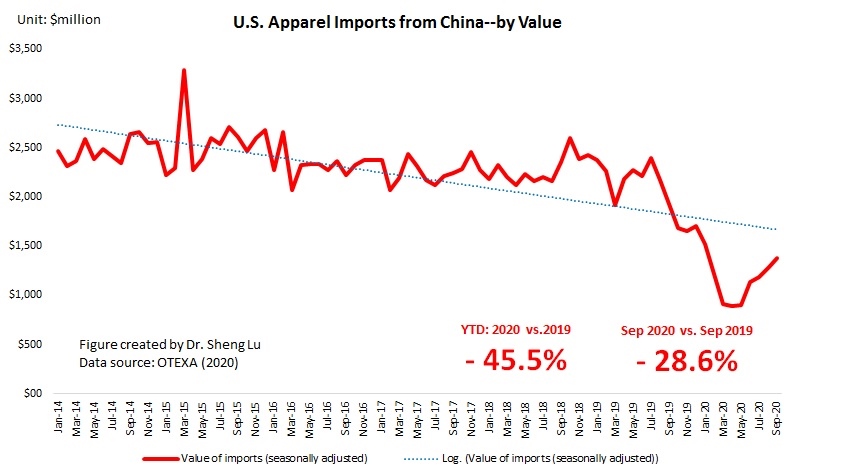

First, U.S. apparel imports continue to rebound thanks to consumers’ robust demand. The value of U.S. apparel imports in September 2020 went up by 8.8% from August 2020 (seasonally adjusted), a new record high since March 2020 when COVID-19 broke out in the States. As of September 2020, the volume of U.S. apparel imports has recovered to around 84-85% of the pre-coronavirus level. This result echoes the trend of U.S. apparel retail sales (NAICS 4481), which also indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports hopefully will last for another 1-2 months.

Data also shows that compared with the 2008 world financial crisis, Covid-19 has caused a more significant drop in the value of U.S. apparel imports. However, it seems the post-Covid recovery process has been more robust than the 2008 financial crisis. Notably, the Auto Regressive Integrated Moving Average (ARIMA) model forecasts that at the current speed of recovery, the value of U.S. apparel imports (seasonally adjusted) could start to enjoy a positive year over year (YoY) growth by February 2021 (or around 11 months after the outbreak of Covid-19 in March 2020). In comparison, when recovering from the 2008 world financial crisis, it took almost 15 months to turn the YoY growth rate from negative to positive.

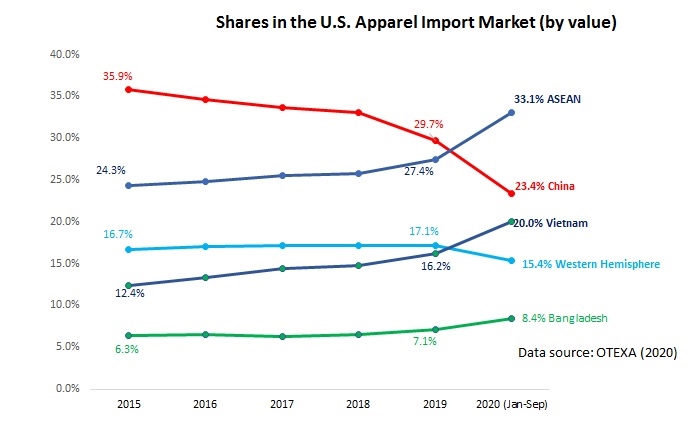

Second, still, no evidence suggests that U.S. fashion companies are giving up China as one of their essential apparel-sourcing bases. Notably, since May 2020, China had quickly regained its position as the top apparel supplier to the U.S. market. From June to September 2020, China’s market shares have stably stayed at around 27-28% in value and 40-42% in quantity.

According to the media, some sourcing orders are returning to China as China’s competitors in Asia are struggling with more limited production capacity, shortage of raw material and supply chain disruption caused by Covid-19.

