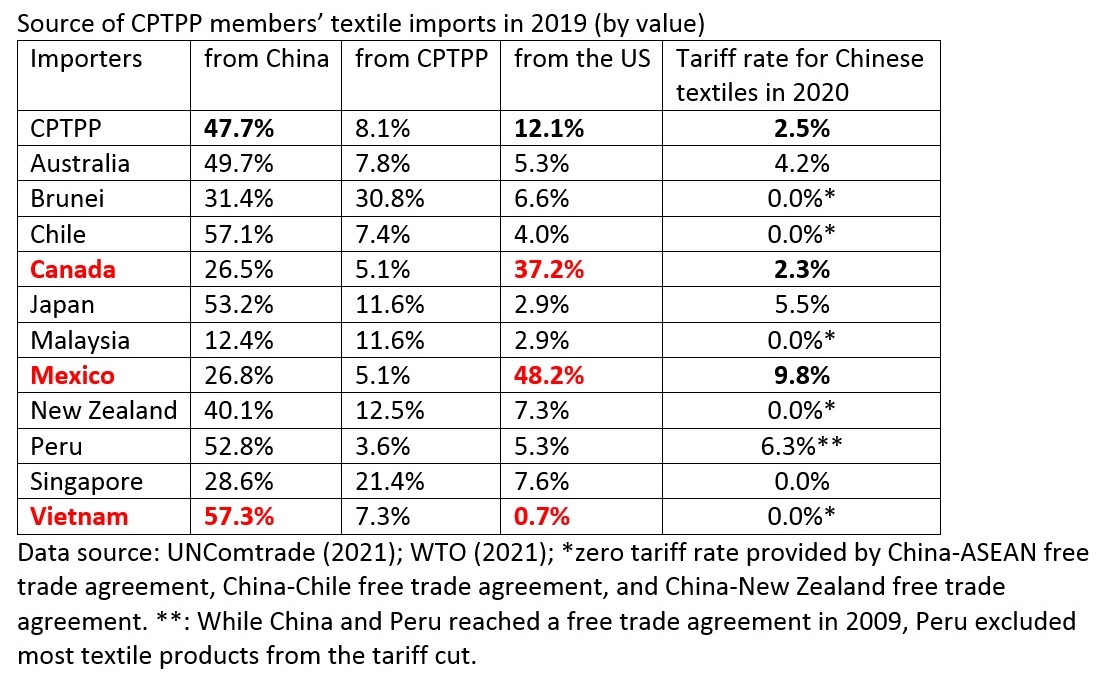

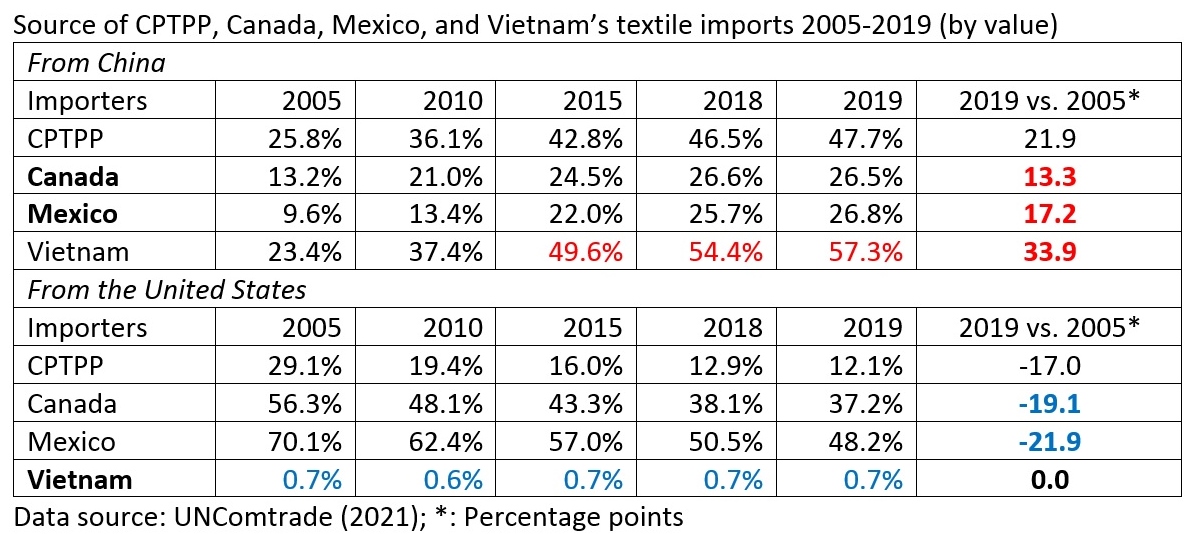

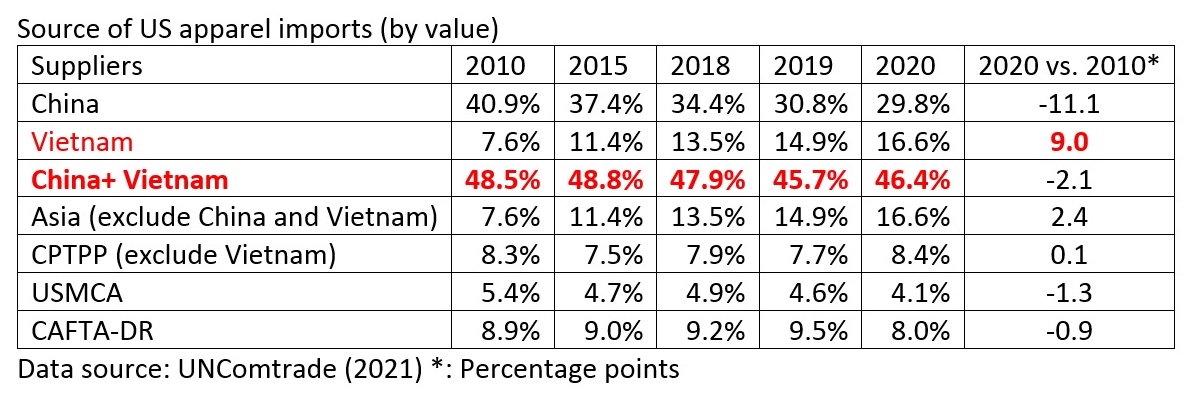

The latest OTEXA trade data suggests several US apparel import patterns:

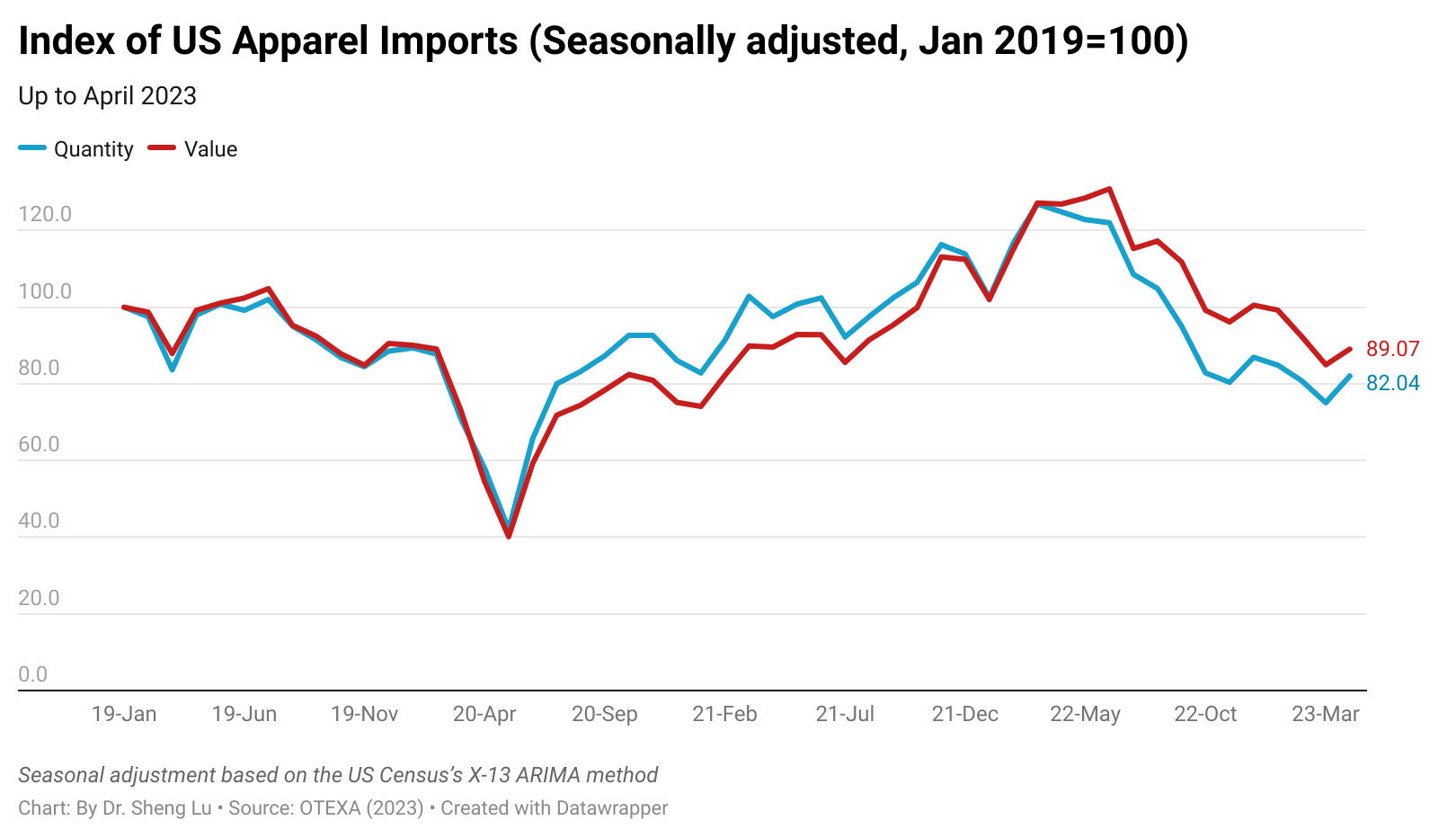

First, US apparel imports indicated a slow improvement in April 2023 but remained weak this year. For example, measured in quantity, US apparel imports fell by 33.9% in April 2023 from a year ago, but it was less significant than in March (i.e., down 40.2% YoY*). Likewise, measured in value, US apparel imports fell by 29.3% YoY in April 2023, which improved from a 32.7% YoY decline in March 2023. (*YoY: Year-over-year)

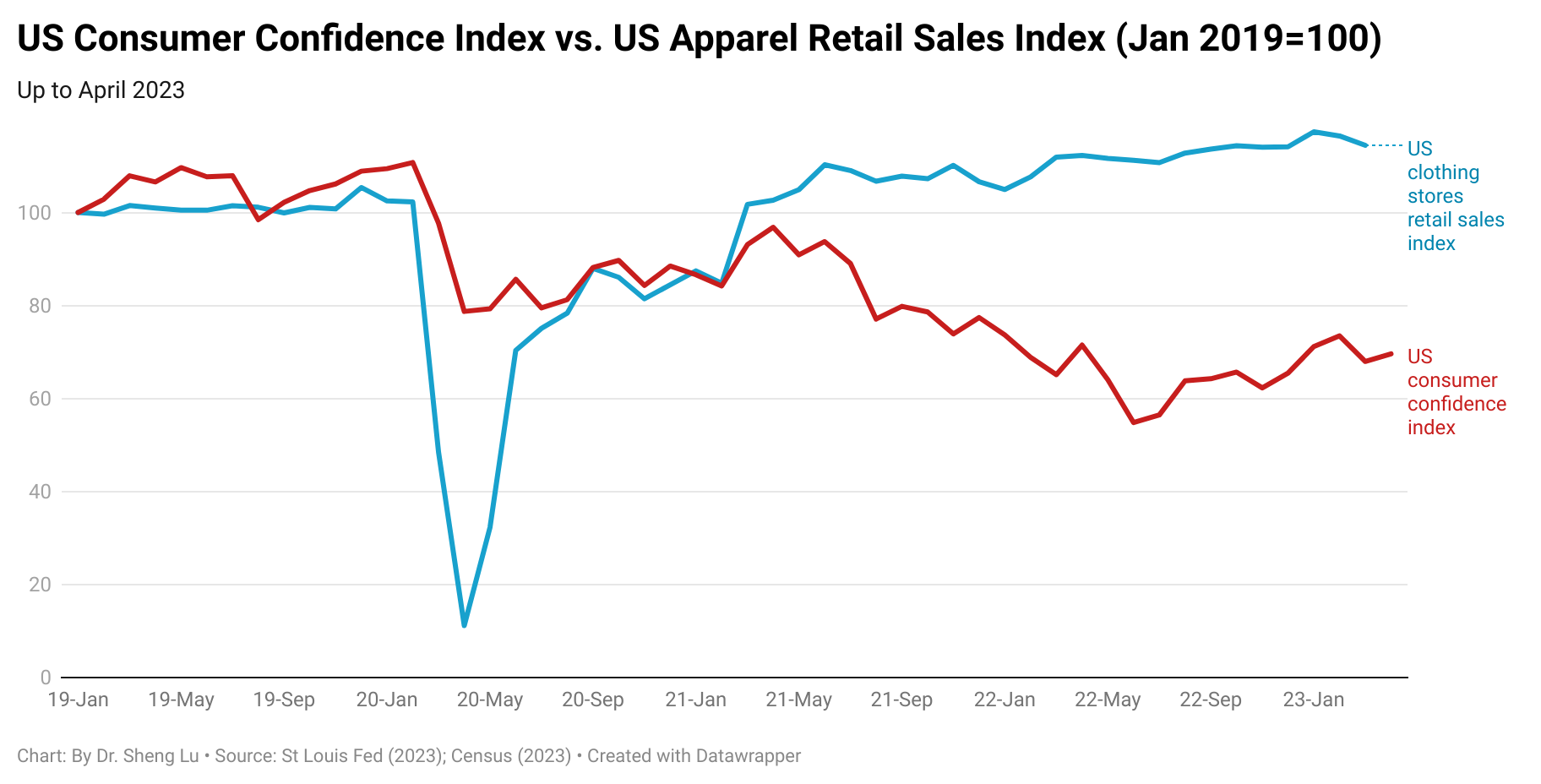

Overall, the shrinking US apparel import volume reflected the headwinds in the US economy and consumers’ hesitancy to purchase clothing amid financial uncertainties and high inflation. Recent economic indicators also present a mixed picture of the US economy’s growth trajectory. For example, while the US consumer confidence index slightly went up from 68.0 in March to 69.6 in April 2023 (January 2019=100), the advanced clothing store sales index in April fell to 115.6 (Jan 2019=100), the lowest so far in 2023 (e.g., was 120.6 in January 2023). However, since summer is traditionally a peak season for clothing sales, followed by events like back-to-school shopping, there remains hope that US apparel imports may experience a slight recovery at some point in the second half of the year.

