Event summary by Mariel Abano (FASH455 student, Spring 2022)

COVID-19 and other external shocks such as the Ukraine-Russia war shifted the fashion supply chain from its conventional low-cost model. In response to the changes, brands and companies focus on flexibility, strengthening their relationships with suppliers, and sustainability.

Regarding the pandemic’s impacts on the apparel supply chain, fashion brands need to be more future-oriented to better prepare for unexpected market shocks that may come up in the fluctuating world. Flexibility within their merchandising teams allowed Neiman Marcus to pivot during the pandemic and market differently within the context of the pandemic. The company explored new ways to connect with its consumers via digital platforms as many physical stores closed. However, fashion companies need to be flexible enough to respond to the increasing demand from its growing e-commerce platform. This is not always easy to happen.

Likewise, Reformation tries its best to predict demand, build supply chain capacity, and manage lead time during COVID-19. Their manufacturing chains within the U.S. and vertical integration helped them respond quickly to supply chain disruptions. As a result, the company pivoted quickly to athleisure even though its brand is typically known for its event-wear dresses.

Meanwhile, when evaluating their supply chain, Amanda Martin explains that Neiman Marcusprioritizes labor, speed, and cost. With this, there is a balance between investment of capital and resources and mitigating costs like surging fuel prices.

The relationship with vendors also matters during the pandemic. For example, Neiman Marcus’s relationships with its vendors built over the years allowed the company to move more quickly from ocean to air shipping during the pandemic. In the discussion, Amanda Martin explained why the relationship between retailers/brands and manufacturers needs to help both sides grow and benefit. Likewise, Reformation also focuses on people and their relationships with their suppliers during the pandemic. Kathleen Talbot emphasizes that brand-supplier relationships are evolving. Fostering two-way conversations is key to moving away from the previous model that prioritized the needs and wants of the brand over the manufacturer.

Sustainability is NOT ignored during the pandemic. For example, fashion companies increasingly use technology and process management to take accountability for supply chains and improve traceability. In terms of environmental impact, there are more applications within sourcing emphasizing recycled and renewable materials. For example, Reformation recently launched a new circularity initiative that focuses on extending a product’s lifetime and then recycling that back into the system. When creating new styles, the company started from sustainable fibers. Further, they hope to shift transportation from air to other means to minimize their carbon footprint.

Trade and sourcing play a critical role in building a more sustainable fashion apparel supply chain. Below are recent FASH455 blog posts addressing climate change, sustainability, recycling, and transparency issues. Feel free to join our online discussion and share your ideas on improving sustainable, ethical, and more socially responsible sourcing.

Japan has one of the world’s largest apparel consumption markets, with retail sales totaling USD$100bn in 2021, only after the United States (USD$476bn) and China (USD$411bn). Meanwhile, like many other developed economies, most apparel consumed in Japan are imported, making the country a considerable sourcing and market access opportunity for fashion companies and sourcing agents around the globe.

Japanese fashion companies primarily source apparel from Asia. Data shows that Japanese fashion brands and retailers consistently imported more than 90% of clothing from the Asia region, much higher than their peers in the US (about 75%), the EU (50%), and the UK (about 60%). This pattern reflects Japan’s deep involvement in the Asia-based textile and apparel supply chain.

Notably, Japan’s apparel imports from Asia often contain textile raw materials “made in Japan.” Data shows that in 2021, about 65% of Japan’s yarn exports, 75% of woven fabric exports, and 90% of knit fabric exports went to the Asia region, particularly China and ASEAN members. Understandably, in Japan’s apparel retail stores, it is not rare to find clothing labeled “made in China” or “Made in Vietnam” but include phrases like “high-quality luster unique to Japanese fabrics” and “with Japanese yarns” in the product description.

The Global value chain analysis further shows that of Japan’s $5.32 billion gross textile exports in 2017, around 34% (or $1.79 billion) contributed to export production in other economies, mainly China ($496 million), Vietnam ($288 million), South Korea ($98 million), and Taiwan ($92 million).

China remains Japan’s top apparel supplier at the country level. However, Japanese fashion brands and retailers have been diversifying their sourcing base. Since the elimination of the quota system in 2005, China, for a long time, was the single largest apparel supplier for Japan, with an unparalleled market share of more than 80% measured by value. However, as “Made in China” became more expensive, among other factors, China’s market share dropped to 56.4% in 2021. Japanese fashion brands and retailers actively seek China’s alternatives like their US and EU counterparts. Notably, Japan’s apparel imports from Vietnam, Bangladesh, and Indonesia have grown particularly fast, even though their production capacity and market shares are still far behind China’s.

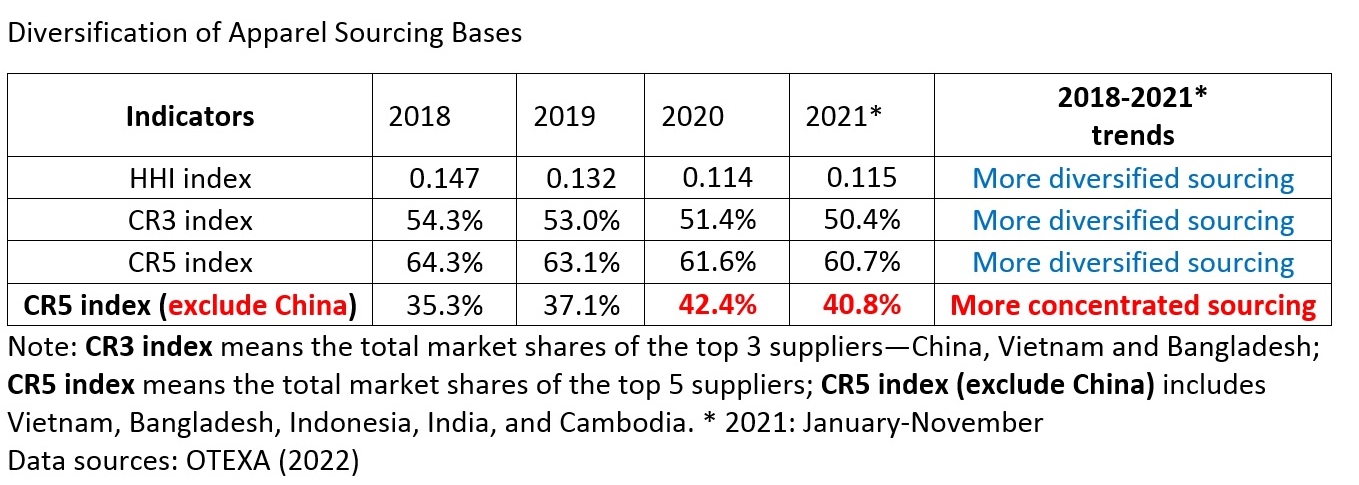

As Japanese fashion companies source from more places, the total market shares of the top 5 apparel suppliers, not surprisingly, had dropped from over 94% back in 2010 to only 82.3% in 2021, measured by value. Similarly, the Herfindahl-Hirschman Index (HHI), commonly used to calculate market concentration, dropped from 0.64 in 2011 to 0.35 in 2021 for Japan’s apparel imports. In other words, Japanese fashion companies’ apparel sourcing bases became ever more diverse.

