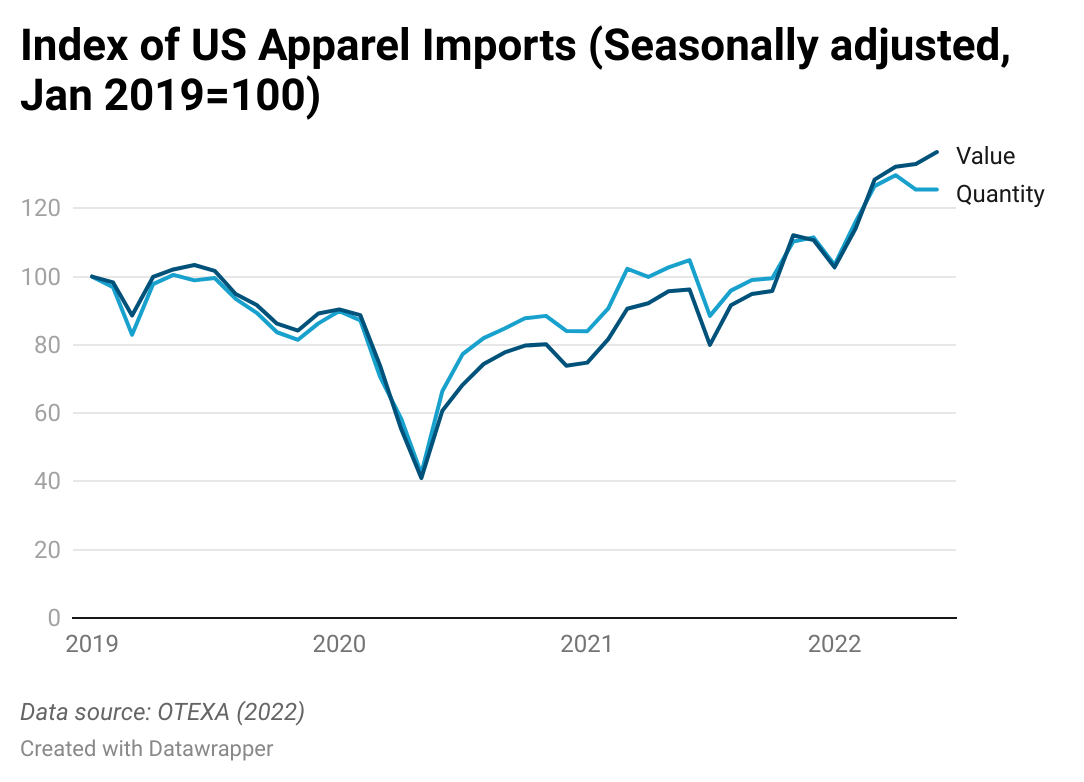

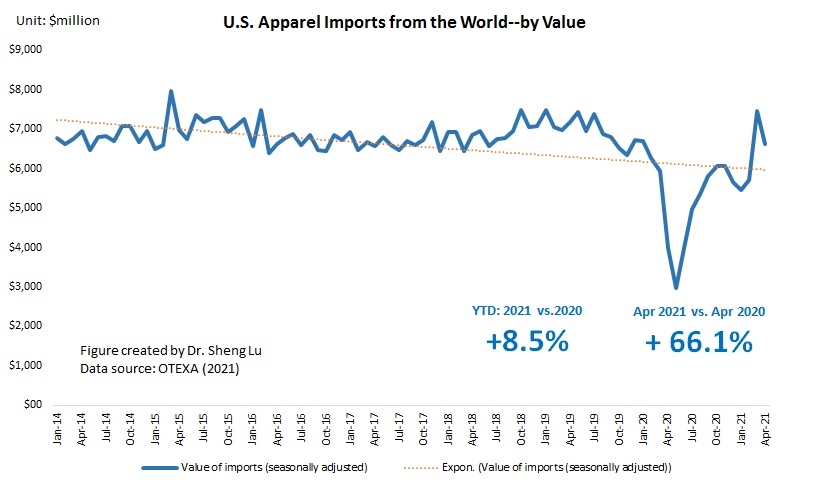

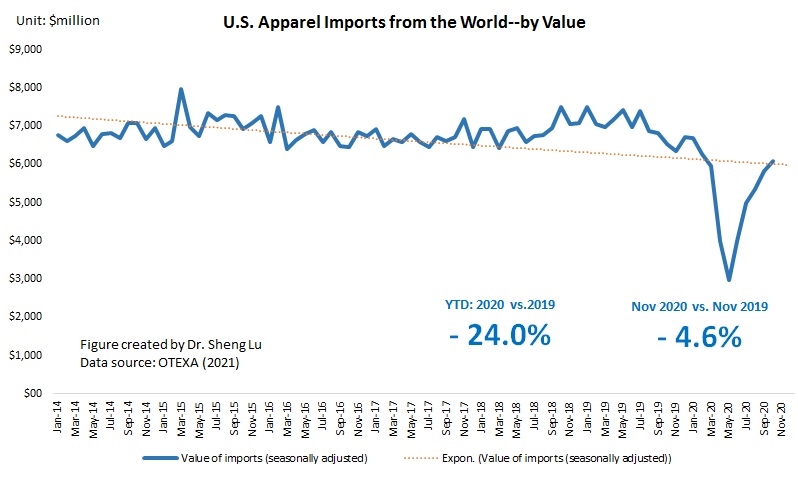

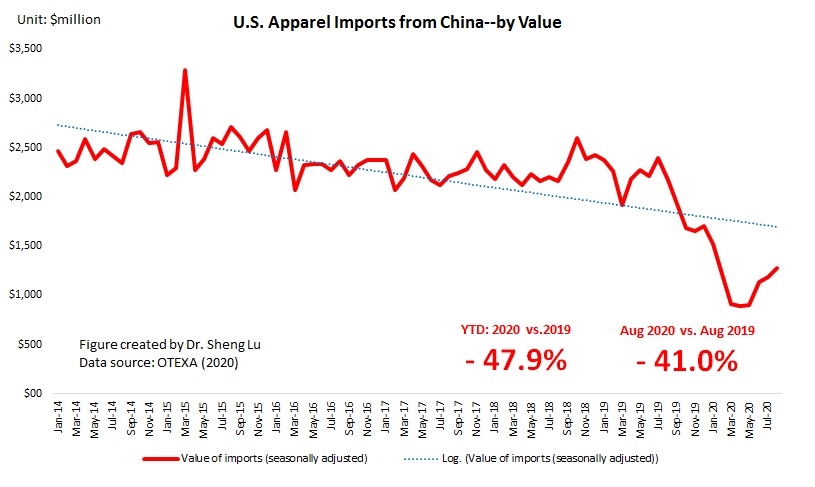

First, US apparel imports enjoyed a decent growth but started to face softening demand.

