Speaker: Wilson Zhu, the Chief Operating Officer of Li & Fung

Event summary:

The originator of the US-China trade war was not actually about the “trade deficit”, but rather a lack of “trust” between the two countries.

Trade deficit could be a “misleading concept”–while the iPhone was claimed to be “Made in China”, it wasn’t manufactured there at all—instead, China only played the role of a “middle-man of the supply chain.” Such a misunderstanding is within the ancient country of origin rules used in international trade.

The “Made in China” label is becoming “obsolete.” As China continues to expand its supply chain globally, ports in China are evolving into “managers” of products “Made in the world.”

There is still great hope for the global apparel supply chain in the post-Covid world. Less economically developed countries like Vietnam are now mimicking the former industrialization of China in its factories with the help of advanced technology. And, the United States continues to advance the efficiency and sophistication of its textile production. It seems that all in all, the only way to make it through this crisis successfully, is through global collaboration, not conflict.

The surveyed U.S. fashion companies demonstrate more readiness and interest in using the US-Mexico-Canada Trade Agreement (USMCA) for apparel sourcing purposes in 2020 than a year ago:

For companies that were already using NAFTA for sourcing, the vast majority (77.8 percent) say they are “ready to achieve any USMCA benefits immediately,” up more than 31 percent from 2019.

Even for respondents who were not using NAFTA or sourcing from the region, about half of them this year say they may “consider North American sourcing in the future” and explore the USMCA benefits.

Nevertheless, when asked about the potential impact of USMCA on companies’ apparel sourcing practices, some respondents expressed concerns about the rules of origin changes. These worries seem to concentrate on denim products in particular. For example, one respondent says, “USMCA changes negatively affects our denim jeans sourcing particularly with the new pocketing rules of origin.” Another adds, “Denim pocketing ROO change is a concern but manageable.”

It also remains to be seen whether USMCA will boost “Made in the USA” fibers, yarns, and fabrics by limiting the use of non-USMCA textile inputs. For example, while the new agreement expands the Tariff Preference Level (TPL) for U.S. cotton/man-made fiber apparel exports to Canada (typically with a 100 percent utilization rate), these apparel products are NOT required to use U.S.-made yarns and fabrics.

1. The garment industry in the Asia-Pacific region is particularly vulnerable to the adverse impact of COVID-19 because of the size of the industry present and the high stakes involved. Notably, garment workers (over 60 million in total, including 35 million women) accounted for 21.1% of the manufacturing employment in the region as of 2019. Over 60% of the world’s apparel exports currently come from the Asia-Pacific region.

2. The cumulative impacts of COVID-19 on garment supply chains have been both far-reaching and complex: 1) As of September 9, 2020, more than 31 million garment workers in the Asia Pacific region were still affected by factory closure (i.e., mandatory closures of non-essential workplaces). 2) The drop in consumer demand and the decline in retail sales in the primary apparel consumption markets across the world have affected garment workers in the Asia-Pacific region negatively. As of September 9, 2020, 49% of all jobs in the Asia-Pacific garment supply chains (29 million) were dependent on demand for garments from consumers living in countries with the most stringent lockdown measures in place. Another 31 million jobs (51%) depended on consumer demand that is based in countries with a medium level of lockdown measures in place. 3) COVID-19 has further caused supply chain disruptions and prevented imported inputs into garment production from arriving in time. The heavy reliance on textile raw material supply from China makes many apparel producing countries in South-East Asian countries highly vulnerable to shortages of inputs.

3. The world apparel trade has fallen in the first half of 2020 sharply. This includes a 26% YoY drop in the US, a 25% drop in the EU, and a 17% drop in Japan. However, the timing and magnitude of these import declines vary significantly — China’s exports started to drop first at the beginning of the year,2020. Then, the exports from Vietnam, Bangladesh, Indonesia, and India began to decrease also since February (a joint effect of the shortage of raw material + decreased import demand). Data further shows that the drop in world apparel trade has been more significant than other products in the first half of 2020.

4. Apparel suppliers in the Asia Pacific region have been struggling with order cancellations AND longer payment terms insisted on by Western fashion brands and retailers. Garment factories say that they don’t have the leverage to ‘push back’ against these changes to contract terms and buyer policies.