Fast Retailing Group’s apparel sourcing base (Data source: Open Apparel Registry)

We can observe the same pattern at the company level. For example, the Fast Retailing Group, the largest Japanese apparel retailer which owns Uniqlo, used to source nearly 100% of its products from China. However, as of 2021, the Fast Retailing Group sourced finished apparel from over 550 factories in more than 20 countries. While about half of these factories were in China, the Fast Retailing Group had strategically developed production capacity in Vietnam, Bangladesh, Indonesia, and India. On the other hand, in April 2021, the Fast Retailing Group opened a 3D-knit factory in Shinonome, allowing the company to re-shoring some production back to Japan.

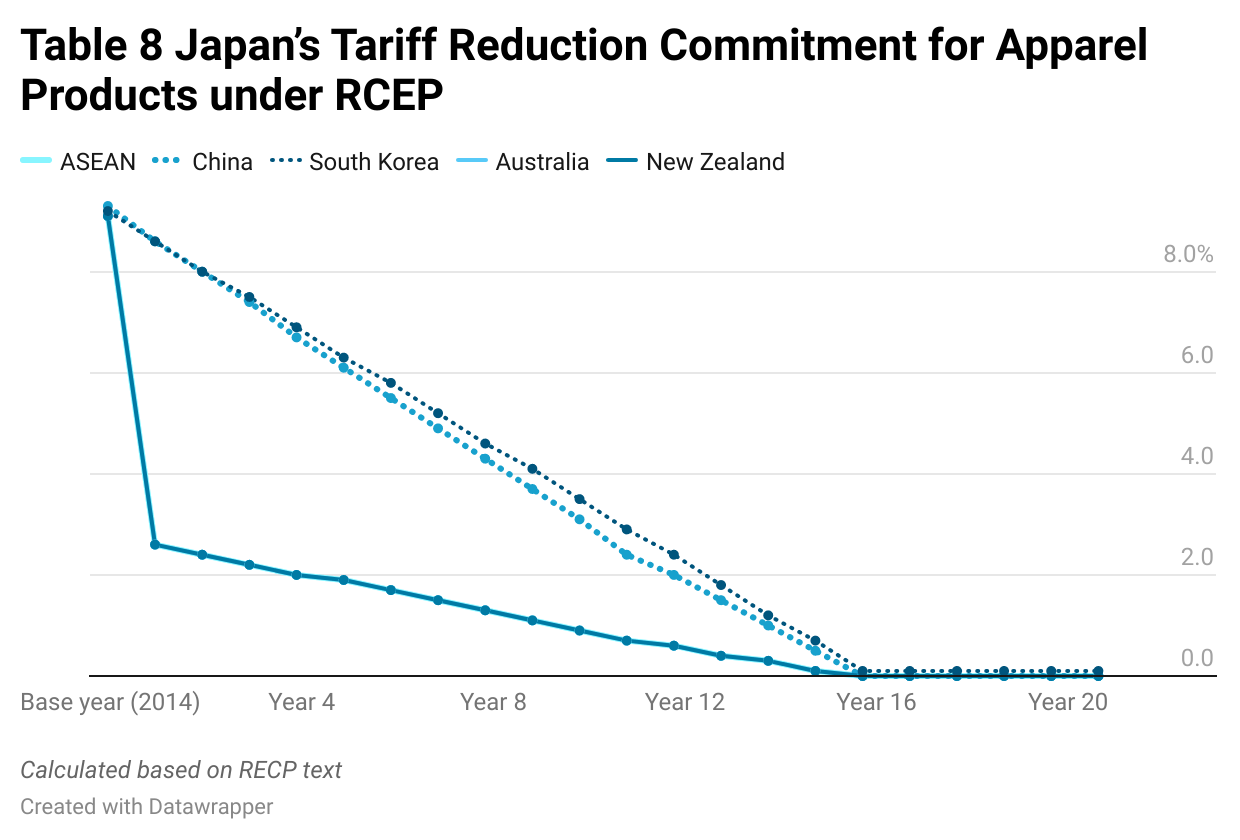

Additionally, Japan is a member of the Regional Comprehensive Economic Partnership (RCEP), the world’s most economically influential free trade agreement. Notably, Japan commits to reducing its apparel import tariffs to zero for RCEP members following a 21-year phaseout schedule. However, as Table 8 shows, Japan’s tariff cut for apparel products is more generous toward ASEAN members and less for China and South Korea due to competition concerns. For example, by 2026, Japan’s average tariff rate will be reduced from 9.1% today to only 1.9% for apparel imports from ASEAN members but will remain above 6% for imports from China. Given the tariff difference, it can be highly expected that ASEAN members such as Vietnam could become more attractive sourcing destinations for Japanese fashion companies.

The full study is available here(need Just-Style subscription)

By leveraging production and trade statistics from government databases, we examined the critical trends of US textile manufacturing and supply. Particularly, we try to understand the strengths and weaknesses of the United States as a textile raw material supplier for domestic garment manufacturers and those in the Western Hemisphere. Below are the key findings:

