Tarek Kabil – Egyptian Ministry of Trade & Industry

Ashraf Rabiey – QIZ Minister of Egypt

Gabi Bar – QIZ Minister of Israel

Mark D’Sa – Special Project Director for Haiti

Moderator: Gail Strickler – former Assistant US Trade Representative for Textiles

Discussion questions:

What are the financial incentives for US brands and retailers to source apparel in preference program countries? Why do U.S. apparel imports from members of AGOA, QIZs and HELP overall remain at a fairly low level despite the trade preference programs? How to improve the situation?

Overall, why or why not should the US keep the trade preference programs or any critical reforms are needed?

Any other interesting points you learned from the video or questions you may have?

Dr. Marsha Dickson, Irma Ayers Professor, Department of Fashion and Apparel Studies at the University of Delaware discusses her co-founded Better Buying project(http://www.betterbuying.org), a meaningful effort to improve the social responsibility practices in the global apparel industry. The video is produced by Mallory Metzner, reporter of channel 49 of the University of Delaware.

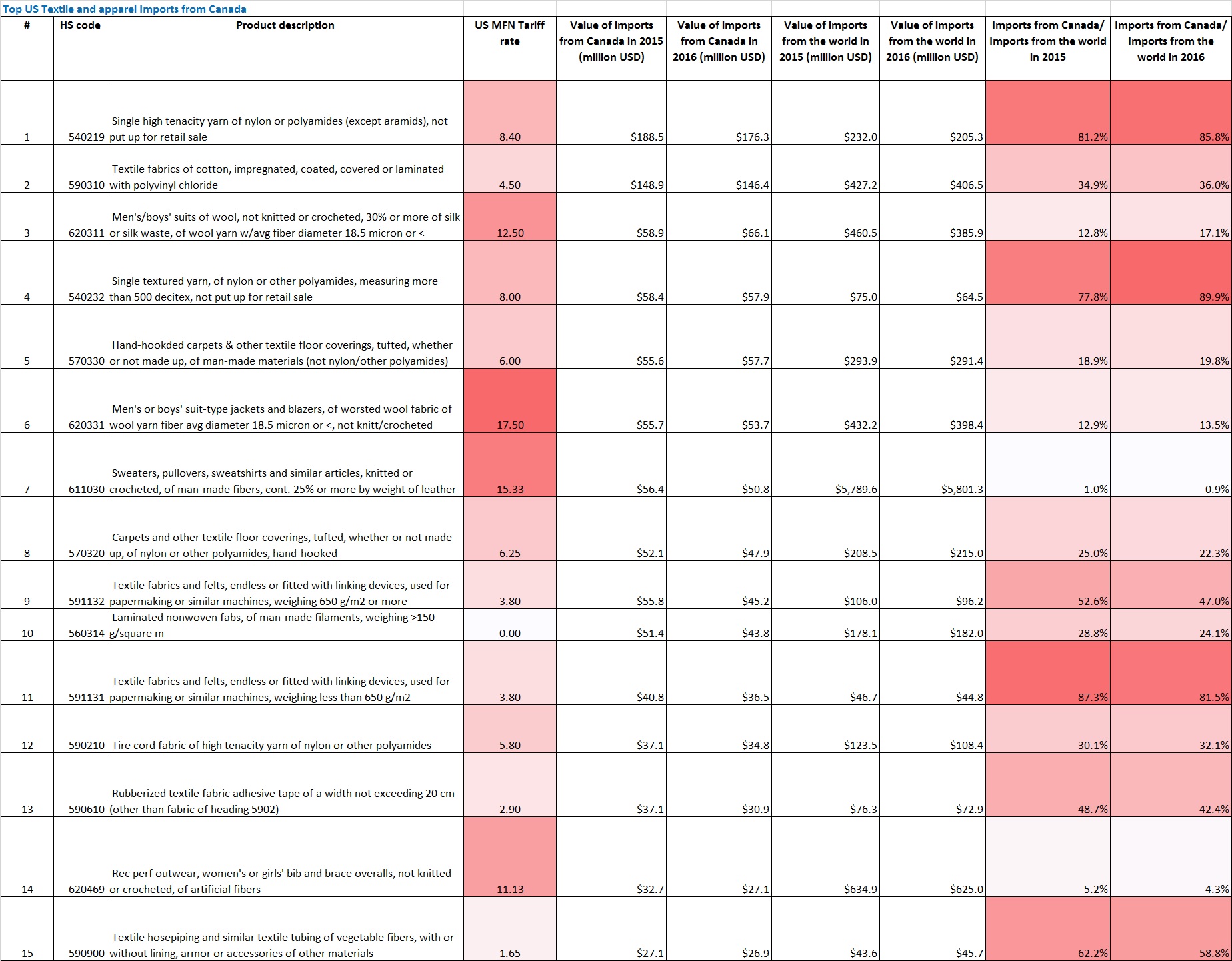

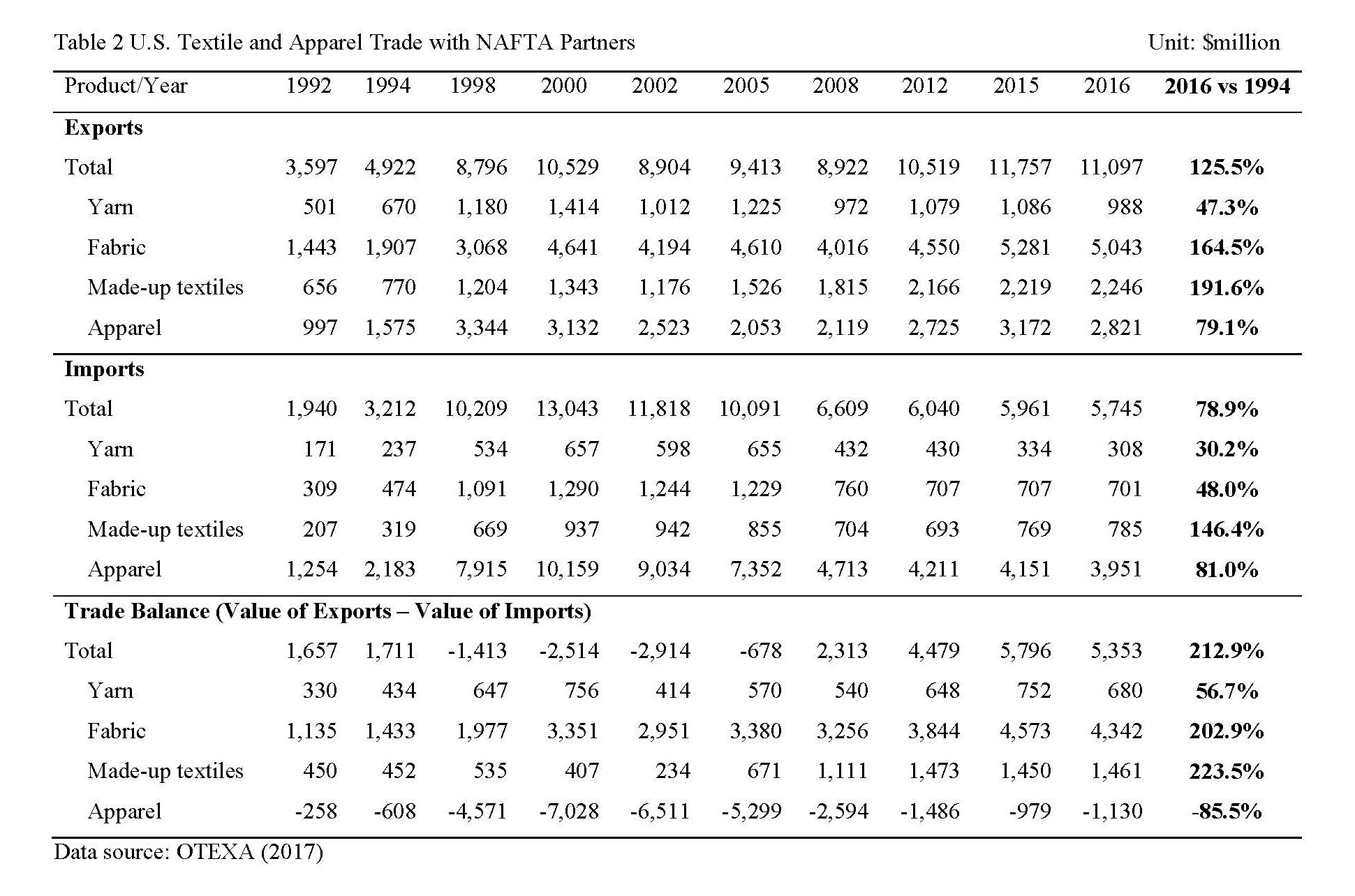

The United States maintains a bilateral trade surplus in yarns and fabrics ($4.1 billion in 2016) as well as made-up textiles ($720 million in 2016) with NAFTA members.

Regarding apparel, the United States had a trade surplus with Canada of $1.4 billion and a trade deficit with Mexico of $2.7 billion in 2016.

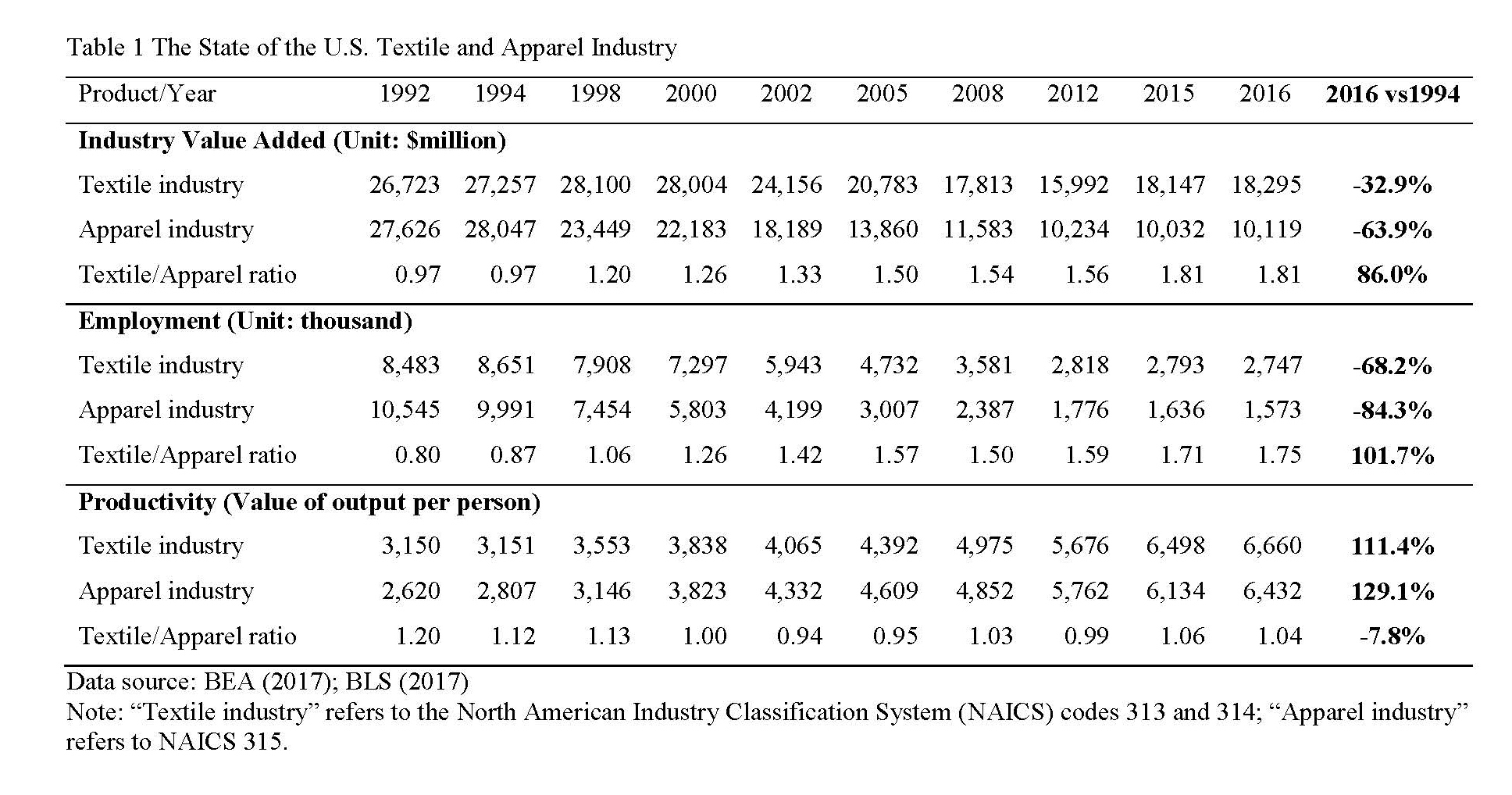

Impact of NAFTA on employment and production in the U.S. textile and apparel industry

The effects of NAFTA are NOT straightforward, and the drop in U.S. domestic textile and apparel production and jobs cannot be blamed solely on NAFTA.