5. Thousands of garment factories in the Asia-Pacific region closed at least temporarily because of COVID-19, some of them indefinitely. For example, In Cambodia, approximately 15-25% of factories had no orders at the end of the June 2020. Likewise, around 60% of garment factories in Bangladesh reported closing for more than 3 weeks. Related, layoffs have been widespread. For example, according to Indonesia’s Ministry of Industry, approximately 30% of their apparel and footwear workforce had been laid-off by July 2020 (812,254 in total). In Cambodia, approximately 15% of their garment workers (more than 150,000 workers) were reported to have lost their jobs during the pandemic. Further, garment factories have been operating at reduced capacity during the pandemic. For example, in Bangladesh, as of July 2020, the proportion of workers returning to work after re-opening was only 57% of the pre-pandemic level. Similarly, in Vietnam, as of July 2020, the proportion of workers returning to work after re-opening was also just around 50% of the pre-pandemic level.

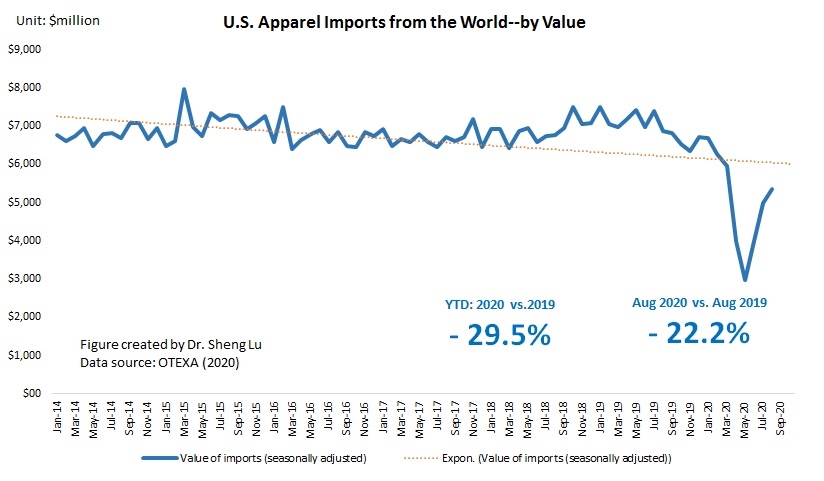

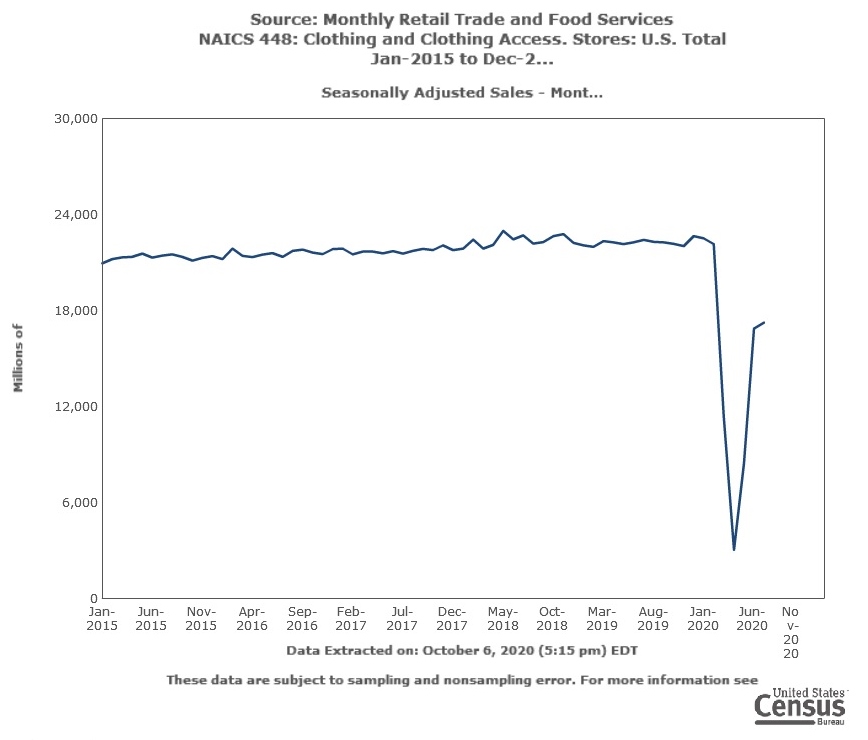

First, U.S. apparel imports continue to rebound thanks to consumers’ robust demand. The value of U.S. apparel imports in August 2020 went up by 7.6% from July 2020 (seasonally adjusted), a new record high since March 2020 when COVID-19 broke out in the States. As of August 2020, the volume of U.S. apparel imports has recovered to around 80% of the pre-coronavirus level. This result echoes the trend of U.S. apparel retail sales (NAICS 448), which also indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports hopefully will last for another 1-2 months.