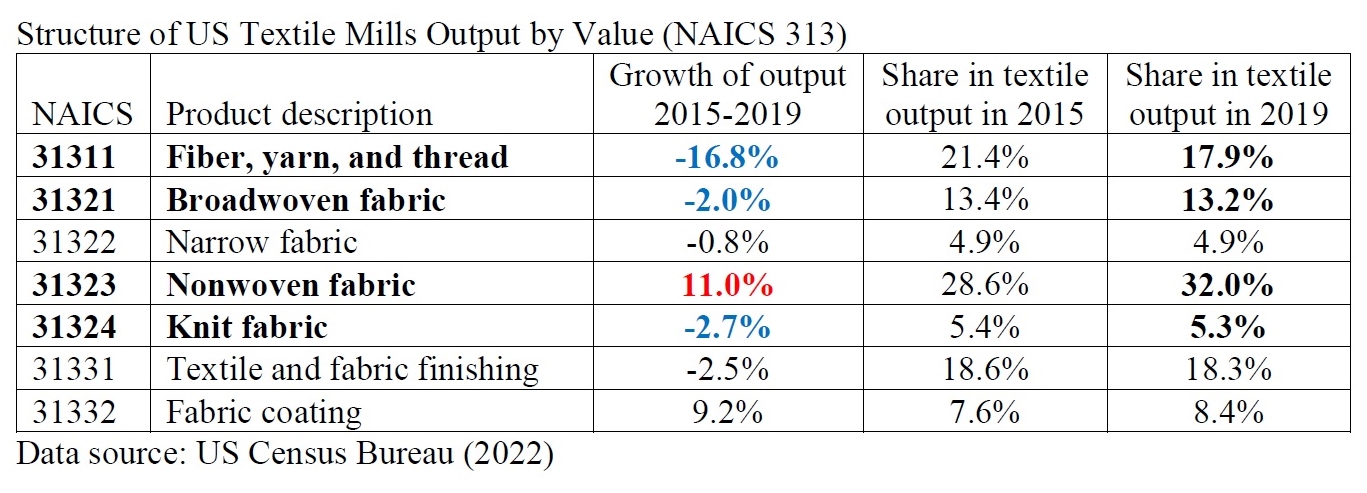

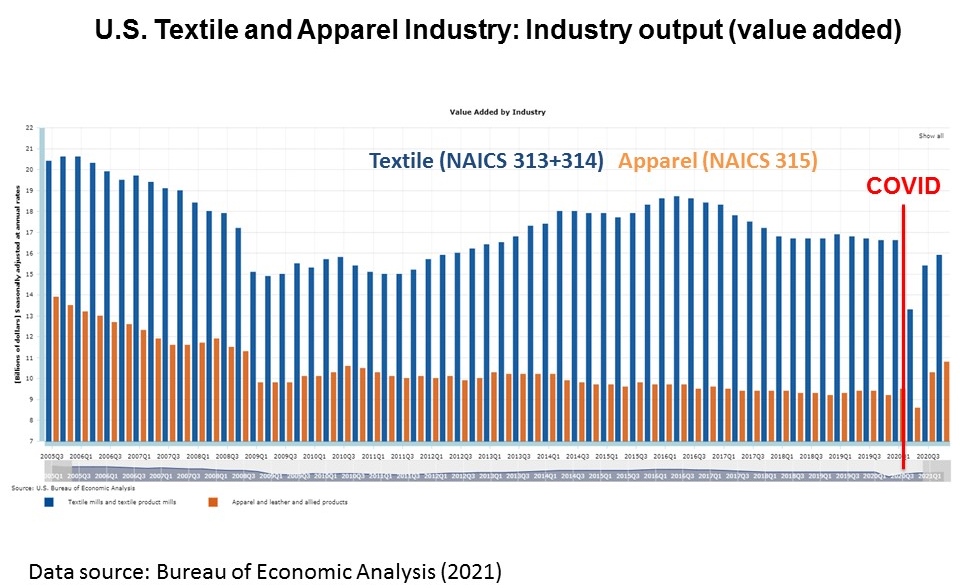

First, fiber, yarn, and thread manufacturing is a long-time strength in the US, whereas fabric production is much smaller in scale. Specifically, fiber, yarn, and thread (NAICS 31311) accounted for nearly 18% of US textile mills’ total output in 2019. In comparison, less than 13% of the production went to woven fabrics (NAICS 31321) and only about 5% for knit fabrics (NAICS 31324).

Second, the US textile industry shifts to make more technical textiles and less apparel-related yarns, fabrics, and other raw materials. Data shows that from 2015 to 2019, the value of US fiber, yarn, and thread manufacturing (NAICS code 31311) dropped by as much as 16.8 percent. Likewise, US broadwoven fabric manufacturing (NAICS code 31321) and knit fabric (NAICS code 31324) decreased by 2.0 percent and 2.7 percent over the same period. Labor cost, material cost, and capital expenditure are critical factors behind the structural shift of US textile manufacturing.

Third, the structural change of US textile manufacturing directly affects the role of the US serving as a textile supplier for domestic apparel producers and those in the Western Hemisphere.

On the one hand, the US remains a critical yarns and threads supplier in the Western Hemisphere. For example, from 2010 to 2019, the value of US fibers, yarn and threads exports (NAICS31311) increased by 25%, much higher than other textile categories. Likewise, in 2021, fibers, yarns, and threads accounted for about 23.3% of US textile exports, higher than 21.0% in 2010. Additionally, nearly 40% of Mexico and CAFTA-DR members’ yarn imports in 2021 (SITC 651) still came from the US, the single largest source. This trend has stayed stable over the past decade.

On the other hand, the US couldn’t sufficiently supply fabrics and other textile accessories for garment producers in the Western Hemisphere, and the problem seems to worsen. Corresponding to the decline in manufacturing, US broadwoven fabric (NAICS 31321) and knit fabric (NAICS 31324) exports decreased substantially.

The US also plays a declining role as a fabric and textile accessories supplier for garment factories in the Western Hemisphere. Garment producers in Mexico and CAFTA-DR members had to source 60%-80% of woven fabrics and 75-82% of knit fabrics from non-US sources in 2021. Likewise, only 40% and 14.6% of Mexico and CAFTA-DR members’ textile accessories, such as labels and trims, came from the US in 2021.

Likewise, the limited US fabric supply affects the raw material sourcing of domestic apparel manufacturers. For example, according to the “Made in the USA” database managed by the Office of Textiles and Apparel (OTEXA), around 36% of US-based apparel mills explicitly say they use “imported material,” primarily fabrics.

The study’s findings echo some previous studies suggesting that textile raw material supply, especially fabrics and textile accessories, could be the single most significant bottleneck preventing more apparel “Made in the USA” and near-sourcing from the Western Hemisphere.

Meanwhile, how to overcome the bottleneck could trigger heated public policy debate. For example, US policymakers could encourage an expansion of domestic fabric and textile accessories manufacturing as one option. However, to make it happen takes time and requires substantial new investments. Also, economic factors may continue to favor technical textiles production over apparel-related fabrics in the US.

As an alternative, US policymakers could make it easier for garment producers in the Western Hemisphere to access their needed fabrics and textile accessories outside the US, such as improving the rules of origin flexibility in CAFTA-DR or USMCA. But this option is likely to face strong opposition from US yarn producers and be politically challenging to implement.