That being said, trade data suggests that U.S. fashion companies continue to reduce their “China exposure” overall. For example, both the HHI index and the market concentration ratios (CR3–total market shares of top 3 suppliers and CR5–total market shares of top 5 suppliers) indicate that apparel sourcing orders are gradually moving from China to other Asian countries–it is interesting to see HHI, CR3 and CR5 all suggest a more diversified apparel sourcing base in 2020 (Jan-Sep) than in 2018 and 2019; however, the value of CR5 (exclude China) reached a new record high in 2020 (Jan-Sep).

Third, related to the point above, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.0% YTD in 2020 vs. 16.2% in 2019), ASEAN (33.1% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.4% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.4% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

Fourth, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first nine months of 2020, only 9.1% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.4% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first nine months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 26% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the major contributing factors.

Just an anecdote–according to some industry insiders, the booming of E-commerce during the pandemic may also possibly explain why “near sourcing” is not reflected in trade data despite its reported growing popularity. Specifically, US fashion retailers would:1) import products from Asia and stock them in the bonded warehouses in Mexico (note: bonded warehouse means dutiable goods may be stored, manipulated, or undergo manufacturing operations without payment of duty). 2) When US consumers place orders, the retailer will ship products directly from these bonded warehouses in Mexico to the final destination. Most importantly, retailers could take advantage of the US de minimis rule (i.e., goods valued at $800 or less could enter the U.S. duty-free one person one day) and avoid paying tariffs– even though these products are counted as imports from Asian countries that do not have a free trade agreement with the United States. In other words, these products are not officially treated as imports from Mexico even though they are shipped from bonded warehouse in Mexico.

by Sheng Lu

It is fascinating that the US didn’t take use Covid-19 as an excuse to get sourcing out of China. The US has been talking about sourcing from other countries for a while but according to a graph in this post, there is no evidence that US fashion companies are giving up China as one of their main sourcing bases. If the US wanted to use the Eastern Hemisphere for sourcing as they have claimed to want before, the Coronavirus outbreak would’ve been the best escape. This article suggested that products coming from Mexico aren’t treated as imports from Mexico which again raises my suspicion as to why the US doesn’t want to source from Eastern Hemisphere countries if they are available.

I definitely agree with this. In a lot of other fields, such as medical, US firms have moved out of countries with poor relationships with the US government and have tried to reduce interdependency on other countries, especially China. As we discussed in class, it is not beneficial to put all of your eggs in one basket, even if it is outside of China. This has been a lesson learned the hard way throughout the pandemic. But, as shown by the graphs, nothing has really changed; no actions have been taken to follow through on these hard lessons. The pandemic should be seen as an opportunity to change many things, including potentially detrimental sourcing decisions.

The fact that the United States is rebounding in consumer spending despite the pandemic is not that surprising to me. This country is driven hugely by capitalism. And, in a time in which there is significantly less social interaction and, simply less things to do and places to go, it makes sense why individuals choose to spend their time shopping. The rise in e commerce, in mega-retailers like Amazon, are greatly responsible for this spike in online shopping. Also, despite US retailer’s initial plans to begin removing orders from China, it was only logical for them to continue relations in this time of crisis. China’s biggest strengths are its speed to market, and evidently, its resiliency. US retailers had no choice but to continue its trade despite the high tariffs because other Asian countries are unable to keep up. Only time will tell if other Asian suppliers will soon catch up, and, whether US retailers will eventually pull orders from China. With all this said, the financial recovery to me, a non-economist is a little bizarre. The reason why the COVID-19 recovery is V-shaped and much different from the 2008 financial crisis is unknown to me. Similarly, the whole phenomenon of “de minimis rule” was entirely new to me. The length at which receivers will go to obtain the goods duty-free proves that the Trade War was devastating to retailers.

After reading about the v-shaped recovery of the apparel industry, there are a few thoughts that come to mind. From what I understand about the US economic recovery from Covid-19 as a whole, severely limited fiscal support has led to a more k-shaped recovery, where the rich recover quickly and the poor do not. This makes me question the extent to which the recovery for the apparel industry so far can be attributed to increased economic activity (retail therapy) as a response to the dullness of quarantine among those who have fared well economically during the pandemic? And should this buzz of activity decline as life returns to normal, what will the new demand for apparel be with a supposedly smaller middle class?

