Video credit: Chenfeng group; 8th China and Asia Textile Forum 2020

Discussion questions (For FASH455, please answer all questions):

From the video, how is textile manufacturing (e.g., yarns and fabrics) different from apparel manufacturing?

Based on our lectures and the video, how do you see the impact of automation on shaping the future landscape of world textile and apparel production and trade?

Will you be interested in working for a textile/apparel factory after graduation? Why or why not?

#1 In class, we discussed that trade always creates both winners and losers. So who are the winners and losers in the US-China tariff war? Also, why should or should not the government use trade policy to pick up winners and losers in international trade?

#2 Why do you think U.S. fashion brands and retailers oppose Section 301 tariffs on apparel imports from China, whereas the National Council of Textile Organizations (NCTO), which represents the US textile industry, supports Trump’s tariff action?

#3 The U.S.-China tariff war continues during the pandemic, resulting in higher sourcing costs for U.S. fashion brands and retailers, which have been struggling hard financially. In such a case, if you were the CEO of Macy’s, why or why not would you pass the tariff burden to consumers, i.e., ask consumers to pay a higher price?

#4 Why or why not do you agree with the Trump Administration to lift the Section 301 tariffs on PPE imports from China? Isn’t a high tariff typically protects the domestic industry and would incentivize more U.S.-based PPE production?

#5 Most classic trade theories (such as the comparative advantage trade theory and the factor proportion trade theory) advocate free trade with no government interventions. However, international trade in the real world has been so heavily influenced by government policy, such as tariffs. How to explain this phenomenon? Are trade theories wrong, or is the government wrong?

[Anyone is welcome to join the online discussion. For students in FASH455, please address at least two questions in your comment. Please also mention the question number in your comment]

Jason Prescott founded JP Communications INC in 2005 and rapidly established TopTenWholesale.com and Manufacturer.com as the largest US-based B2B global trade network for manufacturers, retailers, department stores, discounters, importers, wholesalers, buyers and brands. A decade later, in 2016, he established the Apparel Textile Sourcing trade show platform with the China Chamber of Commerce for Import & Export of Textile & Apparel to connect the global B2B network of over 2 million with manufacturers around the globe via in-person events. By 2020, the ATS brand has created the fastest-growing trade shows in the industry producing annual events in Miami, Toronto, Montreal, Berlin and virtually.

Jason is active in search marketing models and technology and provides consulting and seminars in around the world for organizations looking to invest in the USA market. He is the author of two best-selling books, Wholesale 101 and Retail 101, published by McGraw Hill as well as articles on business and technology appearing in B2B Online, Omma, IMediaConnection, CEO Magazine, Entrepreneur Online, and been cited in Inc Magazine, Business Week and Forbes Online.

Kendall: What has motivated you to get involved in the apparel business, especially running the Apparel Textile Sourcing Trade (ATS) Shows, which has grown into one of the most popular and influential sourcing events today?

Jason: We started our company in 2005 w/ our flagship product – www.TopTenWholesale.com – which is a search engine for wholesale suppliers and products. In 2010 we acquired www.manufacturer.com – a sourcing platform to find global producers and manufacturers. It would be fair to say that never in our wildest imagination did we think we would be producing some of the world’s top sourcing trade fairs in the apparel and textile industry. I’d like to say it was a natural evolution but to be frank the opportunity came up over a cup of tea with a very good friend of mine, Mr. Chen Zhirong – Director for the China Chamber of Commerce for Import & Export of Textiles (CCCT) – in Dec 2015. What started from a cup of tea wound up growing into a trade show company that now produces events 4 cities, 3 countries and 2 continents (Miami, Toronto, Montreal, Berlin).

More than 200 of the world’s top producers of apparel, textiles, accessories, footwear, and personal protective equipment will exhibit virtually at Apparel Textile Sourcing trade shows this fall. Attendance is always free and the interactive event also specializes in seminars, sessions, workshops and panels from experts in the industries of sourcing, fashion, design and retail.

Kendall: COVID-19 is the single biggest challenge facing the textile and apparel industry today. From your observation, how has COVID-19 affected textile and apparel companies’ sourcing practices? What will be the medium to the long-term impact of COVID on textile and apparel sourcing?

Jason: The fallout from the pandemic – particularly in the textile and apparel industry – and how it impacts sourcing, has had such a far-reaching magnitude that it’s still very challenging to figure out how sourcing practices will be impacted. Over the long term, there is no question that this pandemic will speed up near-sourcing, on-shoring, digitization, and real-time production. The interim has resulted in massive layoffs, geo-political uncertainty and a turbulent political atmosphere that has rattled the cages of just about every sourcing director. The industry has seen purchase orders defaulted on, behavior in the supply chain that should not be tolerated, and a general lack of accountability. I also have no question that as we continue to emerge out of the pandemic there will be an advanced focus much more on the global revolution of sustainability, fair labor practices, plus a far-keener eye on the eco-systems in which the textile industry lives and breathes.