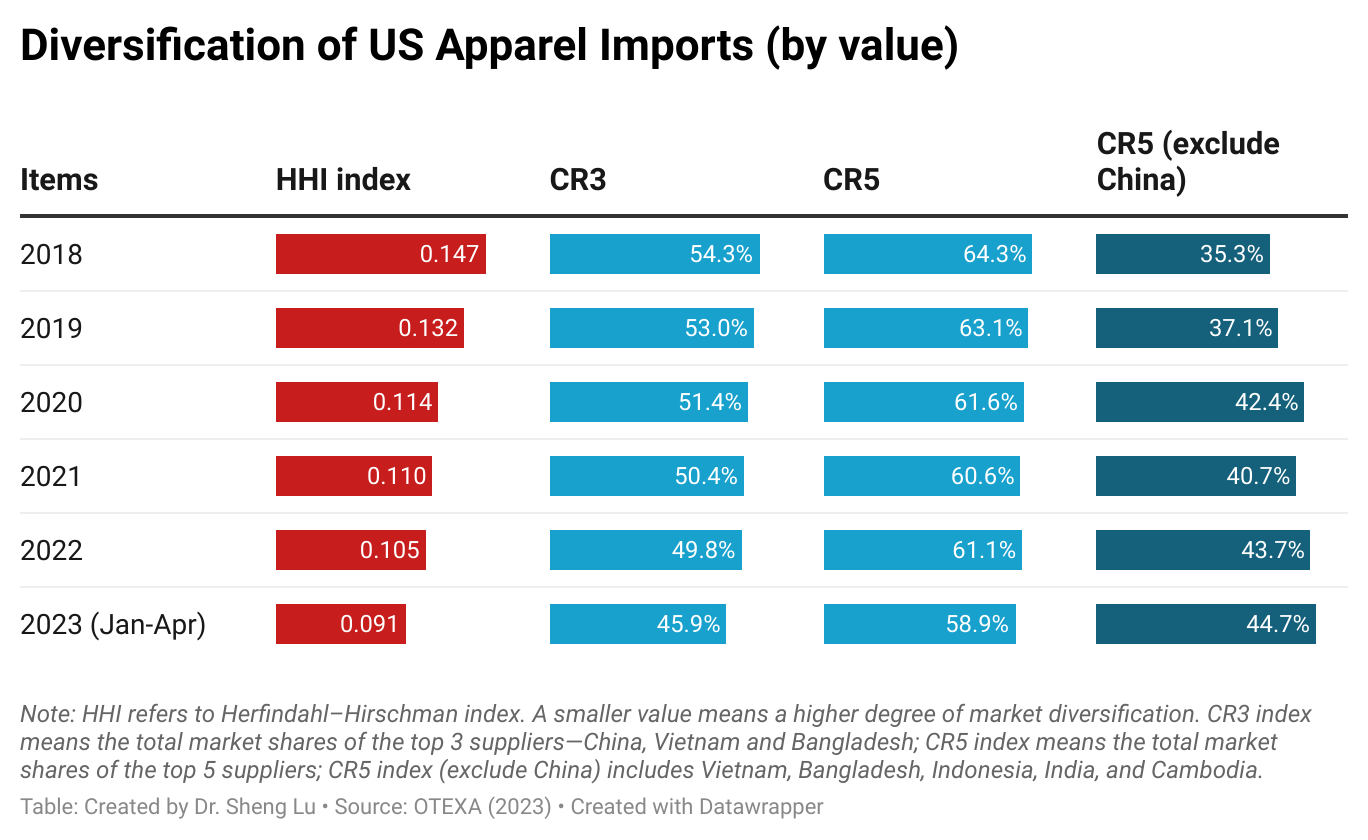

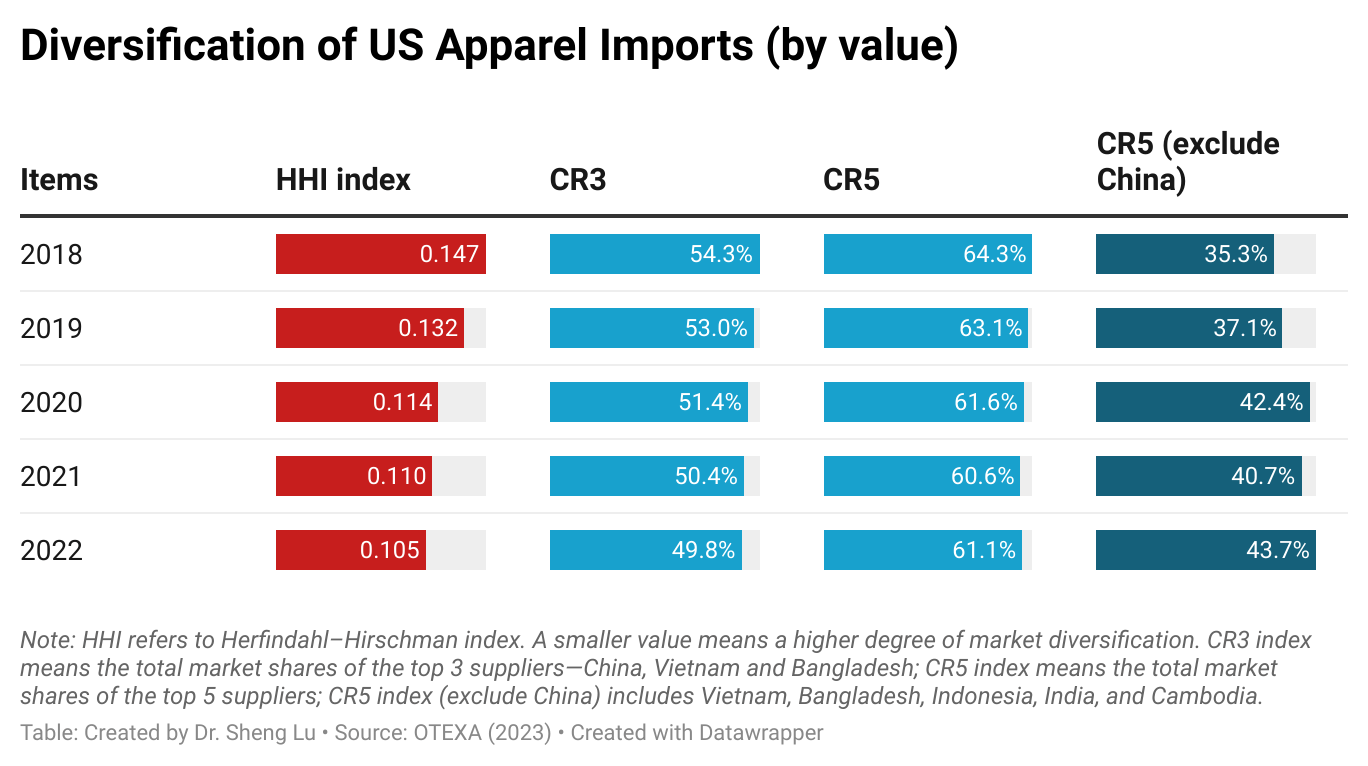

Second, trade data suggested that US apparel imports came from more diverse sources. For example, the Herfindahl–Hirschman index (HHI) fell below 0.1 in the first four months of 2023. Likewise, the market shares of the five largest suppliers (CS5) fell below 60% for the first time since 2018. The result suggested that leveraging sourcing diversification is a prevalent strategy among US fashion companies to mitigate supply chain risks and address market uncertainties.

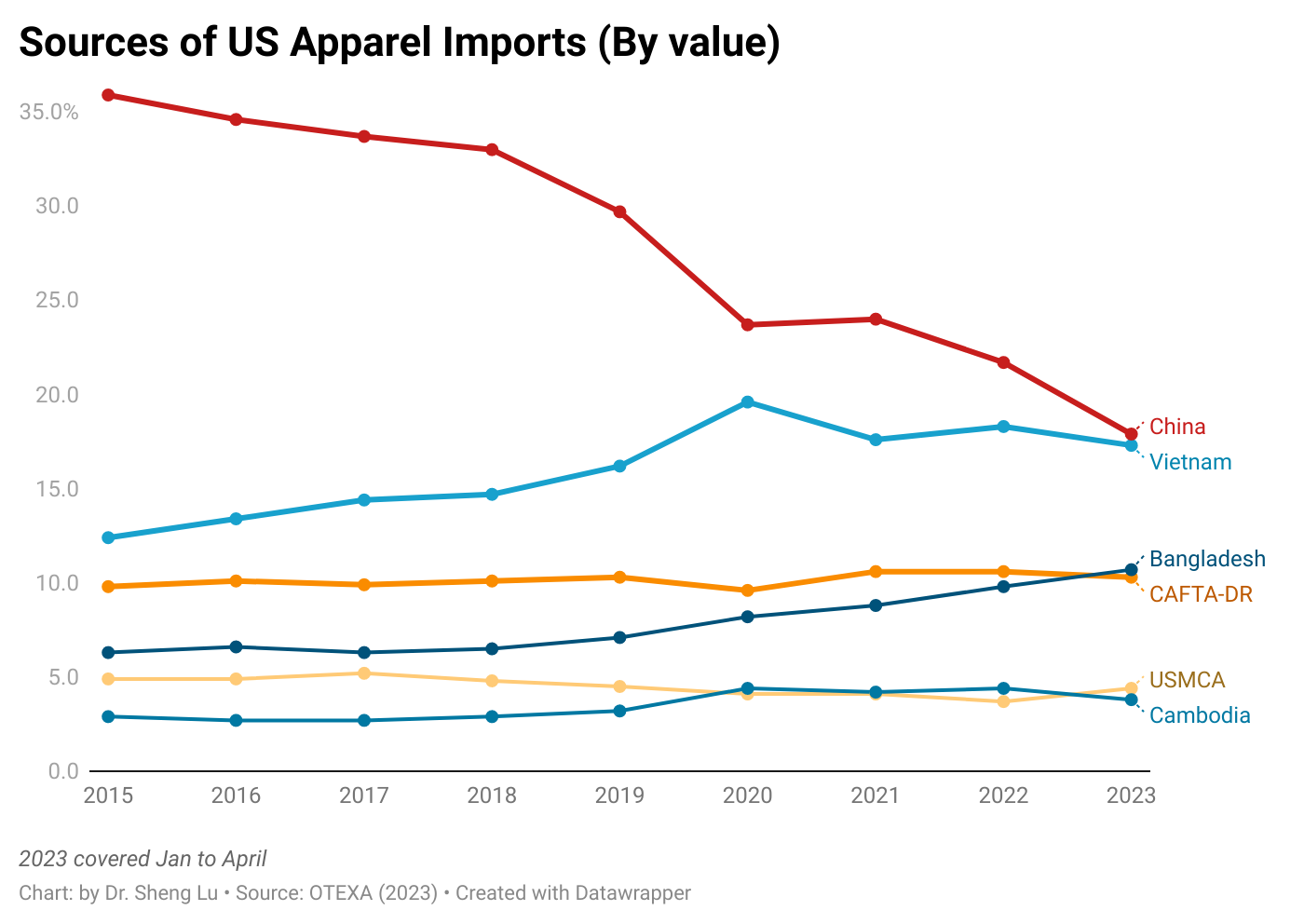

Third, US fashion companies are serious and eager to further reduce their “China exposure.” Although China remained the top apparel supplier to the US, its market share fell to a new low of 17.9% in value and 30.6% in quantity in the first four months of 2023. Notably, for the first time in decades, less than 10% of US cotton apparel imports came from China in March/April 2023, revealing the significant impact of the Uyghur Forced Labor Prevention Act (UFLPA) on US fashion companies’ China sourcing strategies.

Related, US fashion companies appear to be increasingly cautious about sourcing apparel from Vietnam as its supply chain is too exposed to China, raising concerns about forced labor risks. In value, Vietnam accounted for 17.3% of US apparel imports in the first four months of 2023, down from 18.6% a year ago. Notably, almost the same amount of Vietnam’s textile and apparel products were subject to the CBP’s UFLPA investigation as China in FY2023.

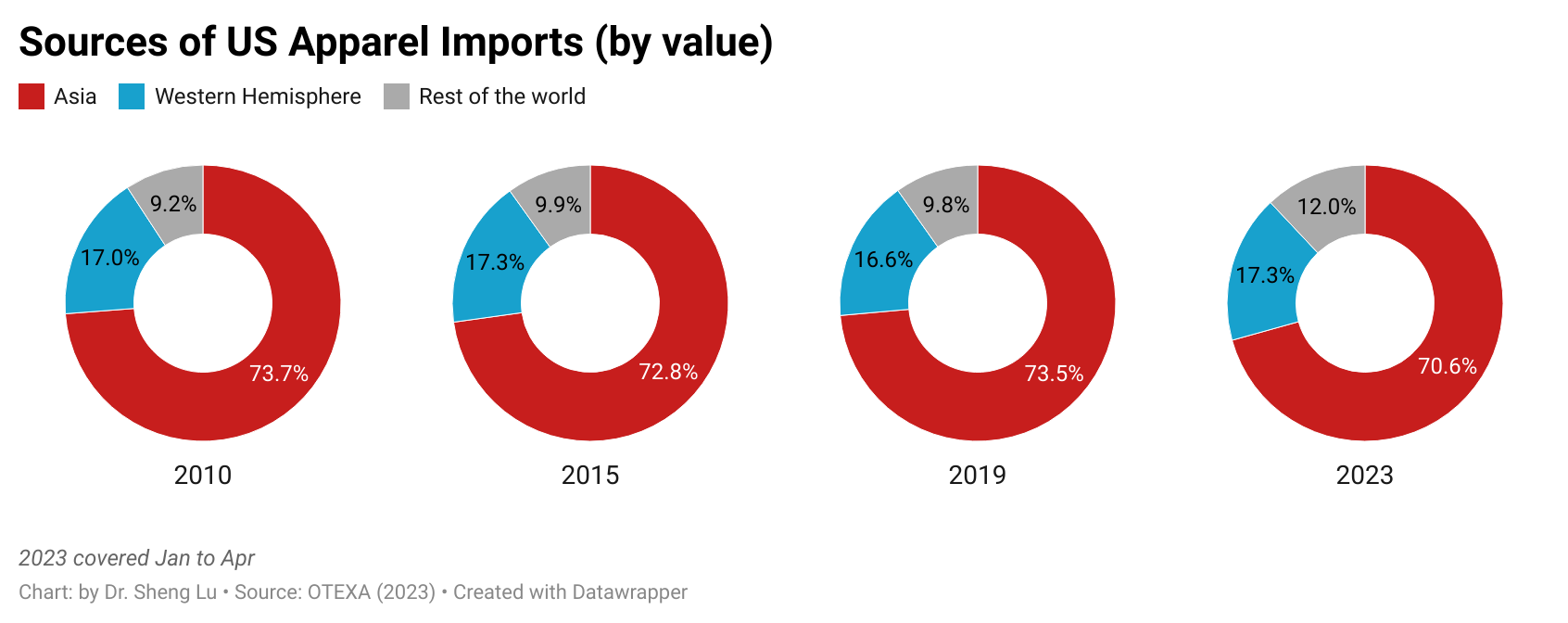

Fourth, large-scale Asian countries benefited the most as US fashion companies looking for China’s alternatives. Specifically, measured in value, about 70.6% of US apparel imports came from Asia in the first four months of 2023, down from 74.9% in 2022. However, the five largest apparel exporting countries in Asia other than China (i.e., Vietnam, Bangladesh, Indonesia, India, and Cambodia) accounted for 44.7% of US apparel imports in the first four months of 2023, a new high since 2018 (i.e., was 35.3%). These countries are among the most popular “alternatives to China” because of their balanced performance regarding production capacity, cost, flexibility, and compliance risks.

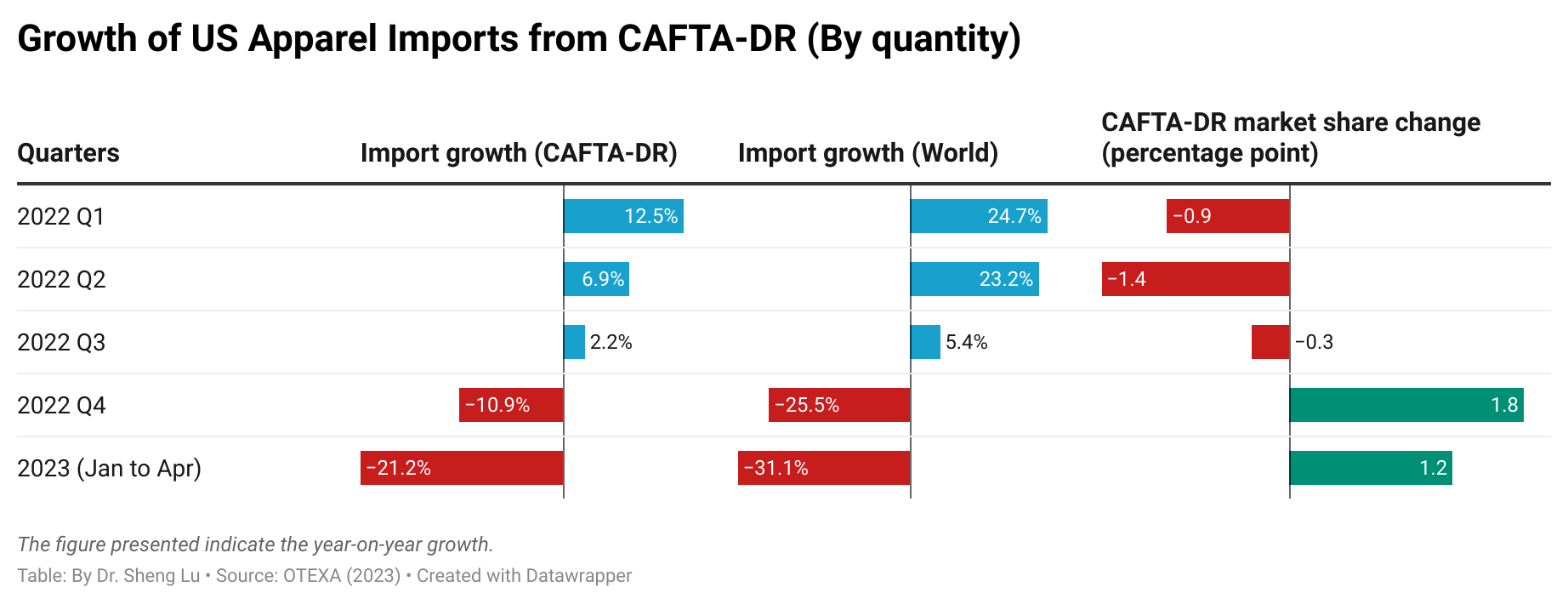

Fifth, US fashion companies are also actively exploring new near-shoring opportunities from the Western Hemisphere. For example, about 17.3% of US apparel imports came from Western Hemisphere countries in the first four months of 2023, up from 15.6% in 2023. That being said, measured in quantity, US apparel imports from Mexico and CAFTA-DR members fell by 13.0% and 21.2% in the first four months of 2023 from a year ago due to the struggling US economy. It will be interesting to see whether CAFTA-DR and Mexico can keep or enhance their market shares when the US import demand recovers.

On April 17, 2023, the US International Trade Commission (USITC) released a new report analyzing the trade and economic impact of the African Growth Opportunity Act (AGOA). The report fulfills the investigation request by the US House of Representatives Committee on Ways and Means in January 2022.

The full report is HERE. Below are the key findings regarding the apparel sector:

The African Growth and Opportunity Act (AGOA) matters significantly to Sub-Saharan African countries (SSA)’s apparel exports to the United States

AGOA has been the primary competitive advantage for SSA’s apparel exports to the United States. For example, US apparel imports from AGOA beneficiaries have risen from $953 million in 2001 to $1.4 billion in 2021 (note: up to $1.76 billion in 2022). More than 96.4% of these imports claimed AGOA’s duty-free benefits, including 98.8% utilized the “third-country fabric” provision.

While twenty countries were eligible for AGOA’s apparel provision, over 90% of US apparel imports from AGOA members in 2021 originated in five SSA countries: Kenya (31.5%), Madagascar (19.9%), Lesotho (20.6%), Ethiopia (18.3%), and Mauritius (5.1%).

AGOA benefits appear essential for SSA countries to maintain their apparel exports to the United States. USITC noted that in every case when a country lost AGOA eligibility between 2000 and 2021, there was a noticeable decrease in US apparel imports from that country, such as Rwanda and Madagascar. (note: according to OTEXA’s latest trade data, US apparel imports from Ethiopia, which lost its AGOA eligibility in 2022, dropped by 42% in the first two months of 2023 from a year ago, far worse than a 5.8% decrease of AGOA members as a whole.)

SSA garment manufacturers often find supplying the US apparel market a better fit than Europe, primarily because US brands tend to place orders for higher volume bulk basics, which allows workers to focus on a narrower set of skills.

The impact of AGOA on SSA’s apparel production and exports varied at the country level

Some SSA countries (e.g., Kenya and Lesotho) already had well-established apparel industries when AGOA was implemented in 2000. In contrast, other SSA countries (e.g., Madagascar, Ethiopia, Tanzania, and Ghana) received substantial investments from foreign-owned firms after AGOA was enacted, which helped jumpstart their apparel sectors.

USITC also identified two “unsuccessful” AGOA cases. For example, Mauritius was the largest AGOA beneficiary apparel supplier to the United States in 2000 but has since fallen to the fifth-largest in 2021, largely due to increased labor costs. Likewise, South Africa’s apparel export to the US was negatively affected by its disqualification from the “third-country fabric” provision under AGOA.

AGOA has had a limited impact on building an integrated regional textile and apparel supply chain in SSA

Currently, SSA countries primarily participate in the cut-and-sew operations of apparel based on imported textile raw materials from outside the region (mostly from Asia).

The USITC identified several challenges in building the local textile industry in SSA. For example, building a textile mill typically requires much higher investments (e.g., $200–300 million) than a garment factory (i.e., $25 million). Also, most SSA manufacturers cannot make the various types of yarns and fabrics in demand from U.S. buyers.

The dilemma is not new: Access to textile inputs from sources outside SSA is essential for garment manufacturers in SSA to meet the specifications of US buyers. However, relying on imported textile inputs reduces the incentives for investing in new textile production capabilities in SSA.

The USITC report found Mauritius an exception as it has developed a relatively competitive capability in producing cotton fabrics, which are supplied to garment factories in Madagascar. There is also some collaboration between cotton producers in Tanzania and Uganda and Kenya’s textile manufacturers.

US fashion companies generally see SSA as a promising emerging sourcing destination

Apparel producers in SSA are less established in global apparel value chains than manufacturers in other parts of the world. Therefore, it is not uncommon that fashion brands and retailers “work more directly with SSA apparel manufacturers to ensure product quality, particularly for new or expanding product lines.”

Most SSA garment factories only have cut, make, and trim (CMT) capability and rely on imported textile materials arranged by fashion brands and retailers.

USITC found that US companies increasingly import man-made fiber (MMF) apparel from AGOA members to benefit from greater import duty savings. (note: US tariff rates for MMF apparel were typically higher than those made with natural fibers like cotton. On the other hand, however, it’s worth noting that SSA countries generally have more competitive advantages in producing cotton apparel products than in producing MMF apparel).

SSA countries also have advantages over their Asia competitors. For example, “a shipment takes about 15–18 days to travel from the port in Lomé to the East Coast of the United States. From China or Bangladesh, lead times range from 40–50 days.”

Many fashion brands “have expressed interest in sourcing from greenfield factories with fewer legacy challenges posed by compliance and environmental impacts.”

US fashion companies’ sourcing diversification strategy to avoid risk exposure also contributed to the expansion of their apparel imports from AGOA members.

Uncertainty of AGOA renewals hurt US apparel imports from SSA

Apparel companies typically make sourcing decisions 12–18 months in advance. This practice underscores the importance of renewing AGOA early rather than granting extensions only within two to nine months of expiration, as in the past.

The USITC report mentioned, “Without the assurance of the “third country fabric” provision, many US apparel companies sourced from AGOA beneficiaries reported holding back orders from the region.”

More can be done to leverage SSA’s cotton production better

Cotton growing is widespread across about thirty SSA countries. SSA accounts for about 7 percent of the world’s cotton production, the fifth-largest globally.

However, most SSA cotton is sold to international buyers and exported to Asian mills that process it into yarns and fabrics. In contrast, the consumption of domestic cotton in SSA is limited.

The SSA cotton industry produces high-quality, “sustainable” cotton that can be used in several high-value end products sold globally. However, because of a lack of mechanization, SSA cotton production struggles to increase supply to meet demand.

Also, cotton-growing regions in SSA tend to be poorer and less politically stable than other parts of the region.

Discussion questions:

Based on the blog post and class discussions, how competitive or attractive are AGOA members as apparel-sourcing destinations for US fashion companies, especially compared with suppliers from Asia and the Western Hemisphere?

Based on the blog post, what improvement can be made to make AGOA or any problems that need to be addressed?

Any other thoughts related to the patterns of apparel trade and sourcing based on the blog post?

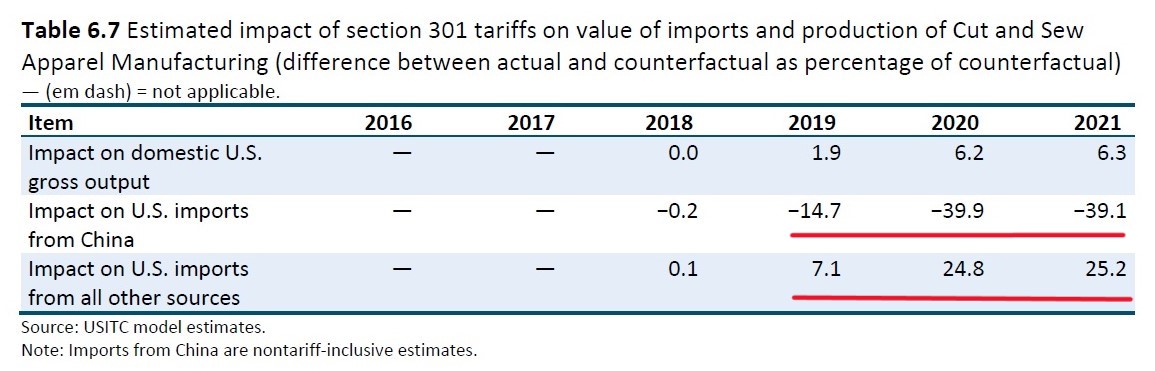

USITC adopted two methods to estimate Section 301 tariffs’ economic impacts:

Econometric model estimates using monthly trade data (10-digit HS code) from January 2017 to December 2021.

A set of partial equilibrium models that linked section 301 tariffs to domestic prices and production at the four-digit NAICS code level. USITC used data from 2018 to 2021 as the base year.

USITC only considered Section 301 tariffs’ direct impacts, i.e., “how tariffs impacted prices, production, and trade for products subject to section 301 tariffs and domestic sectors that compete directly with those imports.”

Regarding the overall impact of Section 301 actions, USITC found that the tariffs imposed on Chinese goods resulted in a price rise paid by US importers, but the exporter prices received by Chinese firms were mostly unchanged. As a result, “imports from China decreased in quantity, leading to a substantial decline in their import value. These changes, in turn, caused an increase in production and prices in US domestic industries that were competing with Chinese imports.”

USITC also evaluated the specific impacts of Section 301 tariffs on the Cut and Sew apparel (NAICS 3152) sector. According to USITC:

“nontariff-inclusive value” refers to the change in the value of imports from China excluding the value of the section 301 duties themselves, which provide an indication of the change in import quantities because export prices are mostly unchanged.

First, Section 301 tariffs hurt US apparel imports from China. USITC estimated that US woven apparel (NAICS 3152) imports from China decreased by 14.7% in 2019 but fell nearly 40% in 2020 and 2021 due to Section 301 tariffs. However, USITC didn’t explain why imports from China suddenly worsened, nor if other factors, such as the Uyghur Forced Labor Prevention Act (UFLPA), played a role.

Second, Section 301 tariffs mostly replaced US woven apparel (NAICS3152) imports from China with other sources. However, the direct benefits of Section 301 tariffs to US domestic cut and sew manufacturing seemed limited. Specifically, USITC estimated that US woven apparel imports from sources other than China increased by 7.1% in 2019, 24.8% in 2020, and 25.2% in 2021 due to Section 301 tariffs. In comparison, Section 301 tariffs resulted in modest growth of US domestic woven apparel (NAICS3152) production (up to 6.3%) over the same period.

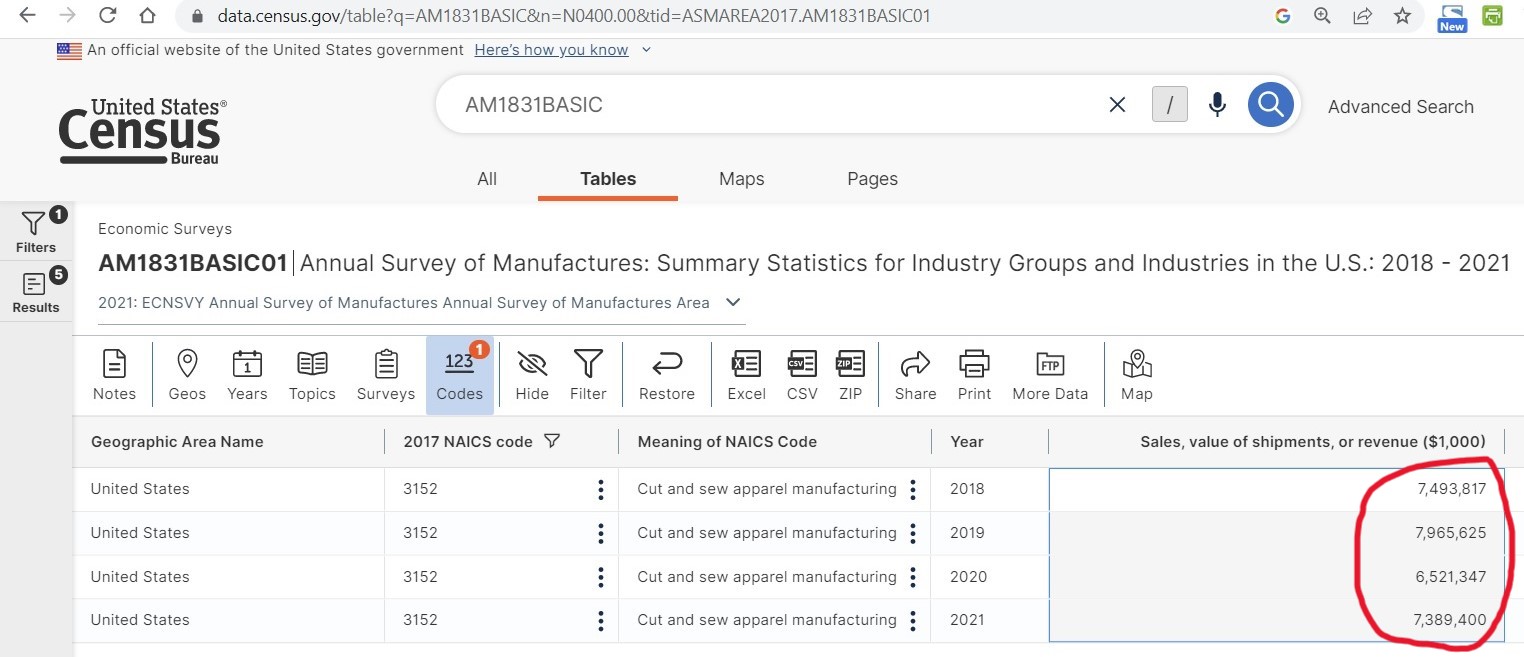

Actual trade and production data further showed that US woven apparel (NAICS 3152) imports from sources other than China increased from $55.3 billion in 2018 to $61.2 billion in 2021 (or up 10.7%). Over the same period, US domestic woven apparel (NAICS 3152) sales & value of shipments declined from $7.49 billion to $7.38 billion (or down 1.4%) (Data source: Census). In other words, no clear evidence suggests that Section 301 tariffs boosted US domestic woven apparel production.

Third, Section 301 tariffs made US woven apparel (NAICS 3152) imports from EVERYWHERE more expensive. On the one hand, USITC found that the price of US woven apparel (NAICS 3152) imports from China increased by 4.4% in 2019, 14.7% in 2020, and 14.5% in 2021 due to the Section 301 tariffs. However, similar to the case of trade volume, USITC didn’t explain why Section 301 tariffs’ price impact suddenly became more significant in 2020 and 2021. (Note: In fact, the Tranche 4A tariffs were 15% since September 1, 2019, but were reduced to 7.5% effective February 14, 2020, because of the US-China Phase One deal.)

Meanwhile, due to limited production capacity outside of China, the Section 301 tariffs caused an increase in the cost of US woven apparel imports from all other countries. Specifically, USITC found that the price of US woven apparel (NACIS 3152) imports from sources other than China increased by 3.2% from 2018 to 2021. (Note: given the hiking sourcing costs in 2022, the price increase could be more significant should USITC include updated 2022 trade data in the estimation.)

Additionally, USITC acknowledged that its estimation may “likely captures the most significant impacts of these tariffs in the short run.” However, some effects of section 301 tariffs would likely be delayed. For example, USITC said, “if importers and domestic producers anticipated the tariffs remaining in place long enough,” they may consider more costly changes, such as adjusting their supply chains and investing in domestic production.

Discussion questions:

Based on USITC’s assessment, should President Biden keep or remove the Section 301 tariffs on imports from China? Why or why not?

Regarding the impact of Section 301, any questions remain unanswered or can be studied further?

Any findings in the USITC report surprised you and why?

In March 2023, the Office of the United States Trade Representative (USTR) released its 2024 Fiscal Year Budget report, outlining six major goals and objectives for FY2024. USTR’s FY2024 goals and objectives for textile and apparel are similar to FY2023, but keywords such as “near-shoring” are newly emphasized.

