The EU region as a whole remains one of the world’s leading producers of textile and apparel (T&A). The value of EU’s T&A production totaled EUR137.3 bn in 2019, down around 2% from a year ago (Note: Statistical Classification of Economic Activities or NACE, sectors C13, and C14). The value of EU’s T&A output was divided almost equally between textile manufacturing (EUR68.7bn) and apparel manufacturing (EUR68.6bn).

Regarding textile production, Southern and Western EU, where most developed EU members are located such as Germany, France, and Italy, accounted for nearly 75% of EU’s textile manufacturing in 2019. Further, of EU countries’ total textile output, the share of non-woven and other technical textile products (NACE sectors C1395 and C1396) has increased from 19.2% in 2011 to 23.0% in 2017, which reflects the on-going structural change of the sector.

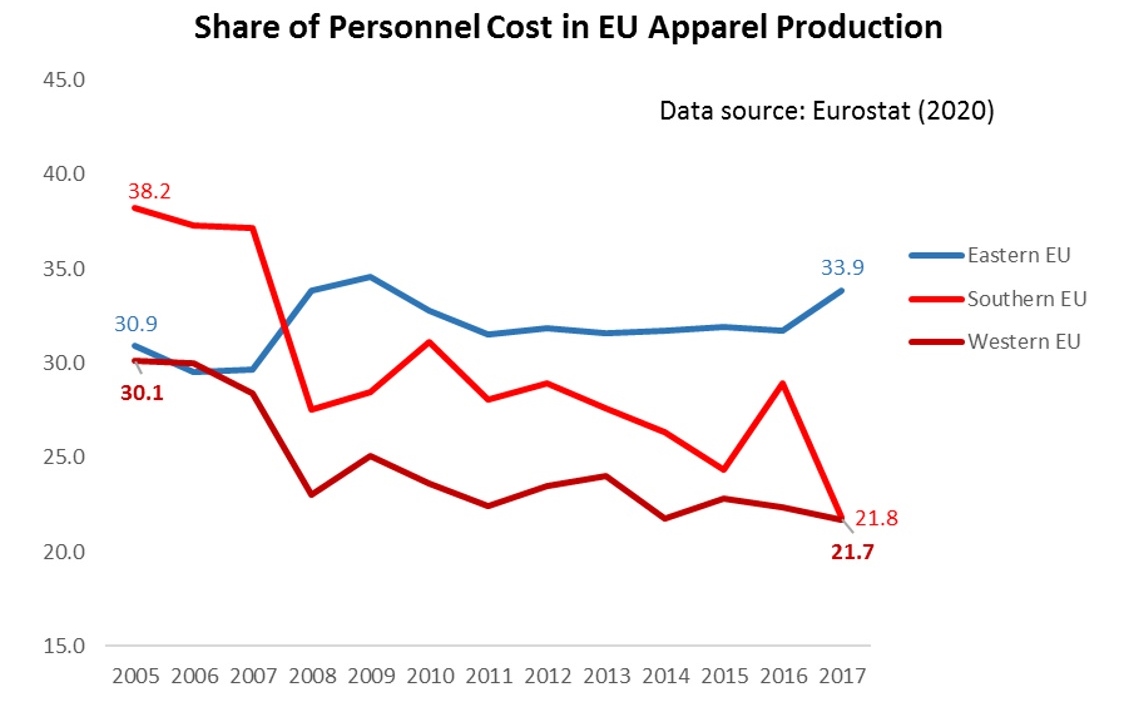

Apparel manufacturing in the EU includes two primary categories: one is the medium-priced products for consumption in the mass market, which are produced primarily by developing countries in Eastern and Southern Europe, such as Poland, Hungary, and Romania, where cheap labor is relatively abundant. The other category is the high-end luxury apparel produced by developed Western EU countries, such as Italy, UK, France, and Germany.

It is also interesting to note that in Western EU countries, labor only accounted for 21.7% of the total apparel production cost in 2017, which was substantially lower than 30.1% back in 2006. This change suggests that apparel manufacturing is becoming capital and technology-intensive in some developed Western EU countries—as companies are actively adopting automation technology in garment production.

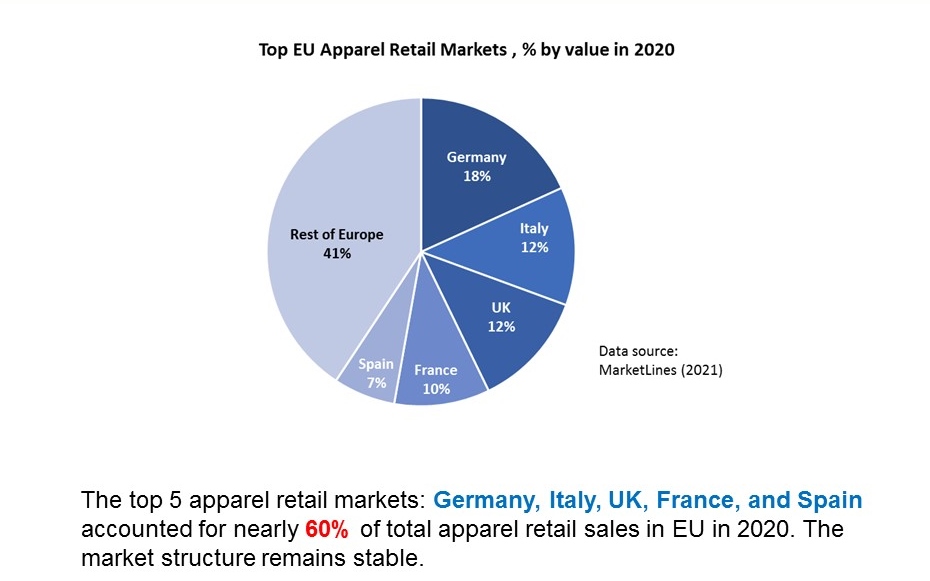

Because of their relatively high GDP per capita and size of the population, Germany, Italy, UK, France, and Spain accounted for nearly 60% of total apparel retail sales in the EU in 2020. Such a market structure has stayed stable over the past decade.

Data source: UNcomtrade (2021)

Intra-region trade is an important feature of the EU’s textile and apparel industry. Despite the increasing pressure from cost-competitive Asian suppliers, statistics from UNComtrade show that of the EU region’s total US$73.8bn textile imports in 2019, as much as 54.6% were in the category of intra-region trade. Similarly, of EU countries’ total US$204.0bn apparel imports in 2019, as much as 37.4% also came from other EU members. In comparison, close to 98% of apparel consumed in the United States are imported in 2019, of which more than 75% came from Asia (Eurostat, 2021; UNComtrade, 2021).

Regarding EU countries’ textile and apparel trade with non-EU members (i.e., extra-region trade), the United States remained one of the EU’s top export markets and a vital textile supplier (mainly for technical and industrial textiles). Meanwhile, Asian countries served as the dominant apparel sourcing base outside the EU region for EU fashion brands and retailers.

The EU textile and apparel industry is not immune to COVID-19. According to the European Apparel and Textile Federation (Euratex), the EU textile and apparel production feel 9.3% and 17.7% respectively in 2020 from a year ago.

