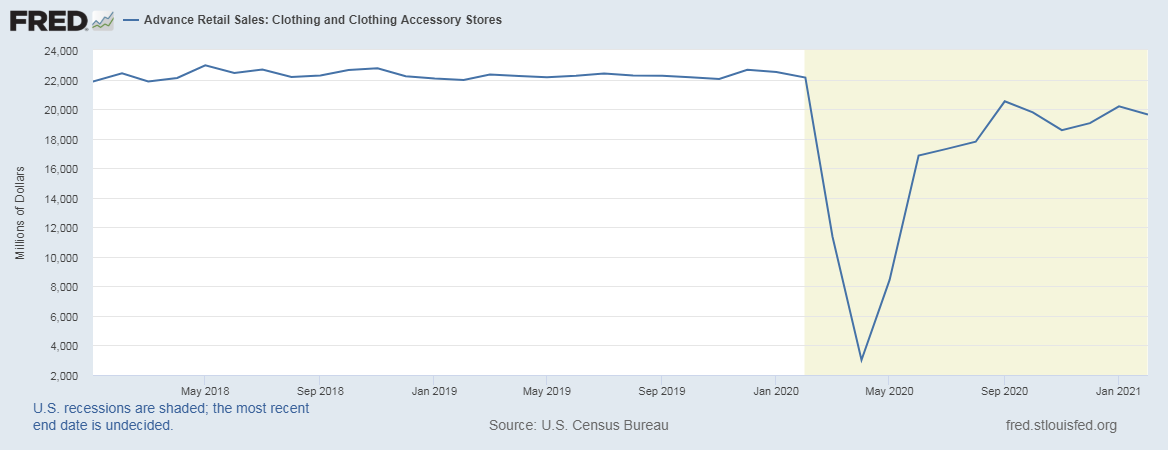

First, thanks to consumers’ resumed demand and a more optimistic outlook for the U.S. economy, US apparel imports went back to the robust recovery trajectory in February 2021. Specifically, the value of U.S. apparel imports in February 2021 went up by 4.5% from January 2021 (seasonally adjusted) after a straight three-month drop. Even though the absolute value of U.S. apparel imports in February 2021 was still 8.7% lower than last year, it was the best performance since December 2020.

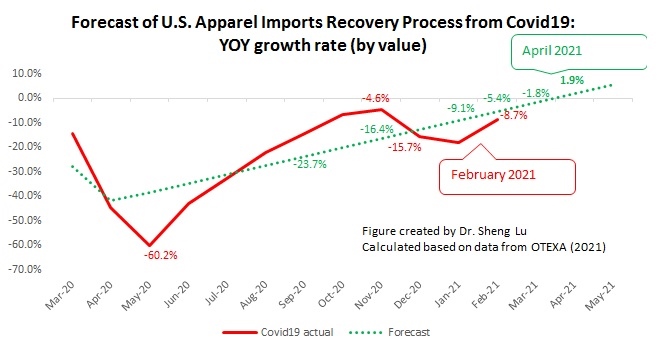

The Auto Regressive Integrated Moving Average (ARIMA) model forecasts that at the current speed of recovery, the value of U.S. apparel imports (seasonally adjusted) may start to enjoy a positive year over year (YoY) growth by April 2021. Euromonitor also forecasts that U.S. apparel retail sales in 2021 may enjoy a 3.6%-6.7% growth from 2020 (in value).

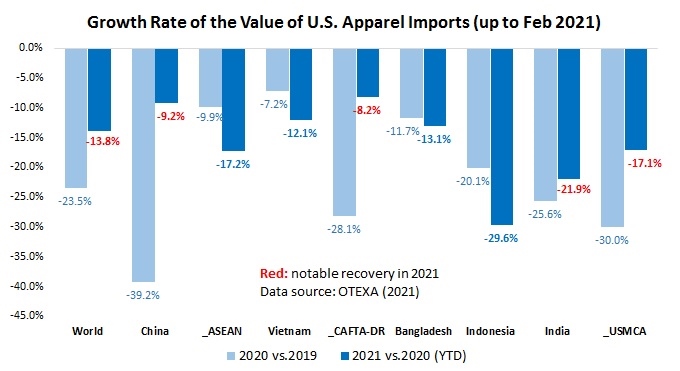

Second, data indicates that China remains the top apparel supplier for the U.S. market both in quantity (36%) and value (22.5%) in 2021 (Jan-Feb). Meanwhile, U.S. fashion brands and retailers continue to reduce their “China exposure” amid the pandemic. For example, both the HHI index and market concentration ratios (CR3 and CR5) suggest that apparel sourcing orders are gradually moving from China to other Asian countries.

The constant market share (CMS) model also shows that before the tariff war and COVID-19, the competitiveness of apparel “Made in China” has weakened in the U.S. market. While the increased U.S. import demand partially mitigated the impact of negative factors (such as the tariff war) on China’s apparel exports to the U.S. market from 2018 to 2019, the demand collapsed during the pandemic. On the other side, while China gained an additional $202 million in exports by adjusting its apparel export product structure during the pandemic, it continued to lose market shares in many regular product categories (especially cotton and wool products).

Further, the latest data confirms that some non-economic factors negatively affect China’s prospect as an apparel sourcing destination. For example, the alleged forced labor issue related to Xinjiang, China, and a series of actions taken by the U.S. government (such as the CBP withhold release orders) have significantly affected U.S. cotton apparel imports from China. Measured by value, only 15.4% of U.S. cotton apparel came from China in 2020 (and 15.6% in the most recent 12 months), a significant drop from 27% back in 2018. While China’s total textile and apparel exports to the US decreased by 26% in the most recent 12 months (i.e., March 2020-February 2021), China’s cotton textiles and cotton apparel exports to the US went down by over 40%.

Third, Asia as a whole remains the single largest source of apparel for the U.S. market amid the pandemic, stably accounting for around 75% of the import value. Other than China, Vietnam, ASEAN, Bangladesh, and Cambodia ALL gain additional market shares both from 2019 to 2020 and during the most recent 12 months (i.e., March 2020-February 2021 vs. March 2019-February 2020).

Fourth, while U.S. apparel imports from the Western Hemisphere stay stable overall, sourcing from CAFTA-DR members seems to gain new momentum. For example, 16.5% of U.S. apparel imports came from the Western Hemisphere in 2021 (Jan-Feb), slightly up from 15.9% in 2020 (Jan-Feb). Notably, CAFTA-DR members’ market shares increased to 10.1% in 2021 (Jan-Feb) from 9.5% in 2020 (Jan-Feb), compared with USMCA members’ loss of 0.2% market shares over the same period. CAFTA-DR and USMCA members currently account for around 60% and 25% of U.S. apparel imports from the Western Hemisphere. They are also the single largest export market for U.S. textile products (around 70% in value). Strengthening the western hemisphere textile and apparel production will remain a hot topic in the Biden administration.

by Sheng Lu

What is interesting about the article is how big Asia’s production is overall. Asia as a whole remains the single largest source of apparel for the U.S. market amid the pandemic even with the trade barriers available. Furthermore, the data indicates that China remains the top apparel supplier for the U.S. market even with companies shifting. It just shows how just how massive apparel suppliers are in these nations, and how China is able to use massive economies of scale to its advantage.

I agree with your response on the article. I just want to add to your comment about economies of scale. Yes, China is using massive economies of scale to its advantage, especially after we see what the RCEP has done. The RCEP has made a trade agreement between Asia’s top trading competitors, China, Japan, and South Korea. Thus, now all of these powerhouses are cohesively working together, ultimately becoming unstoppable in the apparel and textile production and trading sector.

I agree that China will proceed with leading soucing for U.S. fashion brands; non-economic factors, such as forced labor in Xinjiang, have yet to elicit the reduction of “China exposure” and the start of vertical integration. However, I expect China to lose its overall share as apparel companies offshore production to Vietnam and Bangladesh.

I am still overall surprised with how much apparel sourcing is being done after the pandemic. I would have thought it was a done deal to instantly start near shoring. Although it is known how difficult and timely it is to create new trading partners and relationships, I just wasn’t expecting how much sourcing is still being done even after a year we have endured the pandemic. I do agree with the Biden administration to start moving our sourcing to the Western Hemisphere. I think we can benefit a lot from that, especially in having a protected and lucrative market in exporting textiles. Furthermore, it is extremely hard to compete with China and we just seem to keep being the losers from their trade deals. My opinion is we have to stop relying on them and cut off a lot of trading deals with them.

I think that it is impressive and interesting to see how China’s cotton textiles and cotton apparel exports have dropped by 40% to the US. It is also important to note that sourcing from CAFTA-DR members are gaining momentum. This is extremely important because this shows that the trade agreements/incentives are working. 16.5% of apparel imports to the US has come from the western hemisphere in 2021. As hard as it is to compete with China, the western hemisphere is doing a good job in trying to keep production nearshore and support countries within the western hemisphere. Using these trade agreements are already strengthening the US textile industry, but we want to increase that strength even further. Even though there is proof that the agreements are working, the US needs to decrease their overall dependency on China and other Asian countries. This can only happen if we continue to support trade within the western hemisphere.

I’m surprised that data indicates China remaining the top apparel supplier for the U.S. market, albeit losing market share in product categories and facing scrutiny as an apparel sourcing destination. I anticipate further diversification throughout Asia and for global retailers with multinational supply chains to take advantage of the RCEP – which offers an incentive for brands to enter signatory countries other than China. The strengthening of the Asian market may disrupt the threat of cheap apparel “Made in China,” presenting a narrow opportunity for the Western Hemisphere to remain competitive and reduce its “China exposure.”

I am somewhat surprised that data still indicates China remains as the top apparel supplier for the U.S. market, even though the U.S. market has made attempts to diversify their sourcing strategy. I think within the next few years we will see the U.S. start to move away from China because of several reasons. One reason including the alleged forced labor issue related to Xinjiang, China. Another reason is the US-China tariff war, and as brands have more time to develop new sourcing strategies that don’t include such high tariff rates, they will move away from China. I agree with Sarah and her statement that the strengthening of the Asian market may disseminate the cheap apparel benefits that are usually associated with China. I specifically think we will see the U.S. start to increase sourcing from Vietnam and Bangladesh.

I find it interesting that so much sourcing is still being done from china following the pandemic and the tariff war I anticipated more companies moving out of China to quickly growing production markets such as Vietnam or Bangladesh. Additionally, because of COVIDs impact to supply chains, I’m surprised more companies did not near shore to increase their efficiency and flexibility.

Im shocked to see China as the top apparel supplier for the United States considering that fashion brands and retailers started reducing their exposure to the China market amid the pandemic. It seems as if some companies have started to move their production into other markets, but I would have expected more of a ripple effect for more companies to do so. I think it will be easy for companies to reduce dependency on China, however it takes a lot to change suppliers involving many different logistic strategies. These may be too timely and costly to take on during an uncertain time.

I have to say, because of the recent covid surge in India & southeast Asia, US fashion brands may have no choice but to switch to source from China. Even though it could be a minority view, I still think it make sense to continue sourcing from China from the economic perspective

It’s mind-blowing how massive China’s production currently is for the U.S. market, even with the trade barriers it must endure. Data shows that it remains the number-one place for apparel suppliers even with a pandemic and companies changing their business plans. If the Biden administration were to move the US’s sourcing to the western hemisphere, a lot of good could come from that especially since we have a protected and lucrative market for textiles. It’s also important to note that this could help us to become less dependent on other countries.

This was very shocking to see that China still remains the largest apparel supplier during the pandemic. During the pandemic a lot of brands restricted their connections with China to avoid exposure. This just goes to show how popular China is within the industry. The pandemic did allow specific brands to diversify where they are sourcing from and choose countries that are less developed than others. Developing countries and smaller brands gained a lot of recognition because people wanted to keep small businesses afloat during such a hard time. China is a large competition for the United States and the pandemic has emphasized this a lot as countries and businesses are still sourcing from China over the United States.

