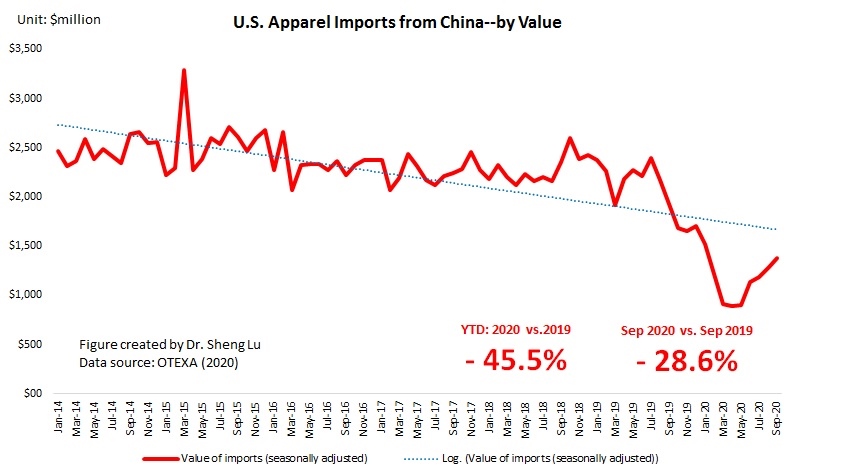

First, U.S. apparel imports continue to rebound thanks to consumers’ robust demand. The value of U.S. apparel imports in September 2020 went up by 8.8% from August 2020 (seasonally adjusted), a new record high since March 2020 when COVID-19 broke out in the States. As of September 2020, the volume of U.S. apparel imports has recovered to around 84-85% of the pre-coronavirus level. This result echoes the trend of U.S. apparel retail sales (NAICS 4481), which also indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports hopefully will last for another 1-2 months.

Data also shows that compared with the 2008 world financial crisis, Covid-19 has caused a more significant drop in the value of U.S. apparel imports. However, it seems the post-Covid recovery process has been more robust than the 2008 financial crisis. Notably, the Auto Regressive Integrated Moving Average (ARIMA) model forecasts that at the current speed of recovery, the value of U.S. apparel imports (seasonally adjusted) could start to enjoy a positive year over year (YoY) growth by February 2021 (or around 11 months after the outbreak of Covid-19 in March 2020). In comparison, when recovering from the 2008 world financial crisis, it took almost 15 months to turn the YoY growth rate from negative to positive.

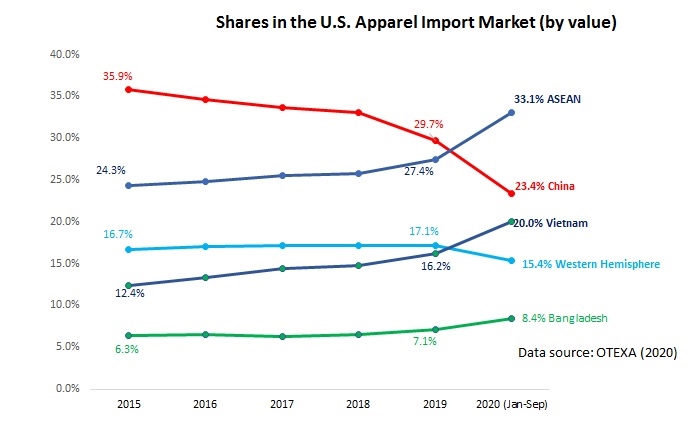

Second, still, no evidence suggests that U.S. fashion companies are giving up China as one of their essential apparel-sourcing bases. Notably, since May 2020, China had quickly regained its position as the top apparel supplier to the U.S. market. From June to September 2020, China’s market shares have stably stayed at around 27-28% in value and 40-42% in quantity.

According to the media, some sourcing orders are returning to China as China’s competitors in Asia are struggling with more limited production capacity, shortage of raw material and supply chain disruption caused by Covid-19.

That being said, trade data suggests that U.S. fashion companies continue to reduce their “China exposure” overall. For example, both the HHI index and the market concentration ratios (CR3–total market shares of top 3 suppliers and CR5–total market shares of top 5 suppliers) indicate that apparel sourcing orders are gradually moving from China to other Asian countries–it is interesting to see HHI, CR3 and CR5 all suggest a more diversified apparel sourcing base in 2020 (Jan-Sep) than in 2018 and 2019; however, the value of CR5 (exclude China) reached a new record high in 2020 (Jan-Sep).

Third, related to the point above, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.0% YTD in 2020 vs. 16.2% in 2019), ASEAN (33.1% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.4% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.4% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

Fourth, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first nine months of 2020, only 9.1% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.4% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first nine months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 26% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the major contributing factors.

Just an anecdote–according to some industry insiders, the booming of E-commerce during the pandemic may also possibly explain why “near sourcing” is not reflected in trade data despite its reported growing popularity. Specifically, US fashion retailers would:1) import products from Asia and stock them in the bonded warehouses in Mexico (note: bonded warehouse means dutiable goods may be stored, manipulated, or undergo manufacturing operations without payment of duty). 2) When US consumers place orders, the retailer will ship products directly from these bonded warehouses in Mexico to the final destination. Most importantly, retailers could take advantage of the US de minimis rule (i.e., goods valued at $800 or less could enter the U.S. duty-free one person one day) and avoid paying tariffs– even though these products are counted as imports from Asian countries that do not have a free trade agreement with the United States. In other words, these products are not officially treated as imports from Mexico even though they are shipped from bonded warehouse in Mexico.

by Sheng Lu