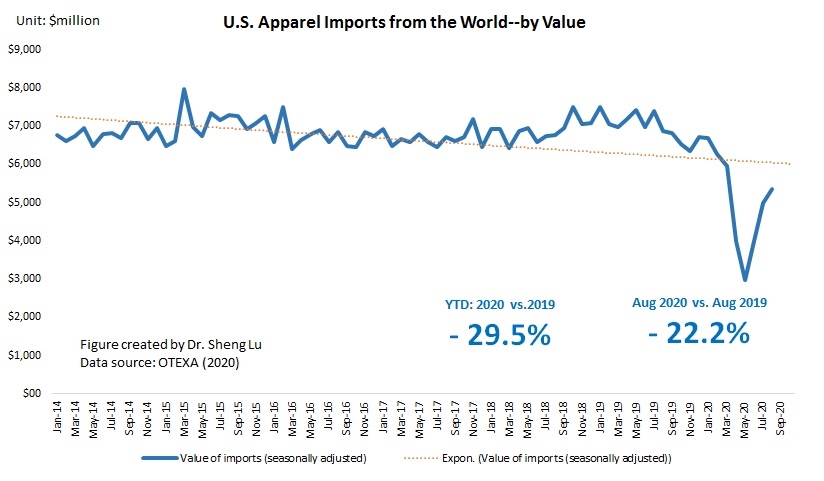

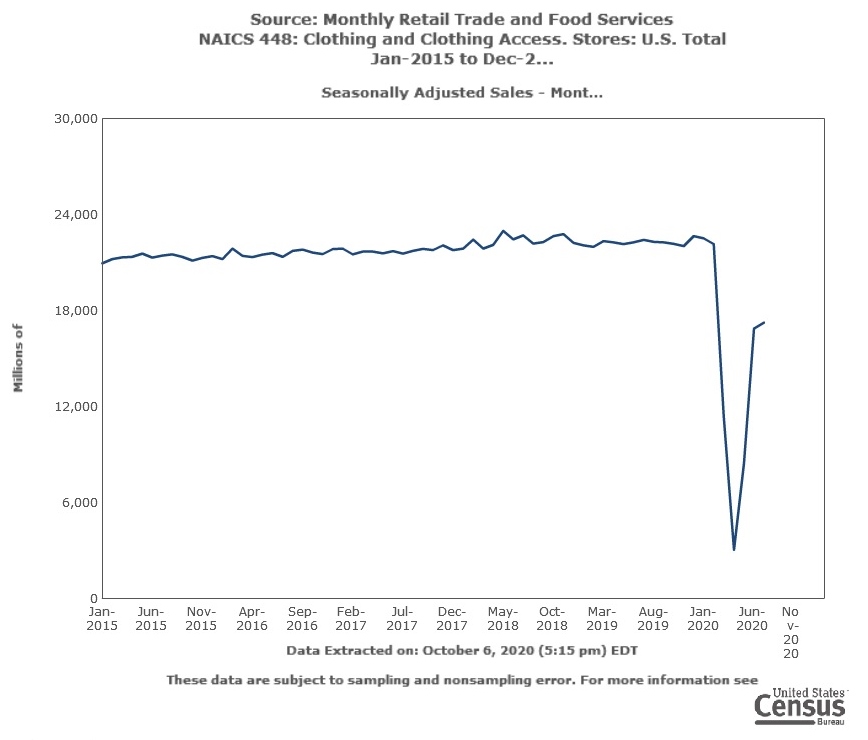

First, U.S. apparel imports continue to rebound thanks to consumers’ robust demand. The value of U.S. apparel imports in August 2020 went up by 7.6% from July 2020 (seasonally adjusted), a new record high since March 2020 when COVID-19 broke out in the States. As of August 2020, the volume of U.S. apparel imports has recovered to around 80% of the pre-coronavirus level. This result echoes the trend of U.S. apparel retail sales (NAICS 448), which also indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports hopefully will last for another 1-2 months.

