According to the latest statistics released by the American Apparel and Footwear Association (AAFA):

In 2020, the US apparel and footwear industry directly employed about 3 million Americans and employed another 2.3 million indirectly.

In 2020, on average, every man, woman, and child in the United States spent $1,067.93 to buy 51.8 pieces of clothes and 5.8 pairs of shoes.

In 2020, US apparel and footwear production accounted for 3.5 percent and 2.3 percent of the US market, respectively.

Due to COVID-19, in 2020, US imports of apparel and footwear sank 16.4 percent and 23.5 percent, respectively. However, imports still supplied 96.5 percent of apparel and 97.7 percent of footwear available in the US market.

In 2020, the average effective tariff rate hit records for both apparel and footwear, reaching 15.5 percent and 13.0 percent, respectively.

First, footwear sourcing is much less diversified than apparel. As manufacturing footwear both requires specialized machines and can be labor-intensive, over 80% of US footwear imports came from three countries only, namely China, Vietnam, and Indonesia. This sourcing pattern is very different from apparel products, for which US companies have far more choices. Other than the top three, US also imports some high-end footwear products from Italy.

Second, while China remains No.1, Vietnam has quickly become the second-largest footwear supplier for the US market. Vietnam’s market shares (by value) reached a new record high of 32.9% in the first six months of 2021, up from 20% in 2017. Especially since the US Section 301 action began to affect footwear imports from China, US retailers have increasingly moved sourcing orders from China to Vietnam to mitigate trade war’s negative impacts [Note: most footwear products are covered by Tranche 4A].

As of June 2021, top US retailers that carry footwear “Made in Vietnam” include Puma, Nike, UGG, Vans, and New Balance.