Nevertheless, between January and August 2020, the value of U.S. apparel imports decreased by almost 30% year over year, which has been MUCH worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

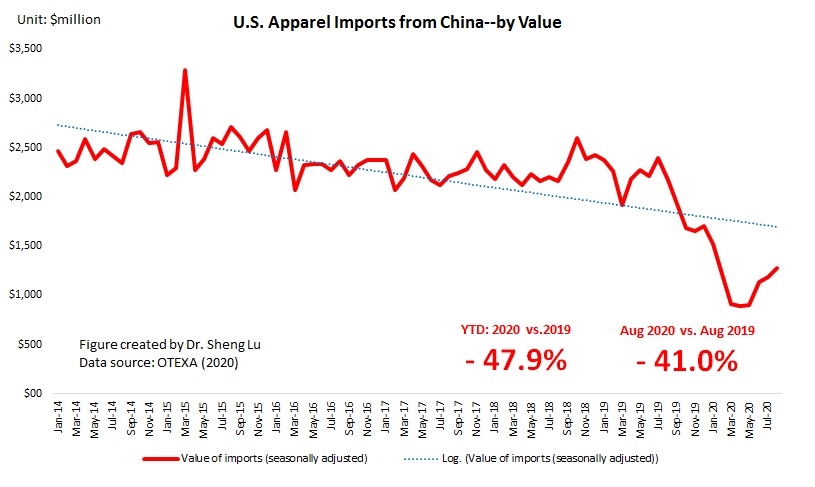

Second, no evidence suggests that U.S. fashion companies are giving up China as one of their essential apparel-sourcing bases. Notably, since May 2020, China had quickly regained its position as the top apparel supplier to the U.S. market. From June to August 2020, China’s market shares have stably stayed at around 27-28% in value and 40-42% in quantity.

Some industry sources show that “Made in China” enjoys two notable advantages that other apparel supplying countries cannot catch up in the short term. 1) unparalleled production capacity, meaning importers can source almost all products in any quantity from China vs. more limited production capacity (both in terms of variety and volume) in other alternative sourcing destinations. 2) China can mostly produce textile raw material locally vs. many apparel exporting countries still rely heavily on imported yarns and fabrics (supplied by China).

However, non-economic factors, particularly the reported Xinjiang forced labor issue, are complicating fashion companies’ sourcing decisions. Notably, US cotton apparel imports from China year-to-date (YTD) in 2020 (Jan to August) significantly decreased by 54% from a year ago, much higher than the 22% drop in US imports from the rest of the world. As a result, China’s market share in the US cotton apparel import market sharply declined from 22% in 2019 to only 15.1% in 2020 (Jan-Aug), a record low in the past ten years. This unusual trade pattern suggests that the concerns about social compliance risk are holding US fashion companies back from sourcing cotton apparel products from China. As the forced labor issue continues to evolve and become ever more sensitive and high profile, it is not unlikely that US fashion companies may substantially cut their China sourcing further, even if it is not a preferred choice economically.

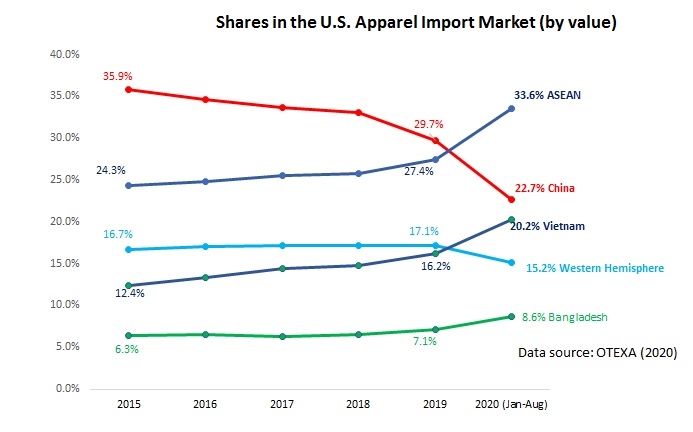

Third, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.2% YTD in 2020 vs. 16.2% in 2019), ASEAN (33.6% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.6% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.5% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

Likewise, thanks to a highly integrated regional textile and apparel supply chain, Asian countries all together were able to maintain fairly stable market shares on the world stage over the past decade despite all market disruptions, from the financial crisis, trade war to the wage increase.

