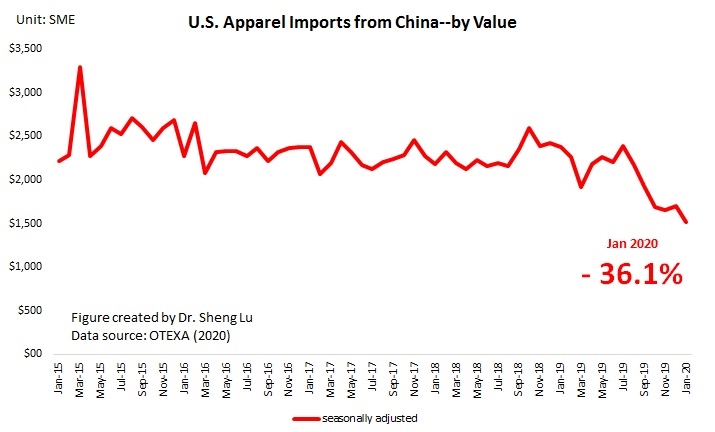

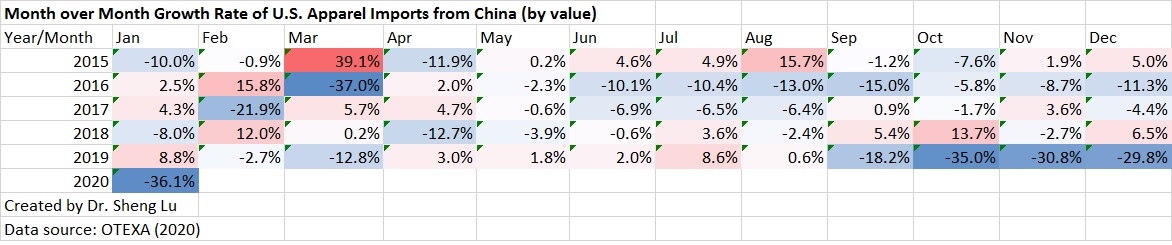

Jointly affected by the U.S.-China tariff war and the spread of the coronavirus, the value of U.S. apparel imports from China see a significant drop in January 2020.

Specifically, the value of U.S. apparel imports from China went down by as much as 36.1% month over month in January 2020. As a result, China’s market shares also dropped from nearly 30% in 2019 to a new record low of 23.9% in January 2020. However, it is important to note that such a downward trend started in October 2019, as U.S. fashion brands and retailers were eager to reduce their exposure to sourcing from China.

China’s lost market shares have been picked up mostly by other Asian suppliers, particularly Vietnam and Bangladesh. However, there is no evidence showing that U.S. fashion brands and retailers are giving more apparel sourcing orders to suppliers from the Western Hemisphere. In January 2020, only 8.1% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 3.7% from NAFTA members (down from 4.5% in 2019). Recent studies show that there’s more divergence in the products imported into the US from Asian countries and the western hemisphere.

Meanwhile, according to the latest statistics from China’s Customs, the value of China’s apparel exports in the first two months of 2020 dropped by nearly 20% from a year earlier.

I believe that a third factor for the decline attracts less public attention even as it draws greater scrutiny from those responsible for human rights in the supply chain: the mass detention of ethnic and religious minorities in the Xinjiang Uygur Autonomous Region. For those unfamiliar with the issue and its impact on supply chain human rights, I have written about it here: https://seventhgenerationinterfaith.org/2019/11/27/raise-the-alarm-for-xinjiang/

Yes, it could be another factor too and the issue has been a growing concern to many US fashion brands and retailers sourcing from China. Look forward to more systematic evaluation and empirical studies on the topic.