Goal 1: Open Foreign Markets and Combat Unfair Trade

Provide policy guidance and support for international negotiations or initiatives affecting the textile and apparel sector to ensure that the interests of U.S. industry and workers are taken into account and, where possible, to provide new or enhanced export opportunities for U.S. industry. (Note: no change from FY2023)

Conduct reviews of commercial availability petitions regarding textile and apparel products and negotiate corresponding FTA rules of origin changes, where appropriate, in a manner that takes into account market conditions while preserving export opportunities for U.S. producers and employment opportunities for U.S. workers. (Note: no change from FY2023)

Engage relevant trade partners to address regulatory issues potentially affecting the U.S. textile and apparel industry’s market access opportunities. (Note: no change from FY2023)

Continue to engage with CAFTA-DR partner countries to address trade-related issues to optimize inclusive economic opportunities; strengthen trade rules and transparency and address non-tariff trade impediments; provide capacity building in areas such as textile and apparel trade-related regulation and practice on customs, border and market access issues, including agricultural and sanitary and phytosanitary regulations, to avoid barriers to trade. (note: newly mentioned “transparency”)

Continue to engage CAFTA-DR partners and stakeholders to identify and develop means to increase two-way trade in textiles and apparel and strengthen the North American supply chain and near-shoring to enhance formal job creation. (note: newly emphasized “Near-shoring”)

Provide policy guidance and support for international negotiations or initiatives affecting the textile and apparel sector to ensure that the interests of U.S. industry and workers are taken into account and, where possible, to provide new or enhanced export opportunities for U.S. industry. (Note: no change from FY2023)

Conduct reviews of commercial availability petitions regarding textile and apparel products and negotiate corresponding FTA rules of origin changes, where appropriate, in a manner that takes into account market conditions while preserving export opportunities for U.S. producers and employment opportunities for U.S. workers (note: no change from FY2023)

Engage relevant trade partners to address regulatory issues potentially affecting the U.S. textile and apparel industry’s market access opportunities. (note: no change from FY2023)

Goal 2: Fully Enforce U.S. Trade Laws, Monitor Compliance with Agreements, and Use All Available Tools to Hold Other Countries Accountable

Closely collaborate with industry and other offices and Departments to monitor trade actions taken by partner countries on textiles and apparel to ensure that such actions are consistent with trade agreement obligations and do not impede U.S. export opportunities. (note: no change from FY2023)

Research and monitor policy support measures for the textile sector, in particular in the PRC, India, and other large textile producing and exporting countries, to ensure compliance with international agreements. (note: no change from FY2023)

Continue to work with the U.S. textile and apparel industry to promote exports and other opportunities under our free trade agreements and preference programs, by actively engaging with stakeholders and industry associations and participating, as appropriate, in industry trade shows. (note: no change from FY2023)

Goal 4: Develop Equitable Trade Policy Through Inclusive Processes

Take the lead in providing policy advice and assistance in support of any Congressional initiatives to reform or re-examine preference programs that have an impact on the textile and apparel sector. (note: no change from FY2023)

Other Priorities for USTR in FY2024:

#1 “Advancing a Worker-Centered Trade Policy.” For example, given “communities of color and lower socio-economic backgrounds were more negatively affected by free trade policies that have reduced tariffs and distributed supply chains across the globe,” USTR will develop “a new strategic approach to trade relationships that is not built on traditional free trade agreements…USTR is embarking on trade engagements with allies and like-minded economies, like Taiwan and Kenya and [through] multinational economic frameworks that focus on clean energy and supply chains rather than tariffs.”

#2 Address forced labor. For example, USTR developed the first-ever focused trade strategy to combat forced labor. Paired with the implementation of the Uyghur Forced Labor Prevention Act, and the Memorandum of Cooperation (MOC) launching of a Task Force on the Promotion of Human Rights and International Labor Standards in Supply Chains under the U.S.-Japan Partnership on Trade. And USTR will “use every tool available to block the importation of goods made partially or entirely with forced labor.”

#3 Re-Aligning the U.S. – Beijing Trade Relationship. “USTR continues to keep the door open to conversations with the PRC, including on its Phase One commitments. However, USTR acknowledges the Agreement’s limitations. USTR’s strategy is expand beyond only pressing Beijing for change and includes vigorously defending our values and economic interests from the negative impacts of the PRC’s unfair economic policies and practices.”

#4 Strengthen enforcement of US trade policy. For example, USTR sees enforcement “a key component of our worker-centered trade policy.” USTR is “upholding the eligibility requirements in preference programs,” such as the African Growth and Opportunity Act (AGOA). As many enforcement tools were “were crafted decades ago,” USTR will be “reviewing our existing trade tools and working with Congress to develop new tools as needed.”

Trend 1: US fashion companies continue to diversify their sourcing base in 2022

Numerous studies suggest that US fashion companies leverage sourcing diversification and sourcing from countries with large-scale production capacity in response to the shifting business environment. For example, according to the 2022 fashion industry benchmarking study from the US Fashion Industry Association (USFIA), more than half of surveyed US fashion brands and retailers (53%) reported sourcing apparel from over ten countries in 2022, compared with only 37% in 2021. Nearly 40% of respondents plan to source from even more countries and work with more suppliers over the next two years, up from only 17% in 2021.

Trade data confirms the trend. For example, the Herfindahl–Hirschman index (HHI), a commonly-used measurement of market concentration, went down from 0.110 in 2021 to 0.105 in 2022, suggesting that US apparel imports came from even more diverse sources.

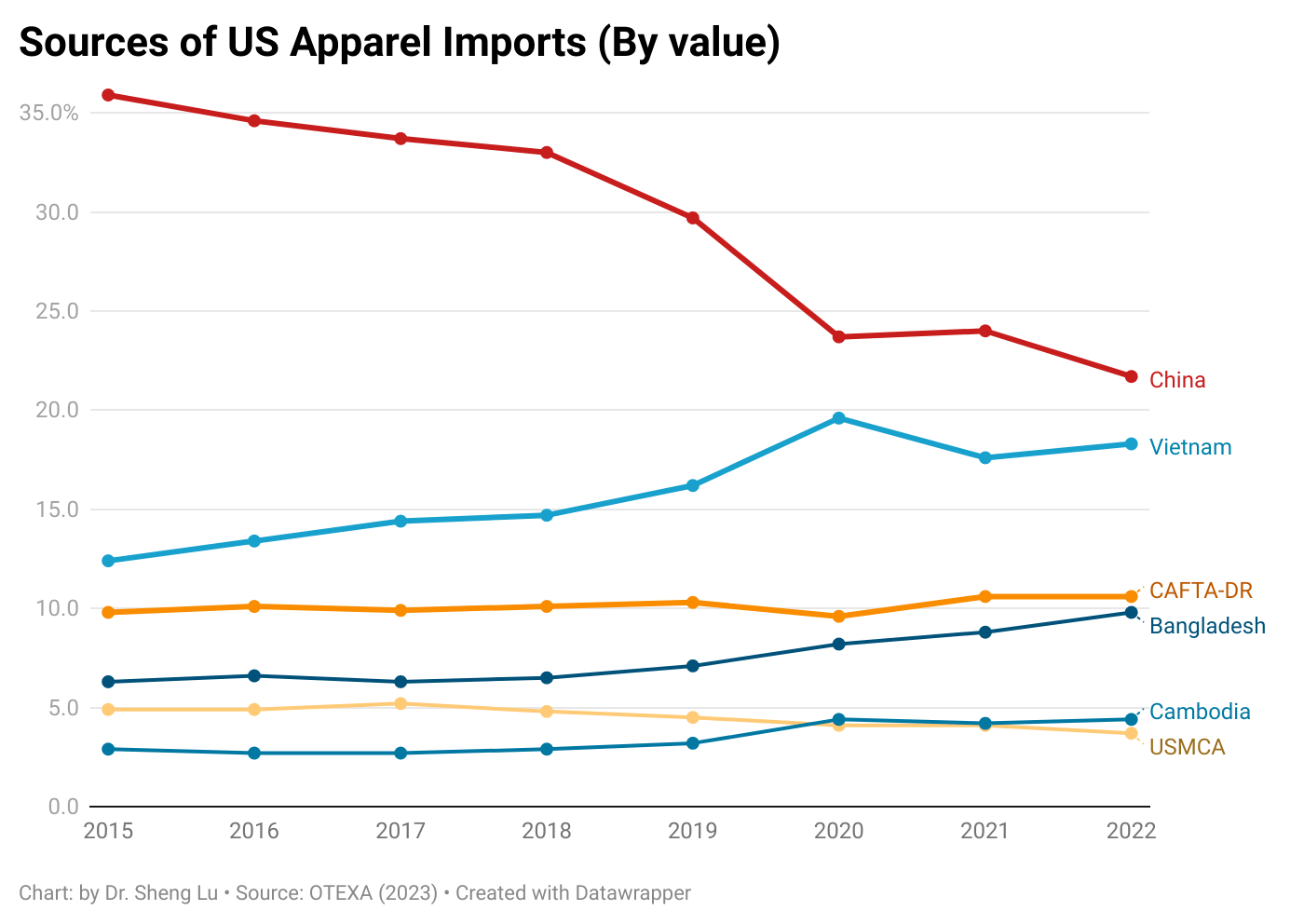

Trend 2: Asia as a whole will remain the dominant source of imports

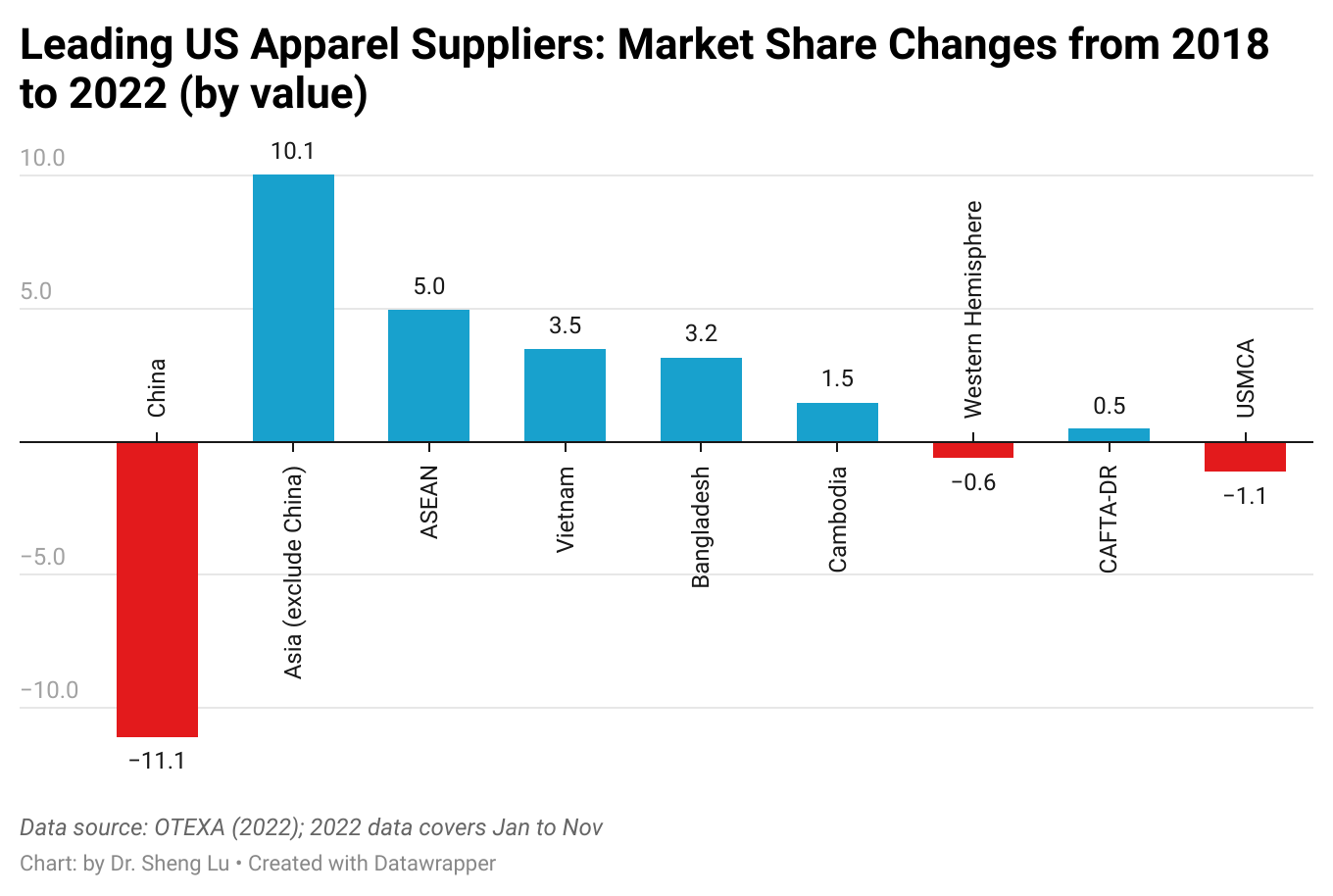

Measured in value, about 73.5% of US apparel imports came from Asia in 2022, up from 72.8% in 2021. Likewise, the CR5 index, measuring the total market shares of the top five suppliers—all Asia-based, i.e., China, Vietnam, Bangladesh, Indonesia, and India, went up from 60.6% in 2021 to 61.1% in 2022. Notably, the CR5 index without China (i.e., the total market shares of Vietnam, Bangladesh, Indonesia, India, and Cambodia) enjoyed even faster growth, from 40.7% in 2021 to 43.7% in 2022.

Additionally, facing growing market uncertainties and weakened consumer demand amid high inflation pressure, US fashion companies may continue to prioritize costs and flexibility in their vendor selection. Studies consistently show that Asia countries still enjoy notable advantages in both areas thanks to their highly integrated regional supply chain, production scale, and efficiency. Thus, US fashion companies are unlikely to reduce their exposure to Asia in the short to medium term despite some worries about the rising geopolitical risks.

Trend 3: US fashion companies’ China sourcing strategy continues to evolve

Several factors affected US apparel sourcing from China negatively in 2022:

One was China’s stringent zero-COVID policy, which led to severe supply chain disruptions, particularly during the fall. As a result, China’s market shares from September to November 2022 declined by 7-9 percentage points compared to the previous year over the same period.

The second factor was the implementation of the Uyghur Forced Labor Prevention Act (UFLPA) in June 2022, which discouraged US fashion companies from sourcing cotton products from China. For example, only about 10% of US cotton apparel came from China in the fourth quarter of 2022, down from 17% at the beginning of the year and much lower than nearly 27% back in 2018.

The third contributing factor was the US-China trade tensions, including the continuation of Section 301 punitive tariffs. Industry sources indicate that US fashion companies increasingly source from China for relatively higher-value-added items targeting the premium or luxury market segments to offset the additional sourcing costs.

Further, three trends are worth watching regarding China’s future as an apparel sourcing base for US fashion companies:

One is the emergence of the “Made in China for China” strategy, particularly for those companies that view China as a lucrative sales market. Recent studies show that many US fashion companies aim to tailor their product offerings further to meet Chinese consumers’ needs and preferences.

Second is Chinese textile and apparel companies’ growing efforts to invest and build factories overseas. As a result, more and more clothing labeled “Made in Bangladesh” and “Made in Vietnam” could be produced by factories owned by Chinese investors.

Third, China could accelerate its transition from exporting apparel to providing more textile raw materials to other apparel-exporting countries in Asia. Notably, over the past decade, most Asian apparel-exporting countries have become increasingly dependent on China’s textile raw material supply, from yarns and fabrics to various accessories. Moreover, recent regional trade agreements, particularly the Regional Comprehensive Economic Partnership (RCEP), provide new opportunities for supply chain integration in Asia.

