This study was based on a statistical analysis of 3,307 randomly selected clothing items made from recycled textile materials for sale in the U.S. retail market between January 2019 and August 2022 (see the sample picture above). The results show that:

First, U.S. retailers sourced clothing made from recycled textile materials from diverse countries.

Specifically, the sampled clothing items came from as many as 36 countries, including developed and developing economies in Asia, America, the EU, and Africa.

However, reflecting the unique supply chain composition of clothing made from recycled textile materials, U.S. retailers’ sourcing patterns for such products turned out to be quite different from regular new clothing. For example, whereas the vast majority (i.e., over 90%) of U.S. regular new clothing came from developing countries as of 2022 (UNComtrade, 2022), as many as 43% of the sampled clothing items made from recycled textile materials (n=1,408) were sourced from developed countries. Likewise, U.S. retailers seemed to be less dependent on Asia when sourcing clothing made from recycled materials (41.9%, n=1,387) and instead used near-sourcing from America (30.1%, n=994) more often, particularly domestic sourcing from the United States (14.8%, n=490).

Second, U.S. retailers appeared to set differentiated assortments for products imported from developed and developing countries when sourcing clothing made from recycled textile materials.

Among the sampled clothing items made from recycled textile materials, those imported from developing countries, on average, included a broader assortment than developed economies. Likewise, imports from developing countries also concentrated on products relatively more complex to make as opposed to developed countries. Developing countries’ more extensive clothing production capability, including the available production facilities and skilled labor force, than developed economies could have contributed to the pattern.

On the other hand, likely caused by developed countries’ overall higher production costs, the average retail price of sampled clothing items sourced from developed countries was notably higher than those from developing ones. However, NO clear evidence shows that U.S. retailers used developed countries primarily as the sourcing bases for luxury or premium items and used developing countries only for items targeting the mass or value market.

Third, an exporting country’s geographic location was another statistically significant factor affecting U.S. retailers’ sourcing pattern for clothing made from recycled textile materials. Specifically,

Imports from Asia had the most diverse product assortment (e.g., sizing options) and focused on complex product categories (e.g., outwear) that targeted mass and value markets.

Imports from America (North, South, and Central America) concentrated on simple product categories (e.g., T-shirts and hosiery) with moderate assortment diversity and mainly targeted the mass and value market.

Imports from the EU were mainly higher-priced luxury items in medium-sophisticated or sophisticated product categories with diverse assortment.

Imports from Africa concentrated on relatively higher-priced premium or luxury items in simple product categories (i.e., swim shorts) with a limited assortment diversity.

The study’s findings demystified the country of origin of clothing made from recycled textile materials hidden behind macro trade statistics. The findings also created critical new knowledge that contributed to our understanding of the supply chain of clothing made from recycled textile materials and U.S. retailers’ distinct sourcing patterns and affecting factors for such products. The findings have several other important implications:

First, the study’s findings revealed the broad supply base for clothing made from recycled textile materials and suggested promising sourcing opportunities for such products. Whereas existing studies illustrated consumers’ increasing interest in shopping for clothing made from recycled textile materials, the study’s results indicated that the “enthusiasm” also applied to the supply side, with many countries already engaged in making and exporting such products. Meanwhile, the results showed that U.S. retailers sourced clothing made from recycled textile materials in different product categories with a broad price range targeting various market segments to meet consumers’ varying demands. Moreover, as textile recycling techniques continue to advance, potentially enriching the product offer of clothing made from recycled textile materials, U.S. retailers’ sourcing needs and supply base for such products could expand further.

Second, the study’s findings suggest that sourcing clothing made from recycled textile materials may help U.S. retailers achieve business benefits beyond the positive environmental impacts. For example, given the unique supply chain composition and production requirements, China appeared to play a less dominant role as a supplier of clothing made from recycled textile materials for U.S. retailers. Instead, a substantial portion of such products was “Made in the USA” or came from emerging sourcing destinations in America (e.g., El Salvador, Nicaragua) and Africa (e.g., Tunisia and Morocco). In other words, sourcing clothing made from recycled textile materials could help U.S. retailers with several goals they have been trying to achieve, such as reducing dependence on sourcing from China, expanding near sourcing, and diversifying their sourcing base.

Additionally, the study’s findings call for strengthening U.S. domestic apparel manufacturing capability to better serve retailers’ sourcing needs for clothing made from recycled textile materials. On the one hand, the results demonstrated U.S. retailers’ strong interest in sourcing clothing made from recycled textile materials that were “Made in the USA.” Also, the United States may enjoy certain competitive advantages in making such products, ranging from the abundant supply of recycled textile waste and the affordability of expensive modern recycling machinery to the advanced research and product development capability. On the other hand, the results showed that U.S. retailers primarily sourced simple product categories (e.g., T-shirts and hosiery), targeting the value and mass markets from the U.S. and other American countries. This pattern somewhat mirrored the production and sourcing pattern for regular new clothing, for which apparel “Made in the USA” also lacked product variety and focused on basic fashion items compared with Asian and EU suppliers. Thus, strengthening the U.S. domestic apparel production capacity, especially for those complex product categories (e.g., outwear and suits), could encourage more sourcing of “Made in the USA” apparel using recycled textile materials and support production and job creation in the U.S. apparel manufacturing sector.

In December 2022, Just-Style consulted a panel of industry experts and scholars in its Outlook 2023–what’s next for apparel sourcing briefing. Below is my contribution to the report. All comments and suggestions are more than welcome!

2023 is likely another year full of challenges and opportunities for the global apparel industry.

First, the apparel industry may face a slowed world economy and weakened consumer demand in 2023. Apparel is a buyer-driven industry, meaning the sector’s volume of trade and production is highly sensitive to the macroeconomic environment. Amid hiking inflation, high energy costs, and retrenchment of global supply chains, leading international economic agencies, from the World Bank to the International Monetary Fund (IMF), unanimously predict a slowing economy worldwide in the new year. Likewise, the World Trade Organization (WTO) forecasts that the world merchandise trade will grow at around 1% in 2023, much lower than 3.5% in 2022. As estimated, the world apparel trade may marginally increase between 0.8% and 1.5% in the new year, the lowest since 2021. On the other hand, the falling demand may somewhat help reduce the rising sourcing cost pressure facing fashion companies in the new year.

Second, fashion brands and retailers will likely continue leveraging sourcing diversification and strengthening relationships with key vendors in response to the turbulent market environment. According to the 2022 fashion industry benchmarking study I conducted in collaboration with the US Fashion Industry Association (USFIA), nearly 40 percent of surveyed US fashion companies plan to “source from more countries and work with more suppliers” through 2024. Notably, “improving flexibility and reducing resourcing risks,” “reducing sourcing from China,” and “exploring near-sourcing opportunities” were among the top driving forces of fashion companies’ sourcing diversification strategies. Meanwhile, it is not common to see fashion companies optimize their supplier base and work with “fewer vendors.” For example, fashion companies increasingly prefer working with the so-called “super-vendors,” i.e., those suppliers with multiple-country manufacturing capability or can make textiles and apparel vertically, to achieve sourcing flexibility and agility. Hopefully, we could also see a more balanced supplier-importer relationship in the new year as more fashion companies recognize the value of “putting suppliers at the core.”

Third, improving sourcing sustainability and sourcing apparel products using sustainable textile materials will gain momentum in the new year. On the one hand, with growing expectations from stakeholders and pushed by new regulations, fashion companies will make additional efforts to develop a more sustainable, socially responsible, and transparent apparel supply chain. For example, more and more fashion brands and retailers have voluntarily begun releasing their supplier information to the public, such as factory names, locations, production functions, and compliance records. Also, new traceability technologies and closer collaboration with vendors enable fashion companies to understand their raw material suppliers much better than in the past. Notably, the rich supplier data will be new opportunities for fashion companies to optimize their existing supply chains and improve operational efficiency.

On the other hand, with consumers’ increasing interest in fashion sustainability and reducing the environmental impact of textile waste, fashion companies increasingly carry clothing made from recycled textile materials. My latest studies show that sourcing clothing made from recycled textile materials may help fashion companies achieve business benefits beyond the positive environmental impacts. For example, given the unique supply chain composition and production requirements, China appeared to play a less dominant role as a supplier of clothing made from recycled textile materials. Instead, in the US retail market, a substantial portion of such products was “Made in the USA” or came from emerging sourcing destinations in America (e.g., El Salvador, Nicaragua) and Africa (e.g., Tunisia and Morocco). In other words, sourcing clothing made from recycled textile materials could help fashion companies with several goals they have been trying to achieve, such as reducing dependence on sourcing from China, expanding near sourcing, and diversifying their sourcing base. Related, we are likely to see more public dialogue regarding how trade policy tools, such as preferential tariffs, may support fashion companies’ efforts to source more clothing using recycled or other eco-friendly textile materials.

Additionally, the debates on fashion companies’ China sourcing strategy and how to meaningfully expand near-sourcing could intensify in 2023. Regarding China, fashion companies’ top concerns and related public policy debates next year may include:

What to do with Section 301 tariff actions against imports from China, including the tariff exclusion process?

