Last week in FASH455, we discussed the unique critical role played by textile and apparel trade in generating economic growth in many developing countries. The developed countries also use trade policy tools, such as trade preference programs, to encourage the least developed countries (LDCs) making and exporting more apparel. However, a debate on these trade programs is that they have done little to improve the genuine competitiveness of LDCs’ apparel exports in the world marketplace, but instead have made LDCs rely heavily on these trade programs to continue their apparel exports. Here is one more example:

With growing concerns about “the deterioration of democracy, respect for human rights and the rule of law in Cambodia”, in a statement made on February 12, 2019, the European Union says it has started the process that could lead to a temporary suspension of Cambodia’s eligibility for EU’s Everything But Arms (EBA) program. Specifically, the EU process will include the following three stages:

Stage 1: six

months of intensive monitoring and engagement with the Cambodian government;

Stage 2: another three months for the EU to produce a

report based on the findings in stage 1

Stage 3: after

a total of twelve months in stages 1

& 2, the EU Commission will conclude the procedure with a final decision on

whether or not to withdraw tariff preferences; it is also at this stage that

the Commission will decide the scope and duration of the withdrawal. Any

withdrawal would come into effect after a further six-month period.

However, the EU

Commission also stressed that launching the temporary withdrawal procedure does

not entail an immediate removal of Cambodia’s preferential access to the EU

market, which “would be the option of last resort.”

Developed in 2001, the EBA program establishes duty-free and quota-free

treatment for all Least Developed Countries (LDCs) in the EU market. EBA includes

almost all industries other than arms and armaments. As of February 2019, there

are 49

EBA beneficiary countries.

The EBA program has benefited the apparel sector in particular given clothing accounts for the lion’s share in many LDCs’ total merchandise exports. Because of the preferential duty benefits provided by EBA, many LDCs can compete with other competitive apparel powerhouses such as China. Notably, the EBA program also adopts the “cut and sew” rules of origin for apparel, which is more general than the “double transformation” rules of origin typically required by EU free trade agreement and trade preference programs. Under the “cut and sew” rule, Cambodia’s apparel exports to the EU can enjoy the import duty-free treatment while using yarns and fabrics sourced from anywhere in the world.

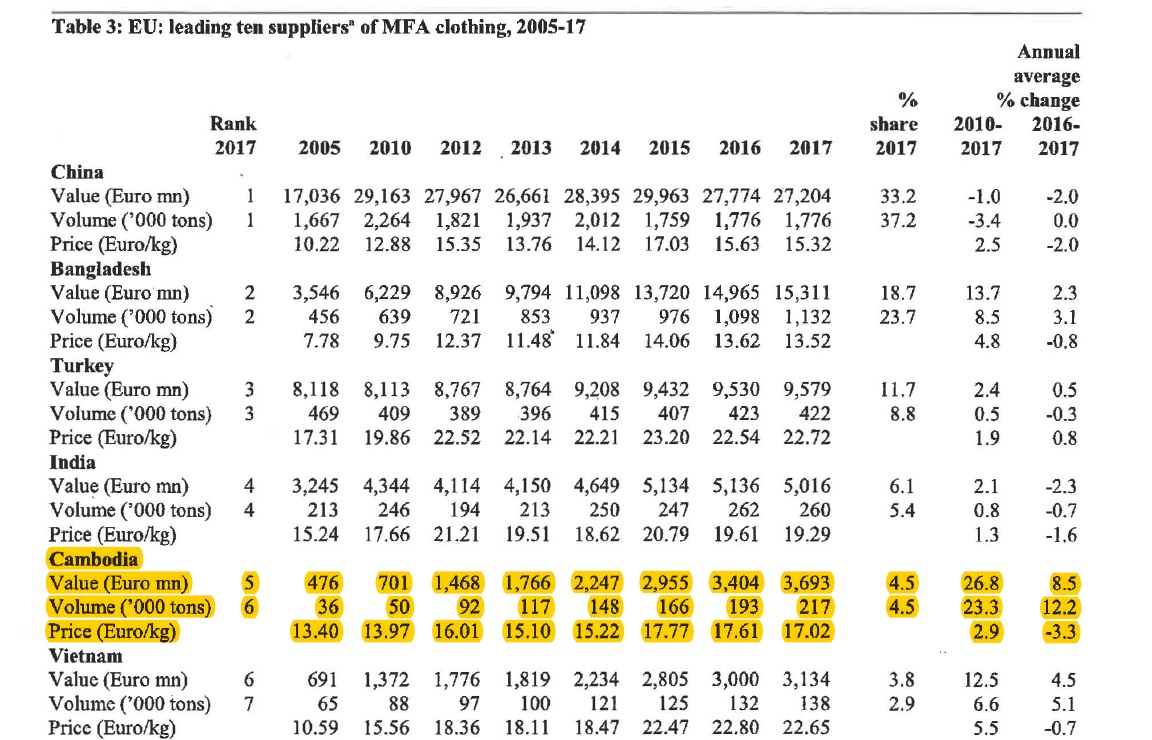

Cambodia is a major apparel supplier for the EU market, accounting for approximately 4% of EU’s

total apparel imports in 2017. Exporting

apparel to EU through the EBA program is also of particular importance to

Cambodia economically. In 2016, the apparel sector created over 500,000

jobs in Cambodia, of whom 86% were female, working in 556 registered factories.

According to Eurostat, of EU’s €4.9bn imports from Cambodia in 2017, around 74.9% were apparel (HS chapters 61 and

62). Meanwhile, of EU’s €3.7bn apparel imports from Cambodia in 2017, as high

as 96.6% claimed the EBA benefits. Understandably,

losing the EBA eligibility could hurt Cambodia’s apparel exports to the EU significantly.

“Globotics” or Globalization + Artificial intelligence (AI) is changing the world. Globotics means globalization mixed with new kinds of robotics, from artificial intelligence to technologies that make it easier to outsource services jobs. Particularly, globotics is injecting pressure into our socio-politico-economic system (via job displacement) faster than our system can absorb it (via job replacement). Overall, AI and robots will take jobs — but make the world better.

Past globalization and automation were mostly about goods— making them and shipping them. However, the era of globotics is about service-sector automation—driven by information and data.

The competition from software robots and telemigrants will seem monstrously unfair to white collar works who lost their jobs. When white-collar workers start sharing the same pain [as blue-collar workers], some sort of backlash is inevitable.

As technologies reduce the need for face-to-face contact, some developing nations stand to benefit. For example, India, with its sizeable English-speaking population and armies of techies, could become a hub for services outsourcing, just as China was for manufacturing.

Future jobs (that are left) will be more human and involve more face-to-face contact since software robots and tele-migrants will do everything else. In other words, the future economy will be more local and more human.

The problem is the short-term. In the era of globotics, it is important to make the rapid job displacement politically acceptable to a majority of voters. Governments may set the policy goal to protect workers, not jobs.