The U.S. International Trade Commission (USITC) concluded that imports of textiles had a tiny effect on U.S. textile industry employment (a 0.4% decline) from 1998 to 2014, which covers most of the period since NAFTA’s enactment. However, the collapse of the U.S. domestic apparel industry and changing clothing tastes may have had a more significant impact on domestic textile production.

There is little evidence that NAFTA was the decisive factor for the loss of jobs in the U.S. apparel manufacturing sector, given that the major growth in apparel manufacturing for the U.S. market has occurred in Asian countries that receive no preferences under NAFTA.

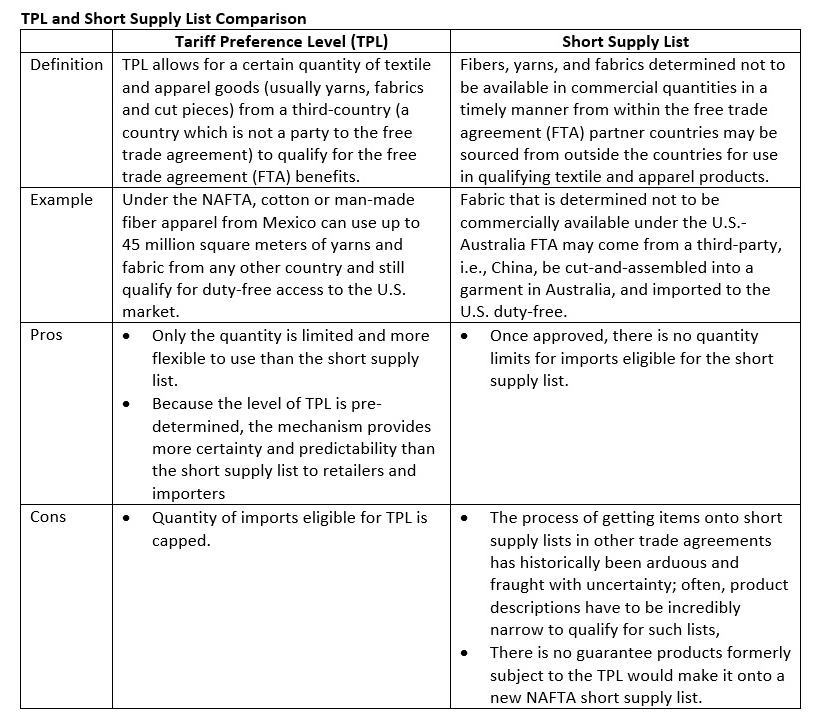

Impact of the Tariff Preference Level (TPL) in NAFTA

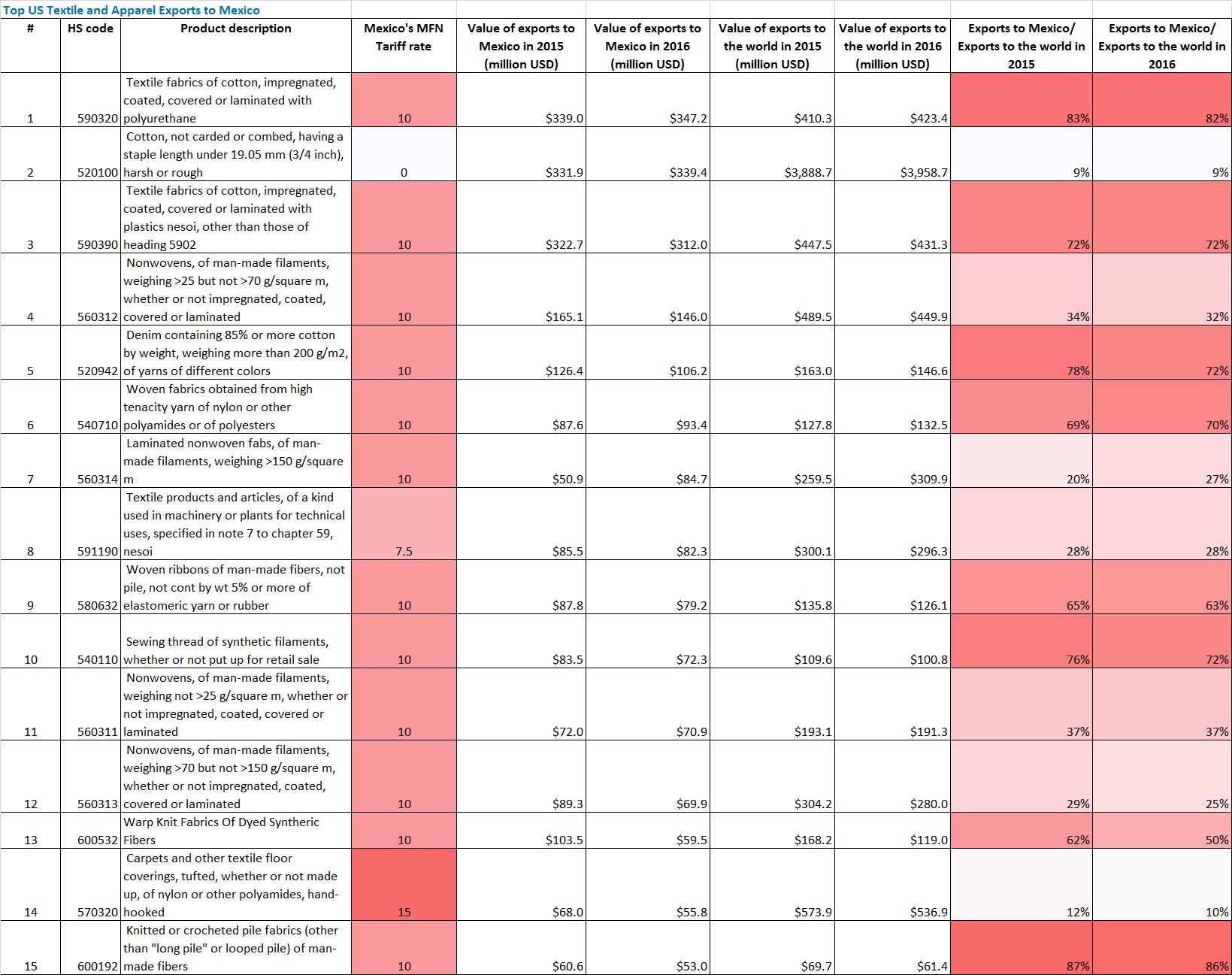

In nearly every year since 2010, Mexico has come close to exporting the maximum allowable amount of cotton and man-made fiber apparel with duty-free foreign content. Canada’s TPL fill rates are typically highest for cotton and man-made fiber fabric and made-up products but are not usually fully filled.

It is not clear that eliminating the TPL program would result in a substantial return of textile production or jobs to the United States;if it were to raise the cost of Mexican apparel production, it could instead result in imports from other countries displacing imports from Mexico.

Other than U.S. fashion brands and retailers, Mexico and Canada reportedly oppose the elimination of the NAFTA TPL program too.

Possible Effects of Potential NAFTA Modification

Mexico’s focus on basic apparel items suggests that S. importers could quickly source from elsewhere if duty savings under NAFTA are eliminated. However, even now, some U.S. fashion companies say the duty savings are not worth the time and resources required to comply with the NAFTA rules of origin and documentation requirements. In 2016, roughly 16% of qualifying textile and apparel imports from NAFTA failed to take advantage of the duty-free benefits and instead paid applicable tariffs.

Whatever the outcome of the NAFTA renegotiation, in the medium and long run, the profitability of the North American textile and apparel industry will likely depend less on NAFTA preferences such as yarn forward and more on the capacity of producers in the region to innovate to remain globally competitive.

One change in NAFTA proposed by the United States would require motor vehicles to have 85% North American content and 50% U.S. content to qualify for tariff-free treatment. If auto manufacturers were to import more passenger cars from outside the NAFTA region and pay the 2.5% U.S. import duty rather than complying with stricter domestic content requirements, automotive demand for U.S.-made technical textiles could be adversely affected.

If the TPP-11 countries strike a trade deal, one possible effect is that Canada and Mexico may import more textile and apparel products from other TPP countries, including Vietnam. This could ultimately be a disadvantage for U.S.-based producers. How the inclusion of Canada and Mexico in a fresh TPP-11 arrangement would affect their participation in NAFTA is unknown.

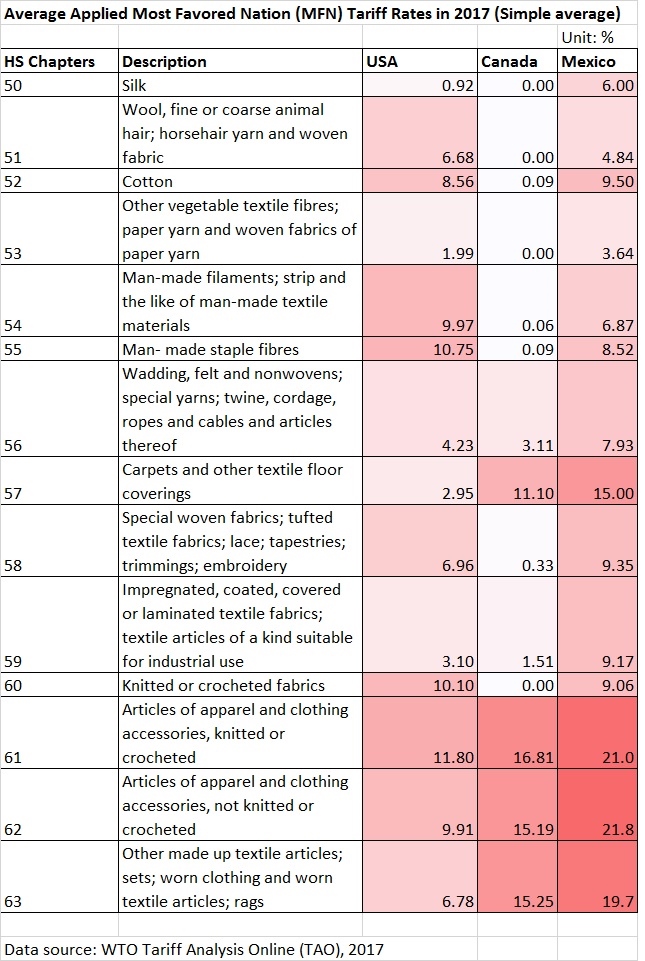

If the North American Free Trade Agreement (NAFTA) is terminated by President Trump, the immediate impact will be an increase in tariff rate for textile and apparel (T&A) products traded between the three NAFTA members from zero to the most-favored-nation (MFN) rates applied for regular trading partners. In 2017, the average applied MFN tariff rates for textile and apparel were 7.9% and 11.6% respectively in the United States, 2.3% and 16.5% in Canada and 9.8% and 21.2% in Mexico (WTO Tariff Profile, 2017).

Below is NAFTA members’ average applied MFN tariff rate in 2017 for chapters 50-63, which cover T&A products:

Data source: World Trade Organization (2017); US International Trade Commission (2017)

According to the newly released World Trade Statistical Review 2017 by the World Trade Organization (WTO), the current dollar value of world textiles (SITC 65) and apparel (SITC 84) exports totaled $284 billion and $443 billion respectively in 2016, marginally decreased by 2.3 percent and 0.4 percent respectively from a year earlier. This is the second year in a roll since 2015 that the value of world textiles and apparel exports grew negatively.

However, textiles and apparel are not alone. The current dollar value of world merchandise exports also declined by 3 percent in 2015, to $11.2 trillion, mostly caused by the strong decline in exports of fuels and mining products (-14 percent). On the other hand, as noted by the WTO, the steep drop in commodity prices recorded in 2015 mostly halted in 2016, except energy prices.

Textile and apparel exports

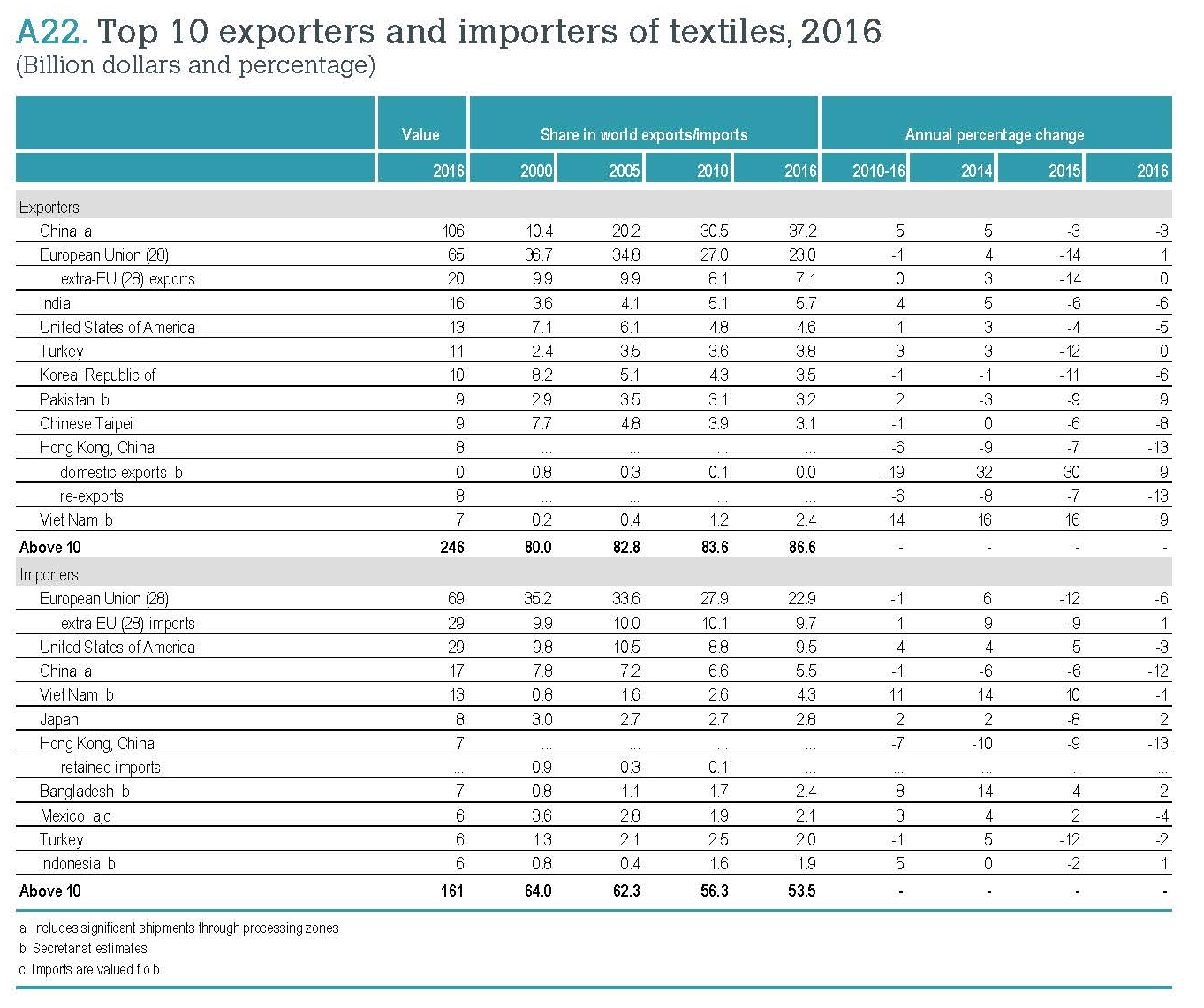

Measured in value, China, European Union, and India remained the top three exporters of textiles in 2016. Altogether, these top three accounted for 65.9 percent of world exports in 2016, slightly down from 66.5 percent in 2015, which is mostly due to India’s shrinking market shares.

The United States remained the fourth top textile exporter in 2016, accounting for 4.6 percent of the shares (down from 4.8 percent in 2015). Over half of the top ten exporters experienced a decline in the value of their exports in 2016, with the highest declines seen in Hong Kong (-13 percent), Taiwan (-8 percent), South Korea (-6 percent) and the United States (-6 percent). Notably, Vietnam entered the world’s top ten textile exporters for the first time (2 percent market shares, 9 percent growth rate from 2015).

Top three exporters of apparel include China, the European Union, and Bangladesh. Altogether, they accounted for 69.1 percent of world exports, close to 70.3 percent in 2015. Among the top ten exporters of apparel, increases in export values were recorded by Cambodia (+6 percent), Bangladesh (+6 percent), Vietnam (+5 percent), and European Union (+4 percent). Other leading exporters saw stagnation in their export values (such as Turkey) or recorded a decline (such as China, India, and Indonesia).

Could be negatively affected by the rising labor and production cost, China’s shares in the world textile exports dropped from 37.4 percent in 2015 to 37.2 percent in 2016, and the shares in the world apparel exports fell from 39.2 percent in 2015 to 36.4 percent in 2016—a record low since 2010.

Textile and apparel imports

Measured in value, the European Union, the United States, and China were the top three importers of textiles in 2016. These top three altogether accounted for 38 percent of world textile imports, slightly up from 37 percent in 2015, but remains much lower than over 53 percent back in 2000. Notably, over the past decade, apparel manufacturing continues to shift from developed to developing countries and many developing countries heavily rely on imported textile inputs due to the lack of local manufacturing capacity. This explains why more textile exports now go to the developing nations.

On the other hand, affected by consumers’ purchasing power (often measured by GDP per capita) and size of the population, the European Union, the United States, and Japan remained the top three importers of apparel in 2016. Altogether, these top three accounted for 62.9 percent of world apparel imports in 2016, up from 59 percent in 2015. Notably, China is quickly becoming one of the world’s top apparel importers. From 2010 to 2016, China’s apparel imports enjoyed an annual 17 percent growth, much higher than most other countries.

Mexico’s textile and apparel (T&A) exports totaled USD$6,441 million in 2016, fell by 5.1% from 2015. Around 63% of these exports were apparel (or USD$4,061 million), and 37% (or USD$2,379 million) was textiles.

Could be negatively affected by the appreciation of the Mexican Peso against the U.S. dollar, plus the uncertainty associated with the renegotiation of the North American Free Trade Agreement (NAFTA), Mexico’s apparel exports further went down 7.2% in the first half of 2017 compared to 2016.

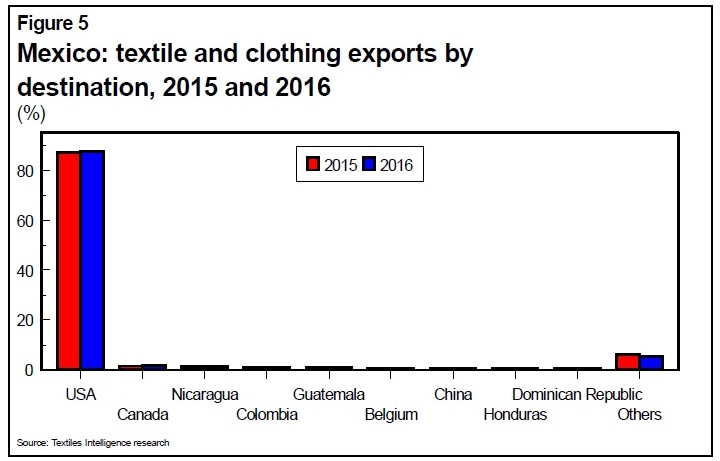

In 2016, the United States remains Mexico’s top T&A export market with an 87.3% share (up from 87.0% in 2015, 86.7% in 2014 and 84.7% in both 2013 and 2012), followed by Canada with a 1.9% share (up from 1.6% in 2015). Overall, Mexico was the sixth largest T&A supplier for the U.S. market, accounting for 4.3% of the market shares measured by value in 2016.

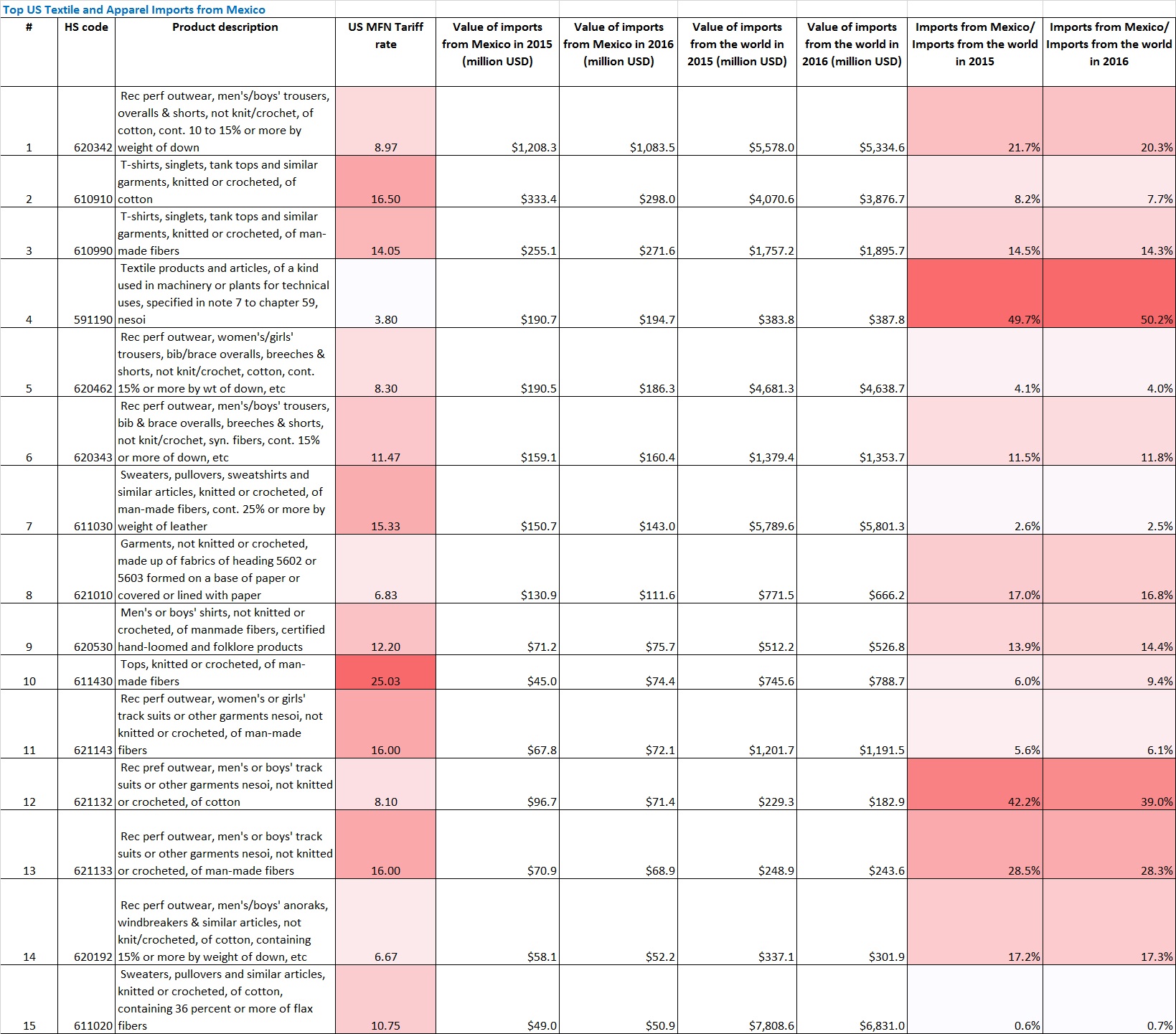

Nevertheless, Mexico’s T&A exports to the United States fell by 4.7% between 2015 and 2016 (from USD$5,902 million to USD$5,625 million). Product categories that suffered the deepest drop include cotton hosiery (down by 57.3%), men’s and boys’ wool suits (down by 35.9%), manmade fiber underwear (down by 29.0%), and men’s and boys’ cotton woven shirts (down by 27.9%).

Overall, Mexican T&A exporters feel relieved that the United States has decided to withdraw from the Trans-Pacific Partnership (TPP). However, without TPP, the Mexican T&A industry is still expected to face an increased competition from Vietnam and China both in the leading export markets (such as the United States and Canada) and the domestic market. Notably, the Mexican government has decided to lower the Most Favored Nation (MFN) import duty rates on the 73 clothing items and seven made-up textile items effective in January 2019.

References: Textile Outlook International (October 2017)

Pete Bauman, Senior VP, Burlington Worldwide / ITG

Joann Kim, Director, Johnny’s Fashion Studio

Tricia Carey, Business Development Manager, Lenzing USA

Michael Penner, CEO, Peds Legwear

Moderator: Arthur Friedman, Senior Editor, Textiles and Trade, WWD

Video Discussion Questions

How does “Made in the USA” fit into US textile and apparel companies’ overall business strategy today?

What measures have been taken by US textile and apparel companies to bring more production back to the US? Can any measures be linked to the restructuring strategies we discussed in the class?

What are the significant obstacles to bringing textile and apparel manufacturing back to the US?

Any other exciting points/buzzwords did you learn from the panel discussion?

According to Inside US Trade, in the third round the NAFTA renegotiation (September 23-27, 2017), the United States has put forward several possible changes to the existing rules related to textile and apparel in the agreement:

USTR proposes to eliminate the tariff preference level (TPL) in NAFTA. The goal of eliminating TPL is to limit the exceptions to the yarn-forward rules of origin and “incentivize” more production in the NAFTA region as advocated by the U.S. textile industry.

As a potential replacement for TPL, USTR also proses to add a short supply list mechanism to NAFTA, but details remain unclear (e.g., whether the list will be temporary or permanent; the application process).

USTR further proposes a new chapter devoted to textile and apparel in NAFTA in line with more recent agreements negotiated by the U.S.. The current NAFTA does not include a textile chapter.

Eliminating TPLs would disrupt supply chains that have been in place for more than two decades.

Eliminating TPLs would not move production back to the U.S. but would instead further incentivize sourcing from outside the NAFTA region and put textile and apparel factories in the region out of business. For example, some apparel factories remain production in the NAFTA region largely because TPL allows them to use third-party textile inputs and the finished goods can still be treated as NAFTA originating.

Without the TPL, companies would opt to produce textile and apparel products in the least expensive way possible, likely outside the NAFTA region, and ship items into North America despite being hit with most-favored-nation (MFN) tariffs.

A short supply list would not ease the supply chain disruptions that would result from the removal of the TPLs because there is no guarantee products formerly subject to the TPL would make it onto a new NAFTA short supply list.

A potential compromise could involve a reduction in Canadian and Mexican TPLs to the U.S. and an increase in the U.S. TPLs to Mexico and Canada, which could boost the U.S. trade surplus in textiles and apparel with its NAFTA partners and throw a bone to the U.S. textile industry by ostensibly incentivizing domestic production.

Fact-check about TPL

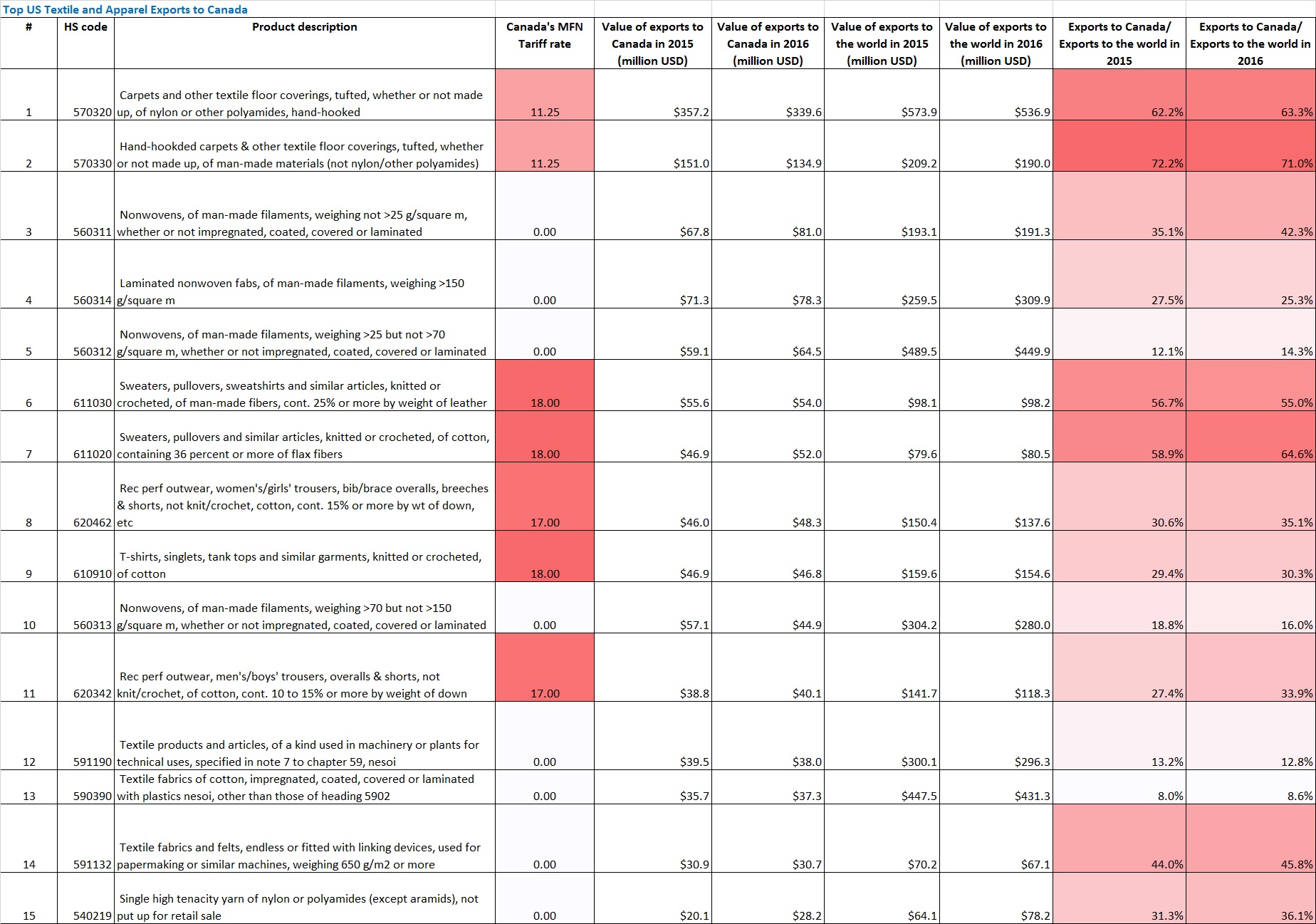

TPL was included in NAFTA as a compromise for adopting the yarn-forward rules of origin in the agreement. Before NAFTA, the US-Canada trade agreement adopted the less restrictive fabric-forward rules of origin.

The TPL mechanism has played a critical role in facilitating the textile and apparel (T&A) trade and production collaboration between the United States and Canada, in particular, the export of Canada’s wool suits to the United States and the U.S. cotton or man-made fiber apparel to Canada. Statistics from the Office of Textiles and Apparel (OTEXA) show that in 2016 more than 70% of the value of Canada’s apparel exports to the United States under NAFTA utilized the TPL provision, including almost all wool apparel products. Over the same period, the TPL fulfillment rate for U.S. cotton or man-made fiber apparel exports to Canada reached 100%, suggesting a high utilization of the TPL mechanism by U.S. apparel firms too (Global Affairs Canada, 2017). Several studies argue that without the TPL mechanism, the U.S.-Canada bilateral T&A trade volume could be in much smaller scale (USITC, 2016). Notably, garments assembled in the United States and Canada often contained non-NAFTA originating textile inputs, which failed them to meet the “yarn-forward” rules of origin typically required for the preferential duty treatment under NAFTA.

At an event hosted by the Center for Strategic and International Studies (CSIS) on September 18, U.S. Trade Representative Robert Lighthizer addressed the U.S. trade policy in the Trump Administration, particularly Trump’s beliefs on trade:

Philosophy 1: The reason why some Americans oppose free trade is NOT that they were “ill-informed.” Rather, it is because the U.S. trade policy for decades has failed to create a “level playing field.” The Trump Administration will proactively use all instruments to “make it expensive” for U.S. trading partners to engage in the non-economic behavior, convince U.S. trading partners to treat U.S. workers, farmers, and ranchers fairly and demand “reciprocity” both in the home and international markets.

Philosophy2: Trade deficits matter. Although trade policy is not the only cause for the trade deficit, it can be a major contributor, such as high tariffs that deny the market access for U.S. products, not imposing the border adjustment tax and currency manipulation.

Philosophy 3: China is the top challenge. According to Lighthizer, “the sheer scale of China’s coordinated efforts to develop their economy, to subsidize, to create national champions, to force technology transfer, and to distort markets in China and throughout the world is a threat to the world trading system that is unprecedented.”

Philosophy 4: The Trump Administrations will exam all existing trade agreements to make sure they provide “roughly equivalent” measured by trade deficits. “Where there the numbers and other factors indicate a disequilibrium, one should renegotiate.”

During the Q&A session, Lighthizer further shared his views on some cutting-edge trade issues:

Regarding the NAFTA renegotiation, Lightlizher said that the negotiation is “moving at warp speed, but we don’t know whether we’re going to get to a conclusion, that’s the problem.” The consultation process with U.S. Congress is complicated and time-consuming, but it is unavoidable.

The Trump Administration prefers bilateral trade deal over regional and multilateral ones. Given the size of the U.S. economy, Lighthizer believes that bilateral trade agreement will provide more negotiation leverages and ensure better enforcement.

The Trump Administration will still stay very much engaged in Asia.

The WTO Dispute-Settlement mechanism doesn’t work well—it has both imposed new obligations for the U.S. and reduced a lot of U.S. benefits.

Regarding the outlook for the Trans-Atlantic Trade and Investment Partnership (T-TIP) negotiation, Lighthizer stressed the importance of the US-EU trade relations. He said that the series of elections in EU is a reason why the negotiation of the agreement hasn’t moved forward.

Regarding TISA (Trade in services agreement), the U.S. objective is to open markets and eliminate market access barriers for U.S. companies.

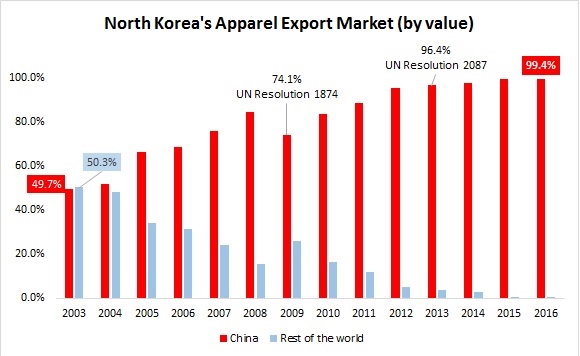

First, apparel (defined by HS Chapters 61 & 62) is one of the top categories of North Korea’s merchandise exports.Statistics from the International Trade Center (ITC) show that of North Korea’s total US$2,339.9 million merchandise exports in 2016, US$564.7 million (or 19.4%) were apparel.

Second, apparel is also one of the fastest-growing categories of North Korea’s exports over the past decade. From 2003 to 2016, the value of North Korea’s apparel exports surged by 416%, compared to only 171% increase of other products over the same period.

Third, over 99.4% of North Korea’s apparel exports went to China in 2016. Notably, back in 2003, China only accounted for 49.7% of North Korea’s apparel exports. However, apparel exports from North Korea to China received two substantial boosts just in the past ten years: one in 2009 (the year when UN resolution 1874 was adopted) and another in 2013 (the year when UN resolution 2087 was adopted).

Fourth, interesting enough, North Korea’s apparel exports predominantly concentrate on men and women’s overcoats (HS 6201 and 6202) as well as suits, jackets, and blazers (HS 6203 and 6204). This is a notable difference from most other developing countries, such as Bangladesh, Vietnam, and Cambodia whose apparel exports usually focus on more basic items like shirts and trousers.

Disclaimer: All blog posts on this site are for FASH455 educational purposes only and they are nonpolitical and nonpartisan in nature. No blog post has the intention to favor or oppose any particular public policy, nor shall be interpreted in that way.

