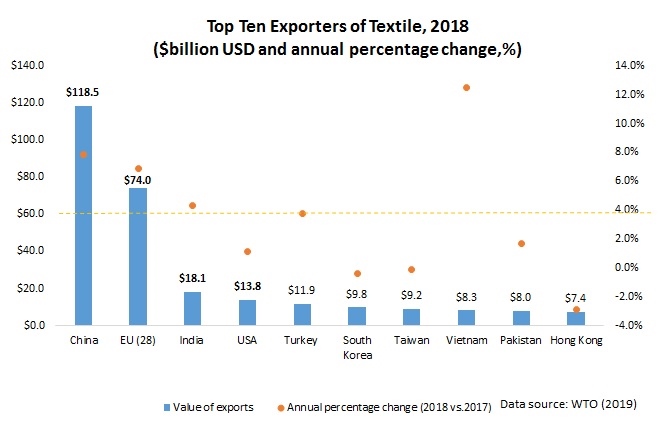

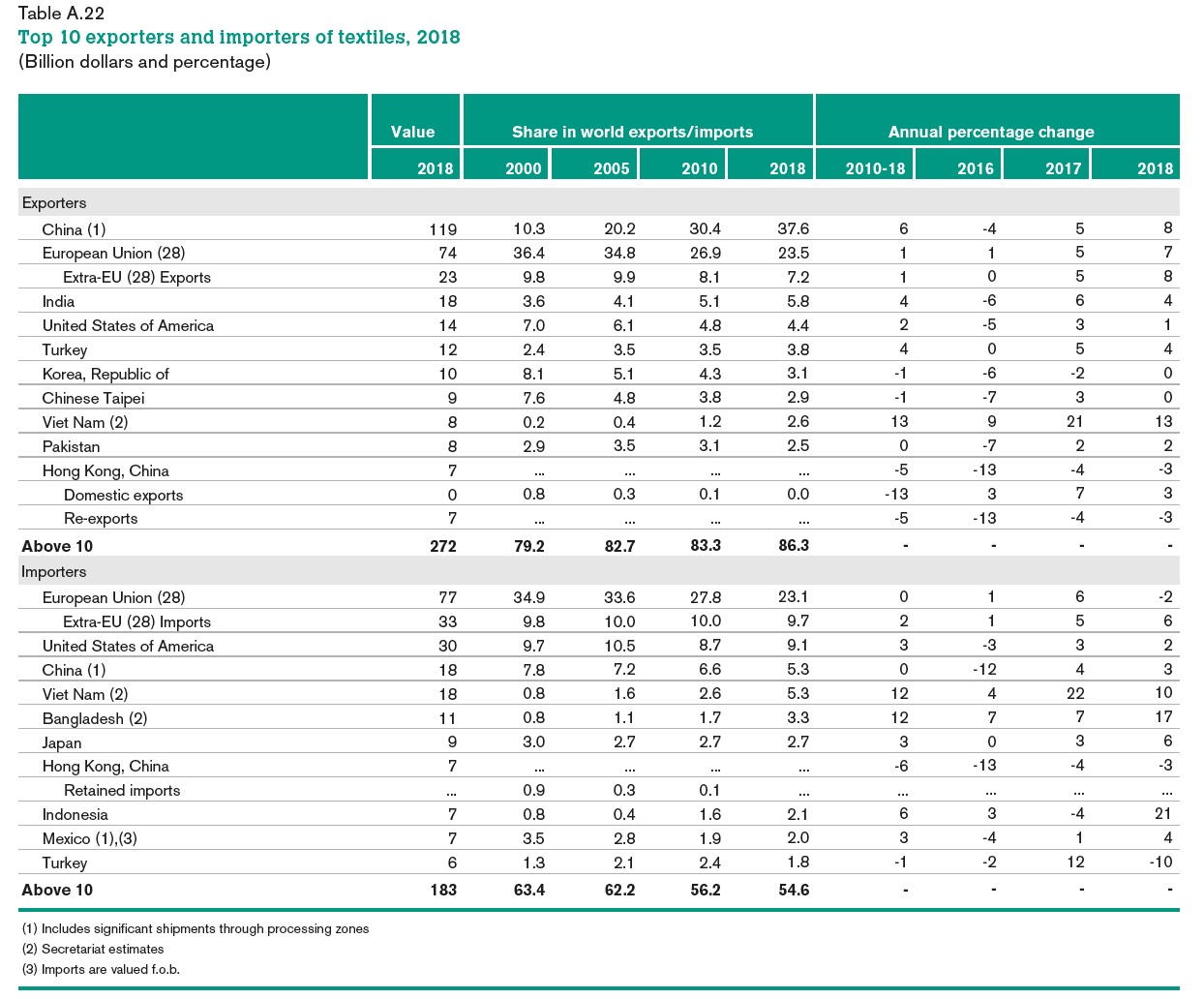

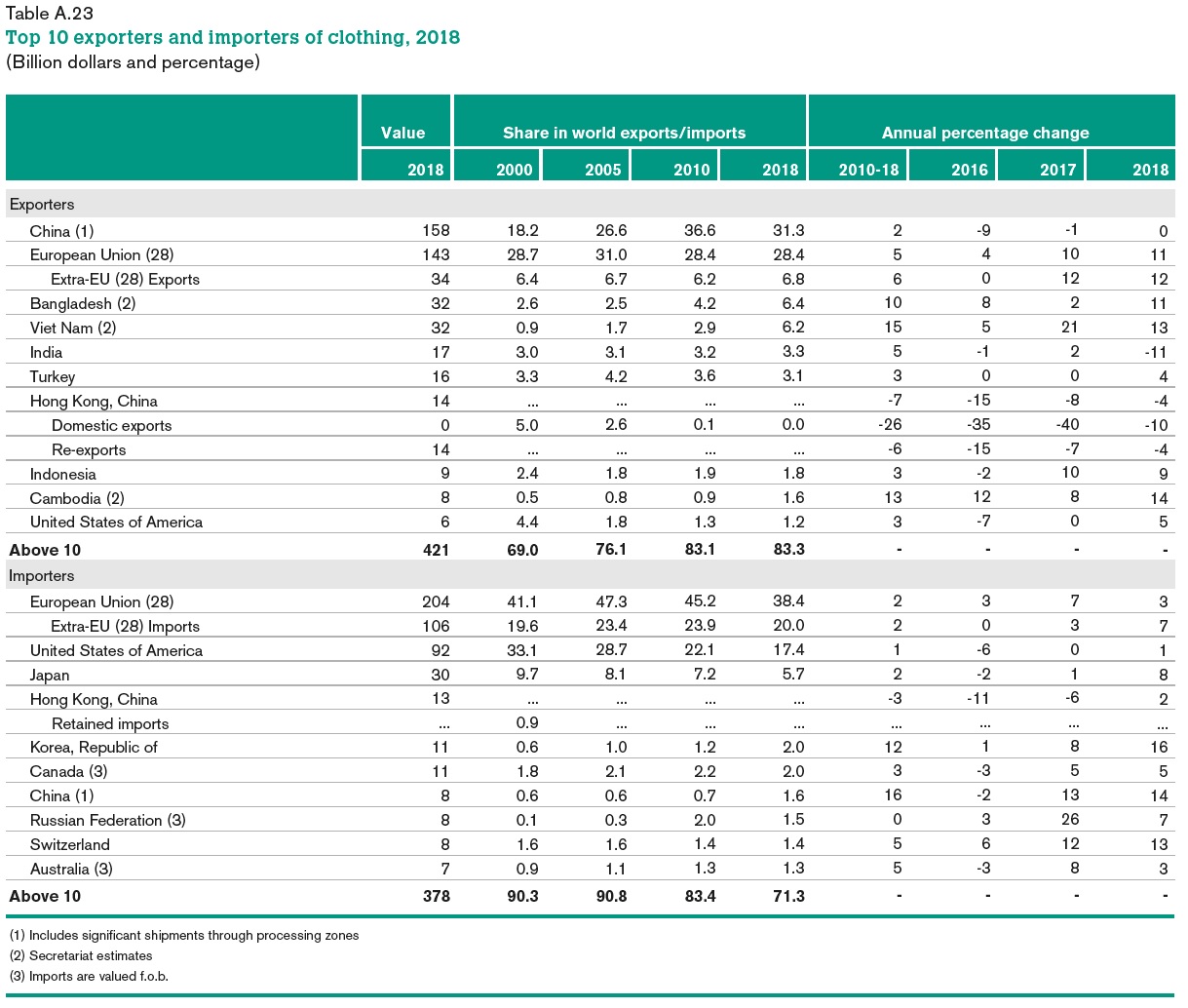

Patterns of world textile and apparel trade

#1 Based on the readings, why or why not do you think Africa is on the right track to become the next hub for apparel sourcing for western fashion brands?

#2 Based on the readings, do you think that any of the countries/regions discussed can become the “next China?” If so, what are the challenges faced by these exporters that have been gaining market shares (such as Vietnam and Bangladesh)?

#3 Why is Asian companies investing the most into the apparel industry in Sub Saharan Africa (SSA) rather than U.S. or EU investors? Notably, the African Growth and Opportunity Act (AGOA) is a trade preference program between the U.S. and SSA countries.

#4 If the punitive tariffs on Chinese goods are removed next year, why or why do you think U.S. retailers will increase apparel sourcing from China again?

#5 To which extent do you think the comparative advantage theory can explain the evolving world textile and apparel trade patterns?

#6 What policies or strategies could the US government use to convince companies to invest in the Sub-Saharan African region instead of countries like China and Vietnam?

Debate on used clothing trade

#7 Did you feel that the United States really explored every and any possible solution before deciding to suspend Rwanda’s eligibility under the AGOA? If not, what more could they have done or done differently?