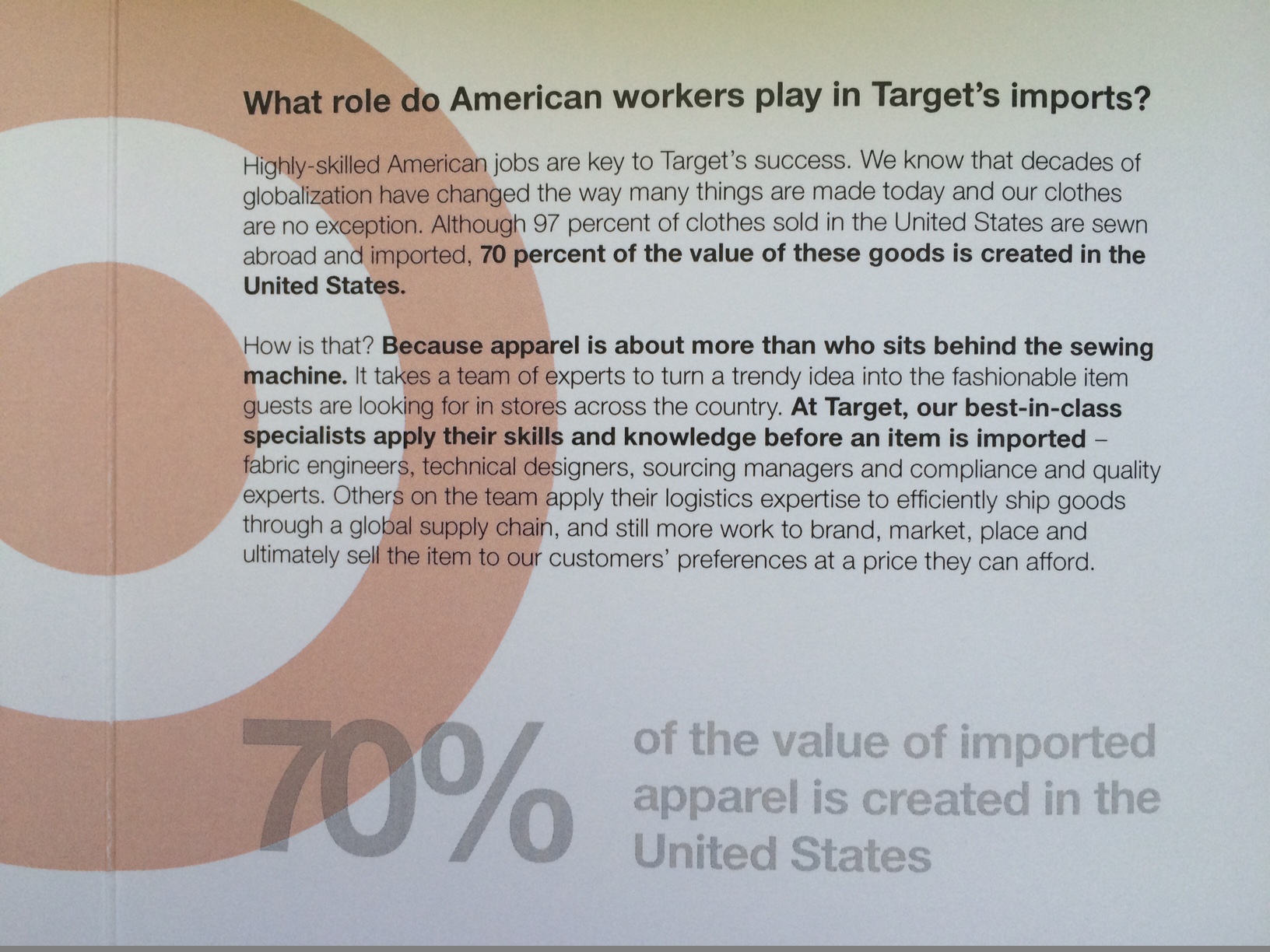

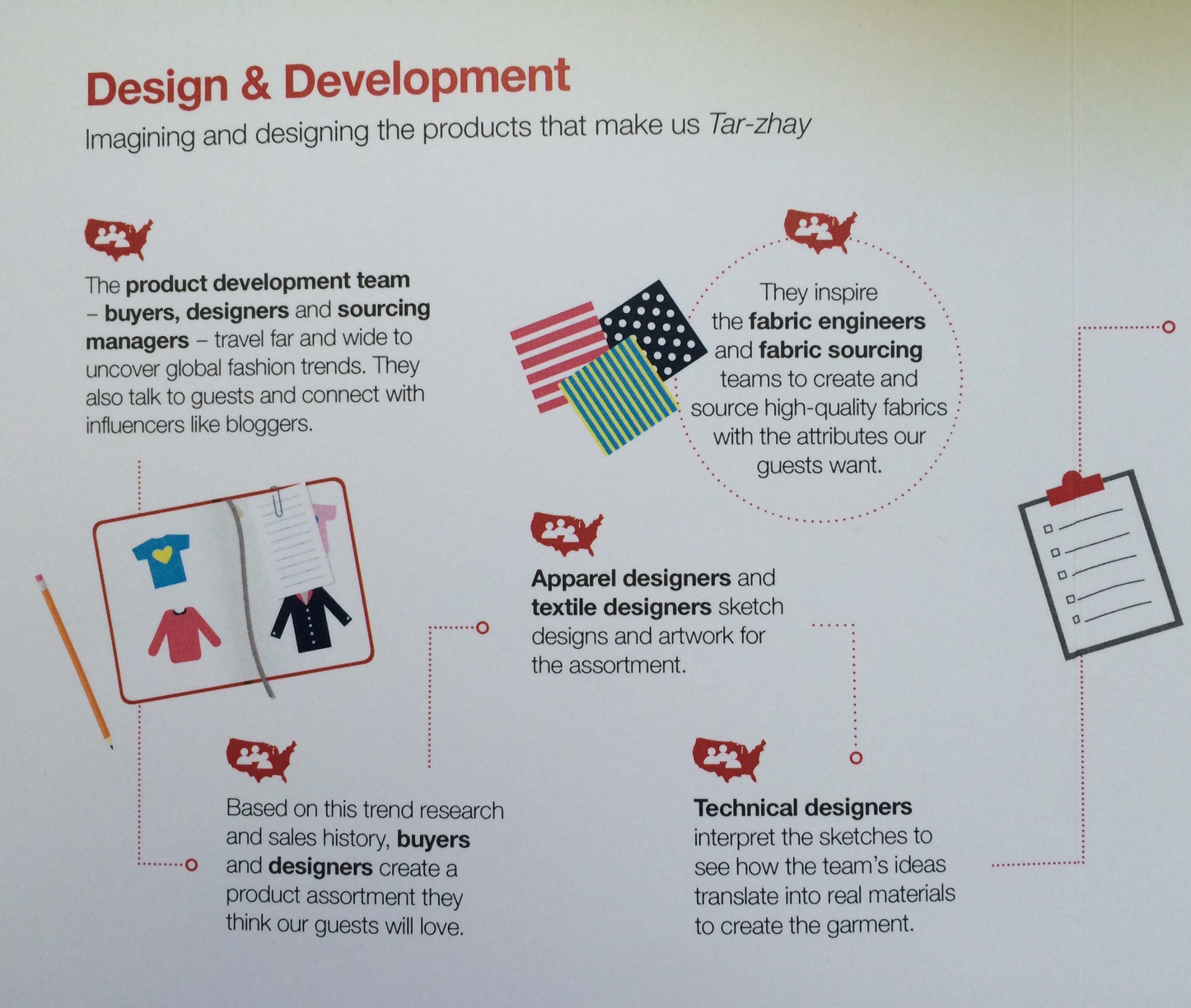

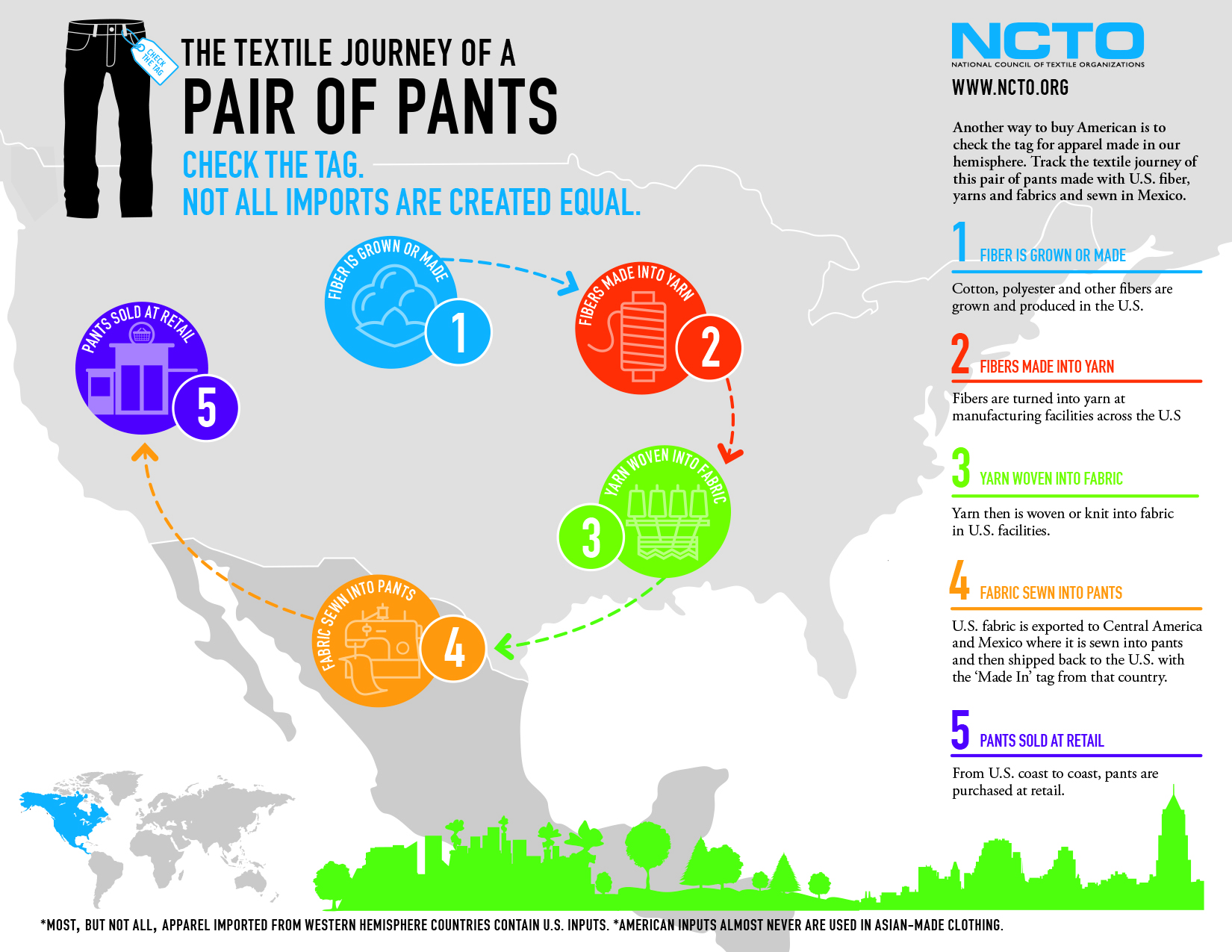

A global view in mind means more career opportunities: except material production and cut and sew, other well-paid jobs in the apparel value chain stay in the United States.

Source: Moongate Association (2017). Analyzing the Value Chain for Apparel Designed in the United States and Manufactured Overseas

While the majority of apparel consumed in the United States come from overseas, “Made in the USA” is growing in popularity. According to the 2018 U.S. Fashion Industry Benchmarking Study released by the U.S. Fashion Industry Association (USFIA) in July 2018, around 46 percent of surveyed U.S. fashion brands and apparel retailers report currently sourcing “Made in the USA” products, even though local sourcing typically only account for less than 10 percent of these companies’ total sourcing value or volume. Likewise, the State of Fashion 2019 report published by Business of Fashion (BOF) and McKinsey & Company in November also forecasts that over 20 percent of U.S. fashion companies’ sourcing volume could be from nearshore by 2025, thanks to automation technology and consumers’ increasing demand for speed to market.

However, the detailed practice of the “Made in the USA” apparel sourcing strategy–including who is sourcing, what products are sourced, and what the typical price range of these products remain largely unknown.

To answer these questions, we recently analyzed the pricing, product assortment and inventory information of over 90,000 fashion retailers and 300,000,000 fashion apparel products at the Stock-Keeping Unit (SKU) level based on EDITED, a big data and business analytics tool developed for the fashion industry. For the research purpose, we selected apparel products newly launched to the U.S. market in the past twelve months (i.e., between 1 December 2017 and 30 November 2018) with “Made in the USA” explicitly mentioned in the product description. Below are the key findings:

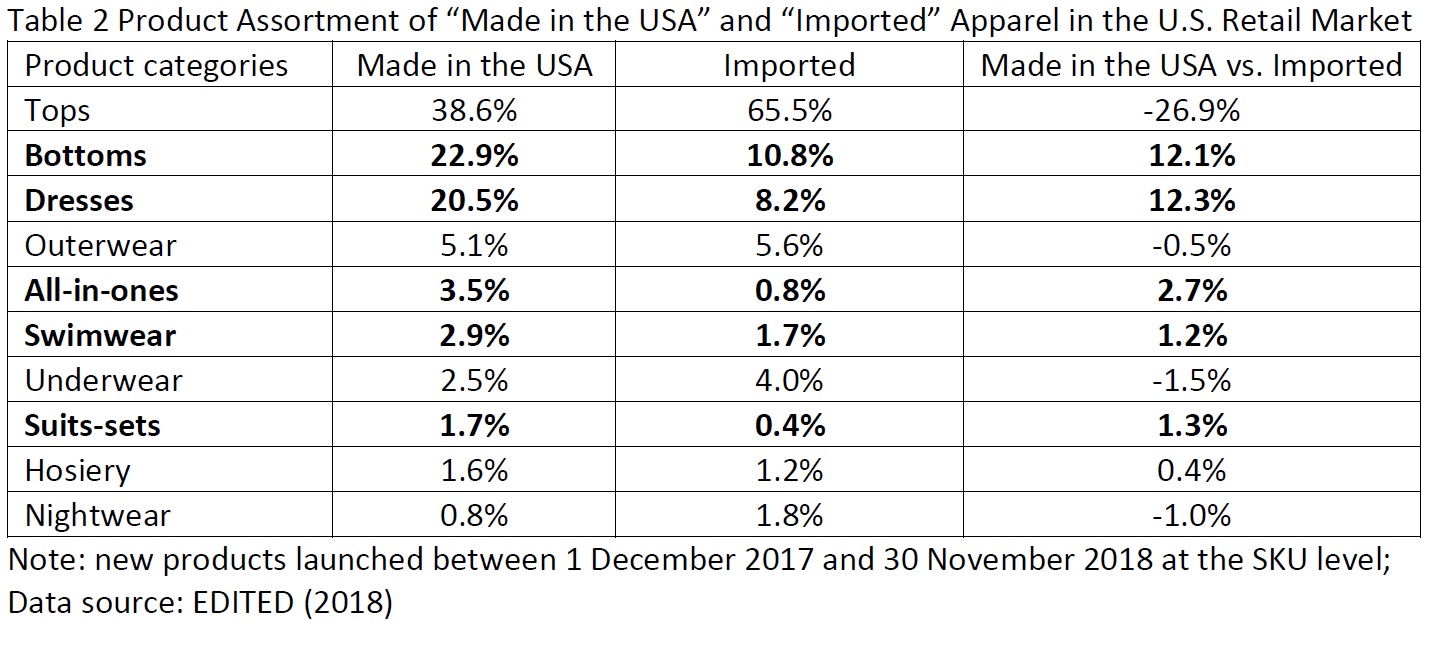

First, “Made in the USA”

apparel overall are treated as a niche product in U.S. fashion brands and

retailers’ sourcing portfolio.

During

the 12 months we examined (1 December 2017-30 November 2018), 94 out of the

total 348 retailers (or 27 percent) sold “Made in the USA” apparel in the U.S.

market. The top 10 sellers list includes BOTH retailers that focus on the value

market such as Walmart and relatively high-end department stores such as

Bloomingdale and Saks Fifth Avenue. However, even for these top sellers, “Made

in the USA” apparel accounted for less than 8 percent of their total product

offers on average.

Second, U.S. fashion brands and retailers are most

likely to source“Made in the

USA” apparel for relatively fashion-oriented items, particularly bottoms (such

as skirts, jeans, and trousers), dresses, all-in-ones (such as playsuits and

dungarees), swimwear and suits-sets.

The competitive

edge for these product categories in the retail market, in general, increasingly depends on unique designs, high

product quality, and speed to market,

which makes sourcing from the United States commercially beneficial. In comparison, imported products are more concentrated

on basic fashion items often competing on price in the U.S. retail market,

including tops (such as T-shirt and polo shirt), underwear, and nightwear.

It is also interesting to note that

“Made in the USA” apparel were predominately women’s wear (92 percent), whereas imported

clothing adopted a more balanced gender combination (63 percent women’s wear

and 37 percent men’s wear). Because the fashion trends for women’s wear usually

are shorter-lived and harder to predict, this result once again indicates that seeking

quick response and shorter lead time for stylish and trendy items could be an

important incentive for local sourcing by U.S. fashion brands and retailers.

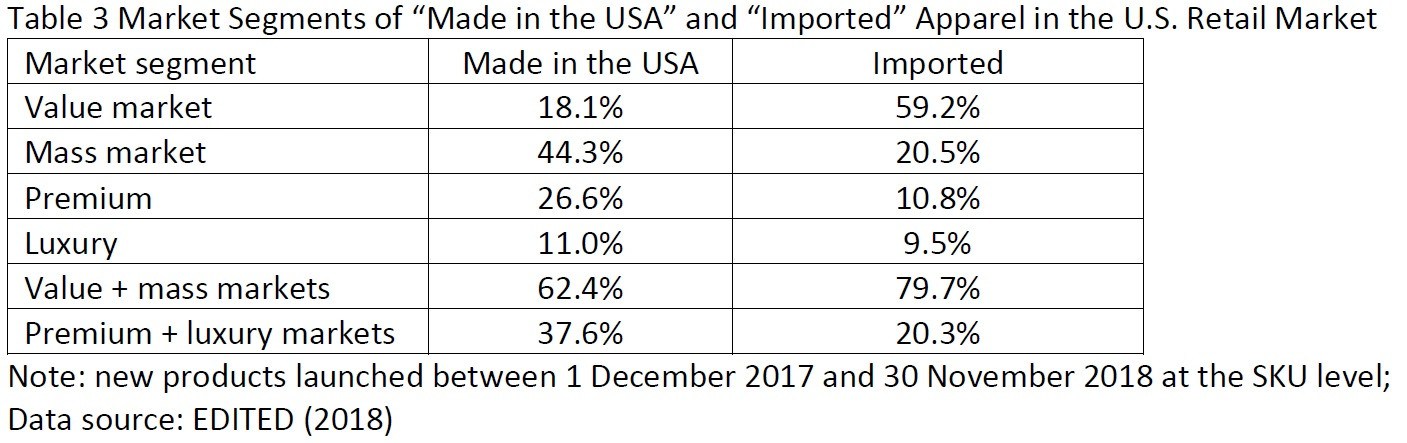

Third, consistent with the common perception,

“Made in the USA” apparel overall are pricier than imported ones in the U.S.

retail market.