Kendall: There have been more heated debates on the future of China as an apparel sourcing base for US fashion companies, especially given the escalating U.S.-China trade war and the COVID-19. What is your view?

Jason: It should be noted that more than a billion dollars of trade in the textile sector in China was lost in export shipments to the USA during the first half of 2019 – primarily due to the trade war. The pandemic has since crippled exports of textile and apparel – in not just China – but also in every sourcing region on the planet. While many media outlets and others talk about the demise of China as a producer for textile and apparel that is just not the case. The Chinese have built an infrastructure, invested billions of dollars in the best technology, and have mastered the art of production over the last 3+ decades. We must not also forget that much of this infrastructure was built with trillions of dollars by the world’s leading brands, retailers, and governments. To bail on that would not be prudent. The Chinese are extremely adaptive and there is no question they have taken the time during the pandemic – and I should also note that they have emerged quicker than anyone else from the pandemic – to invest much more in technology, made-to-order, customization, and enhances on sustainable practices by utilizing more renewables.

Kendall: Many studies suggest that fashion companies continue to actively look for China’s alternatives. Do we have a “Next China” yet– Vietnam, Bangladesh, India, Ethiopia, or somewhere else?

Jason: No we do not have a next China yet. The production in many regions that have competent supply chains – like Vietnam – are full and at over-capacity. It should further be noted that a large portion in places like Vietnam are owned in partnerships thru the Chinese. Simply stated, many of the other regions such as Bangladesh, India, and the AGOA regions lack infrastructure and the decades of experience that the Chinese have.

Kendall: Some predict that near sourcing rather than global sourcing will become ever more popular as fashion companies are prioritizing speed to market and building a shorter supply chain. Why or why not do you think the shift to near sourcing or reshoring is happening?

Jason: This is correct. On-demand production, near-sourcing, and the evolution of digitization will of course lead to increased manufacturing domestically. Neither of these options are yet a solution for the high-volume production which is at the heart of the industry. I will agree that the continued emergence of micro-brands, and continually evolving shifts in consumer behavior which generally has resulted in ‘disloyalty’ to brands is another factor that makes on-shoring or near-shoring more attractive.

Kendall: Building a more sustainable and socially responsible textile and apparel supply chain is also growing in importance. From interacting with fashion brands and retailers, can you provide us with some updates in this area, such as companies’ best practices, issues they are working on, or the key challenges that remain?

Jason: The circularity of the industry encompassing the producer, the brand, logistics, and the consumer will continue to evolve in their social responsibilities and awareness of sustainable practices engaged in by the brand. There are great organizations out there like WRAP, TESTEX and Better Buying who are growing and have a much larger voice than what they have had in the past. Post-pandemic, I believe we will see social responsibility as one of the top priorities with so many millions of people displaces from COVID-19.

Kendall: For our students interested in pursuing a career in the textile and apparel industry, especially related to sourcing, do you have any suggestions?

Jason: The top suggestion I can offer is to pursue experience as you are actively engaged in your studies. One of the key elements I can advise of is to take the time and learn culture over language. Having a cultural understanding of the key regions where sourcing occurs will catapult your career and bring significant relationships to the table that you never thought you would have had before. Also, attend trade shows! Walking thru international apparel trade shows – like The Apparel Textile Sourcing – will help you immerse yourself with numerous different nationalities and personalities that you would otherwise never have the chance to meet. Jump on any opportunity you can to go abroad. Especially to regions in Asia and Latin America. Most importantly never forget that your credibility in life is everything and maintain the highest pedigree of integrity as possible.

The latest statistics from the Office of Textiles and Apparel (OTEXA) show that the patterns of U.S. apparel imports continue to involve because of COVID-19 and the escalating US-China tensions. Meanwhile, there appeared to be more potent signs of gradual economic recovery in the U.S. driven by consumers’ robust demand. Specifically:

While the value of U.S. apparel imports decreased by 32.0% in July 2020 from a year ago, the speed of the decline has significantly slowed (was down 60% and 42.8% year over year in May and June 2020, respectively). This result echoes the trend of U.S. apparel retail sales (NAICS 448), which indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports could continue in the next two to three months.

