Video 1: Is U.S. Clothing Manufacturing at Risk? Tariffs and Competition Threaten Jobs (RT≠ Endorsement)

Video 2: Northern Virginia T-shirt brand faces challenges (RT≠ Endorsement)

Video 3: Tariffs could raise wedding dress prices for American brides (RT≠ Endorsement)

Video 4: Bangladeshi garment industry sweating on Trump tariffs (RT≠ Endorsement)

Video 5: Trump’s Tariff Twist: Can Pakistan’s Textiles Fill China’s Shoes? (RT≠ Endorsement)

Video 6: Tariffs: Europe’s textile sector holds its breath

For FASH455 class: When writing your blog comment, consider addressing the following aspects:

#1 Based on the videos, how do you expect the apparel sourcing strategy of US fashion companies to evolve in response to the tariff increase? For example, will companies continue to diversify sourcing, wait and see, or focus on expanding sourcing to countries or regions regarded as “safe havens”?

#2 Do you expect the higher tariffs on U.S. imports, including textiles and apparel, to benefit domestic “Made in the USA” production? Why or why not?

#3 As consumers, how do you perceive the impact of the tariffs on your shopping behavior and experiences? Have you noticed any changes, such as in price and product availability, while shopping for clothing recently? Feel free to share your observations.

#4 Are there any other notable impacts of the tariff increase on the global fashion apparel industry that we should be aware of? What additional questions do you have in mind about the tariff impacts?

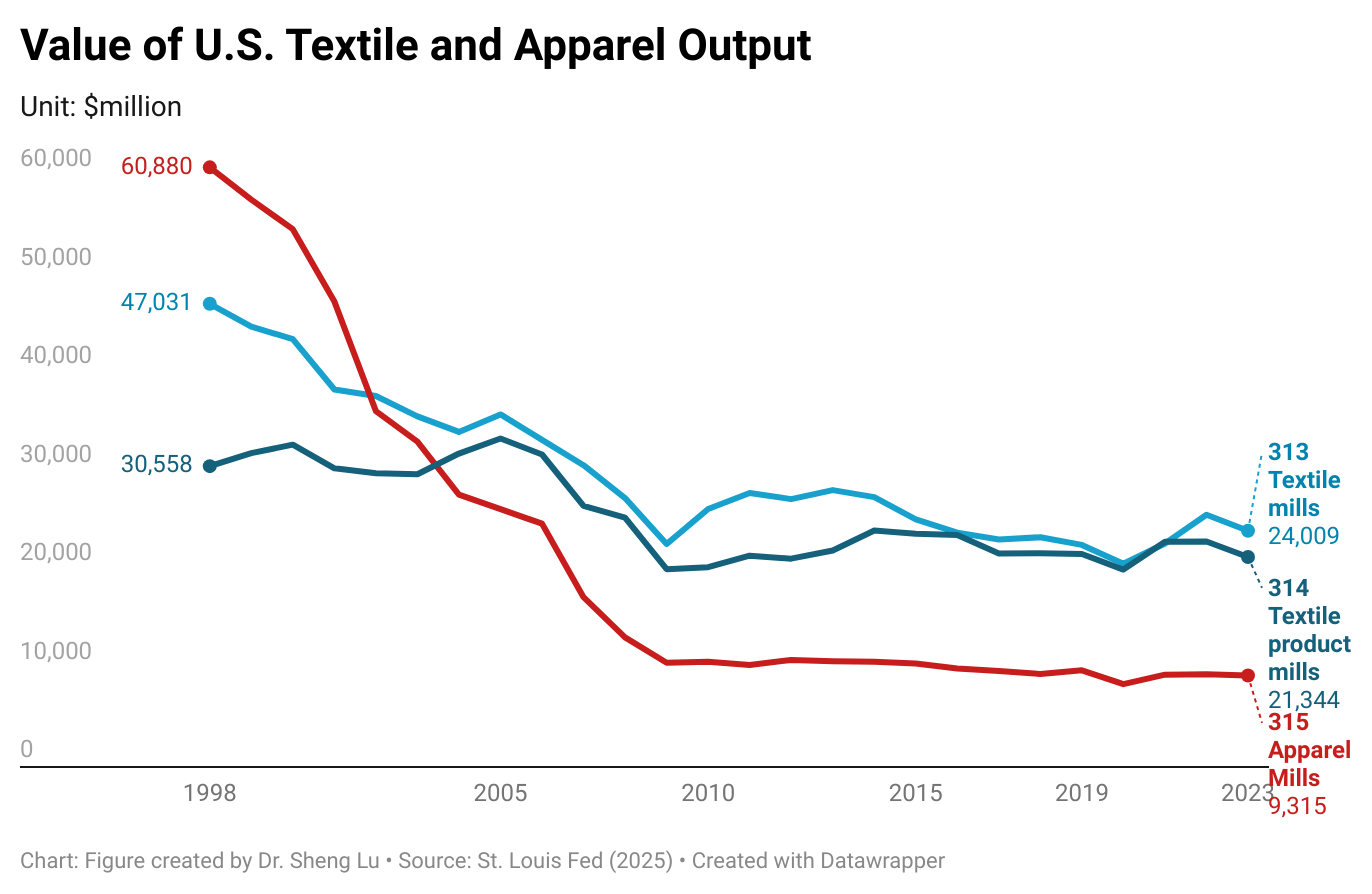

Textile and apparel manufacturing in the U.S. has significantly decreased over the past decades due to factors such as automation, import competition, and the changing U.S. comparative advantages for related products. However, thanks to companies’ ongoing restructuring strategies and their strategic use of globalization, the U.S. textile and apparel manufacturing sector has stayed relatively stable in recent years. For example, the value of U.S. yarns and fabrics manufacturing (NAICS 313) totaled $24 billion in 2023 (the latest data available), up from $23.3 billion in 2018 (or up 2.8%). Over the same period, U.S. made-up textiles (NAICS 314) and apparel production (NAICS 315) moderately declined by only 1.8% and 1.6%.

More importantly, the U.S. textile and apparel manufacturing sector is evolving. Several important trends are worth watching:

