Presenter: Mikayla Dubreuil (MS 2020, Fashion and Apparel Studies)

Canada is one of the world’s top ten largest apparel consumption markets, with retail sales totaling USD$28.04bn in 2019 (Euromonitor, 2020). Similar to other developed nations, clothing sold in Canada is predominately imported, making Canada a significant market access opportunity for clothing manufacturers, wholesalers, fashion brands, and retailers around the world. Based on the latest market and trade data, this study intends to provide an in-depth analysis of the Canadian apparel sourcing patterns.

Key findings:

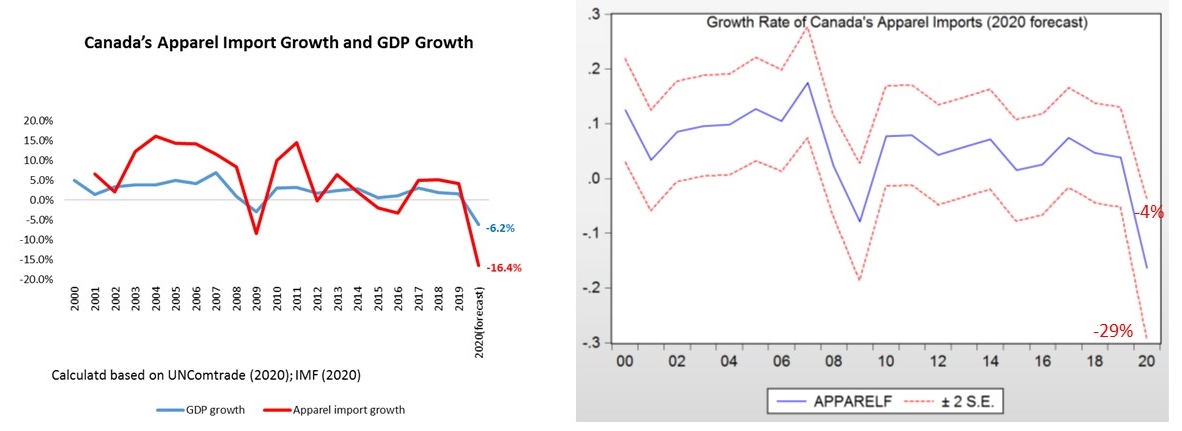

First, the volume of Canada’s apparel imports mirrors its economic growth. As the apparel business is buyer-driven, the performance of Canada’s national economy has a huge impact on its apparel imports. Canada’s GDP growth is an important predictor for its growth in apparel imports. When Canada’s national economy boomed, its apparel imports also enjoyed a proportional expansion thanks to consumers’ higher income and purchasing power. Such a strong correlation, however, also suggests a likely sharp decline in Canada’s apparel imports in 2020 due to its national economy took a hard hit by the Covid-19 pandemic. [Note: with a 6.2% drop in GDP growth as forecasted by IMF, Canada’s apparel imports in 2020 could decrease by 16.4% from 2019. At the 95% confidence level, the worst case in 2020 will be a 29% decline of apparel imports from a year earlier and the most optimistic case will be a 4% decline.]

