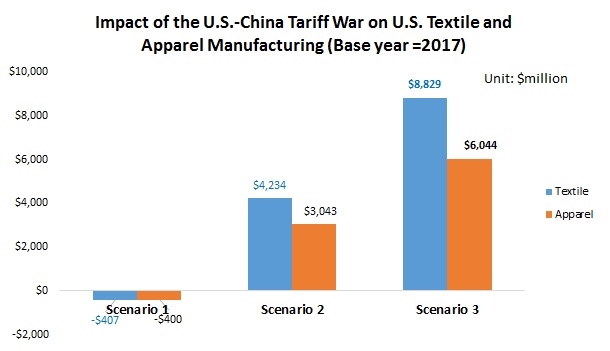

Background: In response to China’s decision to impose 5%–10% retaliatory tariffs on $75 billion U.S. products, on August 23, 2019, the Trump administration announced to raise the Section 301 tariffs from 25% to 30% for around $250 billion Chinese products (tranche 1, 2 and 3), effective October 1, 2019. The scheduled Section 301 tariffs on $300 billion Chinese products (tranche 4) to take into effect on September 1, 2019 and December 15, 2019 will also be increased from 10% to 15%.

U.S. fashion brands and retailers are deeply concerned about the negative impacts of the tariff war on their businesses. According to the 2019 U.S. Fashion Industry Benchmarking Study released by the U.S. Fashion Industry Association, even without considering the upcoming 10-15% tariffs to be imposed on around $35.7 billion Chinese textiles and apparel covered by tranche 4:

- The trade diversion effect of Section 301 has accelerated U.S. fashion companies’ pace of reducing sourcing from China. About 83 percent of respondents expect to decrease sourcing from China over the next two years, up further from 67 percent in 2018.

- The Section 301 action is pushing up the price of U.S. apparel imports across the board, making “increasing production and sourcing cost” the top business challenge for respondents in 2019. As much as 63 percent of respondents explicitly say the U.S. Section 301 tariff action against China “increased my companies’ sourcing cost” in 2019. As companies are moving sourcing orders to Bangladesh, Vietnam, and India, the average price of U.S. apparel imports from these countries – the main alternatives to China — have all gone up very quickly.

- No evidence shows that Section 301 has benefited near-sourcing from the Western Hemisphere and reshoring from the United States significantly. Instead, respondents say Section 301 has increased the production costs of textiles and apparel “Made in the USA.”

- Respondents say they are reluctant but may have to increase their retail prices, should the U.S.-China tariff war escalate further.

Related reading: