This study offers valuable input and practical policy recommendations from U.S. apparel companies’ perspectives regarding expanding U.S. apparel sourcing from CAFTA-DR members. For the study, we consulted executives at 27 leading U.S.-based apparel companies (note: 85% report having annual revenues exceeding $500 million; over 95% have been sourcing apparel from the CAFTA-DR region for more than ten years).

The results confirm that expanding U.S. apparel sourcing from CAFTA-DR could be the best chance to effectively create more jobs in Central America and solve the root causes of migration there. To achieve this goal, we need to focus on four areas:

First, improve CAFTA-DR’s apparel production capacity and diversify its product offers.

As many as 92 percent of respondents report currently sourcing apparel from CAFTA-DR members.

Highly consistent with the macro trade statistics, the vast majority of respondents (i.e., 60 percent) place less than 10 percent of their company’s total sourcing orders with CAFTA-DR members.

Whereas respondents rate CAFTA-DR members overall competitive in terms of “speed to market,” they express concerns about CAFTA-DR countries’ limited production capacity in making various products. As a result, U.S. companies primarily source basic fashion items like T-shirts and sweaters from the region. These products also face growing price competition with many alternative sourcing destinations.

Improving CAFTA-DR’s production capacity and diversifying product offers would encourage U.S. apparel companies to move more sourcing orders from Asia to the region permanently.

Second, practically solve the bottleneck of limited textile raw material supply within CAFTA-DR and do NOT worsen the problem.

The limited textile raw material supply within CAFTA-DR is a primary contributing factor behind the region’s stagnated apparel export volume and a lack of product diversification.

Notably, respondents say for their apparel imports from CAFTA-DR members, only 42.9% of fabrics, 40.0% of sewing threads, and 23.8% of accessories (such as trims and labels) can be sourced from within the CAFTA-DR area (including the United States). CAFTA-DR’s textile raw material supply problem could worsen as the U.S. textile industry switches to making more technical textiles and less so for apparel-related fabrics and textile accessories.

Maintaining the status quo or simply calling for making the CAFTA-DR apparel supply chain more “vertical” will NOT automatically increase the sourcing volume. Instead, allowing CAFTA-DR garment producers to access needed textile raw materials at a competitive price will be essential to encourage more U.S. apparel sourcing from the region.

Third, encourage more utilization of CAFTA-DR for apparel sourcing.

CAFTA-DR plays a critical role in promoting U.S. apparel sourcing from the region. Nearly 90 percent of respondents say the duty-free benefits provided by CAFTA-DR encourage their apparel sourcing from the region.

The limited textile supply within CAFTA-DR, especially fabrics and textile accessories, often makes it impossible for U.S. companies to source apparel from the region while fully complying with the strict “yarn-forward” rules of origin. As a result, consistent with the official trade statistics, around 31 percent of respondents say they sometimes have to forgo the CAFTA-DR duty-free benefits when sourcing from the region.

Respondents say the exceptions to the “yarn-forward” rules of origin, including “short supply,” “cumulation,” and “cut and assemble” rules, provide necessary flexibilities supporting respondents’ apparel sourcing from CAFTA-DR members. Around one-third of respondents utilize at least one of these three exceptions when sourcing from CAFTA-DR members when the products are short of meeting the strict “yarn-forward” rules of origin. It is misleading to call these exceptions “loopholes.”

Fourth, leverage expanded apparel sourcing to incentivize more investments in the CAFTA-DR region’s production and infrastructure.

U.S. apparel companies are interested in investing in CAFTA-DR to strengthen the region’s sourcing and production capacity. Nearly half of respondents explicitly say they will make investments, including “building factories or expanding sourcing or manufacturing capacities” in the CAFTA-DR region through 2026.

CAFTA-DR will be better positioned to attract long-term investments in its textile and apparel industry with a sound and expanded apparel sourcing volume.

U.S. fashion companies report significant challenges coming from the macro-economy in 2022, particularly inflation and rising cost pressures. However, most respondents still feel optimistic about the next five years.

Respondents rated “increasing production or sourcing costs” and “inflation and outlook of the U.S. economy” as their 1st and 3rd top business challenges in 2022.

As a new record, 100 percent of respondents expect their sourcing costs to increase in 2022, including nearly 40 percent expecting a substantial cost increase from a year ago. Further, almost everything has become more expensive this year, from textile raw materials, shipping, and labor to the costs associated with compliance with trade regulations.

Over 90 percent of respondents expect their sourcing value or volume to grow in 2022, but more modest than last year.

Despite the short-term challenges, most respondents (77 percent) feel optimistic or somewhat optimistic about the next five years. Reflecting companies’ confidence in their businesses, nearly ALL respondents (97 percent) plan to increase hiring over the next five years.

U.S. fashion companies adopt a more diverse sourcing base in response to supply chain disruptions and the need to mitigate growing sourcing risks.

Asia remains the dominant sourcing base for U.S. fashion companies—eight of the top ten most utilized sourcing destinations are Asia-based, led by China, Vietnam, Bangladesh, and India.

More than half of respondents (53 percent) report sourcing apparel from over ten countries in 2022, compared with only 37 percent in 2021.

Reducing “China exposure” is one crucial driver of U.S. fashion companies’ sourcing diversification strategy. One-third of respondents report sourcing less than 10% of their apparel products from China this year. In addition, a new record of 50 percent of respondents sources MORE from Vietnam than China in 2022.

Nearly 40 percent of respondents plan to “source from more countries and work with more suppliers” over the next two years, up from only 17 percent last year.

Managing the risk of forced labor in the supply chain is a top priority for U.S. fashion companies in 2022, especially with the new implementation of the Uyghur Forced Labor Prevention Act (UFLPA).

Over 95 percent of respondents expect UFLPA’s implementation to affect their company’s sourcing. Notably, more than 85 percent of respondents plan to cut their cotton-apparel imports from China, and another 45 percent to further reduce non-cotton apparel imports from the country.

Most respondents (over 92 percent) do NOT plan to reduce apparel sourcing from Asian countries other than China. However, nearly 60 percent of respondents also would “explore new sourcing destinations outside Asia” in response to UFLPA.

Mapping and understanding the supply chain is a critical strategy adopted by U.S. fashion companies to address the forced labor risks in the supply chain. Almost all respondents currently track Tier 1 and 2 suppliers. With the help of new traceability technologies, 53 percent of respondents have started tracking Tier 3 suppliers this year (i.e., those manufacturing yarn, threads, and trimmings), a substantial increase from 25-36 percent in the past.

There is considerable new excitement about increasing apparel sourcing from members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR). Respondents also call for more textile raw sourcing flexibility to encourage apparel sourcing from the CAFTA-DR region.

CAFTA-DR plays a more significant role as a sourcing base. About 20 percent of respondents place more than 10% of their sourcing orders from the region, doubling from 2021.

Over the next two years, more than 60 percent of respondents plan to increase apparel sourcing from CAFTA-DR members as part of their sourcing diversification strategy.

CAFTA-DR is critical in promoting U.S. apparel sourcing from the region. Around 80 percent of respondents took advantage of the agreement’s duty-free benefits when sourcing apparel from the region this year, up from 50—60 percent in the past.

Respondents say the exceptions to the “yarn-forward” rules of origin, such as the “short supply” and “cumulation” mechanisms, provide essential flexibility that encourages more apparel sourcing from CAFTA-DR members.

Respondents say improving textile raw material supply is critical to encouraging more U.S. apparel sourcing from CAFTA-DR members. Particularly, “allowing more flexibility in souring fabrics from outside CAFTA-DR” and “improving yarn production capacity and variety within CAFTA-DR” are the top two priorities.

U.S. fashion companies strongly support another ten-year renewal of the African Growth and Opportunity Act (AGOA). Meanwhile, Ethiopia’s loss of AGOA eligibility discourages U.S. apparel sourcing from the ENTIRE AGOA region.

As much as 75 percent of respondents say another ten-year AGOA renewal will encourage more apparel sourcing from the region and making investment commitments.

However, despite the tariff benefits and the liberal rules of origin, respondents express explicit concerns about the region’s lack of competitiveness in speed to market, political instability, and having an integrated regional supply chain.

Ethiopia’s loss of AGOA benefits had a notable negative impact on sourcing from the country AND the entire AGOA region. Notably, no respondent plans to move sourcing orders from Ethiopia to other AGOA beneficiaries.

Kekeli Ahiableis a private sector development Advisor with the Tony Blair Institute’s Industrialisation Practice. Working with industry leaders over the past 10 years, she has facilitated business and job creation opportunities in the trade infrastructure, supply chain, and manufacturing sectors across four continents.

In her current technical support role at TBI, she manages the Institute’s regional textile and apparel (T&A) project which aims to support the development of a best in class, sustainable, and circular cotton-to-apparel manufacturing hub across five West African countries.

She holds a Master of Public Policy (MPP) from the University of Oxford, with a focus on trade policy and economic development.

Interview Part:

Sheng: Thank you so much for speaking with us, Kekeli. First of all, would you please tell us a little about the Tony Blair Institute for Global Change (TBI) and your involvement with the textile and apparel (T&A) industry in West Africa?

Kekeli: Sure! The Tony Blair Institute for Global Change (TBI) is a not-for-profit organization that offers strategic advice and practical support to political leaders and governments so they can deliver reforms that raise standards and transform lives. Our work includes advising on a range of sectors including industrialization, energy, and technology. We currently work in 17 African countries.

Since 2019, we have been working with several governments in West Africa – specifically Cote d’Ivoire, Ghana, and Togo – to support the development of a best-in-class and sustainable textile and apparel sector that meets the needs of British, European, and North American retailers and consumers.

Our role has centered around supporting our partner governments to:

prepare for doing business; work with them to develop relevant sector strategy & review policy, etc.

design attractive investment incentives

attract interest in the region from relevant fashion trade actors

For instance, we facilitated a week-long investor roadshow to the three countries in 2019, with participation from three of the largest global apparel brands together with their mills and manufacturers (with a combined turnover of over US$ 70 billion). This was co-sponsored under the banner of Amcham Hongkong.

Covid-19 naturally impacted our physical scoping events and so we moved the conversations to virtual roundtable forums. Last December, eight of the UK’s biggest retailers, plus several European retailers, attended a session we organized, led by Rt Hon. Tony Blair. Representatives from the three main governments and other non-governmental groups involved in developing textiles and apparel in the region were also present to engage in discussion with the investors. We have also worked with the American Apparel and Footwear Association (AAFA) and the United States Fashion Industry Association (USFIA) to update US brands and retailers on West Africa’s potential as a nearshore sourcing destination for the North American market.

In summary, TBI is very much to help create top-of-mind awareness about West Africa’s suitability to grow a viable T&A sourcing hub and ultimately facilitate investment into the priority countries.

Sheng: What is the current state of the textile and apparel (T&A) industry in West Africa? What are the key development trends? How about the impact of COVID?

Kekeli: West Africa’s T&A market is rapidly expanding. Although considered nascent when compared to Asia’s more developed markets, its many greenfield opportunities also mean there are fewer legacy challenges to contend with. This offers a ripe opportunity for investors and manufacturers to start from an almost clean slate, which is crucial as the apparel industry makes strides toward a more environmentally sustainable footprint.

The region also has numerous natural and competitive advantages for textiles and apparel manufacturing and has seen increased interest from global actors, brands, manufacturers, infrastructure developers, development finance institutions, etc., over the last few years.

Key development trends

Recognizing shifting patterns in global T&A trade and the immense value in domestic processing of abundantly available raw materials, West African governments are demonstrating an ambition to harness their competitive advantages and expand their T&A sectors.

The governments of Cote d’Ivoire, Ghana, and Togo especially, are walking the talk. Togo’s agile government closed a ground-breaking €200 million investment deal with Arise IIP, in August 2020. The deal included building a 400-hectare eco-industrial park dedicated to textiles and apparel manufacturing. Apart from the park, the Arise group is investing into vertically integrated (fiber to fashion) knit apparel units which will start commercial operations in mid-2023.

Ghana has the most advanced industrial base of the three highlighted countries and hosts DTRT Apparel, which has been running its operation in Ghana for the past 7 years and is currently the largest apparel exporter from West Africa. As a further boost towards vertical integration, in March, they partnered on a co-creation deal with the International Finance Corporation (IFC) to jointly develop setting up a synthetic fabric mill in the region. Meanwhile, Northshore Apparel, another garment actor, recently began constructing a 10,000-worker garment factory in Ghana. To attract more foreign direct investment (FDI), the government is drafting a new T&A sector policy and incentive framework under the UK’s Foreign, Commonwealth & Development Office (FCDO) funded £16 million-pound JET Programme.

In a similar vein, Cote d’Ivoire, Africa’s second-largest cotton seed grower, is carrying out sector reforms and strategy development aimed at facilitating the domestic transformation of at least 50% of their annual cotton output.

Altogether, it is an exciting time to be developing the T&A sector in West Africa. We are excited to contribute towards this vision to create a best in class, vertical and sustainable manufacturing hub in the region, and help to create 500k direct and indirect jobs.

Impact of COVID

Most existing garment manufacturers pivoted to producing PPE for both domestic and international markets. For instance, DTRT is making this a permanent feature of their production, although orders have resumed from their traditional apparel buyers.

We have also witnessed a stronger resolve from governments to support their domestic T&A manufacturing sectors’ growth. The Togo deal, for instance, happened at the height of covid lockdowns. Some countries also offered waivers on value-add tax for their textile and apparel manufacturers and used the time to restructure their labor codes to meet international standards.

Sheng: How to understand West African countries’ competitiveness as an apparel-sourcing base for western fashion companies?

Kekeli: First, there is an immense opportunity to vertically integrate the T&A manufacturing value chain. The region produces around 1.5 million metric tons of cotton annually, which represents about 60% of Africa’s total output and 15% of global exports. The vast majority of this is exported unprocessed. Farming methods feature rain-fed irrigation with harvest done by handpicking, leading to 80% being labeled as preferred, sustainable cotton under Better Cotton Initiative (BCI) and Cotton made in Africa (CmiA) standards.

Secondly, its geographical location means it offers a natural nearshore market to Europe and US markets – literally less than two weeks away from Europe by sea.

Note: transit times are shorter depending on the shipping line. Transit references for the US are New York and Charleston, Antwerp and Hamburg for Europe, and Hangzhou for China/Asia. Source: Freightos, Bollore Africa Logistics interviews

Other benefits include an abundant trainable labor force, cost savings to manufacturers under favorable trade instruments like African Growth and Opportunity Act (AGOA), EU’s Economic Partnership Agreement (EPA)/Everything But Arms (EBA) program, etc., as well as consolidated political stability in all three countries. Moreover, there is strong potential for developing a circular textile economy facilitated by green manufacturing and initiatives like our West Africa Regeneration Zone (WARZ) initiative, on which TBI is collaborating with key brands and figures from the industry.

Apart from the main retail regions, there is a growing online retail market in Africa – estimated to increase to $75 billion by 2025 with projected $3.4 trillion aggregate GDP under African Continental Free Trade Area (AfCFTA). As we have seen with recent moves to the continent by Twitter, Google, and others, there is large scope for fashion retailers to use manufacturing in West Africa as a launchpad into this growing continental market, with free movement of goods and services under AfCFTA.

These are attractive propositions for buyers and manufacturers looking to diversify their supply chains and leave a greener carbon footprint in the process.

Sheng: It is of concern that used clothing exports from developed countries to Africa hurt the local textile and apparel industry. What is your assessment?

Kekeli: That is correct. The reality is that there is strong consumer demand for second-hand clothing, due to the cheap prices and readily available clothing for re-use. This is the main reason why the supply chains are routing the bales to other markets, including Africa. Most consumers in Africa rely heavily on the second-hand clothing markets. In this configuration, it is difficult for local players to compete and attract the same consumers’ appetites.

Moreover, this is quite complex, especially in an era of global value chains and [free] trade pacts that enjoin countries to offer some levels of reciprocity in their trade relations. Governments wishing to partake in international trade cannot simply ban imports of goods to protect their local industries. It is, therefore, crucial to explore practical win-win solutions.

For instance, there is a fast-growing global market for fabrics made from recycled materials as brands and manufacturers are taking steps to make their footprint greener. Receiver countries of second clothes could develop other business opportunities from the materials that arrive, with funding from relevant partners. Take Ghana as an example – its Kantamanto market, arguably the world’s largest reuse, repair, and upcycle market, process hundreds of tons of clothing each week. A large percentage of what comes to the market however ends up as landfilled waste due to various reasons.

One remedy is recycling, which ploughs back the many unsold and non-reusable clothes into the textile manufacturing economy. This not only reduces the need for virgin fibers but with the scale envisioned for the West Africa T&A manufacturing project, it increases the fabric feedstock available for domestic Cut, Make, Trim (CMT) manufacturers thus supporting to differentiate the region as a destination for circular apparel sourcing. Managed properly, we envision this would have positive spillover effects on the domestic market. At TBI, we published a piece on tackling Ghana’s textile waste which can be read here for a deeper dive into the subject.

Sheng: How does the textile and apparel industry in West Africa embrace sustainability?

Kekeli: The strongest aspect is from an environmental perspective. With rain-fed irrigation, around 80% of the region’s cotton is labeled as preferred cotton. Vertically integrating the cotton value chain by processing within one geographical area supports a lower carbon footprint of each final product.

West Africa’s geographical proximity to main buyer markets also increases its environmental sustainability credentials as a nearshore market.

Moreover, circularity is part of the culture in this part of the world – people reuse and pass on clothes to other family relations after use, with very little going to waste. We see an opportunity to scale this with the West Africa regeneration (WARZ) initiative. The WARZ initiative aims to support the development of a sustainable and circular textile and apparel supply base in West Africa where post-consumer textile waste is recycled at scale and becomes feedstock for making new apparel. This would be underpinned by disruptive recycling and traceability technology.

In our role as non-vested convenors and facilitators, we have convened a consortium of international and domestic stakeholders to develop a pilot project in Ghana, which is the world’s number two importer of second-hand clothing. Preliminary scoping puts the entire project size at over US$500 million with the potential to generate over 60K jobs along the value chain over the next 5-10 years. The following image depicts the initial concept for the regeneration zone project:

Relatedly, to demonstrate emerging support at the continental level, the African Development Bank recently approved the establishment of a €4 million Africa Circular Economy Facility to drive integration of the circular economy into African efforts to achieve nationally defined contribution targets.

Sheng: How important are trade preference programs like the African Growth and Opportunity Act (AGOA) to the development of the textile and apparel industry in West Africa? Do you think AGOA should be extended after 2025? Should the agreement keep the liberal “third-country fabric” rules of origin? Why or why not?

Kekeli: Trade preference programs are extremely important to facilitate the growth of Africa’s manufacturing and export capacity. As fundamentals like infrastructure tend to be less developed on the continent, preferential regimes like AGOA serve as a key enabler for manufacturing FDI. The T&A industries in countries like Kenya, Lesotho, and Madagascar have grown tremendously in the past few years thanks to AGOA’s tariff-free concessions. West Africa’s T&A industry is now in the beginning stages of development and needs an extension of AGOA to grow.

I believe in the short-medium term, maintaining third-country fabric rules is also crucial (note: Third-country fabric rules allow for apparel made with fabrics sourced from outside the AfCFTA/Sub-Saharan Africa region to qualify for duty-free access). The simple reason is that West Africa’s cotton value chain needs support to develop. While countries have ambitions for vertical integration by processing cotton within the region, these backward linkages will take time to develop.

A phase-out period may be negotiated to further incentivize accelerating the move towards domestic production of fibers that qualify to be used by CMT manufacturers in the [sub]-region.

Sheng: What does the African Continental Free Trade Area (AfCFTA) mean for the textile and apparel industry in West Africa?

Kekeli: The AfCFTA pact aims to form the world’s largest free trade area by connecting almost 1.3bn people across 54 African countries. The goal is to create a single market for goods and services to deepen the economic integration of Africa, with a combined GDP of around $3.4 trillion.

Historically, the most developed world regions have been those that have figured out and developed strong regional value chains. The EU, which is the world’s largest regional trade agreement (RTA) by value has over 64% of trade taking place within the regional block. Similar cases pertain in the US-Mexico-Canada (USMCA) and the Association of Southeast Asian Nations (ASEAN) free trade areas.

Intra-Africa trade on the contrary is currently under 20%, with strong potential for growth. Trade figures show that when African countries trade with each other, it is mostly intermediate or finished goods, which naturally have more value. The goal is to encourage more of this.

Textiles and apparel development in West Africa has strong potential to become a flagship example of what AfCFTA implementation could practically look like. In the next couple of years, I envision fabrics from Cote d’Ivoire, Benin, being exported to Ghana duty-free to feed apparel factories, designers from Cote d’Ivoire offering their expertise across the sub-region with no restrictions on their movement, textiles from Ghana being traded in Nigeria, etc. The possibilities are truly endless.

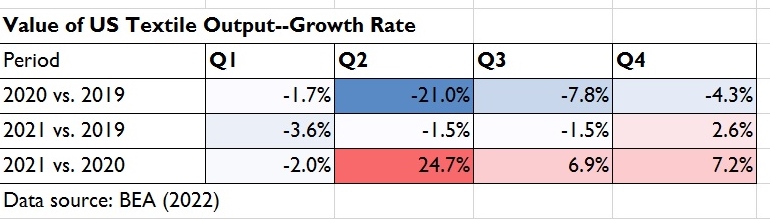

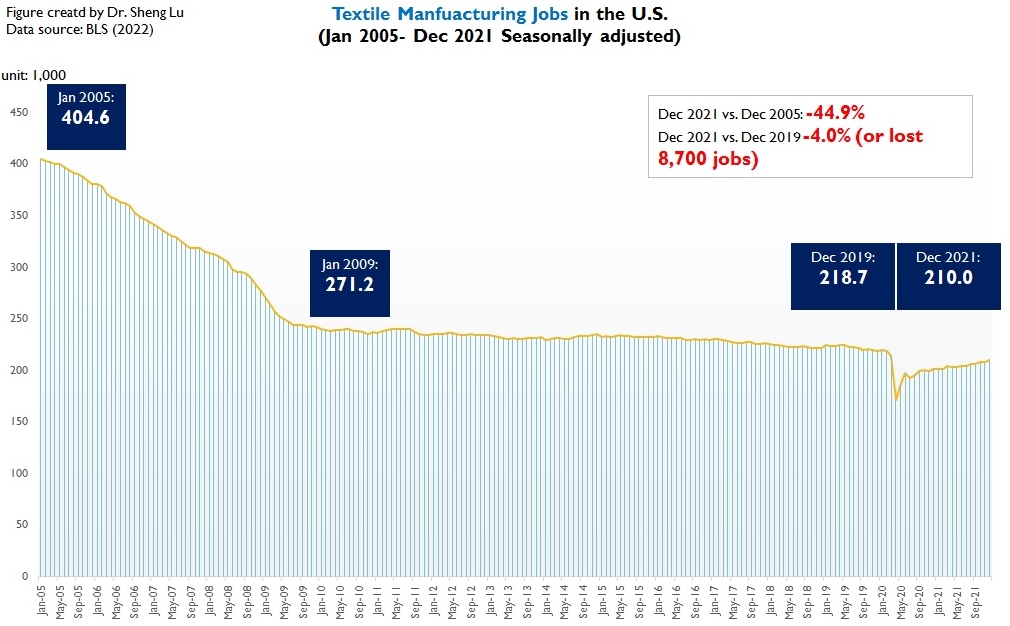

Textile and apparel manufacturing in the U.S. has significantly shrunk in size over the past decades due to multiple factors ranging from automation, import competition to the shifting U.S. comparative advantages for related products. However, U.S. textile manufacturing is gradually coming back. The output of U.S. textile manufacturing (measured by value added) totaled $16.59 billion in 2021, up 23.8% from 2009. In comparison, U.S. apparel manufacturing dropped to $9.5 billion in 2019, 4.4% lower than ten years ago (Bureau of Economic Analysis, 2021).

Meanwhile, like many other sectors, U.S. textile and apparel production was hit hard by COVID-19 in the first half of 2020 but started to recover in the 3rd quarter. Notably, as of December 2021, U.S. textile production had returned to its pre-COVID level.

On the other hand, as the U.S. economy is turning more mature and sophisticated, the share of U.S. textile and apparel manufacturing in the U.S. Gross Domestic Product (GDP) dropped to only 0.12% in 2020 from 0.57% in 1998 (Bureau of Economic Analysis, 2021).