How to reduce “China exposure” further in sourcing, especially regarding textile raw materials?

How should fashion companies respond and mitigate the business impacts of China’s shifting COVID policy and a new wave of COVID surge?

What contingency plan will be should the geopolitical tensions in the Asia-Pacific region directly affect shipping from the region?

Meanwhile, driven by various economic and non-economic factors, fashion companies will likely further explore ways to “bring the supply chain closer to home” in 2023. However, the near-shoring discussion will become ever more technical and detailed. For example, to expand near-shoring from the Western Hemisphere, more attention will be given to the impact of existing free trade agreements and their specific mechanisms (e.g., short supply in CAFTA-DR) on fashion companies’ sourcing practices. Even though we may not see many conventional free trade agreements newly launched, 2023 will be another busy year for textile and apparel trade policy deliberation, especially behind the scene and on exciting new topics.

By Sheng Lu

Discussion question: As we approach the middle of the year, why do you agree or disagree with any predictions in the outlook? Please share your thoughts.

#1. Are classic trade theories (e.g., comparative advantage) still relevant or outdated in the 21st century? Why? Please share your thoughts based on the video and the figures.

#2. Based on the video and the figures above, is the US textile manufacturing sector a winner or loser of globalization and international trade? Why?

#3. Take the following poll (anonymous) and share your reflections.

#4. Should the government’s trade policy consider non-economic factors such as national security and geopolitics? What should be the line between promoting “fair trade” and “trade protectionism”? What’s your view?

#5. Is there anything else you find interesting/intriguing/thought-provoking in the video? Why?

On September 2, 2022, the Office of the US Trade Representative (USTR) announced it would continue the billions of dollars of Section 301 punitive tariffs against Chinese products. USTR said it made the decision based on requests from domestic businesses benefiting from the tariff action. As a legal requirement, USTR will launch a full review of Section 301 tariff action in the coming months.

In her remarks at the Carnegie Endowment for International Peace on Sep 7, 2022, US Trade Representative Katharine Tai further said that the Section 301 punitive tariffs on Chinese imports “will not come down until Beijing adopts more market-oriented trade and economic principles.” In other words, the US-China tariff war, which broke out four years ago, is not ending anytime soon.

A Brief History of the US Section 301 tariff action against China

The US-China tariff war broke out as both unexpected and not too surprising. For decades, the US government had been criticizing China for its unfair trade practices, such as providing controversial subsidies to state-owned enterprises (SMEs), insufficient protection of intellectual property rights, and forcing foreign companies to transfer critical technologies to their Chinese competitors. The US side had also tried various ways to address the problems, from holding bilateral trade negotiations with China and imposing import restrictions on specific Chinese goods to suing China at the World Trade Organization (WTO). However, despite these efforts, most US concerns about China’s “unfair” trade practices remain unsolved.

When former US President Donald Trump took office, he was particularly upset about the massive and growing US trade deficits with China, which hit a record high of $383 billion in 2017. In alignment with the mercantilism view on trade, President Trump believed that the vast trade deficit with China hurt the US economy and undermined his political base, particularly with the working class.

On August 14, 2017, President Trump directed the Office of the US Trade Representative (USTR) to probe into China’s trade practices and see if they warranted retaliatory actions under the US trade law. While the investigation was ongoing, the Trump administration also held several trade negotiations with China, pushing the Chinese side to purchase more US goods and reduce the bilateral trade imbalances. However, the talks resulted in little progress.

President Trump lost his patience with China in the summer of 2018. In the following months, citing the USTR Section 301 investigation findings, the Trump administration announced imposing a series of punitive tariffs on nearly half of US imports from China, or approximately $250 billion in total. As a result, for more than 1,000 types of products, US companies importing them from China would have to pay the regular import duties plus a 10%-25% additional import tax. However, the Trump administration’s trade team purposefully excluded consumer products such as clothing and shoes from the tariff actions. The last thing President Trump wanted was US consumers, especially his political base, complaining about the rising price tag when shopping for necessities. The timing was also a sensitive factor—the 2018 congressional mid-term election was only a few months away.

President Trump hoped his unprecedented large-scale punitive tariffs would change China’s behaviors on trade. It partially worked. As the trade frictions threatened economic growth, the Chinese government returned to the negotiation table. Specifically, the US side wanted China to purchase more US goods, reduce the bilateral trade imbalances and alter its “unfair” trade practices. In contrast, the Chinese asked the US to hold the Section 301 tariff action immediately.

However, the trade talks didn’t progress as fast as Trump had hoped. Even worse, having to please domestic forces that demanded a more assertive stance toward the US, the Chinese government decided to impose retaliatory tariffs against approximately $250 billion US products. President Trump felt he had to do something in response to China’s new action. In August 2019, he suddenly announced imposing Section 301 tariffs on a new batch of Chinese products, totaling nearly $300 billion. As almost everything from China was targeted, apparel products were no longer immune to the tariff war.With the new tariff announcement coming at short notice, US fashion brands and retailers were unprepared for the abrupt escalation since they typically placed their sourcing orders 3-6 months before the selling season.

Nevertheless, Trump’s new Section 301 actions somehow accelerated the trade negotiation. The two sides finally reached a so-called“phase one” trade agreementin about two months. As part of the deal, China agreed to increase its purchase of US goods and services by at least $200 billion over two years, or almost double the 2017 baseline levels. Also, China promised to address US concerns about intellectual property rights protection, illegal subsidies, and forced technology transfers. Meanwhile, the US side somewhat agreed to trim the Section 301 tariff action but rejected removing them. For example, the punitive Section 301 tariffs on apparel products were cut from 15% to 7.5% since implementing the “phase one” trade deal.

Trump lost the 2020 presidential election, and Joe Biden was sworn in as the new US president on January 20, 2021. However, the Section 301 tariff actions and the US-China “phase one” trade deal stayed in force.

Debate on the impact of the US-China tariff war

Like many other trade policies, the US Section 301 tariff actions against China raised heated debate among stakeholders with competing interests. This was the case even among different US textile and apparel industry segments.

On the one hand, US fashion brands and retailers strongly oppose the punitive tariffs against Chinese products for several reasons:

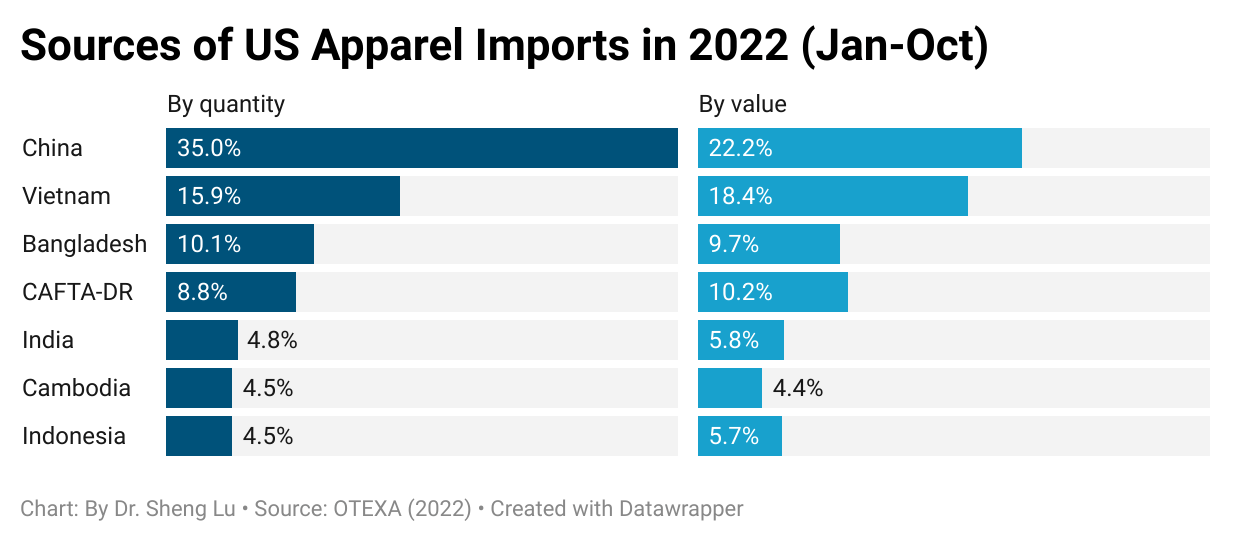

First, despite the Section 301 tariff action, China remained a critical apparel sourcing base for many US fashion companies with no practical alternative. Trade statistics show that four years into the tariff war, China still accounted for nearly 40 percent of US apparel imports in quantity and about one-third in value as of 2021. According to the latest data, in the first ten months of 2022, China remained the top apparel supplier, accounting for 35% of US apparel imports in quantity and 22.2% in value. Studies also consistently find that US fashion companies rely on China to fulfill orders requiring a small minimum order quantity, flexibility, and a great variety of product assortment.