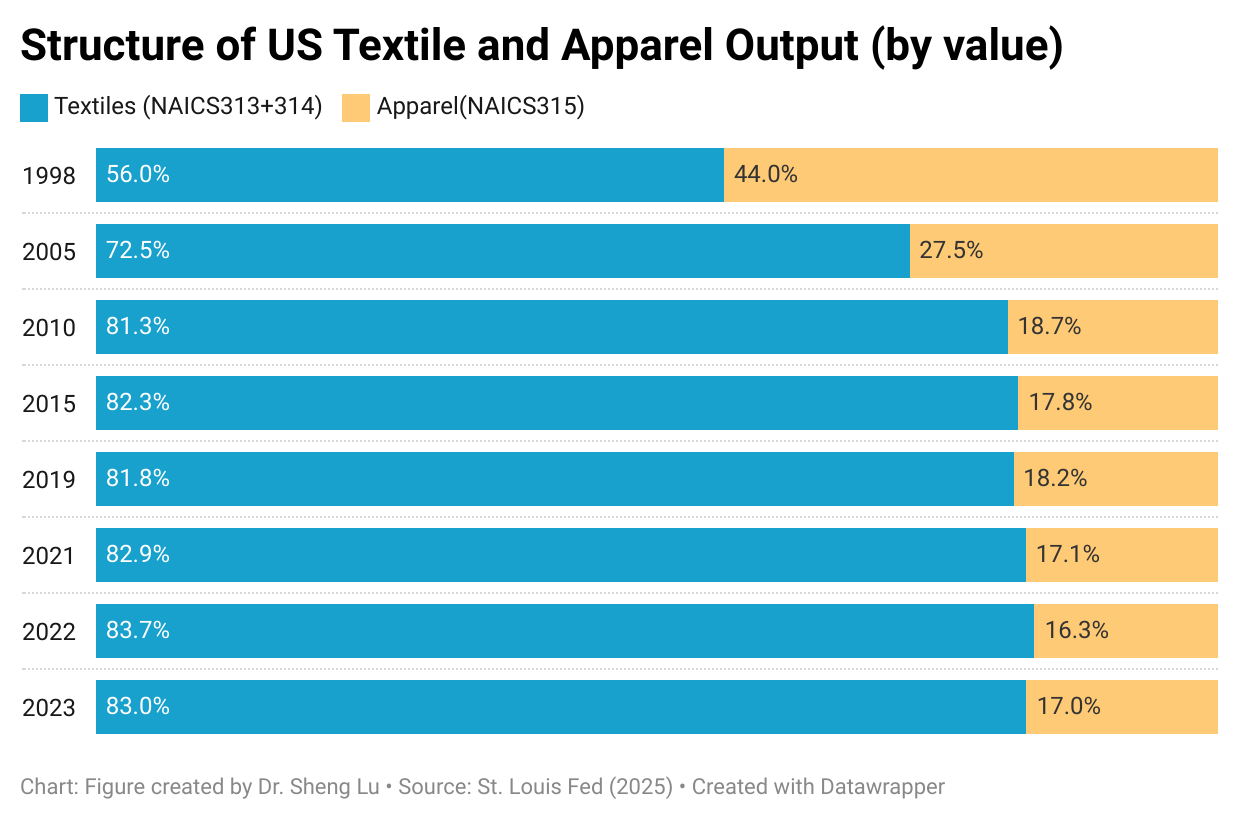

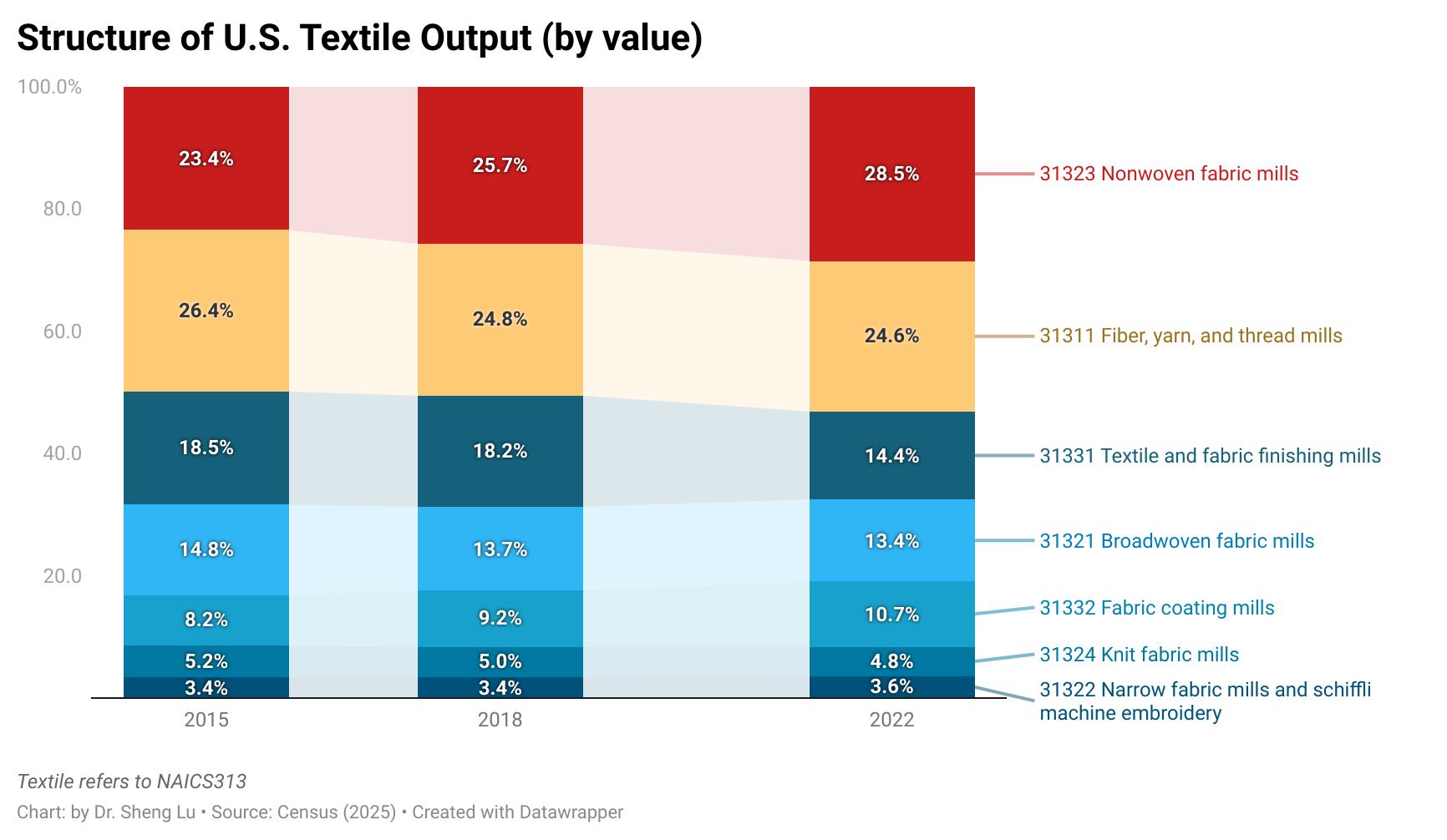

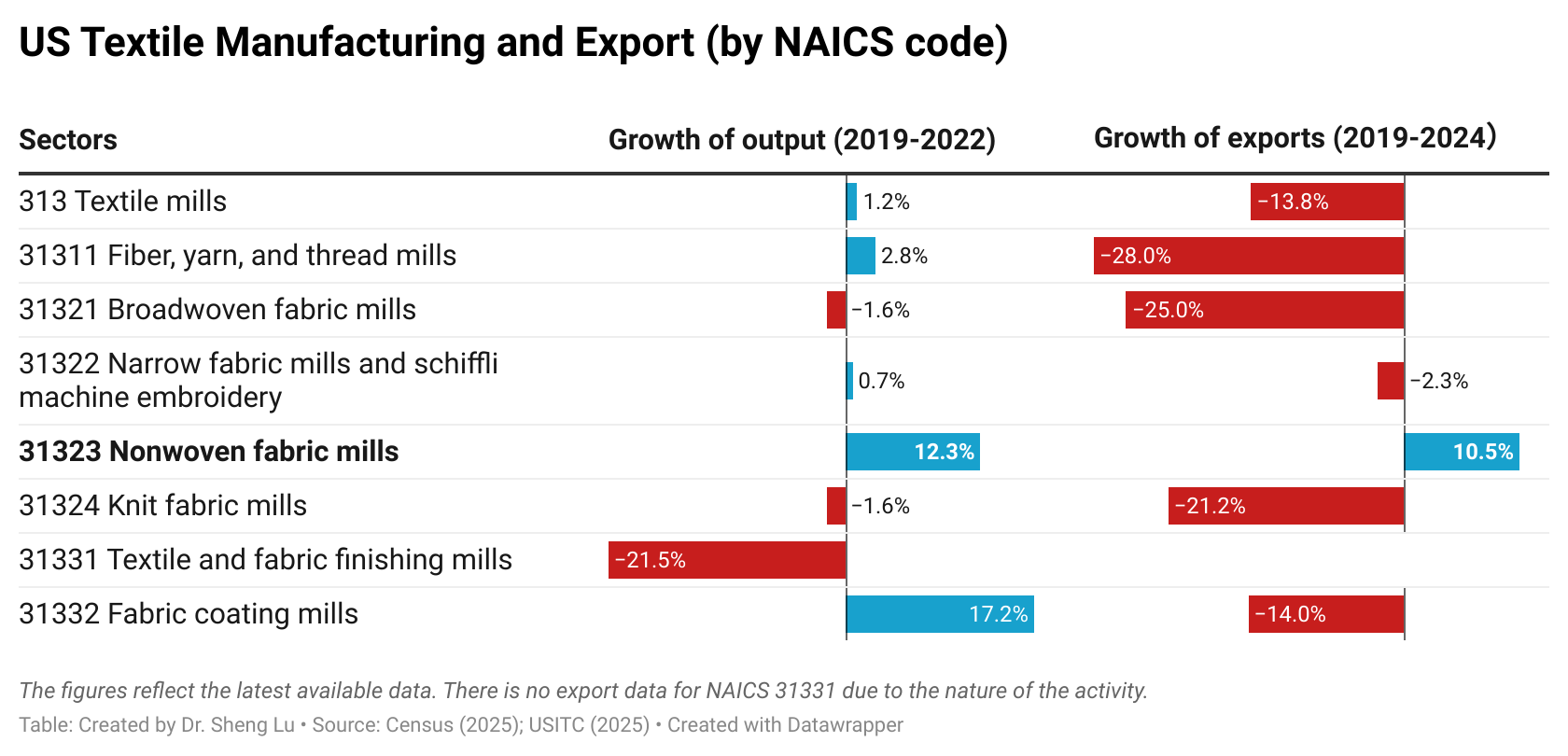

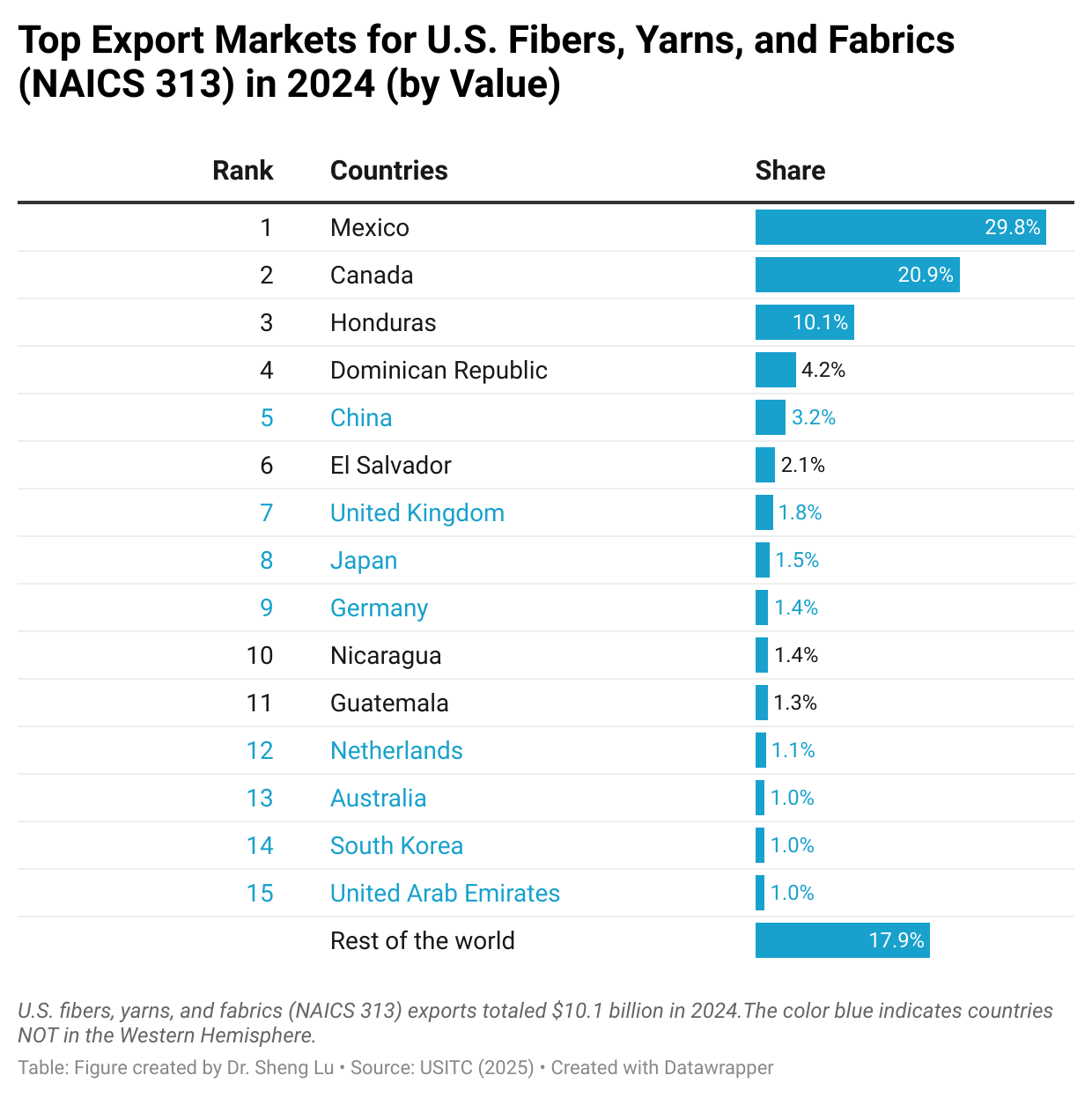

First, “Made in the USA” increasingly focuses on textile products, particularly high-tech industrial textiles that are not intended for apparel manufacturing purposes. Specifically, textile products (NAICS 313+314) accounted for over 83% of the total output of the U.S. textile and apparel industry as of 2023, much higher than only 56% in 1998 (U.S. Census, 2025). Textiles and apparel “Made in the USA” are growing particularly fast in some product categories that are high-tech driven, such as medical textiles, protective clothing, specialty and industrial fabrics, and non-woven. These products are also becoming the new growth engine of U.S. textile exports. Notably, between 2019 and 2022, the value of U.S. “nonwoven fabric” (NAICS 31323) production increased by 12.32%, much higher than the 1.15% average growth of the textile industry (NAICS 313). Similarly, while U.S. textile exports decreased by 13.75% between 2019 and 2024, “nonwoven fabric” exports surged by 10.48%--including nearly 40% that went to market outside the Western Hemisphere (U.S. International Trade Commission, 2025).

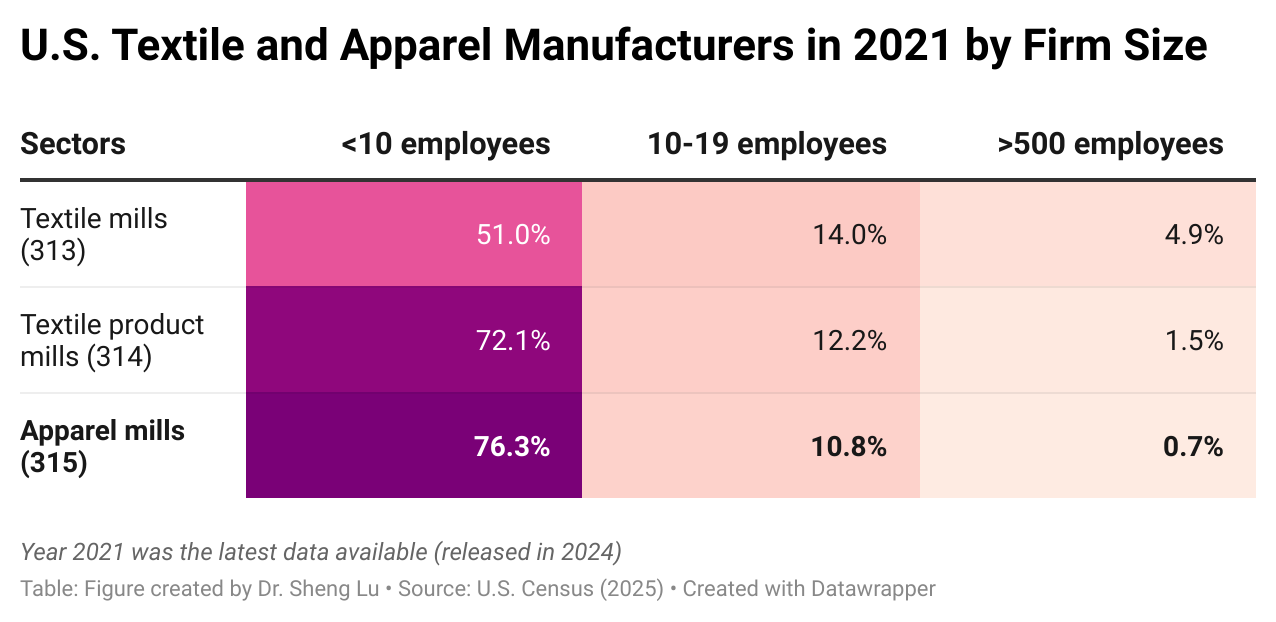

Second, U.S. apparel manufacturers today are primarily micro-factories, and they supplement but are not in a position to replace imports. As of 2021 (the latest data available), over 76% of U.S.-based apparel mills (NAICS 315) had fewer than 10 employees, while only 0.7% had more than 500 employees. In comparison, contracted garment factories of U.S. fashion companies in Asia, particularly in developing countries like Bangladesh, typically employ over 1,000 or even 5,000 workers.

Instead of making garments in large volumes, most U.S.-based apparel factories are used to produce samples or prototypes for brands and retailers. In other words, replacing global sourcing with domestic production is not a realistic option for U.S. fashion brands and retailers in the 21st-century global economy. Nor are U.S. fashion companies showing interest in shifting their business strategies from focusing on “designing + managing supply chain+ marketing” back to manufacturing.

Meanwhile, due to mergers and acquisitions (M&A) and to leverage economies of scale, approximately 5% of U.S. textile mills (NAICS313) had more than 500 employees as of 2021–this is a significant number, considering that textile manufacturing is a highly capital-intensive process.

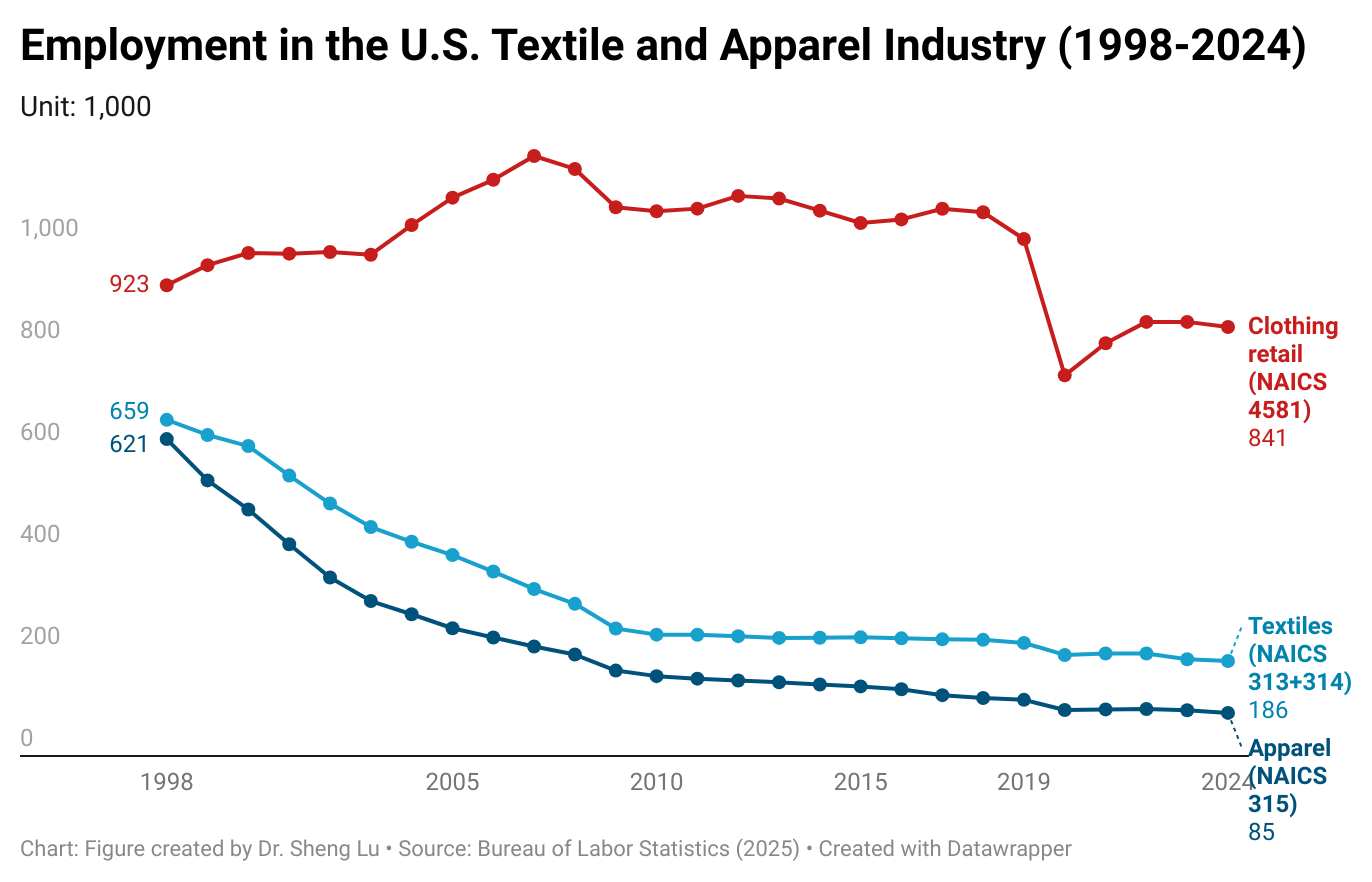

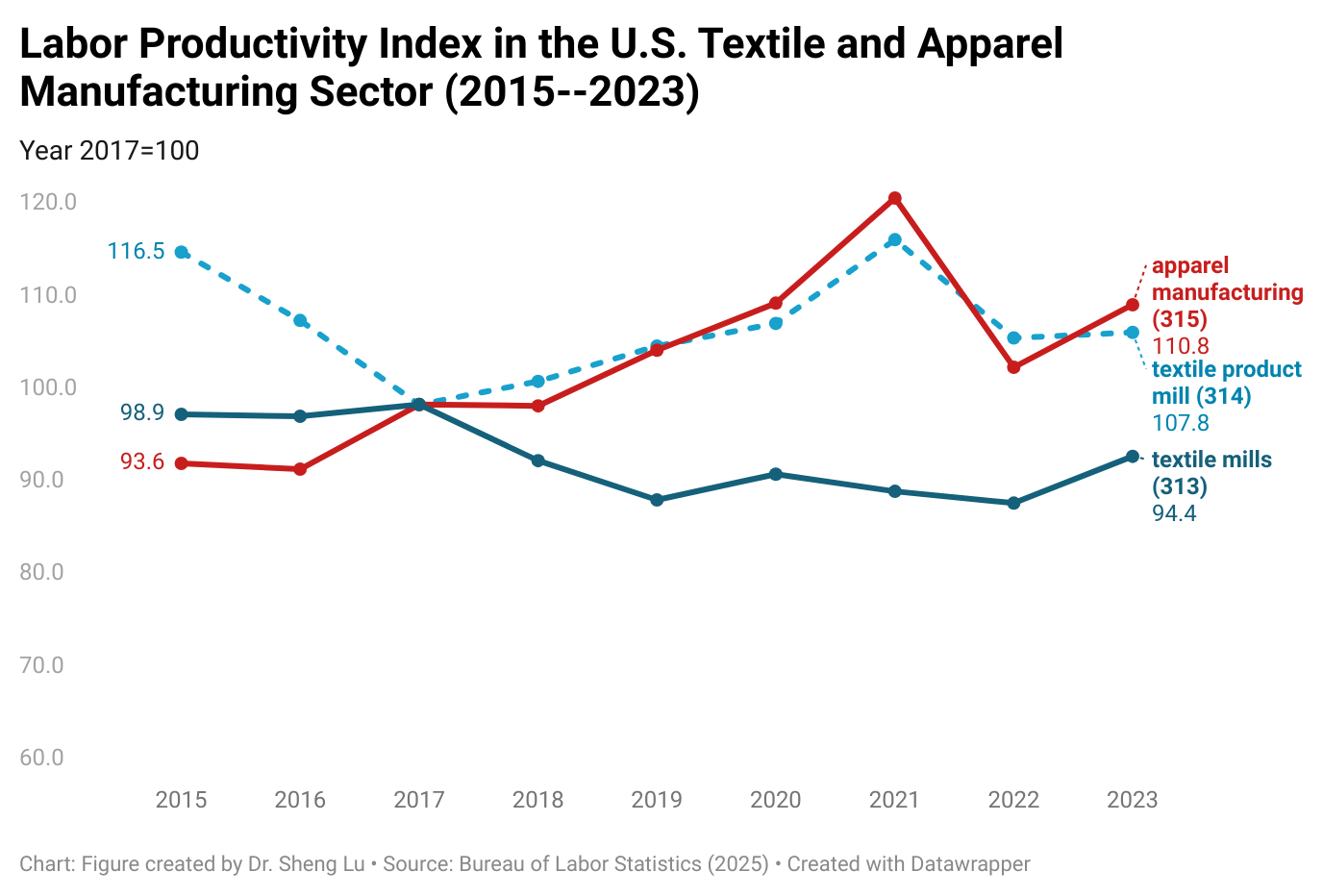

Third, employment in the U.S. textile and apparel manufacturing sector continued to decline, with improved productivity and technology being critical drivers. As of 2024, employment in the U.S. textile and apparel manufacturing sector (NAICS 313, 314, and 315) totaled 270,700, a decrease of 18.4% from 33,190 in 2019. Notably, U.S. textile and apparel workers had become more productive overall—the labor productivity index of U.S. textile mills (NAICS 313) increased from 89.7 in 2019 to 94.4 in 2023, and the index of U.S. apparel mills (NAICS 315) increased from 105.8 to 110.78 over the same period.

