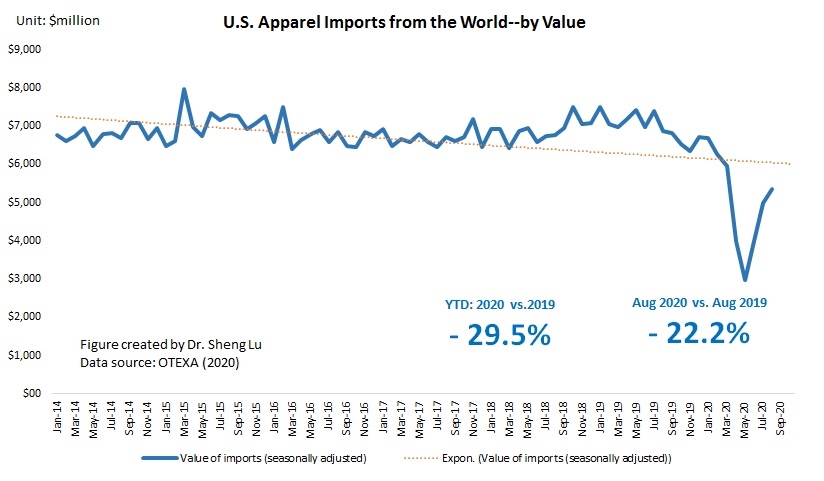

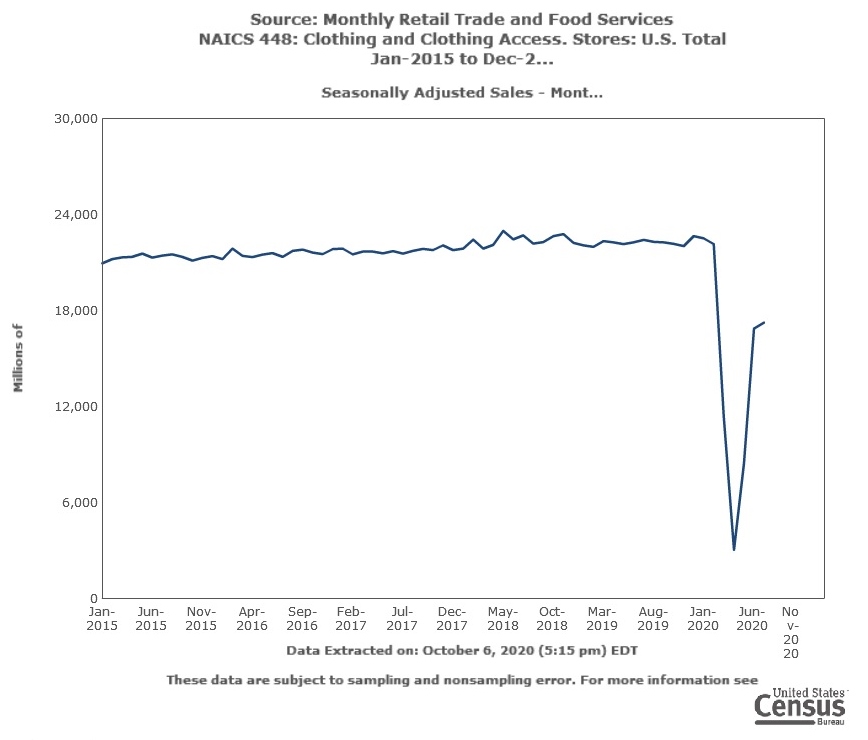

First, U.S. apparel imports continue to rebound thanks to consumers’ robust demand. The value of U.S. apparel imports in August 2020 went up by 7.6% from July 2020 (seasonally adjusted), a new record high since March 2020 when COVID-19 broke out in the States. As of August 2020, the volume of U.S. apparel imports has recovered to around 80% of the pre-coronavirus level. This result echoes the trend of U.S. apparel retail sales (NAICS 448), which also indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports hopefully will last for another 1-2 months.