#8 The US-EAC trade dispute on used clothing import ban is a very multilayered matter, which can be broken down with the help of trade preference programs. How can we improve the effectiveness of these trade preference programs and revolutionize them to become more significant in today’s economy?

#9 EAC countries are having a difficult time developing their local textile and apparel industry due to the large amounts of used clothing being imported and even proposed a high tariff to lower the amount of clothing being imported. Do you believe the ban on used clothing is the only option they have left for economic growth? If not, what are some ideas of ways they can grow their economy?

#10 The EAC countries have shown their unwillingness to used clothing trade. However, the US has presented that they are indifferent to regulate the used clothing trade as they are one of the biggest used clothing exporters. Are there any solutions to achieve the win-win situation on used clothing trade?

#11 The used clothing ban is put in place in order to develop the apparel and textile industry, but there needs to be more education for countries on sustainability. There is a big stigma about used clothing that needs to be abolished as well. An alternative to this ban is allowing used clothing, but also creating new clothing more sustainably so apparel and textile companies can profit. What are some other sustainable alternatives that benefit both sides?

#12 Given the debate on used clothing trade and its impact on East African nations, will you continue to donate used clothing? Why or why not?

[For FASH455: 1) Please mention the question number in your comments; 2) Please address at least TWO questions in your comments]