On the other hand, clothing retailers (NAICS 4481) accounted for over 75.7% of employment in the U.S. textile and apparel sector in 2024.

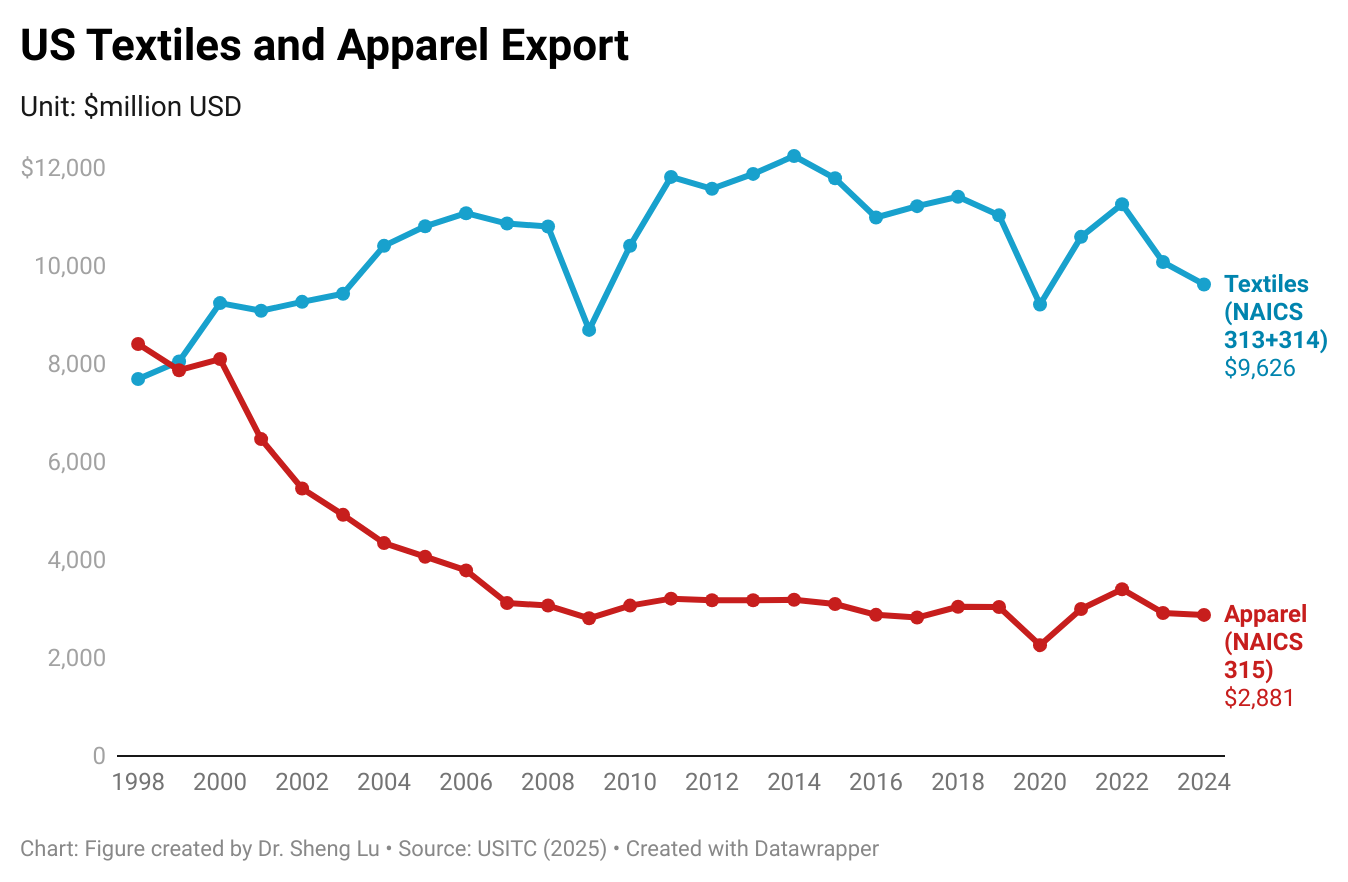

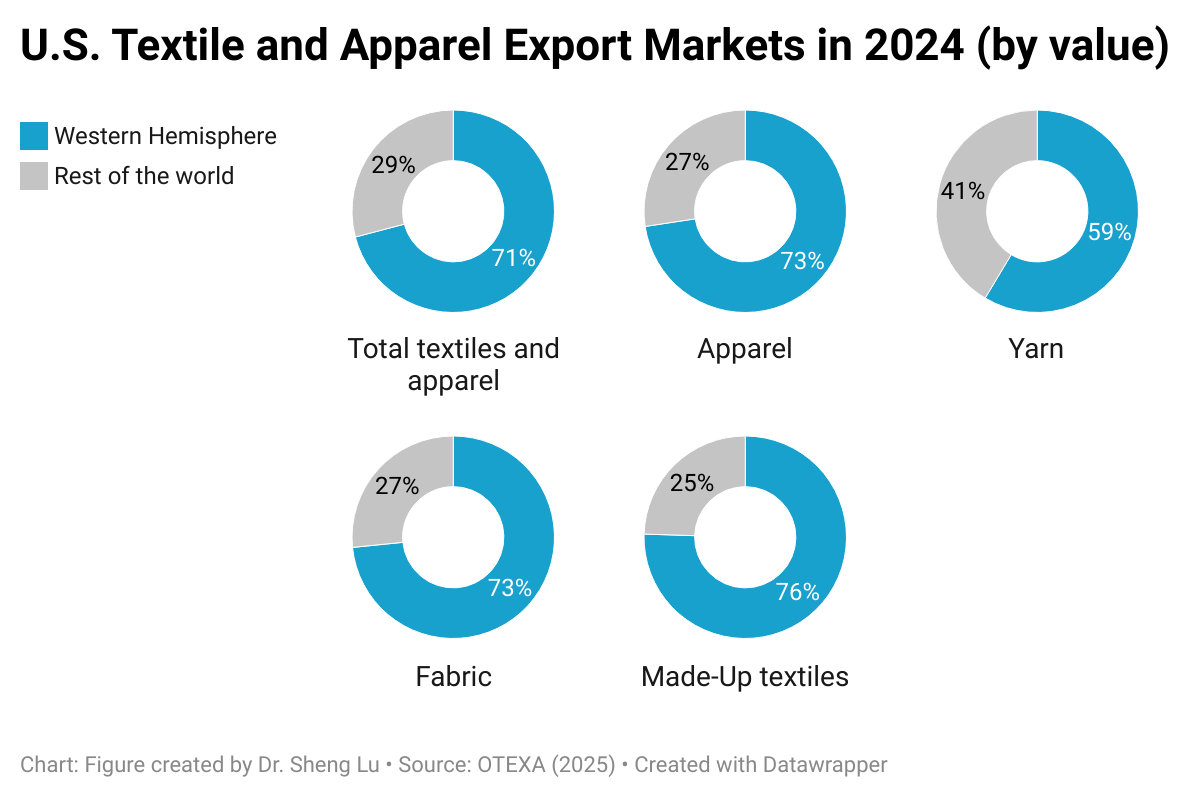

Fourth, international trade, BOTH import and export, supports textiles and apparel “Made in the USA.” On the one hand, U.S. textile and apparel exports exceeded $12.5 billion in 2024, accounting for more than 30% of domestic production as of 2023 (NAICS 313, 314 and 315). Thanks to regional free trade agreements, particularly the U.S.-Mexico-Canada Agreement (USMCA) and the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR), the Western Hemisphere stably accounted for over 70% of U.S. textile and apparel exports over the past decades. However, for specific products such as industrial textiles, markets in the rest of the world, especially Asia and Europe, also become increasingly important. Thus, lowering trade barriers for U.S. products in strategically significant export markets serves the interest of the U.S. textile and apparel industry.

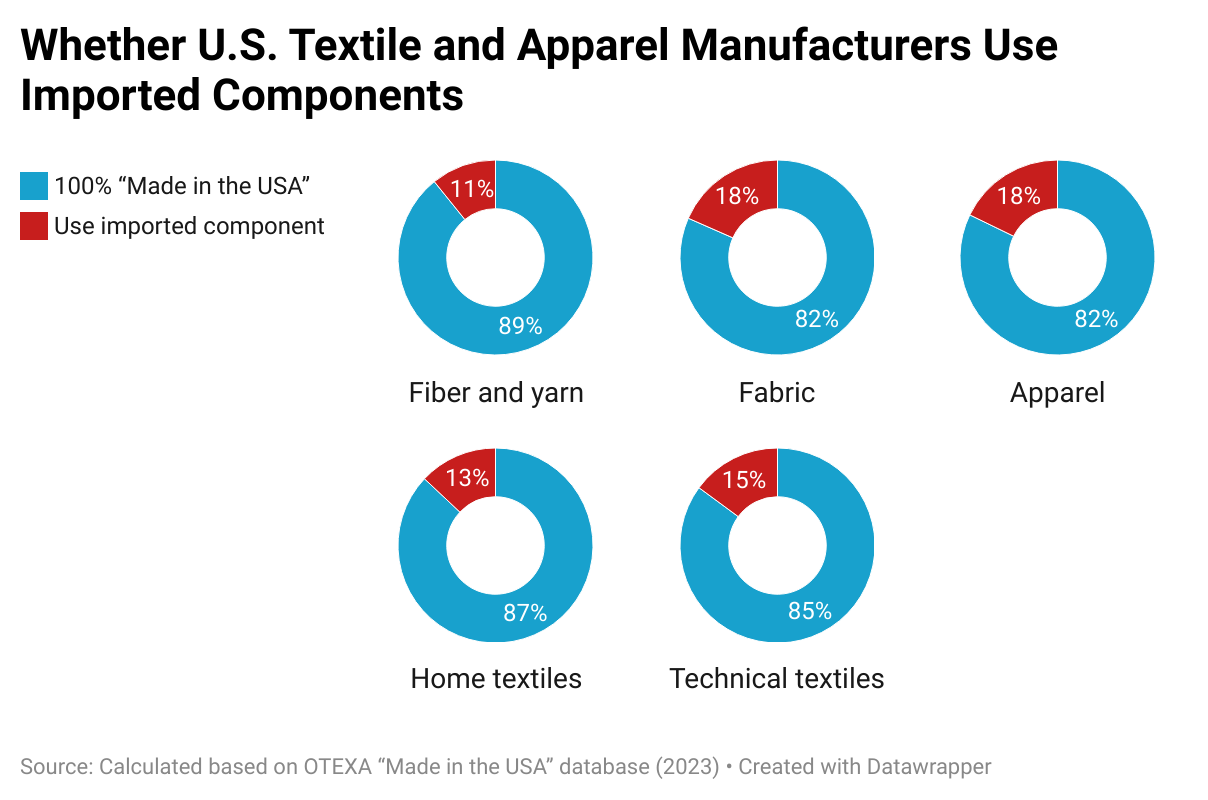

On the other hand, imports support textiles and apparel “Made in the USA” as well. A 2023 study found that among the manufacturers in the “Made in the USA” database managed by the U.S. Department of Commerce Office of Textile and Apparel, nearly 20% of apparel and fabric mills explicitly say they utilized imported components. Partially, smaller U.S. textile and apparel manufacturers appear to be more likely to use imported components–whereas 20% of manufacturers with less than 50 employees used imported input, only 10.2% of those with 50-499 employees and 7.7% with 500 or more employees did so. The results indicate the necessity of supporting small and medium-sized (SME) U.S. textile and apparel manufacturers to more easily access their needed textile materials by lowering trade barriers like tariffs.

What do you think about the pink tariff? How does the pink tariff affect different stakeholders, including consumers and fashion companies?

How can fashion companies respond to or navigate pink tariffs in their global sourcing, particularly considering the tariff escalation in 2025?

What role can governments and international trade organizations play in addressing pink tariffs, and what policy changes could help eliminate the disparities? What are the challenges?

The United States Fashion Industry Association (USFIA), whose members include many leading U.S. fashion brands and retailers, opposes raising tariffs and argues for lowering tariffs on textile and apparel products where the U.S. imposes a higher tariff rate than its trading partners. According to USFIA, higher tariffs on apparel and textiles would disproportionately impact lower-income U.S. consumers:

“A true ‘reciprocal’ trade policy would lower tariffs on the products of trading partners that maintain lower tariffs than the United States.”

“We recommend that the most successful policy to achieve trade reciprocity would be for the United States to lower the tariff rates of products for which our trading partners apply lower tariff rates. For consumer products such as textiles and apparel, this would help combat inflation and assist consumers who struggle to afford basic necessities.”

The American Apparel and Footwear Association (AAFA), representing U.S.-based “apparel, footwear and other sewn products companies”, opposes broad tariffs on apparel, footwear, and textiles. It is of concern to AAFA that the apparel and footwear sector already faces some of the highest tariffs in the U.S., and tariffs are a “hidden, regressive tax that falls harder on lower-income Americans.” Even worse, AAFA worries that higher tariffs would benefit “Illicit traders” and tariff threats would undermine the regional textile and apparel supply chain in the Western Hemisphere:

“Illicit traders are better positioned to escape paying proper duties or any duties at all. Higher tariffs end up maximizing the profit and market access they can gain at the expense of legitimate shippers.”

“Recent tariff threats particularly on our neighbors, Canada and Mexico, are especially concerning as the U.S.-Mexico-Canada Agreement (USMCA) review is about to begin. Canada is a key export market for U.S. made apparel and footwear while Mexico is a major source of a wide variety of apparel, including denim imports. Not only does the threat of tariffs cast uncertainty but it also undermines future investment and nearshoring opportunities.”

“We strongly recommend that the Trump administration take a targeted approach to raise tariffs on specific countries that disrupt markets through the use of blatantly unfair and often illegal trade practices, while simultaneously operating in home markets that remain mostly closed to our products.”

“We must preserve and strengthen existing trade relationships with U.S. free trade agreement (FTA) countries in the Western Hemisphere that offer valuable markets for U.S.-made textiles.”

“We strongly believe that reciprocity should not mean a race to the bottom with lower tariffs on imports from other countries into our market. Rather, reciprocity should hold bad actors accountable for systemic unfair trade practices that have hurt domestic manufacturers.”

“We urge the Trump administration to take several actions immediately to make textile and apparel trade more reciprocal and to support the domestic industry…Aggressively raise tariffs on imports of textile and apparel products from China and other trade predators in Asia…Close the de minimis loophole for all countries…”

SMART (Secondary Materials and Recycled Textiles Association),representing businesses engaged in the collection, reuse, conversion, and recycling of textiles and other secondary materials, advocates for addressing trade barriers that affect U.S. secondhand clothing exports. SMART also opposes CAFTA-DR members using the “yarn-forward” rules of origin for imports of secondhand clothing (HTS 6309) from the U.S. under the agreement.

National Retail Federation (NRF), generally representing all types of U.S. retailers, opposes broad-based tariffs, arguing that they increase consumer costs, disrupt supply chains, and hurt retailers. NRF supports targeted measures against unfair trade practices but warns against policies that could lead to unnecessary retaliation from U.S. trading partners.

“We believe that high, across-the-board tariffs will undermine the economic growth signaled by the other features of the president’s agenda and have lasting negative consequences for consumers and workers. If the goal of reciprocal tariffs is to enter into negotiations to remove barriers to trade, this will unlock economic growth and reduce prices for consumers. However, if the goal is primarily to raise tariffs, then the opposite is true.”

“There are plenty of areas where U.S. tariffs are actually much higher than our trading partners, for example, especially when you look at U.S. tariffs on low value apparel and footwear. These regressive tariffs hurt low- and middle-income consumers the most.”

“The administration should also consider the potential for retaliation from our trading partners on any reciprocal tariffs that are established. We are already witnessing our trading partners respond to strong tariff actions by the administration. This will further impact our farmers and manufacturers who are looking to gain access to those foreign markets.”

“We need to focus on key high-priority sectors where it makes sense to return manufacturing home or areas where there is strategic competition. High tariffs on everyday household goods, which could raise consumer prices, should not be the focus of such a policy.”

Parkdale Mills, a leading producer of spun yarns based in North Carolina, expressed concerns about “unfair trade practices” from its Asian competitors. Parkadel also calls for closing the “De minimis” loophole.

“Each week millions of pounds of product move through our free trade agreement partner countries illegally causing significant damage to the domestic textile industry. Non qualifying goods are shipped using false HTS codes, False Certificates of Origin, and illegal inputs to circumvent the required duty for US entry.”

“Section 321 De Minimis (imports)…are shipped into the US each day without inspection or any type of customs enforcement causing millions in lost revenue and again, thousands of lost jobs. This loophole must be closed.”

Apparel products are often subject to high tariffs for various reasons. In developed countries such as the United States, apparel has long been considered an “import-sensitive” sector, with relatively high tariff rates imposed primarily to “protect” specific domestic interest groups with political influences.