Taking the U.S.

apparel retail market as a whole, close to 40 percent of “Made in the USA” offering

in the past 12 months targeted the premium or luxury market, compared with only

20 percent of imported products. In

contrast, as few as 18 percent of “Made in the USA” offering were in the value

market, which, however, accounted for approximately 60 percent of all imported apparel

sold in the U.S. market. In totality, it

seems U.S. fashion brands and retailers are purposefully targeting “Made in the

USA” apparel for less price-sensitive segments of the market to balance the

high domestic production cost.

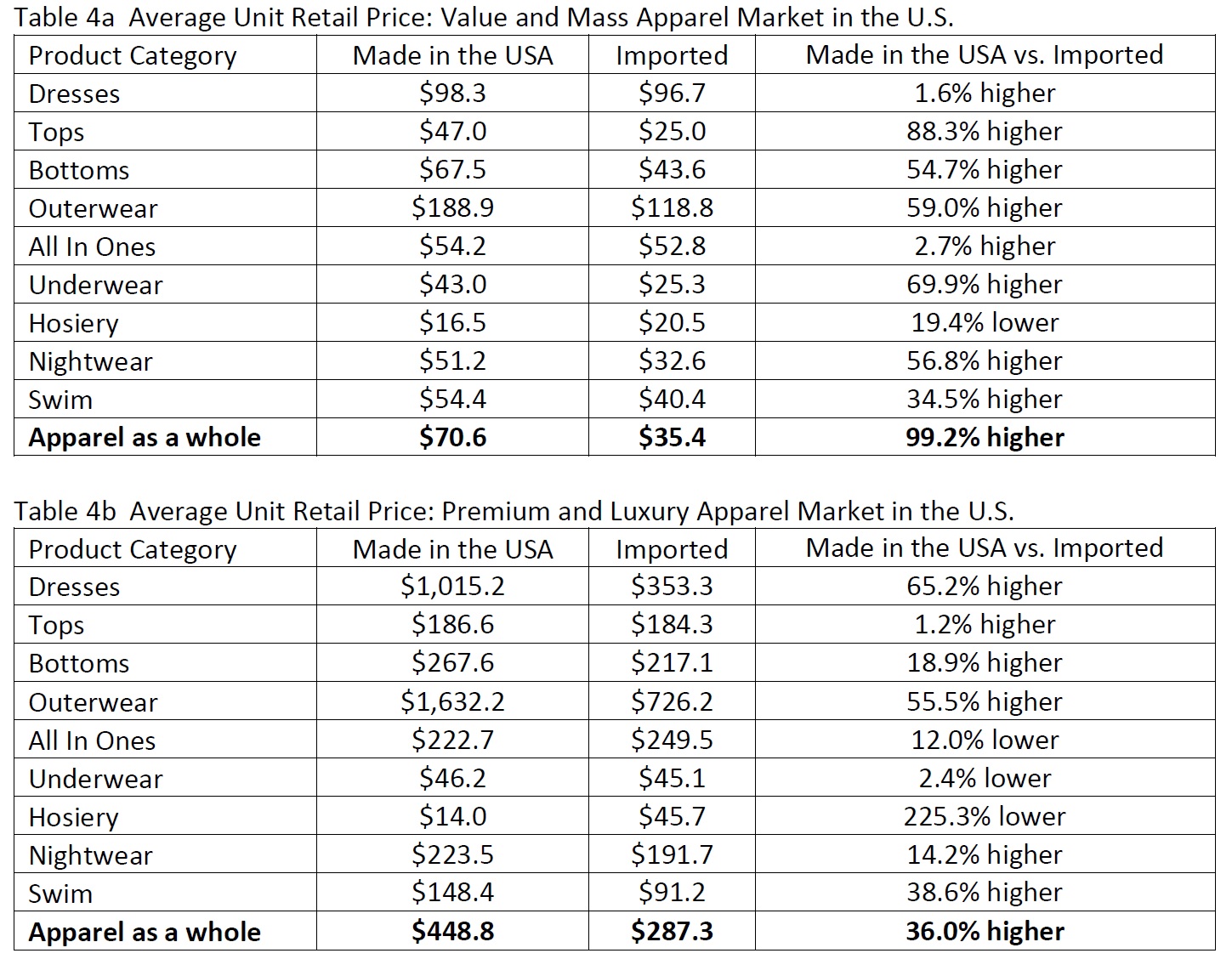

On the other hand, when examining

U.S. fashion brands and retailers’ pricing strategy at the product level, “Made

in the USA” clothing was still priced much higher than imported ones for almost

all major apparel categories, except hosiery. Notably, in the past 12 months, the

average unit retail price of “Made in the USA” clothing was 99.2 percent higher

than imported ones in the value and mass market and 36.0 percent higher in the

premium and luxury market. This interesting phenomenon supports the arguments that

U.S. consumers somehow are willing to pay a premium price for products with the

“Made in the USA” label.

Additionally, during the past 12

months, around 46.3 percent of “Made in the USA” apparel were sold at a

discount compared with more than 54.6 percent of imported ones. The advantage

of proximity to the market, which makes speedy replenishment for in-season items

possible, is an important factor behind the more successful control of

markdowns for “Made in the USA” products. For example, data shows that U.S.

fashion brands and retailers replenished approximately 12.7 percent of their “Made

in the USA” offering in the past 12 months but only 2.8 percent of imported

clothing.

In conclusion, the findings of this study concur with the view that “Made in the USA” apparel are still relevant today. Meanwhile, it does not seem to be the case that “Made in the USA” apparel and imported ones are necessarily competing with each other in the U.S. retail market. With apparel sourcing increasingly requiring striking a balance among various factors ranging from cost, flexibility, compliance to speed to market, it is hopeful that “Made in the USA” apparel will continue to have its unique role to play in U.S. fashion brands and retailers’ merchandising and sourcing strategies.

1: What do you see as the biggest challenges – and opportunities – facing the apparel industry in 2019, and why?

In my view, uncertainty will remain the single biggest challenge facing the apparel industry in 2019, ranging from a more volatile global economy, the unpredictable outlook of the U.S.-China trade talks to the various possible scenarios of Brexit. While uncertainty creates exciting new research opportunities for scholars like me, it could be a big headache for companies seeking a foreseeable market environment to guide their future business plan and investments.

Meanwhile, the increasing digitalization of the apparel supply chain based on big-data tools and artificial intelligence (AI) technologies means a huge opportunity for fashion companies. Indeed, the apparel industry is quickly changing in nature—becoming ever more globalized, supply-chain based, technology-intensive and data-driven. Take talent recruitment as an example. In the 2018 US Fashion Industry Benchmarking Study, which I conducted in collaboration with the US Fashion Industry Association (USFIA), as much as 68 percent of surveyed leading U.S. fashion brands and apparel retailers say they plan to increase hiring of data scientists in the next five years. Googling “apparel industry” together with terms such as “big data” and “data science” also returns much more results than in the past. It is hopeful that the advancement of digital technologies and the smarter use of data will enable apparel companies to overcome market uncertainties better and improve many aspects of their businesses such as speed to market, operational efficiency and even sustainability.

2: What’s happening with sourcing? How is the sourcing landscape likely to shift in 2019, and what can apparel firms and their suppliers do to stay ahead?

Based on my research, I have three observations regarding apparel companies’ sourcing trends and the overall sourcing landscape in 2019:

First, apparel companies overall will continue to maintain a diverse sourcing base. For example, in a recent study, we examined the detailed sourcing portfolios of the 50 largest U.S.-based apparel companies ranked by the Apparel Magazine. Notably, on average these companies sourced from over 20 different countries or regions using more than 200 vendors in 2017. Similarly, in the 2018 US Fashion Industry Benchmarking Study, which I conducted in collaboration with the US Fashion Industry Association (USFIA), we also found companies with more than 1,000 employees typically source from more than ten different countries and regions. Since no sourcing destination is perfect, maintaining a relatively diverse sourcing base allows apparel companies to strike a balance among various sourcing factors ranging from cost, speed, flexibility, to risk management.

Second, while apparel companies are actively seeking new sourcing bases, many of them are reducing either the number of countries they source from or the number of vendors they work with. According to our study, some apparel companies have been strategically reducing the number of sourcing facilities with the purpose of ensuring closer collaborations with their suppliers on social and environmental compliance issues. Some other companies are consolidating their sourcing base within certain regions to improve efficiency and maximize productivity in the supply chain. Related to this trend, it is interesting to note that approximately half of the 50 largest U.S. apparel companies report allocating more sourcing orders to their largest vendor in 2017 than three years ago.

Third, nearshoring or onshoring will become more visible. Take “Made in the USA” apparel for example. According to the 2018 U.S. Fashion Industry Benchmarking Study, around 46 percent of surveyed U.S. fashion brands and apparel retailers report currently sourcing “Made in the USA” products, even though local sourcing typically only account for less than 10 percent of these companies’ total sourcing value or volume. In a recent study, we find that 94 out of the total 348 retailers (or 27 percent) sold “Made in the USA” apparel in the U.S. market between December 2017 and November 2018. These “Made in the USA” apparel items, in general, focus on fashion-oriented women’s wear, particularly in the categories of bottoms (such as skirts, jeans, and trousers), dresses, all-in-ones (such as playsuits and dungarees), swimwear and suits-sets. The advantage of proximity to the market, which makes speedy replenishment for in-season items possible, also allows retailers to price “Made in the USA” apparel substantially higher than imported ones and avoid offering deep discounts. Looking ahead, thanks to automation technology and consumers’ increasing demand for speed to market, I think nearshoring or onshoring, including ”Made in the USA” apparel, will continue to have its unique role to play in fashion brands and retailers’ merchandising and sourcing strategies.

3: What should apparel firms and their suppliers be doing now if they want to remain competitive further into the future? What will separate the winners from the losers?

2019 will be a year to test apparel companies’ resources, particularly in the sourcing area. For example, winners will be those companies that have built a sophisticated but nimble global sourcing network that can handle market uncertainties effectively. Likewise, companies that understand and leverage the evolving “rules of the game”, such as the apparel-specific rules of origin and tariff phase-out schedules of existing or newly-reached free trade agreements, will be able to control sourcing cost better and achieve higher profit margins. Given the heavy involvement of trade policy in apparel sourcing this year, companies with solid government relations should also enjoy unique competitive advantages.

On the other hand, as apparel business is changing in nature, to stay competitive, apparel companies need to start investing the future. This includes but not limited to exploring new sourcing destinations, studying the changing consumer demographics, recruiting new talents with expertise in emerging areas, and adopting new technologies fitting for the digital age.

4: What keeps you awake at night? Is there anything else you think the apparel industry should be keeping a close eye on in the year ahead? Do you expect 2019 to be better than 2018, and why?

Two things are at the top of my watchlist:

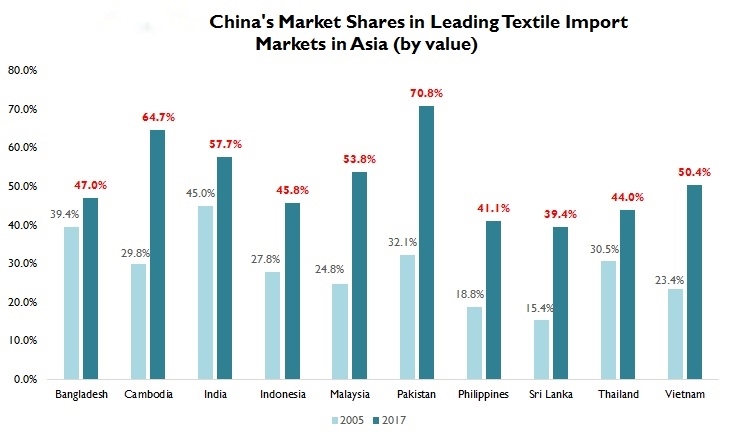

First, what is the future of China as an apparel sourcing base? While external factors such as the U.S.-China tariff war have attracted most of the public attention, the genuine evolution of China’s textile and apparel industry is something even more critical to watch in the long run. From my observation, China is playing an increasingly important role as a textile supplier for apparel-exporting countries in Asia. For example, measured by value, 47 percent of Bangladesh’s textile imports came from China in 2017, up from 39 percent in 2005. Similar trends are seen in Cambodia (up from 30 percent to 65 percent), Vietnam (up from 23 percent to 50 percent), Pakistan (up from 32 percent to 71 percent), Malaysia (up from 25 percent to 54 percent), Indonesia (up from 28 percent to 46 percent), Philippines (up from 19 percent to 41 percent) and Sri Lanka (up from 15 percent to 39 percent) over the same time frame. A key question in my mind is how quickly China’s textile and apparel industry will continue to evolve and upgrade by following the paths of most other advanced economies in history.