- Thanks to consumers’ spending, in the first half of 2022, US apparel imports went up 40% in value and 24% in quantity from a year ago.

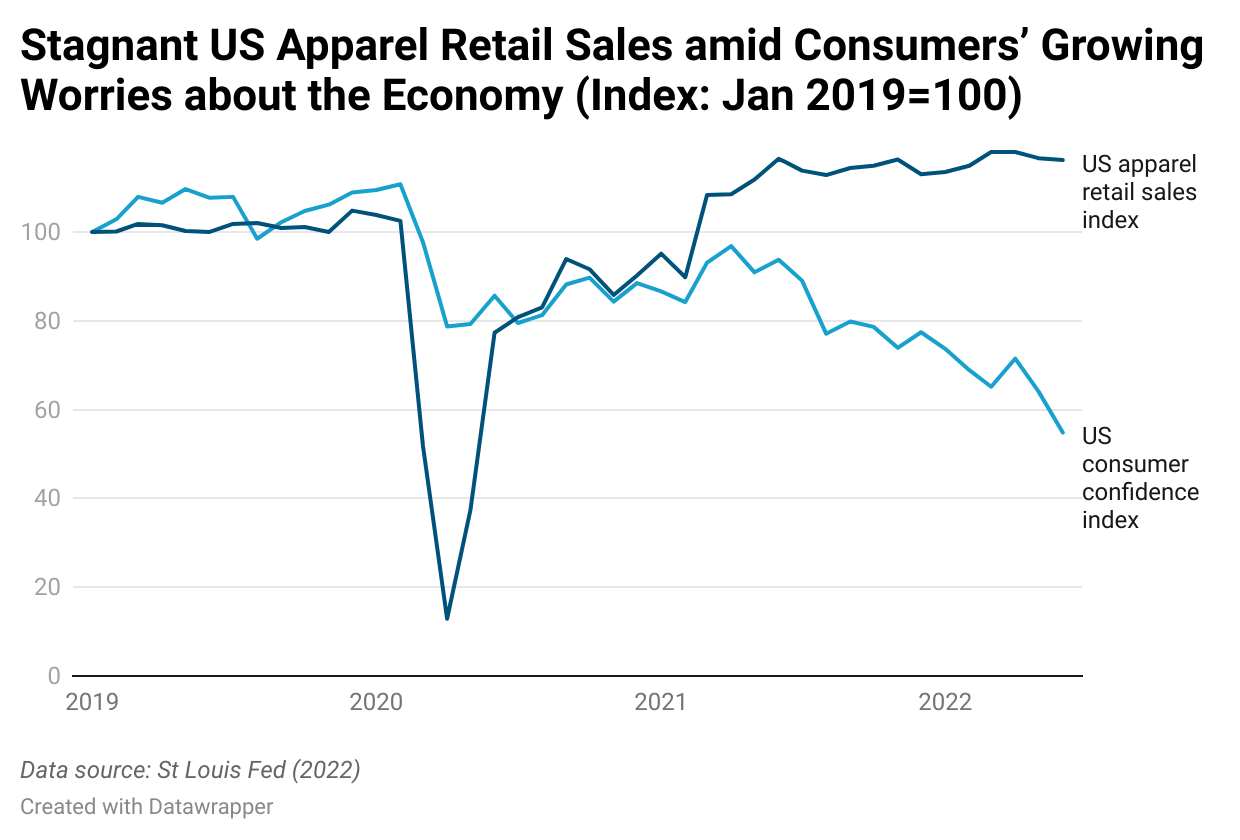

- However, due to US consumers’ weakening demand amid the economic downturn, the speed of import expansion is slowing down quickly. As an alert, the US consumer confidence index (CCI) fell to 54.8 in June 2022 (January 2019=100), the lowest since the pandemic. This result suggests that US consumers were increasingly worried about their household’s financial outlook and would hold back their discretionary clothing spending.

- The month-over-month growth of US apparel imports dropped to only 2.6% in value and nearly zero in quantity in June 2022 from over 10% at the beginning of the year.

- As the trajectory of the US economy remains highly uncertain in the medium term, we could expect many US fashion companies to turn more conservative about placing new sourcing orders in the second half of 2022 to control inventory and avoid overstock.

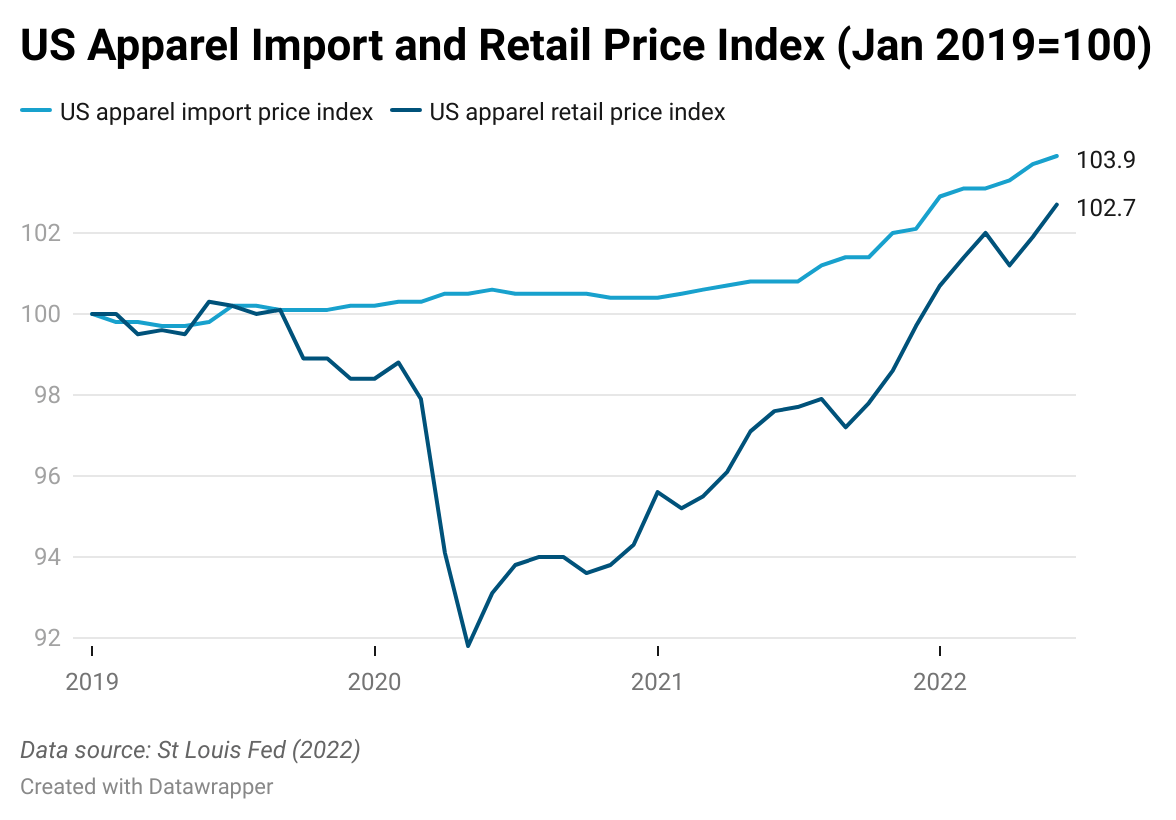

Second, fashion companies struggled with hiking apparel sourcing costs driven by multiple factors.

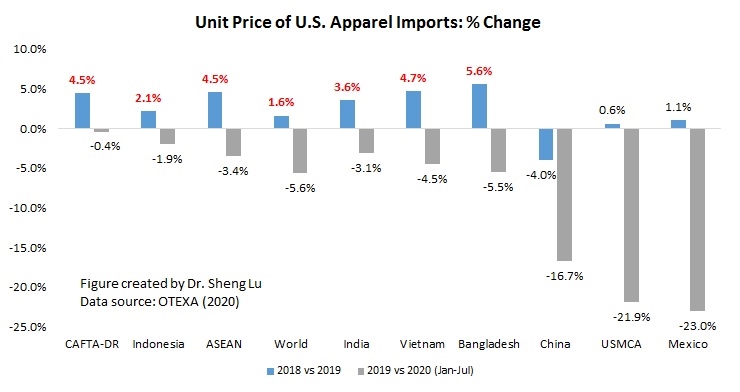

- The price index of US apparel imports reached 103.9 in June 2022 (January 2019=100), a 3.1% increase from a year ago and the highest since 2019. USITC data further shows that, of the over 200 types of apparel items (HS Chapters 61 and 62) at the six-digit code level, nearly 70% had a price increase in the first half of 2022 from a year ago, including almost 40% experiencing a price increase exceeding 10 percent.

- According to the 2022 Fashion Industry Benchmarking Study recently released by the US Fashion Industry Association (USFIA), 100 percent of respondents expect their sourcing costs to increase in 2022, including nearly 40 percent expecting a substantial cost increase from a year ago. Further, respondents say that almost everything has become more expensive this year, from textile raw materials, shipping, and labor to the costs associated with compliance with trade regulations.