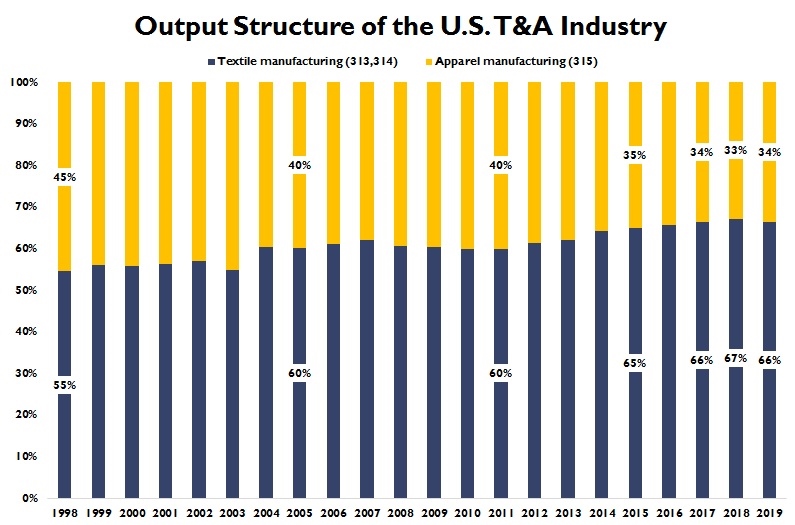

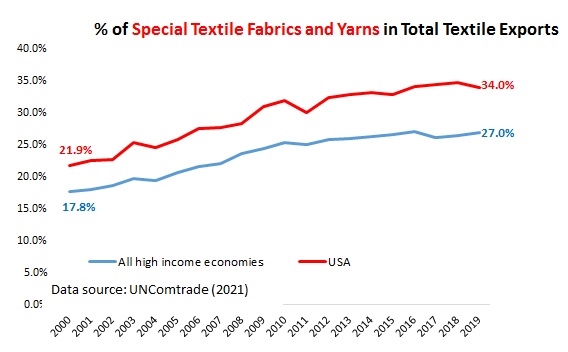

The U.S. textile and apparel manufacturing is changing in nature. For example, textile products had accounted for over 66% of the total output of the U.S. textile and apparel industry as of 2019, up from only 58% in 1998 (Bureau of Economic Analysis, 2020). Textiles and apparel “Made in the USA” are growing particularly fast in some product categories that are high-tech driven, such as medical textiles, protective clothing, specialty and industrial fabrics, and non-woven. These products are also becoming the new growth engine of U.S. textile exports. Notably, “special fabrics and yarns” had accounted for more than 34% of U.S. textile exports in 2019, up from only 20% in 2010 (Data source: UNComtrade, 2021).

Compatible with the production patterns, employment in the U.S. textile industry (NAICS 313 and 314) and apparel industry (NAICS 315) fell to the bottom in April-May 2020 due to COVID-19 but started to recover steadily since June 2020. From January 2021 to December 2021, the total employment in the two sectors increased by 4.5% and 4.2%, respectively (Seasonally adjusted). However, the employment level remains much lower than the pre-COVID level (benchmark: December 2019).

To be noted, as production turns more automated and thanks to improved productivity (i.e., the value of output per worker), U.S. textile and apparel factories have been hiring fewer workers even before the pandemic. The downward trend in employment is not changing for the U.S. textile and apparel manufacturing sector. Related, how to attract the new generation of workforce to the factory floor remains a crucial challenge facing the future of textile and apparel “Made in the USA.”

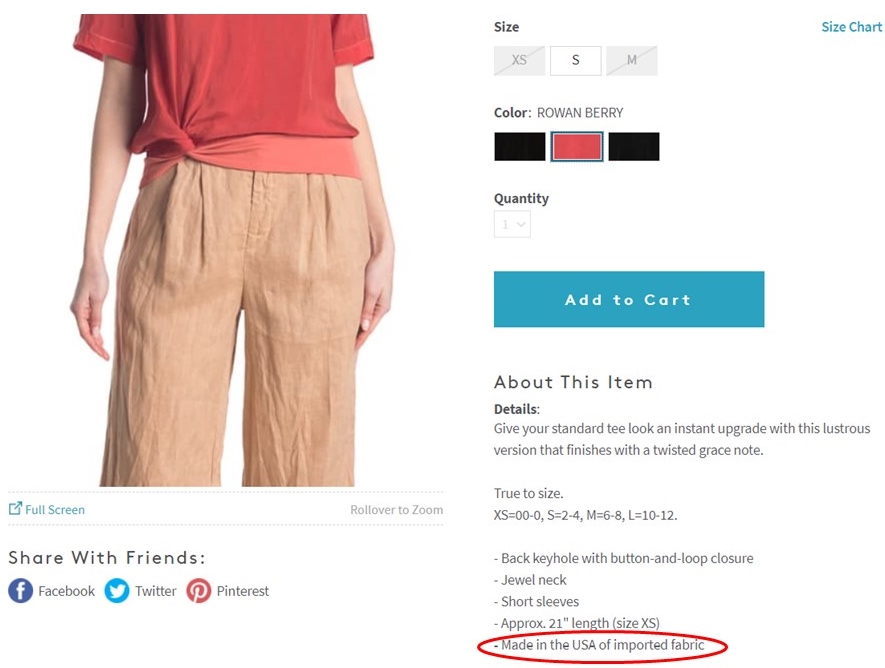

It is not rare to find clothing labeled “made in the USA with imported fabric” or “made in the USA with imported material” in the stores. Statistical analysis shows a strong correlation between the value of U.S. apparel output and U.S. yarn and fabric imports from 1998 to 2019.

Like many other developed economies whose textile and apparel industries had reached the stage of post-maturity, the United States today is a net textile exporter and net apparel importer. COVID-19 has affected U.S. textile and apparel trade in several ways:

Trade volume fell and yet fully recovered: Both affected by the shrinkage of import demand and supply chain disruptions, the value of U.S. textile and apparel imports dropped by as much as 19.3% in 2020 from a year ago, particularly apparel items (down 23.5%). Likewise, the value of U.S. textile and apparel exports in 2020 decreased by 15.6%, including an unprecedented 26% decrease in yarn exports. Further, thanks to consumers’ robust demand, the value of US apparel imports enjoyed a remarkable 27.4% growth in 2021 from a year ago and but was still 2.5% short of the level in 2019.

Trade balance shifted: Before the pandemic, U.S. was a net exporter of fabrics. However, as the import demand for non-woven fabrics (for making PPE purposes) surged during the pandemic, U.S. ran a trade deficit of $502 million for fabrics in 2020; the trade deficit expanded to $975 million in 2021. Meanwhile, as retail sales slowed and imports dropped during the pandemic, the U.S. trade deficit in apparel shrank by 19% in 2020 compared with 2019. However, the shrinkage of the trade deficit did not necessarily boost clothing “Made in the USA” in 2020, reminding us that the trade balance often is not an adequate indicator to measure the economic impact of trade.

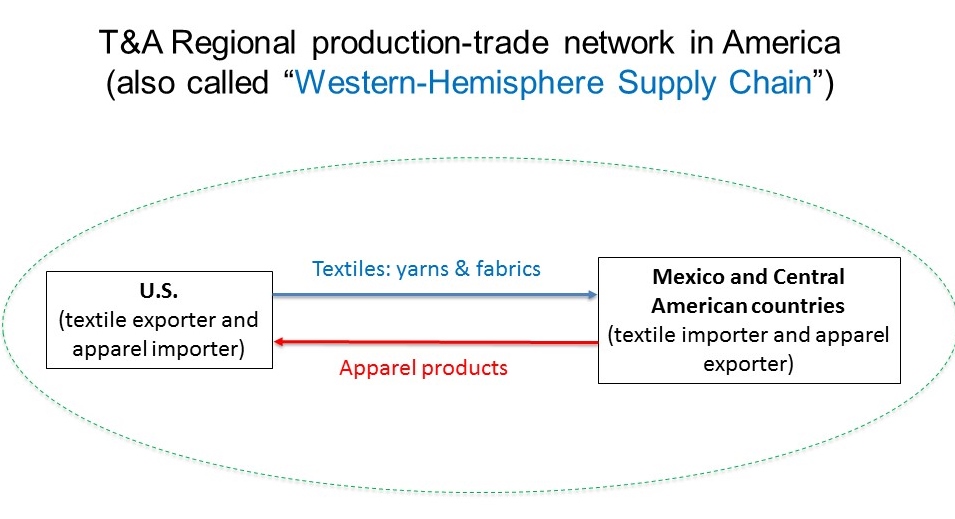

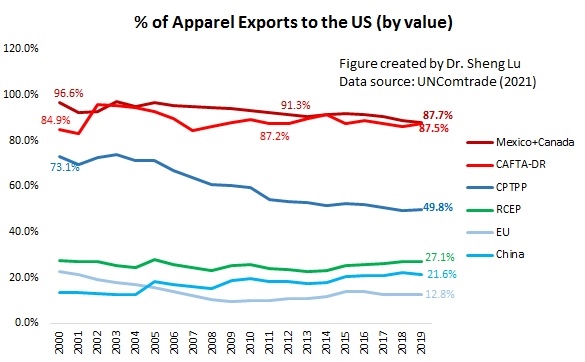

No change in export market: More than 70% of U.S. textile and apparel export went to the Western Hemisphere in 2021, a pattern that has stayed stable over the past decades (OTEXA, 2022). More can be done to strengthen the Western Hemisphere supply chain and textile and apparel production in the region by leveraging regional trade agreements like CAFTA-DR and USMCA.

Trade and sourcing play a critical role in building a more sustainable fashion apparel supply chain. Below are recent FASH455 blog posts addressing climate change, sustainability, recycling, and transparency issues. Feel free to join our online discussion and share your ideas on improving sustainable, ethical, and more socially responsible sourcing.

In April 2022, the Office of the United States Trade Representative (USTR) released its 2023 Fiscal Year Budget report, outlining five goals and objectives for 2023. Notably, textile and apparel is a key sector USTR plans to focus on in the coming year:

Goal 1: Open Foreign Markets and Combat Unfair Trade

Provide policy guidance and support for international negotiations or initiatives affecting the textile and apparel sector to ensure that the interests of U.S. industry and workers are taken into account and, where possible, to provide new or enhanced export opportunities for U.S. industry.

Conduct reviews of commercial availability petitions regarding textile and apparel products and negotiate corresponding FTA rules of origin changes, where appropriate, in a manner that takes into account market conditions while preserving export opportunities for U.S. producers and employment opportunities for U.S. workers.

Engage relevant trade partners to address regulatory issues potentially affecting the U.S. textile and apparel industry’s market access opportunities.

Continue to engage under CAFTA-DR working groups and committees to optimize inclusive economic opportunities; strengthen the agreement and address non-tariff trade impediments; provide capacity building in textile and apparel trade-related regulation and practice on customs, border and market access issues, including agriculture and sanitary and phytosanitary regulation, to avoid barriers to trade.

Continue to engage CAFTA-DR partners and stakeholders to identify and develop means to increase two-way trade in textiles and apparel and strengthen the North American supply chain to enhance formal job creation.

Goal 2: Fully Enforce U.S. Trade Laws, Monitor Compliance with Agreements, and Use All Available Tools to Hold Other Countries Accountable

Closely collaborate with industry and other offices and Departments to monitor trade actions taken by partner countries on textiles and apparel to ensure that such actions are consistent with trade agreement obligations and do not impede U.S. export opportunities.

Research and monitor policy support measures for the textile sector, in particular in China, India, and other large textile producing and exporting countries, to ensure compliance with international agreements.

Continue to work with the U.S. textile and apparel industry to promote exports and other opportunities under our free trade agreements and preference programs, by actively engaging with stakeholders and industry associations and participating, as appropriate, in industry trade shows.

Goal 4: Develop Equitable Trade Policy Through Inclusive Processes

Take the lead in providing policy advice and assistance in support of any Congressional initiatives to reform or re-examine preference programs that have an impact on the textile and apparel sector.