Nevertheless, between January and August 2020, the value of U.S. apparel imports decreased by almost 30% year over year, which has been MUCH worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

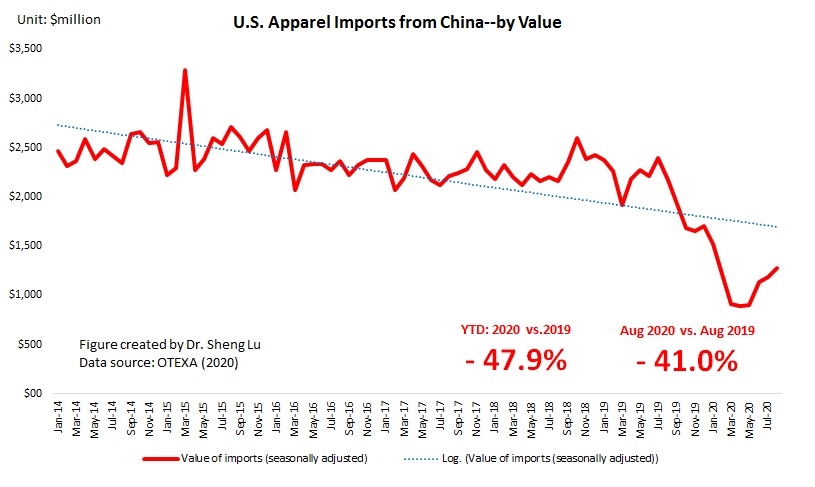

Second, no evidence suggests that U.S. fashion companies are giving up China as one of their essential apparel-sourcing bases. Notably, since May 2020, China had quickly regained its position as the top apparel supplier to the U.S. market. From June to August 2020, China’s market shares have stably stayed at around 27-28% in value and 40-42% in quantity.

Some industry sources show that “Made in China” enjoys two notable advantages that other apparel supplying countries cannot catch up in the short term. 1) unparalleled production capacity, meaning importers can source almost all products in any quantity from China vs. more limited production capacity (both in terms of variety and volume) in other alternative sourcing destinations. 2) China can mostly produce textile raw material locally vs. many apparel exporting countries still rely heavily on imported yarns and fabrics (supplied by China).

However, non-economic factors, particularly the reported Xinjiang forced labor issue, are complicating fashion companies’ sourcing decisions. Notably, US cotton apparel imports from China year-to-date (YTD) in 2020 (Jan to August) significantly decreased by 54% from a year ago, much higher than the 22% drop in US imports from the rest of the world. As a result, China’s market share in the US cotton apparel import market sharply declined from 22% in 2019 to only 15.1% in 2020 (Jan-Aug), a record low in the past ten years. This unusual trade pattern suggests that the concerns about social compliance risk are holding US fashion companies back from sourcing cotton apparel products from China. As the forced labor issue continues to evolve and become ever more sensitive and high profile, it is not unlikely that US fashion companies may substantially cut their China sourcing further, even if it is not a preferred choice economically.

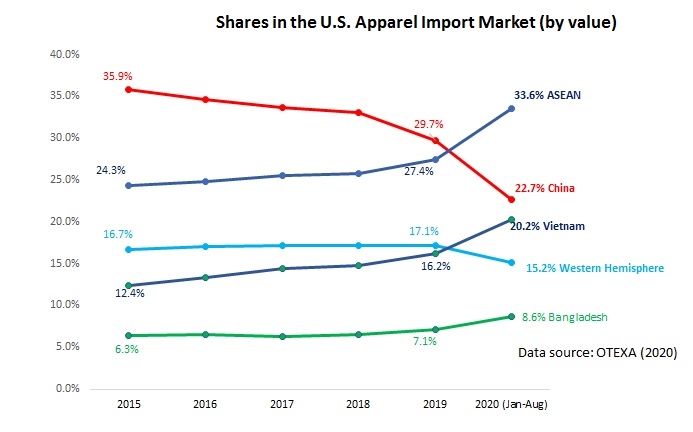

Third, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.2% YTD in 2020 vs. 16.2% in 2019), ASEAN (33.6% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.6% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.5% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

Likewise, thanks to a highly integrated regional textile and apparel supply chain, Asian countries all together were able to maintain fairly stable market shares on the world stage over the past decade despite all market disruptions, from the financial crisis, trade war to the wage increase.

Fourth, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first seven months of 2020, only 8.9% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first eight months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 28.0% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the contributing factors.

Further, industry sources show that the apparel products U.S. fashion companies import from members of USMCA and CAFTA-DR predominantly are tops and bottoms. The lack of production capacity for other product categories significantly limits the growth potential of these countries playing the role as a leading sourcing base.

by Sheng Lu

A lot of this data and the points made remind me of your conference (the 66min video from Lecture 6). China is still unparamount when it comes to exports and sourcing and US consumers remain unparalleled in high consumer demand. It is interesting that we are still sourcing from China, even though so much of our focus these days (due to COVID and other factors) is on sourcing, innovating, and producing inwardly, China still remains a reliable source when we boil it down to where we get these factors that fuel our production. Perhaps, even if the US isn’t considerably as cheap and fast producing as China, we can still produce as effectively, just in a different way. It seems as though China (through unethical trade, too) dominates the world, but there are other ways to succeed by not following the same path.