Trend 4: US fashion companies demonstrate a new interest in expanding sourcing from the Western Hemisphere, but key bottlenecks need to be solved

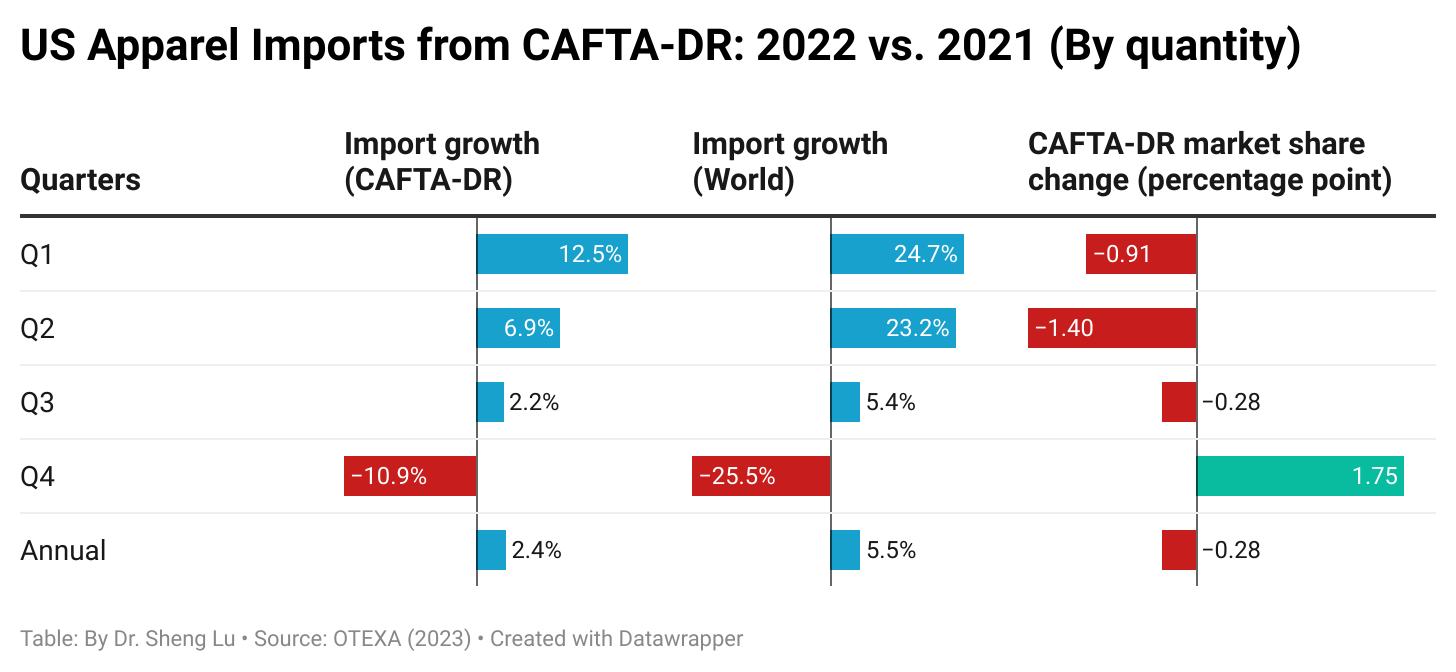

Trade data suggests a mixed picture of near-shoring in 2022. For example, members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) and US-Mexico-Canada Trade Agreement (USMCA) accounted for a declining share of US apparel imports in 2022, measured in quantity and value. While CAFTA-DR and USMCA members showed an increase in their market share of US apparel imports in the fourth quarter of 2022, reaching 10.7% and 3.1%, respectively, this growth was not accompanied by an increase in trade volume. Instead, US apparel imports from these countries decreased by 11% and 15%, respectively, compared to the previous year. CAFTA-DR and USMCA members’ gain in market share was mainly due to a sharper decline in US apparel imports from the rest of the world (i.e., decreased by over 25% in the fourth quarter of 2022).

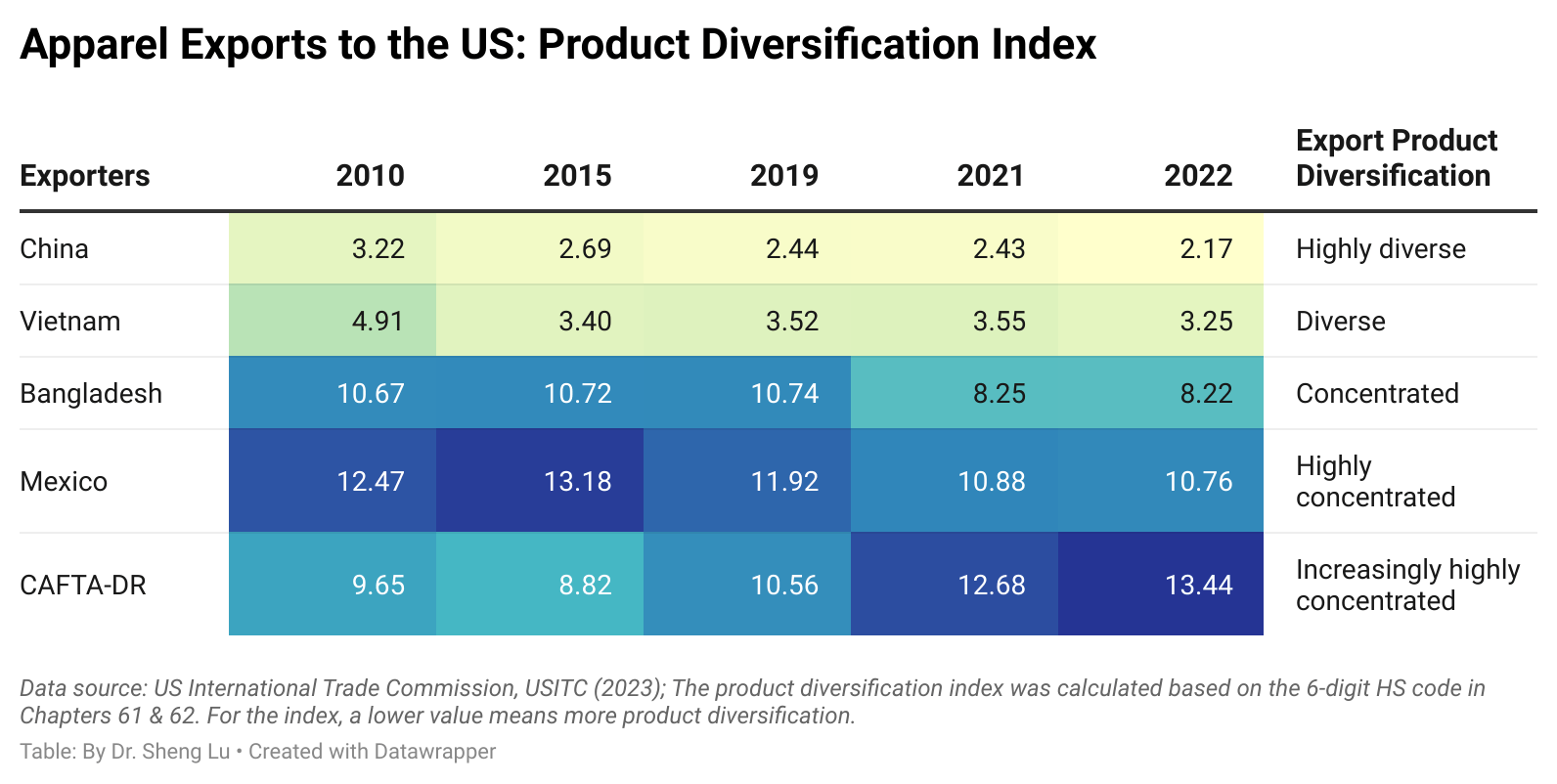

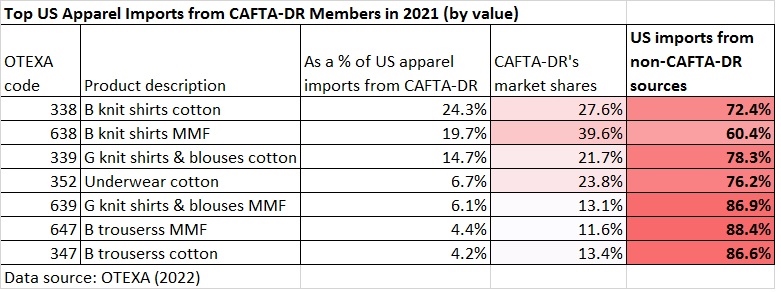

Trade data also suggests two other bottlenecks preventing more US apparel sourcing from CAFTA-DR and USMCA members. One is the lack of product diversity. For example, the product diversification index consistently shows that US apparel imports from CAFTA-DR members and Mexico concentrated on only a limited category of products, and the problem worsened in 2022. The result explained why US fashion companies often couldn’t move souring orders from Asia to CAFTA-DR and USMCA members.

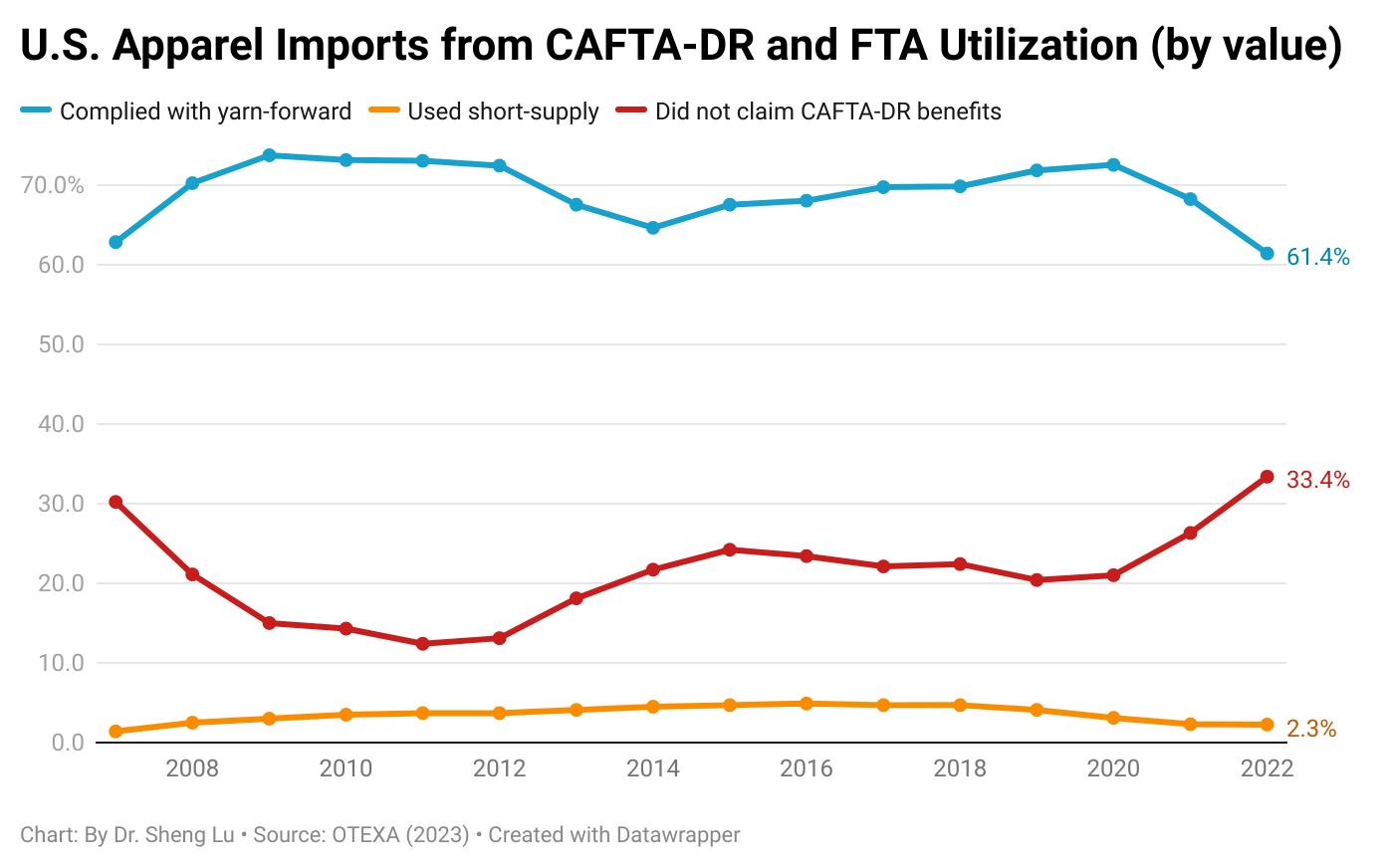

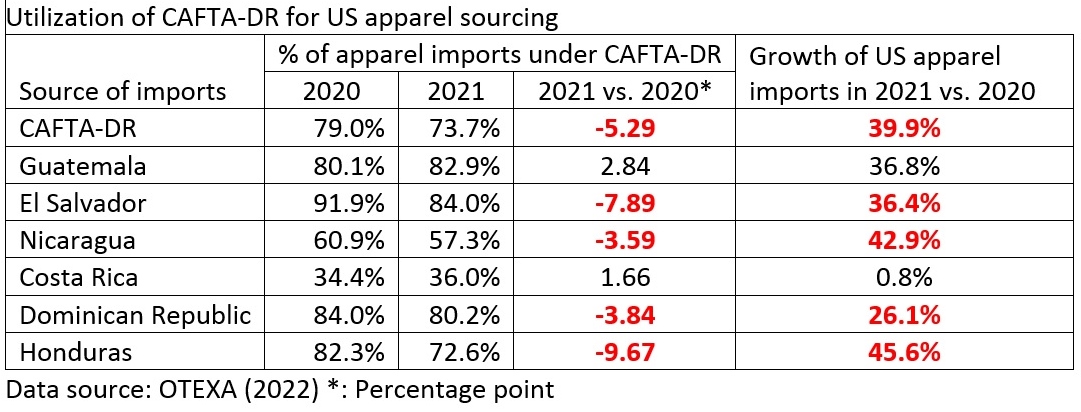

Another problem is the underutilization of the trade agreement. For example, CAFTA-DR’s utilization rate for US apparel imports consistently went down from its peak of 87% in 2011 to only 74% in 2021. The utilization rate fell to 66.6% in 2022, the lowest since CAFTA-DR fully came into force in 2007. This means that as much as one-third of US apparel imports from CAFTA-DR did NOT claim the agreement’s preferential duty benefits. Thus, regarding how to practically grow US fashion companies’ near-shoring, we could expect more public discussions and debates in the new year.

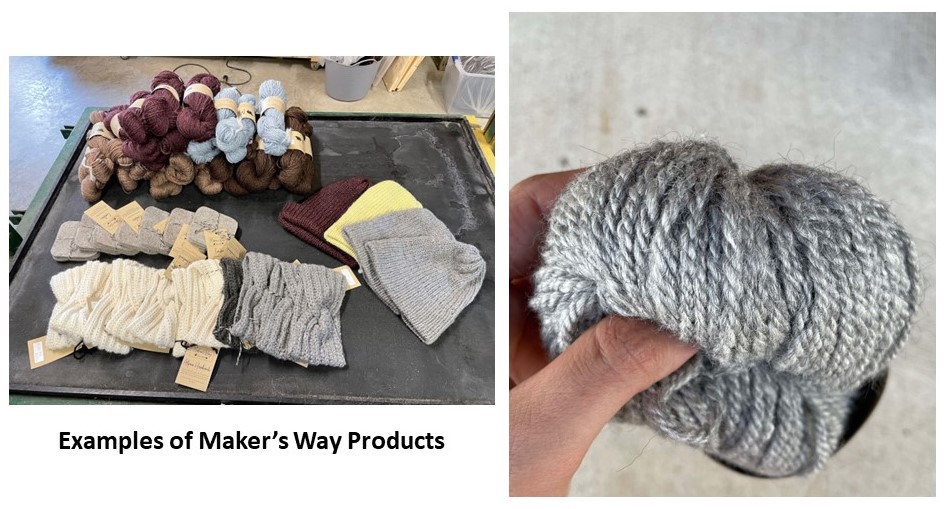

Elizabeth Davelaar is a Co-Owner of Maker’s Way Fiber Mill in Brandon, SD, which opened in October 2021. The mill is a family-run business, with Elizabeth’s sister, Erin, and her mother, Kari, as other co-owners. Elizabeth began her career in the fashion industry at the University of Minnesota, where she graduated with a BS in Apparel Design from the College of Design. She then went to the University of Delaware, where she graduated with an MS in Fashion and Apparel Studies and a Graduate Certificate in Sustainable Apparel Business.

Elizabeth served as a project manager for a non-profit fashion brand in St. Louis and taught sewing to immigrant women in St. Louis and women in Ethiopia. She then moved to Vi Bella Jewelry in Sioux Center, IA, working her way from Shipping Manager to VP of Operations, Sustainability and Design. She then opened Maker’s Way Fiber Mill in 2021 with her family and has been working with local fiber producers to grow the yarn industry in South Dakota and surrounding areas.

Interview Part

Sheng: What inspired you to start your fiber mill business? What makes it special and exciting?

Elizabeth: The mill was born out of the need to solve a problem. I became interested in natural dye at the University of Delaware under Professor Cobb. Once I moved back to the area where I grew up, COVID hit, and I was able to dive deeper into the natural dye and use local plants as a dye source. This also led to being curious about local natural fibers. South Dakota isn’t a state that grows cotton, and the hemp industry is currently small, but it has an abundance of sheep. According to statistics from the US Department of Agriculture, South Dakota has 235,000 sheep and is home to one of the nation’s largest wool co-ops. However, there are only 2 working fiber mills in the area that provide custom processing, which makes yarn made from local fiber very hard to find.

