The latest statistics from the Office of Textiles and Apparel (OTEXA) show that COVID-19 continued to enlarge its negative impact on U.S. apparel imports in May 2020, and the path to recovery will NOT be straightforward and quick. Specifically:

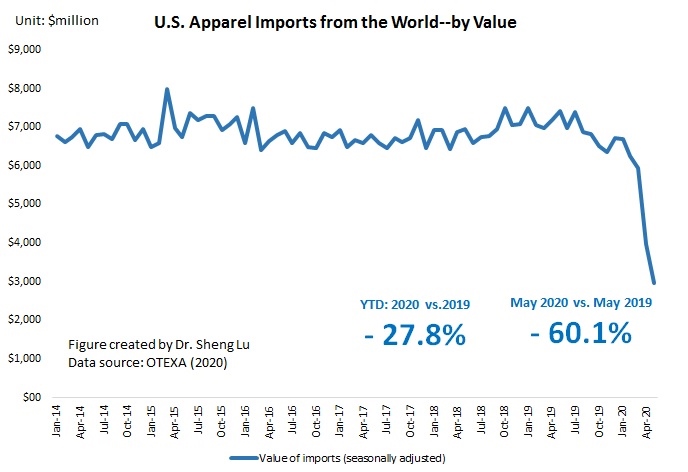

The value of U.S. apparel imports decreased by more than 60% in May 2020 from a year ago, setting a new record of single-month loss in trade volumes. Between January and May 2020, the value of U.S. apparel imports decreased by 27.8% year over year, which has been much worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

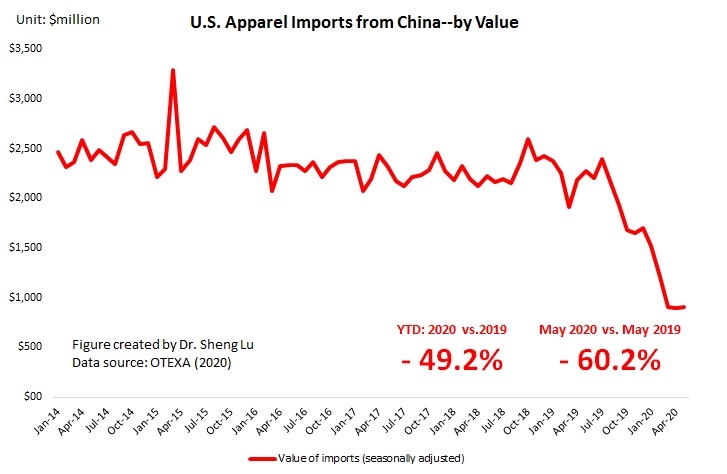

As the first country hit by Covid-19, China’s apparel exports to the U.S. dropped by 60.2% in May 2020 from a year ago, close to its performance in April 2020 (down 59% YoY). While the figure itself is far from exciting, it suggests the sinking of China’s apparel exports could have hit bottom. As an important sign, China regained its position as the largest apparel supplier to the U.S. in May 2020, with 27.2% market shares in value and 41.4% market shares in quantity. Notably, this is a significant rebound from only 11% market shares back in February 2020. Overall, it seems U.S. fashion brands and retailers continue to treat China as an essential and probably indispensable apparel sourcing base, despite a new low of U.S.-China relations and companies’ sourcing diversification strategy. Meanwhile, the official Chinese statistics report a 20.3% drop in China’s apparel exports in the first five months of 2020.

Despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.1% YTD in 2020 vs. 16.2% in 2019), ASEAN (34.6% YTD in 2020 and vs. 27.4% in 2019) and Bangladesh (9.4% YTD in 2020 vs.7.1% in 2019) all gain additional market shares in 2020 from a year ago.

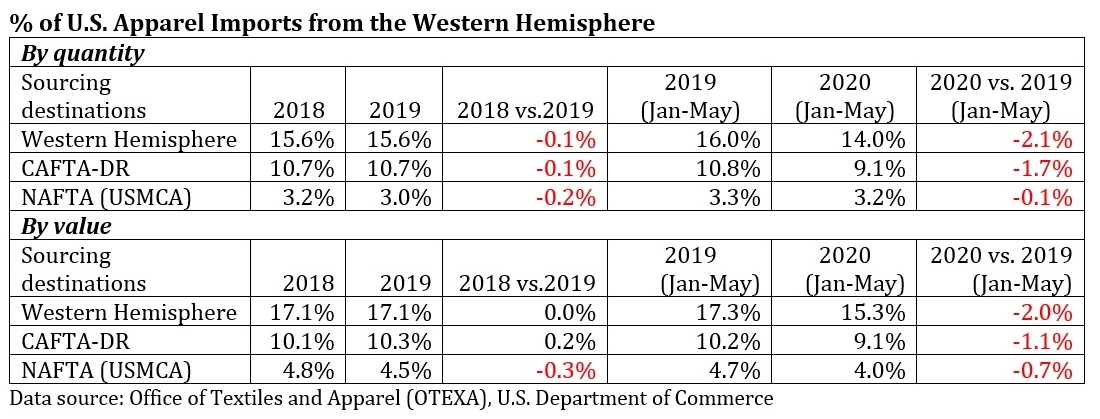

However, no clear evidence has suggested that U.S. fashion brands and retailers are giving more apparel sourcing orders to suppliers from the Western Hemisphere. In the first five months of 2020, still, only 9.1% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.0% from NAFTA members (down from 4.5% in 2019). Two factors might explain the pattern: 1) Due to factory lock-down, the production capacity in the Western Hemisphere is affected negatively; 2) With an unrepresented high level of unemployment, U.S. consumers are becoming ever more price sensitive. However, apparel produced in the Western Hemisphere, in general, are less price competitive than those made in Asia.

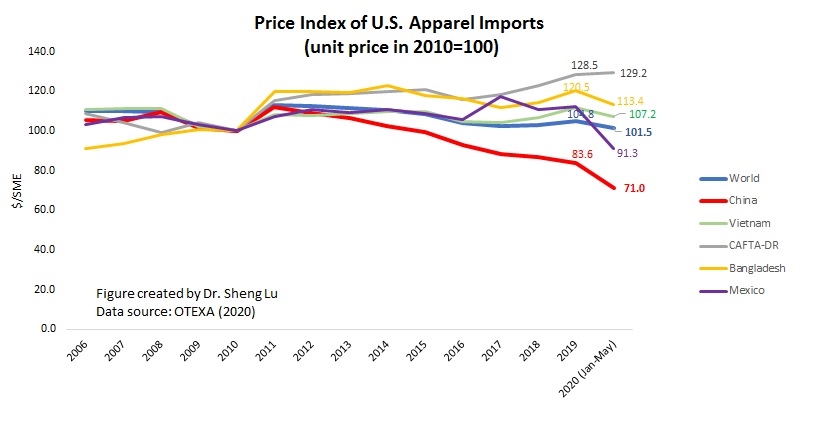

As a reflection of weak demand, the unit price of U.S. apparel imports was lower in the first five months of 2020 (price index =101.5) compared with 2019 (price index =104.7). Imports from China have seen the most notable price decrease so far (price index =71.0 YTD in 2020 vs. 83.5 in 2019).

by Sheng Lu