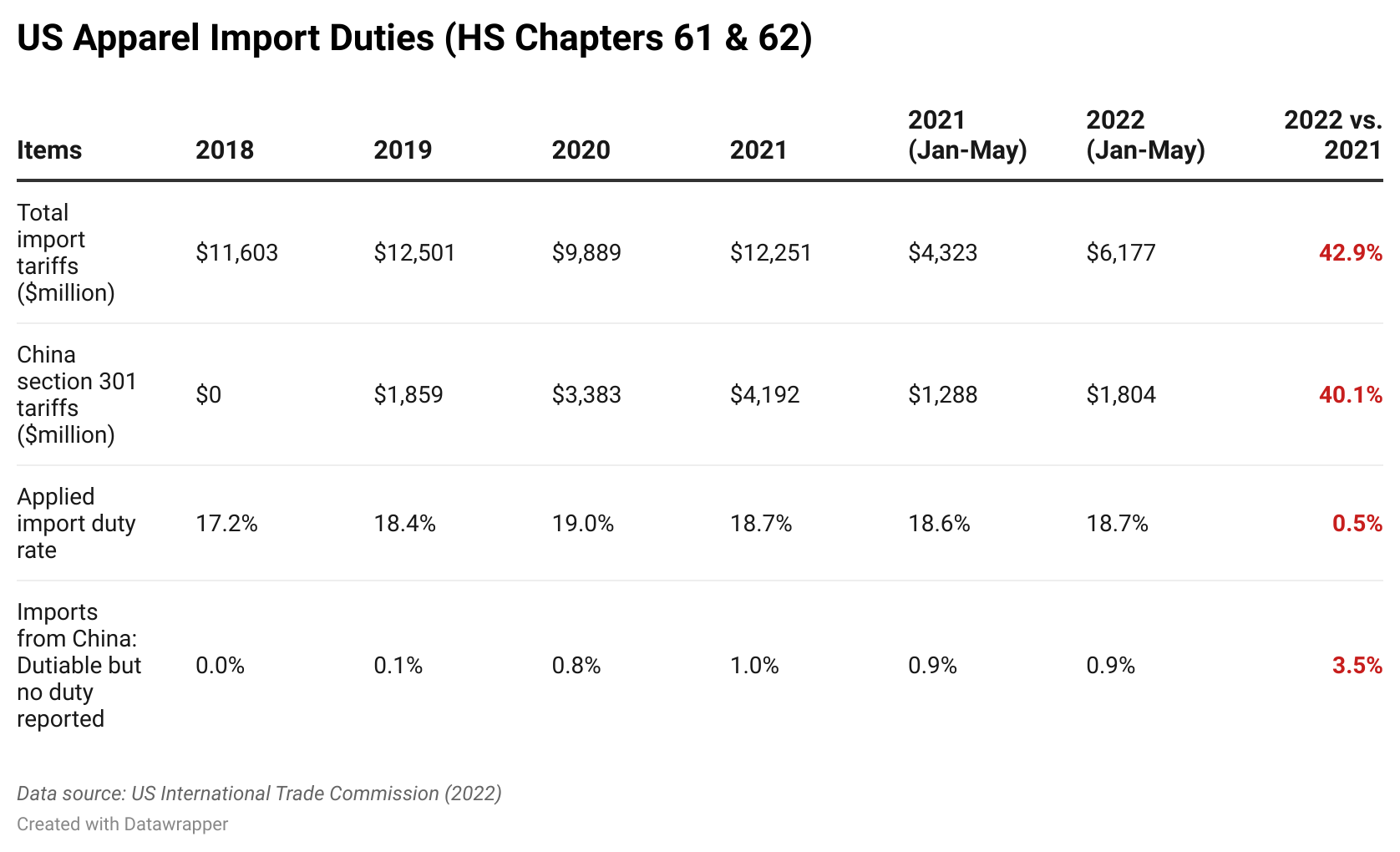

- To make the situation even worse, the more expensive “cost of goods” resulted in heavier burdens of ad valorem import duties for US fashion companies. USITC data shows that in the first five months of 2022, US companies paid $6,117 million in tariffs for apparel imports (HS Chapters 61 and 62), a significant increase of 42.9% from a year ago. Of these import duties paid by US companies, about 30% (or $1,804 million) resulted from the controversial US Section 301 action against Chinese imports. Because of the Section 301 tariff action, the average applied US tariff rate for apparel imports also increased from 17.2% in 2018 to 18.7% in the first half of 2022.

- Even though the US retail price index for clothing reached 102.7 in June 2022 (January 2019=100), the price increase was behind the import cost surge over the same period. In other words, given the intense market competition and weaker demand, US fashion companies couldn’t pass the sourcing cost increase to consumers entirely.