This led to the opening of Maker’s Way Fiber Mill. We are a full-service, custom fiber mill and make yarn, felt, roving, and home goods products from primarily wool and alpaca fiber. Approximately 90% of our time is spent processing for clients who own the animals and use the yarn themselves or sell it, with the other 10% processing yarn that we sell online via our website and in-person at events. The vast majority of our customers are local (within 4-5 hrs) and sell locally to crafters. We take pride in knowing where the fiber we use comes from, sourcing from local farms or using fiber from vintage or second-hand sources.

Hats made from 80% alpaca/20% Wool (both sourced from SD) with a small amount of recycled sari silk blended in. Photo courtesy of Elizabeth Davelaar

(Photo courtesy of Elizabeth Davelaar)

Photo courtesy of Elizabeth Davelaar

Sheng: According to Maker’s Way Fiber Mill’s website, sustainability is a critical feature of your products. Why is that, and how do you make your products sustainable?

Elizabeth: We believe that we are stewards of the earth and should be conscious of how the products we make are grown, created, and then how they can be disposed of. The fashion industry, from creating the product to end life, is a huge polluter. The current market for wool is not great for producers, and there isn’t a good avenue for alpaca producers. We work very hard to ensure that our products are sourced from people that we know and trust or are from vintage or second-hand sources. We also work to ensure our products are made from natural fibers, thus they are biodegradable.

We also work to limit the waste in our mill. Although we try our absolute best to reduce loss in the process, each step produces some loss in fiber. This fiber is swept up and either rewashed and added to our Millie line or added to our bird nest starters. The Millie line is yarn spun up from the scraps, and we end up running about four batches of this a year. Each batch is unique because of the different blends of fiber we run. The bird nest starters use fiber that either falls out of our carder or is swept off the floor. These are then put outside in the spring for birds to use for nesting. The fibers are short enough that the baby birds don’t get tangled in them as they would with yarn and because they are natural animal fibers, the nests will biodegrade, unlike acrylic yarns that are sometimes used.

Photo courtesy of Elizabeth Davelaar

Sheng: Maker’s Way Fiber Mill’s products are 100% locally made in South Dakota. From your perspective, what are the opportunities and challenges for manufacturing textiles in the US today?

Elizabeth: I see two big challenges in the natural animal fiber side of the U.S. textile industry: Lack of consumer knowledge of where clothing comes from and lack of infrastructure. But both also present big opportunities!

First, we have found with our mill that people don’t have a good understanding of how many steps there are in creating yarn in general, let alone clothing. We have people who question our pricing because they don’t understand what it means to make yarn in the United States. From start to finish, it takes eight different steps to get raw fiber from producers to yarn ready to sell. Our consultations for new clients tend to be very educational because even fiber producers don’t necessarily know all the steps. As we open the mill for tours and talk to people at events, they start to understand and respect how much work is behind the yarn we create, and that is when we see buy-in – when people start to see the whole process, as well as the people.

The second challenge I see is the overall lack of infrastructure. We are one of approximately 200 small-scale / artisan-style mills in the country (this number is approximate – there is not a good database) and do not run near the quantity compared to the larger manufacturers. As of 2018, there aren’t any small-scale fiber mill equipment manufacturers in the US, so all of the equipment available to us is either used or has to be imported from Canada or Italy. Wait time for most small producers to get their fiber made into yarn is approximately 8-12 months at many mills, some run up to 18 months out. Our mill currently runs about 6 months out and we have been open for just over a year.

For producers who want to sell their wool to larger manufacturers and not have it custom processed, as far as our research has shown, there is one large-scale scouring (wool washing) facility in the states and most of the large-scale spinners use fiber from this facility to spin into yarn and then send the fiber off to other finishing companies for knitting. Otherwise, all of the wool is shipped overseas, and producers are earning approximately $1.66/lb of wool (in 2020). We have heard of many producers that have stockpiles of wool because they are waiting for higher wool prices. Coops also won’t accept wool that isn’t white, so all dark colors of wool get thrown away as there isn’t a market for it.

We also see this as an opportunity. We have noticed the “buying local” trend extending past food also to include yarn. People also see value in making their own clothing and being intentional through knitting/crocheting. There is a growing market for it. We have also seen some demand for the addition of another large-scale scouring facility that could meet the needs for wool insulation and other home applications.

Sheng: Like other fashion programs in the US, most of our FASH students take job opportunities from fashion brands and retailers, not necessarily textile mills. How to raise the young generation’s interest in pursuing a career in textile and apparel factories? Do you have any suggestions?

Elizabeth: I definitely never intended to start a fiber mill when I was in school. I only took one textile class and am pretty sure only one of my design projects used wool. UD was really what fed the sustainability bug in me and I started to realize that sustainability starts at the very beginning of the lifecycle of clothing. Whether or not something can be biodegradable, recyclable, or repurposed starts with what fiber makes up the clothing. UD also showed me how global apparel is and how much carbon footprint it makes.

Working in a fiber mill is not an easy job. It is dirty, we tend to put in long days, and we are constantly learning new things. I am a very hands-on person, and I love being able to create things from nothing, so this job is a great fit for me. The part I loved most about being in design school was being able to create things, and my current job is that all day, every day. We split the mill into “zones” and between myself, Erin and our mom, we all specialized in a specific part of the process. I am in charge of skirting and cleaning fleeces, which means cleaning off all of the hay and visibly dirty areas (aka manure) and then washing the fiber in 140-180 degree water to get the dirt and lanolin out of the fleece. I then pick and card the fiber, which opens up and organizes the fiber into a long tube that is then drafted, spun, plied, and put into skeins. While most days tend to include the same things, each day is never the same as the last. Each animal fleece we run acts differently, so we are always learning new and better ways to run the equipment we have. It is challenging but also a labor of love. Because we work directly with producers, we know the names of most of the animals and love knowing that their fleeces are being used instead of being discarded! We also love connecting with local people who love purchasing from local producers and makers.

Photo courtesy of Elizabeth Davelaar

One of the biggest things I believe fashion programs can do to help open up students to different options in the fashion industry is to expose them to different opportunities and allow them to follow whatever passion they have and emphasize that there isn’t a “right” path in the industry. My classes opened me up to labor issues around the world and that then led me to Delaware. And the opportunities I was given at UD to follow my passions are a huge reason I am doing what I am doing now. One of the things I think UD does right is having many different professors with varying backgrounds in the FASH department and I think other universities would do well to implement that too.

Sheng: Any other key issues or industry trends you will watch in 2023?

Elizabeth: One of the key trends we are watching is the local craft movements and knowing where your clothing comes from. We saw a crafting resurgence happen during COVID and people are still pickup up their knitting needles and crochet hooks to create items to wear and love. We also see some carryover of the local food scene into the local fiber scene. We believe that this will continue to grow!

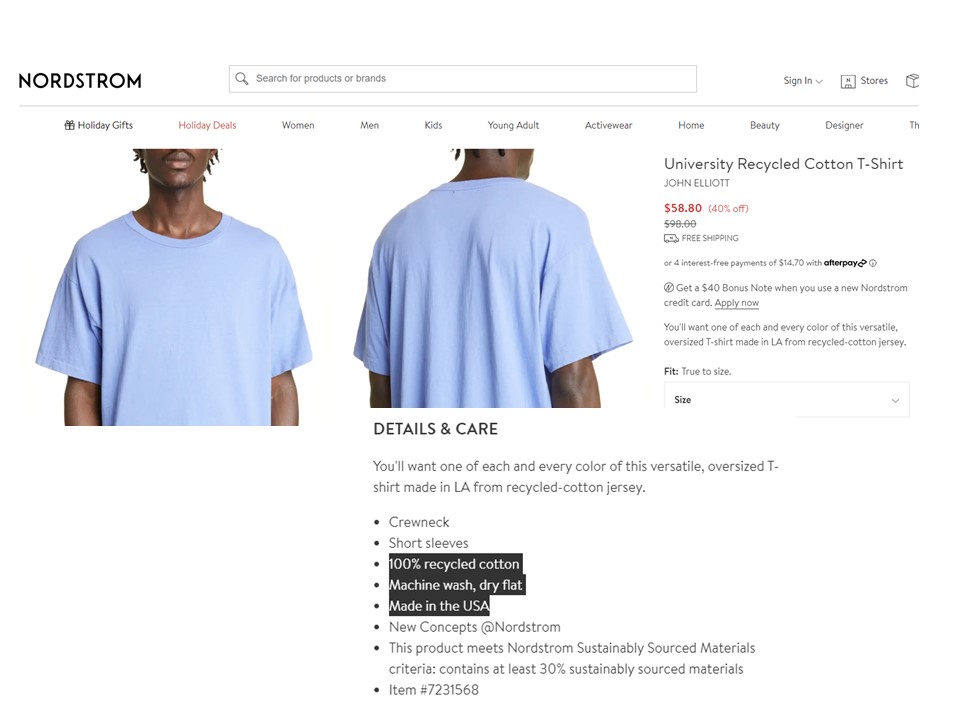

This study was based on a statistical analysis of 3,307 randomly selected clothing items made from recycled textile materials for sale in the U.S. retail market between January 2019 and August 2022 (see the sample picture above). The results show that:

First, U.S. retailers sourced clothing made from recycled textile materials from diverse countries.

Specifically, the sampled clothing items came from as many as 36 countries, including developed and developing economies in Asia, America, the EU, and Africa.

However, reflecting the unique supply chain composition of clothing made from recycled textile materials, U.S. retailers’ sourcing patterns for such products turned out to be quite different from regular new clothing. For example, whereas the vast majority (i.e., over 90%) of U.S. regular new clothing came from developing countries as of 2022 (UNComtrade, 2022), as many as 43% of the sampled clothing items made from recycled textile materials (n=1,408) were sourced from developed countries. Likewise, U.S. retailers seemed to be less dependent on Asia when sourcing clothing made from recycled materials (41.9%, n=1,387) and instead used near-sourcing from America (30.1%, n=994) more often, particularly domestic sourcing from the United States (14.8%, n=490).

Second, U.S. retailers appeared to set differentiated assortments for products imported from developed and developing countries when sourcing clothing made from recycled textile materials.

Among the sampled clothing items made from recycled textile materials, those imported from developing countries, on average, included a broader assortment than developed economies. Likewise, imports from developing countries also concentrated on products relatively more complex to make as opposed to developed countries. Developing countries’ more extensive clothing production capability, including the available production facilities and skilled labor force, than developed economies could have contributed to the pattern.

On the other hand, likely caused by developed countries’ overall higher production costs, the average retail price of sampled clothing items sourced from developed countries was notably higher than those from developing ones. However, NO clear evidence shows that U.S. retailers used developed countries primarily as the sourcing bases for luxury or premium items and used developing countries only for items targeting the mass or value market.

Third, an exporting country’s geographic location was another statistically significant factor affecting U.S. retailers’ sourcing pattern for clothing made from recycled textile materials. Specifically,

Imports from Asia had the most diverse product assortment (e.g., sizing options) and focused on complex product categories (e.g., outwear) that targeted mass and value markets.

Imports from America (North, South, and Central America) concentrated on simple product categories (e.g., T-shirts and hosiery) with moderate assortment diversity and mainly targeted the mass and value market.

Imports from the EU were mainly higher-priced luxury items in medium-sophisticated or sophisticated product categories with diverse assortment.

Imports from Africa concentrated on relatively higher-priced premium or luxury items in simple product categories (i.e., swim shorts) with a limited assortment diversity.

The study’s findings demystified the country of origin of clothing made from recycled textile materials hidden behind macro trade statistics. The findings also created critical new knowledge that contributed to our understanding of the supply chain of clothing made from recycled textile materials and U.S. retailers’ distinct sourcing patterns and affecting factors for such products. The findings have several other important implications:

First, the study’s findings revealed the broad supply base for clothing made from recycled textile materials and suggested promising sourcing opportunities for such products. Whereas existing studies illustrated consumers’ increasing interest in shopping for clothing made from recycled textile materials, the study’s results indicated that the “enthusiasm” also applied to the supply side, with many countries already engaged in making and exporting such products. Meanwhile, the results showed that U.S. retailers sourced clothing made from recycled textile materials in different product categories with a broad price range targeting various market segments to meet consumers’ varying demands. Moreover, as textile recycling techniques continue to advance, potentially enriching the product offer of clothing made from recycled textile materials, U.S. retailers’ sourcing needs and supply base for such products could expand further.

Second, the study’s findings suggest that sourcing clothing made from recycled textile materials may help U.S. retailers achieve business benefits beyond the positive environmental impacts. For example, given the unique supply chain composition and production requirements, China appeared to play a less dominant role as a supplier of clothing made from recycled textile materials for U.S. retailers. Instead, a substantial portion of such products was “Made in the USA” or came from emerging sourcing destinations in America (e.g., El Salvador, Nicaragua) and Africa (e.g., Tunisia and Morocco). In other words, sourcing clothing made from recycled textile materials could help U.S. retailers with several goals they have been trying to achieve, such as reducing dependence on sourcing from China, expanding near sourcing, and diversifying their sourcing base.

Additionally, the study’s findings call for strengthening U.S. domestic apparel manufacturing capability to better serve retailers’ sourcing needs for clothing made from recycled textile materials. On the one hand, the results demonstrated U.S. retailers’ strong interest in sourcing clothing made from recycled textile materials that were “Made in the USA.” Also, the United States may enjoy certain competitive advantages in making such products, ranging from the abundant supply of recycled textile waste and the affordability of expensive modern recycling machinery to the advanced research and product development capability. On the other hand, the results showed that U.S. retailers primarily sourced simple product categories (e.g., T-shirts and hosiery), targeting the value and mass markets from the U.S. and other American countries. This pattern somewhat mirrored the production and sourcing pattern for regular new clothing, for which apparel “Made in the USA” also lacked product variety and focused on basic fashion items compared with Asian and EU suppliers. Thus, strengthening the U.S. domestic apparel production capacity, especially for those complex product categories (e.g., outwear and suits), could encourage more sourcing of “Made in the USA” apparel using recycled textile materials and support production and job creation in the U.S. apparel manufacturing sector.

In December 2022, Just-Style consulted a panel of industry experts and scholars in its Outlook 2023–what’s next for apparel sourcing briefing. Below is my contribution to the report. All comments and suggestions are more than welcome!

2023 is likely another year full of challenges and opportunities for the global apparel industry.

First, the apparel industry may face a slowed world economy and weakened consumer demand in 2023. Apparel is a buyer-driven industry, meaning the sector’s volume of trade and production is highly sensitive to the macroeconomic environment. Amid hiking inflation, high energy costs, and retrenchment of global supply chains, leading international economic agencies, from the World Bank to the International Monetary Fund (IMF), unanimously predict a slowing economy worldwide in the new year. Likewise, the World Trade Organization (WTO) forecasts that the world merchandise trade will grow at around 1% in 2023, much lower than 3.5% in 2022. As estimated, the world apparel trade may marginally increase between 0.8% and 1.5% in the new year, the lowest since 2021. On the other hand, the falling demand may somewhat help reduce the rising sourcing cost pressure facing fashion companies in the new year.

Second, fashion brands and retailers will likely continue leveraging sourcing diversification and strengthening relationships with key vendors in response to the turbulent market environment. According to the 2022 fashion industry benchmarking study I conducted in collaboration with the US Fashion Industry Association (USFIA), nearly 40 percent of surveyed US fashion companies plan to “source from more countries and work with more suppliers” through 2024. Notably, “improving flexibility and reducing resourcing risks,” “reducing sourcing from China,” and “exploring near-sourcing opportunities” were among the top driving forces of fashion companies’ sourcing diversification strategies. Meanwhile, it is not common to see fashion companies optimize their supplier base and work with “fewer vendors.” For example, fashion companies increasingly prefer working with the so-called “super-vendors,” i.e., those suppliers with multiple-country manufacturing capability or can make textiles and apparel vertically, to achieve sourcing flexibility and agility. Hopefully, we could also see a more balanced supplier-importer relationship in the new year as more fashion companies recognize the value of “putting suppliers at the core.”