Second, how will the implementation of several newly-reached free trade agreements (FTAs) affect the big landscape of apparel sourcing and the existing regional apparel supply chains? For example:

The newly-reached U.S.-Mexico-Canada Free Trade Agreement (USMCA or commonly called NAFTA2.0) includes several interesting changes to the textile and apparel specific rules of origin provisions, such as the adjustment of the tariff-preference level (TPL) mechanism. Whether these changes will boost textile and apparel production in the Western-Hemisphere and attract more sourcing from the region will be something interesting to watch.

The implementation of the Comprehensive and Progressive Agreement of the Trans-Pacific Partnership (CPTPP)and the EU-Vietnam Free Trade Agreement (EVFTA)will allow Vietnam to get access to nearly 40% of the world apparel import market (i.e., EU + Japan) duty-free. However, restrained by the country’s relatively small population, the apparel industry is increasingly facing the challenge of competing for labor with other export-oriented sectors in Vietnam. Realistically, what is the growth potential of apparel “Made in Vietnam” after the implementation of CPTPP and EVFTA?

In 2017, close to 80% of Asian countries’ textile imports came from other Asian countries, up from around 70% in the 2000s. Similarly, in 2017, 85.6% of Asian countries’ apparel imports also came from within the region. The negotiation of the Regional Comprehensive and Economic Partnership (RCEP) is likely to conclude in 2019, whose membership includes member states of the Association of Southeast Asian Nations (ASEAN) and other six economies in the Asia-Pacific region (Australia, China, India, Japan, South Korea and New Zealand). Will RCEP result in an ever more integrated Asia-based textile and apparel supply chain and make the Asia region even more competitive as an apparel sourcing destination?

On

October 16, 2018, the Trump

Administration notified U.S. Congress its intention to negotiate the

U.S.-EU Free Trade Agreement. Between

2013 and 2016, the United States and EU were also engaged in the negotiation of

a comprehensive free trade agreement– Trans-Atlantic Trade and Investment Partnership

(T-TIP) with the goal to unlock market access opportunities for

businesses on both sides of the Atlantic through the ambitious elimination of

trade and investment barriers as well as enhanced regulatory coherence. The T-TIP

negotiation was stalled since 2017, although

the Trump Administration has never officially announced to withdraw from the

agreement.

II. Negotiating Objectives

On

January 11, 2019, the Office of the U.S. Trade Representative (USTR) released

thenegotiating

objectives of the proposed U.S.-EU Free Trade Agreement after

seeking inputs from the public. Overall, the proposed agreement aims to address

both tariff and non-tariff barriers and to “achieve fairer, more balanced trade”

between the two sides.

Regarding textiles and apparel, USTR says it will secure duty-free access for U.S. textile and

apparel products and seek to improve competitive opportunities for exports of

U.S. textile and apparel products while taking into account U.S. import

sensitivities” during the negotiation. The proposed U.S.-EU free trade

agreement also will “establish origin procedures for the certification and

verification of rules of origin that promote strong enforcement, including with respect to textiles.” T-TIP

had adopted similar negotiating objectives for the textile and apparel sector.

III. Industry viewpoints on the agreement

As of

January 2019, leading trade associations

representing the U.S. apparel industry and the EU textile and apparel industries

have expressed support for the proposed U.S.-EU Free Trade Agreement. In general,

these industry associations recommend the agreement to achieve the following

goals:

First, eliminate import duties. For example:

American

Apparel and Footwear Association (AAFA): “We

support the immediate and reciprocal elimination of the high duties that both

countries maintain on textiles, travel goods, footwear, and apparel.”…” We also

support the immediate elimination of any retaliatory duties imposed by the

E.U., as well as any duties imposed by the U.S. (that led to that retaliation).

The duties impose costs on activities, including manufacturing activities in

the U.S., and undermine markets for U.S. exporters in Europe.”

European

Apparel and Textile Confederation (Euratex):“The

European Textile and Clothing sector faces high tariffs while exporting to the

US market from 11% to up to 32% for some products, namely sewing thread of

man-made filaments, suits, woven fabrics of cotton, trousers and t-shirts. Zero

customs duties while ensuring modern rules of origin will allow EU companies to

boost exports and offer more choice to American consumers and professional

buyers.”

Second, promote regulatory coherence (Harmonization). For example:

AAFA: “The E.U. and the

United States both maintain an extensive array of product safety, chemical management,

and labeling requirements regarding apparel (including legwear), footwear,

textiles, and travel goods.”…” Yet they often contain different requirements,

such as testing or certification, that greatly add compliance costs.”…” We

believe the U.S.‐E.U. trade agreement presents an important opportunity to achieve

harmonization or alignment for these regulations.”

Euratex: “Maintaining high

level of standards while eliminating unnecessary burdens, removing additional

requirements and facilitating customs procedures that impede business are top

priorities. Mutual recognition of the EU and US standards will preserve high

level of consumer protection on both sides of the Atlantic. Convergence on labelling (fibre

names, care symbols and wool labelling),

consumer safety on children products and flammability standards is key for the

T&C sector.” “EURATEX believes the EU and US standardization bodies should

cooperate on setting standards for Smart Textiles taking into account the

industry views for facilitating development and trade of such products of the

future.”

Third, adopt flexible/modern rules of origin. For example:

AAFA: “We should also support higher usage of the agreement by making sure the rules of origin reflect the realities of the industry today…”the yarn forward” rules, although theoretically promote usage of trade partner inputs, in practice they operate as significant barriers that restrict the ability of companies to use a trade agreement in many cases”…” We need to incorporate sufficient flexibilities into the rules of origin so that different supply chains –and the U.S. jobs they support – can take advantage of the agreement.”

Euratex: “Zero customs

duties while ensuring modern rules of

origin will allow EU companies to boost exports and offer more choice to

American consumers and professional buyers.”

The National Council of Textile Organizations (NCTO), which represents the U.S. textile industry, hasn’t publically stated its position on the proposed U.S.-EU Free Trade Agreement. However, NCTO had strongly urged U.S. trade negotiators to adopt a yarn-forward rule of origin in T-TIP. NCTO also opposed opening the U.S. government procurement market protected by the Berry Amendment to EU companies.

IV. Patterns of U.S.-EU textile and apparel trade

The

United States and the EU are mutually important textile and apparel (T&A)

trading partners. For example, the United States is EU’s largest extra-region

export market for textiles, and EU’s fifth largest extra-region supplier of

textiles in 2017 (Euratex, 2018).

Meanwhile,

the EU is one of the leading export markets for U.S.-made technical textiles as

well as an important source of high-end apparel products for U.S. consumers (OTEXA,

2018). Specifically, in 2017, U.S. T&A exports to the European Union

totaled $2,572 million, of which 73.2% were textile products, such as specialty

& industrial fabrics, felts & other non-woven fabrics and filament

yarns. In comparison, EU’s T&A exports to the United States totaled $4,163

million in 2017, among which textiles and apparel evenly accounted for 48.7%

and 51.3% respectively.

V. Potential economic impact of the agreement

By adopting the Global Trade Analysis Project (GTAP) model, Lu (2017) quantitatively evaluated the potential impact of a free trade agreement between the U.S. and EU on the textile and apparel sector. According to the study:

First,

the trade creation effect of the agreement will expand the EU-U.S.

intra-industry trade for textiles. Meanwhile, the agreement is likely to

significantly expand EU’s apparel exports to the United States.

Second,

the trade diversion effect of the U.S.-EU Free Trade Agreement will affect other

T&A exporters negatively, including Asia’s T&A exports to the U.S. market

and EU and Turkey’s T&A exports to the EU market.

Third, the U.S.-EU Textile and Apparel Trade might affect the intra-region T&A trade in the EU region negatively but in a limited way.

Overall, the study suggests that the EU T&A industry will benefit from the additional market access opportunities created by the U.S.-EU Free Trade Agreement.One important factor is that the U.S. and EU T&A industries do not constitute a major competing relationship. For example, the United States is no longer a major apparel producer, and EU’s apparel exports to the United States fulfill U.S. consumers’ demand for high-end luxury products. The U.S.-EU Free Trade Agreement is also likely to create additional export opportunities for EU textile companies in the U.S. market, especially in the technical textiles area, which accounted for approximately 40% of EU’s total textile exports to the United States in 2017 measured in value. Compared with traditional yarns and fabrics for apparel making purposes, technical textiles are with a greater variety in usage, which allows EU companies to be able to differentiate products and find their niche in the U.S. market.

Further, the study suggests that we shall pay more attention to the details of non-tariff barrier removal under the U.S.-EU Free Trade Agreement, which could result in bigger economic impacts than tariff elimination.

On December 21, 2018, Office of the U.S. Trade Representative (USTR) released negotiating objectives of the proposed U.S.-Japan Free Trade Agreement (USJTA). Overall, USJTA aims to address both tariff and non-tariff barriers to achieve fairer and more balanced trade between the two countries.

Regarding the textiles and apparel sector, USTR says it will “secure duty-free access for U.S. textile and

apparel products and seek to improve competitive opportunities for exports of

U.S. textile and apparel products while taking into account U.S. import

sensitivities” during the negotiation. USJTA also will “establish origin

procedures for the certification and verification of rules of origin that

promote strong enforcement, including with respect to textiles.” According to

the 2015 Trade Promotion Authority Act, the earliest day to start the USJTA

negotiation will be in mid-January 2019.

Regarding the potential economic impact of USJTA on the textile and apparel sector:

First, the overall economic impact is likely to be modest given the limited U.S.-Japan bilateral trade flows for textiles and apparel. Data from the UNComtrade shows that in 2017 U.S. exported $220 million textiles (1.7% of the total) and $141 million apparel (4.7% of the total) to Japan. Meanwhile, U.S. imported $550 million textiles (1.9% of the total) and $104 million apparel (0.1% of the total) from Japan. In comparison, over 70% of U.S. textile and apparel exports went to the Western-Hemisphere and U.S. imported textiles and apparel mostly from NAFTA & CAFTA-DR members and other Asian countries (such as China and Vietnam).

Second, the elimination of tariff and non-tariff barriers under USJTA could expand the bilateral trade flows for technical textiles. Notably, the top categories of U.S. textile and apparel exports to Japan in 2017 were mostly technical textiles such as specialty and industrial fabrics, filament yarns, and non-woven textiles. Likewise, the top categories of Japan’s textile and apparel exports to the U.S. in 2017 also include special purpose fabric, non-woven fabric, and synthetic filament fabrics.

Third, the textiles and apparel-specific rules of origin (RoO) is likely to remain a heated debate in the USJTA negotiation. To protect the interests of the U.S. textile industry and the Western-Hemisphere regional textile and apparel supply chain, most free trade agreements enacted in the United States adopt the so-called “yarn-forward” RoO. Even though USJTA may not be a too big deal economically, the U.S. textile industry is unlikely to give up the RoO fight. However, most free trade agreements enacted in Japan adopt more liberal fabric-forward rules of origin. As textile and apparel production in Japan is increasingly integrated with other Asian countries, the strict “yarn-forward” RoO could prevent Japanese textile and apparel exporters from enjoying the preferential duty benefits under USJTA fully. On the other hand, adopting a liberal RoO in USJTA is also advocated strongly by U.S. fashion brands and apparel retailers.

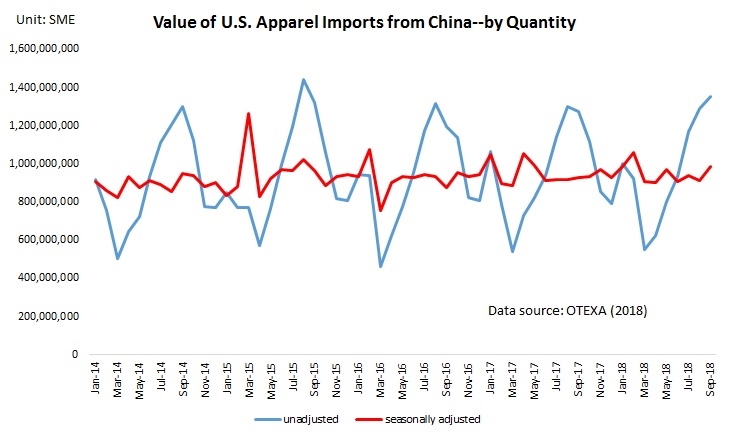

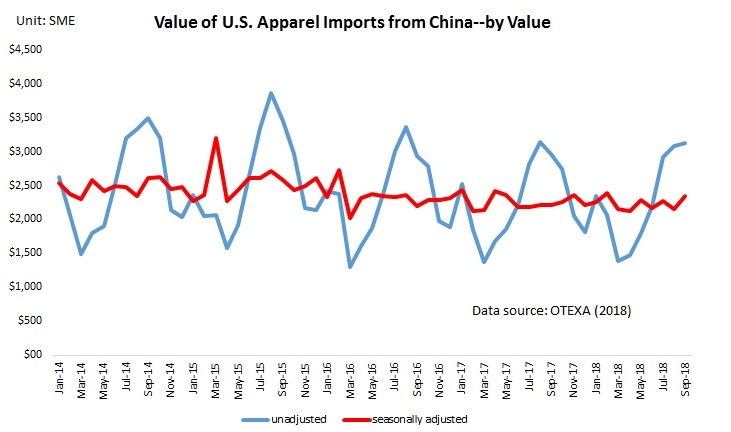

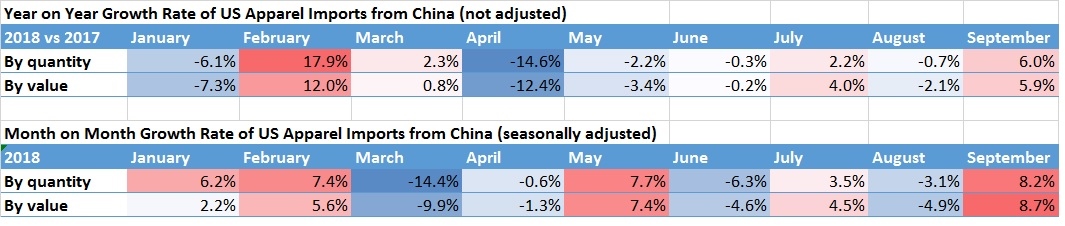

While apparel products are not subject to the Section 301 tariff yet, the trade action nevertheless has created huge market uncertainties for U.S. fashion brands and apparel retailers. Here is how the monthly trade flow of U.S. apparel imports has reflected the impacts of the U.S.-China tariff war:

First, U.S. companies did NOT stop importing from China. Seasonally adjusted data shows that between January and September 2018, the value of U.S. apparel imports from China decreased by 0.6 percent in volume and 0.05 percent in value year on year. Despite the decline, China remained the No.1 apparel supplier for the U.S. market in the first nine months of 2018, accounting for 32.3 percent market share in value and 41.3 percent shares in quantity, only marginally dropped by 1 and 0.7 percentage points from a year earlier respectively .

