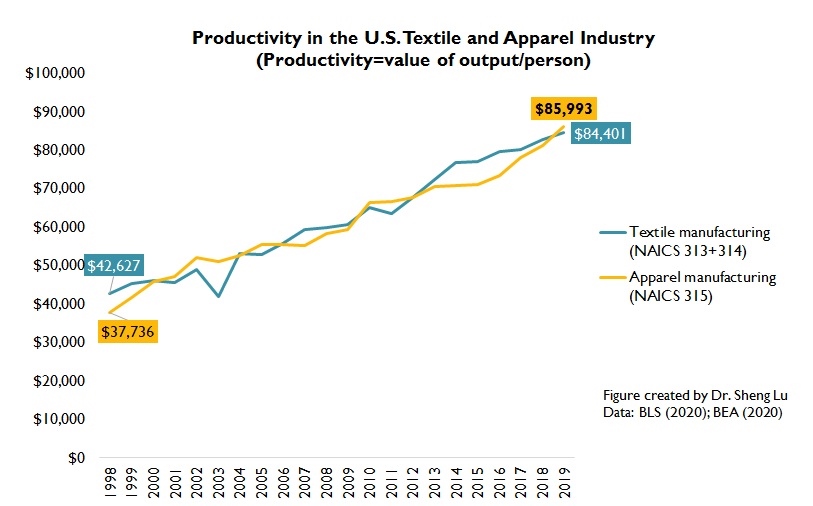

The size of the U.S. textile and apparel industry has significantly shrunk over the past decades. However, U.S. textile manufacturing is gradually coming back. The output of U.S. textile manufacturing (measured by value added) totaled $18.79 billion in 2019, up 23.8% from 2009. In comparison, U.S. apparel manufacturing dropped to $9.5 billion in 2019, 4.4% lower than ten years ago (Bureau of Economic Analysis, 2020).

Meanwhile, COVID-19 has hit U.S. textile and apparel production significantly. Notably, the value of U.S. textile and apparel output decreased by as much as 21.4% and 14.9% in the second quarter of 2020, respectively, compared with a year ago. This result was worse than a 15% decrease during the 2008-2009 world financial crisis. Further, the decline in U.S. textile exports is an essential factor contributing to the significant drop in U.S. textile manufacturing. In the first seven months of 2020, the value of U.S. yarn and fabric exports went down by 31% and 19%, respectively, year over year (OTEXA, 2020).

Additionally, as the U.S. economy is turning more mature and sophisticated, the share of U.S. textile and apparel manufacturing in the U.S. Gross Domestic Product (GDP) dropped to only 0.13% in 2019 from 0.57% in 1998 (Bureau of Economic Analysis, 2020).

The U.S. textile and apparel manufacturing is also changing in nature. For example, textile products had accounted for over 66% of the total output of the U.S. textile and apparel industry as of 2019, up from 58% in 1998 (Bureau of Economic Analysis, 2020). Textiles and apparel “Made in the USA” are growing particularly fast in some emerging markets that are high-tech driven, such as medical textiles, protective clothing, specialty and industrial fabrics, and non-woven.