The full study is available here(need Just-Style subscription)

By leveraging production and trade statistics from government databases, we examined the critical trends of US textile manufacturing and supply. Particularly, we try to understand the strengths and weaknesses of the United States as a textile raw material supplier for domestic garment manufacturers and those in the Western Hemisphere. Below are the key findings:

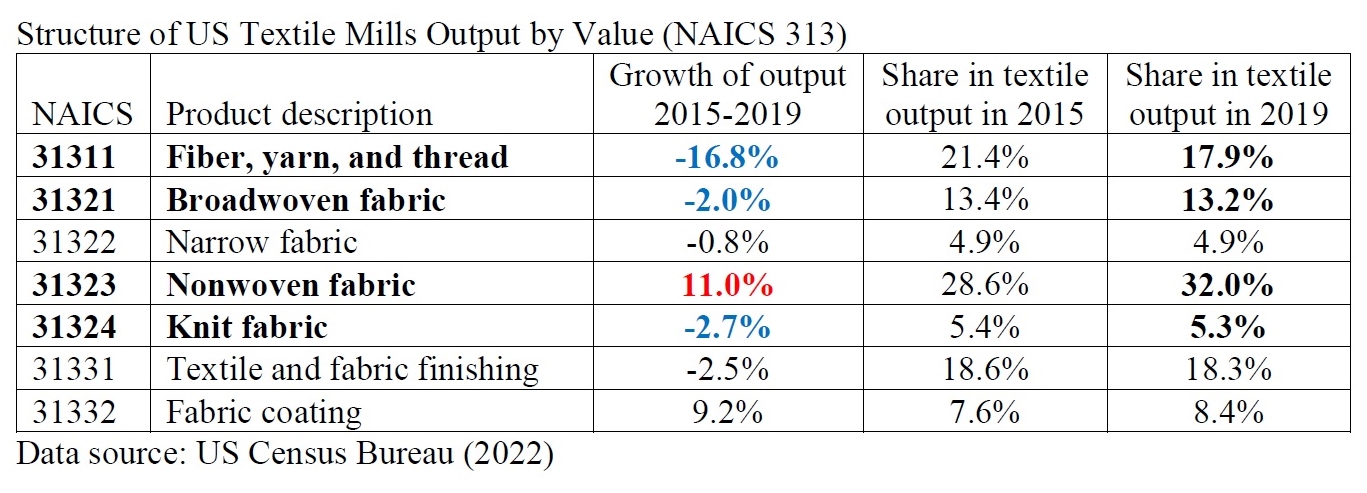

First, fiber, yarn, and thread manufacturing is a long-time strength in the US, whereas fabric production is much smaller in scale. Specifically, fiber, yarn, and thread (NAICS 31311) accounted for nearly 18% of US textile mills’ total output in 2019. In comparison, less than 13% of the production went to woven fabrics (NAICS 31321) and only about 5% for knit fabrics (NAICS 31324).

Second, the US textile industry shifts to make more technical textiles and less apparel-related yarns, fabrics, and other raw materials. Data shows that from 2015 to 2019, the value of US fiber, yarn, and thread manufacturing (NAICS code 31311) dropped by as much as 16.8 percent. Likewise, US broadwoven fabric manufacturing (NAICS code 31321) and knit fabric (NAICS code 31324) decreased by 2.0 percent and 2.7 percent over the same period. Labor cost, material cost, and capital expenditure are critical factors behind the structural shift of US textile manufacturing.

Third, the structural change of US textile manufacturing directly affects the role of the US serving as a textile supplier for domestic apparel producers and those in the Western Hemisphere.

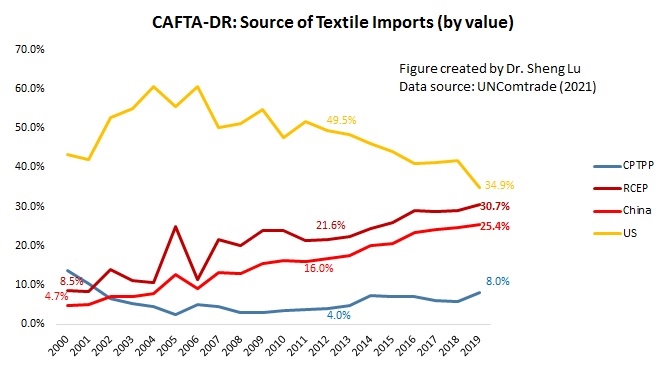

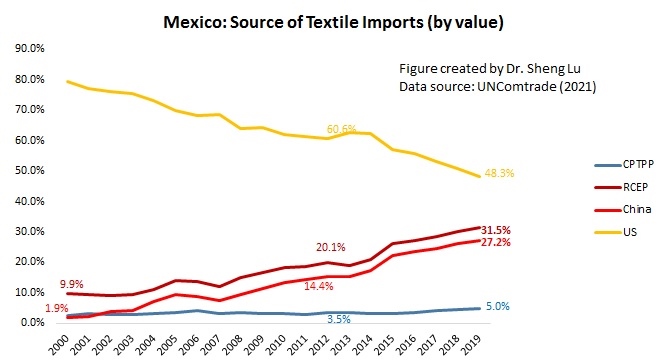

On the one hand, the US remains a critical yarns and threads supplier in the Western Hemisphere. For example, from 2010 to 2019, the value of US fibers, yarn and threads exports (NAICS31311) increased by 25%, much higher than other textile categories. Likewise, in 2021, fibers, yarns, and threads accounted for about 23.3% of US textile exports, higher than 21.0% in 2010. Additionally, nearly 40% of Mexico and CAFTA-DR members’ yarn imports in 2021 (SITC 651) still came from the US, the single largest source. This trend has stayed stable over the past decade.

On the other hand, the US couldn’t sufficiently supply fabrics and other textile accessories for garment producers in the Western Hemisphere, and the problem seems to worsen. Corresponding to the decline in manufacturing, US broadwoven fabric (NAICS 31321) and knit fabric (NAICS 31324) exports decreased substantially.

The US also plays a declining role as a fabric and textile accessories supplier for garment factories in the Western Hemisphere. Garment producers in Mexico and CAFTA-DR members had to source 60%-80% of woven fabrics and 75-82% of knit fabrics from non-US sources in 2021. Likewise, only 40% and 14.6% of Mexico and CAFTA-DR members’ textile accessories, such as labels and trims, came from the US in 2021.

Likewise, the limited US fabric supply affects the raw material sourcing of domestic apparel manufacturers. For example, according to the “Made in the USA” database managed by the Office of Textiles and Apparel (OTEXA), around 36% of US-based apparel mills explicitly say they use “imported material,” primarily fabrics.

The study’s findings echo some previous studies suggesting that textile raw material supply, especially fabrics and textile accessories, could be the single most significant bottleneck preventing more apparel “Made in the USA” and near-sourcing from the Western Hemisphere.

Meanwhile, how to overcome the bottleneck could trigger heated public policy debate. For example, US policymakers could encourage an expansion of domestic fabric and textile accessories manufacturing as one option. However, to make it happen takes time and requires substantial new investments. Also, economic factors may continue to favor technical textiles production over apparel-related fabrics in the US.

As an alternative, US policymakers could make it easier for garment producers in the Western Hemisphere to access their needed fabrics and textile accessories outside the US, such as improving the rules of origin flexibility in CAFTA-DR or USMCA. But this option is likely to face strong opposition from US yarn producers and be politically challenging to implement.

(About the authors: Dr Sheng Lu is an associate professor in fashion and apparel studies at the University of Delaware; Anna Matteson is a research assistant in fashion and apparel studies at the University of Delaware).

According to the video, how has the supply chain for apparel and footwear changed over the past decade?

What are the pros and cons of moving from a global supply chain to a regional one for fashion companies?

For fashion companies interested in “near-shoring” and “re-shoring”, what factors should they consider? Why?

Anything else you find interesting/intriguing/thought-provoking/debatable in the video? Why?

Note: Everyone is welcome to join our online discussion. For students in FASH455, please address at least two questions. Please mention the question number # (no need to repeat the question) in your comment.

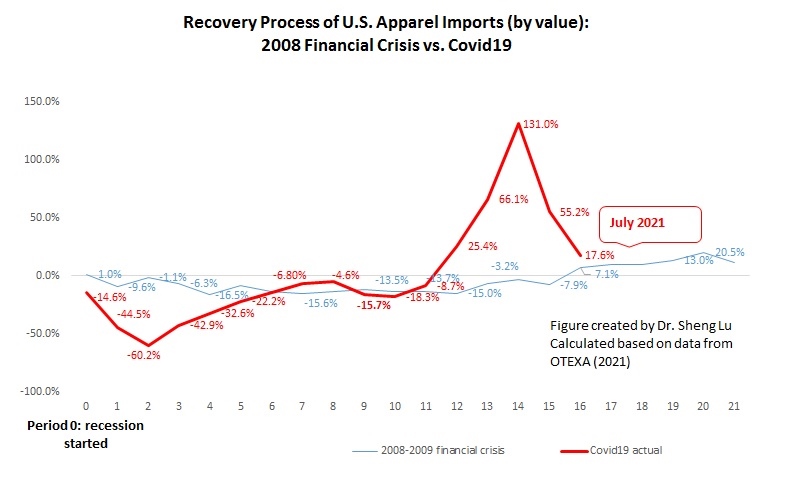

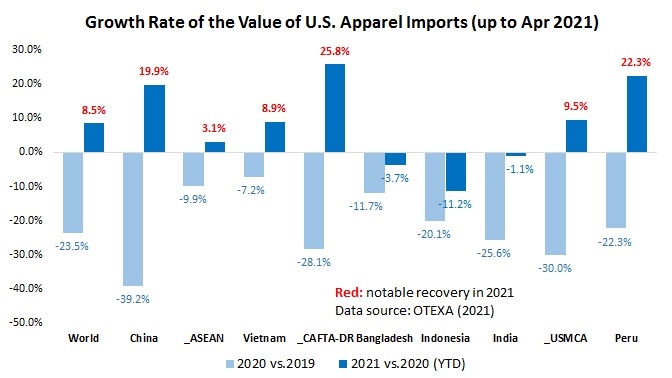

First, US apparel imports continue to rebound in November 2021 as companies build the inventory for the holiday season. Thanks to US consumers’ strong demand and the upcoming holidays, the value of US apparel imports went up by 15.7% in November 2021 from a month ago (seasonally adjusted) and increased by as much as 39.7% from 2020. However, before the pandemic, the value of US apparel imports always peaked in October and then gradually slipped in November and December. The unusual surge of imports in November 2021 could be the combined effects of price inflation and the late arrival of goods due to the shipping crisis.

Meanwhile, US apparel imports so far in 2021 have been far more volatile than in the past few years because of uncertainties and disruptions caused by COVID-19 and the shipping crisis. For example, the year-over-year (YoY) growth rate ranged from 131% in May to 17.6% in July, causing fashion companies additional inventory planning and supply chain management challenges. Unfortunately, the new omicron variant could worsen the market uncertainty and volatility.

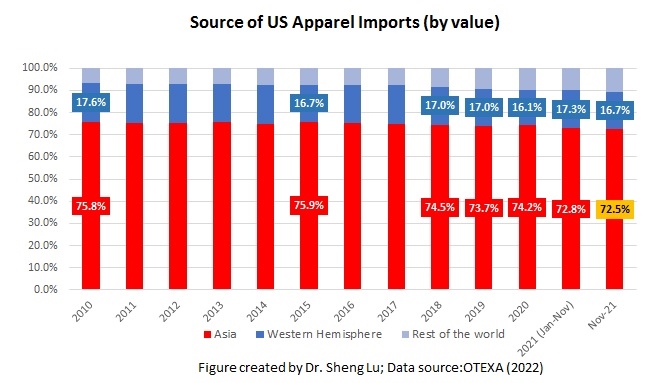

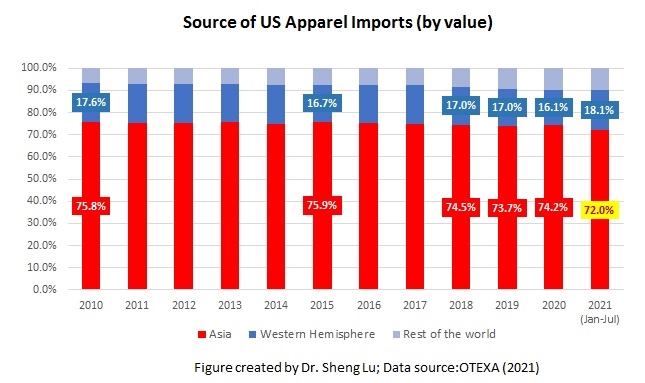

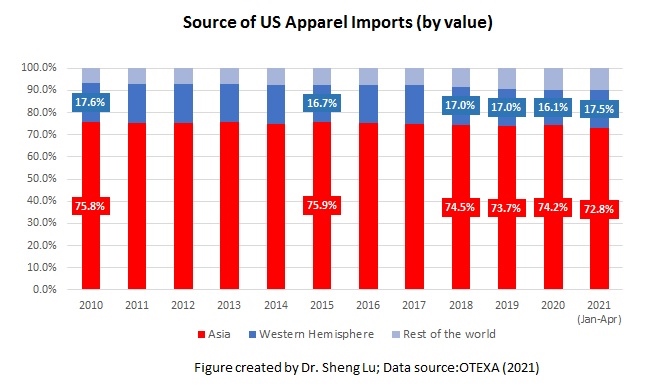

Second, Asian countries remain the dominant sourcing base for US fashion companies as the production capacity elsewhere is limited. Asian countries’ market shares fell from 74.2% in 2020 to 71.3% in July 2021, primarily because of the COVID lockdowns in Vietnam and Bangladesh. US apparel imports came from Asian countries rebounded to 74.8% and 72.5% in October and November 2021, respectively. This result suggests a lack of alternative sourcing destinations outside Asia, especially for large volume items. Meanwhile, the worsening shipping crisis affecting the route from Asia to North America could explain why Asian suppliers’ market shares in November were somewhat lower than a month ago.