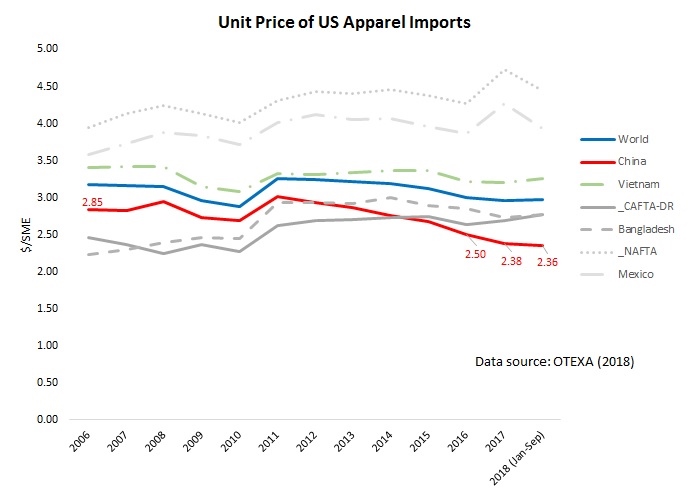

Second, apparel “Made in China” are becoming even cheaper. Notably, the average unit price of U.S. apparel imports from China dropped from $2.5/SME in 2016,$2.38/SME in 2017 to $2.36/SME in the first nine months of 2018. On the one hand, this result suggests that cost concern is not the most influential factor that drives U.S. companies to source less from China. However, it is also likely that Chinese exporters are intentionally reducing their price to keep their orders and overcome the challenges caused by the Section 301.

Third, there is no perfect replacement for “Made in China”. In response to the market uncertainty created by the Section 301 trade action, U.S. apparel importers are diversifying their sourcing base. That being said, it is difficult to identify a single largest beneficiary–notably, the market shares of apparel exports from Vietnam, Bangladesh, NAFTA, and CAFTA regions only marginally increased in the first nine months of 2018 compared with a year ago.

Additionally, it remains unclear whether the section 301 trade action has benefited U.S. textile and apparel manufacturing. Data shows that in the first ten months of 2018, the production index (2012=100) of textile manufacturing in the United States slightly increased from 92.8 in 2017to 94.3. However, over the same period, the index of apparel manufacturing decreased from 73.6 to 72.4.

Looking ahead, the volume of US textile and apparel imports from China is likely to increase in the short run since U.S. importers are eager to complete their sourcing orders before the new tariff hit. Usually, companies place sourcing orders several months ahead of the selling season. However, it will be interesting to see if the trade data in the first half of 2019 will reveal the negative impact of the Section 301 action on China’s apparel exports to the U.S. market.

On November 16, 2018, leading U.S. textile and apparel associations testified before the U.S. International Trade Commission (USITC) to provide industry assessments of the U.S. Mexico Canada Agreement (USMCA, or commonly called “NAFTA2.0”). Below is a summary of these associations’ comments:

First, both the U.S. textile industry and the U.S. apparel industry expressed overall support for USMCA, which is regarded as critical for maintaining the Western-Hemisphere textile and apparel supply chain.

National Council

of Textile Organizations (NCTO): “In an

overarching fashion, the new agreement is an improvement over the original

NAFTA in many areas.”… “The United States, Canada and Mexico have

built a vibrant and prosperous textile production chain over the 24 years

through NAFTA.”

U.S. Fashion

Industry Association (USFIA): “We reviewed the details of the USMCA, and we

were pleased to find much we can support in it.” “USMCA remains a trilateral agreement, and “does no harm”

to existing U.S.-Mexico-Canada supply chains.”

American Apparel and Footwear Association (AAFA): “…state our very strong support of the North American Free Trade Agreement (NAFTA). NAFTA serves as an important anchor for the U.S. textile, apparel, and footwear industry. Much of the textile manufacturing in the United States is tied directly to NAFTA through U.S. exports to NAFTA partners.”…” The USMCA appears to have largely met the goal of “do no harm”. We were pleased to see the USMCA retain this essential trilateral feature.”

Second, not surprisingly, the U.S. textile industry and U.S. fashion brands and apparel retailers hold divided views on the textile and apparel specific rules of origin provision in USMCA—particularly the tariff preference level (TPL). In general, the U.S. textile industry welcomes the changes that limit the usage of-USMCA originating textile inputs, whereas U.S. fashion brands and retailers ask for more flexibilities. Further, even though the agreement seems to be a balanced deal, both the two sides expressed “dissatisfactions” for what they did not get.

Regarding the yarn-forward

rules of origin

NCTO: “We are

pleased that the basic textile origin rules adopted originally in NAFTA were essentially reaffirmed in USMCA. Commend

the creation of a separate textile chapter, which recognized the sensitivities

associated with trade in this sector and allows for unique provisions.”

USFIA: “The

yarn-forward rule of origin already discourages trade in our sector—and some

companies have told us that they don’t claim the duty savings on eligible

products from the region because the compliance requirements are simply too

onerous and expensive.”

Regarding the

tariff preference level (TPL)

NCTO: “While USMCA did reduce the size of some specific TPLs,

the reductions will not cut into existing trade levels. This outcome is

frustrating given the President’s stated goals of increasing benefits for U.S.

manufacturers and eliminating provisions that have helped non-signatory

countries, such as China, taking advantage of tariff preferences intended for

North American producers.”

USFIA: “The

agreement maintains the Tariff Preference Levels (TPLs) for apparel to and from

all three countries. This is one of the

most important elements of the agreement for our industry, and according to

some of our members, the only way they can source textiles and apparel with

these trading partners.”… “We also applaud the elimination of the requirement

that visible linings for tailored clothing come from the NAFTA region. The

maintenance of the TPLs and the elimination of the visible linings

requirement–will help companies continue and expand business with our trading

partners Canada and Mexico.”

AAFA: “we

are discouraged that… the changes made to the rules of origin were to introduce

more restrictive approaches. For example, many tariff preference levels (TPLs) were

lowered…”

“As we argued throughout the talks, the best way to encourage more U.S. content is to weave in more flexibility into the rules. Such flexibilities provide additional opportunities for business to be conducted under the agreement. For example, the USMCA dramatically increases the TPLs that will enable more U.S. apparel and made up goods to be exported to Canada. Even though such articles don’t have to be made with U.S. textiles, the mere presence of their production in the U.S. will mean more customers for U.S. textile firms.”

Sewing thread, pocketing,

narrow elastics and coated fabrics requirements

NCTO: ”We are

very supportive of revisions that will require the use of USMCA-origin sewing

thread, pocketing, narrow elastics and coated fabrics in certain end

items—which will offer a boost for U.S. producers formerly left out of the

origin rules in the original NAFTA ($250 million annual demand for sewing

thread and $70 million for pocketing in the USMCA market).”

USFIA: “the

USMCA creates new technical requirements –for example, the addition of requirements

for originating sewing thread, pocketing and narrow elastic bands—which will

result in higher costs for inputs and higher costs for brands and retailers (as

well as their suppliers in Mexico and Canada) to administer the agreement.”

“We are concerned that the addition of more regulatory

requirements to qualify for duty-free market access may hold back the ability

of some companies to expand their sourcing with Mexico and Canada.”…”There will

be some companies who shift operations out of the Western Hemisphere, or decide

not to move new orders to Canada or Mexico because of these cost increases. The

new regulations WILL make it more expensive and complicated for American brands

and retailers to use the agreement.”

AAFA: “we are

discouraged that – with few exceptions – the changes made to the rules of

origin were to introduce more restrictive approaches. For example, many tariff

preference levels (TPLs) were lowered and the USMCA now includes new requirements

that sewing thread, elastic strips, and pocketing originate. While we

understand U.S. negotiators were attempting to legislate more U.S. content into

North American textile and apparel supply chains, the result, unfortunately,

may be the opposite.”

Additionally, theU.S. textile industry is pleased with the changes to the government procurement provision, which closed a “loophole” regarding the Kissell Amendment.

NCTO: “We are also appreciative of a key change made in the

Government Procurement Chapter of USMCA regarding the Kissell Amendment, which

is a Buy American statute for textiles that applies to the Department of

Homeland Security (DHS). Kissell requires

100% U.S. content, with very limited exceptions, for purchases by the Coast

Guard and Transportation Security Administration (TSA).

Regarding TSA procurement, Kissell has a problematic loophole tied to NAFTA that has allowed Mexico to supply these contracts. As a result, under the terms of NAFTA, Mexico can supply TSA uniforms made from Mexican fiber, yarn, and/or fabric. The TSA Mexico loophole translates to a significant weakening of U.S. Buy American statutes. Noting that DHS spent $34million on clothing and textiles for TSA in FY2017, closing the Kissellloophole was a substantive change from NCTO’s perspective.”

[Note: Not like NAFTA, USMCAwill exclude FSC 83 (Textiles, Leather, Furs, Apparel, Shoe Findings, Tents, and flags) and FSC 84 (Clothing, Individual Equipment, and Insignia and Jewelry)from the procurement list of the Department of Homeland Security (DHS) that opens to Mexico and Canada.]

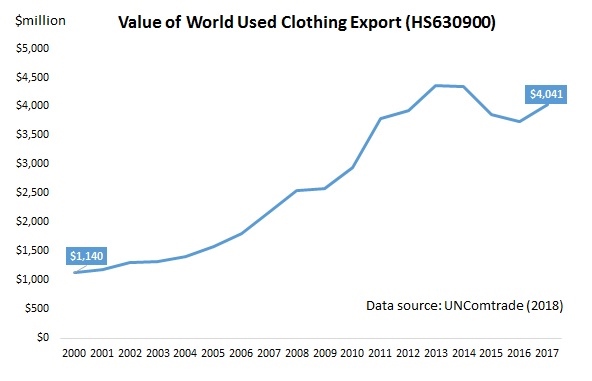

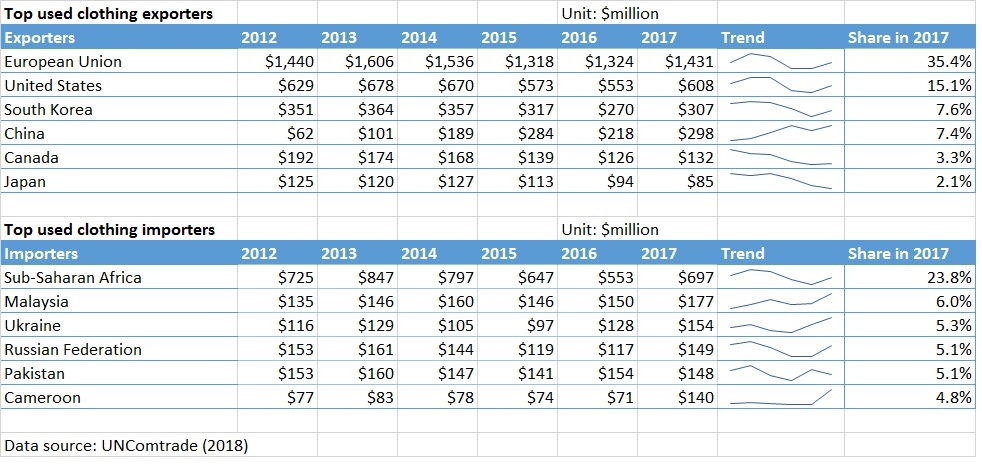

First, the world used

clothing trade has grown significantly over the past ten years. Statistics

from the United Nations show that the value of world used clothing trade (HS

code 630900) has quickly increased from $1.8bn in 2006 to $3.7bn in 2016, an

increase of 106 percent. Between 2006 and 2016, the value of world used

clothing trade enjoyed a 7.6 percent compound annual growth rate (CAGR), which

was almost double the pace of 3.4 percent CAGR for new clothing trade (HS

chapters 61 and 62) over the same period.