The data shows that China remains an important supplier of apparel to the U.S. market. This means that the U.S. import trade is still dependent on China. From the perspective of COVID-19, China has managed to recover its fashion industry and resume normal supply chain operations at a rapid pace. However, the U.S. trade was so affected by COVID-19 that there was no way to continue the normal operation and development of the fashion industry, and everything came to a halt. Coupled with the unending tariff war between the U.S. and China, the negative impact on the U.S. will be even greater. But the U.S. has no way to not rely on Chinese apparel suppliers during this time.

It is very interesting to see that China remainds the top apparel supplier for the U.S market even with U.S fashion brands and retailers attempts to reduce their presence in China. This proves how dominant China has been as an apperel supplier for the United States the past few years. Even with many obstacles thrown at them such as being the epicenter of the COVID-19 pandemic and being in the midst of a tariff war they still remain the top apparel supplier. However, the decrease of China’s total textile and appafrel exports to the US by 26% in the last 12 months suggest that in the recent future we can expect a new country to be our top apparel supplier.

I find it so fascinating how quickly the US and other developed countries are recovering from COVID-19 . According to this article, there has already been a 4.5-8.7% increase in demand for apparel/ textiles after a year. This was matched to the demand during the holidays during the pandemic which shows that consumers have began to get used to the online nature of shopping or are becoming more keen on shopping in stores. It was a bit surprising to see Asean nations surpass China in being top producer even though China was hit with the pandemic first. I felt like China’s recovery was quite quick in comparison, however, that’s amazing that those nations took initiative to step up.

There are several key trends currently within the relationship between covid and the US apparel imports. Primarily, consumers have begun to demand more clothing which has increased US apparel imports by 4.5% from January this year. There was a negative trend for three months straight, however the value of US imports is projected to have a positive year given that retail sales will grow from 3.6 to 6.7 from 2020. On the other hand, the data also shows that China continues to be the top apparel supplier for the US market. Throughout this pandemic however, US fashion brands and retailers are reducing their China exposure. Both the HHI index and market concentration rates indicate that there are more diversified sourcing measures being taken. This thing goes to show that many countries are sourcing away from China and from other Asian countries. The shift away from sourcing from China could potentially be a result of the forced labor issue related to Xinjiang, China as well. This is seen in through the cotton apparel imports dropping from 27% to 15.4% within the last three years. A more encompassing view is that China’s total textile and apparel exports to the US have decreased by 26% over the past 12 months. As reflected in the data here, as well as the release of an abundant number of COVID-19 vaccines, the apparel and textile industry will recover quite smoothly in time.

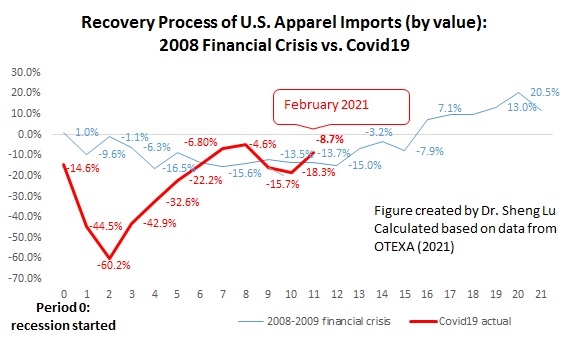

I think it’s interesting to compare the financial crisis of 2008-2009 and the COVID-19 pandemic because although recessions both occurred during these times, there were significant differences between the events. The pandemic affected the entire world, sparked more social and political issues among the United States, and has been able to recover from the economic downfall much quicker. On the other hand, the 2008-2009 financial crisis affected mostly just the U.S. and took a longer time to get better. I believe that the U.S. was able to recover financially from the pandemic because of its access to advanced technology including having wifi in most American households. By 2020, the Internet was flexible enough to allow for more efficient online shopping features and digital marketing was becoming more popular, so not only was online shopping easy for young people, but older markets as well. Back in 2008, the Internet was still new and brick-and-mortar shopping still dominated over e-commerce.

I find it very interesting that the value of the United States apparel imports went up by 4.5% after the three month drop. I say that because it was the best performance since December despite it being lower than the year before that. Another piece of this article that stuck out to me was that China remains the top apparel supplier for the United States market. I am not surprised because I always see signs that say “made in china”. I think it is very interesting that Asia as a whole remains the largest source of apparel for the United States market. I find it intriguing that all these countries are working together.