Third, improving sourcing sustainability and sourcing apparel products using sustainable textile materials will gain momentum in the new year. On the one hand, with growing expectations from stakeholders and pushed by new regulations, fashion companies will make additional efforts to develop a more sustainable, socially responsible, and transparent apparel supply chain. For example, more and more fashion brands and retailers have voluntarily begun releasing their supplier information to the public, such as factory names, locations, production functions, and compliance records. Also, new traceability technologies and closer collaboration with vendors enable fashion companies to understand their raw material suppliers much better than in the past. Notably, the rich supplier data will be new opportunities for fashion companies to optimize their existing supply chains and improve operational efficiency.

On the other hand, with consumers’ increasing interest in fashion sustainability and reducing the environmental impact of textile waste, fashion companies increasingly carry clothing made from recycled textile materials. My latest studies show that sourcing clothing made from recycled textile materials may help fashion companies achieve business benefits beyond the positive environmental impacts. For example, given the unique supply chain composition and production requirements, China appeared to play a less dominant role as a supplier of clothing made from recycled textile materials. Instead, in the US retail market, a substantial portion of such products was “Made in the USA” or came from emerging sourcing destinations in America (e.g., El Salvador, Nicaragua) and Africa (e.g., Tunisia and Morocco). In other words, sourcing clothing made from recycled textile materials could help fashion companies with several goals they have been trying to achieve, such as reducing dependence on sourcing from China, expanding near sourcing, and diversifying their sourcing base. Related, we are likely to see more public dialogue regarding how trade policy tools, such as preferential tariffs, may support fashion companies’ efforts to source more clothing using recycled or other eco-friendly textile materials.

Additionally, the debates on fashion companies’ China sourcing strategy and how to meaningfully expand near-sourcing could intensify in 2023. Regarding China, fashion companies’ top concerns and related public policy debates next year may include:

What to do with Section 301 tariff actions against imports from China, including the tariff exclusion process?

How to reduce “China exposure” further in sourcing, especially regarding textile raw materials?

How should fashion companies respond and mitigate the business impacts of China’s shifting COVID policy and a new wave of COVID surge?

What contingency plan will be should the geopolitical tensions in the Asia-Pacific region directly affect shipping from the region?

Meanwhile, driven by various economic and non-economic factors, fashion companies will likely further explore ways to “bring the supply chain closer to home” in 2023. However, the near-shoring discussion will become ever more technical and detailed. For example, to expand near-shoring from the Western Hemisphere, more attention will be given to the impact of existing free trade agreements and their specific mechanisms (e.g., short supply in CAFTA-DR) on fashion companies’ sourcing practices. Even though we may not see many conventional free trade agreements newly launched, 2023 will be another busy year for textile and apparel trade policy deliberation, especially behind the scene and on exciting new topics.

By Sheng Lu

Discussion question: As we approach the middle of the year, why do you agree or disagree with any predictions in the outlook? Please share your thoughts.

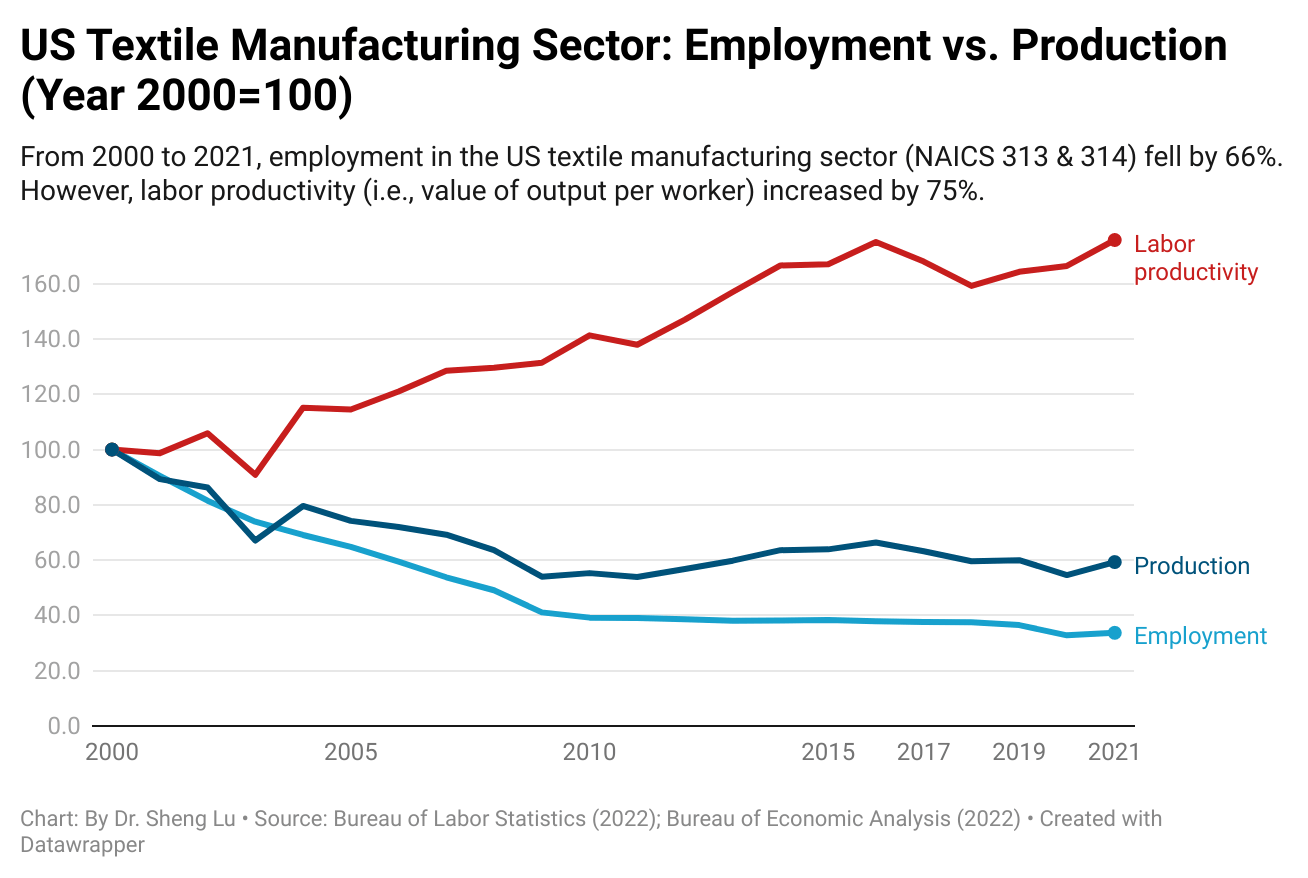

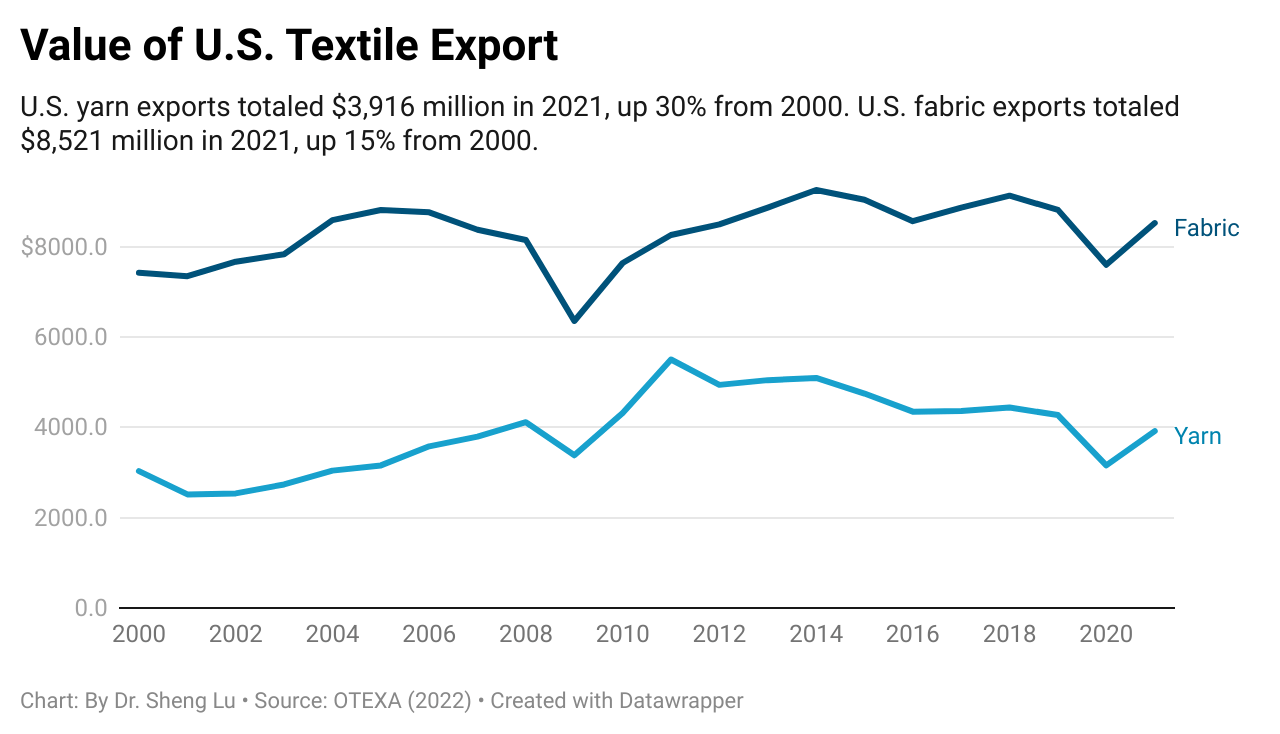

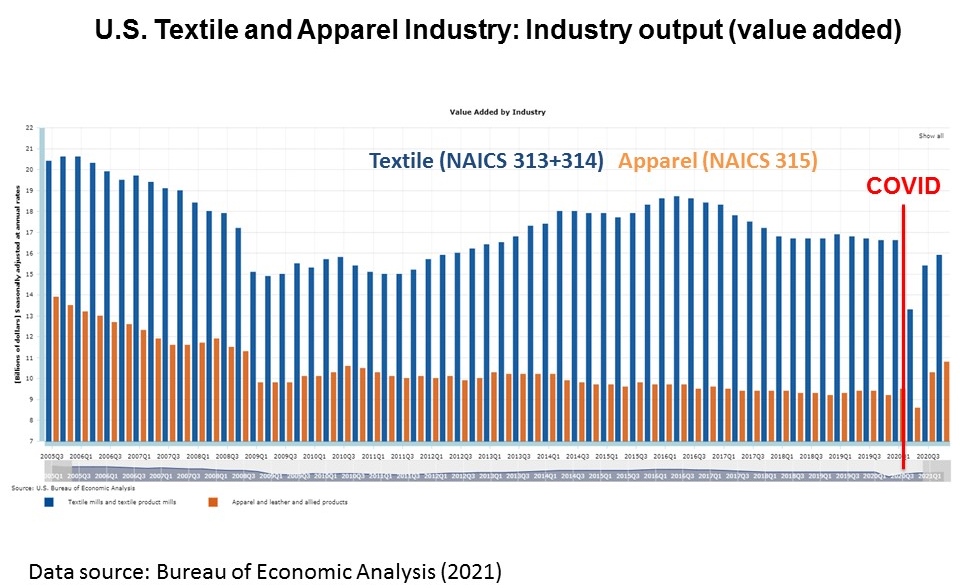

#1. Are classic trade theories (e.g., comparative advantage) still relevant or outdated in the 21st century? Why? Please share your thoughts based on the video and the figures.

#2. Based on the video and the figures above, is the US textile manufacturing sector a winner or loser of globalization and international trade? Why?

#3. Take the following poll (anonymous) and share your reflections.

#4. Should the government’s trade policy consider non-economic factors such as national security and geopolitics? What should be the line between promoting “fair trade” and “trade protectionism”? What’s your view?

#5. Is there anything else you find interesting/intriguing/thought-provoking in the video? Why?

On September 2, 2022, the Office of the US Trade Representative (USTR) announced it would continue the billions of dollars of Section 301 punitive tariffs against Chinese products. USTR said it made the decision based on requests from domestic businesses benefiting from the tariff action. As a legal requirement, USTR will launch a full review of Section 301 tariff action in the coming months.

In her remarks at the Carnegie Endowment for International Peace on Sep 7, 2022, US Trade Representative Katharine Tai further said that the Section 301 punitive tariffs on Chinese imports “will not come down until Beijing adopts more market-oriented trade and economic principles.” In other words, the US-China tariff war, which broke out four years ago, is not ending anytime soon.

A Brief History of the US Section 301 tariff action against China

The US-China tariff war broke out as both unexpected and not too surprising. For decades, the US government had been criticizing China for its unfair trade practices, such as providing controversial subsidies to state-owned enterprises (SMEs), insufficient protection of intellectual property rights, and forcing foreign companies to transfer critical technologies to their Chinese competitors. The US side had also tried various ways to address the problems, from holding bilateral trade negotiations with China and imposing import restrictions on specific Chinese goods to suing China at the World Trade Organization (WTO). However, despite these efforts, most US concerns about China’s “unfair” trade practices remain unsolved.

When former US President Donald Trump took office, he was particularly upset about the massive and growing US trade deficits with China, which hit a record high of $383 billion in 2017. In alignment with the mercantilism view on trade, President Trump believed that the vast trade deficit with China hurt the US economy and undermined his political base, particularly with the working class.

On August 14, 2017, President Trump directed the Office of the US Trade Representative (USTR) to probe into China’s trade practices and see if they warranted retaliatory actions under the US trade law. While the investigation was ongoing, the Trump administration also held several trade negotiations with China, pushing the Chinese side to purchase more US goods and reduce the bilateral trade imbalances. However, the talks resulted in little progress.

President Trump lost his patience with China in the summer of 2018. In the following months, citing the USTR Section 301 investigation findings, the Trump administration announced imposing a series of punitive tariffs on nearly half of US imports from China, or approximately $250 billion in total. As a result, for more than 1,000 types of products, US companies importing them from China would have to pay the regular import duties plus a 10%-25% additional import tax. However, the Trump administration’s trade team purposefully excluded consumer products such as clothing and shoes from the tariff actions. The last thing President Trump wanted was US consumers, especially his political base, complaining about the rising price tag when shopping for necessities. The timing was also a sensitive factor—the 2018 congressional mid-term election was only a few months away.

President Trump hoped his unprecedented large-scale punitive tariffs would change China’s behaviors on trade. It partially worked. As the trade frictions threatened economic growth, the Chinese government returned to the negotiation table. Specifically, the US side wanted China to purchase more US goods, reduce the bilateral trade imbalances and alter its “unfair” trade practices. In contrast, the Chinese asked the US to hold the Section 301 tariff action immediately.

However, the trade talks didn’t progress as fast as Trump had hoped. Even worse, having to please domestic forces that demanded a more assertive stance toward the US, the Chinese government decided to impose retaliatory tariffs against approximately $250 billion US products. President Trump felt he had to do something in response to China’s new action. In August 2019, he suddenly announced imposing Section 301 tariffs on a new batch of Chinese products, totaling nearly $300 billion. As almost everything from China was targeted, apparel products were no longer immune to the tariff war.With the new tariff announcement coming at short notice, US fashion brands and retailers were unprepared for the abrupt escalation since they typically placed their sourcing orders 3-6 months before the selling season.

Nevertheless, Trump’s new Section 301 actions somehow accelerated the trade negotiation. The two sides finally reached a so-called“phase one” trade agreementin about two months. As part of the deal, China agreed to increase its purchase of US goods and services by at least $200 billion over two years, or almost double the 2017 baseline levels. Also, China promised to address US concerns about intellectual property rights protection, illegal subsidies, and forced technology transfers. Meanwhile, the US side somewhat agreed to trim the Section 301 tariff action but rejected removing them. For example, the punitive Section 301 tariffs on apparel products were cut from 15% to 7.5% since implementing the “phase one” trade deal.

Trump lost the 2020 presidential election, and Joe Biden was sworn in as the new US president on January 20, 2021. However, the Section 301 tariff actions and the US-China “phase one” trade deal stayed in force.

Debate on the impact of the US-China tariff war

Like many other trade policies, the US Section 301 tariff actions against China raised heated debate among stakeholders with competing interests. This was the case even among different US textile and apparel industry segments.