Second, having to import from China, fashion companies argued that the Section 301 punitive tariffs increased their sourcing costs and cut profit margins. For example, for a clothing item with an original wholesale price of around $7, imposing a 7.5% Section 301 punitive tariff would increase the sourcing cost by about 5.8%. Should fashion companies not pass the cost increase to consumers, their retail gross margin would be cut by 1.5 percentage points. Notably, according to the US Fashion Industry Association’s 2021 benchmarking survey, nearly 90 percent of respondents explicitly say the tariff war directly increased their company’s sourcing costs. Another 74 percent say the tariff war hurt their company’s financials.

Third, as companies began to move their sourcing orders from China to other Asian countries like Vietnam, Bangladesh, and Cambodia to avoid paying punitive tariffs, these countries’ production costs all went up because of the limited production capacity. In other words, sourcing from everywhere became more expensive because of the Section 301 action against China.

Further, it is important to recognize that fashion companies supported the US government’s efforts to address China’s “unfair” trade practices, such as subsidies, intellectual property rights violations, and forced technology transfers. Many US fashion companies were the victims of such practices. However, fashion companies did not think the punitive tariff was the right tool to address these problems effectively. Instead, fashion brands and retailers were concerned that the tariff war unnecessarily created an uncertain and volatile market environment harmful to their business operations.

“While NCTO members support the inclusion of finished products in Section 301, we are seriously concerned that…adding tariffs on imports of manufacturing inputs that are not made in the US such as certain chemicals, dyes, machinery, and rayon staple fiber in effect raises the cost for American companies and makes them less competitive with China.”

Mitigate the impact of the tariff war: Fashion Companies’ Strategies

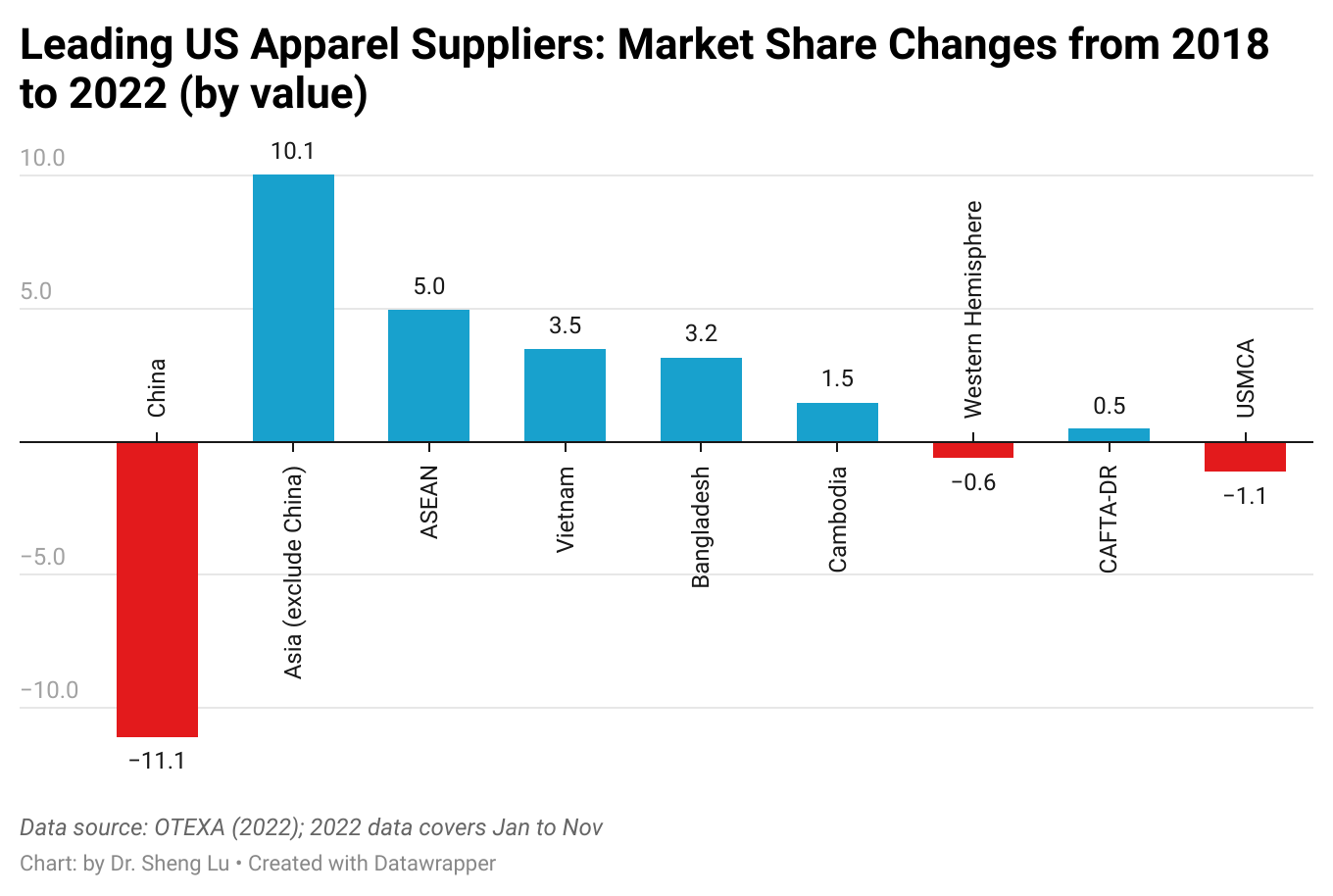

The first approach was to switch to China’s alternatives. Trade statistics suggest that Asian countries such as Vietnam and Bangladesh picked up most of China’s lost market shares in the US apparel import market. For example, in 2022 (Jan-Nov), Asian countries excluding China accounted for 51.2% of US apparel imports, a substantial increase from 41.2% in 2018 before the tariff war. In comparison, about 16.4% of U.S. apparel imports came from the Western Hemisphere in 2021 (Jan-Nov), lower than 17.0% in 2018. In other words, no evidence shows that Section 301 tariffs have expanded U.S. apparel sourcing from the Western Hemisphere.

The second approach was to adjust what to source from China by leveraging the country’s production capacity and flexibility. For example, market data from industry sources showed that since the Section 301 tariff action, US fashion companies had imported more “Made in China” apparel in the luxury and premium segments and less for the value and mass markets. Such a practice made sense as consumers shopping for premium-priced apparel items typically were less price-sensitive, allowing fashion companies to raise the selling price more easily to mitigate the increasing sourcing costs. Studies also found that US companies sourced fewer lower value-added basic fashion items (such as tops and underwear), but more sophisticated and higher value-added apparel categories (such as dresses and outerwear) from China since the tariff war.

China is no longer treated as a sourcing base for low-end cheap product

More apparel sourced from China target the premium and luxuary market segments

Related, US fashion companies such as Columbia Sportswear leveraged the so-called “tariff engineering” in response to the tariff war. Tariff engineering refers to designing clothing to be classified at a lower tariff rate. For example, “women’s or girls’ blouses, shirts, and shirt-blouses of man-made fibers” imported from China can tax as high as 26.9%. However, the same blouse added a pocket or two below the waist would instead be classified as a different product and subject to only a 16.0% tariff rate. Nevertheless, using tariff engineering requires substantial financial and human resources, which often were beyond the affordability of small and medium-sized fashion companies.

Third, recognizing the negative impacts of Section 301 on US businesses and consumers, the Office of the US Trade Representative (USTR) created a so-called “Section 301 exclusion process.” Under this mechanism, companies could request that a particular product be excluded from the Section 301 tariffs, subject to specific criteria determined at the discretion of USTR. The petition for the product exclusion required substantial paperwork, however. Even companies with an in-house legal team typically hire a DC-based law firm experienced with international trade litigation to assist the petition, given the professional knowledge and a strong government relation needed. Also of concern to fashion companies was the low success rate of the petition. The record showed that nearly 90 percent of petitions were denied for failure to demonstrate “severe economic harm.” Eventually, since the launch of the exclusion process, fewer than 1% of apparel items subject to the Section 301 punitive tariff were exempted. Understandably, the extra financial burden and the long shot discouraged fashion companies, especially small and medium-sized, from taking advantage of the exclusion process.

In conclusion, with USTR’s latest announcement, the debate on Section 301 and the outlook of China as a textile and apparel sourcing base will continue. Notably, while economic factors matter, we shall not ignore the impact of non-economic factors on the fate of the Section 301 tariff action against China. For example, with the implementation of the Uyghur Forced Labor Prevention Act (UFLPA), only about 10% of US cotton apparel imports came from China in the first ten months of 2022 (latest data available), the lowest in a decade. As the overall US-China bilateral trade relationship significantly deteriorated in recent years and the friction between the two countries expanded into highly politically sensitive areas, the Biden administration could “willfully” choose to keep the Section 301 tariff as negotiation leverage. Domestically, President Biden also didn’t want to look “weak” on his China policy, given the bipartisan support for taking on China’s rise.