Fourth, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first seven months of 2020, only 8.9% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first eight months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 28.0% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the contributing factors.

Further, industry sources show that the apparel products U.S. fashion companies import from members of USMCA and CAFTA-DR predominantly are tops and bottoms. The lack of production capacity for other product categories significantly limits the growth potential of these countries playing the role as a leading sourcing base.

The size of the U.S. textile and apparel industry has significantly shrunk over the past decades. However, U.S. textile manufacturing is gradually coming back. The output of U.S. textile manufacturing (measured by value added) totaled $18.79 billion in 2019, up 23.8% from 2009. In comparison, U.S. apparel manufacturing dropped to $9.5 billion in 2019, 4.4% lower than ten years ago (Bureau of Economic Analysis, 2020).

Meanwhile, COVID-19 has hit U.S. textile and apparel production significantly. Notably, the value of U.S. textile and apparel output decreased by as much as 21.4% and 14.9% in the second quarter of 2020, respectively, compared with a year ago. This result was worse than a 15% decrease during the 2008-2009 world financial crisis. Further, the decline in U.S. textile exports is an essential factor contributing to the significant drop in U.S. textile manufacturing. In the first seven months of 2020, the value of U.S. yarn and fabric exports went down by 31% and 19%, respectively, year over year (OTEXA, 2020).

Additionally, as the U.S. economy is turning more mature and sophisticated, the share of U.S. textile and apparel manufacturing in the U.S. Gross Domestic Product (GDP) dropped to only 0.13% in 2019 from 0.57% in 1998 (Bureau of Economic Analysis, 2020).

The U.S. textile and apparel manufacturing is also changing in nature. For example, textile products had accounted for over 66% of the total output of the U.S. textile and apparel industry as of 2019, up from 58% in 1998 (Bureau of Economic Analysis, 2020). Textiles and apparel “Made in the USA” are growing particularly fast in some emerging markets that are high-tech driven, such as medical textiles, protective clothing, specialty and industrial fabrics, and non-woven.