It is interesting to read that the Western Hemisphere still don’t provide a lot of sourcing to the apparel and textile industry. I wonder if after Covid-19 is over and the trade war ends if this will change. U.S. companies want to move their sourcing out of China and according to this article have shifted towards Vietnam and Bangladesh. I wonder why we haven’t started to look at countries in the Western Hemisphere and move out of Asia as a whole. It will be very interesting to see where sourcing is in the next 10 years!

a great question! It is a research question I am working on as well 🙂 As I learned from the industry, one big concern about sourcing from the Western Hemisphere is the limitation of fabric supply–without which you can only make certain categories of apparel. Next week, we will specifically look at the Western Hemisphere supply chain and I hope after learning the unit you will have more insights about the region as a sourcing destination.

I think there are a lot of things to be worried about as it seems there won’t be a big enough shift away from dependence on single location production facilities and towards more vertical integration, however it is good that demand is rebounding for clothing and imports. The recession we are in is deeply concerning, but showing this demand bounce back quickly, as well as the bolstering/stable Chinese Apparel market as a whole even through the virus, are glimmers of hope that the apparel market as a whole will be able to survive and thrive as the pandemic drags on and when it comes to an end.

I think it is very interesting that Covid did not really make US fashion brands rethink sourcing from the western hemisphere. Even through this time China remains a leader in manufacturing due to their large production ability and their ability to produce their own resources such as yarn and textiles. I would think that Covid would provide US fashion brands a great opportunity to move production out of China to the western hemisphere as it is closer to them and tariffs may not apply, however these brands are turning towards places like Vietnam and Bangladesh first. It will be interesting to see where brands actually decide to shift in the future once Covid is more under control and the trade war ends.

I think it is very interesting to learn that so many U.S. retailers are continuing to source from China despite high tariffs being put in place. I understand the benefits of sourcing from China: cheap labor, being able to produce just about every product and making materials locally. These are definitely benefits for the retailers, however the tariffs are going to continue to increase and I would think that this would be the perfect time for retailers to start figuring out how they can move production into countries within our free trade agreements. Sourcing costs would most likely be lower and the products would arrive fast since they are being made near by. I also think this would be a really good time for retailers to get in touch with their customers and maybe start producing fewer clothes to turn away from the whole idea of fast fashion. I am interested to continue watching this and see how retailers respond. It seems like many will turn to countries like Vietnam and Bangladesh instead of taking advantage of our free trade agreements. I wonder if any of this will have an impact on fast fashion and if any companies will use this time to reconsider their business plans.

I think it was very interesting reading that there is no evidence suggesting that U.S. fashion companies are giving up on sourcing from China. With the harsh effects of COVID-19 on top on the ongoing trade war, I would’ve thought that American apparel companies would start to consider sourcing elsewhere. I understand that China is an ideal country for American apparel companies to source from due to the low costs and wide variety of production capabilities; however, I was worried that President Trump’s leadership and blaming China for the COVID-19 pandemic would start to steer American companies away from souring from China. Since discovering that the source of COVID-19 was traced back to China, unfortunately some Americans have developed prejudices against China and have begin questioning whether it’s a place they want to do business with. This is another factor that I would’ve thought could impact American apparel companies sourcing from China, however I’m glad that most U.S. companies have not felt this way and have continued sourcing from them.

I was also surprised by the fact that there is no evidence suggesting that U.S. fashion companies haven’t been souring from more Western suppliers due to those two significant factors. From previous readings and assignments we’ve done in class, we learned that one of the main reasons President Trump initiated the U.S.-China Trade War was because he wanted to encourage, or practically force, more American companies to source domestically. I wonder how this will look in the future, especially if President Trump gets re-elected and continues to raise tariffs.

I think to actually decrease the market share of China and not heavily rely on Chinese manufacturing takes time. COVID-19 does promote U.S. retailers to achieve this. However, different from suppliers from the Western Hemisphere, China still have advantage in offering diverse products in lower price. China itself, more likely to be a well-established supply chain. Starting from raw material to apparel manufacturing. Furthermore, comparing with the limited production capacity of members of USMCA and CAFTA-DR, China to able to provide a larger amount of inventory for U.S retailers and importers. To actually rebalancing the market share of imports in the U.S., retailers and importers still need to consider and seeking for another countries who have potential growth ability like Vietnam.