Nike, “Made in Vietnam”, retail price =$100

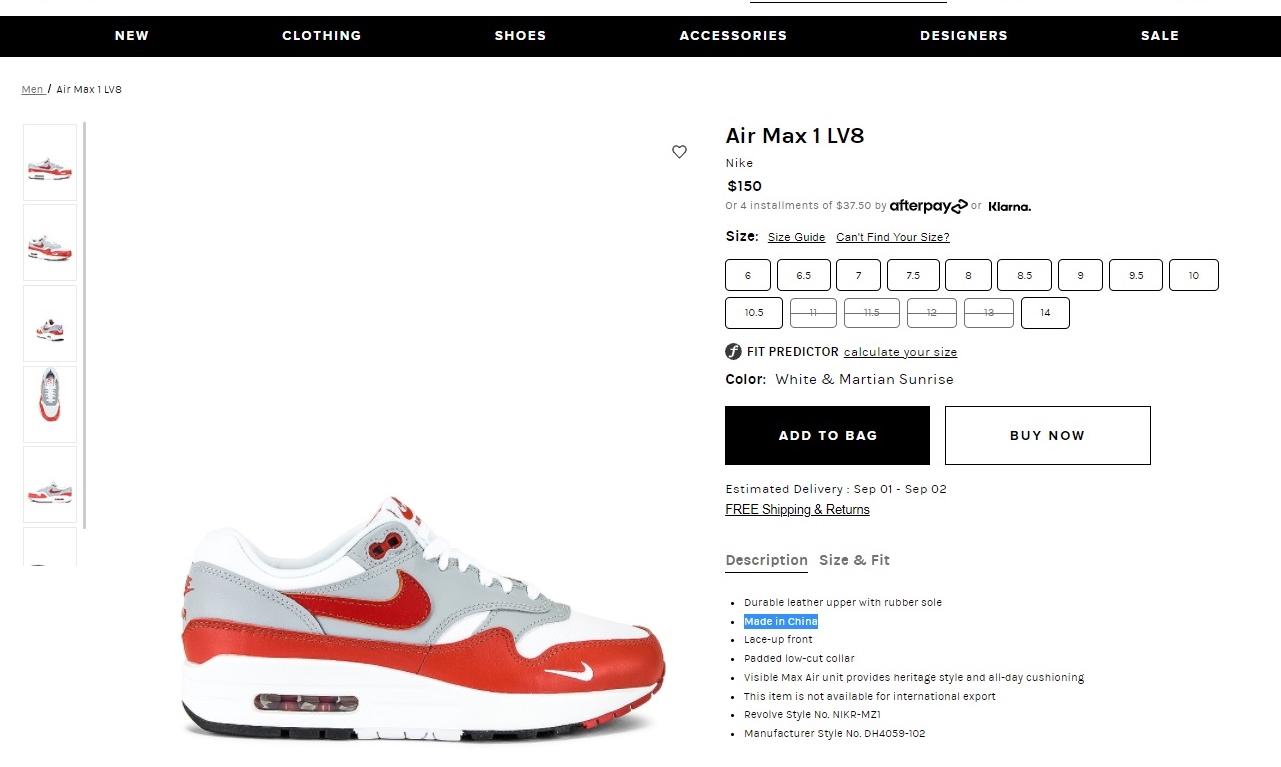

Nike, “Made in China”, retail price =$150

Third, US retailers source from Vietnam primarily for volume items targeting the mass market. Industry sources show that from Aug 2020 to Aug 2021, sneakers/trainer shoes “Made in Vietnam” on average were priced 30%+ cheaper than those “Made in China” in the US retail market.

Meanwhile, Vietnam still lags far behind China in terms of the variety of products it makes. For example, industry sources show that from Aug 2020 to Aug 2021, US retailers imported around 110K different types of footwear (at the SKU level) from China, but only 13K from Vietnam.

Overall, Vietnam’s COVID lockdown will primarily affect medium to lower-priced volume products carried by US footwear retailers. However, the lockdown’s impacts on retailers’ sourcing portfolio and product availability in the market could be modest. In other words, US consumers may still find many footwear products to choose from in the store but with a higher price tag.Notably, from June 2020 to July 2021, the US retail price for footwear went up by over 7.4% already.

Discussion question: How has the container shipping crisis affected the fashion apparel industry? While shopping for clothing, do you observe any market trends related to the shipping crisis (e.g., retail price and product availability)? Why or why not do you think the container shipping crisis will go away anytime soon?

The cosmetics and beauty (C&B) is a $50 billion market in the United States. Like many other retail businesses, U.S. C&B companies face significant challenges during the pandemic. This study aims to explore how U.S.-based C&B companies have adjusted their merchandising and marketing strategies to survive the pandemic. By leveraging StyleSage, a big data tool for the fashion industry, we checked millions of C&B items (at the Stock Keeping Unit, SKU level) sold in the U.S. retail market during the pandemic (from March 1, 2020, to May 31, 2021). The results show that:

First, despite the tremendous challenges facing C&B companies during the pandemic, the U.S. C&B retail market is not at all depressing. Cosmetic and beauty retailers prioritized three categories during COVID: fragrance (up 226.3%), haircare (up 150.9%), and skincare (up 165.6%), all see a significant increase in the number of products newly launched to the market than before the pandemic.

Second, U.S. C&B retailers adjusted their product assortment during the pandemic. While most C&B products still target women, the number of unisex products newly launched to the market during COVID-19 saw impressive high growth in some product categories, such as skincare. There is also a notable increase in products catered explicitly towards male consumers during the pandemic.

Third, during COVID-19, the average selling price goes up for most C&B product categories sold in the U.S. retail market. Except for bath & body and haircare, C&B retailers are selling more popular items in higher price-zones. C&B retailers also created new price zones with unique product combinations to fulfill consumers’ shifting demands during the pandemic.

Further U.S. C&B retailers adjusted their discount strategies during the pandemic. Notably, markup products were more commonly sold at a discounted price during the pandemic, although the depth of their markdowns was lower.

The study’s findings provide new insights into the C&B-specific sectoral impact of the pandemic, especially firm-level business mitigation strategies. The findings also call for more attention to the shifting product offers in the C&B market and the emerging product niches, such as unisex C&B items, that may continue to enjoy fast growth in the post-COVID world.