Vietnam has a substantial textile and clothing industry comprising around 4,000 enterprises, of which the majority were located in the country’s two principal population centers—Ho Chi Minh City and Hanoi. Around 70% of these enterprises were involved in the manufacture of clothing. A further 17% were involved in the fabric sector, 6% in the yarn sector, 4% in the dyeing sector and 3% in the accessories sector.

It is estimated that around 70% of Vietnam’s textile and clothing production is dependent on the cut and trims operations, using imported textiles and other inputs predominantly from China. This problem is not limited to a single category as the country needs to import man-made fibers, yarns, fabrics, and accessories as well as raw cotton.

The dyeing and finishing segments of the supply chain remain fairly underdeveloped. In the past, the Vietnamese government has issued tightly controlled permits for these operations. Also, there has been a deficiency of investment in these segments because of unclear regulations, and this has resulted in a bottleneck in the supply chain.

Similarly, high added-value design and “downstream” activities rely on the input of foreign companies are also underdeveloped. Consequently, in carrying out these activities, the industry relies heavily on the help or participation of foreign companies.

State of Vietnam’s Textile and Apparel Export

Vietnamese textile and clothing exports began to gain momentum in 2001 when trading relationships were established with Western countries (e.g., the US-Vietnam Textile Agreement). The industry’s exports received a further boost after Vietnam joined the World Trade Organization (WTO) at the start of 2007, and the quotas which had been restricting imports of Vietnamese goods in the US market were eliminated.

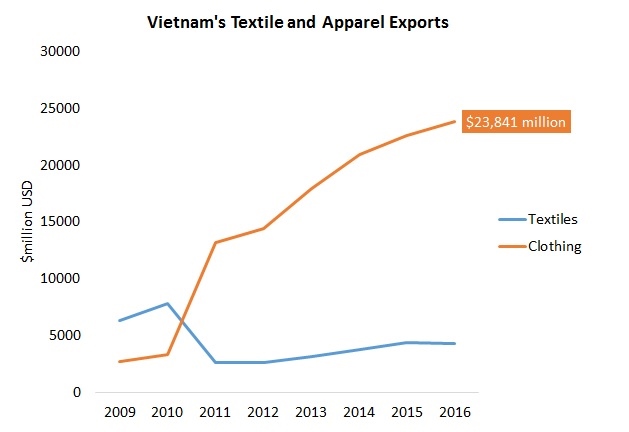

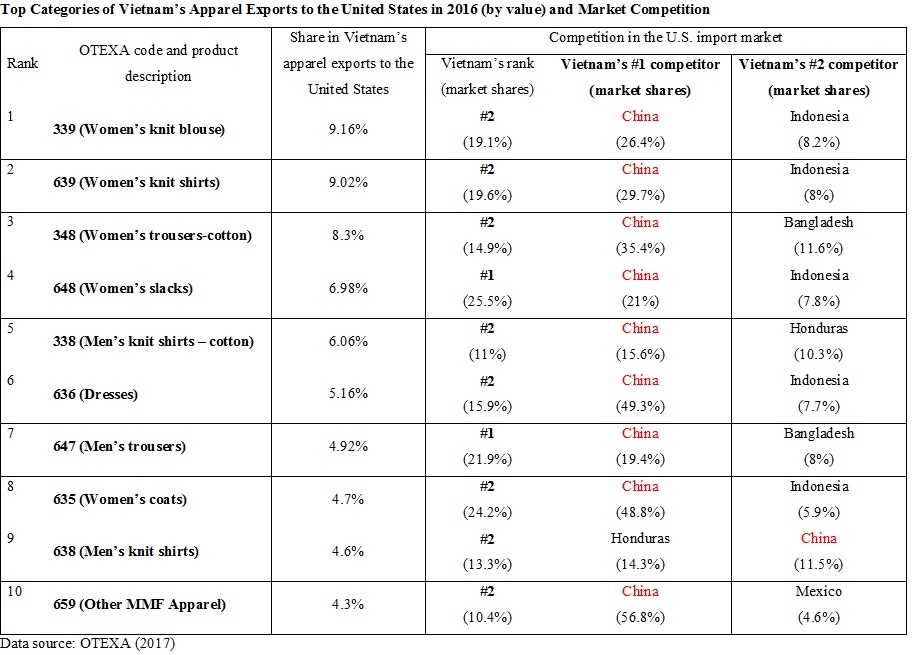

In 2016, Vietnam’s textile and clothing exports totaled $28 billion (84% were clothing), which represented 16.0% of Vietnam’s total merchandise exports. Globally, Vietnam was the world’s third largest apparel exporter in 2015, after China and Bangladesh (WTO, 2016).

The Vietnam Textile & Apparel Association (VITAS) expects Vietnam’s textile and clothing exports to enjoy an average 15% annual growth in the next four years and exceed $50 billion USD by 2020.

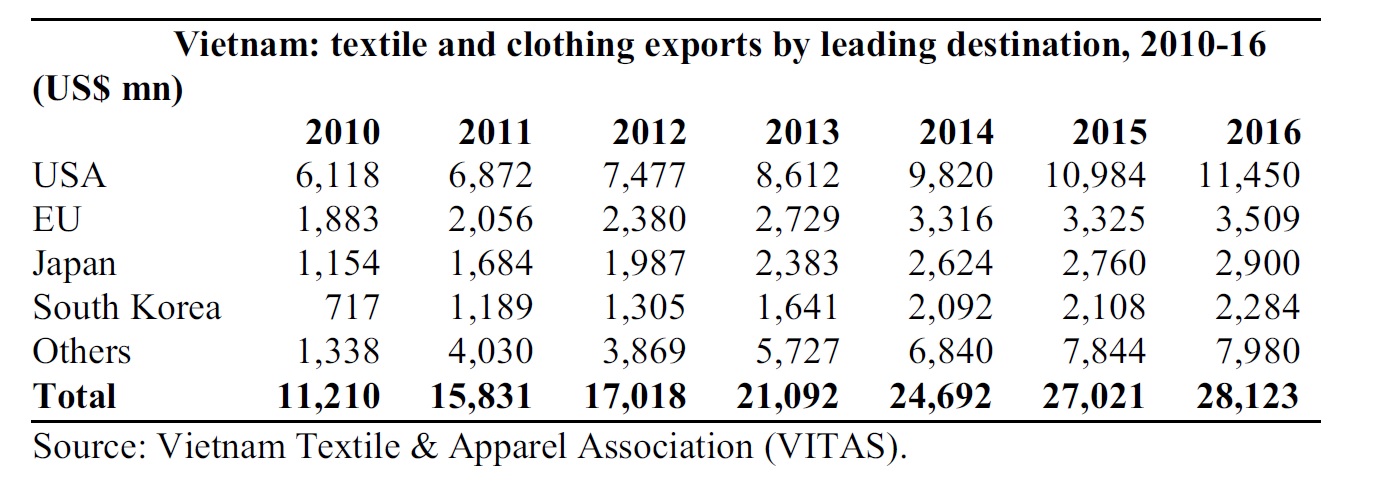

Vietnam’s textile and clothing exports went to around 180 countries. The United States is Vietnam’s top export market (around 40%), followed by the EU (around 12.5%), Japan (10.3%) and South Korea (8.1%).

Outlook of Sourcing from Vietnam by US Fashion Companies

According to the 2017 US Fashion Industry Benchmarking Study, Vietnam is the 2nd most used sourcing destination by respondents. Particularly, the most commonly adopted sourcing model is shifting from “China Plus Many” to “China Plus Vietnam Plus Many”:

China typically accounts for 30-50 percent of respondents’ total sourcing value or volume.

Vietnam typically accounts for 11-30 percent of companies’ total sourcing value or volume.

For the “many” part, each additional country (such as US, NAFTA members and CAFTA members, EU countries and members of AGOA) typically accounts for less than 10 percent of respondents’ total sourcing value or volume.

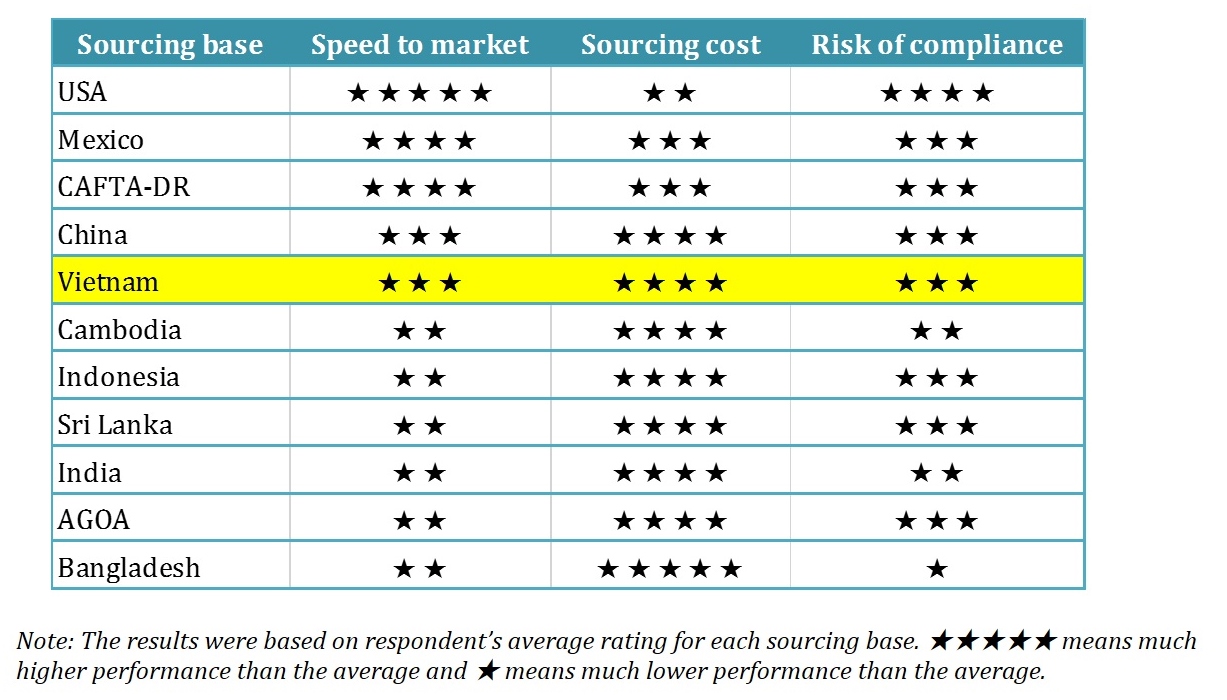

Respondents also see Vietnam overall a balanced sourcing destination, regarding “speed to market”, “sourcing cost” and “compliance risk”.

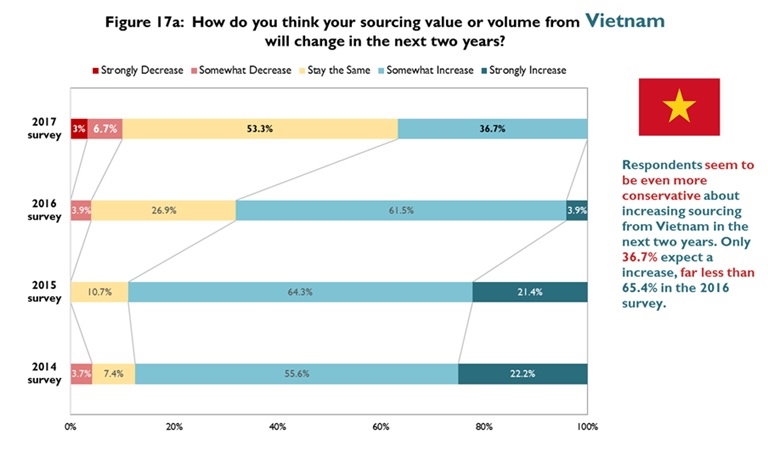

Additionally, U.S. fashion companies intend to source more from Vietnam through 2019, but imports may grow at a relatively slow pace, possibly due to the United States’ withdrawal from the Trans-Pacific Partnership (TPP) and the increasing labor costs in the country.

References:Textile Outlook International (2017); WTO (2017); UN Comtrade (2017)

While the majority of respondents remain confident about the five-year outlook for the U.S. fashion industry, the percentage of those who are “optimistic” or “somewhat optimistic” dropped to a record low since we began conducting this study in 2014. This change could be due to concerns about the “protectionist trade policy agenda in the United States” and “market competition in the United States from e-commerce,” the top two concerns this year.

