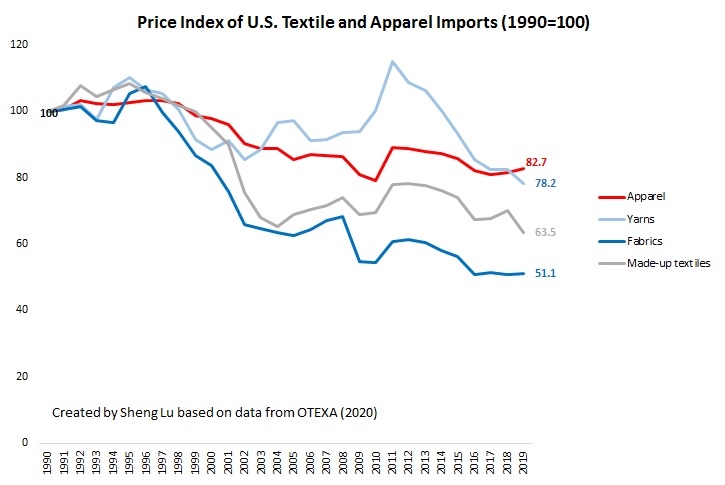

The top challenge facing apparel sourcing and trade in the shadow of Covid-19 has quickly shifted from a lack of textile raw material to order cancellation. In major apparel consumption markets such as the EU and US, clothing stores are locked down, making retailers have no choice but to postpone or even cancel sourcing orders.

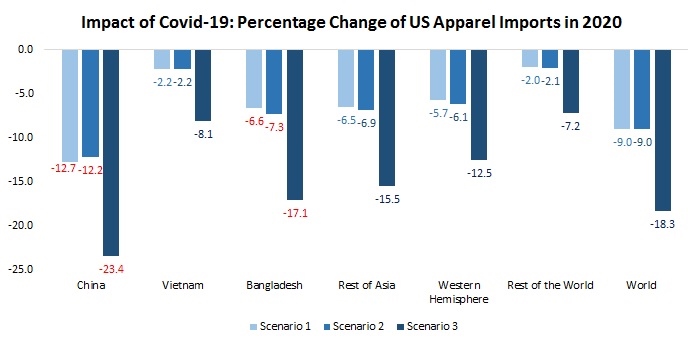

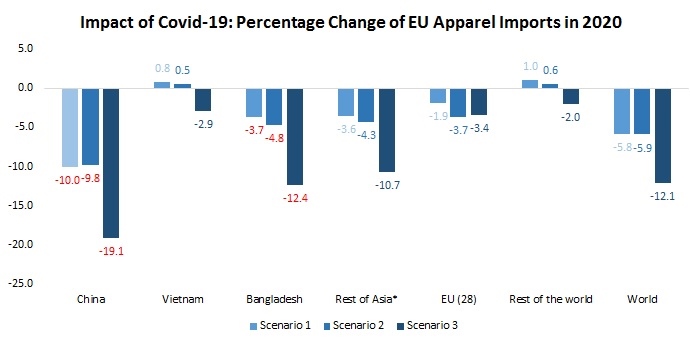

Based on the Global Trade Analysis Project Recursive Dynamic (GTAP-RD) Model and its latest database, we estimated the trade impact of Covid-19 in three possible scenarios, as summarized in the table below. All these three scenarios are pretty bad but likely situations we may have to face this year. (Note: Because China, US, and EU are the epic-centers of Covid-19, in the study, we assume these three countries/regions’ economies will be hit harder than the rest of the world.)

There are four preliminary findings:

First, the volume of the world apparel trade will be hit hard by Covid-19. As clothing stores are forced to shut down and consumers are losing jobs and struggling financially, the demand for apparel consumption in the EU and US, the world’s top two apparel consumption markets, is expected to drop sharply. As shown in the figures below, every 1% decline in the US and EU Gross Domestic Product (GDP) in 2020 could lead to at least a 2-3% drop in the value of their apparel imports. Notably, during the 2008 financial crisis, the value of world apparel imports also decreased by as much as 11.5% when the EU and US GDP suffered a 2.5-3% negative growth.