By Valerie Light (2021 UD Summer Scholar, Honors Public Relations Communication major and Fashion management minor); Faculty advisor: Dr. Sheng Lu

The textile and apparel industry plays a significant role in Myanmar’s economy, particularly the export sector. Data from UNComtrade shows that textile and apparel accounted for nearly 69% of Myanmar’s total exports of manufactured goods in 2020, a substantial increase from only 27% in 2011. Data from the International Labor Organization (ILO) also indicates that the textile and industry (ISIC 17 & 18) employed more than 1.1 million workers in Myanmar in 2019, up from 0.69 million in 2015. Most garment workers in Myanmar are women today (around 87%).

Since the United States lifted the import ban on Myanmar and the EU reinstated the Everything But Arms (EBA) trade preferences in 2013, Myanmar was one of the most popular emerging apparel sourcing bases among fashion companies. From 2020 to July 2021, some of the top fashion brands that carry “Made in Myanmar” apparel items include United Colors of Benetton, Next, Only, H&M, Guess, and Jack & Jones.

Thanks to foreign investment (note: nearly half of Myanmar’s garment factories are foreign-owned), Myanmar specializes in making relatively higher-quality functional/technical clothing (i.e., outwear like jackets and coats. Here is an example). This is different from many other apparel-exporting countries like Bangladesh, Vietnam, and Cambodia, mostly exporting low-cost tops and bottoms.

However, the latest trade data shows that Myanmar’s military coup that broke out in early 2021 had hurt the country’s apparel exports significantly. According to the US International Trade Commission (USITC), even though the total US apparel imports enjoyed a robust recovery in the first half of 2021 (up nearly 27%), the value of US apparel (HTS chapters 61 and 62) imports from Myanmar dropped by 0.4%. Almost ALL Myanmar’s top apparel exports to the US suffered a substantial decline or much slower growth in 2021 than the trend BEFORE the military coup (see the Table above). As US fashion companies switch sourcing orders from Myanmar to other suppliers, Myanmar’s market shares fell from 0.5% in 2020 to only 0.3% in the first half of 2021.

Highly consistent with the trade data, according to the 2021 Fashion Industry Benchmarking Study, many surveyed US fashion companies expressed concerns about the military coup in Myanmar and the rising labor and social compliance risks when sourcing from the country. Some respondents explicitly say they are leaving because of the current situation. “(We) have terminated sourcing from Myanmar due to instability.” says one respondent. Another adds, “We had orders in Myanmar that have already been moved to Cambodia. We are unlikely to place orders until the current situation is resolved.”

In another recent study, we find that apparel sourcing is not merely about “competing on price.” Instead, fashion companies give substantial weight to the factors of “political stability” and “financial stability” in their sourcing decisions today. In other words, the reputation risks matter for sourcing.

Unfortunately, the situation could get worse. The international community, including the US and the EU, is considering new sanctions against Myanmar, including suspending Myanmmar’s trade-preference program eligibility.

Designated as a “least developed country” (LDC) by the World Trade Organization, Myanmar’s apparel exports enjoy duty-free market access in the EU, Japan, and South Korea. These countries also, in general, offer very liberal “single transformation” (or commonly known as cut and sew) rules of origin for qualifying apparel made in Myanmar. This explains why Myanmar’s apparel exports mostly go to the EU (56%), Japan, and South Korea (around 30%).

The United States is another important export market for Myanmar, accounting for 7% of the country’s total apparel exports in 2020. As a beneficiary of the US Generalized System of Preferences (GSP) program, Myanmar’s luggage exports enjoy duty-free benefits in the US market. However, the US GSP program excludes textile and apparel products, meaning Myanmar’s apparel exports to the US still are subject to the regular Most-Favored-Nation (MFN) tariff rate at around 14.3% on average in 2020.

Further, given Myanmar’s highly concentrated apparel export markets and the pandemic, it will be challenging for Myanmar’s garment producers to find alternative apparel export markets in a relatively short period. For example, although China is recognized as one of the world’s largest and fastest-growing emerging import markets, only 1.4% of Myanmar’s apparel exports went to China in 2020.

According to the World Trade Statistical Review 2021 report released by the World Trade Organization (WTO), the textiles and apparel trade patterns in 2020 include both continuities and new trends affected by the pandemic and companies’ evolving production and sourcing strategies in response to the shifting business environment.

Pattern #1: COVID-19 significantly affected the world textile and apparel trade volumes, resulting in substantial growth of textile exports and a declined demand for apparel.

Driven by increased personal protective equipment (PPE) production, global textile exports grew by 16.1% in 2020, reaching $353bn. In comparison, affected by lockdown measures, worsened economy, and consumers’ tighter budget for discretionary spending, global apparel export decreased by nearly 9% in 2020, totaling $448bn, the worst performance in decades. The apparel sector is not alone. The world merchandise trade in 2020 also suffered an unprecedented 8% drop from a year ago, with COVID-19 to blame.

Notably, as economic activities returned in the second half of 2020, the world clothing export quickly rebounded to around 95% of the pre-covid level by the end of 2020. That being said, the unexpected resurgence of COVID cases in summer 2021, especially the delta variant, caused new market uncertainties. Overall, the world textile and apparel trade recovery process from COVID-19 will differ from our experiences during the 2008 global financial crisis.

Pattern #2: COVID-19 did NOT shift the competitive landscape of the world textile exports; Meanwhile, textile exports from China and Vietnam gained new momentum during the pandemic.

China, the European Union (EU), and India remained the world’s three largest textile exporters in 2020. Together, these top three accounted for 65.8% of the world’s textile exports in 2020, similar to 66.9% before the pandemic (2018-2019).

Notably, China and Vietnam enjoyed a substantial increase in their textile exports in 2020, up 28.9% and 10.7% from a year ago, respectively. The complete textile and apparel supply chain and considerable production capability allow these two countries to switch clothing production to PPE manufacturing quickly. In particular, Vietnamexceeded South Korea and ranked the world’s sixth-largest textile exporter in 2020 ($10 bn of exports), the first time in history.

The United States dropped one place and ranked the world’s fifth-largest textile exporter in 2020 (was 4th from 2015 to 2019), accounting for 3.2% of the shares (was 4.4% in 2019). Production disruptions at the beginning of the pandemic and the shift toward PPE production for domestic consumption were the two primary contributing factors behind the decline in U.S. textile exports. Due to the regional trade patterns, around 67% of U.S. textile exports went to the Western Hemisphere in 2020, including 46% for members of the U.S.-Mexico-Canada Trade Agreement (USMCA) and another 17.2% for members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR).

Pattern #3: Fashion companies’ efforts to diversify apparel sourcing from China somehow slowed during the pandemic.

China, the European Union, Vietnam, and Bangladesh unshakably remained the world’s four largest apparel exporters in 2020. Altogether, these top four accounted for 72.2% of the world market shares in 2020, higher than 71.4% in 2019.

Notably, while China steadily accounted for declining shares in the world’s total apparel exports since 2015, its market shares rebounded to 31.6% in 2020 from 30.7% in 2019. We can observe a similar pattern in Canada (up from 36.2% to 41.2%) and the EU (31.2% to 31.3%), two of the world’s leading apparel import markets. Even in the U.S. market, where Chinese goods face adverse impacts of the tariff war, the market shares of “Made in China” only marginally decreased from 30.8% in 2019 to 29.8% in 2020, compared with a more significant drop before the pandemic (i.e., fell from 34.4% 2018 to 30.8% in 2019).

Several factors could explain the resilience of China’s apparel exports: 1) fashion brands and retailers’ particular sourcing criteria match China’s competitiveness during the pandemic (e.g., flexibility, agility, and total landed sourcing cost). 2) China has one of the world’s most complete textile and apparel supply chains, allowing garment factories to access textile raw material and accessories locally. 3) Compared with many other apparel exporting countries, China suffered a shorter COVID lockdown period and resumed apparel production earlier and more quickly. Most Chinese textile and apparel factories started to reopen in April 2020, and they resumed an overall 90%-95% operational capacity rate by July 2020.

Nonetheless, fashion companies are NOT reversing their long-term strategies to reduce “China exposure” for apparel sourcing. On the contrary, non-economic factors, particularly the concerns about forced labor in China’s Xinjiang region, push most western fashion brands and retailers to develop apparel sourcing capacities beyond China. Meanwhile, no single country has yet and will likely become the “Next China” because of capacity limits. Instead, from 2015 to 2020, China’s lost market shares in the world apparel exports (around 7.8 percentage points) were picked up jointly by its competitors in Asia, including ASEAN members (up 4.4 percentage points), Bangladesh (up 1.3 percentage points), and Pakistan (up 0.3 percentage point). Such a trend is most likely to continue in the post-COVID world.

Pattern #4: Developed economies led textile PPE imports during the pandemic, whereas the developing countries imported fewer textiles as their apparel exports dropped.

On the one hand, the value of textile imports by developed economies, including EU members, the United States, Japan, and Canada, surged by more than 30 percent in 2020, driven mainly by their demand for PPE. The result also reveals the significant contribution of international trade in supporting the supply and distribution of textile PPE globally. On the other hand, the developing countries engaged in apparel production and export drove the import demand for textile raw materials like yarns and fabrics. However, most of these developing countries’ textile imports fell in 2020, corresponding to their decreased apparel exports during the pandemic.

Pattern #5: Despite COVID-19, the world apparel import market continues to diversify. The import demand increasingly comes from emerging economies with a booming middle class.

Affected by consumers’ purchasing power (often measured by GDP per capita) and the size of the population, the European Union, the United States, and Japan remained the world’s three largest apparel importers in 2020, a stable pattern that has lasted for decades. While these top three still absorbed 56.2% of the world’s apparel imports in 2020, it was a new record low in the past ten years (was 58.1% in 2019 and 61.5% in 2018), and much lower than 84% back in 2005.

Behind the numbers, it is not the case that consumers in the EU, the United States, and Japan necessarily purchase less clothing over the years. Instead, several emerging economies have become fast-growing apparel-consuming markets with robust import demand. For example, despite COVID-19, China’s apparel imports totaled $9.5bn in 2020, up 6.5% from 2019. From 2010 to 2020, China’s apparel imports enjoyed a nearly 15% annual growth, compared with only 0.56% of the traditional top three. Around 30% of China’s apparel imports today are luxury items made in the EU.

With consumers’ increasing awareness of sustainability and building a circular economy, more and more fashion retailers carry clothing made from recycled materials. This study aims to explore U.S. fashion retailers’ detailed merchandising and pricing strategies for clothing made from recycled material to provide more business insights into this fast-growing market.

By leveragingStyleSage, a big data tool for the fashion industry, we checked millions of clothing items (at the Stock Keeping Unit, SKU level) made from recycled materials available in the U.S. retail market from June 2018 to June 2021. The results show that:

First, top U.S. sellers of clothing made with recycled materials include BOTH sustainability-based brands and fast-fashion brands.

Second, the most utilized recycled textile fibers include Polyester, Nylon, and Cotton.

Third, U.S. retailers adopt unique product assortment strategies for clothing made from recycled material. Recycled clothing, in general, carry more “Shorts” and “outerwear, coats, and jackets,” and fewer “Sleepwear” and “dresses.”

Fourth, U.S. retailers adopt unique color strategies for clothing made from recycled materials, using “black” more often but using “Neutral color” much less.

Fifth, U.S. retailers typically price clothing using recycled materials at least 50% lower than regular new clothing. The price difference for “Bridal”, “Suits”, “Causal jackets and blazers” and “Outerwear, coats, and jackets” was particularly notable.

The study’s findings confirm that clothing made from recycled materials is a critical market to watch with growing business opportunities. The findings also suggest that U.S. fashion retailers adopt unique merchandising and pricing strategies for recycled clothing, affected by the product supply and consumers’ preferences. Additionally, the study’s findings call for more exploration of leveraging recycled clothing to achieve sustainability and lower sourcing costs.

By Ally Botwinick (2021 UD Summer Scholar, Fashion merchandising and Management Major); Faculty advisor: Dr. Sheng Lu