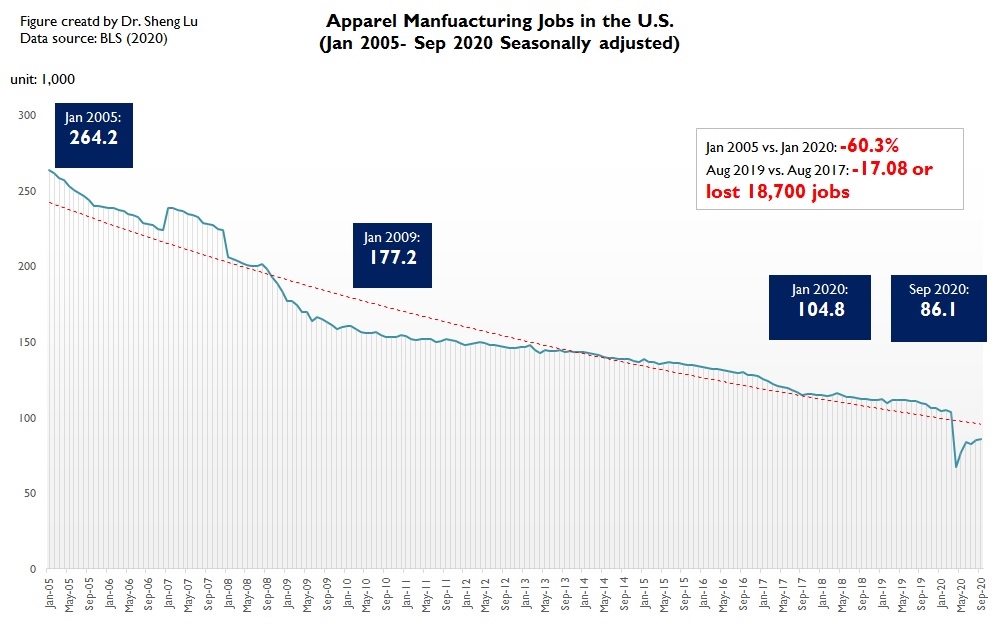

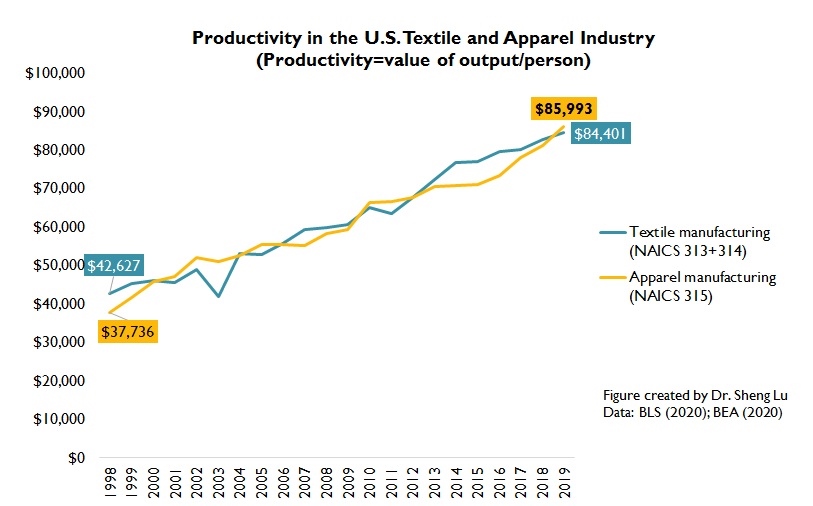

As production turns more automated, the U.S. textile and apparel manufacturing sector is NOT creating more jobs. Even before the pandemic, from January 2005 to January 2020, employment in the U.S. textile manufacturing (NAICS 313 and 314) and apparel manufacturing (NAICS 315) declined by 44.3% and 59.3%, respectively (Bureau of Labor Statistics, 2020). However, improved productivity (i.e., the value of output per employee) could be a critical factor behind the net job losses.

Data further shows that COVID19 has resulted in more than 83,700 job losses in the U.S. textile and apparel manufacturing sector between March-April 2020, of which around 80% have returned as of September 2020. Nevertheless, the downward trend in employment is not changing for the U.S. textile and apparel manufacturing sector.

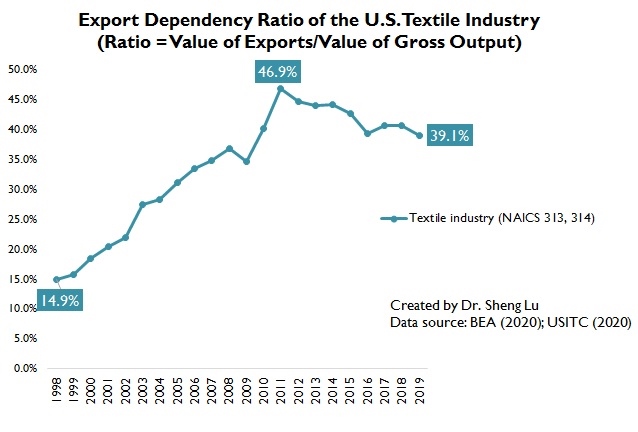

Consistent with the theoretical prediction, U.S. remains a net textile exporter and a net apparel importer. In 2019, the U.S. enjoyed a $1,633million trade surplus in textiles and suffered an $80,637 million trade deficit in apparel (USITC, 2020). Notably, nearly 40% of textiles “Made in the USA” (NAICS 313 and 314) were sold overseas in 2019, up from only 15% in 2000 (OTEXA, 2020). On the other hand, because of the regional supply chain, close to 70% of U.S. textile and apparel export go to the western hemisphere, a pattern that stays stable over the past decade.

by Sheng Lu

Discussion questions:

Why or why not do you think the U.S. textile industry (NAICS 313 +314) and the apparel industry (NAICS 315) are in good shape?

Based on the statistics, do you think textile and apparel “Made in the USA” have a future? Please explain.

What are the top challenges facing the U.S. textile industry and the apparel industry in today’s global economy and during the COVID19?