#1: Is the sole benefit of globalization helping us get cheaper products? How to convince US garment workers who lost their jobs because of increased import competition that they benefit from globalization also?

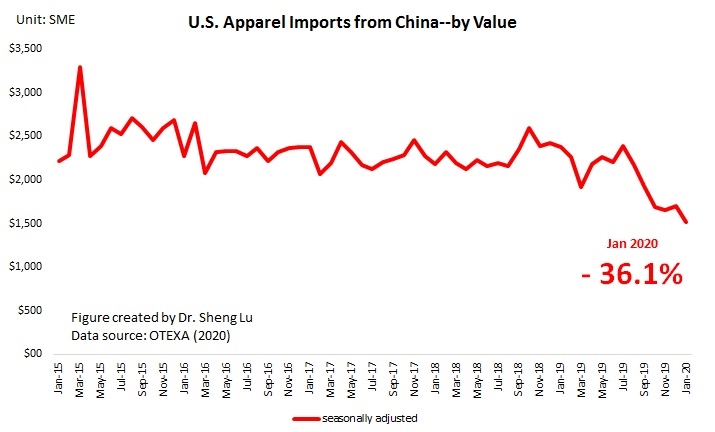

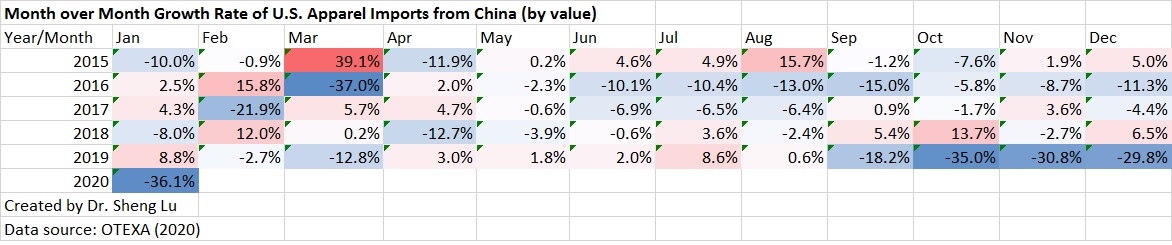

#2 How to explain the phenomenon that US apparel imports from China continue to rise despite the tariff war? Do you think the tariff war is a wrong strategy or a good strategy implemented at the wrong time given COVID?

#2: In the class, we mentioned that major driving forces of globalization include economic growth, lowered trade and investment barriers, and technology advancement. What will be the primary driving forces of globalization or deglobalization in the post-COVID world, and why?

#3: Based on the reading “U.S.-China Trade War Still Hurting Ohio Family-Owned Business,” what results of the US-China tariff war are expected and unexpected? What is your recommendation for the Biden administration regarding the Section 301 tariff exclusion process and why?

#4: We say textile and apparel is a global sector. How does the US-China tariff war affect textile and apparel producers and companies in other parts of the world? Why?

#5: From this week’s readings, why do we say textile and apparel trade and sourcing involve economic, social, and political factors and implications? Please provide 1-2 specific examples from the articles to support your viewpoints.

(Welcome to our online discussion. For students in FASH455, please address at least two questions and mention the question number (#) in your reply)