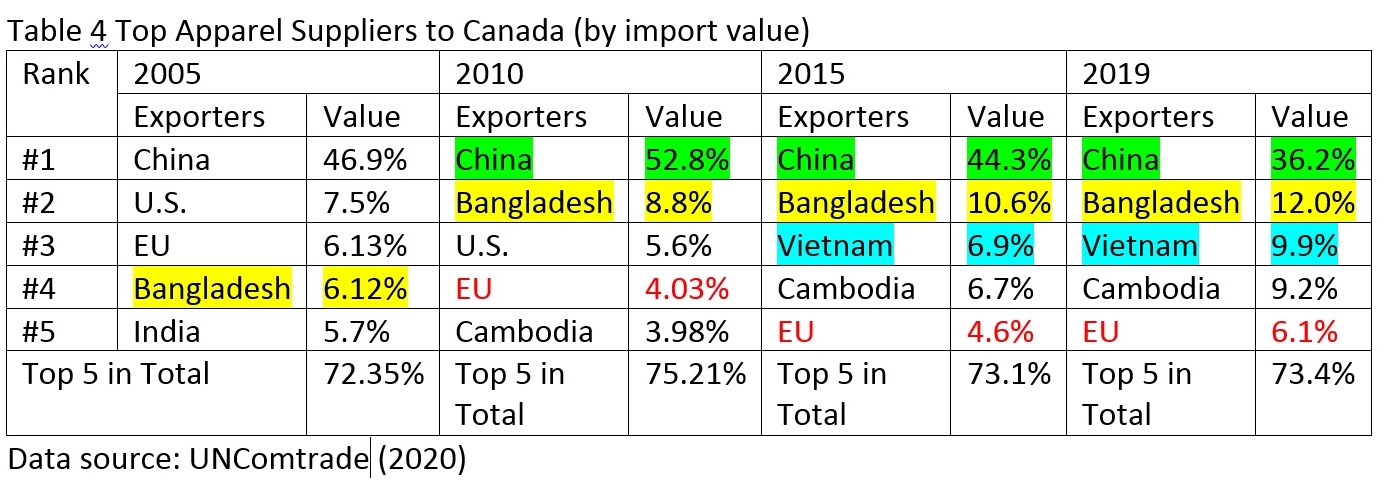

Second, although China remains the top apparel supplier for Canada, Canadian fashion companies are increasingly sourcing from South Asia. Three trends to note: 1) China’s market share in Canada has been declining steadily from its peak in the 2010s. 2) Meanwhile. Canada is moving more sourcing orders to other Asian countries, particularly Vietnam and Bangladesh. 3) Additionally, thanks to the EU-Canada Free Trade Agreement (CETA), which provisionally entered into force in 2017, Canada’s apparel imports from the European Union (EU) has been rising steadily. In 2019, EU members altogether accounted for 6% of Canada’s apparel imports, an increase from 4% in 2010. Around half of Canada’s apparel imports from the EU are made in Italy, whose high-end luxury apparel exports could be among the biggest beneficiaries of the duty-saving opportunities provided by CETA.

Third, near sourcing from the Americas remains an essential component of Canadian fashion companies’ sourcing portfolio; However, sourcing from the NAFTA regions is in decline. Approximately 9% of Canada’s apparel imports come from North, Central, and South Americas altogether, a pattern that has stayed relatively stable since 2010. As consumers in Canada are seeking “faster fashion”, Canadian fashion companies are attaching even greater importance to leveraging near sourcing from the Americas and improving their speed to market. For example, Lululemon placed around 8% of its sourcing orders with factories in the Americas in 2018, higher than 3%-5% five years ago.

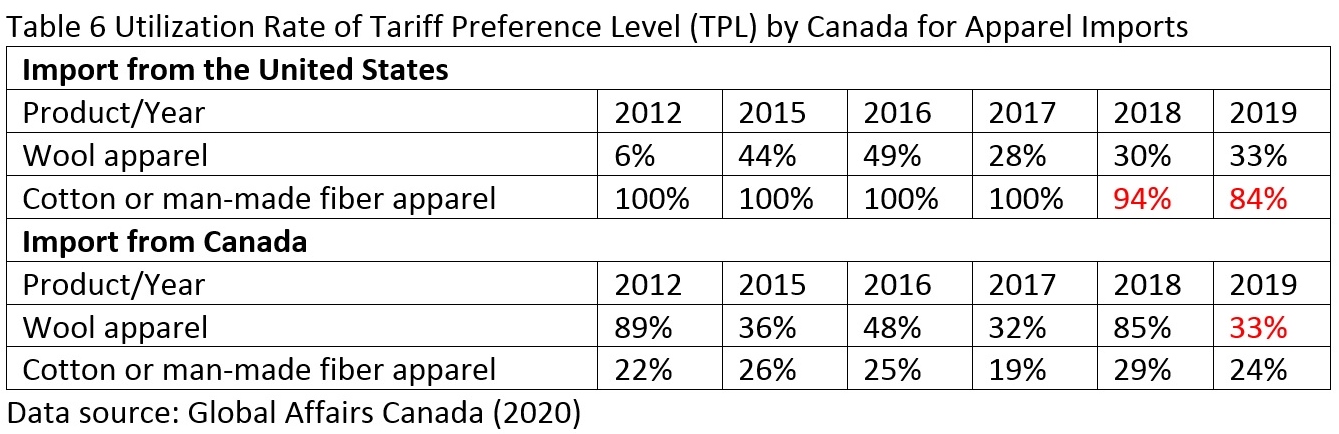

Canada’s apparel imports from members of the North American Free Trade Agreement (NAFTA), however, has suffered a notable drop from 12.3% back in 2005 to the record low of 5.4% in 2019. As President Trump repeatedly threatened to withdraw the United States from NAFTA since he took office in 2017, the mounting uncertainty had caused Canadian fashion companies to cut sourcing from the region. For years, many Canadian fashion companies have been actively using the tariff preference level (TPL) mechanism to import apparel from the NAFTA region, although only a limited amount of TPL quota is allowed each year. While the TPL utilization rate for Canada’s cotton and man-made fiber apparel imports from the United States always reached 100%, the utilization rate slipped to a record low of 84% in 2019.

The upcoming implementation of the U.S.-Mexico-Canada Free Trade Agreement (USMCA or NAFTA2.0) on July 1, 2020 could help create a more stable environment for Canadian fashion companies interested in sourcing from the United States and Mexico. However, as USMCA fails to add any significant flexibility to the NAFTA apparel-specific rules of origin, whether the new agreement will improve the attractiveness of sourcing from North America for Canadian fashion companies remains to be seen.

by Mikayla DuBreuil and Sheng Lu

Additional Reading: Mikayla DuBreuil and Sheng Lu (2020). Canada’s clothing market – Top selling and sourcing trends. Just-Style.