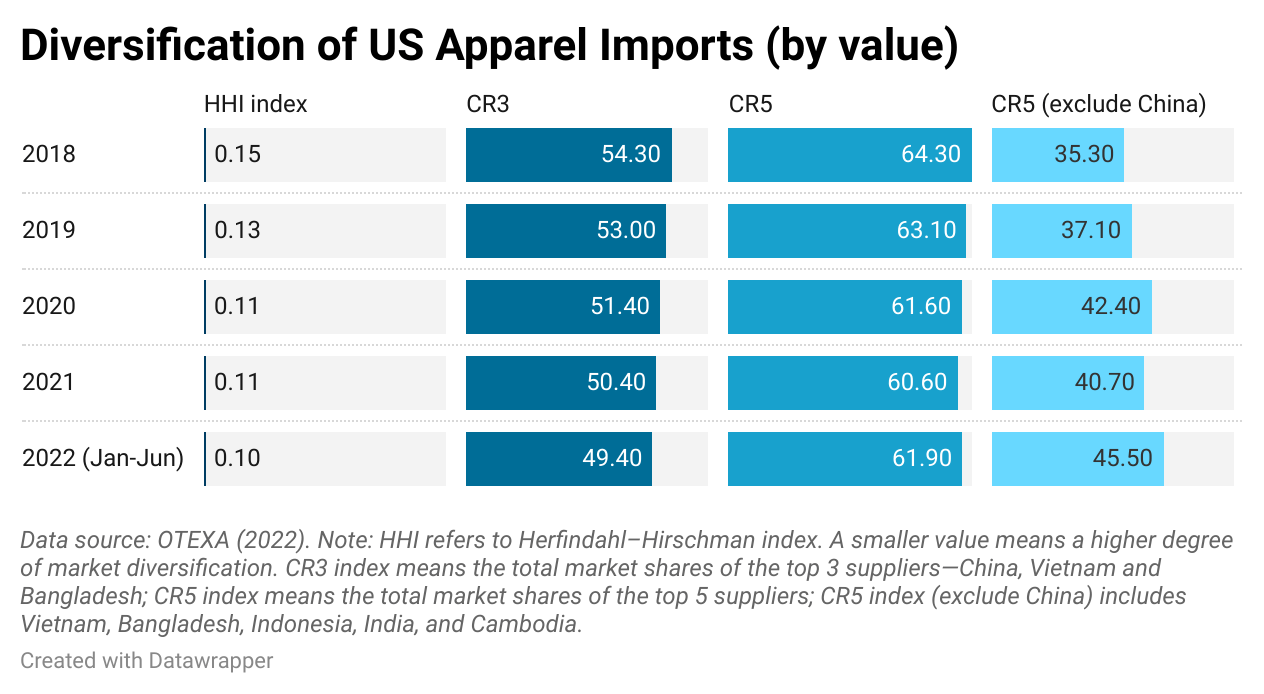

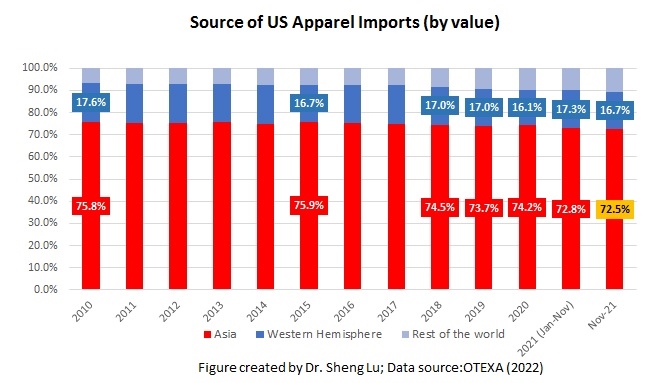

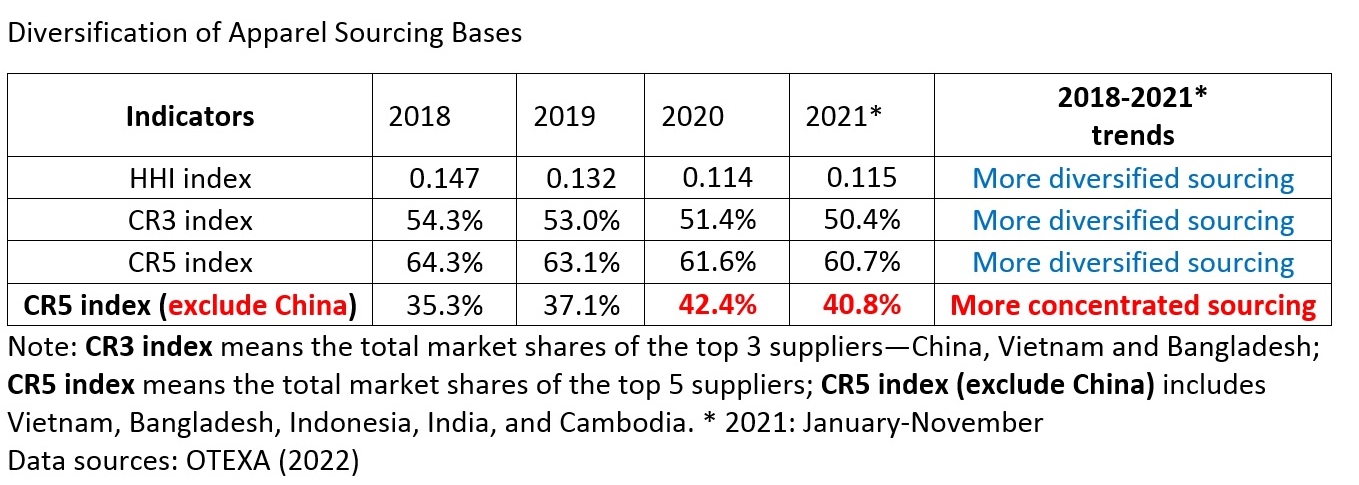

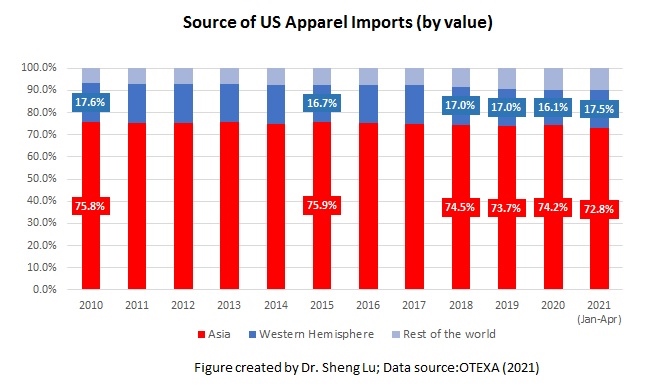

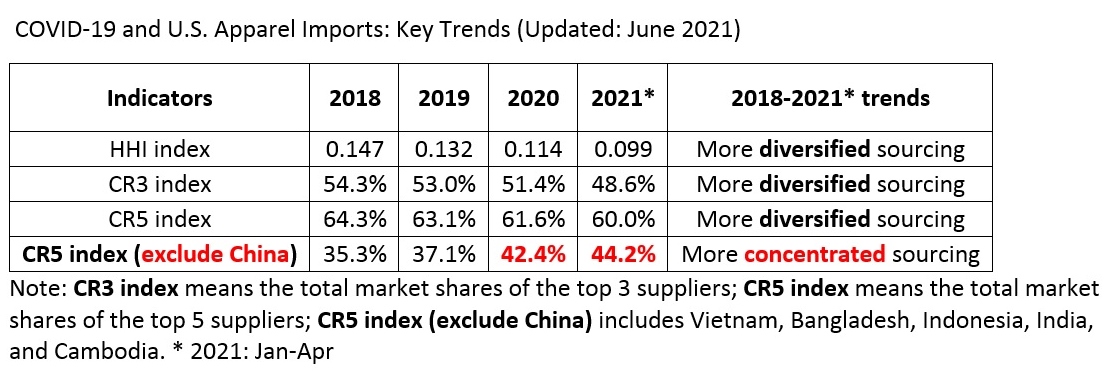

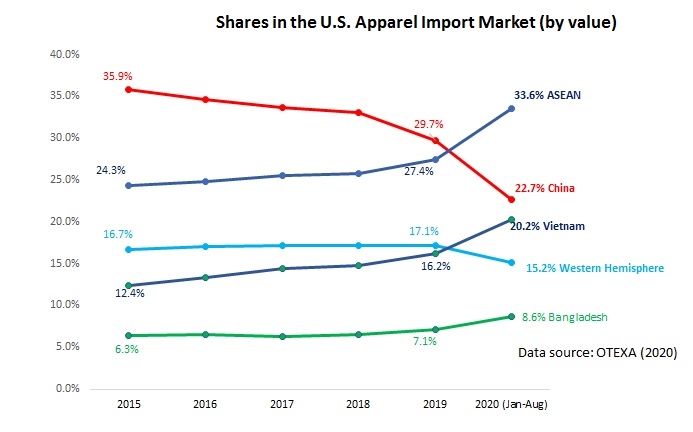

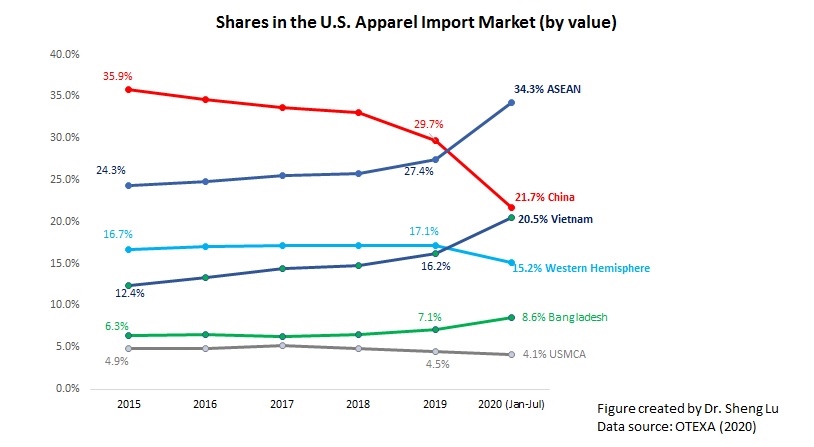

Third, US fashion companies continued to diversify their sourcing base in 2022, which benefited large-scale suppliers in Asia.

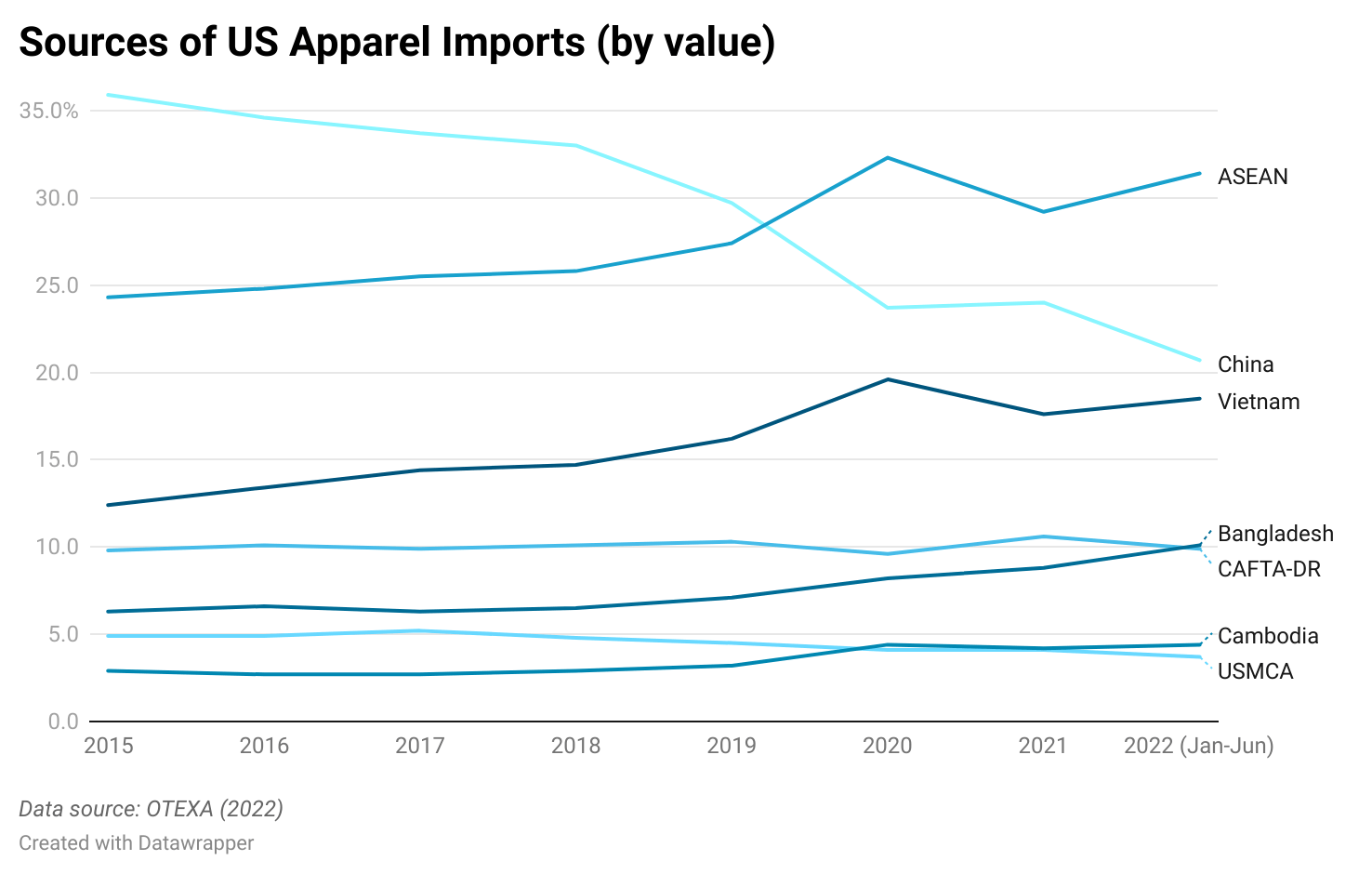

- The Herfindahl–Hirschman index (HHI), a commonly-used measurement of market concentration, went down from 0.11 in 2021 to 0.10 in the first half of 2022, suggesting that US apparel imports came from even more diverse sources. Similarly, the CS3 index, measuring the total market shares of the top three suppliers (i.e., China, Vietnam, and Bangladesh), fell below 50% in the first half of 2022, the lowest since 2018.