The percentage of those who are “optimistic” or “somewhat optimistic” fell from 92.3 percent in 2016 to 71.0 percent in 2017, a record low since we began conducting this study in 2014. As many as 12.9 percent of respondents are “somewhat pessimistic” about the next five years, mostly large-scale retailers with more than 3,000 employees.

Despite the challenges, demand for human talent in the industry overall remains robust. This year, around 80 percent of respondents plan to hire more employees in the next five years, especially supply chain specialists, data scientists, sourcing specialists, and marketing analysts.

Cost is no longer one of the top concerns; respondents are less stressed about “increasing production or sourcing cost,” which slipped from #2 challenge in 2016 to #7 challenge in 2017. Only 34 percent rate the issue among their top five challenges this year, significantly lower than 50 percent in 2016 and 76 percent in 2015. Labor cost remains the top factor driving up sourcing cost in 2017.

Although U.S. fashion companies continue to seek alternatives to “Made in China,” China’s position as the top sourcing destination remains unshakable. Meanwhile, sourcing from Vietnam and Bangladesh may continue to grow over the next two years, but at a relatively slow pace.

91 percent of respondents source from China; while 100 percent sourced from China in our past three studies, China is still the top-ranked sourcing destination this year, and the percentage of those expecting to decrease sourcing from the country fell from 60 percent in 2016 to 46 percent this year—and many more expect to maintain their current sourcing value or volume from the country in the next two years.

Likely reflecting the United States’ withdrawal from the Trans-Pacific Partnership (TPP) and the expectation of increasing labor costs, only 36 percent of respondents expect to increase sourcing from Vietnam in the next two years, much lower than 53 percent who said the same in 2016.

Respondents are cautious about expanding sourcing from Bangladesh in the next two years, with only 32 percent expecting to somewhat increase sourcing While “Made in Bangladesh” enjoys a prominent price advantage over many other Asian suppliers, respondents view Bangladesh as the having the highest risk for compliance.

U.S. fashion companies continue to maintain truly global supply chains.

Respondents source from 51 countries or regions in 2017, close to the 56 in last year’s study.

57.6 percent source from 10+ different countries or regions in 2017, up from 51.8 percent in last year’s survey. In general, larger companies have a more diversified sourcing base than smaller companies. Additionally, retailers maintain a more diversified sourcing base than brands, importers/wholesalers, and manufacturers.

Around 54 percent expect their sourcing base will become more diversified in the next two years, up from 44 percent in 2016; among these respondents, over 60 percent currently source from more than 10 different countries or regions.

The most common sourcing model is shifting from “China Plus Many” to “China Plus Vietnam Plus Many.” The typical sourcing portfolio today is 30-50 percent from China, 11-30 percent from Vietnam, and the rest from other countries.

While Asia as a whole remains the dominant sourcing region for U.S. fashion companies, the Western Hemisphere is growing in popularity. This year, we see a noticeable increase in sourcing from the United States (70 percent, up from 52 percent in 2016) and countries in North, South, and Central Americas, which offer a shorter lead time and relatively lower risk of compliance.

Today, ethical sourcing and sustainability are given more weight in U.S. fashion companies’ sourcing decisions. Respondents also see unmet compliance (factory, social and/or environmental) standards as the top supply chain risk.

5 percent of respondents say ethical sourcing and sustainability have become more important in their company’s sourcing decisions in 2017 compared to five years ago.

100 percent of respondents currently audit their suppliers, including how suppliers treat their workers, suppliers’ fire safety, and suppliers’ building safety. The majority (93 percent) use third-party certification programs to audit, with a mix of announced and unannounced audits.

As many as 90 percent of respondents map their supply chains, i.e., keep records of name, location, and function of suppliers. More than half track not only Tier 1 suppliers, suppliers they contract with directly, but also Tier 2 suppliers, i.e. supplier’s suppliers. It is less common for U.S. fashion companies to map Tier 3 and Tier 4 suppliers though, which could be because of the difficulty of getting access to related information with such a globalized and highly fragmented supply chain.

Free trade agreements (FTAs) and trade preference programs remain underutilized, and several FTAs, including CAFTA-DR, are utilized even less this year than in previous years.

Of the 19 FTAs/preference programs we examined this year, only NAFTA is used by more than 50 percent of respondents for import purposes.

Even more concerning, some U.S. fashion companies source from countries/regions with FTAs/preference programs but, for whatever reason, do not claim the benefits. For example, as many as 38 percent and 6 percent of respondents, respectively, do not use CAFTA-DR and NAFTA when they source from these two regions.

Respondents unanimously oppose the U.S. border adjustment tax (BAT) proposal and call for the further removal of trade barriers, including restrictive rules of origin and high tariffs.

100 percent of respondents oppose a border adjustment tax; 84 percent “strongly oppose” it.

Respondents support initiatives to eliminate trade barriers of all kinds, from high tariffs to overcomplicated documentation requirements, to the restrictive yarn-forward rules of origin in NAFTA and future free trade agreements.

Respondents say the “complex standards on labeling and testing”, “complex rules for the valuation of goods at customs” and “administrative and bureaucratic delays at the border” are the top non-tariff barriers they face when sourcing today.

Several released negotiating objectives address textile and apparel (T&A) directly or are highly relevant to the sector:

Trade in Goods

Improve the U.S. trade balance and reduce the trade deficit with the NAFTA countries.

Maintain existing duty-free access to NAFTA country markets for U.S. textile and apparel products and seek to improve competitive opportunities for exports of U.S. textile and apparel products while taking into account U.S. import sensitivities.

Rules of Origin

Update and strengthen the rules of origin, as necessary, to ensure that the benefits of NAFTA go to products genuinely made in the United States and North America.

Ensure the rules of origin incentivize the sourcing of goods and materials from the United States and North America.

Establish origin procedures that streamline the certification and verification of rules of origin and that promote strong enforcement, including with respect to textiles.

-Establish origin procedures that streamline the certification and verification of rules of origin and that promote strong enforcement, including with respect to textiles.

Customs and Trade Facilitation

Provide for automation of import, export, and transit processes, including through supply chain integration; reduced import, export, and transit forms, documents, and formalities; enhanced harmonization of customs data requirements; and advance rulings regarding the treatment that will be provided to a good at the time of importation.

Comments:

Notably, reducing the trade deficit and bringing more manufacturing jobs back to the United States are at the core of the NAFTA’s renegotiating objectives. These two goals are also highly consistent with Trump’s rhetoric on his trade policy.

A dilemma facing the T&A sectoral negotiation is that the United States currently runs a robust trade surplus with Canada and Mexico for textiles: in 2016, the value of U.S. trade surplus (i.e. the value of exports minus the value of imports) totaled $680 million for yarns (up 56.7% from 1994), $4,342 million for fabrics (up 202.9% from 1994) and $1,461 million for made-up textiles (up 223.5% from 1994). Meanwhile, although the United States is in a trade deficit with NAFTA partners for apparel ($1,130 million in 2016), U.S. apparel imports from Canada and Mexico often contain textile inputs “Made in the USA” through the Western-Hemisphere supply chain. Blindly cutting the trade deficit on apparel ironically could affect the U.S. textile exports to the NAFTA region negatively.

Based on the released objectives, it seems unlikely that the NAFTA renegotiation will liberalize the yarn-forward rules of origin for textile and apparel. On the contrary, USTR could review the current exceptions to the yarn-forward rules, including the tariff preference levels (TPL) and some special regimes such as the 9802 program related to fabric sourcing to strengthen the manufacturing base and create MANUFACTURING jobs in the United States. Recognizing the competing arguments between the U.S. textile industry and the apparel industry (fashion brands and retailers) regarding the necessity and impact of these exceptions, USTR also needs more inputs of how companies use exceptions like the TPL in sourcing and why they use them.

Other than the rules of origin, trade facilitation and customs enforcement will be another major agenda related to the T&A sector in the NAFTA renegotiation. Elements from the newly enforced Trade Facilitation and Trade Enforcement Act of 2015 could be added to the updated NAFTA.

A positive aspect of the NAFTA T&A sectoral negotiation is that all parties alongside the supply chain, from U.S. cotton growers, textile mills to apparel retailers and brands recognize the value of NAFTA and no one calls for pulling out of the agreement. It is also a consensus view of the U.S. T&A industry that NAFTA renegotiation should “do no harm”, i.e. strengthening rather than weakening the current supply-chain partnership between NAFTA members. Additionally, stakeholders in the U.S. T&A industry unanimously support keeping the renegotiation trilateral, but agree to use bilateral provisions to address some particular concerns.

The NAFTA renegotiation may officially start on August 17 or 18, 2017. However, Time is the enemy of the NAFTA renegotiation. While there is a strong incentive for all parties to finish the negotiation by the end of 2017 given the upcoming U.S. mid-term election and the Mexican presidential election in 2018, the ambitious renegotiation agenda makes it extremely challenging to meet that goal. Risks are still there that Trump may pull the United States out of NAFTA should he lose patience for the renegotiation. Notably, Trump’s dislike of NAFTA is real.

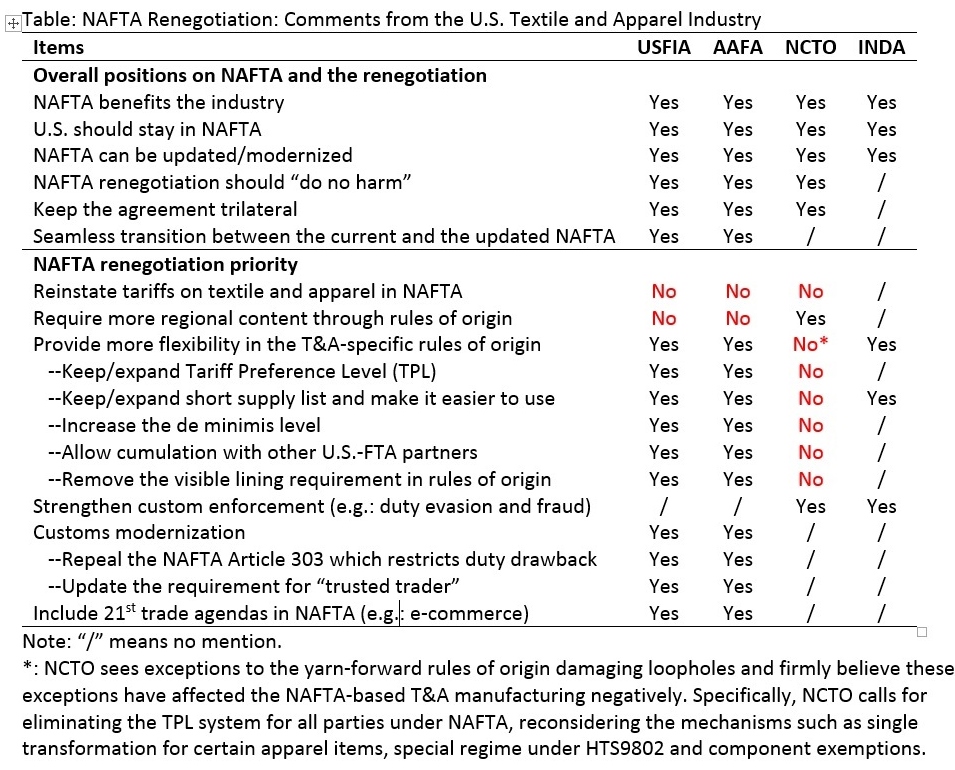

This week, several leading U.S. textile and apparel industry associations submitted their comments to the Office of the United States Trade Representative (USTR) regarding the renegotiation objectives of the North American Free Trade Agreement (NAFTA). Below is a summary of these organizations’ viewpoints based on their submissions:

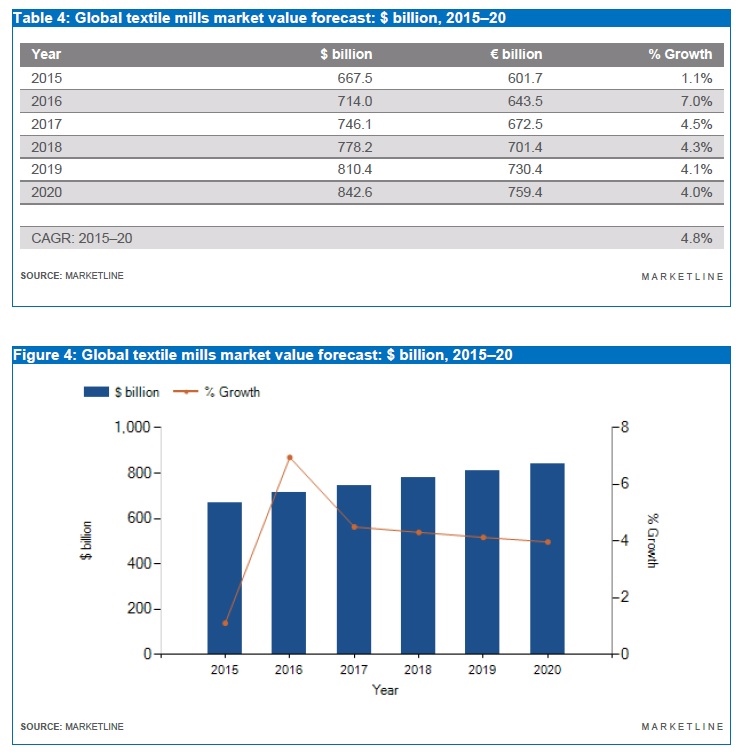

The textile mills market includes yarns and fabrics. The market value includes domestic production plus imports minus exports, all valued at manufacturer prices.