(About the authors: Dr Sheng Lu is an associate professor in fashion and apparel studies at the University of Delaware; Anna Matteson is a research assistant in fashion and apparel studies at the University of Delaware).

(The following comments are from students in FASH455 based on the readings)

Yes, US fashion companies should continue to diversify their apparel sourcing bases in 2022 because…

“It is said that you never keep all your eggs in one basket. If something happens in one of the countries that brands are sourcing from, whether it’s economically or politically, their business could be in jeopardy because they have no other sourcing bases anywhere else. As we see now with the Russian and Ukraine War, anything can happen at any time, and huge businesses like Mcdonalds and Starbucks have shut down their stores in Russia. Having connections in the business world is what takes a company further and makes them wealthier.

“The demand for sustainability and transparencyis only rising from consumers and this is causing brands to need to take accountability and action for more ethical sourcing. In order for brands to find factories that will work with the stricter regulations and policies, it may require them to find different and new locations and countries to work with.”

“The pandemic proved to be detrimental to brands only sourcing from a few countries. Pandemic lockdowns and government restrictions were harmful to companies that did not have a diverse sourcing base… A diverse sourcing base will allow companies to have the ability to continue to source new products in case of government lockdowns in other sourcing nations.”

“I think that US fashion companies should continue to diversify their sourcing base in 2022 to benefit other developing countries who are looking to build their economy. The majority of apparel sourcing is done out of China and Vietnam. A diverse apparel sourcing base would be a great way to take the heat off of these countries and benefit others.”

“I think fashion companies should continue to diversify their sourcing bases because it can help them remain competitive while stillkeeping costs down. Keeping costs down can also help prevent giant unpredictable spikes. Lastly, the company will have more flexibility if they are diverse because they won’t be relying on a single source and won’t run into issues if that single source fails.”

“I understand the argument that it is easier for smaller companies to produce solely in China seeing as it can be seen as a one-stop-shop. I also understand why some companies are looking to bring their sourcing closer together and closer to home to mitigate some of the sourcing costs. However, I find this view to be short-sighted and will be detrimental to companies in the long run. As we saw with the pandemic, diversification is helpful in the wake of disaster. If one country is suffering from a natural, economic, or political disaster it would be helpful to have production capabilities in other countries. This way if production is shut down in one country, it is not as detrimental to obtaining products because you can lean on the factories in other countries. I personally would rather wait out the incredibly high costs, which will hopefully go down soon, and keep my sourcing base diversified to be better prepared for unforeseen challenges in the future.”

No, US fashion companies should consolidate their apparel sourcing bases in 2022 because…

“US companies need to work on reducing the number of factories to increase sustainability and labor efforts. It would not be beneficial for the industry to continue to expand their sourcing bases, as that allows for less transparency with consumers. By diversifying their sourcing base they are proving to their consumers they only care about costs and how their clothing is affecting the environment.”

“I do not think US fashion companies should continue to diversify their sourcing base in 2022. These fashion companies should rather focus on nearshoring and local-to-local supply chain. Many retailers are interested in nearshoring as it helps eliminate the need to order months ahead, as the merchandise will have a shorter distance to travel. On top of this, many consumers want transparency and fast delivery. By sourcing more locally, fashion companies will be able to provide shorter shipping times as well as be more aware of sustainability in the supply chain and will then be able to relay the information to the consumers.”

“The very diverse sourcing base is exactly why some fashion companies struggled with supply chain disruptions and shipping delays. As the business environment remains highly uncertain, why not cut ties with some high-risk countries and only source products from the most secure and stable sourcing bases?”

“The present sourcing techniques used by US fashion corporations need to be refined and improved. The number of factories used for sourcing has to be reduced in order to improve sustainability and labor efforts. Increasing the number of sourcing bases does not benefit the industry since it reduces customer trust in the supply chain.”

“From trade data, it seems the top apparel suppliers to the US market barely changed—China, Vietnam, Bangladesh, Cambodia, Indonesia, or India. So, realistically, if a company intends to diversify sourcing, where else can they go?”

“During the pandemic, many US companies focused on strengthening their relationships with key vendors to gain a competitive advantage to achieve more flexibility in sourcing. It worked, then why companies should give up this strategy in 2022? Also, I think it would be wise for fashion companies to give MORE rewards to business partners that helped them survive the difficult times, rather than give sourcing orders to “new vendors”…further, using long-term loyalty and fiscal leverage with strategic business partners as an advantage could prove to be a good option for companies looking to obtain high production capacity, low prices, flexibility, and speed to market from their suppliers.”

Discussion questions:

Which side do you agree with or disagree with and why? What is your recommendation for US fashion companies regarding their apparel sourcing diversification strategies in 2022? Please join our online discussion and leave your comments.

Question #2: Primark sources from 28 countries work with around 928 contracted factories. What are the pros and cons of using such a diverse sourcing base?

Question #3: Near-shoring, meaning bringing manufacturing closer to home, is growing in popularity. Does it mean globalization is “in retreat”? What is your view?

Question #4: In the current state of the fashion industry, ethical labor laws are really important, especially to consumers. For example, activists are protesting Pretty Little Thing in London to protest the low wages paid to garment workers at the factories that Pretty Little Thing sources from. With this in mind, do you think that it would be wise for Primark to look for sourcing opportunities outside of Asia? Or do you believe Primark’s Ethical Trade and Environmental Sustainability team is sufficient to ensure ethical and sustainable sourcing?

Question #5: As of May 2021, Primark has the most workers in its Asian factories. Should we still call Primark an EU company? Does a company’s national identity still matter in today’s globalized world?

(Welcome to our online discussion. For students in FASH455, please address at least two questions and mention the question number (#) in your reply)

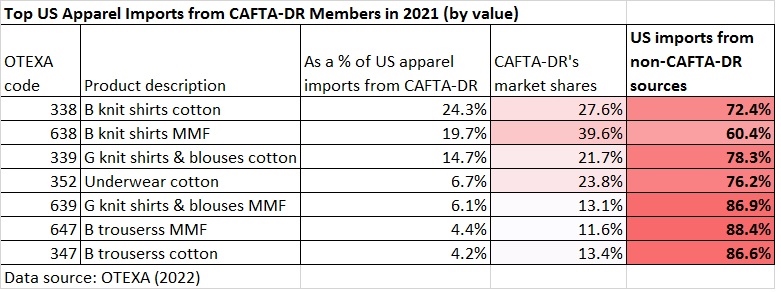

As US fashion companies diversify their sourcing from Asia, near-sourcing from the Western Hemisphere, particularly members of the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) seems to benefit. According to the latest trade data from the Office of Textiles and Apparel (OTEXA), US apparel companies placed relatively more sourcing orders with suppliers in the Western Hemisphere in 2021. For example, CAFTA-DR members’ market shares increased by 0.31 percentage points in quantity and nearly one percentage point in value compared with a year ago.

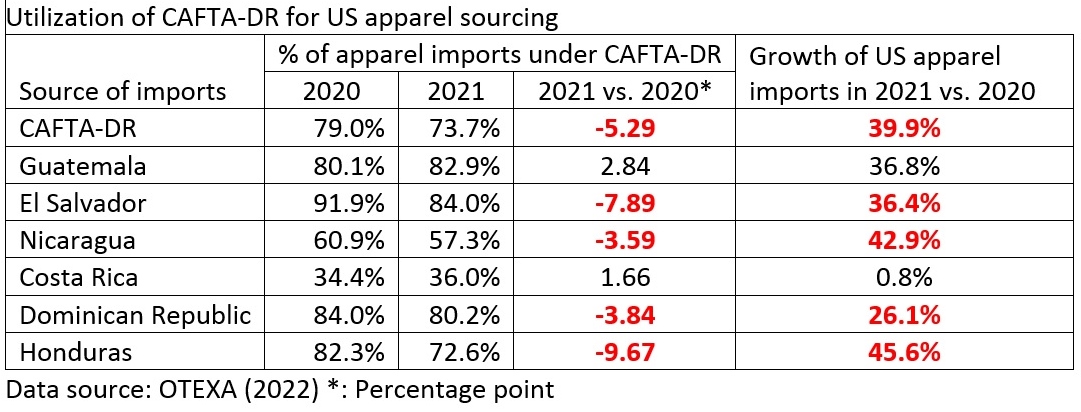

However, it is concerning to see the utilization rate of CAFTA-DR for apparel sourcing fall to a new record low of only 73.7% in 2021. This means that as much as 26.3% of US apparel imports from CAFTA-DR members did NOT claim the duty-free benefits.

The lower free trade agreement (FTA) utilization rate became a problem, particularly among CAFTA-DR members with fast export growth to the US market in 2021. For example, whereas US apparel imports from Honduras enjoyed an impressive 45.6% growth in 2021, only 72.6% of these imports claimed the CAFTA-DR duty benefits, down from 82.3% a year ago. We can observe a similar pattern in El Salvador, Nicaragua, and the Dominican Republic.

The phenomenon is far from surprising, however. For years, US fashion companies have expressed concerns about the limited textile supply within CAFTA-DR, especially fabrics and textile accessories. The lack of textile supply plus the restrictive “yarn-forward” rules of origin in the agreement often creates a dilemma for US fashion companies: either source from Asia entirely or source from CAFTA-DR but forgo the duty-saving benefits.

Likewise, because of a lack of sufficient textile supply within the region, US apparel imports from CAFTA-DR members become increasingly concentrated on basic fashion items, typically facing intense competition with many alternative sourcing destinations. For example, measured in value, over 80% of US apparel imports from CAFTA-DR members in 2021 were shirts, trousers, and underwear. However, US companies import the vast majority (70%-88%) from non-CAFTA-DR sources for these product categories.

Understandably, it will be unlikely to substantially expand US apparel sourcing from CAFTA-DR members without solving the textile supply shortage problem facing the region.

According to the video, how has the supply chain for apparel and footwear changed over the past decade?

What are the pros and cons of moving from a global supply chain to a regional one for fashion companies?

For fashion companies interested in “near-shoring” and “re-shoring”, what factors should they consider? Why?

Anything else you find interesting/intriguing/thought-provoking/debatable in the video? Why?

Note: Everyone is welcome to join our online discussion. For students in FASH455, please address at least two questions. Please mention the question number # (no need to repeat the question) in your comment.

First, US apparel imports continue to rebound in November 2021 as companies build the inventory for the holiday season. Thanks to US consumers’ strong demand and the upcoming holidays, the value of US apparel imports went up by 15.7% in November 2021 from a month ago (seasonally adjusted) and increased by as much as 39.7% from 2020. However, before the pandemic, the value of US apparel imports always peaked in October and then gradually slipped in November and December. The unusual surge of imports in November 2021 could be the combined effects of price inflation and the late arrival of goods due to the shipping crisis.

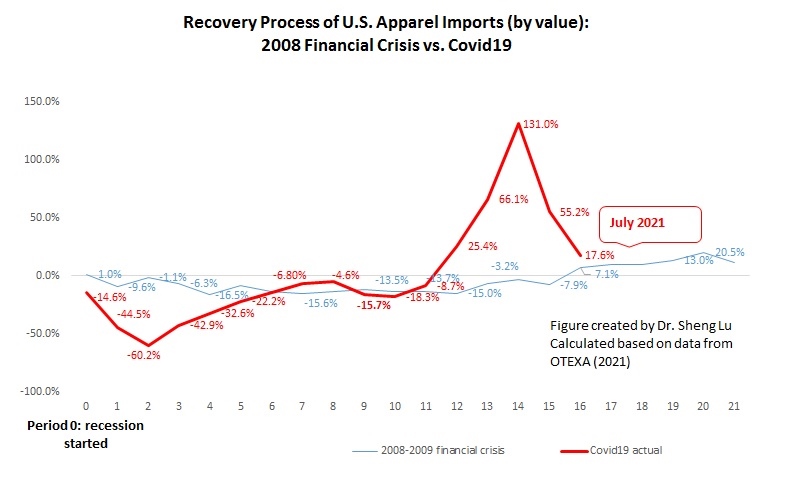

Meanwhile, US apparel imports so far in 2021 have been far more volatile than in the past few years because of uncertainties and disruptions caused by COVID-19 and the shipping crisis. For example, the year-over-year (YoY) growth rate ranged from 131% in May to 17.6% in July, causing fashion companies additional inventory planning and supply chain management challenges. Unfortunately, the new omicron variant could worsen the market uncertainty and volatility.