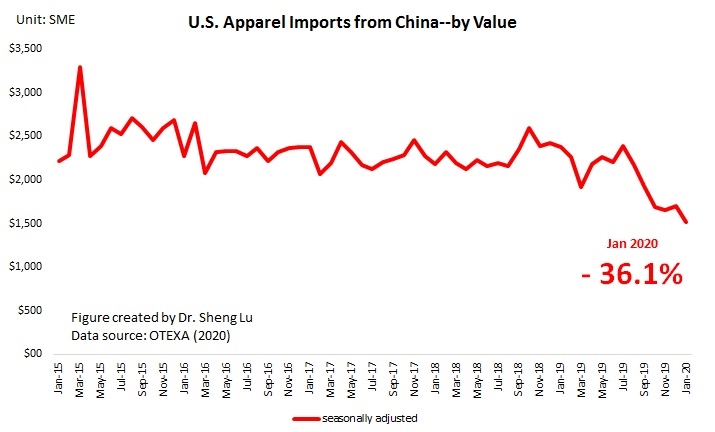

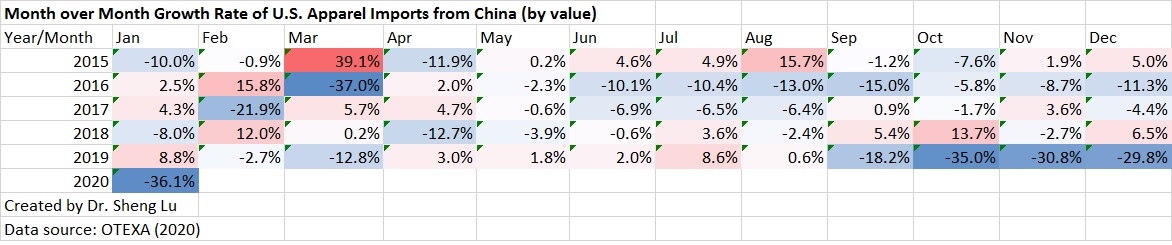

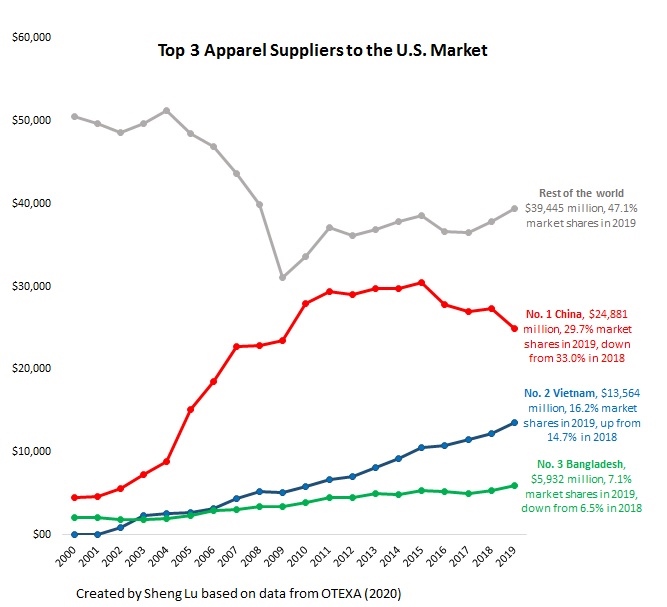

Second, with a sharp decline in U.S. and EU apparel imports this year, China could be hit the hardest. In all the three scenarios we estimated, China will suffer the most significant drop in its apparel exports to the US and EU markets. The reasons are threefold: The first factor is the size effect—as the largest source of US and EU apparel imports and with its unparalleled production capacity, China is often used to fulfill large-volume sourcing orders. In the current situation, however, retailers are most likely to cancel these large-quantity orders, resulting in a disproportional loss of China’s apparel exports. Secondly, the US and EU apparel imports from China currently cover almost all major categories, which also makes China the most exposed to order cancellation. Furthermore, jointly affected by last year’s US-China trade war and the outbreak of Covid-19 in China earlier this year, many US and EU fashion brands and retailers have been shifting sourcing orders from China to other Asian countries, such as Bangladesh and Vietnam. To prioritize their limited resources, US and EU retailers are most likely to accelerate this process in the current difficult time.

Other than China, apparel factories in Bangladesh also could suffer severe export decline. Similar to the case of China, Bangladesh serves as a leading apparel supplier for BOTH the EU and US markets, making it more exposed to order cancellation than other countries. Notably, as a beneficiary of the EU Everything But Arms (EBA) program, around 60% of Bangladesh’s apparel currently go to the EU. In comparison, with a more diversified export market, apparel factories in Vietnam are in a better position and have more flexibility to mitigate the impact of a declined import demand from the EU and the US. In 2018, around 40% of Vietnam’s apparel exports went to other markets in the world.

Third, the decreased US and EU apparel imports will have a notable impact on employment in many apparel exporting countries. In history, a 10% change in the value of apparel exports typically results in a 4%-9% change in garment employment. This means, should the US and EU apparel imports drop by 10% in 2020, leading apparel exporting countries such as Bangladesh, Vietnam, Cambodia and India may have to cut 4%-9% of their jobs in the garment sector accordingly. Notably, in developing countries such as Bangladesh and Cambodia, the apparel sector remains the single largest job creator for the local economy, especially for women. The social and economic impact of job losses in the apparel sector due to Covid-19 is very concerning.

Fourth, the economic performance in the US, EU, and China will largely shape the pattern of apparel trade this year. The results in scenarios 1 and 2 overall are pretty close, suggesting the economic cloud of these three countries and regions altogether far exceed the rest of the world.

Last but not least, the global apparel supply chain could continue to face a turbulent time in the next 1-2 years, even if Covid-19 gradually gets under control in the second half of 2020. In history, affected by the 2008 global financial crisis, the value of world apparel exports dropped by 12.8% in 2009. However, the growth rate quickly rebounded to 11.5% the following year. Likewise, should the EU and US apparel imports were able to recover to its normal level in 2021, both importers and garment factories may have to deal with a new round of labor shortage, the price increase of raw material and a lack of production capacity.

by Sheng Lu

Additional reading: