The latest statistics from the Office of Textiles and Apparel (OTEXA) show that the patterns of U.S. apparel imports continue to involve because of COVID-19 and the escalating US-China tensions. Meanwhile, there appeared to be more potent signs of gradual economic recovery in the U.S. driven by consumers’ robust demand. Specifically:

While the value of U.S. apparel imports decreased by 32.0% in July 2020 from a year ago, the speed of the decline has significantly slowed (was down 60% and 42.8% year over year in May and June 2020, respectively). This result echoes the trend of U.S. apparel retail sales (NAICS 448), which indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports could continue in the next two to three months.

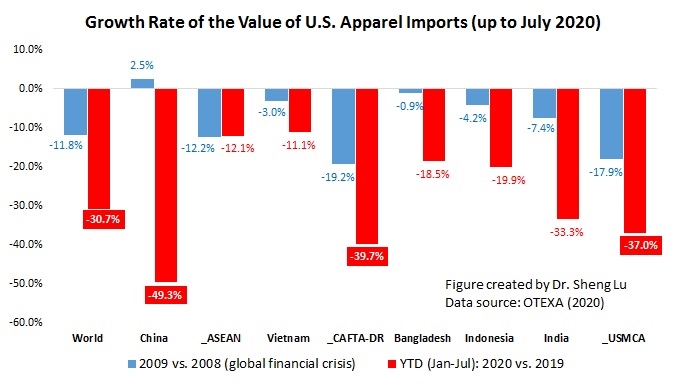

Nevertheless, between January and July 2020, the value of U.S. apparel imports decreased by 30.7% year over year, which has been much worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

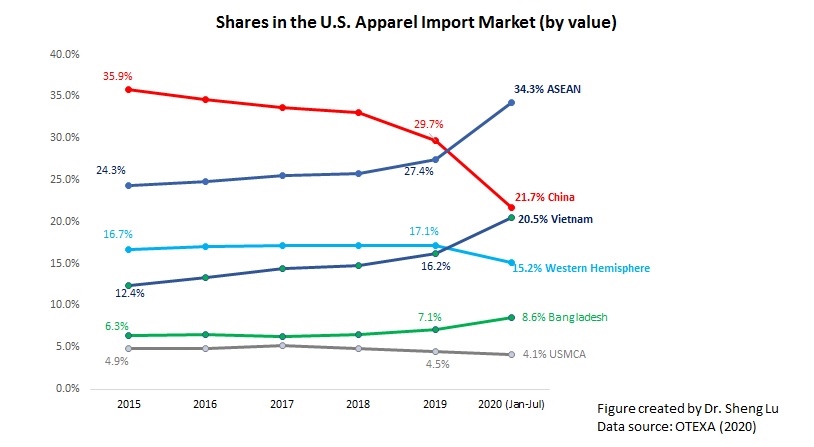

The latest trade statistics suggest that based on economic factors, U.S. fashion companies would like to continue to treat China as an essential apparel-sourcing base. As the first country hit by COVID-19, China’s apparel exports to the U.S. dropped by as much as 49.3% from January to July 2020 year over year. In February 2020, China’s market shares slipped to only 11%, and both in March and April 2020, U.S. fashion companies imported more apparel from Vietnam than from China. However, China had quickly regained its position as the top apparel supplier to the U.S., with a 26.3% market share in value and a 38.8% share in quantity in July 2020.

Different from the impact of the trade war, COVID-19 could benefit China as an apparel sourcing base as fashion companies have to “do more with fewer resources.” In general, China still enjoyed two notable advantages that other apparel supplying countries are unable to catch up in the short term. 1) unparalleled production capacity, meaning importers can source almost all products in any quantity from China vs. more limited production capacity (both in terms of variety and volume) in other alternative sourcing destinations. 2) China can mostly produce textile raw material locally vs. many apparel exporting countries still rely heavily on imported yarns and fabrics (supplied by China).

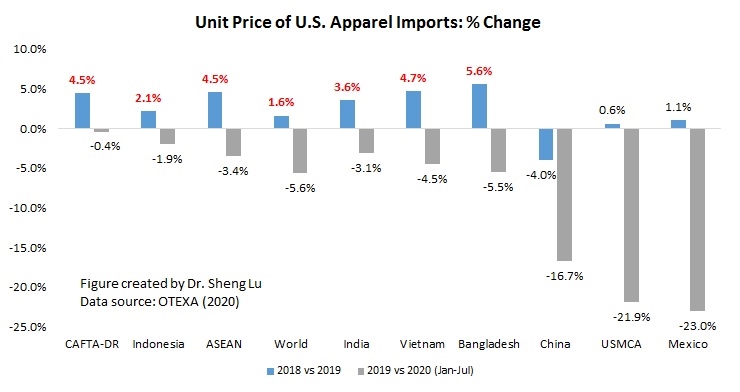

Contrary to common perceptions, apparel “Made in China” apparently are also becoming more price-competitive–the unit price slipped from $2.25/Square meters equivalent (SME) in 2019 to $1.88/SME in 2020 (January to July), or down more than 16.7% (compared with a 5.6% price drop of the world average). As of July 2020, the unit price of U.S. apparel import from China was only 65.7% of the world average, and around 25—35 percent lower than those imported from other Asian countries.

That being said, non-economic factors, from the deteriorating US-China relations to the reported Xinjiang forced labor issue, are increasingly complicating fashion companies’ sourcing decisions. Somehow as a warning sign, China’s market shares in the U.S. apparel import market slipped in both quantity and value terms in July 2020 compared with a month ago.

Despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.5% YTD in 2020 vs. 16.2% in 2019), ASEAN (34.3% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.6% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.5% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

However, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first seven months of 2020, only 8.8% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first seven months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 28.9% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the contributing factors why near sourcing has been stagnant.

As a reflection of weak demand, the unit price of U.S. apparel imports was lower in the first six months of 2020. The price index declined from 104.7 in 2019 to 99.0 YTD (Jan to Jul) in 2020 (Year 2010 =100). The imports from Mexico (price index =86.4 YTD in 2020 vs. 112.1 in 2019) and China (price index = 69.7 YTD in 2020 vs. 83.5 in 2019) have seen the most notable price decrease so far.

by Sheng Lu

One thought on “COVID-19 and U.S. Apparel Imports (Updated: September 2020)”

Comments are closed.