Second, the world

used clothing trade flow is highly unbalanced. On the one hand, the developed

economies are the dominant suppliers of used clothing to the world. In

2016, nearly 40 percent of the world’s used clothing exports came from three

countries alone: the United States (15 percent), the United Kingdom (13

percent) and Germany (11 percent). Data also shows that the European Union and

the United States together stably accounted for as much as 65 percent of the

value of world clothing exports between 2006 and 2016. The other country worth

mentioning is China, which is quickly becoming another leading used clothing

exporter in the world. In 2016, China’s used clothing exports totaled US$218m

from only US$0.32m in 2006, an increase of more than 684 percent!

On the other hand,

most of the world used clothing exports end up sold in the developing

countries, especially the least developed ones. For example, in 2016,

Sub-Saharan Africa (SSA) as a whole imported approximately 20 percent of the

world’s used clothing, far more than any other regions in the world. By value,

the top three individual importers of used clothing in 2016 are all developing

countries as well, namely Pakistan (6.0 percent), Malaysia (5.8 percent) and

Ukraine (4.9 percent).

Third, trade policies

regulating used clothing trade often raise controversies. While trade

barriers on new clothing attract much of the public attention, the used

clothing trade is facing even heavier and trickier restrictions of various

kinds. The World Trade Organization (WTO) data shows that in 2016 the average

applied tariff rate for used clothing imports was 19.3 percent, higher than

15.4 percent of new clothing (HS Chapters 61 and 62). Of the total 180

countries covered by the WTO tariff database, 115 (or 64 percent) set an equal

or higher tariff rate for used clothing than the new one. Further, it is not

rare to see extremely high import tariff rates and other quantitative

restrictions applied to used clothing trade. For example, in 2016 the applied

most-favored-nation (MFN) ad valorem equivalent tariff rate for used clothing

was as high as 356.9 percent in Uzbekistan, 167.3 percent in Zimbabwe, 149.2

percent in South Africa, 116.8 percent in Rwanda and 100 percent in Vietnam.

After all, because of

the complicated social, economic and political factors involved, how to

regulate and manage used clothing trade remains a key challenge facing the

world community.

First, Canada is one of the largest and fastest growing apparel import markets in the world. Data from the UN Comtrade show that the value of Canada’s apparel imports totaled $10.7bn in 2017, which ranked the fifth in the world, only after the European Union (EU), the United States, Japan, and Hong Kong.

Second, the Asian region as a whole is the dominant apparel supplier for Canada. Measured in value, as much as 80.9 percent of Canada’s apparel imports in 2017 came from Asia. Specifically, China (40.6 percent), Bangladesh (11.1 percent), Cambodia (8.1 percent) and Vietnam (7.7 percent) were the top individual supplier for Canada in 2017, and all of them are located in Asia. Meanwhile, Canadian apparel companies are gradually diversifying their sourcing base: the Herfindahl Index (HHI), a commonly adopted measure of market concentration, declined from 0.3 in 2010 to 0.19 in 2017.

Third, the NAFTA-region remains an important apparel-sourcing base for Canada, but its overall influence is in decline. Measured in value, the United States and Mexico were the 6th and 9th top apparel supplier for Canada in 2017 respectively. However, facing the competition from Asia, the United States and Mexico combined accounted for only 6.4 percent of Canada’s apparel imports in 2017, a significant drop from 9.8 percent back in 2007.

Fourth, free trade agreements and trade preference programs provide duty-saving opportunities for apparel sourcing in Canada. In 2017, Canada applied an average tariff rate of 17.1 percent on imports of knitted apparel (HS Chapter 61) and 15.9 percent on woven apparel (HS chapter 62). As of August 2018, Canada has 17 free trade agreements (FTAs) and trade preference programs (TPAs) in force, offering preferential or duty-free market access to Canada. Traditionally, a substantial portion of Canada’s FTA partners come from the Western Hemisphere, such as Chile, Costa Rica, Colombia, Peru, Honduras, and Panama. However, in recent years, Canada has been actively negotiating and reaching new FTAs with countries in Asia (such as South Korea, India, and Japan) and Europe (including the European Union and Ukraine).

Compared with the United States, in general, Canada adopts more liberal rules of origin (RoO) for apparel products. Quite a few Canada FTAs allow companies to source yarns or even fabrics from anywhere in the world – with the finished products still enjoying duty-free treatment when exported to Canada.

Following the steps of many countries in history, China is gradually shifting its role in the world textile and apparel supply chain. While China unshakably remains the world’s largest apparel exporter, its market shares measured by value fell from 38.6 percent in 2015 to 33.7 percent in 2017. China’s market shares in the world’s top three largest apparel import markets, namely the United States, EU, and Japan, also indicate a clear downward trend in the past five years. This result is consistent with several recent survey studies, which find that fashion brands and retailers are actively seeking alternative apparel sourcing bases to China. Indeed, no country, including China, can forever keep its comparative advantage in making labor-intensive garments when its economy becomes more industrialized and advanced.

However, it is also important to recognize that China is playing an increasingly important role as a textile supplier for apparel-exporting countries in Asia. For example, measured by value, 47 percent of Bangladesh’s textile imports came from China in 2017, up from 39 percent in 2005. We observe similar trends in Cambodia (up from 30 percent to 65 percent), Vietnam (up from 23 percent to 50 percent), Pakistan (up from 32 percent to 71 percent), Malaysia (up from 25 percent to 54 percent), Indonesia (up from 28 percent to 46 percent), Philippines (up from 19 percent to 41 percent) and Sri Lanka (up from 15 percent to 39 percent) over the same time frame.

So maybe the right question to ask in the future is: how much value of “Made in China” actually contains in Asian countries’ apparel exports to the world?

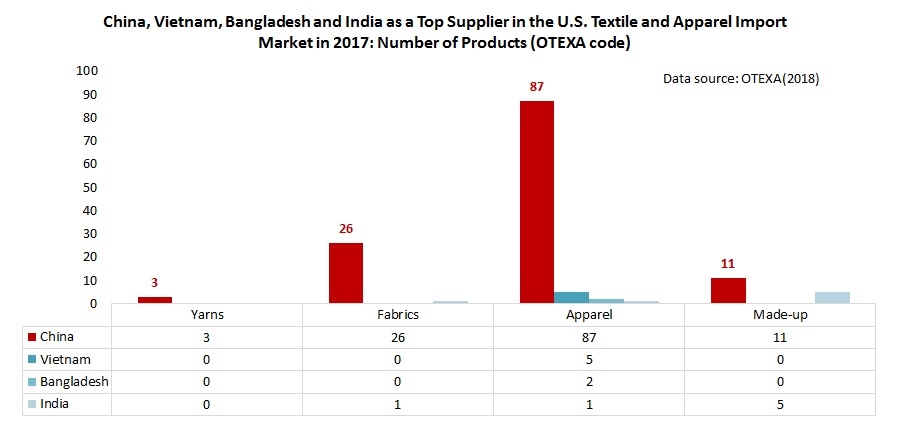

A fact-checking review of trade statistics in 2017 of a total 167 categories of textile and apparel (T&A) products categorized by the Office of Textiles and Apparel (OTEXA) suggests that T&A products “Made in China” still have no near competitors in the U.S. import market. Specifically, in 2017:

Of the total 11 categories of yarn, China was the top supplier for 3 categories (or 27.3%);

Of the total 34 categories of fabric, China was the top supplier for 26 categories (or 76.5%);

Of the total 106 categories of apparel, China was the top supplier for 87 categories (or 82.1%);

Of the total 16 categories of made-up textiles, China was the top supplier for 11 categories (or 68.8%);

In comparison, for those Asian T&A suppliers regarded as China’s top competitors:

Vietnam was the top supplier for only 5 categories of apparel (less than 5% of the total);

Bangladesh was the top supplier for only 2 categories of apparel (less than 2% of the total)

India was the top supplier for 1 category of fabric (2.9% of the total), 1 category of apparel (1% of the total) and 5 categories of made-up textiles (41.7% of the total)

Notably, China not only was the top supplier for many T&A products but also held a lion’s market shares. For example, in 2017:

For the 26 categories of fabric that China was the top supplier, China’s average market shares reached 40.5%, 22 percentage points higher than the 2nd top suppliers for these categories

For the 87 categories of apparel that China was the top supplier, China’s average market shares reached 52.4%, 36 percentage points higher than the 2nd top suppliers for these categories.

For the 11 categories of made-up textiles that China was the top supplier, China’s average market shares reached 58%, 43 percentage points higher than the 2nd top suppliers for these categories.

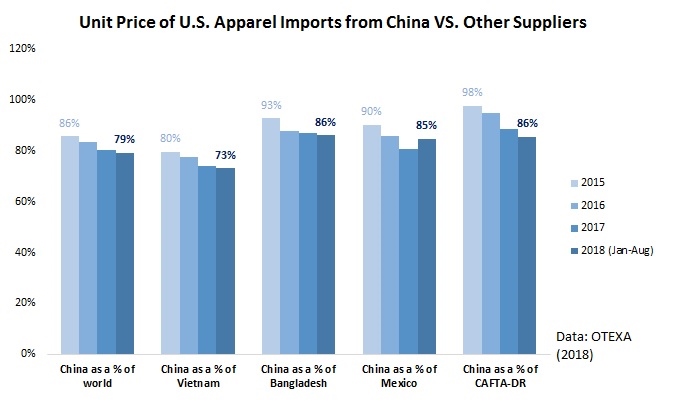

Furthermore, T&A “Made in China” are demonstrating even bigger price competitiveness compared to other suppliers in the U.S. market. For example, in 2017, the unit price of apparel “Made China” was only 74% of the price of “Made in Vietnam” (in 2015 was 80%), 86% of “Made in Bangladesh” (in 2015 was 93%), 85% of “Made in Mexico” (in 2015 was 90%) and 86% of products by members of CAFTA-DR (in 2012 was 98%).

Last but not least, the U.S.-China tariff war apparently has NOT affected China’s textile and apparel exports to the United States significantly. From January to August this year, China’s apparel exports to the U.S. declined by 1% in value and 0.3% in quantity from a year earlier, but China’s textile exports to the U.S. increased by 12.3% in value and 7.2% in quantity. China’s market shares in the U.S. market also remains overall stable.

Are the results surprising? How to explain China’s increasing price competitiveness despite its reported rising labor cost? What’s your outlook for the future of China as a sourcing destination for U.S. fashion brands and retailers? Please feel free to share your views.

First, in general, USMCA still adopts the so-called “yarn-forward” rules of origin. This means that fibers may be produced anywhere, but each component starting with the yarn used to make the garments must be formed within the free trade area – that is, by USMCA members.

Second, other than the source of yarns and fabrics, USMCA now requires that some specific parts of an apparel item (such as pocket bag fabric) need to use inputs made in the USMCA region so that the finished apparel item can qualify for the import duty-free treatment.

Third, USMCA allows a relatively more generous De minimis than NAFTA 1.0.

1) Compared with NAFTA, USMCA will cut the TPL level, but only to those product categories with a low TPL utilization rate;

2) Compared with NAFTA, USMCA will expand the TPL level for a few product categories with a high TPL utilization rate.

Fifth, USMCA will make no change to the Commercial availability/short supply list mechanism in NAFTA 1.0.

Sixth, it remains to be seen whether USMCA will boost Made-in-the-USA fibers, yarns and fabrics by limiting the use of non-USMCA textile inputs. For example, while the new agreement expands the TPL level for U.S. cotton/man-made fiber apparel exports to Canada (currently with a 100 percent utilization rate), these apparel products are NOT required to use U.S.-made yarns and fabrics. The utilization rate of USMCA will also be important to watch in the future.

About USMCA

On 30 September 2018, The United States reached an agreement with Canada, alongside Mexico on the updated North American Free Trade Agreement (NAFTA), now called the United States-Mexico-Canada Agreement (USMCA).

Before taking into effect, USMCA still needs to be ratified by all member countries. In the United States, the earliest that President Trump can sign the agreement will be 11/29/2018 (i.e., 90 days after notifying the Congress). The U.S. International Trade Commission has until 3/14/2019 (i.e., 150 days after President signing the agreement) to release an assessment of the new trade agreement. Afterward, the Trump Administration will need to work with the Congress to develop legislation to approve and implement the agreement.

A recent study released by the U.S. International Trade Commission (USITC) provides a comprehensive review and valuable insights into the state of textile and apparel manufacturing in the United States. According to the study:

First, data suggests a mixed picture of the recovery of textile manufacturing in the U.S.

Total capital expenditures in plants and equipment for the textile sector increased by 36 percent in the 2013–16 period. Interesting enough, much of the new investment is by foreign firms, including new investments by Chinese and Indian firms, as well as by firms from Mexico, Canada, Turkey, and Saudi Arabia.