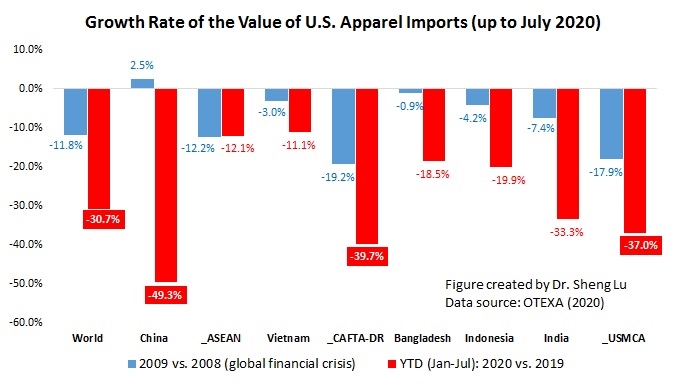

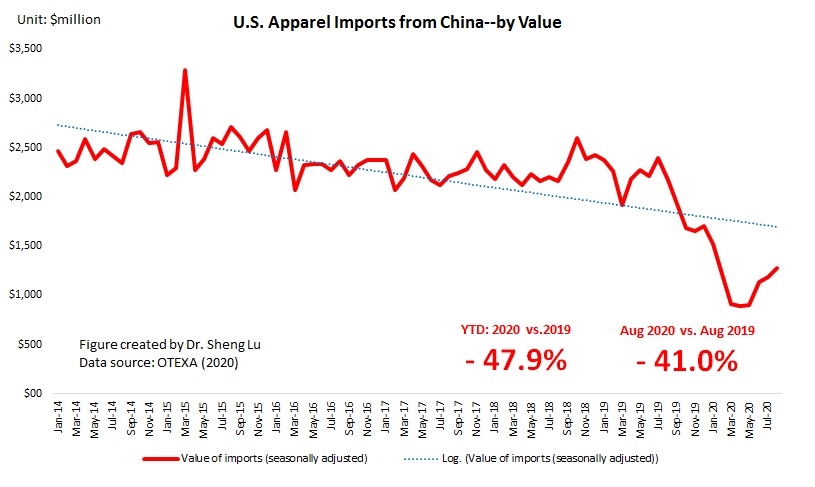

Nevertheless, between January and August 2020, the value of U.S. apparel imports decreased by almost 30% year over year, which has been MUCH worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

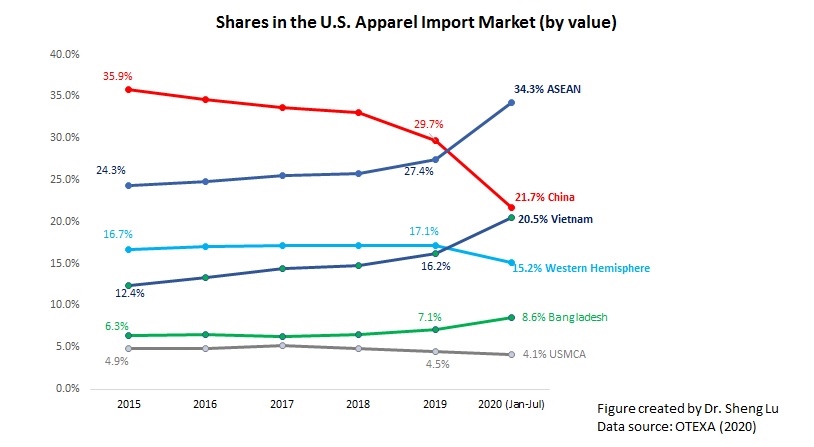

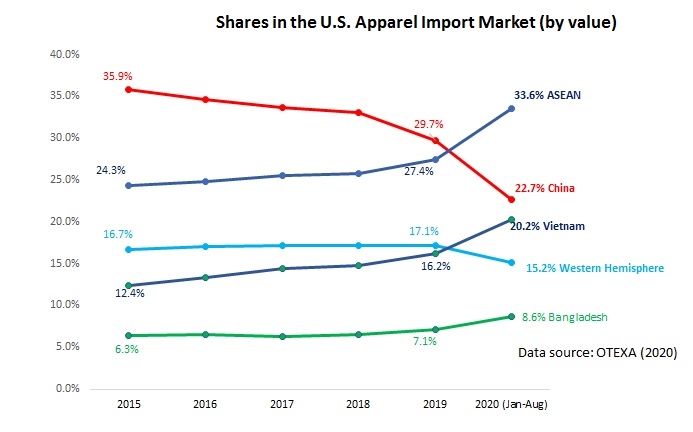

Second, no evidence suggests that U.S. fashion companies are giving up China as one of their essential apparel-sourcing bases. Notably, since May 2020, China had quickly regained its position as the top apparel supplier to the U.S. market. From June to August 2020, China’s market shares have stably stayed at around 27-28% in value and 40-42% in quantity.

Some industry sources show that “Made in China” enjoys two notable advantages that other apparel supplying countries cannot catch up in the short term. 1) unparalleled production capacity, meaning importers can source almost all products in any quantity from China vs. more limited production capacity (both in terms of variety and volume) in other alternative sourcing destinations. 2) China can mostly produce textile raw material locally vs. many apparel exporting countries still rely heavily on imported yarns and fabrics (supplied by China).

However, non-economic factors, particularly the reported Xinjiang forced labor issue, are complicating fashion companies’ sourcing decisions. Notably, US cotton apparel imports from China year-to-date (YTD) in 2020 (Jan to August) significantly decreased by 54% from a year ago, much higher than the 22% drop in US imports from the rest of the world. As a result, China’s market share in the US cotton apparel import market sharply declined from 22% in 2019 to only 15.1% in 2020 (Jan-Aug), a record low in the past ten years. This unusual trade pattern suggests that the concerns about social compliance risk are holding US fashion companies back from sourcing cotton apparel products from China. As the forced labor issue continues to evolve and become ever more sensitive and high profile, it is not unlikely that US fashion companies may substantially cut their China sourcing further, even if it is not a preferred choice economically.

Third, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.2% YTD in 2020 vs. 16.2% in 2019), ASEAN (33.6% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.6% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.5% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

Likewise, thanks to a highly integrated regional textile and apparel supply chain, Asian countries all together were able to maintain fairly stable market shares on the world stage over the past decade despite all market disruptions, from the financial crisis, trade war to the wage increase.

Fourth, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first seven months of 2020, only 8.9% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first eight months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 28.0% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the contributing factors.

Further, industry sources show that the apparel products U.S. fashion companies import from members of USMCA and CAFTA-DR predominantly are tops and bottoms. The lack of production capacity for other product categories significantly limits the growth potential of these countries playing the role as a leading sourcing base.

by Sheng Lu