The value of the global textile mills market totaled $667.5 billion in 2015 (around 83.1% were fabrics and 16.9% were yarns), up 1.5% from a year earlier. The compound annual growth rate of the market was 4.4% between 2011–15. Asia-Pacific accounted for 54.6% of the global textile mills market value in 2015 and Europe accounted for a further 20.6% of the market.

The global textile mills market is forecast to reach $842.6 billion in value in 2020, an increase of 26.2% since 2015. The compound annual growth rate of the market in the period 2015–20 is predicted to be 4.8%.

Apparel market

The apparel market covers all clothing except leather, footwear, and knitted items as well as other technical, household, and made-up products. The market value includes domestic production plus imports minus exports, all valued at manufacturer prices.

The value of the global apparel market totaled $842.7 billion in 2016 (estimated), up 5.5% from a year earlier. The compound annual growth rate of the market was 5.2% between 2012–16. Asia-Pacific accounted for 60.7% of the global apparel market value in 2016 and Europe accounted for a further 15.0% of the market.

The global apparel market is forecast to reach $1,004.6 billion in value in 2021, an increase of 19.2% since 2016. The compound annual growth rate of the market in the period 2015–20 is predicted to be 3.6%.

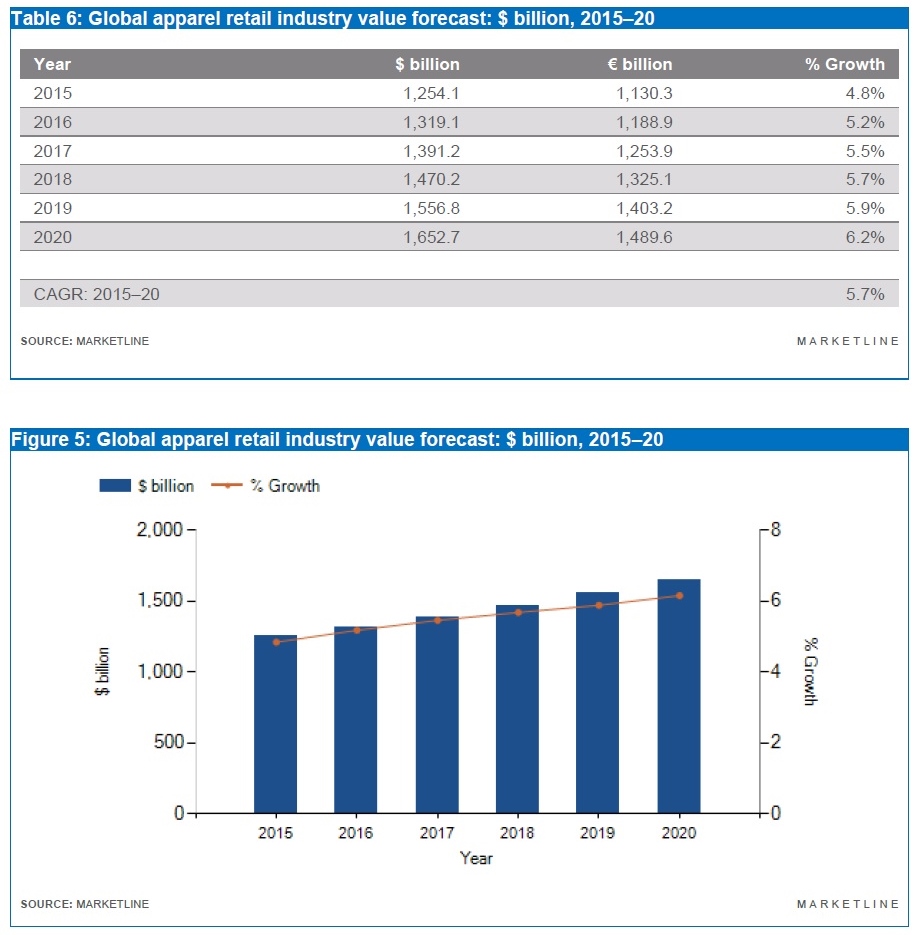

Apparel retail market

The apparel retail industry consists of the sale of all menswear, womenswear and childrenswear. The industry value is calculated at retail selling price (RSP), and includes all taxes and duties.

The value of the global apparel retail market totaled $1,254.1 billion in 2015 (52.9% womenswear, 31.2% menswear and 15.9% childrenswear), up 4.8% from a year earlier. The compound annual growth rate of the market was 4.5% between 2011–15. Asia-Pacific accounted for 36.8% of the global apparel retail market in 2015, followed by Europe (27.8%) and the United States (24.0%).

The global apparel retail market is forecast to reach $1,652 billion in value in 2020, an increase of 31.8% since 2015. The compound annual growth rate of the market in the period 2015–20 is predicted to be 5.7%.

A New York Times article back in August 2015 suggests that “yarn production costs in China are now 30 percent higher than in the United States” because of savings in raw and auxiliary material. The article believes the cost difference is why some Chinese textile companies are coming to build factories in the United States, such as Keer Group’s cotton mill in South Carolina.

However, in a recent interview with China Textile News, Chairman of the Cixi Jiangnan Chemical Fiber Co (Cixi) provides a different cost sheet (above). In September 2013, Cixi invested a $45million polyester staple fiber mill in South Carolina. Because nearly 80% of Cixi’s outputs are sold outside of China, and the United States is its single largest export market, the investment intends to help the company maintain its presence in the U.S. market and substantially save transportation cost.

According to Cixi, it is a misunderstanding that making textiles in the United States is cheaper than in China. Although moving factories to the United States may help Chinese companies save money in land, electricity, natural gas, and logistics, it will significantly increase the costs in purchasing manufacturing equipment, building factories and managing daily operation of the company. Additionally, culture and language barriers, as well as labor policy in the United States, could also become critical challenges facing Chinese investors. Cixi admits that to keep its U.S. factory running smoothly, members of its management team all come from China.

#1 Why or why not the textile and apparel industry should get involved in policy advocacy?

#2 Do you think the current U.S. trade policy reflects the interests of the U.S. textile and apparel industry? Please provide detailed examples.

#3 It is said that “trade is a way for countries to strengthen partnerships and alliances, promote peace and trust between the cooperating nations, and help other countries in need.” Do you think this principle still holds today?

#4 President Trump proposes an “America First Trade Policy,” which intends to encourage more “buy America” and reduce the U.S. trade deficit. How should President Trump respond if other countries adopt a similar approach by proposing initiatives such as “EU first trade policy,” “China first trade policy” and “Mexico first trade policy”?

#5 What do you take away from Case Study 2 regarding the making of U.S. trade policy?

Since its taking effect in 1995, NAFTA, a trade deal between the United States, Mexico, and Canada, has raised heated debate regarding its impact on the U.S. economy. President Trump has repeatedly derided NAFTA, describing it as “very, very bad” for U.S. companies and workers, and he promised during his campaign that he would remove the United States from the trade agreement if he could not negotiate improvements.

The U.S. textile and apparel (T&A) industry is a critical stakeholder of the potential policy change, because of its deep involvement in the regional T&A supply chain established by the NAFTA. Particularly, over the past decades, trade creation effect of the NAFTA has significantly facilitated the formation of a regional T&A supply chain among its members. Within this supply chain, the United States typically exports textiles to Mexico, which turns imported yarns and fabrics into apparel and then exports finished apparel back to the United and Canada for consumption.

So what will happen to the U.S. T&A industry if NAFTA no longer exists? Here is what I find*:

First, results show that ending the NAFTA will significantly hurt U.S. textile exports. Specifically, the annual U.S. textile exports to Mexico and Canada will sharply decline by $2,081 million (down 47.7%) and $351 million (down 14%) respectively compared to the base year level in 2015.Although U.S. textile exports to other members of the Central America Free Trade Agreement (CAFTA-DR), will slightly increase by $42 million (up 1.5%), the potential gains will be far less than the loss of exports to the NAFTA region.

Second, results show that ending the NAFTA will significantly reduce U.S. apparel imports from the NAFTA region. Specifically, annual U.S. apparel imports from Mexico and Canada will sharply decrease by $1,610 million (down 45.3%) and $916 million (down 154.2%) respectively compared to the base year level in 2015 (H2 is supported). However, ending the NAFTA would do little to curb the total U.S. apparel imports, largely because U.S. companies will simply switch to importing more apparel from other suppliers such as China and Vietnam.

Third, ending NAFTA will further undercut textile and apparel manufacturing in the United States rather than bring back “Made in the USA.” Specifically, annual U.S. textile and apparel manufacturing will decline by $1,923 million (down 12.8%) and $308 million (down 3.0%) respectively compared to the base year level in 2015 (H3 is supported). Weaker demand from the NAFTA region is the primary reason why U.S. T&A manufacturing will suffer a decline.

These findings have several important implications. On the one hand, the results suggest that the U.S. T&A will be a big loser if the NAFTA no longer exists. Particularly, ending the agreement will put the regional T&A supply chain in jeopardy and make the U.S. textile industry lose its single largest export market—Mexico. On the other hand, findings of the study confirm that in an almost perfectly competitive market like apparel, raising tariff rate is bound to result in trade diversion. With so many alternative suppliers out there, understandably, ending the NAFTA will NOT increase demand for T&A “Made in the USA,” nor create more manufacturing jobs in the sector. Rather, Asian textile and apparel suppliers will take away market shares from Mexico and ironically benefit most from NAFTA’s dismantlement.

*Note: The study is based on the computable general equilibrium (CGE) model developed by the Global Trade Analysis Project (GTAP). Data of the analysis came from the latest GTAP9 database, which includes trade and production data of 57 sectors in 140 countries in 2015 as the base year. For the purpose of the study, we assume that if NAFTA no longer exists, the tariff rate applied for T&A traded between NAFTA members will increase from zero to the normal duty rate (i.e. the Most-Favored-Nation duty rate) in respective countries.

In its latest trade statistics and outlook report, the World Trade Organization (WTO) forecasts the world merchandise trade volume to grow within a range of 1.8-3.6% in 2017 (on average 2.4%). This growth rate is slightly up from a very weak growth of 1.3% in 2016. WTO expects trade growth to further pick up to 2.1-4% in 2018.

On the positive side, the global GDP growth is expected to rebound to 2.7% in 2017 from 2.3% in 2016, which will contribute to the expansion of world trade. Notably, WTO expects emerging economies to return to modest economic growth in 2017. However, WTO sees policy uncertainty, including the imposition of restrictive trade measures and monetary tightening, a main risk factor to world trade this year.

WTO also noted that since the financial crisis, the ratio of trade growth to GDP growth has fallen to around 1:1. And 2016 marked the first time since 2001 that this ratio has dropped below 1, to a ratio of 0.6:1. Historically, the volume of world merchandise trade has tended to grow about 1.5 times faster than world output. WTO is cautiously optimistic that the ratio will partly recover in 2017, but the ratio will remain a cause for concern.

