See updated data: What’s Happening with Myanmar’s Apparel Exports (Updated August 2022)

First, the textile and apparel industry plays a significant role in Myanmar’s economy, particularly the export sector. Data from the UNComtrade shows that textile and apparel accounted for nearly 30% of Myanmar’s total merchandise exports in 2019, followed by footwear and luggage. Industry data also indicates that the textile, apparel, and footwear industry employed more than 1.1 million workers in Myanmar in 2018, up from only 0.3 million in 2016.

On the other hand, as a developing country, Myanmar highly depends on the imported textile raw material. As of 2019, nearly 83% of Myanmar’s textile imports came from China.

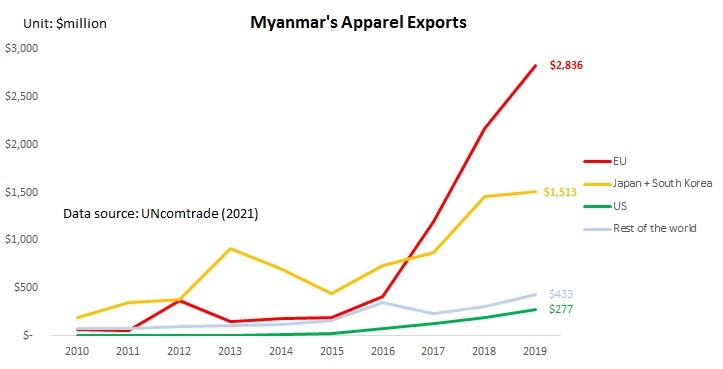

Second, since the United States lifted the import ban on Myanmar and the EU reinstated the Everything But Arms (EBA) trade preferences for the country in 2013, Myanmar has been one of the most popular emerging apparel sourcing bases among fashion companies. From 2015 to 2019, Myanmar’s apparel exports to the world enjoyed an impressive 57% annual growth. Myanmar’s apparel exports to the EU (97% annual growth) and the United States (78% annual growth) have been growing particularly fast.

From 2019 to 2020, some of the top fashion brands that carry apparel items “Made in Myanmar” include United Colors of Benetton, Next, Only, Guess, Jack & Jones, and Mango.

Second, the reasons why fashion companies source apparel from Myanmar are multiple:

- Thanks to foreign investment (e.g., nearly half of Myanmar’s garment factories are foreign-owned), Myanmar specializes in making relatively higher-quality functional/technical clothing (i.e., outwear like jackets and coats). This is different from many other apparel exporting countries like Bangladesh, Vietnam, and Cambodia, mostly exporting low-cost tops and bottoms.

- Myanmar’s apparel exports were able to enjoy duty-free market access in the EU, Japan, and South Korea. Myanmar was also a beneficiary of the US Generalized System of Preferences (GSP) program. This explains why Myanmar’s apparel exports mostly go to the EU (56%), Japan and South Korea (30%), and the US (5.5%).

- Relatively low production cost—garment workers earn around $85/month in 2019.

However, Myanmar still accounts for a tiny share in fashion companies’ total sourcing portfolio because of the size effect. For example, as of 2019, less than 0.1% of US and EU countries’ apparel imports came from Myanmar.

Third, western fashion brands could reevaluate their sourcing strategy from Myanmar because of its recent coup. Notably, in a new study, we find that apparel sourcing is not merely about “competing on price.” Instead, fashion companies give substantial weight to the factors of “political stability” and “financial stability” in their sourcing decisions—reputation risk matters. The country’s latest political instability will hurt Myanmar’s attractiveness as an apparel sourcing base, given many other alternatives out there.

Further, the international community, including the US and the EU, is considering new sanctions against Myanmar. Should Myanmar lose its EU’s EBA eligibility or no longer enjoy duty-free access to its key apparel export markets, the country’s apparel exports could be among the biggest losers. Notably, it could be challenging for Myanmar to find an alternative apparel export market during the pandemic. (for example, only 1.3% of Myanmar’s apparel exports went to China in 2019).

By Sheng Lu

Further reading:

- Myanmar’s Garment Factories Suffer One-Two Punch of Covid and Coup (Wall Street Journal)

- Myanmar coup clouds future of country’s crucial garment industry (Nikkei Asia Review)