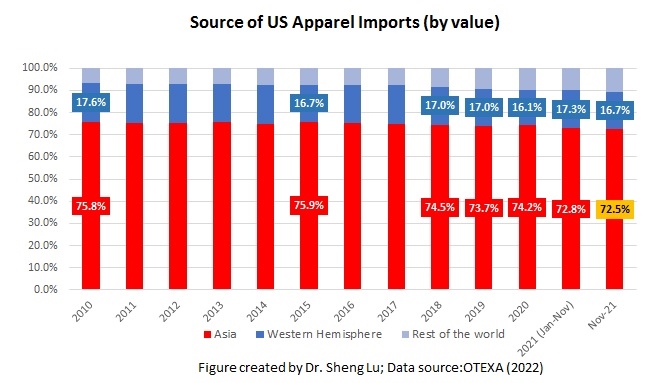

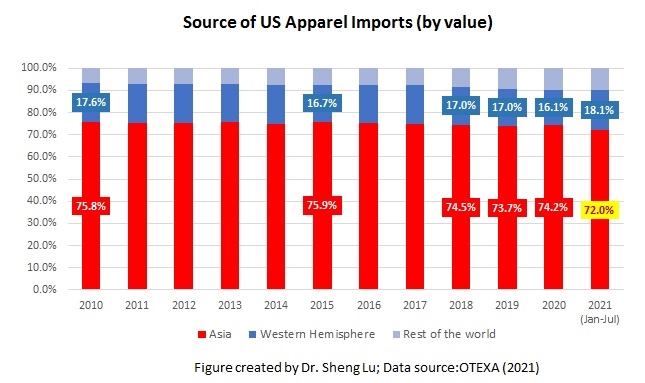

Second, Asian countries remain the dominant sourcing base for US fashion companies as the production capacity elsewhere is limited. Asian countries’ market shares fell from 74.2% in 2020 to 71.3% in July 2021, primarily because of the COVID lockdowns in Vietnam and Bangladesh. US apparel imports came from Asian countries rebounded to 74.8% and 72.5% in October and November 2021, respectively. This result suggests a lack of alternative sourcing destinations outside Asia, especially for large volume items. Meanwhile, the worsening shipping crisis affecting the route from Asia to North America could explain why Asian suppliers’ market shares in November were somewhat lower than a month ago.

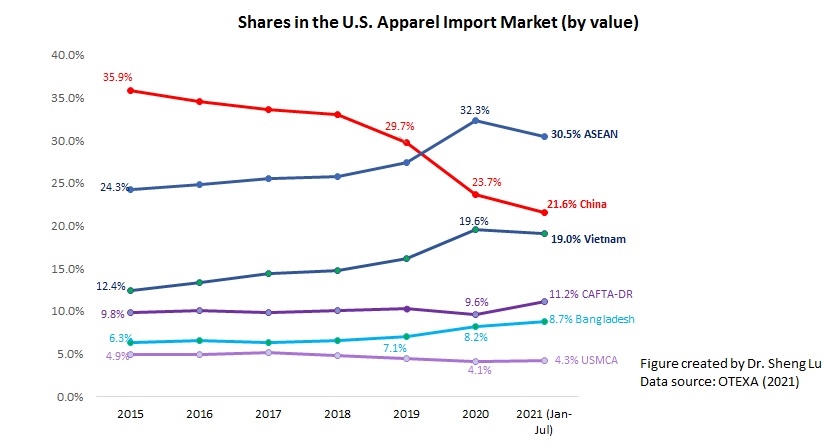

Third, US companies continue to treat China as one of their essential sourcing bases in the current business environment. However, companies are NOT reversing their long-term strategy of reducing “China exposure.” China stays the largest supplier for the US market in November 2021, accounting for 41.5% of total US apparel imports in quantity and 25.8% in value. Due to the seasonal factor, China’s market shares typically peak from June to September and then drop from October until March-April.

Both industry sources and the export product diversification index also consistently show that China supplied the most variety of products to the US market with no near competitors. In comparison, US apparel imports from Bangladesh, Mexico, and CAFTA-DR members concentrate more on specific product categories.

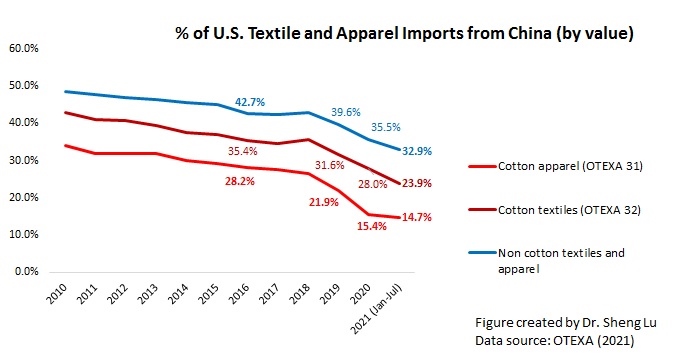

Nevertheless, the HHI index and market concentration ratios (CR3 and CR5) calculated based on the latest data suggest that US fashion companies continue to move their apparel sourcing orders from China to other Asian countries overall. For example, only around 15% of US cotton apparel comes from China, compared with about 27% in 2018. My latest studies also indicate that it has become ever more common to see a fashion company places only around 10% of its total sourcing value or volume from China compared to over 30% in the past. Furthermore, with the growing tensions of the US-China relations and the newly enacted Uyghur Forced Labor Prevention Act, fashion companies could take another look at their China sourcing strategy to avoid potential high-impact disruptions.

Fourth, near sourcing from the Western Hemisphere, especially CAFTA-DR members, continue to gain popularity. Specifically, 17.3% of US apparel imports came from the Western Hemisphere year-to-date (YTD) in 2021 (January-November), higher than 16.1% in 2020. Notably, CAFTA-DR members’ market shares increased to 10.6% in 2021 (January to November) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 41.7% growth in 2021 (January—November) from a year ago, one of the highest among all sourcing destinations. The imports from El Salvador (up 42.6%), Honduras (up 47.1%), and Guatemala (36.6%) had grown particularly fast so far in 2021. However, the political instability in some Central American countries could make fashion companies feel hesitant to permanently switch their sourcing orders to the region or make long-term investments.

Additionally, the latest trade data suggests a notable increase in the price of US apparel imports. Notably, the unit price of US apparel imports from almost all leading sources went up by more than 10% from January 2021 to November 2021. As worldwide inflation continues, the rising sourcing cost pressure won’t ease anytime soon.

In December 2021, Just-Style consulted a panel of industry leaders and scholars in its Outlook 2022–what’s next for apparel sourcing briefing. Below is my contribution to the report. All comments and suggestions are more than welcome!

What next for apparel sourcing?

As “COVID sets the agenda” and the trajectory of several critical market and non-market forces hard to predict (for example, global inflation, and geopolitics), fashion companies may still have to deal with a highly volatile and uncertain market environment in 2022. That being said, it is still hopeful that fashion companies’ toughest sourcing challenges in 2021 will start to gradually ease at some point in the new year, including the hiking shipping costs, COVID-related lockdowns, and supply chain disruptions.