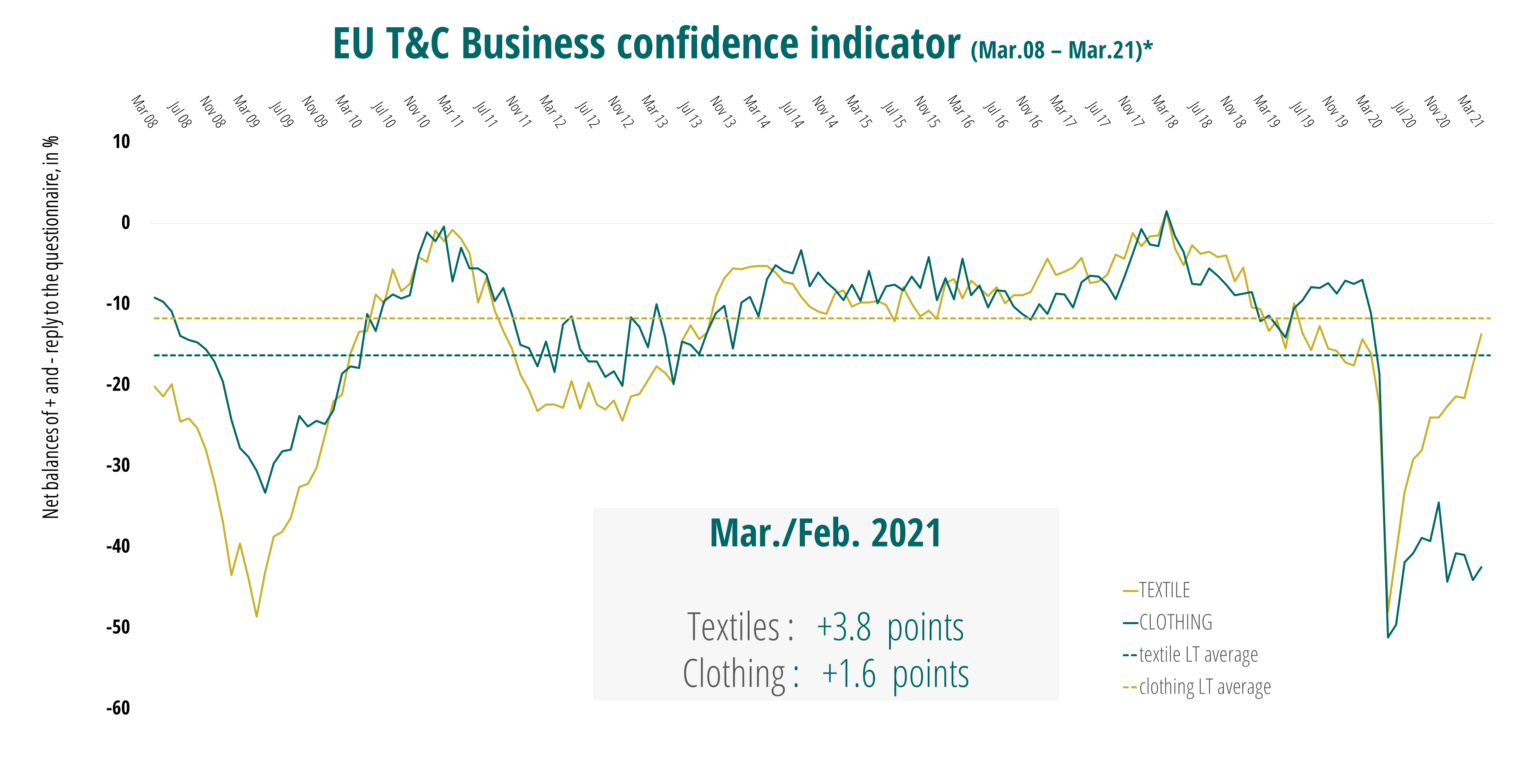

2021 hopefully will be a year of recovery and growth for the EU textile and apparel industry. According to Euratex, the EU Business Confidence indicator of March 2021 gained momentum, with a confirmed upward trend in the textile industry (+3.8 points), and a modest recovery in the clothing industry (+1.6 points). However, Euratex also noted that EU textile and apparel companies still face daunting challenges and uncertainties in 2021, ranging from the rising raw material price, increasing transportation cost, to political instability in some key sourcing destinations (such as China and Myanmar).

by Sheng Lu