Third, US companies continue to treat China as one of their essential sourcing bases in the current business environment. However, companies are NOT reversing their long-term strategy of reducing “China exposure.” China stays the largest supplier for the US market in November 2021, accounting for 41.5% of total US apparel imports in quantity and 25.8% in value. Due to the seasonal factor, China’s market shares typically peak from June to September and then drop from October until March-April.

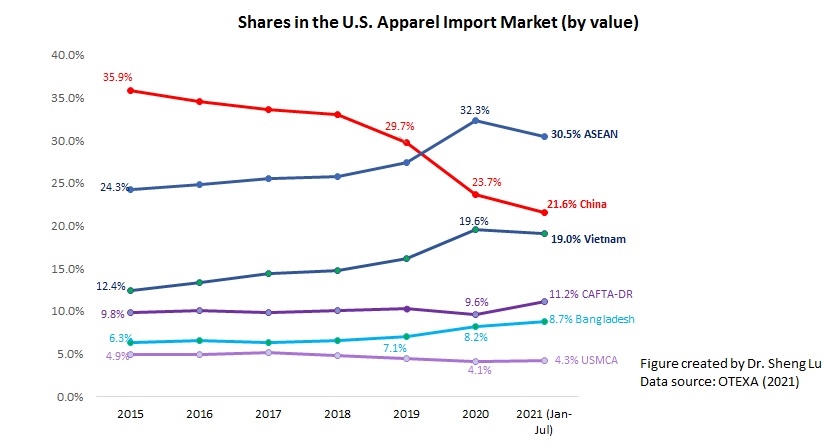

Both industry sources and the export product diversification index also consistently show that China supplied the most variety of products to the US market with no near competitors. In comparison, US apparel imports from Bangladesh, Mexico, and CAFTA-DR members concentrate more on specific product categories.

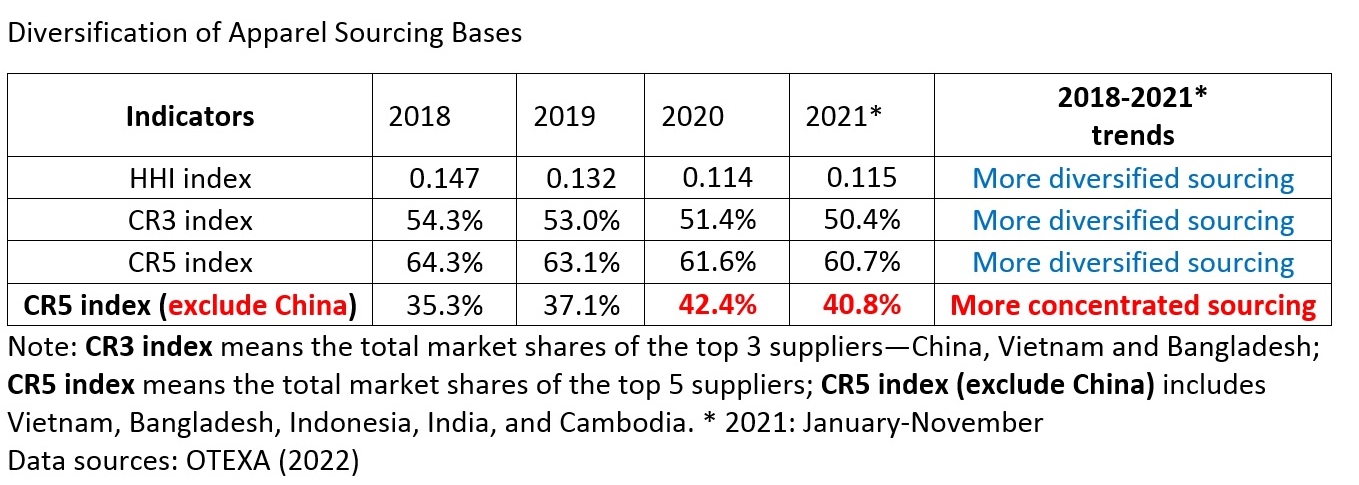

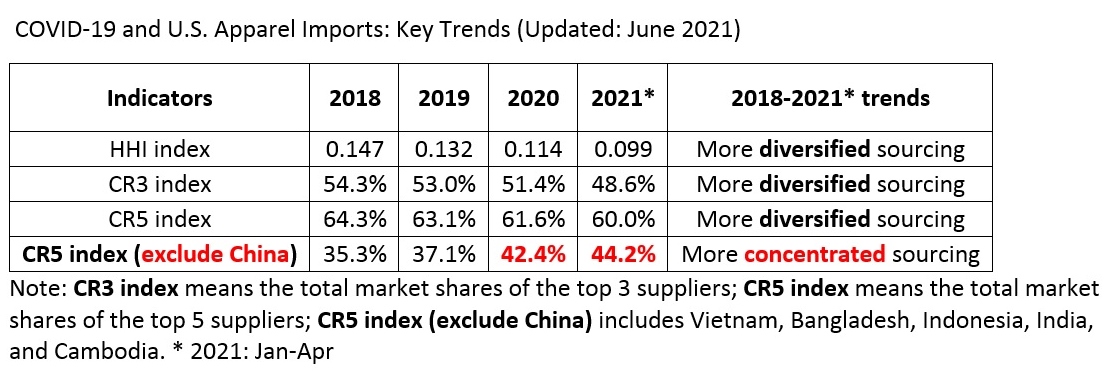

Nevertheless, the HHI index and market concentration ratios (CR3 and CR5) calculated based on the latest data suggest that US fashion companies continue to move their apparel sourcing orders from China to other Asian countries overall. For example, only around 15% of US cotton apparel comes from China, compared with about 27% in 2018. My latest studies also indicate that it has become ever more common to see a fashion company places only around 10% of its total sourcing value or volume from China compared to over 30% in the past. Furthermore, with the growing tensions of the US-China relations and the newly enacted Uyghur Forced Labor Prevention Act, fashion companies could take another look at their China sourcing strategy to avoid potential high-impact disruptions.

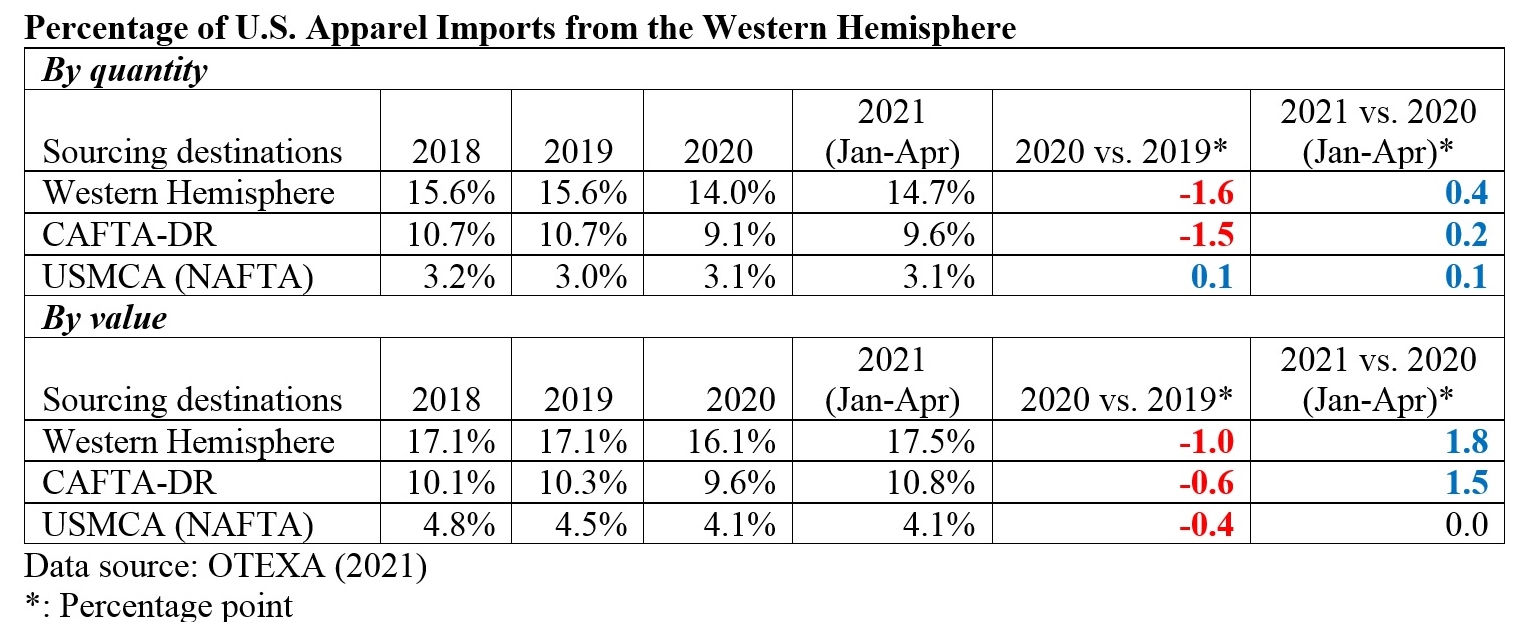

Fourth, near sourcing from the Western Hemisphere, especially CAFTA-DR members, continue to gain popularity. Specifically, 17.3% of US apparel imports came from the Western Hemisphere year-to-date (YTD) in 2021 (January-November), higher than 16.1% in 2020. Notably, CAFTA-DR members’ market shares increased to 10.6% in 2021 (January to November) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 41.7% growth in 2021 (January—November) from a year ago, one of the highest among all sourcing destinations. The imports from El Salvador (up 42.6%), Honduras (up 47.1%), and Guatemala (36.6%) had grown particularly fast so far in 2021. However, the political instability in some Central American countries could make fashion companies feel hesitant to permanently switch their sourcing orders to the region or make long-term investments.

Additionally, the latest trade data suggests a notable increase in the price of US apparel imports. Notably, the unit price of US apparel imports from almost all leading sources went up by more than 10% from January 2021 to November 2021. As worldwide inflation continues, the rising sourcing cost pressure won’t ease anytime soon.

In December 2021, Just-Style consulted a panel of industry leaders and scholars in its Outlook 2022–what’s next for apparel sourcing briefing. Below is my contribution to the report. All comments and suggestions are more than welcome!

What next for apparel sourcing?

As “COVID sets the agenda” and the trajectory of several critical market and non-market forces hard to predict (for example, global inflation, and geopolitics), fashion companies may still have to deal with a highly volatile and uncertain market environment in 2022. That being said, it is still hopeful that fashion companies’ toughest sourcing challenges in 2021 will start to gradually ease at some point in the new year, including the hiking shipping costs, COVID-related lockdowns, and supply chain disruptions.

In response to the “new normal,” fashion companies may find several sourcing strategies essential:

One is to maintain a relatively diverse apparel sourcing base. The latest trade data suggests that US, EU, and Japan-based fashion companies have been steadily sourcing from a more diverse group of countries since 2018, and such a trend continues during the pandemic. Echoing the pattern, in the latest annual benchmarking study I conducted in collaboration with the United States Fashion Industry Association (USFIA), we find that “China plus Vietnam plus many” remains the most popular sourcing model among respondents. This strategy means China and Vietnam combined now typically account for 20-40 percent of a fashion company’s total sourcing value or volume, a notable down from 40-60 percent in the past few years. Fashion companies diversify their sourcing away from “China plus Vietnam” to avoid placing “all eggs in one basket” and mitigate various sourcing risks. In addition, more than 85 percent of surveyed fashion companies say they will actively explore new sourcing opportunities through 2023, particularly those that could serve as alternatives to sourcing from China.

The second strategy is to strengthen the relationship with key vendors further. As apparel is a buyer-driven industry, fashion brands and retailers fully understand the importance of catering to consumers’ needs. However, the supply chain disruptions caused by COVID-19 remind fashion companies that building a close and partner-based relationship with capable suppliers also matters. For example, working with vendors that have a presence in multiple countries (or known as “super-vendors”) offers fashion companies a critical competitive edge to achieve more flexibility and agility in sourcing. Sourcing from vendors with a vertical manufacturing capability also allows fashion companies to be more resilient toward supply chain disruptions like the shortage of textile raw materials, a significant problem during the pandemic.

Further, we could see fashion companies pay even closer attention to textile raw material sourcing in the year ahead. On the one hand, given the growing concerns about various social and environmental compliance issues like forced labor, fashion brands and retailers are making more significant efforts to better understand their entire supply chain. For example, in addition to tracking who made the clothing or the fabrics (i.e., tier 1 & 2 suppliers), more companies have begun to release information about the sources of their fibers, yarns, threads, and trimmings (i.e., tier 3 & tier 4 suppliers). On the other hand, many fashion brands and retailers intend to diversify their textile material sourcing from Asia, particularly China, against the current business environment. Compared with cutting and sewing garments, much fewer countries can make textiles locally, and it takes time to build textile production capacity. Thus, fashion companies interested in taking more control of their textile raw material sourcing need to take concrete actions such as shifting their sourcing model and making long-term investments intentionally.

Apparel industry challenges and opportunities

One key issue we need to watch closely is the US-China relations. China currently remains the single largest source of apparel globally, with no near alternative. China also plays an increasingly significant role as a textile supplier for many leading apparel exporting countries in Asia. However, as the US-China relations become more concerning and confrontational, we could anticipate new trade restrictions targeting Chinese products and products from any sources that contain components made in China. Notably, with strong bipartisan support, President Biden signed into law the Uyghur Forced Labor Prevention Act on December 23, 2021. The new law is a game-changer! Depending on the detailed implementation guideline to be developed by the Customs and Border Protection (CBP), US fashion companies may find it not operationally viable to source many textiles and apparel products from China. In response, China may retaliate against well-known western fashion brands, disrupting their sales expansion in the growing Chinese consumer market. Further, as China faces many daunting domestic economic and political challenges, a legitimate question for fashion companies to think about is what an unstable China means for their sourcing from the Asia-Pacific region and what the contingency plan will be.

Another critical issue to watch is the regional textile and apparel supply chains and related free trade agreements. While apparel is a global sector, apparel trade remains largely regional-based, i.e., countries import and export products with partners in the same region. Data shows that from 2019 to 2020, around 80% of Asian countries’ textile and apparel imports came from within Asia and about 50% for EU countries. Over the same period, over 87% of Western Hemisphere (WH) countries’ textile and apparel exports went to other WH countries and about 75% for EU countries.

Notably, the reaching and implementation of new free trade agreements will continue to alter and shape new regional textile and apparel supply chains in 2022 and beyond. For example, the world’s largest free trade agreement, the Regional Comprehensive Economic Partnership (RCEP), officially entered into force on January 1, 2022. The tariff reduction and the very liberal rules of origin in the agreement could strengthen Japan, South Korea, and China as the primary textile suppliers for the Asia-based regional supply chain and enlarge the role of ASEAN as the leading apparel producer. RCEP could also accelerate other trade agreements in the Asia-Pacific region, such as the China-South Korea-Japan Free Trade Agreement currently under negotiation.

As one of RCEP’s ripple effects, we can highly anticipate the Biden administration to announce its new Indo-pacific economic framework soon to counterbalance China’s influences in the region. The Biden administration also intends to leverage trade programs such as the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) to boost textile and apparel production, trade, and investment in the Western Hemisphere and address the root causes of migration. These trade initiatives will be highly relevant to fashion companies that could use the opportunity to expand near sourcing, take advantage of import duty-saving benefits and explore new supply chains.

Additionally, fashion companies need to be more vigilant toward political instability in their major sourcing destinations. We have already seen quite a turmoil recently, from Myanmar’s military coup, Ethiopia’s loss of the African Growth and Opportunity Act (AGOA) benefits, concerns about Haiti and Nicaragua’s human rights, and the alleged forced labor in China’s Xinjiang region. Whereas fashion brands and retailers have limited or no impact on changing a country’s broader human rights situation, the reputational risks could be very high. Having a dedicated trade compliance team monitoring the geopolitical situation routinely and ensuring full compliance with various government regulations will become mainstream among fashion companies.

And indeed, sustainability, due diligence, recycling, digitalization, and data analytics will remain buzzwords for the apparel industry in the year ahead.

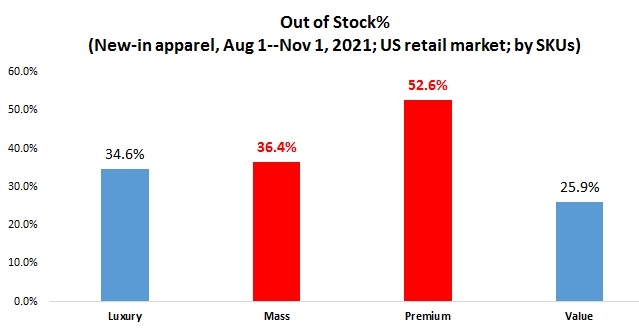

US fashion brands and apparel retailers face the challenge of running out of inventory amid the holiday season and the ongoing shipping crisis. Based on consultation with industry insiders and resources, we take a detailed look at which apparel products are more likely to be out of stock in the US retail market. Several patterns are noteworthy:

First, clothing products targeting the premium and mass market face more significant shortages than luxury or value apparel items in the US. Take clothing items in the premium market, for example. Of those apparel products newly launched to the US retail market from August 1 to November 1, 2021, nearly half of them were already out of stock as of November 10, 2021 (note: measured by SKUs). The increased demand from middle-class US consumers could be among the primary contributing factors.

Second, seasonal products and stable fashion items are more likely to be out of stock. For example, as we are already in the winter season, it is not surprising to see many swimwear products run out of stock. Meanwhile, it is interesting to see stable fashion products like hosiery and underwear also report a relatively high percentage of inventory shortage. The result could be the combined effects of consumers’ robust demand and the shipping delay.

Third, apparel products locally sourced from the US seem to have the lowest out-of-stock rate. Reflecting the shipping crisis, clothing items sourced from Bangladesh and India report a much higher out-of-stock rate. However, a substantial percentage of “made in the USA” apparel was in the category of “T-shirt”, implying switching to domestic sourcing often is not a viable option for US fashion brands and retailers.

Additionally, fast fashion retailers overall report a much lower out-of-stock rate than department stores and specialty clothing stores. This result showcases fast fashion retailers’ competitive advantages in supply chain management, which payoffs in the current challenging business environment.

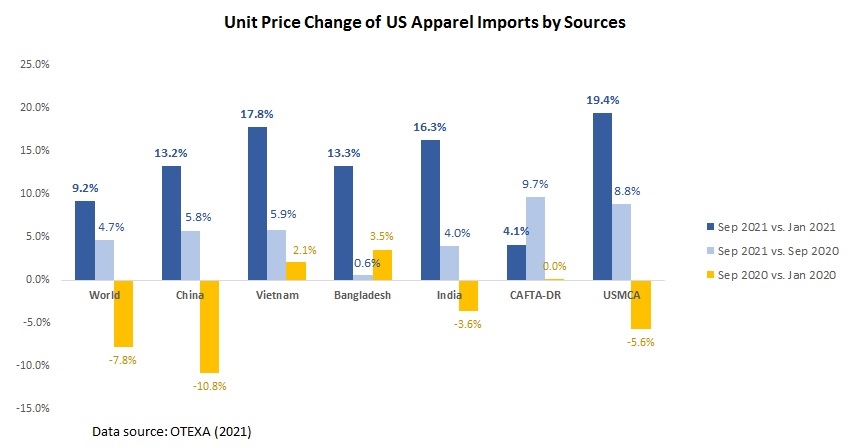

On the other hand, the latest trade data suggests a notable increase in the price of US apparel imports. Notably, the unit price of US apparel imports from almost all leading sources went up by more than 10% from January 2021 to September 2021.

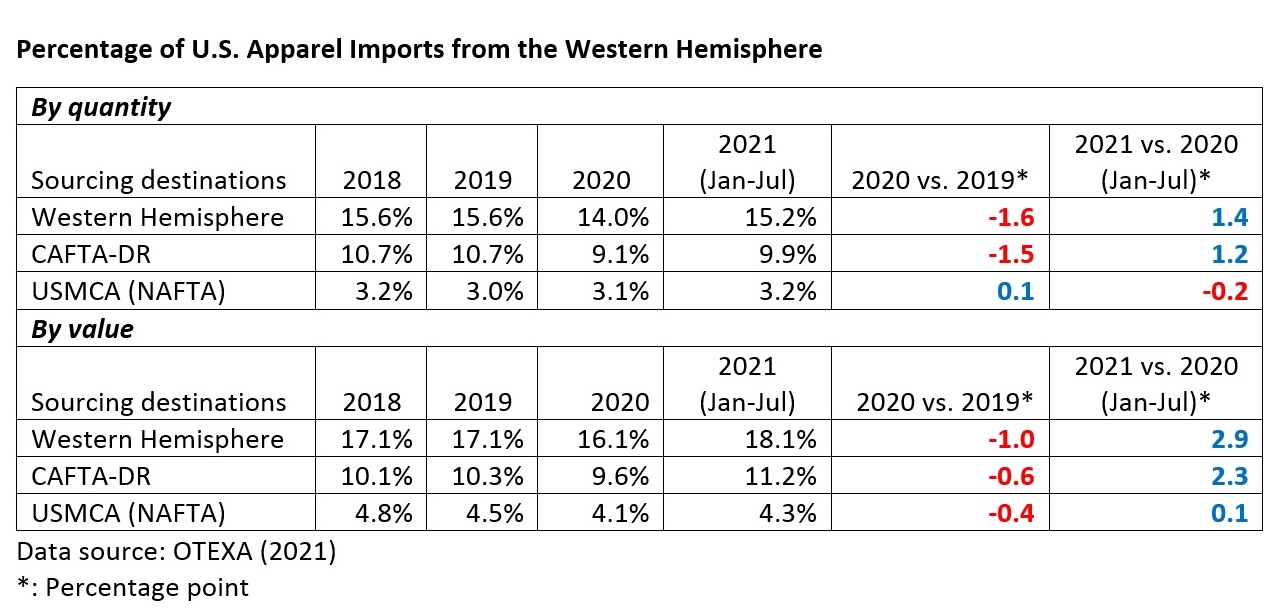

Data shows that 15.2% of US apparel imports came from USMCA and CAFTA-DR members YTD in 2021 (January-August), higher than 13.7% in 2020 and about 14.7% before the pandemic (2018-2019). Notably, CAFTA-DR members’ market shares increased to 11% in 2021 (January to Aug) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 54% growth in 2021 (January—Aug) from a year ago, faster than 25% of the world’s average.

#2 Sourcing apparel from USCMA and CAFTA-DR members helps US fashion brands and retailers save around $1.6-1.7 billion tariff duties annually. (note: the estimation considers the value of US apparel imports from USMCA and CAFTA-DR members at the 6-digit HTS code level and the applied MFN tariff rates for these products; we didn’t consider the additional Section 301 tariffs US companies paid for imports from China). Official trade statistics also show that measured by value, about 73% of US apparel imports under free trade agreements came through USMCA (25%) and CAFTA-DR (48%) from 2019 to 2020.

