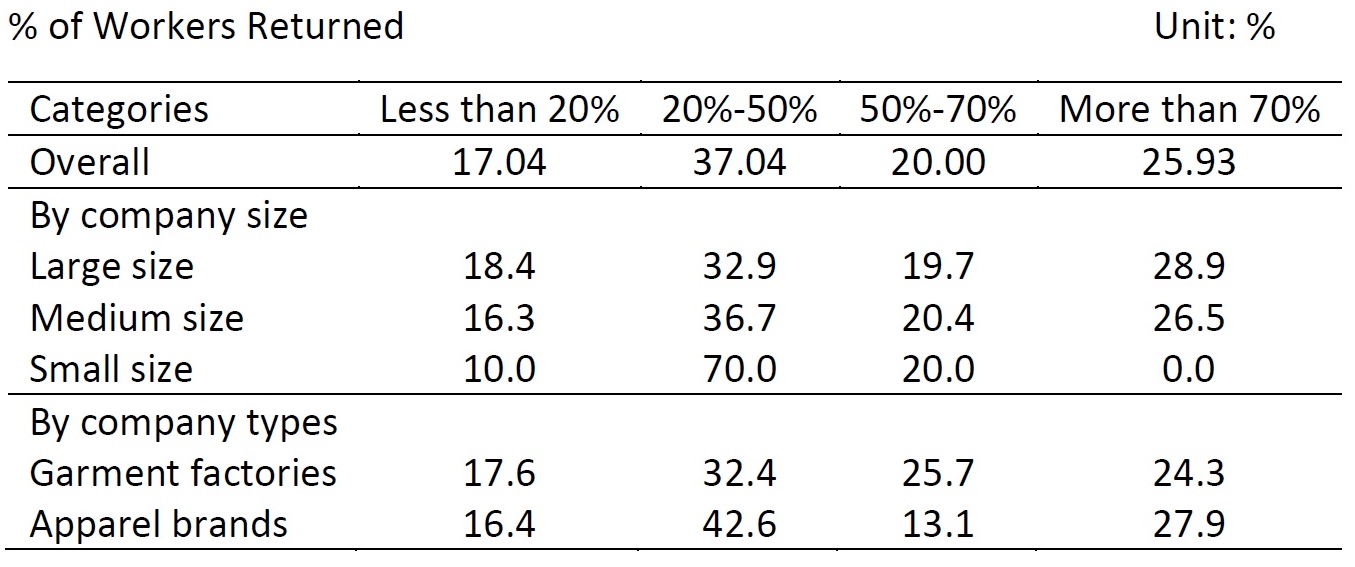

- Around 87.2% surveyed “large companies” have resumed production, much higher than “medium-sized” (65.4%) and “small-sized” (34.7%) enterprises. [Note: according to China’s Bureau of Statistics, for manufacturers, “large companies” typically refer to those with over 1,000 employees and over RMB400 million (or $57million) annual sales revenue; “small or mini-sized companies” are those with employees less than 200 and less than RMB3million (or $0.43million) annual sales revenues. “medium-sized companies” are those in between].

- Further, around 74.3% of surveyed apparel brands have resumed business operations, higher than 64.9% of garment factories. Meanwhile, some apparel brands say only their management team have resumed work or those positions that can be done through work from home; however, their plants remain closed.

- Over half of the surveyed companies (54.08%) say less than 50% of their workers have returned. The lack of workers is a more pressing issue for small-sized companies, with over 80% having less than 50% of workers returned.

Key challenges facing the surveyed companies:

- #1: Lack of workers, especially to have those workers from other parts of China return to the factory due to travel restrictions (68.7%)

- #2: Production cost increase and a lack of supply of raw material from the upstream sector (29.9%)

- #3: Slow and stagnant sales, overstock of finished products due to delayed orders and tight with cash flows (20.6%)

- #4: Weak market demand and cancellation of orders (19.2%)

- #4: Disrupted logistics and transportation (19.2%)

- #6: Hard to procure protective equipment for staffs and workers (such as facial masks) (16.8%)

- #7: Cancellation of exhibitions, harder to explore markets and more financial burdens (8.4%)

(*Note: apparel industry clusters refer to geographic concentrations of interconnected factories that manufacture a particular type of apparel product)

Related reading: Apparel Sourcing in the Shadow of Coronavirus (updated February 2020)