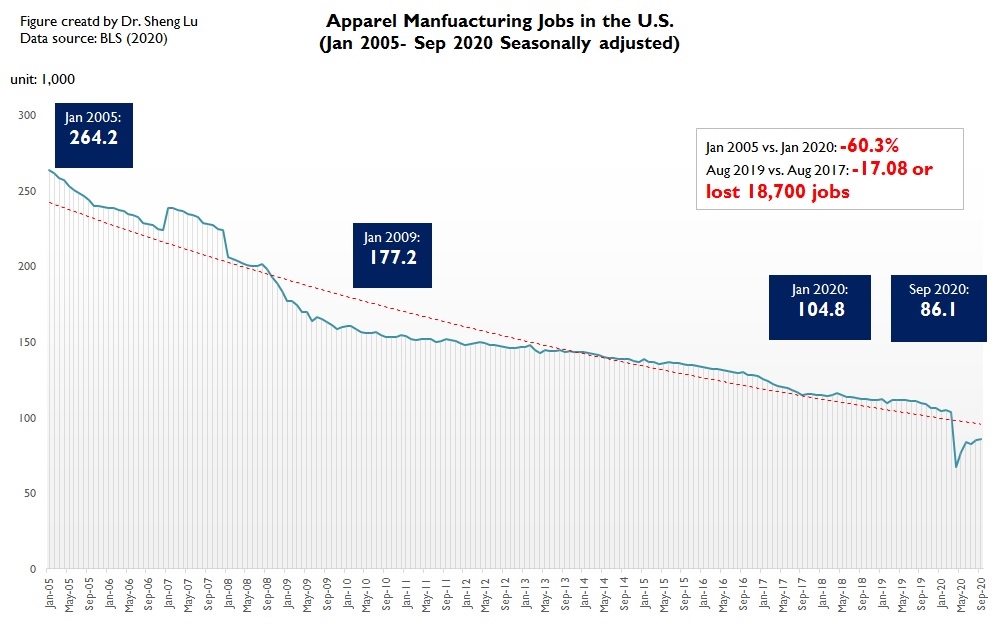

As production turns more automated, the U.S. textile and apparel manufacturing sector is NOT creating more jobs. Even before the pandemic, from January 2005 to January 2020, employment in the U.S. textile manufacturing (NAICS 313 and 314) and apparel manufacturing (NAICS 315) declined by 44.3% and 59.3%, respectively (Bureau of Labor Statistics, 2020). However, improved productivity (i.e., the value of output per employee) could be a critical factor behind the net job losses.

Data further shows that COVID19 has resulted in more than 83,700 job losses in the U.S. textile and apparel manufacturing sector between March-April 2020, of which around 80% have returned as of September 2020. Nevertheless, the downward trend in employment is not changing for the U.S. textile and apparel manufacturing sector.

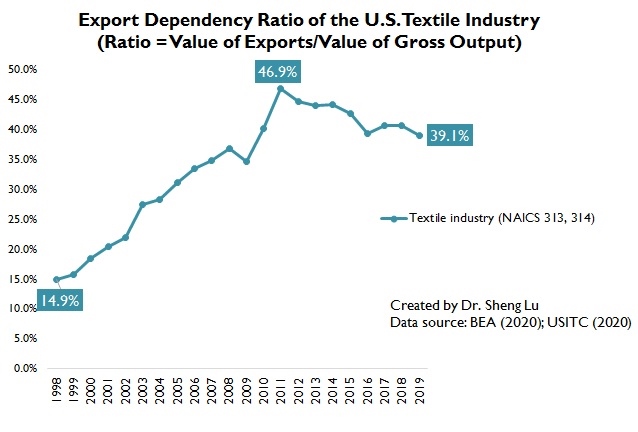

Consistent with the theoretical prediction, U.S. remains a net textile exporter and a net apparel importer. In 2019, the U.S. enjoyed a $1,633million trade surplus in textiles and suffered an $80,637 million trade deficit in apparel (USITC, 2020). Notably, nearly 40% of textiles “Made in the USA” (NAICS 313 and 314) were sold overseas in 2019, up from only 15% in 2000 (OTEXA, 2020). On the other hand, because of the regional supply chain, close to 70% of U.S. textile and apparel export go to the western hemisphere, a pattern that stays stable over the past decade.

by Sheng Lu

Discussion questions:

- Why or why not do you think the U.S. textile industry (NAICS 313 +314) and the apparel industry (NAICS 315) are in good shape?

- Based on the statistics, do you think textile and apparel “Made in the USA” have a future? Please explain.

- What are the top challenges facing the U.S. textile industry and the apparel industry in today’s global economy and during the COVID19?