This article provided a comprehensive review of the world textiles and clothing trade patterns in 2021 based on the newly released data from the World Trade Statistical Review 2022 and the United Nations (UNComtrade). Affected by the ongoing pandemic and companies’ evolving production and sourcing strategies in response to the shifting business environment, the world textiles and clothing trade patterns in 2021 included both continuities and new trends. Specifically:

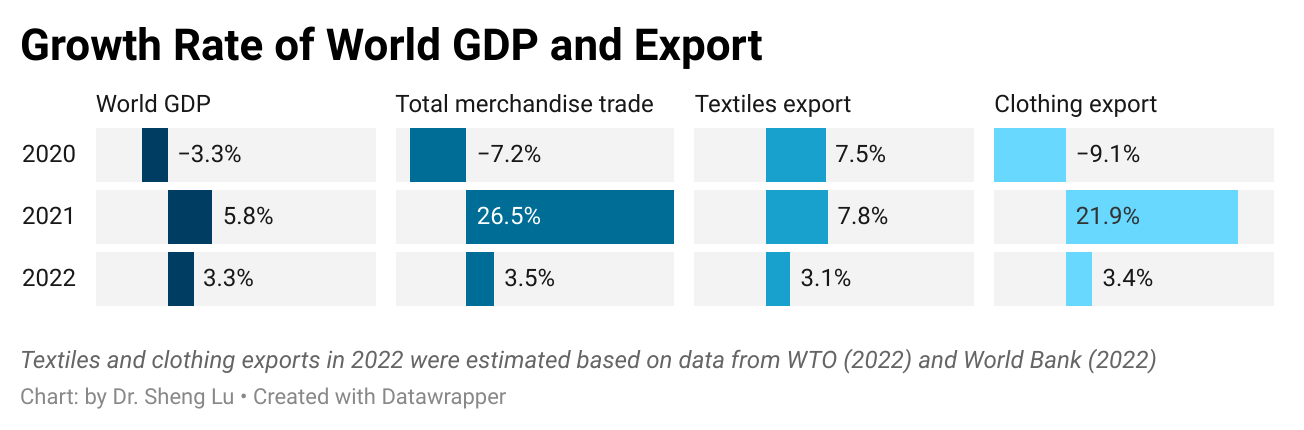

Pattern #1: As the world economy recovered from COVID, the world clothing export boomed in 2021, while the world textile exports grew much slower due to a high trade volume the year before. Specifically, thanks to consumers’ strong demand, world clothing exports in 2021 fully bounced back to the pre-COVID level and exceeded $548.8bn, a substantial increase of 21.9% from 2020. The apparel sector is not alone. With economic activities mostly resumed, the world merchandise trade in 2021 also jumped 26.5% from a year ago, the fastest growth in decades.

In comparison, the value of world textiles exports grew slower at 7.8% in 2021 (i.e., reached $354.2bn), lagging behind most sectors. However, such a pattern was understandable as the textile trade maintained a high level in 2020, driven by high demand for personal protective equipment (PPE) during the pandemic.

Nevertheless, the world textiles and clothing trade could face strong headwinds down the road due to a slowing world economy and consumers’ weakened demand. Notably, amid hiking inflation, high energy costs, and retrenchment of global supply chains, leading international economic agencies, from the World Bank to the International Monetary Fund (IMF), unanimously predict a slowing economy worldwide. Likewise, the World Trade Organization (WTO) forecasts that the growth of world merchandise trade will be cut to 3.5% in 2022 and down further to only 1% in 2023. As a result, the world textiles and clothing trade will likely struggle with stagnant growth or a modest decline over the next two years.

Pattern #2: COVID did NOT fundamentally shift the competitive landscape of textile exports but affected the export product structure. Meanwhile, some long-term structural changes in world textile exports continued in 2021.

Specifically, China, the European Union (EU), and India remained the world’s three largest textile exporters in 2021, a pattern that has stayed stable for over a decade. Together, these top three accounted for 68% of the world’s textile exports in 2021, similar to 66.9% before the pandemic (2018-2019). Other textile exporters that made it to the top ten list in 2021 were also the same as a year ago and before the pandemic (2018-2019).

Meanwhile, the growth rate of the top ten textile exporters varied significantly in 2021, ranging from -5.5% (China) to 47.8% (India). The demand shift from PPE to apparel-related yarns and fabrics was a critical contributing factor behind the phenomenon. For example, China’s PPE-related textile exports decreased by more than $33bn (or down 43%) in 2021. In contrast, the world knit fabric exports (SITC code 655) surged by more than 30% in 2021, led by India (up 74%) and Pakistan (up 72%). Nevertheless, as consumers’ lifestyles almost reached a “new normal,” we could expect the textile export product structure to stabilize soon.

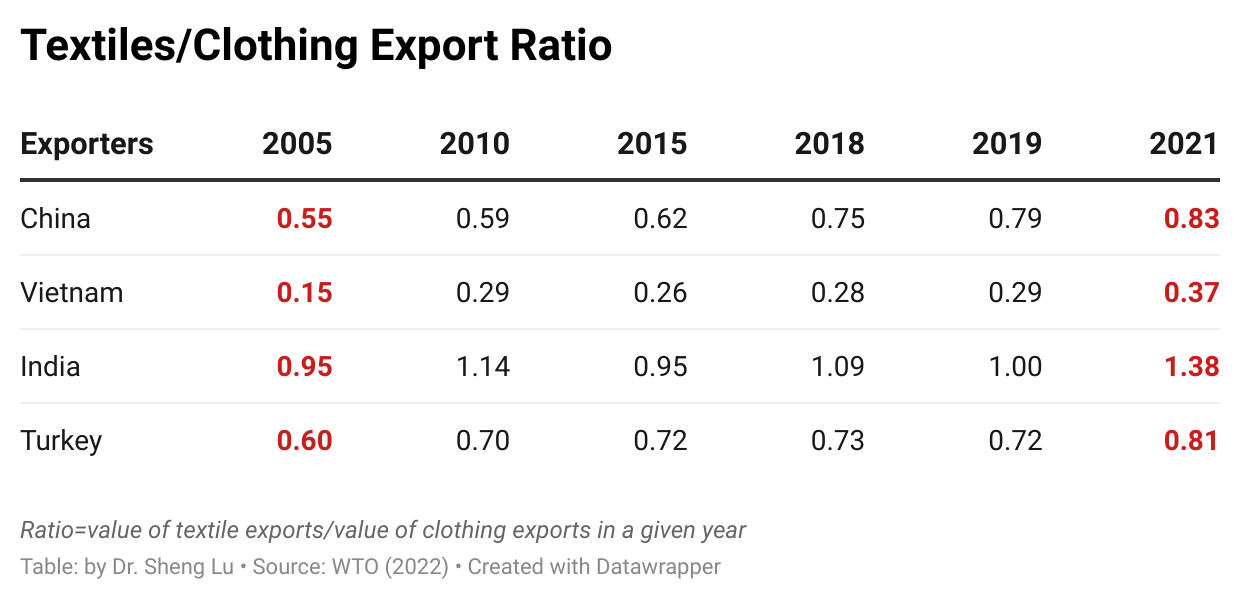

On the other hand, as a trend already emerged before the pandemic, middle-income developing countries continued to play a more significant role in textile exports, whereas developed countries lost market shares. For example, the United States, Germany, and Italy led the world’s textile exports in the 2000s, accounting for more than 20% of the market shares. However, these three countries’ shares fell to 12.8% in 2019 and hit a new low of 11.3% in 2021. In comparison, middle-income developing countries like China, Vietnam, Turkey, and India have entered the development stage of expanding textile manufacturing. As a result, their market share in the world’s textile exports rose steadily. These countries also achieved a more balanced textiles/clothing export ratio over the years, meaning more textile raw materials like yarns and fabrics can be locally produced instead of relying on imports. For example, Vietnam, known for its competitive clothing products, achieved a new high of $11.5bn in textile exports in 2021 and ranked sixth globally. Vietnam’s textiles/clothing ratio also doubled from 0.15 in 2005 to 0.37 in 2021. It is not unlikely that Vietnam’s textile exports may surpass the United States over the next few years.

Pattern #3: Countries with large-scale production capacity stood out in world clothing exports in 2021. Meanwhile, clothing exporters compete to become China’s alternatives, but there seems to be no clear winner yet.

Consumers’ surging demand and COVID-related supply chain disruptions significantly impacted the world’s clothing export patterns in 2021. As fashion brands and retailers were eager to find sourcing capacity, countries with large-scale production capacity and relatively stable supply enjoyed the fastest growth in clothing exports. For example, except for Vietnam, which suffered several months of COVID lockdowns, all other top five clothing exporters enjoyed a more than 20% growth of their exports in 2021, such as China (up 24%), Bangladesh (up 30%), Turkey (up 22%), and India (up 24%).