However, as importers, not exporters, pay the tariffs, heavy import duties have been a significant concern for US fashion companies for decades. According to data from the US International Trade Commission (USITC), in 2024, apparel (HS chapters 61 and 62) accounted for about 2.5 percent of total US imports but contributed approximately 15.6 percent of total tariff duties. Likewise, US fashion companies paid $11.9 billion in tariffs on apparel imports in 2024, an increase from $11.6 billion in 2023. The average applied tariff rate for apparel items reached 14.6% in 2024, a notable increase from 13.7% before the imposition of Section 301 tariffs on Chinese products. Additionally, due to retail markups, every $1 in tariffs could result in a $1.50 to $2 increase in the final retail price.

Meanwhile, developing countries, especially those least developed, also often impose high tariffs on apparel—either to protect their nascent domestic industries from import competition or to generate government revenues. For example, in Africa, the apparel import tariff rate commonly exceeds 35% as of 2023 (the latest data available).

In February 2025, President Trump announced the imposition of a so-called “reciprocal tariff,” aiming to “match” the tariff rates that other countries impose on US exports, thereby promoting “fairer trade practices.” However, the details of the “reciprocal tariff” idea remain highly uncertain.

In theory, if strict “tariff matching” is required on a product-by-product basis, US apparel imports from most leading sourcing destinations—particularly those in Asia without a free trade agreement with the US–would face a significant increase in tariffs. Similarly, beneficiary countries under the African Growth and Opportunity Act (AGOA) could face a similar issue, as AGOA is a trade preference program that does not provide duty-free market access for US products in Africa. If apparel exports from AGOA-member countries to the US were subjected to the same 35%+ tariff rates that US products currently face in their markets, it would be a devastating scenario.

By Sheng Lu

(note: this post is not open for comment/discussion)

VF Corporation (VF) is one of the largest apparel companies in the US, with an estimated global sales revenue to exceed $10 billion in 2024. VF owns several well-known apparel and outdoor performance brands, including The North Face, Timberland, and Icebreaker. VF also has a global presence. According to its latest annual report, in Fiscal 2024, “VF derived 52% of its revenues from the Americas, 33% from Europe, and 15% from Asia-Pacific.”

The following analysis is based on VF’s publicly released supplier list. Only factories identified as producing “apparel” products and related textile raw materials are included in the analysis.

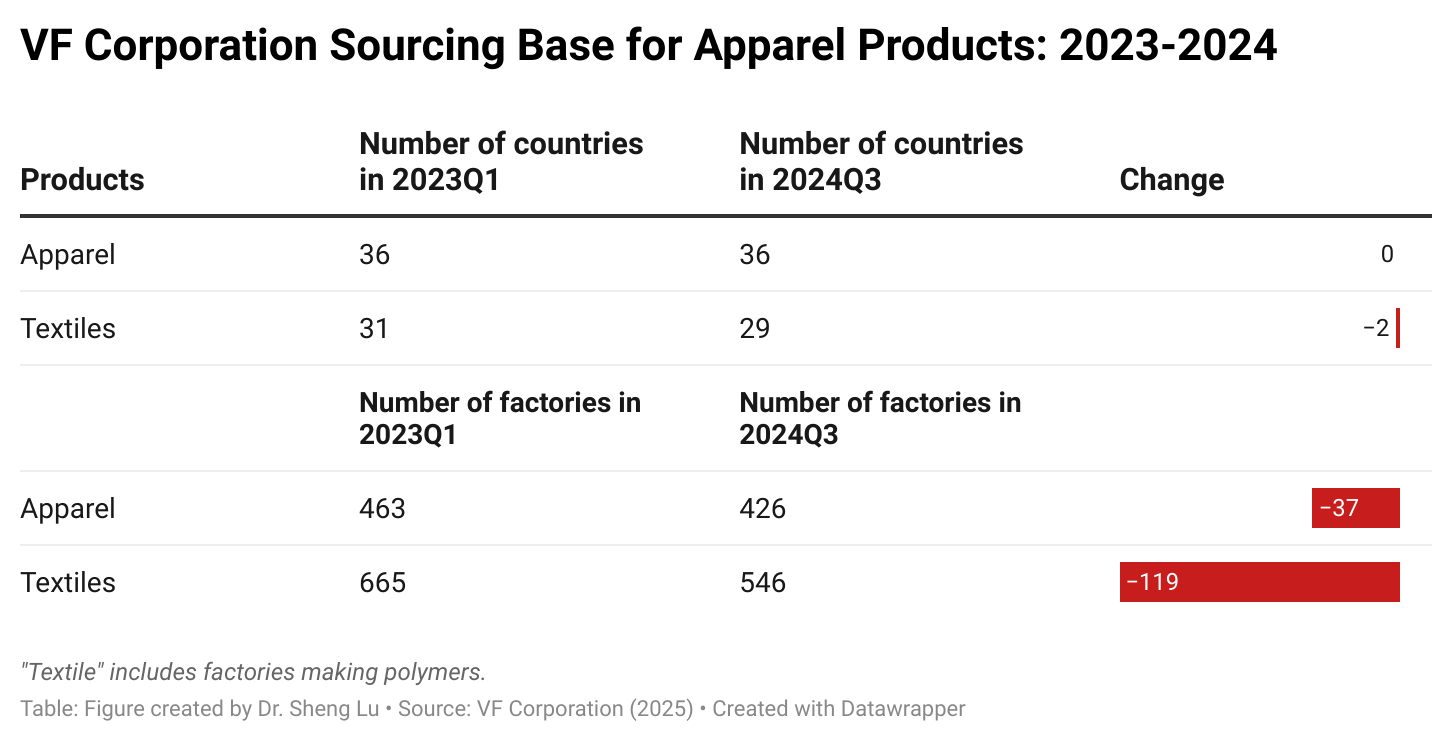

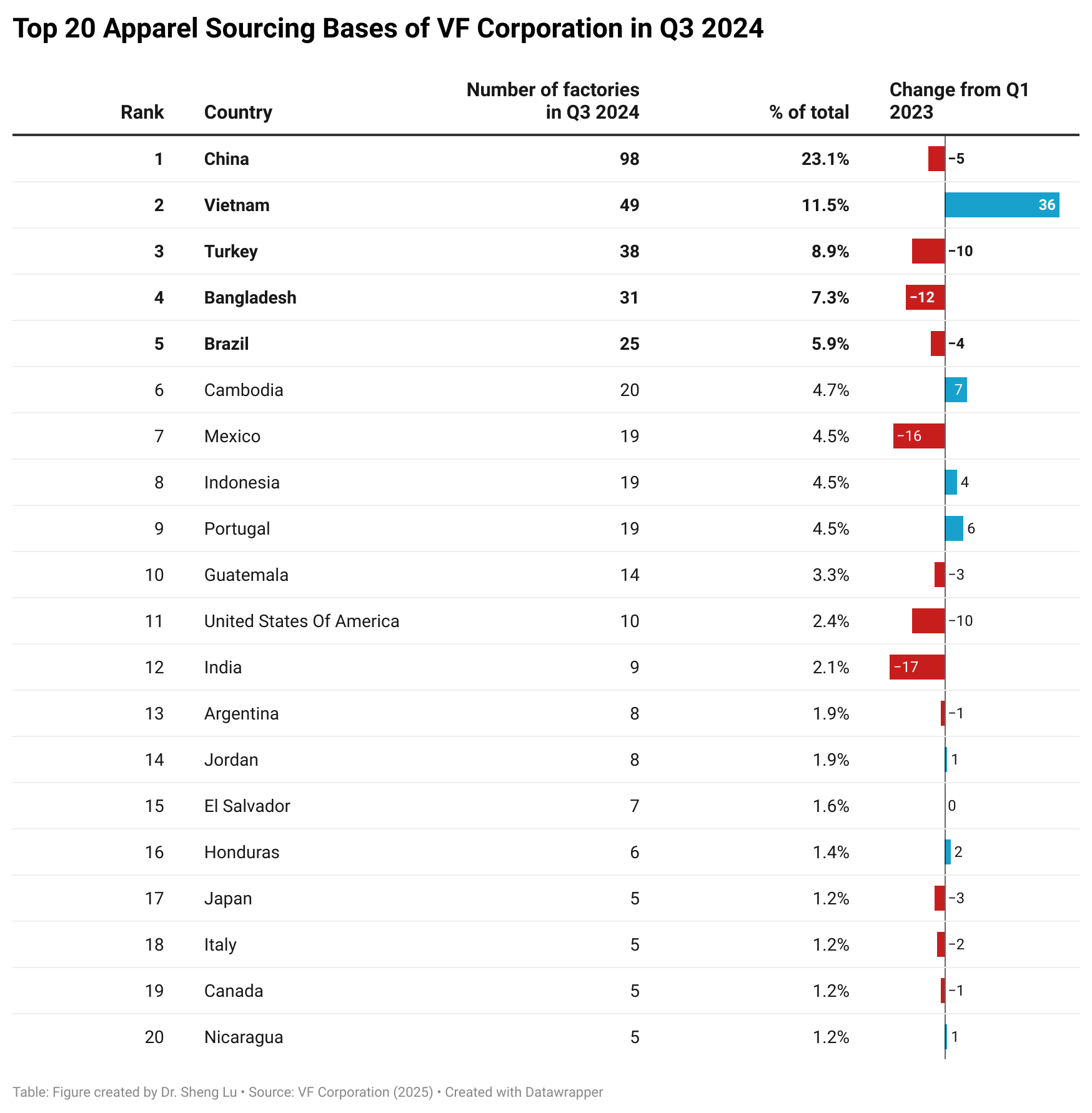

First, while VF maintained a geographically diverse global sourcing base, it reduced the number of factories it sourced from between 2023 and 2024. Specifically, as of Q3 2024 (the latest data available), VF sourced apparel from 36 countries, the same number as in Q1 2023. These countries spanned almost all continents, including Asia, the Americas, Europe, and Africa. Similarly, over the same period, VF sourced textile raw materials for apparel production—including factories producing polymers—from approximately 30 countries.

However, between Q1 2023 and Q3 2024, VF reduced the number of apparel factories it contracts with from 463 to 426. The number of textile mills VF contracts also declined, from 665 to 546. This pattern aligned with the findings of other industry studies, which indicate that many U.S. fashion companies, particularly larger ones, are consolidating their vendor base to reduce sourcing risks and enhance operational efficiency.

Additionally, VF’s annual reports indicate that no single supplier accounted for more than 6% of its total cost of goods sold during Fiscal Year 2024, the same as in 2023, but lower than 7% in Fiscal Year 2021.

Second, in line with macro trade data, Asia served as VF’s largest apparel sourcing base in Q3 2024, led by China (23.1 percent) and Vietnam (11.5 percent). Specifically, as of Q3 2024, approximately 55.3 percent of VF’s garment factories were located in Asia, an increase from 48.8 percent in Q1 2023. Meanwhile, VF is also adjusting its apparel sourcing strategy within the Asia region. For example, between 2023 and 2024, VF decreased the number of garment factories it worked with in China (down 5), Bangladesh (down 12), and India (down 17), while adding more contract factories in Vietnam (up 36), Cambodia (up 7), and Indonesia (up 4). The pattern indicates that while VF may attempt to reduce its “China exposure,” it also actively seeks new sourcing opportunities within Asia.

Conversely, in Q3 2024, around 21.2 percent of VF’s garment factories were based in the Western Hemisphere, a decrease from 27.0 percent in Q1 2023. In most situations, VF worked with about 10-20 garment factories in each Western Hemisphere country. Furthermore, from 2023 to 2024, VF cut the number of garment factories in Mexico (down 16) and the United States (down 10), indicating that expanding near-shoring and on-shoring was not the company’s preferred strategy in the current environment.

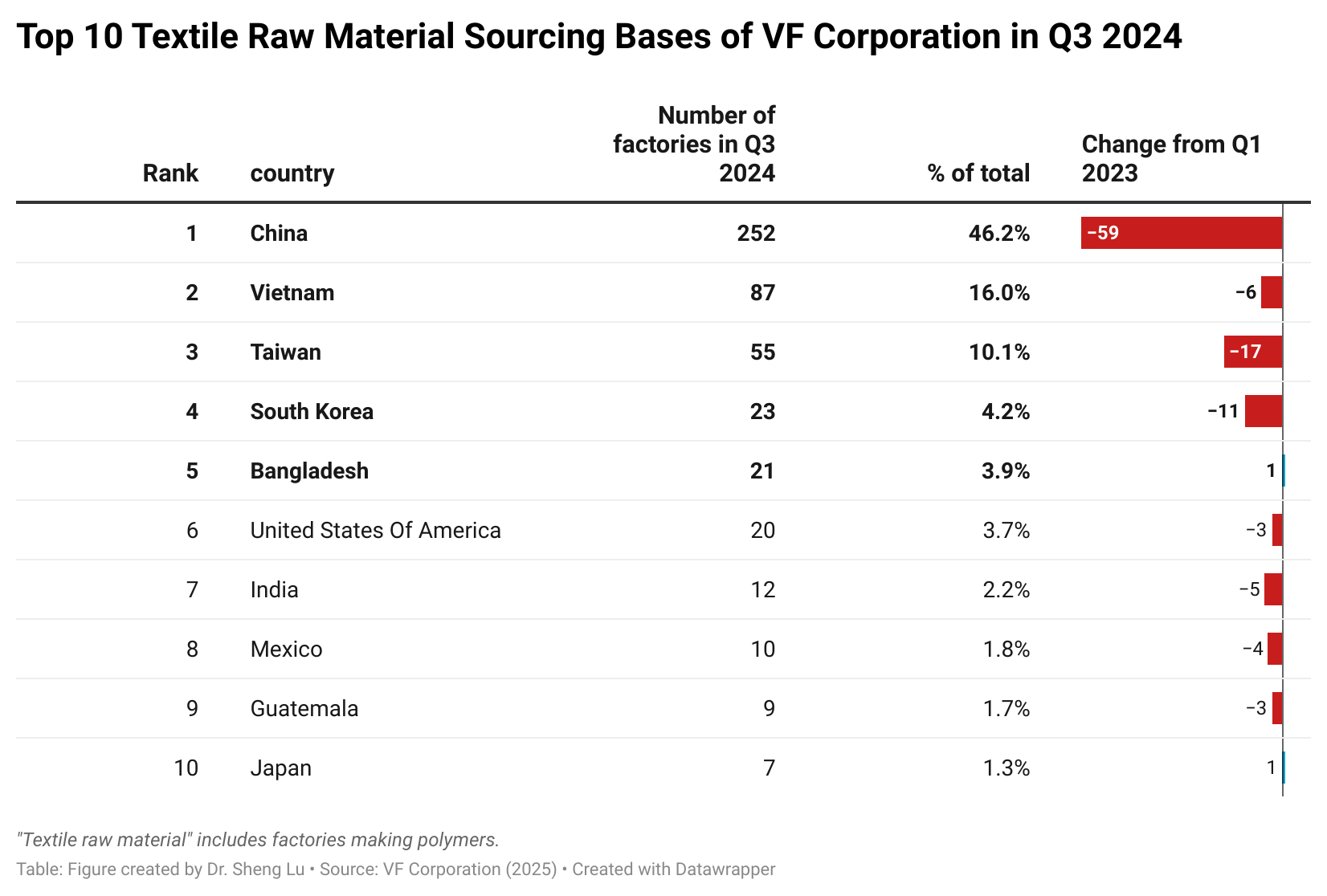

Third, compared to garments, VF’s supply of textile raw materials relies even more heavily on Asia, especially China. Specifically, as of Q3 2024, approximately 83.5 percent of VF’s textile raw material suppliers were located in Asia, the same as in Q1 2023. Notably, China represented nearly half of VF’s textile material suppliers in Q3 2024, including 41.2 percent of textile yarn and fabric mills and 50.9 percent of trim mills. Although VF reduced the number of textile mills in China from Q1 2023 to Q3 2024, China’s share of VF’s total textile raw material supplier base remained the same. Overall, the pattern aligns with previous research suggesting that finding alternative sourcing bases for textile raw materials outside of China and Asia will be more difficult and time-consuming for US fashion companies, considering the capital-intensive nature of making textile products.

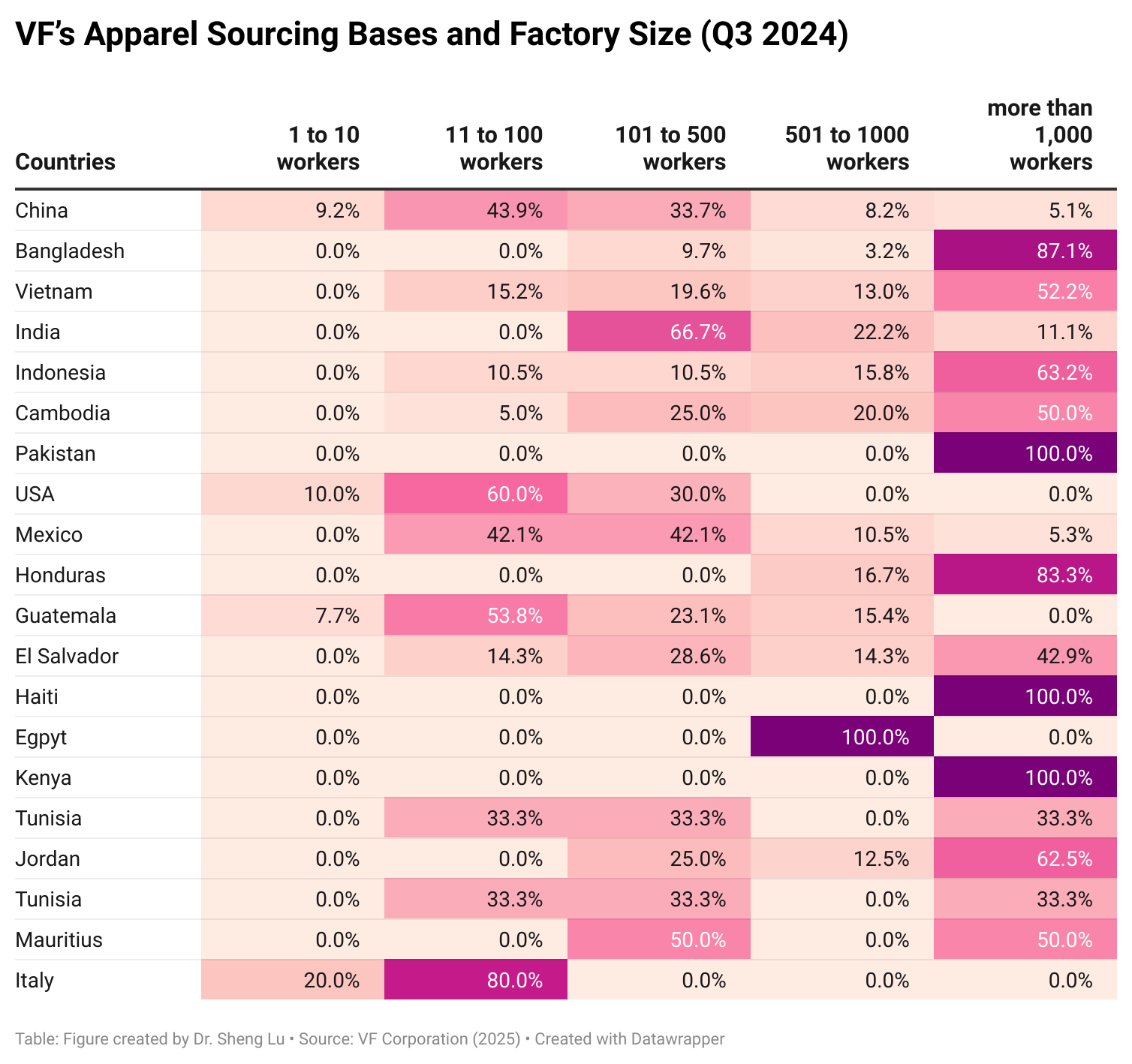

Fourth, VF’s contract garment factories worldwide varied in size, reflecting the company’s diverse sourcing needs. Specifically, in Asia, garment factories in China typically were small and medium-sized, with 11-100 workers (43.9 percent) or 101-500 workers (33.7 percent). In contrast, nearly 90 percent of VF’s contract garment factories in Bangladesh had more than 1,000 workers, with similar patterns observed in Vietnam (52.2 percent), Cambodia (50.0 percent), Indonesia (63.2 percent), and Pakistan (100 percent). These findings suggest that VF may use China as a sourcing base for relatively small, diverse orders while relying on other Asian countries with lower labor costs for high-volume production.

Meanwhile, in the Americas and Africa, VF’s contract garment factories in Haiti, Honduras, El Salvador, Kenya, and Jordan included more large-scale operations with over 1,000 workers. These locations could serve as emerging alternatives to sourcing from Asia, especially for specific categories. In contrast, VF’s contract garment factories in Mexico, the US, and Guatemala featured many medium and small operations, which are more likely to fulfill replenishment orders or produce specialized products.

About the interview: Fashion is possible because of international trade. Each year, the global fashion industry generates more than $4 trillion USD and provides families with affordable clothing options. However, as fast fashion continues to grow, so does awareness of pressing issues such as labor standards and environmental sustainability. How are the United States and China involved in the global fashion industry? How can they collaborate on the issues facing the global fast fashion industry, from production to consumption?

Sheng Lu joins the National Committee to discuss how fast fashion is a global phenomenon and how the United States and China can address common areas of concern.

In December 2024, Just-Style consulted a panel of industry experts and scholars in its Shape of apparel sourcing in 2025 briefing. Below is my contribution to the report. Welcome any comments and suggestions!

What’s next for apparel sourcing

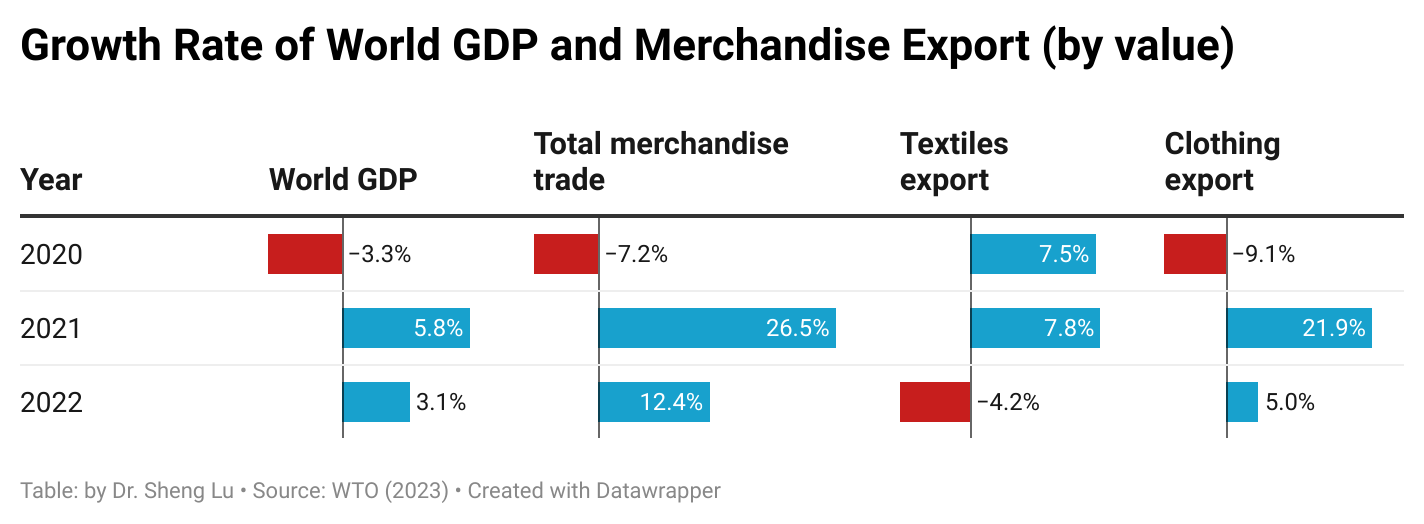

Although the world economy is predicted to grow at a similar pace in 2025 from 2024, the slowing US and Chinese economies could impose new challenges to apparel sourcing, from weakened demand to intensified price competition.

Regarding the macroeconomic environment in 2025, which “sets the tone” for apparel sourcing, the International Monetary Fund (IMF) and the World Bank estimated that the world economy would grow by approximately 2.7-3.2 percent in 2025, with almost no change from the previous year. Similarly, the World Trade Organization (WTO) projected that world merchandise trade would increase by 3.3 percent in 2025, slightly higher than 2.6 percent in 2024.

Despite this incremental improvement, the world’s two largest economies–the US (with 2.2 percent GDP growth in 2025, down from 2.8 in 2024 and 2.9 in 2023) and China (with 4.5 percent GDP growth in 2025, down from 4.8 in 2024 and 5.2 in 2023) are expected to experience slower economic growth in the new year ahead. This slowdown means that apparel producers around the world, particularly those developing countries making large-volume basic items, will likely continue to struggle with a shortage of souring orders in 2025 due to overall weak import demand.

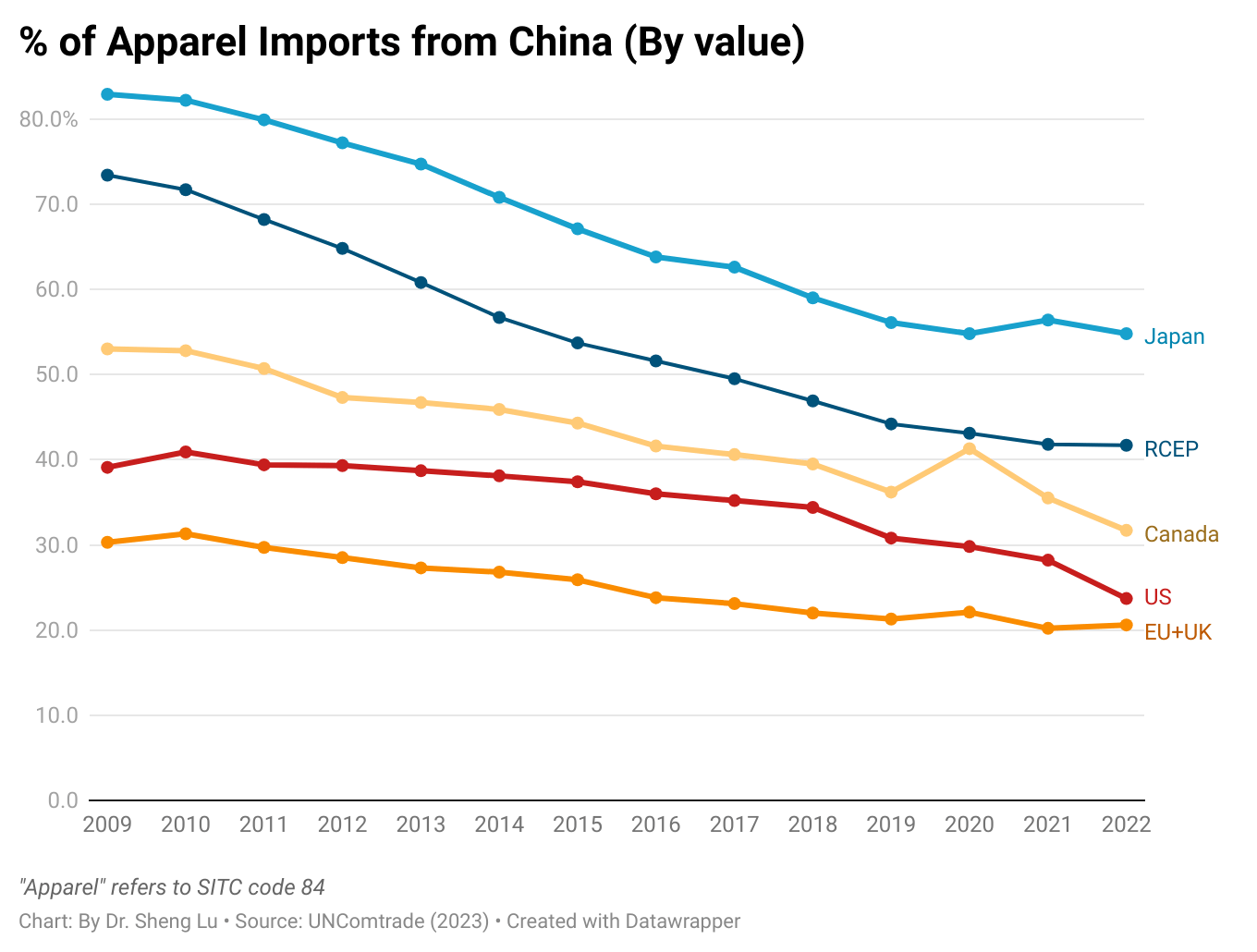

Even more concerning, as China grapples with declining domestic sales, the world clothing market could see an additional influx of low-cost Chinese products, especially through new e-commerce channels. Notably, less than half of China’s clothing production is exported, indicating its significant untapped export capacity. Furthermore, while China’s wage levels are higher than those in many other Asian apparel-producing countries, the unit price of U.S. apparel imports from China measured in dollar per square meter equivalent ($/SME) dropped by more than 21% between 2018 and 2024 (up to October). In contrast, U.S. apparel import prices from the rest of the world increased by 7.8% over the same period. Related to this, what is often overlooked is that even Shein, the “ultra-fast fashion” retailer known for its exceptionally competitive pricing, deliberately opted out of the vast Chinese market due to concerns about the intense price competition there. In other words, disregarding the new Trump tariff, 2025 could see an escalation of trade tensions targeting Chinese products in the US market and beyond.

Meanwhile, due to concerns about rising geopolitical tensions worldwide and trade policy uncertainty during Trump’s second term, fashion companies will likely continue to leverage sourcing diversification to mitigate risks. However, the “reducing China exposure” and sourcing diversification movement has yet to substantially benefit near-shoring or emerging sourcing destinations such as the Western Hemisphere and Sub-Saharan Africa (SSA). This result was mainly because fashion companies utilized China to source a wide range of various products, whereas Western Hemisphere and SSA suppliers can only produce a few basic categories.

For example, my latest studies show that in the first nine months of 2024, even excluding major platforms like Shein, Amazon, and Temu, US fashion companies sourced more than 60K Stock Keeping Units (SKUs) of clothing items from China. In comparison, India and Vietnam each supplied approximately 15K SKUs, Cambodia and Bangladesh each contributed 3,000 SKUs, Mexico provided only 2K SKUs, and CAFTA-DR and AGOA member countries supplied around 200 SKUs each. Therefore, even if fashion companies report sourcing from more countries, they are likely to stay sourcing from more Asian countries with closer export capacity and structure to China. Meanwhile, the total value or volume of trade may not fully capture the whole picture of sourcing diversification. This trend may persist in 2025, even with new tariff escalations.

Apparel industry challenges and opportunities

Today’s fashion business is highly global and relies heavily on the frequent movement of goods and services across borders. Thus, the uncertain and protectionist nature of U.S. trade policy during Trump’s second term could present significant challenges to the fashion industry in 2025. Of particular concern is that Trump’s new tariff actions would raise fashion companies’ sourcing costs, create additional inflationary pressure, reduce US consumers’ purchasing power on clothing, and trigger retaliatory trade measures from U.S. trading partners, ultimately hurting the U.S. economy. Notably, when the 7.5% Section 301 tariff was imposed on selected Chinese clothing products in 2018, the U.S. Consumer Price Index (CPI) growth was relatively low at 1.9%. However, imposing a 20% global tariff, a 60% tariff on Chinese products, and the existing 15%-30% regular tariff on clothing when the CPI is historically high is like “adding fuel to the fire.”

Besides tariffs, in 2025, if not sooner, U.S. fashion companies and many e-commerce suppliers worldwide will closely watch how Congress and the new Trump administration reform the de minimis rule, which currently exempts small-value shipments under $800 from tariffs and most customs procedures. With Trump’s new tariffs looming, some argue that closing the de minimis “loophole” has become even more urgent, as it creates more financial incentives to use the rule to bypass the tariff increase. Meanwhile, proposals under consideration suggest removing textile and apparel products entirely from de minimis, a move that could be an “earthquake” for those fashion companies utilizing the rule heavily.

Trump’s approach and philosophy toward conventional trade agreements and trade preference programs in 2025 also deserve attention. During his first term, Trump launched a few bilateral trade negotiations, from the one with the United Kingdom and Japan to Kenya. Back then, Trump saw a bilateral agreement would give the U.S. more leverage for a better “deal.” Specifically related to apparel sourcing and trade, two flagship U.S. trade preference programs–the African Growth and Opportunity Act (AGOA) and the Haiti HOPE/HELP Act, will expire in September 2025. It remains uncertain whether the new Trump administration will support the early renewal of these two trade preference programs with minimal changes or prefer to renegotiate them and add new bilateral elements.

Additionally, even though the new Trump administration may not prioritize addressing climate change, it is an irreversible trend for fashion companies to allocate more resources to comply with upcoming or newly implemented sustainability and environmental-related legislation, whether from the EU or the US state level. Unlike in the past, when being more sustainable only meant adding operational costs or paying a “one-time fee,” today’s new generation of sustainability-focused regulations—such as Extended Producer Responsibility (EPR)—requires companies to shift their mindset and demonstrate continuous improvement. Interestingly, my recent study tracking apparel products’ sustainability claims shows that vague terms like “sustainable” and “eco-friendly” are gradually being replaced by more neutral, fact-based keywords such as “regenerative,” “textile waste,” and “low impact.”