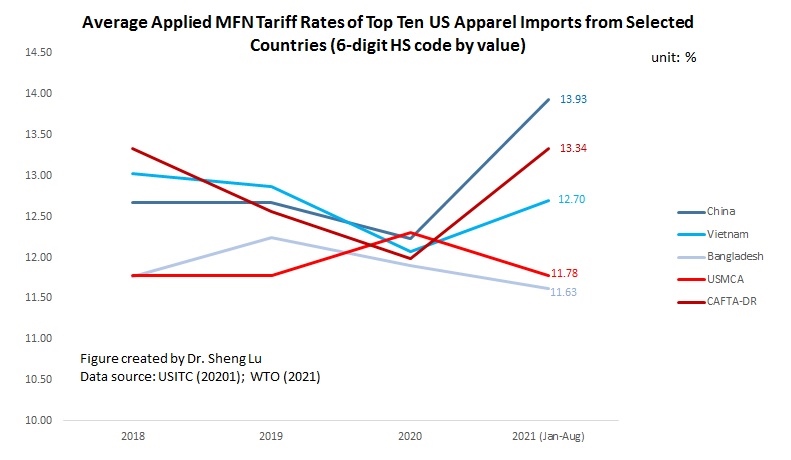

#3 US apparel imports from USMCA and CAFTA-DR members do NOT necessarily focus on items subject to a high tariff rate. Measured at the 6-digit HS code level, apparel items subject to a high tariff rate (i.e., applied MFN tariff rate >17%) only accounted for about 8-9% of US apparel imports from USMCA members and 7-8% imports from CAFTA-DR members. In comparison, even having to pay a significant amount of import duties, around 17% of US apparel imports from Vietnam and 10% of imports from China were subject to a high tariff rate (see table below).

The phenomenon suggests that USCMA and CAFTA-DR members still have limited production capacity for many man-made fibers(MMF) clothing categories (such as jackets, swimwear, dresses, and suits), typically facing a higher tariff rate. This result also implies that expanding production capacity and diversifying the export product structure could make USMCA and CAFTA-DR more attractive sourcing destinations.

#4 US apparel imports from USMCA and CAFTA-DR members tend to focus on large-volume items subject to a medium tariff rate. Specifically, from 2017 to 2021 (Jan-Aug), ten products (at the 6-digit HTS code level) typically contributed around half of the US tariff revenues collected from apparel items (HS chapters 61-62). However, the average applied MFN tariff rates for these items were only about 13%. Meanwhile, these top tariff-revenue-contributing apparel items accounted for about 50% of US apparel imports from USMCA members and nearly 64%-69% of imports from CAFTA-DR members.

Likewise, the top ten products (at the 6-digit HTS code level) typically accounted for 65%-68% of US apparel imports from USMCA members and nearly 73-75% of US apparel imports from CAFTA-DR members. These products also had a medium average applied MFN rate at 11-12% for USMCA and 12-13% in the case of CAFTA-DR.

Given the duty-saving incentives, expanding “near-sourcing” from USMCA and CAFTA-DR members could prioritize these large-volume apparel items with a medium tariff rate in short to medium terms. However, in the long run, a shortcoming of this strategy is that many such items are basic fashion clothing that primarily competes on price (such as T-shirts and trousers) and cannot leverage the unique competitive edge of near-sourcing (such as speed to market). When the US reaches new free trade agreements, particularly those involving leading apparel-producing countries in Asia, it could offset the tariff advantages enjoyed by USMCA and CAFTA-DR members and quickly result in trade diversion.

By leveraging theGlobalData Apparel Intelligence Center’s “Company Filing Analytics” tool, we took a detailed look at apparel companies’ latest efforts on addressing climate change. Specifically, we conducted a content analysis of annual and quarterly filings (e.g., 10-Q report and corporate annual report) submitted by over a hundred leading apparel companies worldwide from June 2020 to September 2021.

Key findings:

First, addressing climate change has become a more critical topic for apparel companies over the past five years. The percentage of apparel companies that mention “climate change” in their corporate filings nearly doubled from 43% in 2016 to 80% in 2020. Notably, different from the public perception, fast fashion brands like Inditex and H&M were among apparel companies that most frequently mentioned “climate change” in their corporate reports over that period.

Second, many apparel companies see their business risks associated with climate change growing. Results from GlobalData show that apparel companies are particularly concerned about potential supply chain disruption caused by climate change. Apparel companies are also concerned that climate change could increase their sourcing and production costs and hurt financials. As a leading fashion brand noted, “Disasters, climate change…may cause escalating prices or difficulty in procuring the raw materials (such as cotton, cashmere, down, etc.)”. Another added, “In the long term, the broader impacts of climate change may impact the cost and accessibility of materials used to manufacture products or other resources needed to operate business.”

Third, an increasing number of apparel companies have incorporated climate change into their corporate strategies or long-term business visions. Some apparel companies also established a dedicated office or governance structure to address climate change.

Further, apparel companies call for more detailed and transparent regulatory guidelines that can help them combat climate change. As one leading fashion brand commented, “Any assessment of the potential impact of future climate change legislation, regulations or industry standards, as well as any international treaties and accords, is uncertain given the wide scope of potential regulatory change in the countries in which we operate… As a result, the effects of climate change could have a long-term adverse impact on our business and the results of operations.”

In conclusion, addressing climate change is no longer a topic apparel companies can only ignore or treat as a marketing slogan. Instead, we are likely to see companies allocate more dedicated resources to this area in the long run, from human resources to research & development (R&D) spendings. Meanwhile, apparel companies may find it necessary and beneficial to effectively communicate their efforts and needs to address climate change with key stakeholders like consumers and public policymakers.

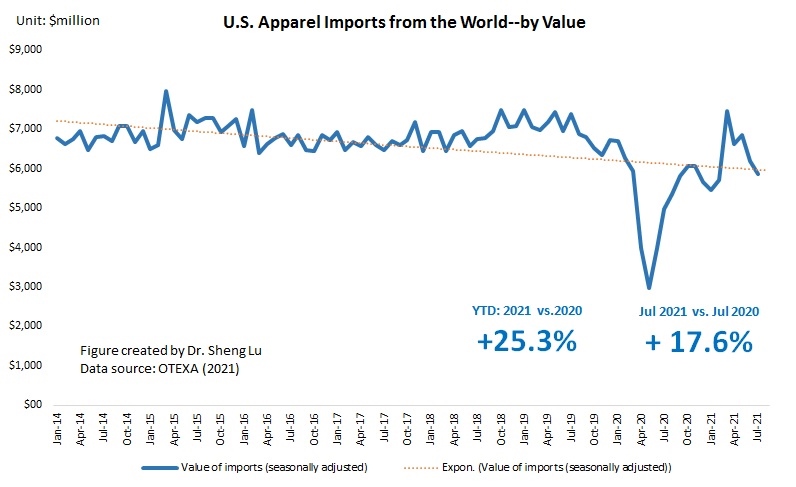

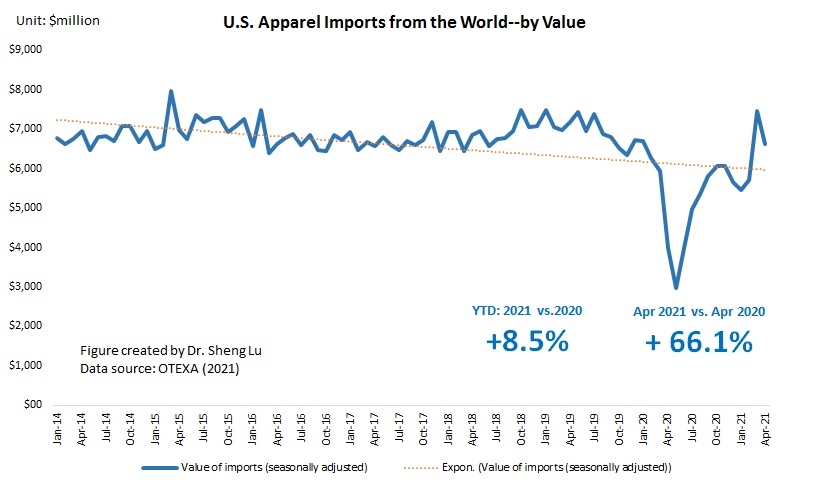

First, the shipping crisis and new wave of COVID cases start to affect US apparel imports negatively. While US consumers’ demand for clothing overall remains strong, for the second month in a row, the value of US apparel imports (seasonally adjusted) in July 2021 decreased by 5.5% from a month ago and down 9.7% from May to June. The absolute value of US apparel imports year to date (YTD) in 2021 (January—July) was 25.3% higher than in 2020 and around 87% of the pre-COVID level (benchmark: January-July, 2019). However, the year-over-year growth in July 2021 was only 15.4%, compared with 60.0% in May 2021 and 29.1% in June 2021. Overall, the results remind us that the market environment is far from stable yet as the COVID situation in the US and other parts of the world continues to evolve.

Second, Asian countries lost market shares as some leading apparel supplying countries, including Vietnam and Bangladesh, struggled with new COVID lockdowns. While Asia as a whole remains the single largest apparel sourcing base for US companies, Asian countries’ market shares fell from 74.2% in 2020 to 71.3% in July 2021, the lowest since 2010. The new COVID lockdowns in Vietnam and Bangladesh, the No. 2 and No. 3 top suppliers for the US market, post significant challenges to US fashion companies trying to build inventory for the upcoming holiday season. Notably, US companies source many high-volume products from these two countries, and there is a lack of alternative sourcing destinations in the short run.

Third, US companies continue to treat China as an essential sourcing base during the current challenging time. However, there is no clear sign that companies are reversing their long-term strategy of reducing “China exposure.” China stays the largest supplier for the US market in July 2021, accounting for 41.3% of total US apparel imports in quantity and 26.0% in value. The export product diversification index also suggests that China supplied the most variety of products to the US market. US apparel imports from Bangladesh, Mexico, and CAFTA-DR members are more concentrated on specific product categories. In other words, should China were under lockdowns, the negative impacts on US companies’ inventory management could be even worse.

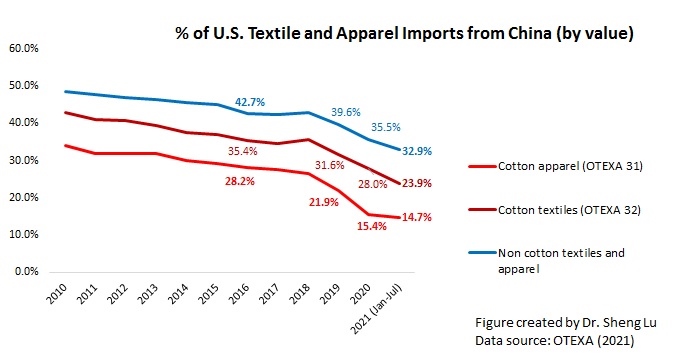

Nevertheless, the HHI index and market concentration ratios (CR3 and CR5) calculated based on the latest data suggest that US fashion companies continue to move their apparel sourcing orders from China to other Asian countries overall. For example, only 14.7% of US cotton apparel imports came from China in 2021 (January—July), a new record low in the past ten years. Further, as US apparel imports from China typically peak from June to September because of seasonal factors, China’s market shares are likely to drop in the next few months. Additionally, the fundamental concerns about sourcing from China are NOT gone. On the contrary, new US actions against alleged forced labor in Xinjiang are likely in the coming months and affect imports from China beyond cotton products.

Fourth, US apparel sourcing from the Western Hemisphere, especially CAFTA-DR members, gains new momentum. Specifically, 18.1% of US apparel imports came from the Western Hemisphere YTD in 2021 (January-July), higher than 16.1% in 2020 and 17.1% before the pandemic. Notably, CAFTA-DR members’ market shares increased to 11.2% in 2021 (January to July) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 58.4% growth in 2021 (January—July) from a year ago, one of the highest among all sourcing destinations. The imports from El Salvador (up 75.2%), Honduras (up 74.6%), Dominican Republic (45.1%), and Guatemala (40.6%) had grown particularly fast so far in 2021.

Meanwhile, US apparel imports from USMCA members stayed stable (i.e., no significant change in market shares). CAFTA-DR and USMCA members currently account for around 60% and 25% of US apparel imports from the Western Hemisphere. They are also the single largest export market for US textile products (about 70%).

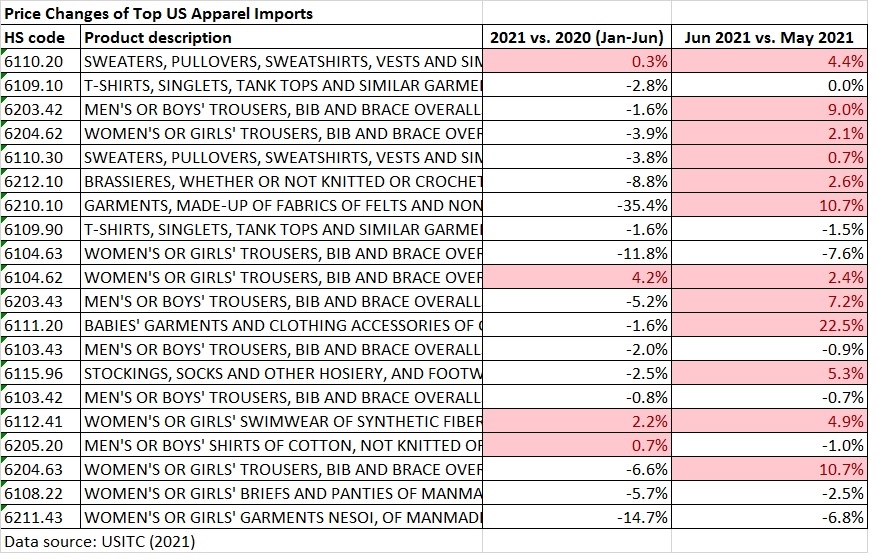

Fifth, US apparel imports start to see a notable price increase. While an across-the-board price increase was not a big concern at the beginning of 2021, the increase has become more noticeable since June 2021. For example, of the top 20 US apparel imports (HS chapters 61-62) at the 6-digit HS code level based on import value, the price of thirteen products increased from May to June 2021. The price increase at the country level is even more significant. From May to July 2021, the average unit price of US apparel imports from leading sources all went up substantially, including China (7%), Vietnam (13%), Bangladesh (13.9%), and India (15.6%).

As almost everything is becoming more expensive, from raw material, shipping to labor, the August and September trade data (to be released in October and November) could suggest an even more significant price increase.

According to the latest statistics released by the American Apparel and Footwear Association (AAFA):

In 2020, the US apparel and footwear industry directly employed about 3 million Americans and employed another 2.3 million indirectly.

In 2020, on average, every man, woman, and child in the United States spent $1,067.93 to buy 51.8 pieces of clothes and 5.8 pairs of shoes.

In 2020, US apparel and footwear production accounted for 3.5 percent and 2.3 percent of the US market, respectively.

Due to COVID-19, in 2020, US imports of apparel and footwear sank 16.4 percent and 23.5 percent, respectively. However, imports still supplied 96.5 percent of apparel and 97.7 percent of footwear available in the US market.

In 2020, the average effective tariff rate hit records for both apparel and footwear, reaching 15.5 percent and 13.0 percent, respectively.

The textile and apparel industry plays a significant role in Myanmar’s economy, particularly the export sector. Data from UNComtrade shows that textile and apparel accounted for nearly 69% of Myanmar’s total exports of manufactured goods in 2020, a substantial increase from only 27% in 2011. Data from the International Labor Organization (ILO) also indicates that the textile and industry (ISIC 17 & 18) employed more than 1.1 million workers in Myanmar in 2019, up from 0.69 million in 2015. Most garment workers in Myanmar are women today (around 87%).

Since the United States lifted the import ban on Myanmar and the EU reinstated the Everything But Arms (EBA) trade preferences in 2013, Myanmar was one of the most popular emerging apparel sourcing bases among fashion companies. From 2020 to July 2021, some of the top fashion brands that carry “Made in Myanmar” apparel items include United Colors of Benetton, Next, Only, H&M, Guess, and Jack & Jones.

Thanks to foreign investment (note: nearly half of Myanmar’s garment factories are foreign-owned), Myanmar specializes in making relatively higher-quality functional/technical clothing (i.e., outwear like jackets and coats. Here is an example). This is different from many other apparel-exporting countries like Bangladesh, Vietnam, and Cambodia, mostly exporting low-cost tops and bottoms.

However, the latest trade data shows that Myanmar’s military coup that broke out in early 2021 had hurt the country’s apparel exports significantly. According to the US International Trade Commission (USITC), even though the total US apparel imports enjoyed a robust recovery in the first half of 2021 (up nearly 27%), the value of US apparel (HTS chapters 61 and 62) imports from Myanmar dropped by 0.4%. Almost ALL Myanmar’s top apparel exports to the US suffered a substantial decline or much slower growth in 2021 than the trend BEFORE the military coup (see the Table above). As US fashion companies switch sourcing orders from Myanmar to other suppliers, Myanmar’s market shares fell from 0.5% in 2020 to only 0.3% in the first half of 2021.

Highly consistent with the trade data, according to the 2021 Fashion Industry Benchmarking Study, many surveyed US fashion companies expressed concerns about the military coup in Myanmar and the rising labor and social compliance risks when sourcing from the country. Some respondents explicitly say they are leaving because of the current situation. “(We) have terminated sourcing from Myanmar due to instability.” says one respondent. Another adds, “We had orders in Myanmar that have already been moved to Cambodia. We are unlikely to place orders until the current situation is resolved.”

In another recent study, we find that apparel sourcing is not merely about “competing on price.” Instead, fashion companies give substantial weight to the factors of “political stability” and “financial stability” in their sourcing decisions today. In other words, the reputation risks matter for sourcing.

Unfortunately, the situation could get worse. The international community, including the US and the EU, is considering new sanctions against Myanmar, including suspending Myanmmar’s trade-preference program eligibility.

Designated as a “least developed country” (LDC) by the World Trade Organization, Myanmar’s apparel exports enjoy duty-free market access in the EU, Japan, and South Korea. These countries also, in general, offer very liberal “single transformation” (or commonly known as cut and sew) rules of origin for qualifying apparel made in Myanmar. This explains why Myanmar’s apparel exports mostly go to the EU (56%), Japan, and South Korea (around 30%).

The United States is another important export market for Myanmar, accounting for 7% of the country’s total apparel exports in 2020. As a beneficiary of the US Generalized System of Preferences (GSP) program, Myanmar’s luggage exports enjoy duty-free benefits in the US market. However, the US GSP program excludes textile and apparel products, meaning Myanmar’s apparel exports to the US still are subject to the regular Most-Favored-Nation (MFN) tariff rate at around 14.3% on average in 2020.

Further, given Myanmar’s highly concentrated apparel export markets and the pandemic, it will be challenging for Myanmar’s garment producers to find alternative apparel export markets in a relatively short period. For example, although China is recognized as one of the world’s largest and fastest-growing emerging import markets, only 1.4% of Myanmar’s apparel exports went to China in 2020.

According to the World Trade Statistical Review 2021 report released by the World Trade Organization (WTO), the textiles and apparel trade patterns in 2020 include both continuities and new trends affected by the pandemic and companies’ evolving production and sourcing strategies in response to the shifting business environment.

Pattern #1: COVID-19 significantly affected the world textile and apparel trade volumes, resulting in substantial growth of textile exports and a declined demand for apparel.

Driven by increased personal protective equipment (PPE) production, global textile exports grew by 16.1% in 2020, reaching $353bn. In comparison, affected by lockdown measures, worsened economy, and consumers’ tighter budget for discretionary spending, global apparel export decreased by nearly 9% in 2020, totaling $448bn, the worst performance in decades. The apparel sector is not alone. The world merchandise trade in 2020 also suffered an unprecedented 8% drop from a year ago, with COVID-19 to blame.

Notably, as economic activities returned in the second half of 2020, the world clothing export quickly rebounded to around 95% of the pre-covid level by the end of 2020. That being said, the unexpected resurgence of COVID cases in summer 2021, especially the delta variant, caused new market uncertainties. Overall, the world textile and apparel trade recovery process from COVID-19 will differ from our experiences during the 2008 global financial crisis.

Pattern #2: COVID-19 did NOT shift the competitive landscape of the world textile exports; Meanwhile, textile exports from China and Vietnam gained new momentum during the pandemic.

China, the European Union (EU), and India remained the world’s three largest textile exporters in 2020. Together, these top three accounted for 65.8% of the world’s textile exports in 2020, similar to 66.9% before the pandemic (2018-2019).

Notably, China and Vietnam enjoyed a substantial increase in their textile exports in 2020, up 28.9% and 10.7% from a year ago, respectively. The complete textile and apparel supply chain and considerable production capability allow these two countries to switch clothing production to PPE manufacturing quickly. In particular, Vietnamexceeded South Korea and ranked the world’s sixth-largest textile exporter in 2020 ($10 bn of exports), the first time in history.

The United States dropped one place and ranked the world’s fifth-largest textile exporter in 2020 (was 4th from 2015 to 2019), accounting for 3.2% of the shares (was 4.4% in 2019). Production disruptions at the beginning of the pandemic and the shift toward PPE production for domestic consumption were the two primary contributing factors behind the decline in U.S. textile exports. Due to the regional trade patterns, around 67% of U.S. textile exports went to the Western Hemisphere in 2020, including 46% for members of the U.S.-Mexico-Canada Trade Agreement (USMCA) and another 17.2% for members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR).

Pattern #3: Fashion companies’ efforts to diversify apparel sourcing from China somehow slowed during the pandemic.

China, the European Union, Vietnam, and Bangladesh unshakably remained the world’s four largest apparel exporters in 2020. Altogether, these top four accounted for 72.2% of the world market shares in 2020, higher than 71.4% in 2019.

Notably, while China steadily accounted for declining shares in the world’s total apparel exports since 2015, its market shares rebounded to 31.6% in 2020 from 30.7% in 2019. We can observe a similar pattern in Canada (up from 36.2% to 41.2%) and the EU (31.2% to 31.3%), two of the world’s leading apparel import markets. Even in the U.S. market, where Chinese goods face adverse impacts of the tariff war, the market shares of “Made in China” only marginally decreased from 30.8% in 2019 to 29.8% in 2020, compared with a more significant drop before the pandemic (i.e., fell from 34.4% 2018 to 30.8% in 2019).

Several factors could explain the resilience of China’s apparel exports: 1) fashion brands and retailers’ particular sourcing criteria match China’s competitiveness during the pandemic (e.g., flexibility, agility, and total landed sourcing cost). 2) China has one of the world’s most complete textile and apparel supply chains, allowing garment factories to access textile raw material and accessories locally. 3) Compared with many other apparel exporting countries, China suffered a shorter COVID lockdown period and resumed apparel production earlier and more quickly. Most Chinese textile and apparel factories started to reopen in April 2020, and they resumed an overall 90%-95% operational capacity rate by July 2020.

Nonetheless, fashion companies are NOT reversing their long-term strategies to reduce “China exposure” for apparel sourcing. On the contrary, non-economic factors, particularly the concerns about forced labor in China’s Xinjiang region, push most western fashion brands and retailers to develop apparel sourcing capacities beyond China. Meanwhile, no single country has yet and will likely become the “Next China” because of capacity limits. Instead, from 2015 to 2020, China’s lost market shares in the world apparel exports (around 7.8 percentage points) were picked up jointly by its competitors in Asia, including ASEAN members (up 4.4 percentage points), Bangladesh (up 1.3 percentage points), and Pakistan (up 0.3 percentage point). Such a trend is most likely to continue in the post-COVID world.

Pattern #4: Developed economies led textile PPE imports during the pandemic, whereas the developing countries imported fewer textiles as their apparel exports dropped.

On the one hand, the value of textile imports by developed economies, including EU members, the United States, Japan, and Canada, surged by more than 30 percent in 2020, driven mainly by their demand for PPE. The result also reveals the significant contribution of international trade in supporting the supply and distribution of textile PPE globally. On the other hand, the developing countries engaged in apparel production and export drove the import demand for textile raw materials like yarns and fabrics. However, most of these developing countries’ textile imports fell in 2020, corresponding to their decreased apparel exports during the pandemic.

Pattern #5: Despite COVID-19, the world apparel import market continues to diversify. The import demand increasingly comes from emerging economies with a booming middle class.

Affected by consumers’ purchasing power (often measured by GDP per capita) and the size of the population, the European Union, the United States, and Japan remained the world’s three largest apparel importers in 2020, a stable pattern that has lasted for decades. While these top three still absorbed 56.2% of the world’s apparel imports in 2020, it was a new record low in the past ten years (was 58.1% in 2019 and 61.5% in 2018), and much lower than 84% back in 2005.