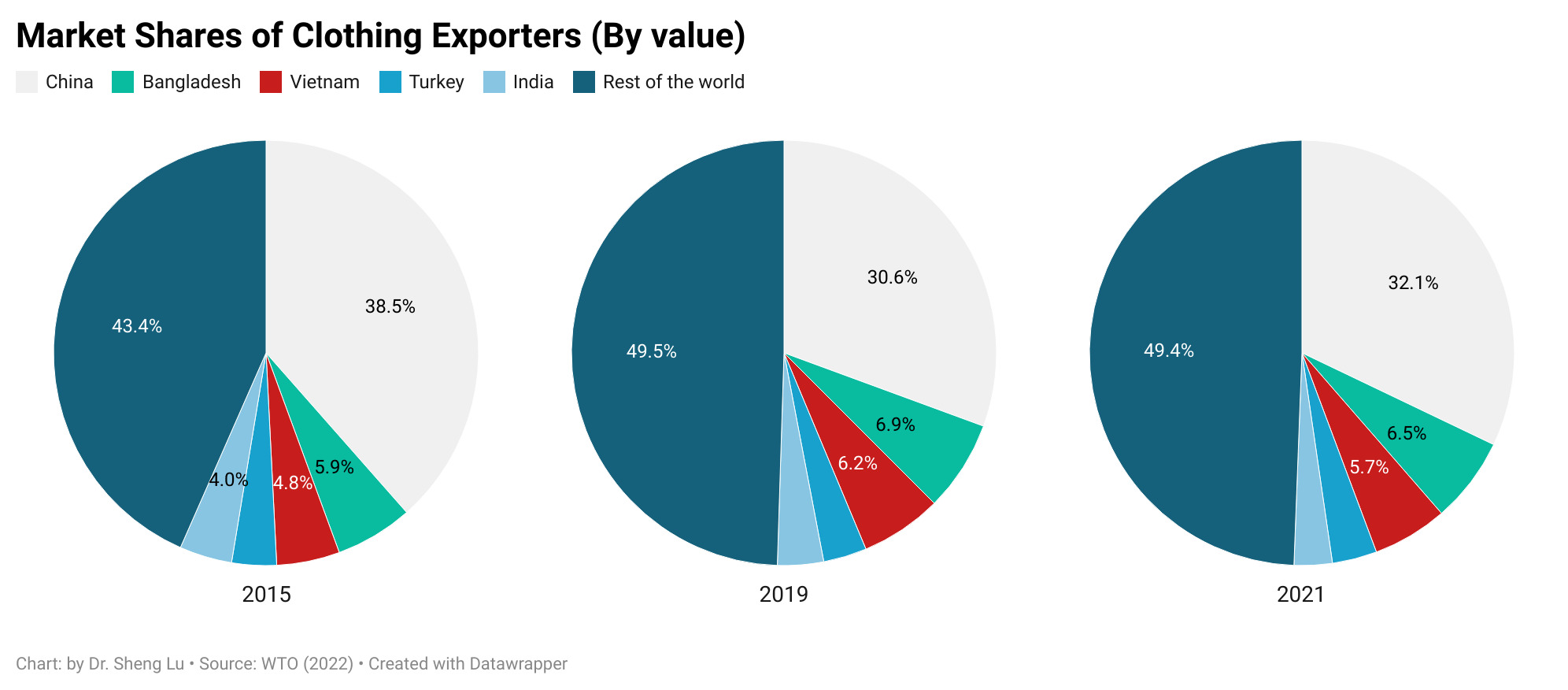

As another critical trend, many international fashion brands and retailers have been trying to reduce their apparel sourcing from China, driven by various economic and non-economic factors, from cost considerations and trade tensions to geopolitics. Notably, despite its strong performance in 2021, China accounted for only 23.1% of US apparel imports in 2022 (January to September), much lower than 36.2% in 2015. Likewise, China’s market shares in the EU, Japanese, and Canadian clothing import markets also fell over the same period, suggesting this was a worldwide phenomenon.

With reduced apparel sourcing from China, fashion companies have actively sought alternative sourcing destinations, but the latest trade data suggests no clear winner yet. For example, Vietnam and Bangladesh, the two most popular candidates for “Next China,” accounted for 6.5% and 5.7% shares in the world’s clothing export in 2021, still far behind China (32.1%). Interestingly, from 2015 to 2021, the world’s top four largest clothing exporters next to China (i.e., Bangladesh, Vietnam, Turkey, and India) did not substantially gain new market shares. Instead, China’s lost market was filled by “the rest of the world.”

Additionally, recent studies show that many fashion companies have switched back to the sourcing diversification strategy in 2022 as managing risks and improving sourcing flexibility become more urgent priorities. In other words, the world’s clothing export market could turn more “crowded” and competitive in the coming years.

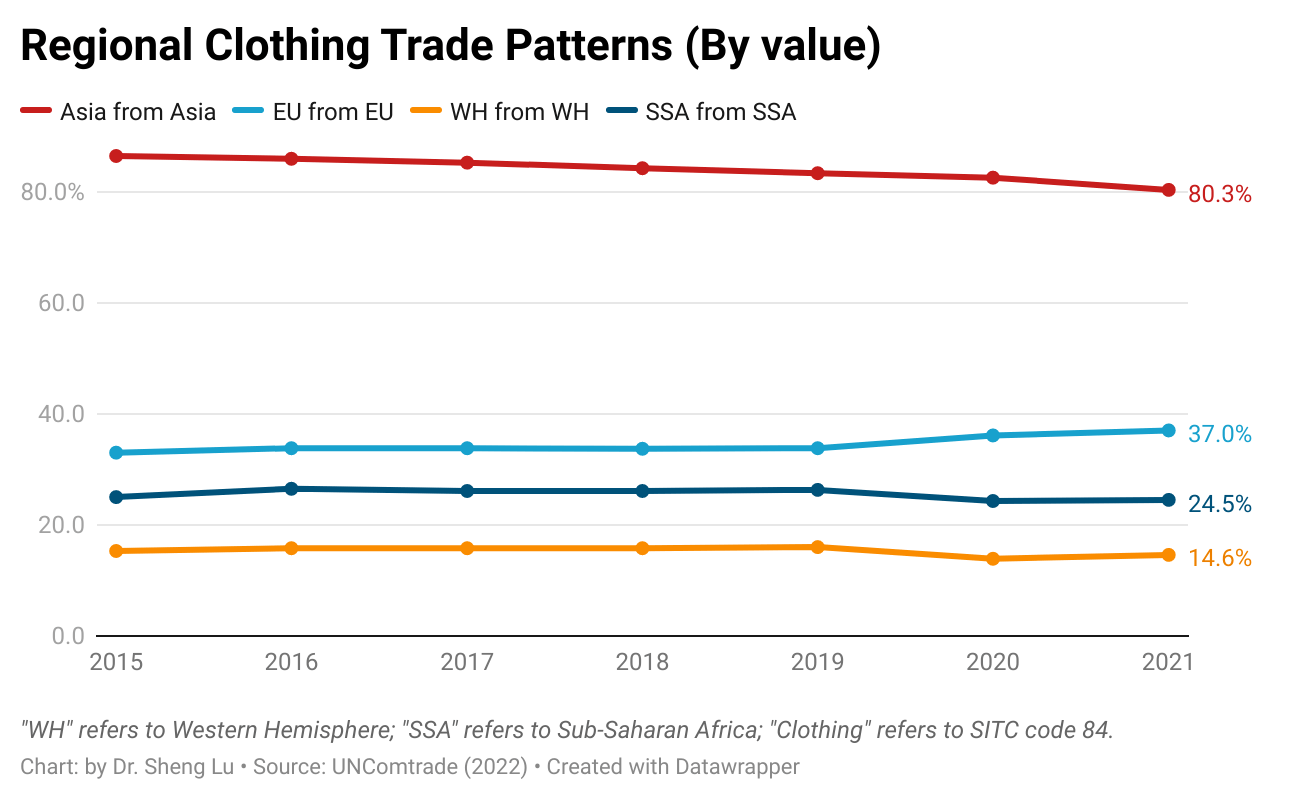

Pattern #4: Regional supply chains remain critical features of the world textiles and clothing trade. Several factors support and shape the regional textiles and clothing trade patterns. First, as clothing production often needs to be close to where textile materials are available, many developing clothing-producing countries rely heavily on imported textile materials, primarily from more advanced economies in the same region. Second, through lowered trade barriers, regional free trade agreements also financially encouraged garment producers, particularly in Asia, the EU, and Western Hemisphere (WH), to use locally or regionally made textile materials. Further, fashion companies’ interest in “near-shoring” supported the regional supply chain, and related textiles and clothing trade flows between neighboring countries.