Meanwhile, offering “sustainable” apparel products and those using “preferred sustainable fibers” could provide fashion companies new opportunities to diversify their sourcing base and expand their vendor networks. For example, studies show that in the U.S. market, China and many other Asian countries are not necessarily the top suppliers of clothing made with recycled materials. Instead, Europe and countries in the Western Hemisphere or even Africa present unique sourcing advantages and capacities due to the unique nature of such products. Therefore, in 2025, we can expect an ever-closer collaboration between design, product development, merchandising, sourcing, and legal teams within fashion companies, working together to meet the growing demand for sustainable apparel and ensure compliance with evolving regulations.

Reflecting fashion companies’ interest in carrying more sustainable apparel products to meet consumers’ demand, there has been a notable increase in clothing using recycled cotton in the U.S. retail market since 2022. For example, based on information collected from US apparel retailers’ websites, only about 100 Stock Keeping Units (SKUs) of “Made in the USA” clothing explicitly indicated that they contained recycled cotton in 2022 and 2023, respectively. However, in the first nine months of 2024, this number had already doubled to around 200.

Despite the impressive growth, clothing containing recycled cotton remains a “niche” in the U.S. retail market. As of 2024, the total SKUs of “Made in the USA” clothing containing recycled cotton accounted for only about 0.1% of those made with regular virgin cotton.

Meanwhile, measured by SKU count, 70% of “Made in the USA” clothing containing recycled cotton was sold in the mass and value segments in the U.S. retail market from 2022 to 2024. In comparison, over the same period, “Made in the USA” clothing made with regular cotton catered to a more diverse consumer base, with a relatively balanced distribution across the mass and value segment (57%) and the luxury and premium segment (43%).

Product Features

There appears to be a notable distinction between the product categories of “Made in the USA” clothing using recycled cotton and those made with regular cotton. Specifically, from 2022 to 2024, by SKU count, “Made in the USA” clothing containing recycled cotton mainly focused on basics such as T-shirts (35.6%), jeans (20.1%), other bottoms (20.7%) and other tops (18.4%). Particularly, jeans appear more likely to contain recycled cotton than any other apparel category.

Using recycled cotton also appears to affect clothing’s design patterns. For example, from 2022 to 2024, nearly 85% of “Made in the USA” clothing containing recycled cotton chose plain design patterns compared to only 65% of those exclusively using regular cotton. These results echo findings from previous studies, suggesting that the shorter fiber length and lower quality of recycled cotton may limit the use of more intricate and complex design details.

Fiber Content

Reflecting the significant limitations of the quality and properties of the fiber, clothing labeled as using “100% recycled cotton” was rarely available in the U.S. retail market from 2022 to 2024, regardless of where the item was made. In most cases, recycled cotton accounted for no more than 30% of the total fiber content in a garment, with typical labels read like “49% cotton, 21% recycled cotton, 17% recycled polyester” (jeans), “Made from 70% cotton and 30% recycled cotton” (T-shirt), and “Made from 70% cotton, 29% recycled cotton, and 1% elastane” (skirt).

Results show that over 95% of “Made in the USA” clothing containing recycled cotton was blended with regular virgin cotton, and 92% of imported clothing did the same. According to textile scientists, this blend helps overcome the physical limitations of recycled cotton and enhances the fabric’s durability and softness. Approximately 14% of “Made in the USA clothing” containing recycled cotton was blended with polyester. This blend was commonly used for jeans and T-shirts to improve durability and flexibility and may also reduce production costs. However, compared with “Made in the USA” clothing made from regular cotton, it was uncommon to see recycled cotton blended with specific fiber types such as nylon, spandex, rayon, and linen. This result again revealed the physical limitations of recycled cotton and explained the narrow range of apparel products currently suited for its use.

Sustainability Claims

In practice, the sustainability claims of “Made in the USA” clothing containing recycled cotton in the U.S. retail market appear to be a “mixed bag.” On the one hand, as anticipated, “Made in the USA” clothing containing recycled cotton seems to be more likely to highlight its sustainability attributes than those using regular cotton only. From 2022 to 2024, by SKU count, more than 23.1% of “Made in the USA” items containing recycled cotton mentioned the word “sustainable” in the product description or label, and another 16.2% mentioned “eco-friendly.” In comparison, less than 2% of “Made in the USA” clothing made from regular cotton included these two terms. Similarly, a higher percentage of “Made in the USA” clothing using recycled cotton also featured other sustainability-related terms such as “impacts,” “waste,” and “certified,” compared to those made from regular cotton.

On the other hand, however, the sustainability claims of “Made in the USA” clothing containing recycled cotton are not without concerns. For example, in many cases, the product descriptions or labels provide no detailed and verifiable information about the actual “sustainability benefits” of producing and consuming clothing made from recycled cotton aside from vaguely saying the product was “sustainable,” “eco-friendly,” or “certified.”

To complicate the issue further, as clothing made from regular cotton increasingly emphasizes its sustainability benefits as a natural fiber, it somehow diminishes the exclusivity of recycled cotton as a sustainable option. For example, there is no clear evidence indicating that consumers generally perceive clothing using “recycled cotton” as more or less sustainable than those using “organic cotton” or cotton certified by reputable programs such as the “Better Cotton Initiative, BCI” and the “U.S. Cotton Trust Protocol.” In other words, “recycled cotton” faces intense competition as the preferred sustainable fiber among many choices available to fashion companies, including regular cotton.

Pricing Practices

Results show that “Made in the USA” clothing containing recycled cotton is not always “cheap” for U.S. consumers. For instance, for those targeting the mass market segment, between 2022 and 2024, adding recycled cotton increased the selling price of “Made in the USA” clothing by more than 10% compared to items made with virgin cotton, with jeans being the only exception (i.e., 12% lower).

Price data also show that “Made in the USA” recycled cotton items generally have higher price tags than comparable non-U.S.-made items across both mass and premium markets, particularly in popular categories like T-shirts and bottoms. This trend suggests that higher U.S. domestic production costs, particularly the higher wage level than Asian countries, could contribute to these elevated prices.

Reflections

As the findings highlighted, while visibility is increasing, promoting recycled cotton in clothing still encounters significant challenges. For instance, technical advancements in the quality of recycled cotton fiber are critical to enhancing its competitiveness among other “preferred sustainable fibers,” raising its perceived market value and enabling its use across a broader range of clothing categories beyond T-shirts and jeans.

Notably, due to slow progress in improving the physical properties of recycled cotton, some have seemingly “given up” on using it for clothing and suggest focusing more on repurposing recycled cotton for other categories, such as non-wovens, carpets, packaging, and home textiles. However, as sustainability legislation, such as the Extended Producer Responsibility (EPR) law, increasingly mandates fashion companies to recycle textile waste, not promoting recycled cotton could lead to greater reliance on recycled polyester or other man-made fibers in clothing, which may not serve the long-term business interests of the cotton industry.

by Katherine Yasik(Fashion Design and Product Innovation major & Sustainable apparel minor, Fashion and Apparel Studies, University of Delaware) and Sheng Lu

Implemented in June 2022, the Uyghur Forced Labor Prevention Act (UFLPA) prohibits U.S. companies from importing apparel wholly or in part produced in China’s Xinjiang region. UFLPA could significantly alter U.S. apparel import patterns as fashion companies have begun or anticipate adjusting their sourcing base to comply with the law and mitigate the forced labor risks in the supply chain.

This study quantitatively evaluated the impacts of the UFLPA on U.S. apparel imports nearly two years after the law’s implementation. Unlike existing studies primarily focusing on UFLPA’s political or legal aspects, this study’s findings would enhance our understanding of the economic and trade implications of the new law.

A panel regression model was adopted to evaluate the quantitative impact of UFLPA on U.S. apparel imports based on data collected from OTEXA (2024) and USITC (2024), the most authentic government data source. Four countries in three categories were included in the study: 1) China; 2) Vietnam and Bangladesh representing top Asian apparel exporting countries other than China; 3) member countries of the Central America Free Trade Agreement (CAFTA-DR) representing near-shoring sourcing destinations. The annual trade activities of these four countries from 2010 to 2023 (the latest available) were used for the analysis.

The panel regression model suggests several interesting findings*:

Firstly, the results showed that holding other factors constant, U.S. cotton apparel imports from China decreased significantly by approximately 350 million square meter equivalent (SME) annually following UFLPA’s implementation. In other words, the result confirmed that UFLPA had negatively affected U.S. cotton apparel imports from China. This result is far from surprising as Xinjiang accounted for nearly 90% of China’s cotton production, causing significant forced labor risks associated with importing cotton apparel from China.

Secondly, holding other factors constant, U.S. cotton apparel imports from Vietnam and Bangladesh and CAFTA-DR also respectively decreased by approximately 81 million SME, 51 million SME, and 20 million SME annually after UFLPA’s implementation in 2022. The results revealed U.S. fashion companies’ concerns about UFLPA compliance risks associated with sourcing from countries other than China, particularly Asia, due to their heavy reliance on cotton yarns and fabrics from China through a highly integrated regional supply chain.

Thirdly, the results revealed a more significant positive relationship between U.S. cotton exports to China, Vietnam, Bangladesh, and CAFTA-DR countries and U.S. cotton apparel imports from these countries after UFLPA’s implementation. Related, trade data also showed a declining ratio of U.S. cotton apparel imports from China, Vietnam, Bangladesh, and CAFTA-DR countries relative to these countries’ cotton imports from the U.S. This pattern implies a closer alignment in the trade flow of raw cotton from the U.S. to these countries and the return of finished cotton apparel to the U.S. It could be the case that leading apparel exporting countries increasingly used US cotton after UFLPA to mitigate the forced labor risks.

Additionally, there was a negative relationship between U.S. cotton apparel imports from China, Vietnam, Bangladesh, and CAFTA-DR members and U.S. MMF apparel imports from these countries. In other words, cotton apparel and MMF apparel appear to compete within the total U.S. apparel import market. However, UFLPA’s implementation has not significantly impacted the relationship. Nonetheless, MMF apparel has accounted for a growing share of China’s total apparel exports to the United States after UFLPA’s implementation (down from 46% in 2010 to only 19% in 2023).

The study’s findings revealed a broad trade impact of UFLPA’s implementation that goes far beyond China. Notably, cotton apparel exporters from other Asian countries and those in the Western Hemisphere also appeared to be negatively affected by the new law. Also, unlike theoretical prediction, no clear evidence shows that UFLPA has significantly expanded the near-shoring of U.S. cotton apparel imports from the Western Hemisphere, such as CAFTA-DR members.

Meanwhile, the results call for further investigation of the net impact of UFLPA on U.S. cotton exports. While UFLPA may help U.S. cotton gain more shares in the global marketplace, the reduced U.S. import demand for cotton apparel due to forced labor risk concerns may also unexpectedly “shrink the pie size.”

*:The fixed effects (FE) model was selected for the study based on the likelihood ratio test results (p<.01). The result of the F-test suggests the FE model is statistically significant at the 99% confidence level (p<.01). The value of R2 exceeds 0.90, indicating an overall high goodness-of-fit of the panel regression. All the independent variables were statistically significant at the 99% confidence level (p<.01).

By Sheng Lu and Emilie Delaye

Note: The study will be presented at the 2024 International Textile and Apparel Association (ITAA) annual conference in November 2024.

The event was hosted by the Washington International Trade Association on October 9, 2024

Panelists

Ralph Carter, Staff Vice President, Regulatory Affairs, FedEx

Kim Glas, President & CEO, National Council of Textile Organizations; Commissioner, U.S.-China Economic and Security Review Commission

Melissa Irmen, Director of Advocacy, NAFTZ-National Association of Foreign-Trade Zones

John Pickel, Senior Director, International Supply Chain Policy, National Foreign Trade Council

Felicia Pullam, Executive Director, Office of Trade Relations, U.S. Customs and Border Protection

Ana Swanson, Trade and International Economics Reporter, The New York Times (Moderator)

Event summary: Competing views about de minims and its reform

Arguments supporting De Minimis: Proponents like Ralph from FedEx argue that de minimis reduces trade friction, drives international supply chain efficiency, and allows U.S. companies to offer competitive pricing through free returns and streamlined customs processes. Meanwhile, they argue that the de minimis supports low-income U.S. consumers and enables small U.S. businesses to remain competitive.

Criticism of De Minimis: Critics, including Kim Glas from the National Council of Textile Organizations (NCTO), argue that it undercuts U.S. manufacturers, especially in industries like textiles, by allowing cheap imports from countries like China, often bypassing tariffs and safety regulations. They also say that de minimis was unfair to U.S. retailers that pay millions of dollars of tariff duties. Additionally, there are significant concerns about the safety risks posed by counterfeit goods and dangerous products (e.g., fentanyl) entering under de minimis exemptions.

Challenges of dealing with de Minimis: Felicia from the U.S. Customs and Border Protection (CBP) emphasizes the strain on the agency’s resources due to the sheer volume of de minimis shipments—it surged from about 2.8 million shipments per day in fiscal year 2023 to close to 4 million shipments per day in fiscal year 2024. She highlighted challenges such as the often unreliable information the de minimis imports submitted and the outdated authorities that hinder CBP’s enforcement.

Equal treatment for U.S. Foreign Trade Zones: U.S. Foreign Trade Zones (FTZs) are designated areas within the United States that are considered outside U.S. customs territory for import duties. They allow businesses to import, store, assemble, manufacture, or process goods with deferred or reduced customs duties, which are only paid when goods leave the FTZ and enter U.S. commerce. Currently, U.S. FTZs do not benefit from the de minimis exemption, meaning goods imported directly into the U.S. from overseas warehouses can qualify for de minimis, but goods entering through U.S. FTZs do not.

Melissa Irmen from NAFTZ-National Association of Foreign-Trade Zones advocates for U.S. foreign trade zones to be given the same de minimis privileges as foreign warehouses, arguing that this would ensure better oversight and security while maintaining trade efficiency. Critics, however, say that expanding de minimis in this way would exacerbate the problem rather than fix it.

Reforming the De minimis: There is a push for comprehensive reform of the De minimis system, with proposals ranging from raising duties on certain products to eliminating the exemption altogether for specific categories of goods (e.g., textiles, products subject to Section 301 tariffs).

Particularly, in a face sheet released in September 2024, the Biden Administration announced it would address “the significant increased abuse of the de minimis exemption, in particular China-founded e-commerce platforms.” The announcement said the Biden Administration would issue a Notice of Proposed Rulemaking that would exclude from the de minimis exemption all shipments containing products covered by tariffs imposed under Sections 201 or 301 of the Trade Act of 1974, or Section 232 of the Trade Expansion Act of 1962. The announcement also called for Congress to pass new legislation to reform the de minimis rule comprehensively.

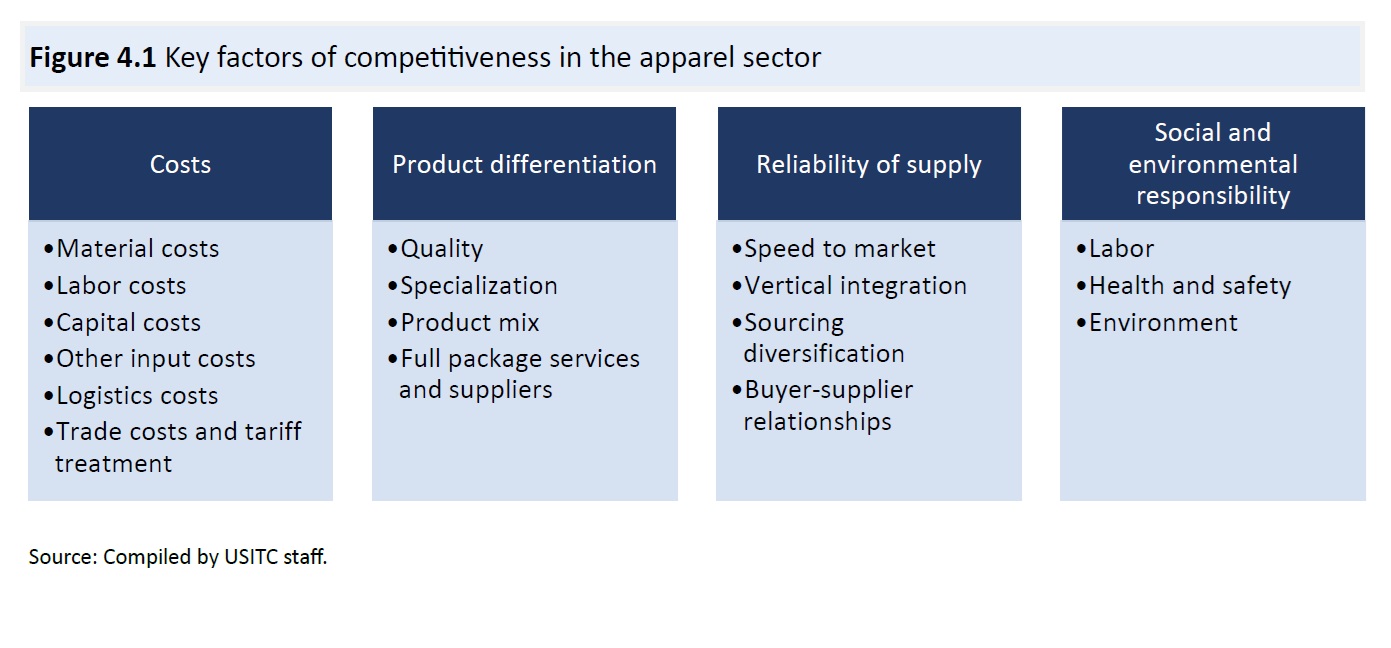

The United States International Trade Commission (USITC) released its new fact-finding report examining the competitiveness of Bangladesh, Cambodia, India, Indonesia, and Pakistan as apparel suppliers to the United States. The study was conducted in 2024 based on input from secondary sources (e.g., trade statistics, public hearings, and desk studies) and fieldwork. Below are summaries of the key findings regarding apparel export competitiveness.

Factors that affect export competitiveness in the global apparel sector

One key issue the study explored is what factors affect a country’s apparel export competitiveness and how to become a preferred apparel sourcing base for U.S. fashion companies.

The studies suggest that four types of factors are most important (see the figure above). However, consistent with existing literature, the USITC report could not determine which factor is decisive in fashion companies’ apparel sourcing decisions. For example, the report found that:

“cost—the price buyers pay their suppliers—plays a key role in sourcing decisions, although opinions vary regarding the importance of cost relative to other factors.”

“Depending on the product, target consumer, and identity of a brand or buyer, apparel buyers will place varying degrees of importance on product differentiation factors such as quality, specialization, product mix, and full package offerings, which include design services, finishing, packaging, and logistics.”

“The emphasis on reliability has particularly grown in response to various recent disruptions to global apparel supply chains such as a global pandemic, geopolitical conflicts, and trade policy.”

“Although emerging research suggests that compliance programs concerning wages, social inclusion, and climate change mitigation may increase competitiveness, buyers and brands remain divided on the topic…the relative importance, or “weight,” of such compliance in sourcing decisions remains a topic of active study and discussion within the industry.”

Cost and export competitiveness

The USITC report highlighted the complex and nuanced relationship between “costs” and a country’s apparel export competitiveness. Several patterns are noteworthy:

Apparel is a buyer-driven industry, meaning “the global apparel supply chain gives buyers the power to negotiate based on price, which can push down prices and transfer greater costs to the supplier.”

The ability to produce textile raw materials locally can provide cost advantages in garment production—“Material inputs are widely recognized as the largest component in the cost of a final apparel product, and these prices are largely determined by the presence of a domestic textile industry or costs of importing textiles.”

It is difficult to compare wages across countries to measure labor competitiveness. In particular, low labor costs “do not reflect the true cost of doing business (e.g., via wage suppression)” in a country and “they can harm a country’s reputation for social compliance and negatively affect labor productivity.”

Buyer-supplier relationships in apparel sourcing

The USITC report revealed some positive developments in the buyer-supplier relationships involving U.S. fashion companies.

Fashion companies increasingly recognize the value of building long-term relationships with their vendors. Buyers emphasize that maintaining these relationships is a key factor in sourcing decisions, largely due to the cost and time involved in finding and establishing relationships with new suppliers.

Fashion companies’ efforts to improve supply chain transparency and traceability also need “suppliers who will act in line with their brand’s values.”

Suppliers benefit from the long-term relationship, too. As the USITC report noted, some fashion companies guarantee suppliers a particular profit margin to ensure their continued operation. Additionally, some buyers gain a deep understanding of their suppliers’ cost structures, enabling them to calculate the costs of compliance with various standards and assist suppliers in reducing costs where possible.

Subcontracting is still regarded as necessary for the garment industry. As noted in the USITC report, apparel orders fluctuate seasonally, making it impractical for suppliers to hire additional permanent workers or invest in machinery for peak demand. To meet buyer expectations during busy periods, manufacturers often subcontract parts of orders and increase overtime or rely on temporary contract workers. This practice is seen as essential for ensuring a reliable supply of apparel.

Social and environmental responsibility and apparel sourcing

The USITC report acknowledged the growing importance of social and environmental compliance to a country’s apparel export competitiveness. However, the relationship remains complex.

The extent to which voluntary social and environmental responsibility programs and their associated auditing practices have influenced outcomes, especially regarding worker rights, remains unclear.

Suppliers report that the increased frequency of flooding and high temperatures due to climate change negatively affect their ability to meet labor and environmental standards.

Increased compliance with social and environmental standards raises supplier costs, negatively impacting their cost competitiveness. Many stakeholders note that while brands and consumers demand greater responsibility, this often does not come with a “price premium” for suppliers, who ultimately absorb these increased costs.

Note: The USITC report also evaluated the export competitiveness of each apparel-exporting country it examined, including their respective competitive advantages and issues to address.

Part I: Watch the following two videos on tariffs—one from an economic perspective and the other from a political perspective.

Part II: Check the respective tariff rate for the following products by copying and pasting the HS code into the search box

Product 1 (men’s and boys’ overcoat, cotton): HS code 6101.20.00

Product 2 (cotton): HS code 5201.00.05

Product 3 (smartphone): HS code 8517.13.00

Discussion question: Based on the videos and your findings, how would you explain the differences in tariff rates for these products? Do you think tariffs are still necessary in the 21st century?

How does the video enhance your understanding of the complexity of apparel supply chain and sourcing? What is your evaluation of Ferrara Manufacturing’s strategies and best practices for maintaining apparel production in New York? Are high-end luxury brands the only viable opportunity for apparel “Made in the USA”? Feel free to share your thoughts and other reflections on the video.

#1 Respondents reported growing sourcing risks of various kinds in 2024, from navigating an uncertain U.S. economy, managing forced labor risks, and responding to shipping and supply chain disruptions to facing rising geopolitical tensions and trade protectionism.

Over half of the respondents ranked “Inflation and economic outlook in the U.S.” and “Managing the forced labor risks in the supply chain” as their top business challenges in 2024.

The issues of “Shipping delays and supply chain disruptions” and “Managing geopolitics and other political instability related to sourcing” have newly emerged among respondents’ top five concerns in 2024.

About 45 percent of respondents rated “Protectionist trade policy agenda in the United States” as a top five business challenge this year, a jump from only 15 percent in 2023.

#2 U.S. fashion companies leverage sourcing diversification to respond to the growing sourcing risks and market uncertainty in 2024.

Nearly 70 percent of large-sized companies with 1,000+ employees reported sourcing from ten or more countries, significantly higher than the 45-55 percent range in the past few years. It also has become more common for medium to small-sized companies with fewer than 1,000 employees to source apparel from six or more countries in 2024 than in the past.

Nearly 80 percent of respondentsplan to source from the same number of countries or even more countries through 2026, aiming to mitigate sourcing risks more effectively. However, their approaches differ at the firm level—some U.S. fashion companies plan to work with fewer vendors, while others intend to source from more.

#3 Managing the risk of forced labor in the supply chain continues to be a top priority for U.S. fashion companies in 2024.

U.S. fashion companies have adopted a comprehensive approach to comply with UFLPA and mitigate forced labor risks. On average, each surveyed company has implemented approximately six distinct practices across various aspects of their business operations this year, up from an average of five in 2023.

More than 90 percent of respondents say they are “Making more efforts to map and understand our supply chain, including the sources of fibers and yarns contained in finished products.” Notably, nearly 90 percent of respondents report mapping their entire apparel supply chains from Tier 1 to Tier 3 in 2024, a significant increase from about 40 percent in the past few years.

More than 80 percent of respondents say they “intentionally reduce sourcing from high-risk countries” in response to the UFLPA’s implementation. Another 75 percent of respondents explicitly state that their company has “banned the use of Chinese cotton in the apparel products” they carry.

About 45 percent of respondents have been actively “exploring sourcing destinations beyond Asia to mitigate forced labor risks.” However, this year, fewer respondents (i.e., under 10 percent) plan to cut apparel sourcing from Asian countries other than China directly, implying a more targeted and balanced approach to mitigating risks and meeting sourcing needs.

Based on field experience, respondents call for greater transparency in U.S. Customs and Border Protection (CBP)’s UFLPA enforcement, specifically in shipment detention and release decisions and in targeted entities and commodities information. Respondents also suggested that CBP reduce repeated detentions, focus on “bad actors” only, clarify enforcement on recycled cotton, and continue to partner with U.S. fashion companies on UFLPA enforcement.

#4 U.S. fashion companies remain deeply concerned about the deteriorating U.S.-China bilateral relationship and plan to further “reduce China exposure” to mitigate risks.

A record 43 percent of respondents sourced less than 10 percent of their apparel products from China this year, compared to only 18 percent in 2018. Likewise, nearly 60 percent of respondents no longer use China as their top apparel supplier in 2024, much higher than the 25-30 percent range before the pandemic.

Respondents rated China as economically competitive as an apparel sourcing base compared to many of its Asian competitors regarding vertical manufacturing capability, relatively low minimum order quantity (MOQ) requirements, flexibility and agility, sourcing costs, and speed to market. However, non-economic factors, particularly the perceived high risks of forced labor and geopolitical tensions, are driving U.S. fashion companies to move sourcing out of China. This trend applies to surveyed U.S. fashion companies selling products in China.

Nearly 80 percent of respondents plan to reduce their apparel sourcing from China further over the next two years through 2026. Consistent with last year’s results, large-size U.S. fashion companies with 1,000+ employees currently sourcing more than 10 percent of their apparel products from China are among the most eager to “de-risk.”

#5 U.S. fashion companies are actively exploring new sourcing opportunities, with a particular focus on emerging destinations in Asia and the Western Hemisphere.

This year, more respondents reported sourcing from India (89 percent utilization rate) than from Bangladesh (86 percent utilization rate) for the first time since we began the survey. Also, nearly 60 percent of respondents plan to expand apparel sourcing from India over the next two years, exceeding the planned expansion from any other Asian country.

For the second year in a row, three non-Asian countries made it to the top ten most utilized apparel sourcing destination list in 2024, including Guatemala (ranked 7th), Mexico (ranked 7th), and Egypt (ranked 10th). All three countries also witnessed an improved utilization rate in 2024 compared to last year’s survey results.

This year, a new record 52 percent of respondents plan to expand apparel sourcing from members of the Dominican Republic-Central American Free Trade Agreement (CAFTA-DR), over the next two years, up from 40 percent in 2023. However, most U.S. fashion companies consider expanding near-shoring from the Western Hemisphere as part of their overall sourcing diversification strategy. For example, nearly ALL companies that plan to increase sourcing from CAFTA-DR over the next two years also plan to increase sourcing from Asia.

75 percent of respondents identified the “lack of sufficient access to textile raw materials” as the main bottleneck preventing them from sourcing more apparel from CAFTA-DR members. Respondents say the local manufacturing capability for yarns and fabrics using fiber types other than cotton and polyester, such as spandex, nylon, viscose, rayon, and wool, was modest or low in the CAFTA-DR region, even when including the United States.

The U.S.-Mexico-Canada Trade Agreement (USMCA) entered into force on July 1, 2020, replacing the North American Free Trade Agreement (NAFTA). Within the context of expanding nearing-shoring from the Western Hemisphere, in 2024, about 65 percent of respondents reported sourcing from Mexico and Canada (or USMCA members), a noticeable increase from about 40 percent in 2019-2020. About 36 percent of respondents say their companies “expanded apparel sourcing from USMCA members because of the agreement.”

#6 Respondents underscore the importance of immediate renewal of AGOA before its expiration in September 2025 and extending the agreement for at least another ten years.

This year, respondents reported sourcing from seven AGOA members or countries in Sub-Saharan Africa (SSA), including Lesotho, Ethiopia (note: lost AGOA eligibility in 2022), Kenya, Madagascar, Mauritius, Tanzania, and Ghana, an increase from four countries in 2023, and six countries in 2022. Most respondents sourcing from AGOA in 2024 are typically large-scale U.S. fashion brands or retailers with 1,000+ employees. Generally, these companies treat AGOA as part of their extensive global sourcing network.

Over 86 percent of respondents support renewing AGOA for at least another ten years, and none object to the proposal. This reveals U.S. fashion companies’ strong support for the trade preference program and the non-controversial nature of continuing this agreement.

Over 70 percent of respondentssay another 10-year renewal of AGOA is essential for their company to expand sourcing from the region.

About 30 percent of respondents reported that they had already held back sourcing from AGOA members due to the pending renewal of the agreement and associated policy uncertainty. This figure could increase to half of the respondents if AGOA is not renewed by the end of 2024.

Another 30 percent of respondents indicate that keeping the flexible rules of origin in AGOA, such as the “third country fabric provision” for least-developed members, is essential for their company to source from the region.

Other topics the report covered include:

5-year outlook for the U.S. fashion industry, including companies’ hiring plan by key positions

The competitiveness of major apparel sourcing destinations in 2024 regarding sourcing cost, speed to market, flexibility & agility, minimum order quantity (MOQ), vertical integration and local textile manufacturing capability, social and environmental compliance risks and geopolitical risks (assessed by respondents)

Respondents’ detailed sourcing portfolio in 2024 for garments and textile materials (i.e., yarns, fabrics and accessories)

Respondents’ latest strategies to mitigate forced labor risks in the supply chain and fashion companies’ suggestions for CBP’s UFLPA enforcement based on field experience

U.S. fashion companies’ latest social responsibility and sustainability practices related to sourcing

U.S. fashion companies’ trade policy priorities in 2024

About the study

This year’s benchmarking study was based on a survey of executives from 30 leading U.S. fashion companies from April to June 2024. The study incorporated a balanced mix of respondents representing various businesses in the U.S. fashion industry. Approximately 80 percent of respondents were self-identified retailers, 60 percent were self-identified brands, 41 percent were importers/wholesalers, and 3 percent were manufacturers.

The survey respondents included large U.S. fashion corporations and medium-sized companies. Around 80 percent of respondents reported having over 1,000 employees; the rest (20 percent) represented medium-sized companies with 100-999 employees.

The new punitive tariffs on Chinese steel and aluminum: The overcapacity problem in the steel industry globally could raise national security concerns. While the Biden Administration is more focused on outreach to allies and partners to address the issue collectively, the Trump Administration took a different approach with the Section 232 tariffs specifically targeting China. However, the impact of China-targeted measures could be muted due to the limited amount of US steel imported from China today. The next administration is expected to face the challenge of addressing global overcapacity in various industries. Like it or not, tariffs seem to be one of the few tools available to the US government to tackle these issues directly.

Currency debate: “Currency manipulation” refers to the deliberate actions taken by a country’s government or central bank to artificially influence the value of its currency in the foreign exchange market. When a foreign government deliberately lowers the value of its currency, it could result in more US imports from that country and hurt the price competitiveness of US exports. While currency manipulation has not been a significant concern in recent years, the recent strength of the US dollar against other currencies, such as the Japanese yen, Chinese yuan, and Vietnamese dong, may reignite debate over the issue. The Biden Administration struggles to fight high inflation using high-interest rates, making it extremely challenging to “devalue the US dollar” in a macro sense. In comparison, the second Trump administration could designate countries of concern as currency manipulators, followed by new retaliatory measures, including tariffs or other trade barriers.

Industrial policy and subsidy: The Biden administration has packaged industrial policy as a core pillar of “Bidenomics,” which has pledged more than $805 billion in new subsidies for semiconductor manufacturing and research, climate and energy investments, and infrastructure spending. In comparison, the Republicans would be more inclined to let market forces determine the outcome of these policies rather than funding them through the government. It is also likely that the second Trump administration will tighten certain rules related to foreign entities taking advantage of US tax credits. However, there could be coordinated investments and supply chain resilience efforts in Biden and Trump’s second term, such as tactical coordination to prevent global subsidy races and disruptions in supply chains.

Trade policy as a tool for other issues: Reviving the Trans-Pacific Partnership (TPP) or similar mid-2010s era trade agreements was slim during the Biden administration. Instead, the Biden administration prioritizes a climate and trade agenda, as evidenced by the launch of a new White House Climate and Trade Task Force. Biden administration will continue to prioritize investments in domestic production capacity while looking outward to use trade to support other non-trade objectives.