U.S. textile shipments increased in 2017 to $39.6 billion, but remained 3 percent below the 2013 level. The result suggests that rather than simply increasing capacity, some of the new investment is likely replacing existing equipment, as firms upgrade and modernize their manufacturing processes and/or focus their operations on different products. [Note: shipments measure the dollar value of products sold by manufacturing establishments and are based on net selling values, f.o.b. (free on board) plant, after discounts and allowances are excluded]

At $10.6 billion, U.S. textile exports in 2017 were also below the five-year high of $12.1 billion in 2014.

Employment in the textiles sector declined by 4 percent from 131,000 in 2013 to an estimated 126,000 in 2017. Meanwhile, official data on labor productivity index for yarns and fabrics show steady declines during 2013–16.

Second, some evidence suggests that reshoring has taken place in recent years in the apparel sector, although on a modest scale.

For the 2013–16 period, capital expenditures were up 5 percent to $301 million, suggesting capital investment in the apparel sector may be increasing, as the industry begins to adopt more labor-saving technologies.

Domestic shipments of apparel showed modest increases in the past two years, reaching $12.0 billion in 2016 and $12.5 billion in 2017, after a record low of $11.5 billion in 2014 and 2015.

Employment in the apparel sector steadily declined during 2013–17, down 21 percent from 145,000 workers in 2013 to 120,000 workers in 2017. Official data on labor productivity also showed steady declines during 2013–16.

U.S. fashion companies continue to source apparel from the United States, although in a relatively small amount.

Third, the advantages of making textiles and apparel in the United States include:

Advantages of producing textiles in the United States include local and state incentives for investment, and the benefits afforded by free trade agreement (FTA) preferences (i.e., the “yarn-forward” rules of origin) that encourage the use of U.S.-produced inputs in downstream production in FTA partner countries, energy cost and the availability and reliability of high-quality cotton. Meanwhile, product innovation and automation are important aspects of the U.S. textile sector’s competitiveness strategy.

Advantages of producing apparel in the United States include improved lead times, better quality control, and more flexible production. Many domestically made products also use “Made in USA” branding to capitalize on the buy-American trend and the appeal of “Made in USA.” The adoption of various automation and digital technologies to accelerate the process of product development, improve the fit of the final product and reduce the needs for skilled sewing operators may also help improve the competitiveness.

The $200 billion imports from China targeted include 5,745 full or partial lines of the original 6,031 tariff lines that were on a proposed list of Chinese imports announced on July 10, 2018. Included among the products removed from the original proposed list are certain consumer electronics products such as smart watches and Bluetooth devices; certain chemical inputs for manufactured goods, textiles and agriculture; certain health and safety products such as bicycle helmets, and child safety furniture such as car seats and playpens.

Below are the textile and apparel related products removed from the original proposed list:

However, the final $200 billion product list still covers several textile and apparel-related products such as backpacks, handbags, purses, wallets, baseball gloves, hats and leather, and fur apparel, as well as textiles and machinery that are used for domestic manufacturing. In general, the final $200 billion product list includes about 20% consumer products (v.s. only 1% in the $50 billion already subject to the 25% additional tariff), 50% intermediary goods and 30% capital goods.

Why does the U.S. textile industry call for additional tariffs on textile and apparel imports from China whereas U.S. fashion brands and apparel retailers oppose the tariffs?

Based on the trade theories we have learned so far, why or why not would you recommend President Trump to impose 25% punitive tariffs on imports from China?

Appendix: Comments on the Proposed Section 301 Tariffs on Imports from China (August 2018)

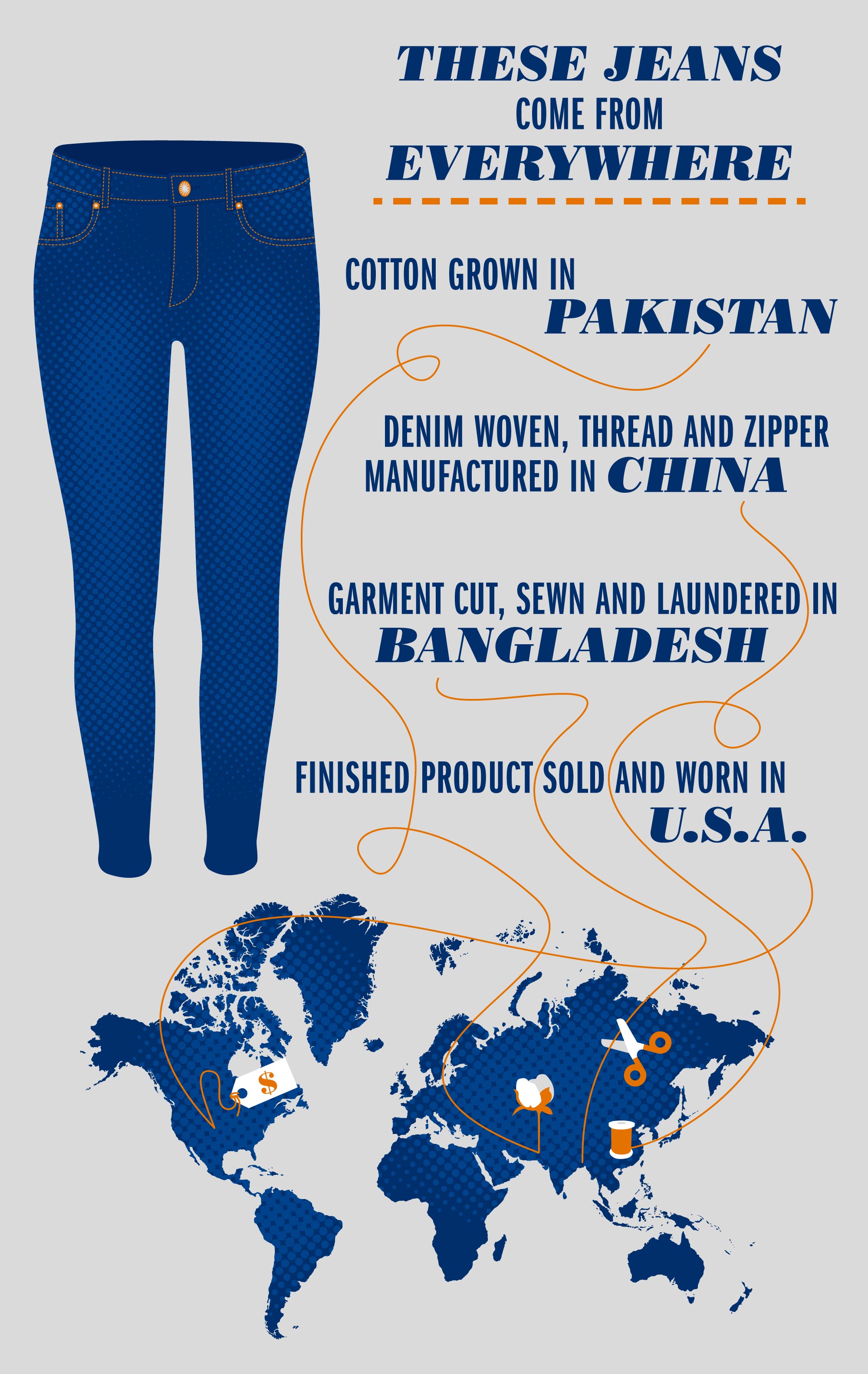

While shopping in SoHo (NYC), Nicole Farese, a student from FASH455, found the label of a Splendid sweater reads “Made of Italian Yarn” and “Made in China”. Splendid is a casual wear store which is known for their high-quality clothing sold at a premium price.

Exercise: Check your wardrobe and can you find any clothing that is also made through a “global supply chain?” Please feel free to submit your picture with a brief description of your item to shenglu@udel.edu.

The Bureau of Industry and Security (BIS) under the U.S. Department of Commerce recently released its assessment report of the U.S. textile and apparel (T&A) manufacturing sector. The report was based on a survey of 571 U.S. T&A manufacturers in summer 2017. These respondents include 230 textile mills (NAICS 313), 128 textile product mills (NAICS 314), and 213 apparel manufacturers (NAICS 315).

Below are the key findings of the study:

The state of the U.S. textile and apparel (T&A) manufacturing sector

U.S. T&A manufacturing has shrunk significantly: the value of T&A shipments (seasonally adjusted) in 2016 ($68 billion) was almost 56% decrease in real terms since 1995 ($153 billion).

U.S. T&A manufacturing has undergone substantial structural change: textiles and textile products accounted for 82% of the total shipments of the U.S. T&A industry as of 2016, compared to 57% in 1995. Notably, only 18% of shipments came from apparel manufacturing in 2016, compared to 43% in 1995.

U.S. T&A manufacturing sector is hiring less: Between 1990 and 2016, total employment decreased by 79%, from 1.7 million to 352,000 workers; over the same period, over 86% of apparel manufacturing jobs disappeared.

U.S. T&A manufacturers are making more capital investments: The overall total Capital Expenditures (CAPEX) of the 571 respondents increased 90 percent from 2012 to 2016 (from $1.6 billion to $3.1 billion). Particularly, the CAPEX of textile mills grew by 80 percent over that period—mostly on “Machinery, Equipment, and Vehicles.”

North Carolina hosted the largest number of U.S. T&A facilities (22 percent of the respondents), followed by Georgia (10 percent), and South Carolina (9 percent).

China, Mexico, and Canada are the most popular destinations for foreign investments by U.S. T&A manufacturers.

Competition landscape and factors

Respondents listed a total of 1,309 U.S. competitors and 552 non-U.S. competitors. Chinese companies were cited as the number one source of foreign competition.

“Quality,” “Lead Time,” and “Innovation” were the top three competitive advantages of U.S. T&A manufacturers as they related to foreign competition. “Labor Costs” was regarded as the top disadvantage of U.S. T&A manufacturing.

43 percent of respondents believed that reshoring was occurring in U.S. T&A manufacturing. Almost all of these respondents believed that “Shorter Lead Times” and the “Marketability of the ‘Made in USA’ Label” were the factors driving the trend.

The Affordable Care Act (ACA), Minimum Wage regulations (Federal, State, and Local), and U.S. Trade Policy were the top governmental regulations and provisions cited as negatively impacting the competitiveness of U.S. T&A manufacturers.

61 percent of respondents reported that they had difficulties hiring and/or retaining employees for their T&A operations, specifically production line workers such as operators and machine technicians. The skill gaps in the labor market for those positions were by far the biggest ones identified for the industry.

43 percent of respondents believed that reshoring was occurring in T&A manufacturing (i.e., the practice of transferring a business operation that was moved to a non-U.S. location back to the United States.) Textile manufacturers were more likely to be aware of reshoring.

Trade and U.S. textile and apparel manufacturing

On average, respondents say 48 percent of their textile and textile products are “100 percent made in the U.S.”, while for apparel it was around 54 percent.

U.S. T&A exports dropped 10 percent between 2012 and 2016, from $2.2 billion to $1.98 billion. On average, exports accounted for only 12 percent of respondents’ total sales.

33 percent of respondents considered themselves to be dependent on foreign sources for supplies, which was highest among textile mills.

37 percent of respondents reported that they considered themselves to be dependent on non-U.S. sourcing for their machinery or equipment.

Berry Amendment and U.S. textile and apparel manufacturing

For textile mills, an average of 12 percent of U.S. output was Berry Amendment-related; for textile product mills the average was 21 percent, and for apparel production, it averaged 26 percent. 67 percent of respondents believed that the Berry Amendment had a positive impact on their organization’s business.

The Office of U.S. Trade Representative (USTR) announced that the United States and Mexico have “reached a preliminary agreement in principle” to update the 24-year old North American Free Trade Agreement (NAFTA). According to USTR, compared with the existing NAFTA, the new deal will

strengthen the labor and environmental protection provisions

provide stronger and more effective protection and enforcement of intellectual property right protection

reduce various non-tariff barriers facing U.S. agriculture exports

include new rules of origin and origin procedures for autos (including requiring 75 percent of auto content be made in the United States and Mexico AND 40-45 percent of auto content be made by workers earning at least $16 per hour.)

include new chapters dealing with digital trade and textiles

include a 16-year “sunset period” with a review every six years, at which time the parties can renew the deal for another 16 years.

Specifically for the textile and apparel sector, USTR said that “The new provisions on textiles incentivize greater United States and Mexican production in textiles and apparel trade, strengthen customs enforcement, and facilitate broader consultation and cooperation among the Parties on issues related to textiles and apparel trade.” More specifically, the new textile chapter in renegotiated NAFTA will:

1) Promote greater use of Made-in-the-USA fibers, yarns, and fabrics by limiting rules that allow for some use of non-NAFTA inputs in textile and apparel trade; and requiring that sewing thread, pocketing fabric, narrow elastic bands, and coated fabric, when incorporated in apparel and other finished products, be made in the region for those finished products to qualify for trade benefits. “

2) Include textile-specific verification and customs cooperation provisions that provide new tools for strengthening customs enforcement and preventing fraud and circumvention.

Based on USTR’s statement, it is likely, although not confirmed, that the US-Mexico deal will allow more limited tariff preference level (TPL) than the existing NAFTA.