In response to the “new normal,” fashion companies may find several sourcing strategies essential:

One is to maintain a relatively diverse apparel sourcing base. The latest trade data suggests that US, EU, and Japan-based fashion companies have been steadily sourcing from a more diverse group of countries since 2018, and such a trend continues during the pandemic. Echoing the pattern, in the latest annual benchmarking study I conducted in collaboration with the United States Fashion Industry Association (USFIA), we find that “China plus Vietnam plus many” remains the most popular sourcing model among respondents. This strategy means China and Vietnam combined now typically account for 20-40 percent of a fashion company’s total sourcing value or volume, a notable down from 40-60 percent in the past few years. Fashion companies diversify their sourcing away from “China plus Vietnam” to avoid placing “all eggs in one basket” and mitigate various sourcing risks. In addition, more than 85 percent of surveyed fashion companies say they will actively explore new sourcing opportunities through 2023, particularly those that could serve as alternatives to sourcing from China.

The second strategy is to strengthen the relationship with key vendors further. As apparel is a buyer-driven industry, fashion brands and retailers fully understand the importance of catering to consumers’ needs. However, the supply chain disruptions caused by COVID-19 remind fashion companies that building a close and partner-based relationship with capable suppliers also matters. For example, working with vendors that have a presence in multiple countries (or known as “super-vendors”) offers fashion companies a critical competitive edge to achieve more flexibility and agility in sourcing. Sourcing from vendors with a vertical manufacturing capability also allows fashion companies to be more resilient toward supply chain disruptions like the shortage of textile raw materials, a significant problem during the pandemic.

Further, we could see fashion companies pay even closer attention to textile raw material sourcing in the year ahead. On the one hand, given the growing concerns about various social and environmental compliance issues like forced labor, fashion brands and retailers are making more significant efforts to better understand their entire supply chain. For example, in addition to tracking who made the clothing or the fabrics (i.e., tier 1 & 2 suppliers), more companies have begun to release information about the sources of their fibers, yarns, threads, and trimmings (i.e., tier 3 & tier 4 suppliers). On the other hand, many fashion brands and retailers intend to diversify their textile material sourcing from Asia, particularly China, against the current business environment. Compared with cutting and sewing garments, much fewer countries can make textiles locally, and it takes time to build textile production capacity. Thus, fashion companies interested in taking more control of their textile raw material sourcing need to take concrete actions such as shifting their sourcing model and making long-term investments intentionally.

Apparel industry challenges and opportunities

One key issue we need to watch closely is the US-China relations. China currently remains the single largest source of apparel globally, with no near alternative. China also plays an increasingly significant role as a textile supplier for many leading apparel exporting countries in Asia. However, as the US-China relations become more concerning and confrontational, we could anticipate new trade restrictions targeting Chinese products and products from any sources that contain components made in China. Notably, with strong bipartisan support, President Biden signed into law the Uyghur Forced Labor Prevention Act on December 23, 2021. The new law is a game-changer! Depending on the detailed implementation guideline to be developed by the Customs and Border Protection (CBP), US fashion companies may find it not operationally viable to source many textiles and apparel products from China. In response, China may retaliate against well-known western fashion brands, disrupting their sales expansion in the growing Chinese consumer market. Further, as China faces many daunting domestic economic and political challenges, a legitimate question for fashion companies to think about is what an unstable China means for their sourcing from the Asia-Pacific region and what the contingency plan will be.

Another critical issue to watch is the regional textile and apparel supply chains and related free trade agreements. While apparel is a global sector, apparel trade remains largely regional-based, i.e., countries import and export products with partners in the same region. Data shows that from 2019 to 2020, around 80% of Asian countries’ textile and apparel imports came from within Asia and about 50% for EU countries. Over the same period, over 87% of Western Hemisphere (WH) countries’ textile and apparel exports went to other WH countries and about 75% for EU countries.

Notably, the reaching and implementation of new free trade agreements will continue to alter and shape new regional textile and apparel supply chains in 2022 and beyond. For example, the world’s largest free trade agreement, the Regional Comprehensive Economic Partnership (RCEP), officially entered into force on January 1, 2022. The tariff reduction and the very liberal rules of origin in the agreement could strengthen Japan, South Korea, and China as the primary textile suppliers for the Asia-based regional supply chain and enlarge the role of ASEAN as the leading apparel producer. RCEP could also accelerate other trade agreements in the Asia-Pacific region, such as the China-South Korea-Japan Free Trade Agreement currently under negotiation.

As one of RCEP’s ripple effects, we can highly anticipate the Biden administration to announce its new Indo-pacific economic framework soon to counterbalance China’s influences in the region. The Biden administration also intends to leverage trade programs such as the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) to boost textile and apparel production, trade, and investment in the Western Hemisphere and address the root causes of migration. These trade initiatives will be highly relevant to fashion companies that could use the opportunity to expand near sourcing, take advantage of import duty-saving benefits and explore new supply chains.

Additionally, fashion companies need to be more vigilant toward political instability in their major sourcing destinations. We have already seen quite a turmoil recently, from Myanmar’s military coup, Ethiopia’s loss of the African Growth and Opportunity Act (AGOA) benefits, concerns about Haiti and Nicaragua’s human rights, and the alleged forced labor in China’s Xinjiang region. Whereas fashion brands and retailers have limited or no impact on changing a country’s broader human rights situation, the reputational risks could be very high. Having a dedicated trade compliance team monitoring the geopolitical situation routinely and ensuring full compliance with various government regulations will become mainstream among fashion companies.

And indeed, sustainability, due diligence, recycling, digitalization, and data analytics will remain buzzwords for the apparel industry in the year ahead.

Discussion questions [Anyone is more than welcome to join our online discussions; For FASH455, please address at least two questions in your comment; please also mention the question number (i.e., #1, or #3; no need to repeat the question) in your comment.]

#1: How to understand apparel is a global sector from the video?

#2: How to understand the economic, social, and political implications of apparel sourcing and trade from the video?

#3: What are the top challenges facing Bangladeshi garment factories during COVID-19? Why or why not do think these challenges will go away soon?

#4: How is the big landscape of apparel sourcing changing because of COVID-19? Any apparel trade or sourcing patterns that COVID-19 didn’t change based on the video?

#5: Anything else you find interesting/intriguing/controversial/thought-provoking from the video? Why?

Note: The video provides a great overview of Amazon’s supply chain strategies in response to the current shipping crisis and their broad industry implications. You will also learn how international shipping and logistics work today, including processes, technologies, innovations, and remaining challenges.