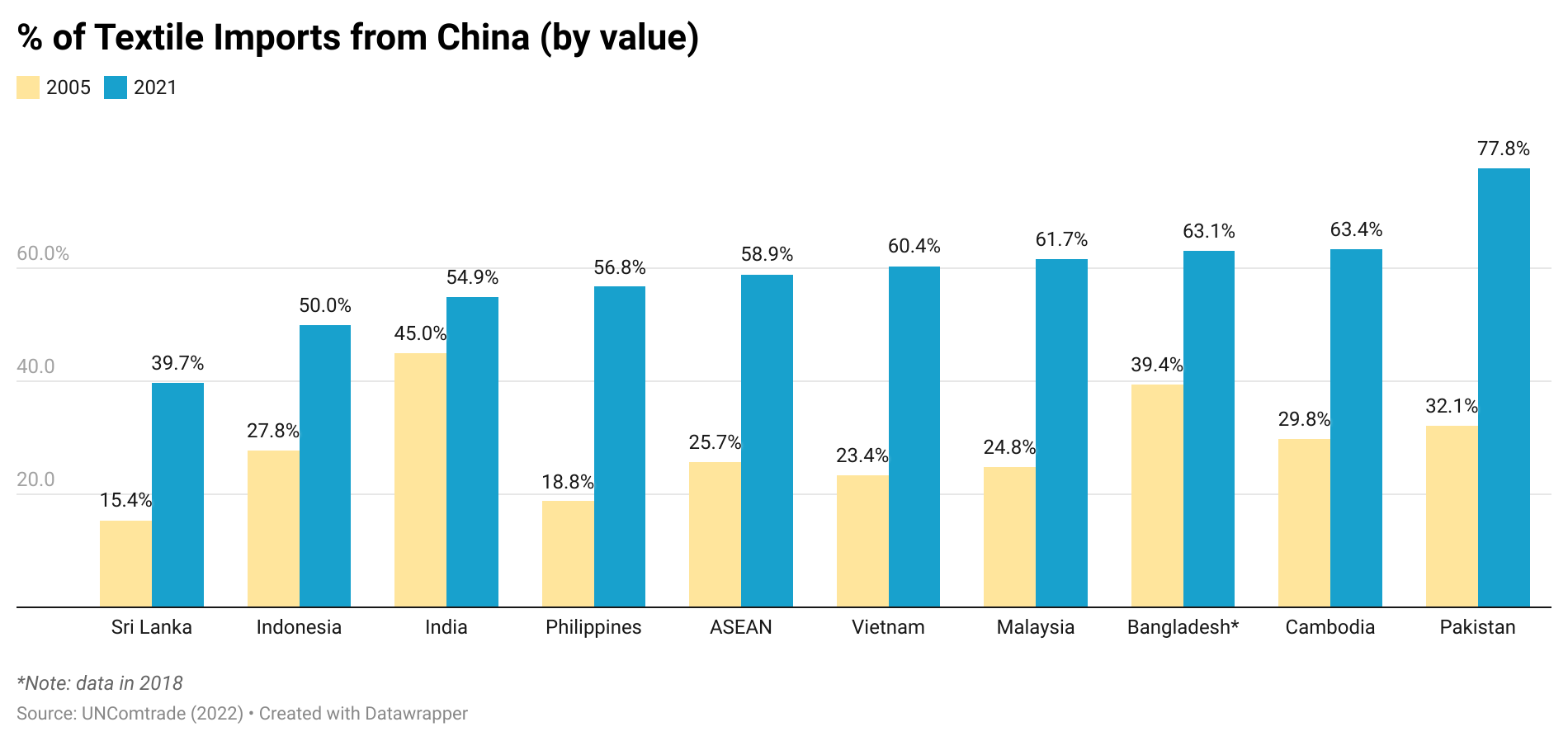

The latest trade data indicated that Asia’s regional textiles and clothing trade patterns strengthened further despite supply chain chaos during the pandemic. Specifically, in 2021, as many as 82% of Asian countries’ textile imports came from within Asia, up from 80% in 2015. China, in particular, has played a more prominent role as a leading textile supplier for other Asian clothing-exporting countries. For example, more than 60% of Vietnam’s textile imports came from China in 2021, a substantial increase from 23% in 2005. The same pattern applied to Pakistan, Cambodia, Bangladesh, and the Association of Southeast Asian Nations (ASEAN) members.

In January 2022, the Regional Comprehensive Economic Partnership (RCEP), a mega free trade agreement involving all major economies in Asia, entered into force. The tariff cut and very liberal rules of origin of the agreement will hopefully drive Asia’s booming regional textiles and clothing trade and further deepen its regional economic integration.

Besides Asia, the regional textiles and clothing trade pattern in the EU (or the so-called Intra-EU trade) was also in good shape. In 2021, 50.8% of EU countries’ textile imports and 37% of clothing imports came from other EU members. This pattern has changed little over the past decade, thanks to many EU countries’ commitment to maintaining local textiles and clothing production rather than outsourcing.

In comparison, the Western Hemisphere (WH) textile and apparel supply chain (e.g., clothing made in Mexico or Central America using US or regionally made textiles) seemed to struggle in recent years. As of 2021, only 20% of WH countries’ textile imports came from within WH, down from 26% in 2015. Likewise, WH countries (mainly the US and Canada) just imported 14.6% of clothing from WH in 2021, down from 15.3% in 2015 and much lower than their EU counterparts (37% in 2021). It will be interesting to see whether US and Canadian fashion companies’ expressed interest in expanding near-shoring may reverse the course.

Furthermore, the regional textiles and clothing trade patterns in Sub-Saharan Africa (SSA) are also worth watching. Compared with Asia and the EU, SSA clothing producers used much fewer locally-made textiles (i.e., stagnant at around 11% only from 2011 to 2021), reflecting the region’s lack of textile manufacturing capability. Most trade programs with SSA countries, such as the US-led African Growth and Opportunity Act (AGOA) and EU’s Everything But Arms (EBA) program, adopt liberal rules of origin for clothing products, allowing third-party textile input to be used. It can be studied whether such liberal rules of origin somehow disincentivize building SSA’s own textile manufacturing sector or are still essential given the reality of SSA’s limited textile production capacity.

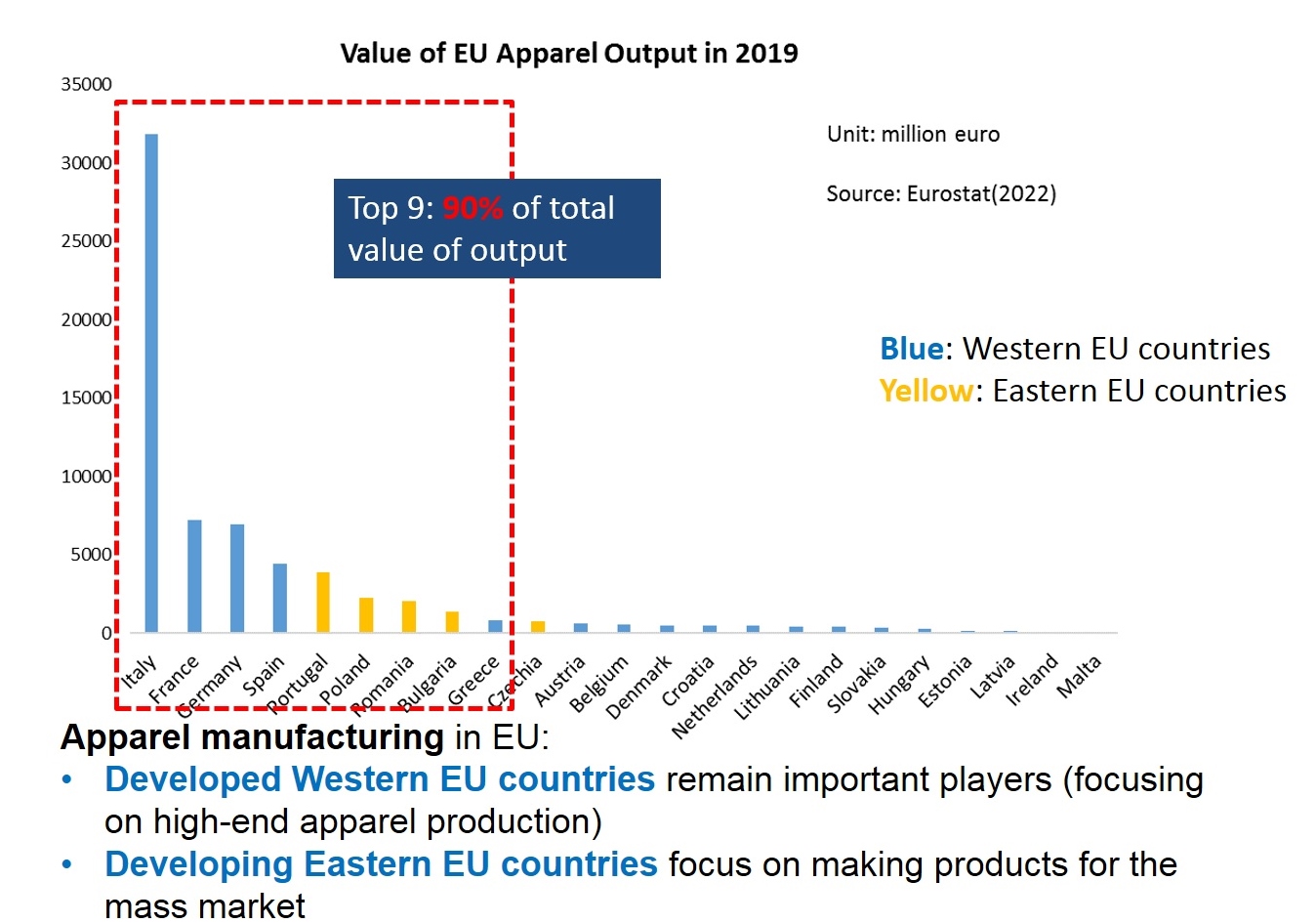

The EU region as a whole remains one of the world’s leading producers of textile and apparel (T&A). The EU’s T&A production value totaled EUR135.6 bn in 2019, down around 6% from a year ago (Note: Statistical Classification of Economic Activities or NACE, sectors C13, and C14). The EU’s T&A output value was divided almost equally between textile manufacturing (EUR69.4bn) and apparel manufacturing (EUR66.2bn).