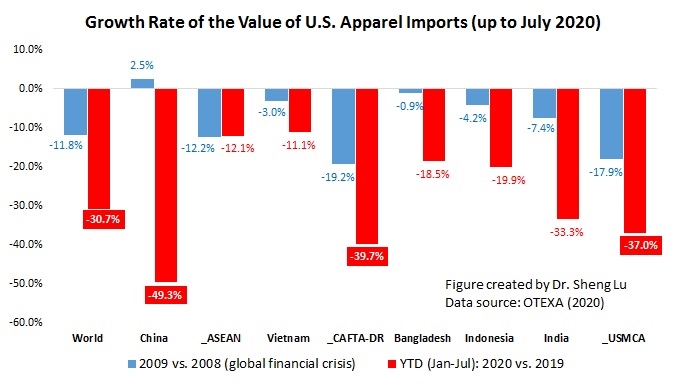

Nevertheless, between January and July 2020, the value of U.S. apparel imports decreased by 30.7% year over year, which has been much worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

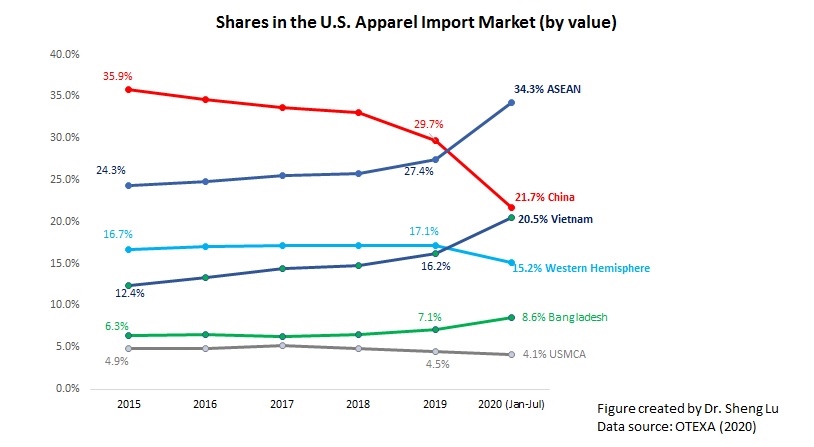

The latest trade statistics suggest that based on economic factors, U.S. fashion companies would like to continue to treat China as an essential apparel-sourcing base. As the first country hit by COVID-19, China’s apparel exports to the U.S. dropped by as much as 49.3% from January to July 2020 year over year. In February 2020, China’s market shares slipped to only 11%, and both in March and April 2020, U.S. fashion companies imported more apparel from Vietnam than from China. However, China had quickly regained its position as the top apparel supplier to the U.S., with a 26.3% market share in value and a 38.8% share in quantity in July 2020.

Different from the impact of the trade war, COVID-19 could benefit China as an apparel sourcing base as fashion companies have to “do more with fewer resources.” In general, China still enjoyed two notable advantages that other apparel supplying countries are unable to catch up in the short term. 1) unparalleled production capacity, meaning importers can source almost all products in any quantity from China vs. more limited production capacity (both in terms of variety and volume) in other alternative sourcing destinations. 2) China can mostly produce textile raw material locally vs. many apparel exporting countries still rely heavily on imported yarns and fabrics (supplied by China).

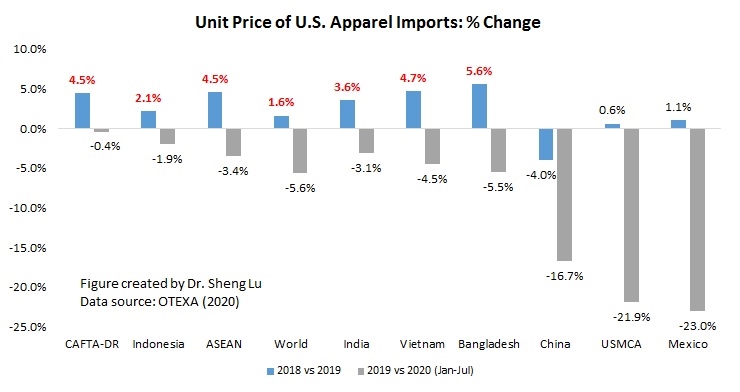

Contrary to common perceptions, apparel “Made in China” apparently are also becoming more price-competitive–the unit price slipped from $2.25/Square meters equivalent (SME) in 2019 to $1.88/SME in 2020 (January to July), or down more than 16.7% (compared with a 5.6% price drop of the world average). As of July 2020, the unit price of U.S. apparel import from China was only 65.7% of the world average, and around 25—35 percent lower than those imported from other Asian countries.

That being said, non-economic factors, from the deteriorating US-China relations to the reported Xinjiang forced labor issue, are increasingly complicating fashion companies’ sourcing decisions. Somehow as a warning sign, China’s market shares in the U.S. apparel import market slipped in both quantity and value terms in July 2020 compared with a month ago.

Despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.5% YTD in 2020 vs. 16.2% in 2019), ASEAN (34.3% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.6% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.5% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

However, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first seven months of 2020, only 8.8% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first seven months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 28.9% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the contributing factors why near sourcing has been stagnant.

As a reflection of weak demand, the unit price of U.S. apparel imports was lower in the first six months of 2020. The price index declined from 104.7 in 2019 to 99.0 YTD (Jan to Jul) in 2020 (Year 2010 =100). The imports from Mexico (price index =86.4 YTD in 2020 vs. 112.1 in 2019) and China (price index = 69.7 YTD in 2020 vs. 83.5 in 2019) have seen the most notable price decrease so far.