I find it so interesting & crazy how the decrease in US apparel imports from January to August 2020 is so much more significant than the decrease in apparel imports during the 2008-09 recession. This really shows how robust the US consumer market is – even when there was a financial crisis people were shopping more than they are now. The only thing stopping people now is lockdown!

It is also interesting to see how quickly the imports bounced back once the summertime came around & lockdowns slightly loosened. China quickly made their way back to the top as the #1 apparel supplier of US markets, showing how reliant we truly are on imports as well. It is not realistic to assume that, even with the big push from COVID-19, the US will be able to quickly adjust to a market that doesn’t rely on imports – this is a process that would take years to execute, especially in an economically efficient way.

do you think the value of US apparel imports will continue to rebound in the next few months? why or why not?

I agree that its incredible how in a financial crisis, people were shopping more than they are now in lockdown! In terms of the rebound, since more brands and retailers are starting to open their stores and offer services such as curbside pickup, more consumers are feeling comfortable to shop again. Especially now that more people are able to work again and gain income to spend. In terms of Dr. Lu’s question below, I believe the value of U.S. apparel imports will continue to rebound, but steadily. Brands and retailers are adjusting to the pandemic and growing their online and omnichannel experiences, such as social media and other smart technology, for customers which are boosting sales. As the pandemic enters into a cold winter, there’s a possibility physical stores may not be the center of sales, but the omnichannel will. With this, brands and retailers will still need to import goods to stock inventory for online or curbside orders. Its possible that imports may eventually surpass its growth from before the pandemic because many consumers are finding the omnichannel and other online services as convenient which may stick around post-pandemic. What do you think?

No one has ever gone through something like COVID-19 before this, and these brands have still decided to go back to working with Chinese suppliers again. I am not surprised that Asia is back at the top because they provide ultimately what companies want, low costs and high quantities. At the end of the day, brands need to make a profit and that happens by having lower costs. I do wonder if ethics will ever become apparent enough for brands to use Western Hemisphere suppliers. However, brands probably feel China is more reliable than ever after going through such a decline and being able to rebound so quickly. It may be hard to convince brands to use suppliers elsewhere.

I attended an industry event last week. One speaker told us that because of the booming of E-commerce during the pandemic, some US fashion retailers:1) import products from Asia and stock them in the bonded warehouses in Mexico (note: bonded warehouse means dutiable goods may be stored, manipulated, or undergo manufacturing operations without payment of duty). 2) When US consumers place orders, the retailer will ship these products directly from these bonded warehouses in Mexico to the final destination. Most importantly, the retailer takes advantage of the US de minimis rule (i.e., meaning that goods valued at $800 or less could enter the U.S. duty-free one person one day) and avoid paying tariffs for these products (even though they counted as imported from Asia). Don’t know how prevalent such a practice is. However, it might explain why sourcing from the western hemisphere has been declining so far this year according to the statistics, despite the assumed increasing popularity of near sourcing. Meanwhile, it also reminds us that the rules of the game matters…

I think it is very interesting to see that the U.S apparel imports continue to rebound even during COVID-19. I am surprised that the imports in the US went up in August by 7.6%. I believe the upward trend will last for only the next fews months due to the holidays.

I found it quite surprising that despite all of the complications and restrictions brought on by covid-19, exports from the United States are continuing to increase. I feel relieved to see that even in the face of these challenges the retail industry in America has been able to bounce back successfully. However, I was less surprised to see that retailers are still continuing to turn to China for manufacturing. At the end of the day, regardless of other factors, brands need to make a profit. With that in mind, China is the ideal place for manufacturing because they can produce the most efficiently at the lowest costs.

Well, i am not too surprised to see the value of US apparel imports started to recover since May–because US consumers began to purchase again (you can see the data from the US Census). However, according to the media, it does seem interesting that some sourcing orders are moving from other Asian countries back to China (https://shenglufashion.com/2020/10/31/battling-the-trade-war-and-covid-19-rethinking-global-supply-chains-in-a-time-of-crisis/). However, it remains unknown whether this is a short-term adjustment or a medium or long term trend. Sourcing is so dynamic

I found it very interesting that U.S. apparel imports have continued to rebound. Even with a global pandemic still taking over the world, the apparel industry has seen a return to 80% volume of apparel imports from pre-covid times. However, it does not change how imports decreased about 30% year over year, which is worse than during the 2009 financial crisis. This is not shocking, as the world has been facing incredible financial turmoil during these trying times. It will be interesting to see if the U.S. can fully recover from this issue, or if we will be seeing major changes throughout production in the fashion industry!