Why “it is very interesting that Asia as a whole remains the largest source of apparel for the United States market.” ? What is your explanation?

What interests me most about this article is that after the US apparel market began to implement the strategy of import diversification sourcing, China is still the largest supplier in the US apparel market. This further shows that China is still very important in the field of exporting countries.

I find it extremely interesting that China still remains the largest supplier in the US apparel market. I would have thought that between the tariff war and the US’s attempts to diversify their suppliers, this statistic would have changed. However, when taking the recent surges of COVID-19 cases in India and other Asian countries into consideration, I suppose that this statistic does make sense. Despite the US’s intentions to diversify their suppliers, these recent surges, especially in India, have had a debilitating effect on the governments and countries as a whole. These surges have made it virtually impossible to rely on India or Asian countries as providers during these times.

It is very interesting that China is still ranked the top apparel supplier for the U.S. market even though the country has lost market share in product categories and countries are really reevaluating them as an apparel sourcing place. I think that as time goes on brands will begin to discover different suppliers within Asia and hopefully even the western hemisphere. On the other hand it makes sense for china to still be top in the list to supply from as well as for other countries to switch to china because of the massive covid outbreaks in other Asian countries.

After reading this article, I was surprised to see that China was a top supplier for the US for multiple reasons. First of all the China Tariff war has been ongoing for multiple years, and I assumed that that would move sourcing more towards other countries, such as Asian countries. I am also surprised that supply chains aren’t moving towards other countries due to diversification. Due to the pandemic, many companies want to diversify their sourcing so they are not completely dependent on one singular country, so I am surprised there is still so much exporting from China. In the future, I predict that many countries will move their production to Asian countries such as Bangladesh or Vietnam. Not only is the labor commonly cheaper in these countries, but it would be beneficial to have a more diversified supply chain. Furthermore, I think the US could even move towards exporting to other Western Hemisphere countries. If this did happen, they would receive fewer tariffs because of the trade agreements, and I think it would be beneficial for all parties involved.

I find it so surprising how big of a supplier China still is during the pandemic. No one else compares to how big they are. I thought that they would be more hurt by some brands moving away from China since Covid began. I also thought that more companies would start to export from Bangladesh and other countries that are even cheaper. It makes sense though that chinas textile and apparel exports to the US decreased by 26% since brands had to pushback orders and lower order numbers as people slowed down shopping.

This article was also very fascinating to read about. China is still at the top for being a supplier for the US. Along with them being a top supplier they are the top supplier in quantity at 36% and also value at 22.5%. This comes shocking due to the fact that many brands and retailers have actually gotten out of China and started reducing the amount they were producing in China. The pandemic was a main reason for all of these retailers and brands to finally step out of China. China was unable to produce lots of products because there was such a high demand for them by there own country. This took a lot of adjustment and wasn’t the most efficient at first. There was many delays when sourcing had to come from other countries. It was honestly very difficult during the hard time. The tariff war between China and the US has been going on constantly for years. Forced labor in certain parts of China have affected the cotton textile. Only 15.4% of U.S. cotton apparel came from China in 2020 according to the chart and overall China’s cotton textiles and cotton apparel exports to the US went down by over 40%. This has decreased significantly over the years.

While reading the article, I was shocked to find out that China still plays a huge part in the US as a supplier. Many companies have taken the time from the pandemic to shift away to better meet the demands of their consumers as well as help their company. In addition, there are many other countries that are able to provide the US with the same amount of “work” or labor just as China would for the same costs. I was not shocked to see that there was a 26% decrease of China exports to the US; with the pandemic, fashion companies and brands were forced to pushback orders and pile on past inventory due to the decrease in shoppers.

COVID has definitely had a major impact on everything worldwide. We Saw large examples of this in the apparel and textiles industries. Due to travel and shipping limitations during quarantine, we saw a major loss is revenue in the apparel industry due to businesses turning away countries. Because these businesses are unable to obtain their products from foreign countries, shipping times lengthened, orders were cancelled and apparel businesses began to take a major hit in it revenue streams. Apparel and textile industry workers were laid off during the beginning of COVID as well.