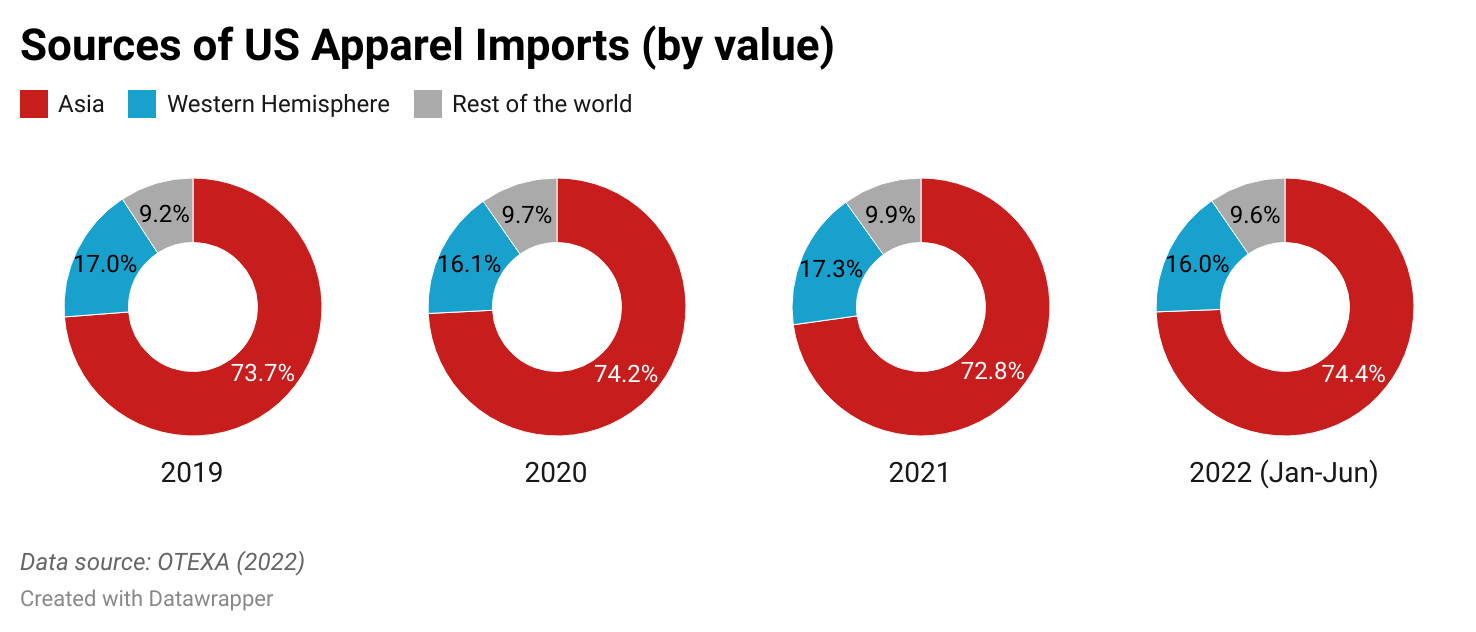

- The Asia region remains the dominant source of apparel for US fashion companies: about 74.4% of US apparel imports came from Asian countries in the first half of 2022 (by value), which has stayed stable for over a decade.

- One critical factor behind the apparent “contradictory” phenomenon is US fashion companies’ intention to reduce their “China exposure” further. Notably, considering all primary sourcing factors, from cost, speed to market, production flexibility, agility, and compliance risks, relatively large-scale Asian suppliers are the most likely alternatives to “Made in China.” Thus, the CR5 index excluding China (i.e., the market shares of Vietnam, Bangladesh, Indonesia, India, and Cambodia) increased from 40.7% in 2021 to 45.5% in the first half of 2022.

Fourth, US fashion companies’ evolving China sourcing strategy is far more subtle and complicated than simply “moving out of China.”

- US fashion companies doubled their efforts to reduce sourcing from China in 2022, particularly in response to the newly implemented Uyghur Forced Labor Prevention Act (UFLPA) and the growing geopolitical risks. For example, measured in value, only 13.2% of US cotton apparel imports (OTEXA code 31) came from China in the first half of 2022, which fell from 14.4% a year ago and much lower than nearly 30% back in 2017.

- Industry sources indicate that US fashion companies are “upgrading” what they source from China, possibly to offset the Section 301 punitive tariffs. The structural change includes importing less basic apparel items (e.g., tops and bottoms) and more sophisticated and higher-valued categories (e.g., dresses). Also, US fashion companies increasingly source from China for apparel items sold in the high-end market. For example, measured by the number of Stock Keeping Units (SKU), about 94% of apparel labeled “Made in China” sold in the US retail market targeted the value segment in 2018. However, of those apparel “Made in China” newly launched to the US retail market between January and July 2022, less than 2% were in the value segment. Instead, items targeting the higher-priced premium and mass market segments surged from 5% to 64%. Another 33% of “Made in China” were luxury apparel items. In other words, US fashion companies no longer see China as a sourcing base for cheap low-end products. Their sourcing decisions regarding China would give more consideration to non-price factors.

- Further, some US fashion companies still see China as a promising sales market with growth potential. Localizing the supply chain (i.e., made in China for China) could be an increasingly popular practice for these companies. Thus, fashion companies’ vision for China could increasingly differ between those that only import products from China and those that see China as an emerging sales market.

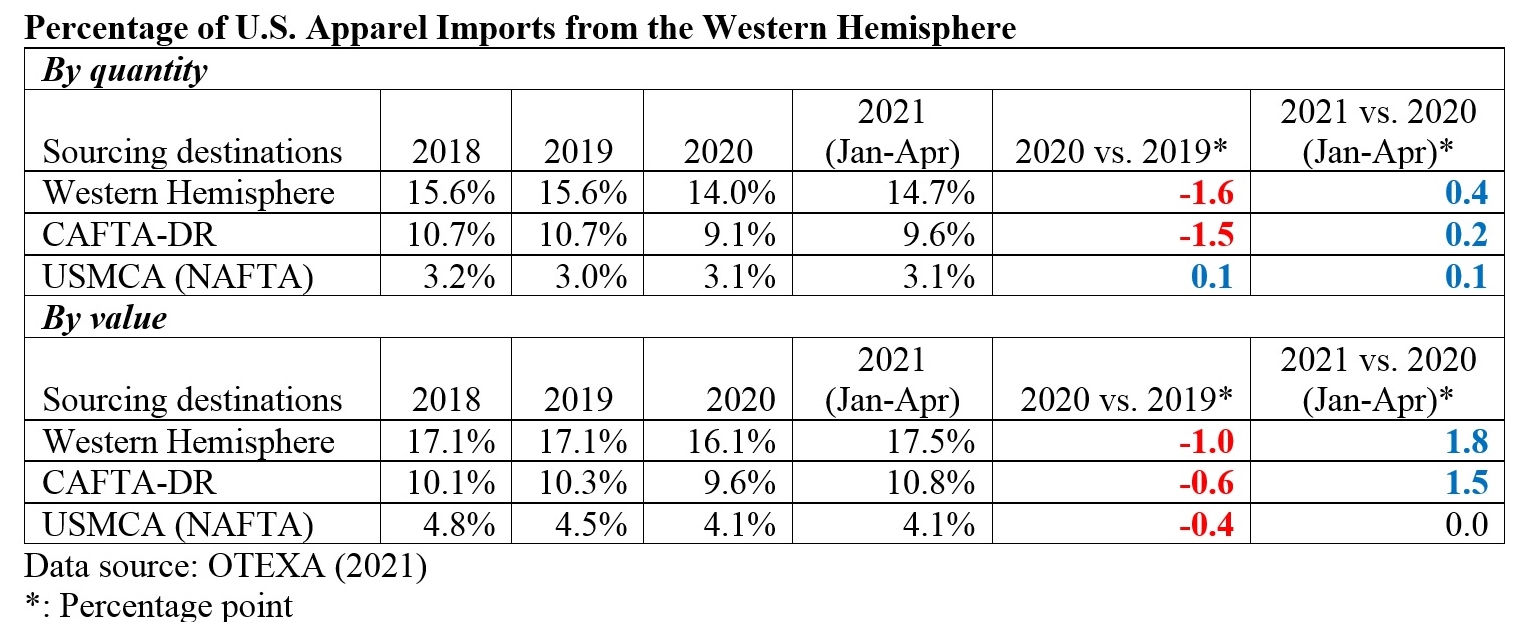

Fifth, US apparel imports from the free trade agreements and trade preference programs partners stayed relatively stable in 2022 but lacked growth.