Also, I am a little surprised that US fashion brands have not used this pandemic as more of an opportunity to restructure their sourcing strategies. The US is still relying heavily on China and increasingly on other countries in Asia such as Vietnam, and the data indicates that there is slightly less of a reliance now on sourcing from the Western Hemisphere. This seems like a plan that prioritizes short-term benefits to me, but I worry that not enough thought is being given to long-term strategies. It would have been nice to see greater investments into developing a more robust Western Hemisphere supply chain (despite its limitations), because of its geographic proximity and therefore stability in the face of adversity. With the Asian region slowly starting to become less reliant on the US as an export market (with the US withdrawing from the TPP and the recent establishment of RCEP), I think it is crucial that US fashion brands start developing long-term strategies that do not revolve around Asia as soon as possible.

It is very interesting to me that even through COVID-19, Asia has remained the largest source of apparel for the United States market, even as some countries struggle with limited production capacity. Because this virus has affected the entire world, many countries were effected in the same way with production, so the United States didn’t have to necessarily change where they get their products. It is confusing however that the United States did not take the Coronavirus as an opportunity to stop sourcing from China and other Asian countries, as we have previously discussed wanting to do. With the trade war especially, the United States should be trying to make their way out of receiving imports from China.

It’s pretty amazing how much COVID effected the apparel industry but also how little it did. The U.S. still sources from China and the same countries it did before even after the trade-war and all the disagreements between the two countries. On the other hand we were obviously all negatively effected by COVID due to a lot of restrictions put in place which impacted the industry as a whole. The graphs depict huge decreases during the first months of COVID and it is scary to see. It makes me question if this will happen again if there is a second wave of COVID and what will happen to the industry then. Maybe countries will have chances to import from other countries that aren’t as affected this time.

U.S. companies have always strived to maximize their profits in the apparel industry. Affected by the epidemic, U.S. companies are abandoning Chinese sources of procurement, but this does not affect Asia’s position in the U.S. apparel market. Under the influence of COVID-19, American fashion retailers do not have many choices. They need to pay high taxes. I believe that in future Asia and the United States will have new sales strategies in the clothing trade in order to deal with the epidemic

This is very thoughtful.

When reading through this article and watching the lectures for this week many facts stuck out to me. To start, I was shocked to learn previously that between January and August of 2020, the value of U.S. apparel imports decreased by almost 30% and that it has been much worse than the performance during the 2008-2009 recession. As we know, the economic impacts that have come with the pandemic have already taken a deep effect, laying people off and causing stocks to fluctuate. Although, an encouraging thought is that many consumers are very much willing to spend considering they don’t have much else to do. For some reason, this article made me think about American consumers and how their spending habits will change with this holiday season. From what I could tell, many large brands and small businesses had massive sales to entice online shoppers. Not to mention, many people have been encouraging others to “shop small” this holiday season to support small business owners. Further, with important social movements such as Black Lives Matter, small black-owned businesses are finally starting to get recognition. I am curious to see that after the pandemic how consumer spending habits will change. Check out the link below for more information about small-business consumer spending. https://www.cnbc.com/2020/11/28/small-business-saturday-holiday-gift-givers-want-their-money-to-matter-.html

COVID has been a struggle for everyone around the world. Surprisingly, production has not changed much since the virus had begun. The US is still manufacturing their apparel in China due to their low costs. Even after COVID-19, the US did not consider manufacturing domestically and providing more jobs domestically. Especially considering that peoples lives were in danger all around he world and people were losing jobs all over the country, it may have been a good idea to consider sourcing domestically for the safety of people in third-world countries who also do not have access to the same health care as we do here in the US.

What I found interesting about this article is how little the Covid-19 pandemic affected the import market of the US in the long run. When the pandemic first hit, the import market dropped dramatically but we have seen it bounce back very quickly, which created the V shape shown on the graphs. As stated in the article, China is still the top apparel supplier for the US, and other countries in Asia also remain top suppliers. I found this data very interesting. I would have thought that more US companies would have had fewer imports from china and had an increase in domestic suppliers. We learned about how during the pandemic it became more difficult to ship from country to country due to the new protocols put into place. Therefore, you would think that the US would choose to source internally to make it easier but no data shows this is the case. Maybe it is still too early to see these changes take place but as time goes on we will see these changes.