On the one hand, US fashion brands and retailers strongly oppose the punitive tariffs against Chinese products for several reasons:

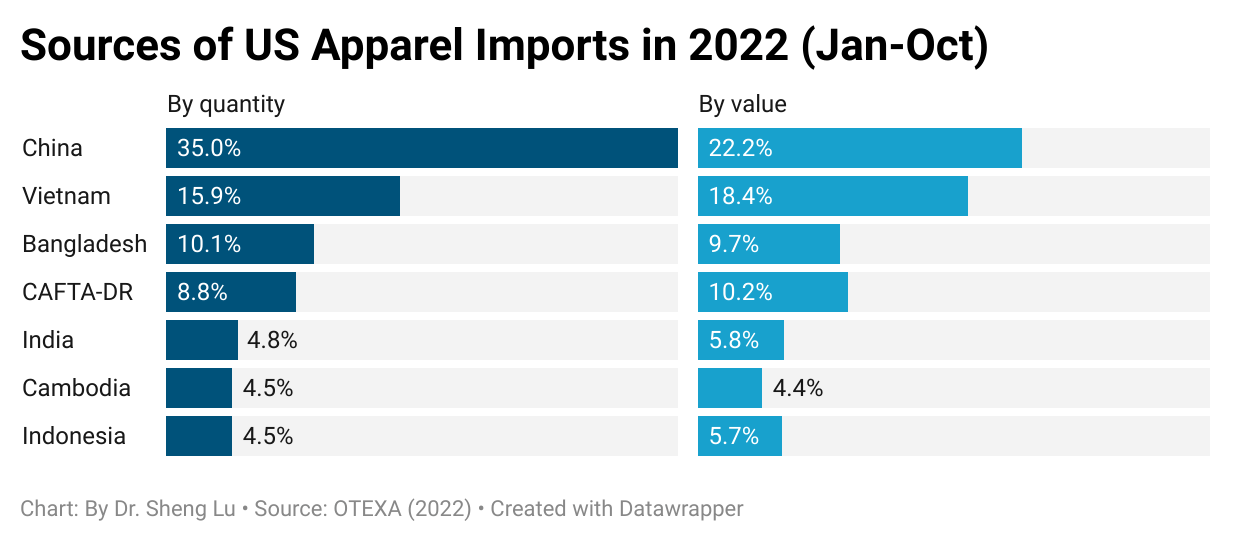

First, despite the Section 301 tariff action, China remained a critical apparel sourcing base for many US fashion companies with no practical alternative. Trade statistics show that four years into the tariff war, China still accounted for nearly 40 percent of US apparel imports in quantity and about one-third in value as of 2021. According to the latest data, in the first ten months of 2022, China remained the top apparel supplier, accounting for 35% of US apparel imports in quantity and 22.2% in value. Studies also consistently find that US fashion companies rely on China to fulfill orders requiring a small minimum order quantity, flexibility, and a great variety of product assortment.

Second, having to import from China, fashion companies argued that the Section 301 punitive tariffs increased their sourcing costs and cut profit margins. For example, for a clothing item with an original wholesale price of around $7, imposing a 7.5% Section 301 punitive tariff would increase the sourcing cost by about 5.8%. Should fashion companies not pass the cost increase to consumers, their retail gross margin would be cut by 1.5 percentage points. Notably, according to the US Fashion Industry Association’s 2021 benchmarking survey, nearly 90 percent of respondents explicitly say the tariff war directly increased their company’s sourcing costs. Another 74 percent say the tariff war hurt their company’s financials.

Third, as companies began to move their sourcing orders from China to other Asian countries like Vietnam, Bangladesh, and Cambodia to avoid paying punitive tariffs, these countries’ production costs all went up because of the limited production capacity. In other words, sourcing from everywhere became more expensive because of the Section 301 action against China.

Further, it is important to recognize that fashion companies supported the US government’s efforts to address China’s “unfair” trade practices, such as subsidies, intellectual property rights violations, and forced technology transfers. Many US fashion companies were the victims of such practices. However, fashion companies did not think the punitive tariff was the right tool to address these problems effectively. Instead, fashion brands and retailers were concerned that the tariff war unnecessarily created an uncertain and volatile market environment harmful to their business operations.

“While NCTO members support the inclusion of finished products in Section 301, we are seriously concerned that…adding tariffs on imports of manufacturing inputs that are not made in the US such as certain chemicals, dyes, machinery, and rayon staple fiber in effect raises the cost for American companies and makes them less competitive with China.”

Mitigate the impact of the tariff war: Fashion Companies’ Strategies

The first approach was to switch to China’s alternatives. Trade statistics suggest that Asian countries such as Vietnam and Bangladesh picked up most of China’s lost market shares in the US apparel import market. For example, in 2022 (Jan-Nov), Asian countries excluding China accounted for 51.2% of US apparel imports, a substantial increase from 41.2% in 2018 before the tariff war. In comparison, about 16.4% of U.S. apparel imports came from the Western Hemisphere in 2021 (Jan-Nov), lower than 17.0% in 2018. In other words, no evidence shows that Section 301 tariffs have expanded U.S. apparel sourcing from the Western Hemisphere.

The second approach was to adjust what to source from China by leveraging the country’s production capacity and flexibility. For example, market data from industry sources showed that since the Section 301 tariff action, US fashion companies had imported more “Made in China” apparel in the luxury and premium segments and less for the value and mass markets. Such a practice made sense as consumers shopping for premium-priced apparel items typically were less price-sensitive, allowing fashion companies to raise the selling price more easily to mitigate the increasing sourcing costs. Studies also found that US companies sourced fewer lower value-added basic fashion items (such as tops and underwear), but more sophisticated and higher value-added apparel categories (such as dresses and outerwear) from China since the tariff war.

China is no longer treated as a sourcing base for low-end cheap product

More apparel sourced from China target the premium and luxuary market segments

Related, US fashion companies such as Columbia Sportswear leveraged the so-called “tariff engineering” in response to the tariff war. Tariff engineering refers to designing clothing to be classified at a lower tariff rate. For example, “women’s or girls’ blouses, shirts, and shirt-blouses of man-made fibers” imported from China can tax as high as 26.9%. However, the same blouse added a pocket or two below the waist would instead be classified as a different product and subject to only a 16.0% tariff rate. Nevertheless, using tariff engineering requires substantial financial and human resources, which often were beyond the affordability of small and medium-sized fashion companies.

Third, recognizing the negative impacts of Section 301 on US businesses and consumers, the Office of the US Trade Representative (USTR) created a so-called “Section 301 exclusion process.” Under this mechanism, companies could request that a particular product be excluded from the Section 301 tariffs, subject to specific criteria determined at the discretion of USTR. The petition for the product exclusion required substantial paperwork, however. Even companies with an in-house legal team typically hire a DC-based law firm experienced with international trade litigation to assist the petition, given the professional knowledge and a strong government relation needed. Also of concern to fashion companies was the low success rate of the petition. The record showed that nearly 90 percent of petitions were denied for failure to demonstrate “severe economic harm.” Eventually, since the launch of the exclusion process, fewer than 1% of apparel items subject to the Section 301 punitive tariff were exempted. Understandably, the extra financial burden and the long shot discouraged fashion companies, especially small and medium-sized, from taking advantage of the exclusion process.

In conclusion, with USTR’s latest announcement, the debate on Section 301 and the outlook of China as a textile and apparel sourcing base will continue. Notably, while economic factors matter, we shall not ignore the impact of non-economic factors on the fate of the Section 301 tariff action against China. For example, with the implementation of the Uyghur Forced Labor Prevention Act (UFLPA), only about 10% of US cotton apparel imports came from China in the first ten months of 2022 (latest data available), the lowest in a decade. As the overall US-China bilateral trade relationship significantly deteriorated in recent years and the friction between the two countries expanded into highly politically sensitive areas, the Biden administration could “willfully” choose to keep the Section 301 tariff as negotiation leverage. Domestically, President Biden also didn’t want to look “weak” on his China policy, given the bipartisan support for taking on China’s rise.

Question: What does a typical day look like during your AAFA internship?

Ally: I would arrive at American Apparel and Footwear Association (AAFA)’s beautiful DC office, take the elevator up to the third floor, greet the two other interns, and make my way over to my desk. For the policy interns, our typical day consisted of working on individual projects and attending committee meetings, such as the weekly Social Responsibility Committee call with member companies, environmental and product safety meetings, trade policy meetings, and others. We also took notes on hearings and events and paid particular attention to topics related to the apparel sector. For example, I listened in and took notes on Hill hearings, workshops hosted by the World Trade Organization (WTO), and International Labour Organization (ILO) meetings. Some additional internship projects included updating country sourcing profiles for AAFA member companies to use in their factory selection process and analyzing trade data.

A very exciting and beneficial component of the AAFA internship experience was being able to attend special industry events such as the Washington International Trade Association (WITA) dinner and AAFA’s Annual Traceability and Sustainability Conference in Pittsburgh, PA. The WITA dinner is often referred to as “Trade Prom” and is packed with a ‘Who’s Who of trade policy professionals–over 500 attendees each year. Volunteering at this event with the other AAFA and WITA interns was incredible. The AAFA 2022 Traceability and Sustainability Conference in Pittsburgh, PA was another highlight of my internship experience. The conference took place at the American Eagle corporate headquarters, which was very exciting to tour. I spent three days in Pittsburgh with the AAFA team and heard presentations from top leaders in the fashion sustainability space, which was a dream! Member retailers spoke about what their companies are working on, what key challenges the industry faces, and how brands can collectively make a difference. It was a truly inspiring event and a phenomenal networking opportunity. This was an experience I will never forget!

Question: Any major projects did you work on during your internship? What did you learn from the experiences?

Ally:One of the main projects I worked on during my internship was updating AAFA’s Sourcing Profiles for their member companies. These country-specific sourcing profiles include essential information relevant to apparel companies’ sourcing decisions, such as a country’s political situation, minimum wage, membership in trade agreements, and economic outlook. Updating these sourcing profiles allowed me to understand why fashion brands and apparel retailers choose to source from particular countries over others. Having this solid background knowledge of leading apparel-sourcing destinations helps me tremendously, especially given that I am very interested in pursuing a career in sourcing. Some other projects I worked on include analyzing the latest US import patterns for travel goods and creating a “Corporate Social Responsibility Checklist” for AAFA members.

Question: What insights did you learn about the fashion apparel industry from the internship? For example, the key issues the industry cares about or the challenges it faces.

Ally: Through this highly valuable internship with AAFA, I saw the fashion industry through a unique policy and “DC” perspective. A key issue the industry cares about is sustainability. For example, fashion companies are increasingly implementing more and more environmentally and socially responsible business practices. Many leading US apparel brands shared their perspectives on building a more sustainable and transparent fashion supply chain at AAFA’s Traceability and Sustainability Conference. Fashion companies are also investing in innovative new technologies to work toward a closed-loop, circular economy.

Another challenge the fashion industry faces today is improving the supply chain’s transparency. For example, the alleged forced labor in China’s Xinjiang region is a huge concern to US apparel companies. With the recent implementation of the Uyghur Forced Labor Prevention Act (UFLPA) in June 2022, many US fashion brands and retailers are seeking advice on how to comply with this new law and minimize potential sourcing disruptions. Now, more than ever, apparel companies need to ensure they can map their supply chains all the way back to the very beginning, such as where they source their raw cotton.

There is also much interest among fashion companies in finding new sourcing destinations outside of China. For example, Sri Lanka sees this as an opportunity, as well as other developing countries such as Vietnam and Cambodia. We could see some notable shifts in US fashion companies’ sourcing patterns in the coming years.

Further, this Fall, I have been interning virtually at Worldwide Responsible Accredited Production (WRAP). WRAP is a non-profit organization headquartered in Arlington VA, with staff worldwide. WRAP certifies factories in the apparel, footwear, and sewn-products sector regarding their social responsibility performance. WRAP helps factories achieve this certification by conducting audits and working with factories directly to improve working conditions. AAFA and WRAP work closely with one another on numerous projects and industry events, and it has been wonderful to connect these two internship experiences. For example, I read and studied factory audit reports at WRAP. This allowed me to see fashion companies’ and auditors’ respective perspectives when examining a factory’s social compliance. Something that I took away from both internships is that garment factories could use auditing as an opportunity rather than a burden. By investing time and energy into improving factory working conditions and getting certified by a third-party organization, such as WRAP, a factory can attract more retailers, gain more business, and provide a better working environment for its workers.

Question: How do your learning experiences at FASH help with your internship? Any specific knowledge or skillsets do you find most critical?

Ally:My learning experiences in the UD’s FASH department were what influenced and inspired me to pursue the internship with AAFA and now with WRAP. FASH455 (Global apparel trade and sourcing), specifically, is what sparked my interest in apparel sourcing, supply chain, and trade. Before taking this class, I certainly had not thought about how free trade agreements affect the fashion industry. I found all the sourcing rules of origin such as “yarn-forward” and “fabric-forward” to be interesting and intriguing and I was eager to learn more. That is part of what led me to seek out these fashion opportunities in DC.

What I’ve learned through my time in the FASH department is that there are so many career directions a fashion merchandising degree can take you. Fashion is not all about runway shows and magazines- although those elements are very exciting. Many people often do not think about so many other aspects of the industry, like sourcing and trade. The fashion department at UD does a great job in providing students with a well-rounded education and improving students’ critical thinking skills, writing skills, data analytic skills, as well as other skills useful in preparing us for our future careers.

Being selected as a UD Summer Scholar during the Summer of 2021 was another fascinating and unique learning experience, which allowed me to begin researching an area of the fashion industry that I am most interested in–sustainability. Specifically, working with Dr. Lu, I researched US fashion retailers’ merchandising and marketing strategies for clothing made from recycled materials. I expanded the Summer Scholar’s research project into my master’s thesis which was recently published in the Journal of Fashion Design, Technology and Education. This is super exciting!

Choosing the University of Delaware and its fashion department for my education was the best choice I could have made. I have such positive memories such as my first business of fashion class with Professor Ciotti, my assortment planning and buying class with Professor Shaeffer, where we simulated working for a department store, and Dr. Cao’s sustainability and textile courses. Being Co-President of the Sustainable Fashion Club was also a highlight of my time in the FASH department. All of my coursework and experiences in the FASH department gave me the confidence needed to succeed in my internship and work experiences.

Question: What’s your plan after graduation?

Ally: I am currently nearing graduation from my Master’s program. I am on track to receive my Master’s degree in Spring 2023 (or earlier!). I am looking for full-time job opportunities in the realm of fashion sourcing, sustainability, and supply chain. I am hoping to live in either New York or DC after graduation, depending on what job opportunities become available. I am also keeping an open mind to other locations/job prospects. I am eager and excited to start my career in an industry that I am so passionate about, and I look forward to seeing where the future takes me!

The full interview, conducted by Modaes’ Editor-in-Chief, Iria P. Gestal, is available HERE (in Spanish). Below is an abridged translation.

Question: Fashion brands have reduced their exposure to China markedly in recent years. What has been the turning point?

Sheng: We could interpret fashion companies’ decisions in the context of their overall sourcing diversification strategy. Many companies want to diversify their sourcing base because of the ever-uncertain business environment, ranging from the continuation of the supply chain disruptions, and the Russia-Ukraine war, to the rising geopolitical tensions. As China is one of the largest sourcing bases for many fashion companies, reducing “China exposure” is unavoidable.

Question: Isn’t there a specific concern about sourcing from China?

Sheng: Definitely! The Uyghur Forced Labor Prevention Act (UFLPA), officially implemented in the summer of 2022, is a big deal. For example, back in 2017, around 30% of US cotton apparel came from China. However, because of the new law and concerns about the risk of forced labor, China’s market shares fell to only 10% as of August 2022. One well-known US brand selling jean products cut their sourcing from China to just 1% of the total.

Question: Is it possible that the apparel sector as a whole reaches that point?

Sheng: Whether we like it or not, it is still unlikely to get rid of China from the supply chain entirely in the short to medium terms. Notably, China continues to play a significant role as a supplier of raw textile materials, particularly for leading apparel-exporting countries in Asia like Vietnam, Bangladesh, and Cambodia. Diversifying textile raw materials sourcing will be a longer and more complicated process.

Question: Is the “China Plus One” strategy no longer enough?

Sheng: The “China Plus One” strategy does not necessarily mean companies only source from “two” countries. Instead, the phrase refers to companies’ sourcing diversification strategy, trying to avoid “putting all eggs in one basket.” However, neither is the case that fashion companies blindly source from more countries today. Notably, many companies attempt to leverage a stronger relationship with key vendors to mitigate sourcing risks and achieve more sourcing flexibility and agility. For example, fashion companies increasingly tend to work with the so-called “super vendors,” i.e., those with multiple country presence and vertical manufacturing capabilities.

Question: Some politicians have said that the war in Russia has been the “geopolitical awakening” of Europe. Has the same thing happened in fashion?