- Despite the growing enthusiasm among US fashion companies for expanding near sourcing from the Western Hemisphere, the trade volume stayed stagnant. For example, in the first half of 2022, members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) accounted for 8.8% of US apparel imports in quantity and 9.9% in value, lower than a year ago (i.e., 9.9% in quantity and 11.1% in value). Likewise, Mexico also reported lower market shares in the US apparel import market in 2022. The results remind us that encouraging more US apparel sourcing from free trade agreements and preference program partners should go beyond offering preferential duty treatment.

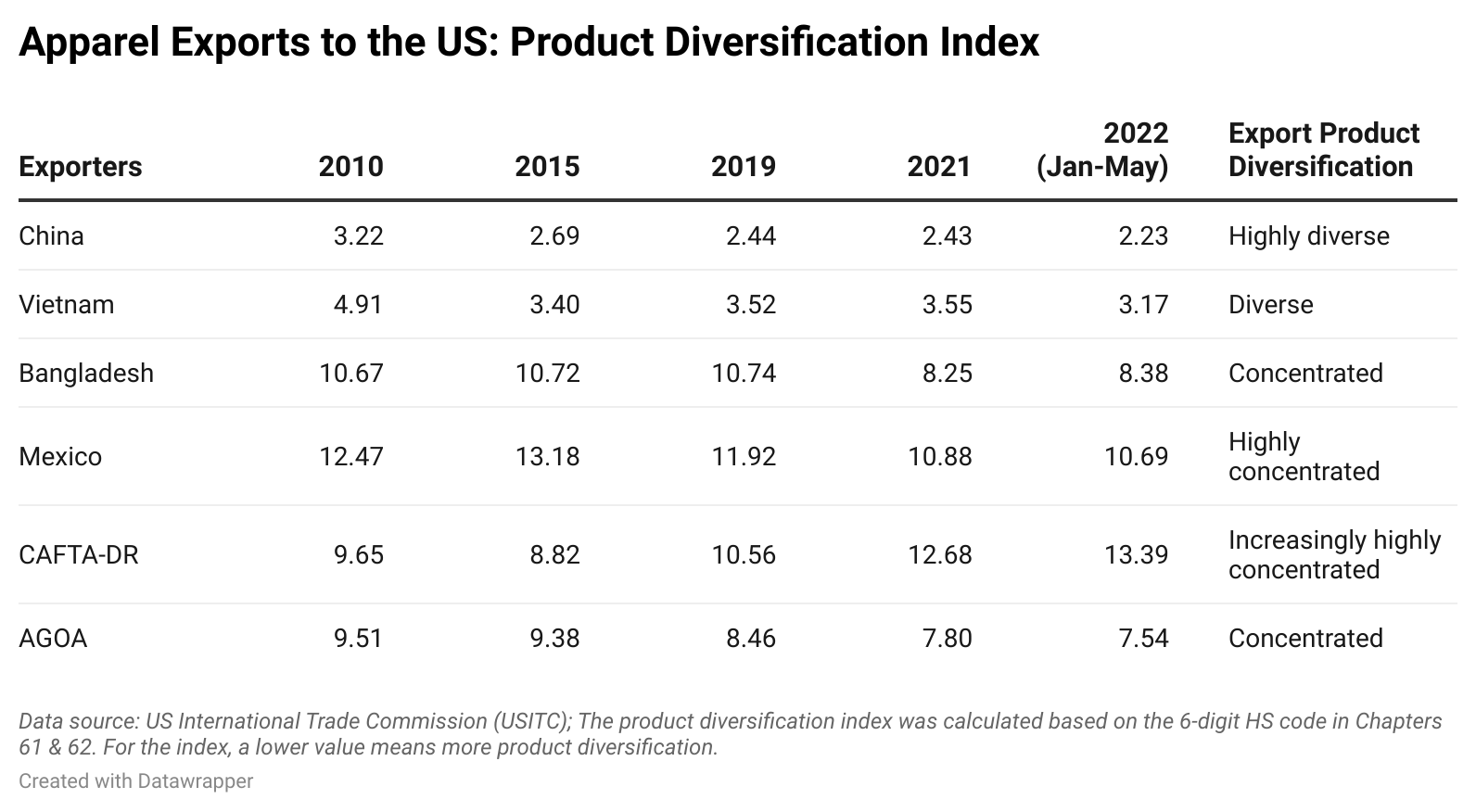

- Product diversification is a critical area that needs improvement, particularly regarding Western Hemisphere sourcing. For example, results show that US apparel sourcing from CAFTA-DR and Mexico generally concentrated on basic items such as tops and bottoms. In comparison, Asian countries, such as China, Vietnam, and Bangladesh, could offer much more diverse categories of products. This explains why US fashion companies treat large-scale Asian countries as their preferred alternatives to “Made in China” rather than moving sourcing orders to CAFTA-DR or Mexico.

- Even though the ultimate goal is to expand US apparel sourcing from the Western Hemisphere, we need to make more efforts to practically and creatively solve the bottleneck of textile raw material supply facing garment producers in the region.

by Sheng Lu

Suggested citation: Lu, S. (2022). Patterns of US Apparel Imports in the First Half of 2022 and Key Sourcing Trends. FASH455 global apparel and textile trade and sourcing. https://shenglufashion.com/2022/08/08/patterns-of-us-apparel-imports-in-the-first-half-of-2022-and-key-sourcing-trends/

{kind=link}

{kind=link}