In comparison, the Trump administration was more aggressive in pushing back against protectionist trade measures against US products but also less optimistic about the willingness of other countries to engage in good-faith negotiations with the US. Further, Trump 2.0 will likely return to trade policies similar to his first term, including potential tariffs of up to 60% on Chinese imports and an across-the-board tariff of 10% on all imports. Further, there is bipartisan support for increasing tariffs on Chinese goods, considering the deteriorating bilateral relationship. However, a 10% global tariff on imports from countries like Switzerland and Ireland could be more controversial due to potential consumer price impacts and damage to US alliances.

Discussion questions:

Any of the aforementioned issues could potentially impact fashion apparel companies? Why?

In your view, is it preferable for the textile and apparel industry not to be a focus of US trade policy? Why?

What are your top 1-2 takeaways from the panel discussion?

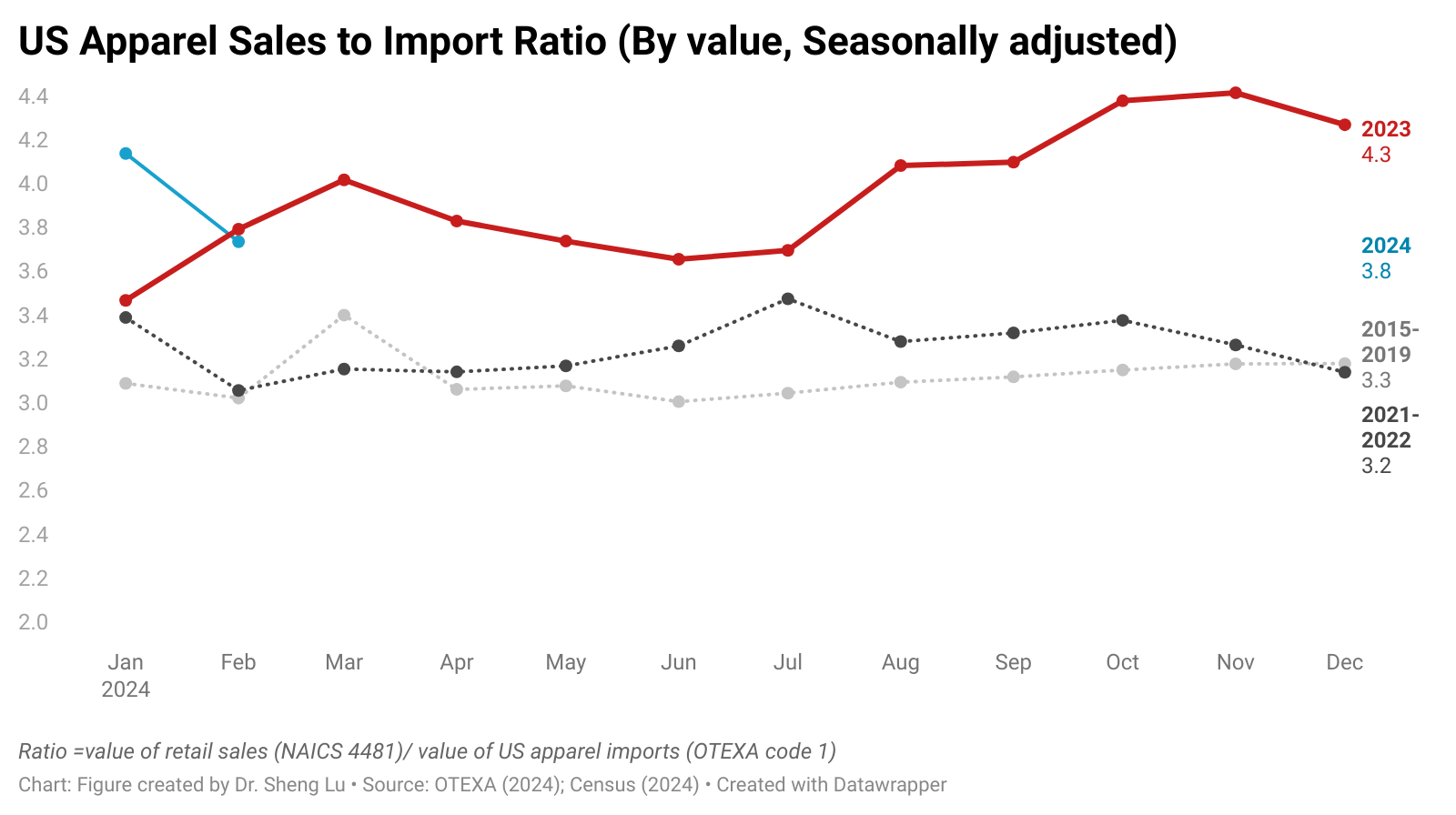

The latest US apparel import data raises several puzzles that deserve to be investigated further.

Question 1: Why did imports suddenly surge, and is this surge sustainable?

Unexpectedly, US apparel imports experienced a significant surge in February 2024. This surge was marked by a 12.9% increase in quantity and a 2.9% increase in value compared to the previous year. Seasonally adjusted US apparel imports in February 2024 were also nearly 10% higher than in January 2024. The import surge was particularly surprising given that the value of US clothing sales in February 2024 was only 1.3% higher than a year ago and even 0.5% lower than in January 2024 (seasonally adjusted).

Therefore, it will be important to watch whether the US apparel trade has indeed reached a turning point and will continue growing in the coming months and throughout the year.

Question 2: Could the volume of US apparel imports in 2023 have been underreported?

With over 98% of clothing sold in the US retail market being imported today, there exists a strong correlation between US apparel retail sales (NAICS code 4481) and the volume of apparel imports. Between 2015 and 2022, the US clothing sales to clothing import ratio remained consistently around 3.0-3.2 (seasonally adjusted). In other words, the value of retail sales was approximately three times the value of apparel imports. However, in 2023, this ratio increased to 4.0-4.5.

One suspicion is that as more apparel imports came into the US through the de minimis, the official US apparel import data in 2023 was somewhat underreported. Notably, according to Euromonitor, about 40% of US apparel retail sales were achieved through e-commerce in 2023, a substantial increase from 9.4% in 2010. Likewise, with US customs tightening controls on “small package shipments” and enhancing UFLPA enforcement, more imports likely began entering through the standard procedure in recent months, which explains why the US apparel sales to import rato fell back to 3.8 in February 2024.

On the other hand, some say the lowered US apparel import volume in 2023 was due to retailers’ efforts to control inventory levels. Data shows that US clothing stores’ stock-to-sales ratio in the last quarter of 2023 averaged 2.34, slightly lower than 2.43 from 2015 to 2019, but was higher than 2.19 back in 2021. In other words, while there was some effort by retailers to control inventory (as seen by the ratio being lower than pre-pandemic levels), it wasn’t a significant enough change to have a large impact on import demand. Also, considering that apparel is a seasonal product, it doesn’t seem too likely that retailers would risk losing sales opportunities during the most critical selling season of the year (i.e., 4th quarter) by promoting outdated items instead of stocking new ones on the shelf.

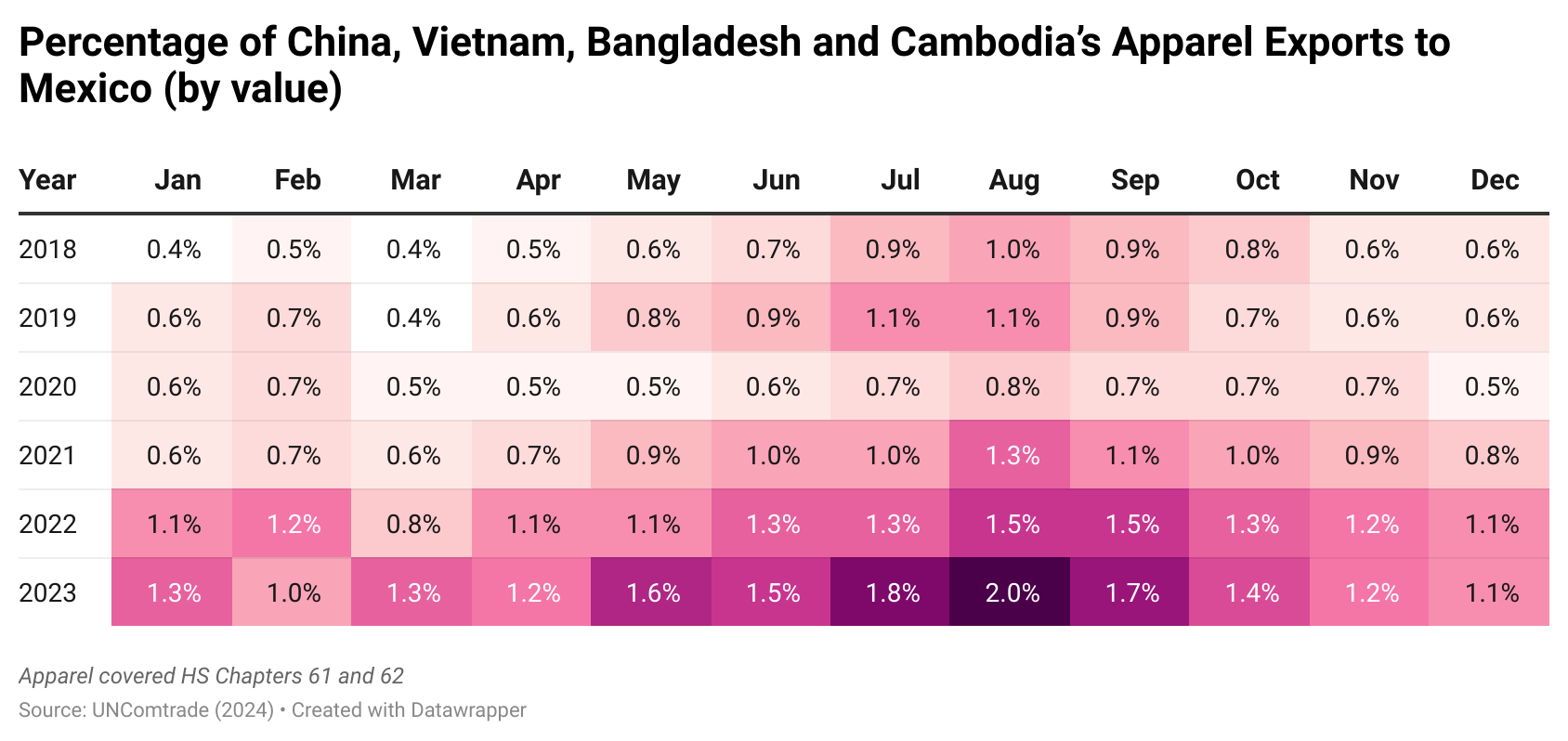

Question 3: Why did Asian countries export more apparel to Mexico?

As a developing country, Mexico is not traditionally a leading apparel import market due to consumers’ limited purchasing power and the sufficient local apparel supply. Take China, Vietnam, Bangladesh, and Cambodia, the four top Asian apparel exporting countries (Asia4), for instance. Between 2018 and 2020, Mexico typically accounted for 0.4%-0.7% of Asia4’s total apparel exports. However, since 2022, Asia4 has almost doubled its apparel exports to Mexico (i.e., increased to 1.5%-2.0%). Moreover, during the same period, the percentage of Asia4’s apparel exports to the United States declined from 27% to below 20%, especially in the last quarter of 2023.

What’s behind the increase in Asian countries’ apparel exports to Mexico needs to be investigated further. As noted earlier, Mexico itself is a leading apparel-producing country. Also, according to Euromonitor, the clothing market in Mexico stayed relatively stable at around 7.6%-7.9% of the size of the US from 2017 to 2023 (in quantity). In other words, Mexico’s increased import demand for Asian clothing doesn’t make much sense.

Others suspect some Asian apparel exports to Mexico eventually entered the US market either by taking advantage of the de minimis rule or the US-Mexico-Canda (USMCA) trade agreement. However, the exact size of this particular trade flow calls for further investigation.

#1: On April 5, 2024, the US Department of Homeland Security (DHS) released its new enhanced strategy to combat illicit trade and level the playing field for the American textile industry and the estimated over 500,000 US textile jobs*. *note: according to the Bureau of Labor Statistics, as of December 2023, the US textile and apparel manufacturing sector employed about 272,400 workers (seasonally adjusted), including 89.3K in NACIS313 textile mills, 95.6K in NAICS314 textile product mills and 87.5K in NAICS315 apparel manufacturing. As of December 2023, NAICS 4482 apparel retail stores employed about 850,000 workers (seasonally adjusted).

According to DHS, the new enforcement plan will focus on the following areas:

Cracking down on small package shipments to prohibit illicit goods from U.S. markets by improving screening of packages claiming the Section 321 de minimis exemption for textile, Uyghur Forced Labor Prevention Act (UFLPA), and other violations, including expanded targeting, laboratory and isotopic testing, and focused enforcement operations.

Conducting joint Customs and Border Protection (CBP)-Homeland Security Investigation (HIS)HSI trade special operations to ensure cargo compliance. This includes physical inspections; country-of-origin, isotopic, and composition testing; and in-depth reviews of documentation. CBP will issue civil penalties for violations of U.S. laws and coordinate with HSI to develop and conduct criminal investigations when warranted.

Better assessing risk by expanding customs audits and increasing foreign verifications. DHS personnel will conduct comprehensive audits and textile production verification team visits to high-risk foreign facilities to ensure that textiles qualify under the U.S.-Mexico-Canada Agreement (USMCA) or the Central America-Dominican Republic Free Trade Agreement (CAFTA-DR). (note: As CBP noted, most US free trade agreements and trade preference programs have complex textiles and apparel-specific rules of origin requirements. CBP is “responsible for ensuring that the trade community complies with all statutory, regulatory, policy, and procedural requirements that pertain to importations under free trade agreements and other trade preference programs.”)

Building stakeholder awareness by engaging in an education campaign to ensure that importers and suppliers in the CAFTA-DR and USMCA region understand compliance requirements and are aware of CBP’s enforcement efforts.

Leveraging U.S. and Central American industry partnerships to improve facilitation for legitimate trade. (note: The Biden Administration aims to leverage textile and apparel trade as part of the solution to address “root causes of migration in Central America. According to the White House Fact Sheet released in March 2024, the Office of the U.S. Trade Representative and Central American Trade Agencies and textiles and apparel industry stakeholders will work together to build a directory with detailed profiles of manufacturing and sourcing companies in the region, including information on business practices and production capabilities, to facilitate transparent sourcing, and bolster the region’s supply chain.)

Expanding the Uyghur Forced Labor Prevention Act (UFLPA) Entity List to identify malign suppliers for the trade community through review of additional entities in the high-priority textile sector for inclusion in the UFLPA Entity List. (note: Once an entity is on this list, in general, it is prohibited from exporting its goods to the United States. Importers are required to ensure the supply chains of their imported products are free from entities on the Entity List).

#2: Several US textile and apparel industry stakeholders have publicly responded to DHS’s new strategy.:

“We strongly commend DHS for the release of a robust textile and apparel enforcement plan today. We also greatly appreciate Secretary Mayorkas’ personal engagement in this urgent effort and believe it’s a strong step forward to addressing pervasive customs fraud that is harming the U.S. textile industry.”

“The essential and vital domestic textile supply chain has lost 14 plants in recent months. The industry is facing severe economic harm due to a combination of factors, exacerbated by customs fraud and predatory trade practices by China and other countries, which has resulted in these devastating layoffs and plant closures. DHS immediately understood the economic harms facing the industry and deployed the development of a critical action plan.”

“The industry requests include

Ramped up textile and apparel enforcement with regard to Western Hemisphere trade partner countries, including onsite visits and other targeted verification measures to enforce rules of origin as well as to address any backdoor Uyghur Forced Labor Prevention Act (UFLPA) violations.

Increased UFLPA enforcement to prevent textile and apparel goods made with forced labor from entering our market, including in the de minimis environment.

Immediate expansion of the UFLPA Entity List, isotopic testing, and other targeting tools. Intensified scrutiny of Section 321 de minimis imports and a review of all existing Executive Branch authorities under current law to institute basic reforms to this outdated tariff waiver mechanism. “

“We appreciate the Department of Homeland Security (DHS)’s announcement today outlining enhanced enforcement activities to prevent illicit trade in textiles. Our members support 55 million (more than one in four) American jobs and invest considerable time and resources in their customs compliance programs. Many of our members are Tier 3 participants in Customs-Trade Partnership Against Terrorism (C-TPAT). They are trusted traders and meet the high standards required to receive that designation by U.S. Customs and Border Protection and DHS. Our members are on the front lines for ensuring that they have safe and secure supply chains.