USTR’s statement also said that the new deal would be subject to “finalization and implementation,” and its relationship with NAFTA remain unclear. The statement did not mention anything about Canada, another NAFTA member, either. Interesting enough, when announcing the US-Mexico deal in front of the press, President Trump said “I will terminate the existing deal (NAFTA). When that happens, I can’t quite tell you; it depends on what the timetable is with Congress. But I’ll be terminating the existing deal and going into this deal. We’ll start negotiating with Canada relatively soon.”

In a statement released on the same day, the American Apparel and Footwear Association (AAFA) said it welcomed the conclusion of bilateral talks with Mexico on NAFTA and emphasized the need for Canada to be a part of any final agreement: “The conclusion of talks between the U.S. and Mexico is a positive step in the NAFTA negotiations, however, it is essential that the updated agreement remain trilateral. At the same time, we encourage the administration to share the details of the agreement so the business community can inspect the impact on North American supply chains and share feedback with the administration and Congress…Any update to the agreement must continue to support these American jobs, promote trade linkages, and be seamlessly implemented to be considered a success. It is with this in mind that we are deeply concerned to hear any mention of withdrawal or termination of the existing agreement at this late stage.”

According to Inside U.S. Trade, the National Council of Textile Organizations (NCTO)which represents the U.S. textile industry says it is “encouraged by the information released by USTR with respect to strengthening the rules of origin for textiles and apparel in the announced agreement with Mexico. U.S. talks with Canada are still ongoing, however, and NCTO will wait to review the text of any final agreement before issuing a more detailed statement on the negotiation outcome.”

According to the newly released World Trade Statistical Review 2018 by the World Trade Organization (WTO), the current dollar value of world textiles (SITC 65) and apparel (SITC 84) exports totaled $296.1bn and $454.5bn respectively in 2017, increased by 4.2% and 2.8% from a year earlier. This is the first time since 2015 that the value of world textile and apparel exports enjoyed a growth.

Textiles and apparel are not alone. Driven by rising demand for imports globally, the current dollar value of world merchandise exports also grew by 4.7% in 2017–its most robust growth in six years, to reach $17.43 trillion. Particularly, the ratio of trade growth to GDP growth finally returned to its historic average of 1.5, compared to the much lower 1.0 ratio recorded in the years following the 2008 financial crisis.

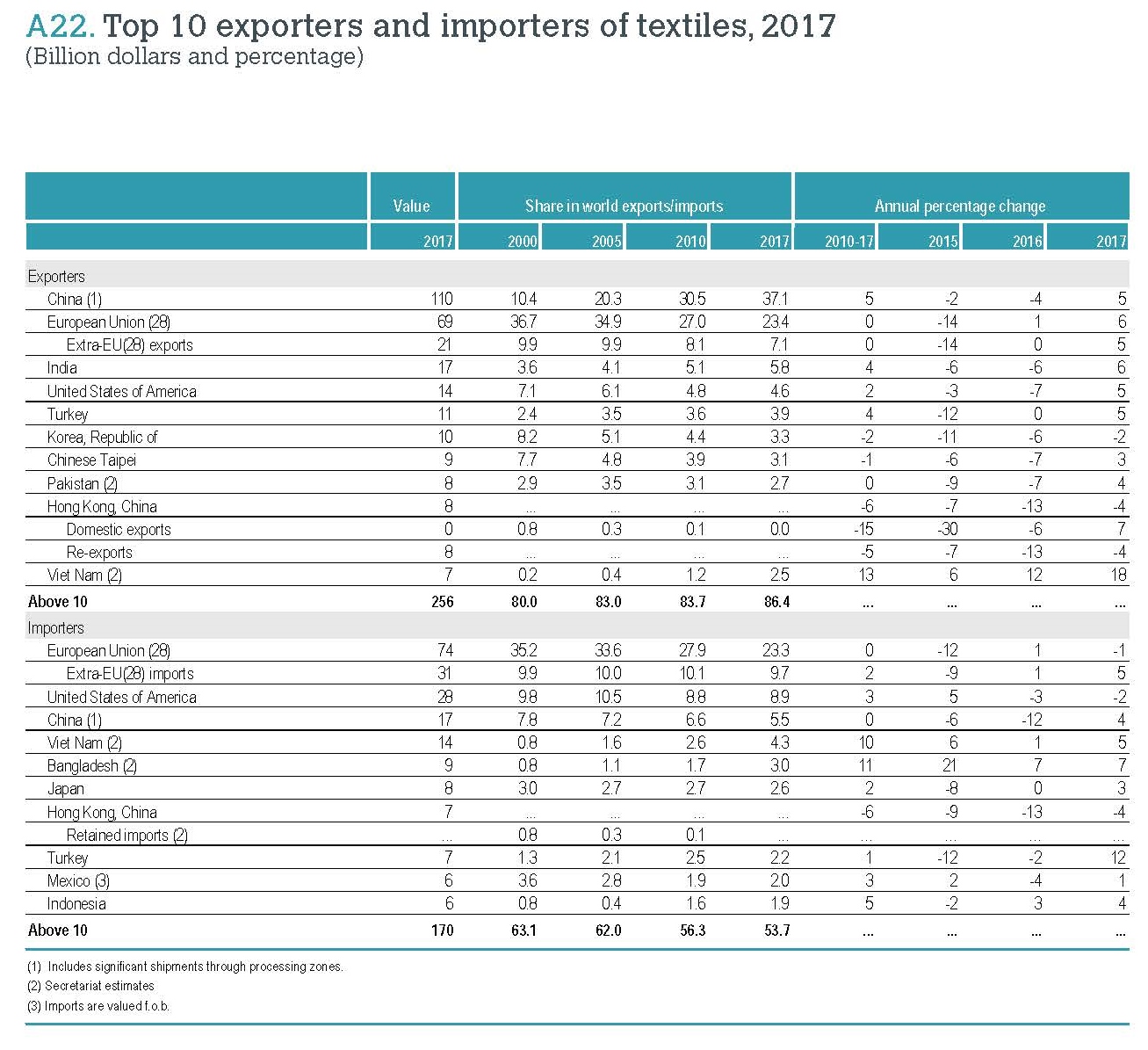

China, European Union (EU28), and India remained the world’s top three exporters of textiles in 2017. Altogether, these top three accounted for 66.3% of world textile exports in 2017, up from 65.9% in 2016. All the top three also enjoyed a faster-than-average export growth in 2017, including 5.0% of China, 5.8% of EU(28) and 5.9% of India. The United States remained the world’s fourth top textile exporter in 2017, accounting for 4.6 percent of the shares, the same as a year earlier.

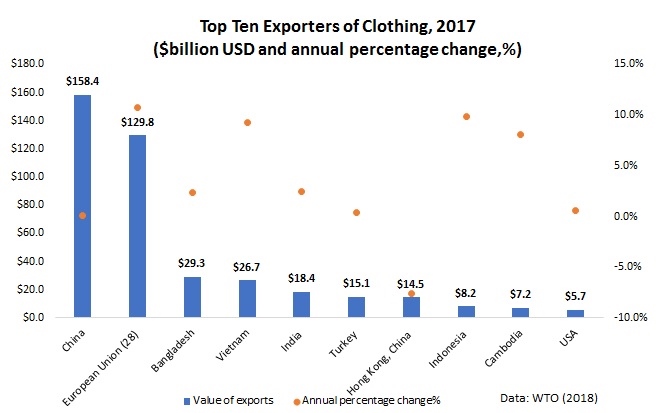

Regarding apparel, China, the European Union (EU28), Bangladesh and Vietnam unshakably remained the world’s top four largest exporters in 2017. Altogether, these top four accounted for as much as 75.8% of world market shares in 2017, which was higher than 74.3% a year earlier and a substantial increase from 68.3% back in 2007.

Continuing with the emerging trend in recent years, China is exporting less apparel and more textiles to the world. Notably, China’s market shares in world apparel exports fell from its peak—38.8% in 2014 to a record low of 34.9% in 2017. Meanwhile, China accounted for 37.1% of world textile exports in 2017, which was a new record high. It is important to recognize that China is playing an increasingly critical role as a textile supplier for many apparel-exporting countries in Asia.Measured by value, 47% of Bangladesh’s textile imports came from China in 2017, up from 39% in 2005. We observe similar trends in Cambodia (up from 30% to 65 %), Vietnam (up from 23 % to 50 %), Pakistan (up from 32 % to 71 %), Malaysia (up from 25 % to 54 %), Indonesia (up from 28 % to 46 %), Philippines (up from 19 % to 41 %) and Sri Lanka (up from 15 % to 39 %) over the same period.

Business challenges facing U.S. fashion companies: Protectionism is the top challenge for the U.S. fashion industry in 2018. More companies worry about increases in production or sourcing cost, too. For the second year in a row, “protectionist trade policy agenda in the United States” ranks the top challenge for U.S. fashion companies in 2018.

Industry outlook:Despite concerns about trade policy and cost, executives are more confident about the five-year outlook for the U.S. fashion industry in 2018 than they were a year ago, although confidence has not fully recovered to the level seen in 2015 and 2016. In addition, 100 percent of respondents say they plan to hire more employees in the next five years, compared with 80-85 percent in previous studies; market analysts, data scientists, sustainability/compliance related specialists or managers, and supply chain specialists are expected to be the most in-demand.

U.S. fashion companies’ sourcing strategy: When it comes to sourcing, diversification is key for many companies.

Most respondents continue to maintain a diverse sourcing base, with 60.7 percent currently sourcing from 10+ different countries or regions, up from 57.6 percent in 2017.

Larger companies, in general, continue to be more diversified than smaller companies.

Reflecting the U.S. fashion industry’s growing global reach, respondents report sourcing from as many as 51 countries or regions in 2018, the same as in 2017. Asia as a whole continues to take the lead as the dominant sourcing region. Meanwhile, with the growing importance of speed-to-market and flexibility, the Western Hemisphere is becoming an indispensable sourcing base.

Keeping a relatively diverse sourcing base will remain a key element of U.S. fashion companies’ sourcing strategy. Nearly 80 percent of respondents plan to source from the same number of countries, or more countries, in the next two years. However, respondents are equally divided on whether to increase or decrease the number of suppliers they will work with.

“China plus Vietnam plus Many” has become an ever more popular sourcing model among respondents. And this model is evolving as companies further diversify their China production. In particular, China now typically accounts for only 11-30 percent of companies’ total sourcing value or volume, compared with 30-50 percent in the past.

Although China’s position as the top sourcing destination is unshakable, companies are actively seeking alternatives to “Made in China.” This does not seem to be due to concerns about cost, but rather the worries about the escalating U.S.-China trade tensions.

Benefiting from the diversification away from China, Vietnam and Bangladesh are expected to play a bigger role as apparel suppliers for the U.S. market in the near future.

Rules of origin and the utilization of trade agreements for sourcing: Rules of origin, and exceptions to the rules of origin, significantly impact whether companies use free trade agreements (FTAs) and trade preference programs for sourcing.

While FTAs and trade preference programs remain largely underutilized by U.S. fashion companies, more companies are using NAFTA (65 percent), CAFTA-DR (58 percent) and AGOA (50 percent) than in the past two years.

Still, it’s concerning that companies often do not claim the duty-free benefits when sourcing from countries with FTAs or preference programs. Companies say this is primarily due to the strict rules of origin.

Exceptions to the “yarn-forward” rules of origin, including tariff preference levels (TPLs), commercial availability/short supply lists, and cumulation, are priorities for respondents; 48 percent say they currently use these mechanisms for sourcing. These exceptions provide critical flexibilities that make companies more likely to use FTAs and source from FTA regions.

NAFTA: U.S. fashion companies call for a further reduction of trade barriers and urge trade negotiators to “do no harm” to NAFTA, the most-utilized free trade agreement by respondents.

Respondents predominantly support initiatives to eliminate trade barriers of all kinds, from high tariffs to overcomplicated documentation requirements, to restrictive rules of origin in NAFTA and future free trade agreements.

More than half of respondents explicitly say NAFTA is important to their business—and they have grave concerns about the uncertain future of the agreement.

Sourcing in sustainable and socially compliant ways: Overall, U.S. fashion companies are making more commitments to sustainability and social responsibility.

85 percent of respondents plan to allocate more resources for sustainability and social compliance in the next two years, in areas including providing training to suppliers and internal employees, adding more employees, and working more closely with third-party certification programs on sustainability and social compliance. However, the availability of operational budget remains the primary hurdle for companies that want to do more.

100 percent of respondents map their supply chains (i.e., keep records of name, location, and function of suppliers), up from 90 percent in 2017. Over 80 percent of respondents track not only Tier 1 suppliers (i.e., factory where the final product is assembled), but also Tier 2 suppliers (i.e., subcontractors or major component suppliers, such as fabrics). However, it’s less common for companies to map Tier 3 (i.e., yarn spinners, finding and trimming suppliers) and Tier 4 suppliers (i.e., raw materials suppliers, such as cattle/pig hides, rubber, cotton, wool, goose down, minerals/metals and chemicals).

100 percent of respondents audit their suppliers for issues including building safety, fire safety, and treatment of workers. The vast majority of respondents (96 percent) currently use third-party certification programs to audit, with both announced and unannounced audits.

The US Fashion Industry Benchmarking Study from 2014 to 2017 can be downloaded from HERE