At the press conference, Trump Administration’s trade policy receives significant attention. But according to Roberto Azevêdo, Director-General of WTO, “just an overall statement of the intention to go one particular way or another, does not tell us what the trade policy is and does not tell us what the impact of that trade policy will be. Instead, the devil is in the details”. Roberto said he is waiting to see Trump’s new trade team in place (for example, the new US Trade Representative) and he looks forward to the meaningful dialogues with the team to know more details and clarity of U.S. trade policy. Until then, any comments on the impact of Trump Administration’s trade policy would be just speculations.

During the talk, Gail made a few comments regarding trade policy in the Trump administration:

First, Gail believes that the existing U.S. free trade agreements (FTAs), trade preference programs (PTAs) and the U.S. commitments at the World Trade Organization (WTO) are unlikely to be undone by President Trump because retaliatory actions from other trading partners would be inevitable.

Second, regarding the North American Free Trade Agreement (NAFTA), Gail doesn’t think the proposed renegotiation would threaten the benefits presently enjoyed by the U.S. textile and apparel industry. Gail also thinks the Central America Free Trade Agreement (CAFTA-DR) is a lifeline for the U.S. domestic textile manufacturing sector. Notably, NAFTA and CAFTA-DR together account for almost 70% of U.S. yarn and fabric exports.

Third, as observed by Gail, Wilbur Ross, the Commerce Secretary, has been given an expanded role in trade in the Trump Administration. Gail believes Ross’s appointment is likely to bode well for NAFTA and CAFTA-DR on textiles because Ross until recently owned the International Textile Group (ITG), which has significant investments in Mexico and relies heavily on CAFTA-DR for its textile sales.

However, Gail doesn’t think concentrating on trade deficits to define trade policy is a very “good method” of navigating the trade world. Interesting enough, last time when the U.S. trade deficit significantly shrank was during the 2008 financial crisis.

Gail is also a strong advocator of sustainability in the textile and apparel sector. She believes that trade programs can play a vital role in encouraging sustainable development, improving labor practices and facilitating sustainable regional supply chains. According to Gail, powerful the labor provisions in trade programs can be if strong incentives are coupled with a credible threat of rapid enforcement – little evidence of effectiveness if only one (or fewer) of these conditions is met. However, comparing with enforcing labor provisions, Gail finds promoting and enforcing environmental sustainability standards through trade agreements is much more complex in the textile and apparel sector and will require creativity and strong participation from private sectors and consumers.

Before the public lecture, Gail visited FASH455 and had a special discussion session with students on topics ranging from the textile and apparel rules of origin in TPP, NAFTA renegotiation, AGOA renewal and state of the U.S. textile and apparel industry.

A fact-checking review of trade statistics in 2016 of a total 167 categories of T&A products categorized by the Office of Textiles and Apparel (OTEXA) suggests that textile and apparel (T&A) “Made in China” have no near competitors in the U.S. import market. Specifically, in 2016:

Of the total 11 categories of yarn, China was the top supplier for 2 categories (or 18%);

Of the total 34 categories of fabric, China was the top supplier for 25 categories (or 74%);

Of the total 106 categories of apparel, China was the top supplier for 88 categories (or 83%);

Of the total 16 categories of made-up textiles, China was the top supplier for 12 categories (or 68%);

In comparison, for those Asian T&A suppliers regarded as China’s top competitors:

Vietnam was the top supplier for only 5 categories of apparel (less than 5% of the total);

Bangladesh was the top supplier for only 2 categories of apparel (less than 2% of the total)

India was the top supplier for 2 categories of fabric (9% of the total), one category of apparel (1% of the total) and 5 categories of made-up textiles (41.7% of the total)

Notably, China not only was the top supplier for many T&A products but also held a lion’s market shares. For example, in 2016:

For the 34 categories of fabric that China was the top supplier, China’s average market shares reached 41%, 23 percentage points higher than the 2nd top suppliers for these categories

For the 88 categories of apparel that China was the top supplier, China’s average market shares reached 53%, 38 percentage points higher than the 2nd top suppliers for these categories.

For the 16 categories of made-up textiles that China was the top supplier, China’s average market shares reached 57%, 40 percentage points higher than the 2nd top suppliers for these categories.

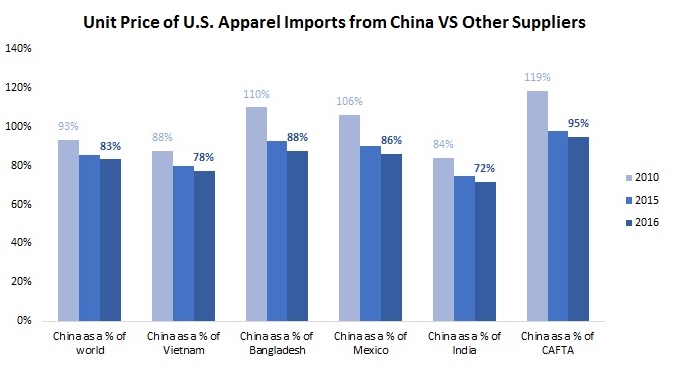

It is also interesting to see that despite the reported rising labor cost, T&A “Made in China” are NOT becoming more expensive. On the contrary, the unit price of U.S. T&A imports from China in 2016 was 6.8% lower than a year earlier, whereas over the same period the unit price for U.S. T&A imports from rest of the world only declined by 2.9%.

Furthermore, T&A “Made in China” are demonstrating even bigger price competitiveness compared with other suppliers to the U.S. market. For example, in 2016, the unit price of “Made China” was only 78% of the price of “Made in Vietnam” (in 2012 was 89%), 88% of “Made in Bangladesh” (in 2012 was 100%), 86% of “Made in Mexico” (in 2012 was 103%) and 72% of “Made in India” (in 2012 was 81%).

Are the results surprising? How to explain China’s demonstrated price competitiveness despite its reported rising labor cost? What’s your outlook for the future of China as a sourcing destination for U.S. fashion brands and retailers? Please feel free to share your views.

This video is a great reminder of the impact of our fashion apparel industry, in particular through trade and sourcing. One key learning objective of FASH455 is to help students get aware of those critical global agendas that are highly relevant to the textile and apparel sector.

Discussion Question: After watching the video, do you have any new thoughts about how you can contribute to the building of a better world as a FASH major?

Do you think the U.S. trade deficit is a problem or not? Please feel free to share your thoughts based on our lectures, the video above as well as a recent op-ed written by Peter Navarro (Director of the White House National Trade Council) for the Wall Street Journal.

Free trade agreements (FTAs) are arrangement among two or more countries under which they agree to eliminate tariffs and non-tariff (NTB) barriers on trade among themselves (Cooper, 2014). Theoretically, companies shall be interested in increasing imports from FTA regions because of the duty-free treatment (i.e., the trade creation effect). Particularly, not paying import tariff duty can be a great cost advantage for textile and apparel (T&A) companies given the fact that the average US import tariff rate was still as high as 8% for textiles and 11.6% for apparel in 2016 (WTO, 2017).

Despite the potential benefit of using FTAs, data from the Office of Textiles and Apparel show that 85.7% of US T&A imports came from non-FTA regions in 2016. Interesting enough, although more FTAs have taken effect in the United States, T&A imported under FTA as a percent of total T&A imports dropped from 15.1% in 2008 to 14.3% in 2016.

Among the FTAs in force, the North American Free Trade Agreement (NAFTA) and the Dominican-Republic-Central America Free Trade Agreement (CAFTA-DR) altogether accounted for 75.9% of the value of total U.S. T&A imports under FTAs in 2016.

Statistics further reveal that sometimes companies did not claim duty free benefits of FTAs even though they imported T&A from the FTA region. For example, in 2016 about 29.9% of U.S. T&A imports from South Korea, 24.3% from CAFTA-DR and 16.3% from NAFTA and 12.9% from Columbia did not enjoy the duty free treatment granted by the respective FTAs.

Some industry experts say the complex T&A rules of origin is a major factor why US T&A companies are not using FTAs enough. According to the Office of Textiles and Apparel (OTEXA), there are more than 20 different tariff lines dealing with various T&A rule of origin situations under respective FTAs.

Additionally, U.S. T&A importers seem to use the “short supply list” mechanism–an exception to the yarn forward rules of origin under FTAs, more actively. For example, in 2016 around 2.4% of US T&A imports under FTAs took advantage of the “short supply list” mechanism, increased from only 1.2% in 2008. Similarly, a record high of 6.2% of U.S. T&A imports under the CAFTA-DR used the short supply list in 2016.

The following results are preliminary findings from the Cooperative Congressional Election Study (CCES) 2016 survey. The survey was administrated by YouGov/Polimetrix and conducted from September to October 2016.

Acknowledgement:

Thanks to the University of Delaware Office of the Provost, Social Science Data Analytics Initiative, and Center for Political Communication in support of the data collection. For questions about the data, please contact Dr. Sheng Lu (shenglu@udel.edu).

From left to right: Julia Hughes (president of USFIA), Auggie Tantillo (president & CEO of NCTO) and Robert Antoshak (Managing Director of Olah Inc., moderator)

Auggie Tantillo: Pleased and excited to see the discussion on the possibility of bringing back/expanding manufacturing in the United States. Still the United States produces $65—70 billion worth of textiles annually, which support many manufacturing jobs in the sector. The U.S. textile industry also makes around $2 billion investment annually (updating machines and equipment). We need to acknowledge the baseline value of manufacturing in the United States.

Border Adjustment Tax(BAT)

Julia Hughes: BAT is a complicated issue. However, if the current BAT proposal is adopted, it will raise the retail price (meaning ordinary US consumers will have to pay more) and appreciate the U.S. dollar (meaning U.S. exports will get hurt). This is why USFIA along with 100+ companies and industry associations opposes any BAT.

Auggie Tantillo: NCTO strongly believes that updating the tax structure in the United States is long overdue. NCTO welcomes a serious look at the BAT proposal, since the United States is the only major economy in the world that does not adopt BAT. The United States doesn’t need to run such a high trade deficit. Instead, we need to make the tax structure supporting the U.S. manufacturing base.

North American Free Trade Agreement (NAFTA)

Julia Hughes: NAFTA is 20 years’ old and it can be improved. However, raising import tax (tariff) is NOT a good idea. NAFTA supports the Western-Hemisphere supply chain, which is critical for the U.S. textile and apparel industry. We need to defend this supply chain.

Auggie Tantillo: NAFTA works and benefits its members on all sides of the border, including the United States. NCTO supports the continuation of NAFTA as well as to update and modernize the agreement as necessary.

Yarn-forward Rules of Origin (RoO)

Julia Hughes: Apparel is a global industry and apparel supply chain needs to be nimble. The yarn-forward RoO prevents apparel companies and retailers from fully enjoying the duty-free benefits under a free trade agreement (FTA) since not always the FTA region makes the needed products or their textile components. Exceptions to the yarn-forward rules such as the tariff preference level (TPL), provide necessary flexibility.

Auggie Tantillo: The yarn-forward RoO has been a great success and we need to keep it (in existing and future trade agreements). The only things that need to be improved is the exception to the yarn-forward RoO (such as short supply list and trade preference level). RoO is supposed to keep benefits of a free trade agreement to its members only, yet these exceptions create loopholes and cause damages (to the U.S. textile industry).

On China

Julia Hughes: We need China, which still provides 40% of textiles and apparel consumed in the United States. It will be a disaster to trigger a trade war between the two countries.

Auggie Tantillo: We need to better help the Western-Hemisphere producers (in competing with textile and apparel made in China). China’s 40%+ market shares in the U.S. textile and apparel import market are not all based on its genuine competitiveness. Rather, China’s unfair trade practices such as IPR violation, government subsidy and unacceptable factory working conditions & environmental practices are of grave concerns.

Trans-Pacific Partnership (TPP)

Julia Hughes: TPP is not dead. On the other hand, countries around the world are actively negotiating new bilateral/regional free trade agreements. The United States doesn’t want to be left behind.

Auggie Tantillo: TPP is “in deep hibernation”, but trade agreement will never be really dead. It is still hopeful that TPP will come back later—but very likely to be in a different form, such as bilateral trade agreements. To be noted, many TPP members have already established bilateral/regional trade agreements with the United States.

Discussion questions: 1) Why do you think Julia Hughes and Auggie Tantillo disagree on many trade issues? On which topics they actually agree with each other and why? 2) What’s your response to Julia Hughes and Auggie Tantillo’s comments on trade issues above? 3) Based on the panel discussion, why do you think textile and apparel companies need to care about trade policy? Please feel free to share your views.