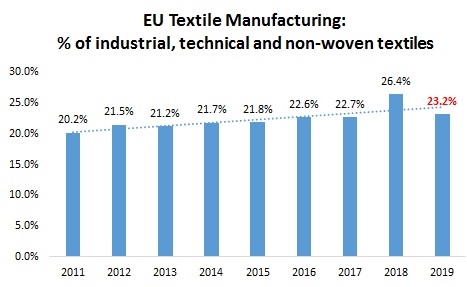

Regarding textile production, Southern and Western EU, where most developed EU members are located, such as Germany, France, and Italy, accounted for nearly 60% of EU’s textile manufacturing in 2020. Further, of EU countries’ total textile output, the share of non-woven and other technical textile products (NACE sectors C1395 and C1396) has increased from 20.2% in 2011 to 23.2% in 2019, which reflects the ongoing structural change of the sector.

Apparel manufacturing in the EU includes two primary segments: one is the medium-priced products for consumption in the mass market, which are produced primarily by developing countries in Eastern and Southern Europe, such as Poland, Hungary, and Romania, where cheap labor is relatively abundant. The other category is the high-end luxury apparel produced by developed Western EU countries, such as Italy, UK, France, and Germany.

It is also interesting to note that in Western EU countries, labor only accounted for 20.3% of the total apparel production cost in 2019, which was substantially lower than 30.1% back in 2006. This change suggests that apparel manufacturing is becoming capital and technology-intensive in some developed Western EU countries—as companies are actively adopting automation technology in garment production.

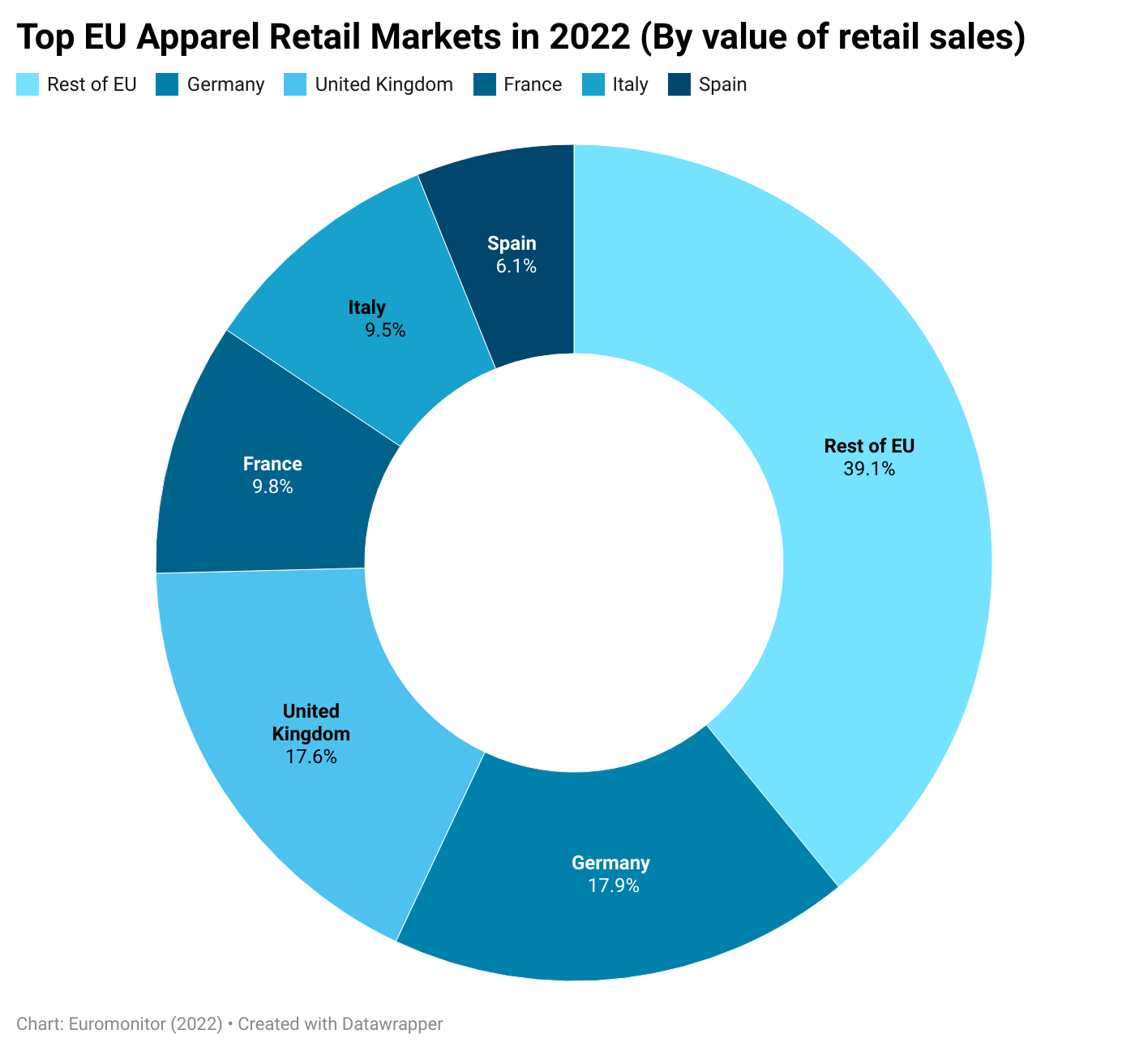

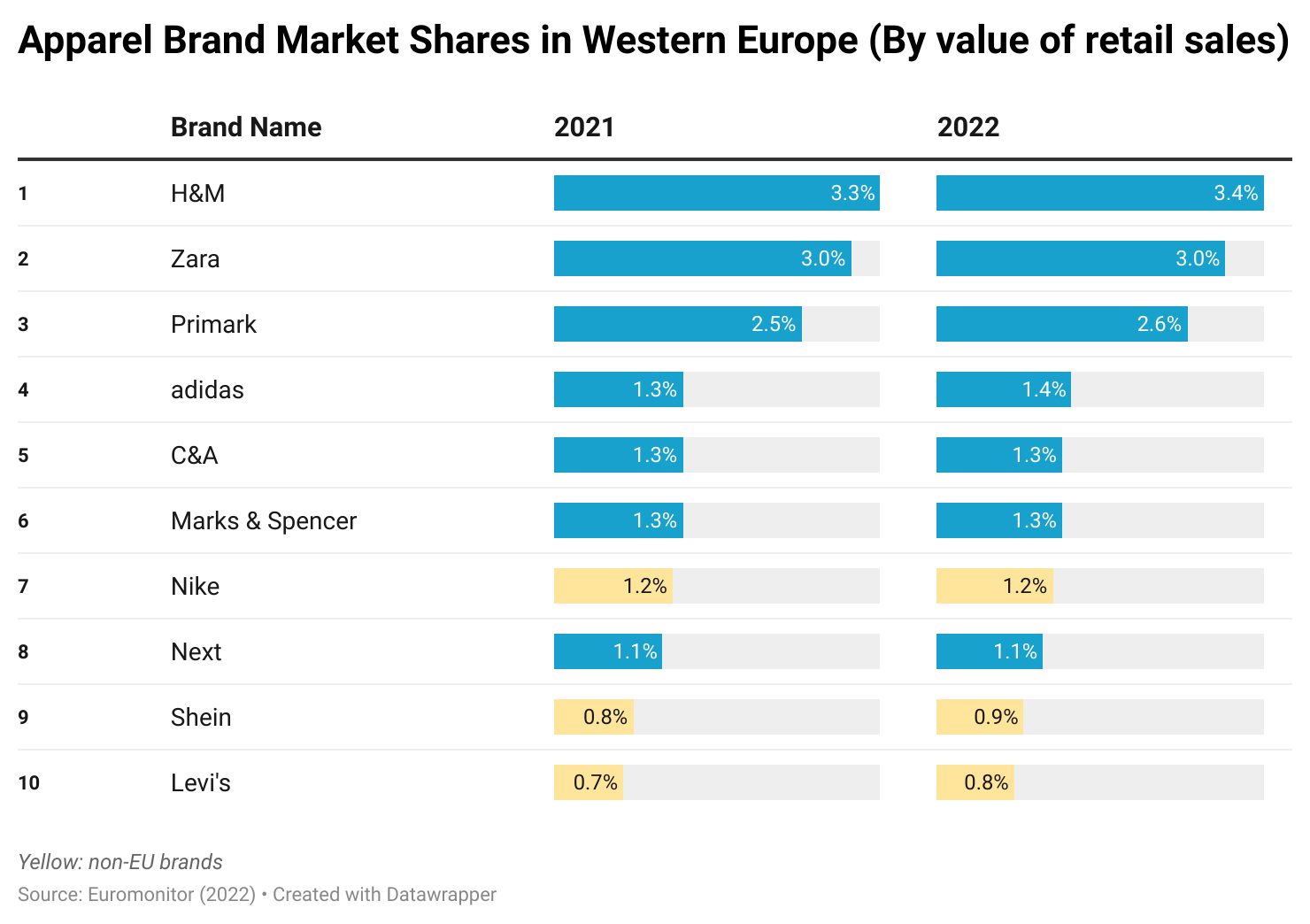

Because of their relatively high GDP per capita and the size of the population, Germany, Italy, the UK, France, and Spain accounted for nearly 60% of total apparel retail sales in the EU in 2021. Such a market structure has stayed stable over the past decade. Also, reflecting local consumers’ preference, EU apparel brands overall outperform non-EU brands in the EU retail market.

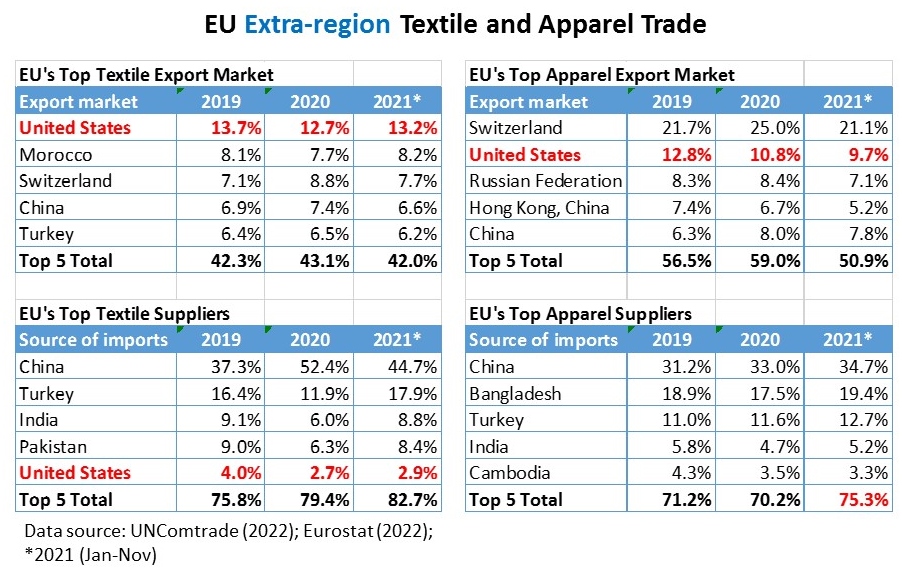

Intra-region trade is an essential feature of the EU’s textile and apparel industry. Despite the increasing pressure from cost-competitive Asian suppliers, statistics from UNComtrade show that of the EU region’s total textile imports in 2019, as much as 53.8% were in the category of intra-region trade. However, it could result from increased PPE imports from Asia, EU countries’ Intra-region trade% for textiles dropped to 40% in 2020.

Meanwhile, about one-third of EU countries’ apparel imports came from other EU members during 2019-2020. In comparison, close to 98% of apparel consumed in the United States was imported over the same period, of which more than 75% came from Asia (Eurostat, 2022; UNComtrade, 2022).

Regarding EU countries’ textile and apparel trade with non-EU members (i.e., extra-region trade), the United States remained one of the EU’s top export markets and a vital textile supplier (mainly for technical and industrial textiles). Meanwhile, Asian countries, led by China, and Bangladesh, served as the dominant apparel sourcing base outside the EU region for EU fashion brands and retailers. Turkey was another important apparel sourcing base for EU fashion companies. There is no sign that COVID-19 has shifted the trade pattern.

Additionally, Vietnam was EU’s sixth-largest extra-region apparel supplier in 2020 (after China, Bangladesh, Turkey, India, and Cambodia), accounting for 4% in value. The EU-Vietnam Free Trade Agreement which took effect in August 2020, could encourage more EU apparel sourcing from the country in the long run.

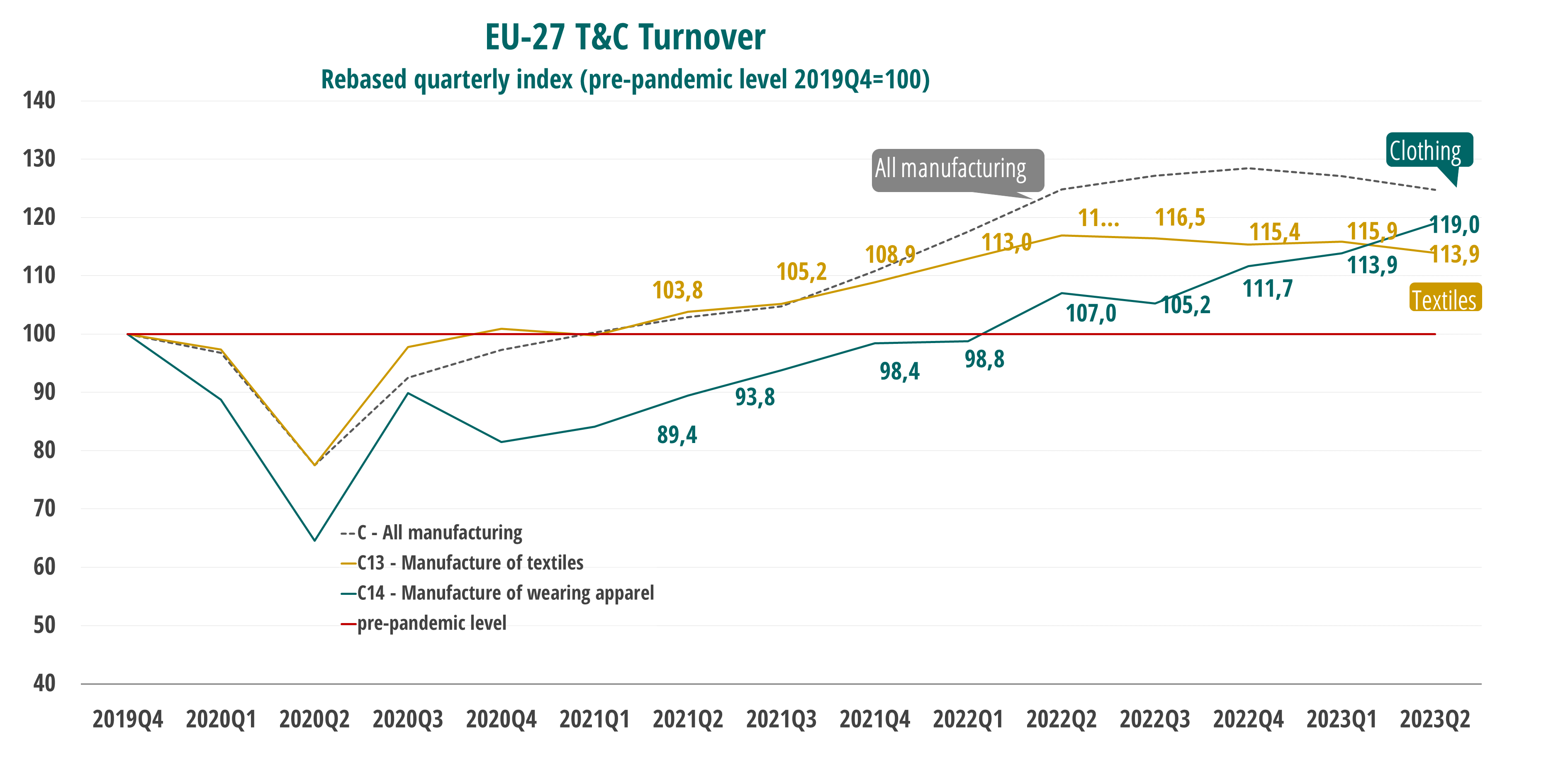

According to the European Apparel and Textile Federation (Euratex), the EU textile and apparel industry continued to recover from COVID-19. For example, the value of textile and apparel output has already reached its pre-pandemic level by the end of 2022. However, Euratex warns that the EU textile and apparel industry still faces significant challenges from a slowed economy, hiking energy costs as a result of the Russia-Ukraine war, and high inflation.

Video 3: Vietnam’s textile and apparel industry amid the pandemic

Video 4: How H&M’s Recycling Machines Make New Clothes From Used Apparel in Hong Kong

Discussion questions:

How are textiles and apparel “Made in Asia” changing their face? What are the driving forces of these changes?

Based on the video, why or why not do you think the “flying geese model” is still valid today?

How to understand COVID-19’s impact on Asia’s textile and apparel industry? What strategies have been adopted by garment factories in Asia to survive the pandemic? What challenges do they still face?

What is your evaluation of Asia’s competitiveness as a textile and apparel production and sourcing hub over the next five years? Why? What factors could be relevant?

Anything else you find interesting/intriguing/thought-provoking/debatable in the video? Why?

Note: Everyone is welcome to join our online discussion. For students in FASH455, please address at least two questions. Please mention the question number # (no need to repeat the question) in your comment.