The latest industry estimates show that Amazon’s apparel and footwear sales in the U.S. grew by roughly 15% in 2020 to more than $41 billion, more than Walmart did. This represents a highly impressive 11%-12% share of all apparel sold in the U.S. and 34%-35% share of all apparel sold online. Amazon achieved early success by offering a wide range of basics, but it has since expanded its fashion business. It now features a growing slate of name brands. The company also launched online luxury fashion shops in the fall of 2019.

Discussion questions:

What are the unique features of Amazon’s supply chain strategies in response to the current shipping crisis? Do these strategies work well? What is your evaluation?

To what extent can other retailers emulate what Amazon is doing? Should they?

Should conventional fashion companies (such as Macy’s and Gap Inc) see Amazon as a competitor or a potential collaborator? Why?

Is there anything else you find interesting/intriguing/thought-provoking in the video? Why?

Shipping & logistics terms mentioned in the video:

TEU (Twenty-foot Equivalent Unit): TEU is a measure of volume in units of twenty-foot long containers. For example, large container ships are able to transport more than 18,000 TEU (a few can even carry more than 21,000 TEU). One 20-foot container equals one TEU.

FEU (Forty-foot Equivalent Unit): Two TEUs equal one FEU.

FCL (Full Container Load): This means that a shipment occupies the entire space of a container without having to share it with other shippers. In an FCL cargo, the complete goods in the container are owned by one shipper.

LCL (Less than Container Load): LCL describes the transportation of small ocean-freight shipments, which do not require the full capacity of a container.

ULD (Unit Load Device): A container used for baggage, cargo and mail on wide-body and narrow-body aircraft.

Freight Forwarder: An agency that receives freight from a shipper and arranges for transportation with one or more carriers to the final destination. While the forwarder does not always handle the freight itself, it contracts with other carriers to move goods via road, rail, ocean and air.

Regarding Levi’s “new normal” for apparel sourcing and supply chain management, what is Harmit Singh’s vision? Why or why not do you agree with him?

How could Levi’s digital transformation plans affect its sourcing practices?

What is your evaluation of Levi’s “tailor shop” program?

What is the rationale behind Levi’s “buy better and wear better” initiative?

What is a chief financial officer (CFO)’s role in helping Levi’s achieve its sustainability goals?

Anything else you find interesting/intriguing/new/inspiring from the video and why?

About Levi’s

Levi’s supplier map (source: Open Apparel Registry)

Levi Strauss & Co is a global apparel company rooted in the jeans category. Its brand portfolio consists of Levi’s brand, Levi’s Signature, Dockers, and Denizen. In 2020, Levi’s global sales exceeded $7.1 billion. The United States is Levi’s largest market, accounting for about 41% of its sales in 2020, followed by Mexico. As of June 2021, Levi’s sources its apparel products from around 350 factories located in about 30 countries.

Years before the pandemic, Levi Strauss has begun to reduce its reliance on wholesalers and instead expand its direct-to-consumer (DTC) business. In response to COVID-19, Levi Strauss has increased flexibility and resilience through diversification across geographies, categories, genders, and distribution channels. Levi’s is also well-known as a leader in sustainability, particularly reducing chemical and water use in products.

Today, fashion companies consider a long list of factors when deciding where to source their apparel products, ranging from cost, speed to market, flexibility to the risk of social and environmental compliance. While existing studies have identified these major sourcing factors, whether they are treated equally in companies’ apparel sourcing decisions remains mostly unknown. Neither is it clear how fashion companies make a trade-off among these sourcing factors, given no sourcing destination is perfect.

This study aims to quantitatively evaluate the influence of primary sourcing factors on fashion companies’ determination of apparel sourcing destinations. For the study, we collected a detailed evaluation of the world’s 27 largest sourcing destinations in 2019 against 15 specific performance indicators from GlobalData, one of the most popular sourcing analytics tools. The evaluation uses a 5-point rating scale for each performance indicator.

Because some of these 15 performance indicators measure similar items, we first conducted an exploratory factor analysis, which reduced these indicators to five principal sourcing factors based on their correlation matrix scores. These five principal sourcing factors cover the following themes:

Capacity: It covers seven performance indicators that measure a sourcing destination’s capabilities (including flexibility and lead time) of providing apparel products and other value-added services.

Price & Tariff: It covers two performance indicators that measure the financial implications of sourcing from a particular destination, including eligibility for preferential import duties.

Stability: It covers two performance indicators that measure a sourcing destination’s macro-business environment, specifically sourcing-related political and economic climates.

Sustainability: It encompasses all social and environmental compliance issues related to apparel production and sourcing.

Quality: It covers two performance indicators that measure whether a sourcing destination obtains skilled workers and the overall quality of its products.

Next, we calculated the 27 apparel exporting countries’ average scores of these five principal sourcing factors. Based on the results, we further conducted a multiple regression analysis to evaluate the impact of the five principal sourcing factors on the value of these 27 countries’ apparel exports to the U.S., EU, and Asia in 2019, respectively. These three regions combined accounted for more than 80% of world apparel imports that year; however, fashion companies in each area are suggested to have unique sourcing preferences.

First, the result suggests that improving the performance in Stability and Quality can help a country enhance its attractiveness as an apparel sourcing base in the U.S. and Asia markets, but not so much in the EU market.

Second, a higher score for the factor Sustainability does not result in more sourcing orders at the country level in all three markets examined. It seems fashion companies’ current sourcing model does not provide substantial financial rewards encouraging better performance in sustainability. It is also likely that sustainability and compliance are treated more as pre-requisite criteria instead of determining the volume of the sourcing orders.

Third, the impact of Price & Tariff and Capacity on the value of apparel imports is not statistically significant in any of the three markets examined. This result does NOT necessarily mean price and production capacity is irrelevant. Instead, the result implies that fashion companies’ sourcing decision today is not merely about “chasing the lowest price.” Meanwhile, due to concerns about supply chain risks, even the most “economically competitive” sourcing destination won’t receive all the sourcing orders.

The findings of the study suggest that fashion companies’ sourcing decisions today appear to be more complicated and subtle than what is revealed by the existing literature and the public perception. Notably, the findings present different views from previous studies regarding how sourcing cost and sustainability affect fashion companies’ selection of sourcing destinations.

The findings also call our attention to the significant impact of non-economic factors on companies’ sourcing decisions, particularly the perceived political risks. This result explained why fashion companies had quickly reacted to the recent forced labor concerns in Xinjiang, China, and the military coup in Myanmar and halted sourcing from the regions.

The Regional Comprehensive Economic Partnership (RCEP)is a free trade agreement between ten member states of the Association of Southeast Asian Nations (ASEAN)* and five other large economies in the Asia-Pacific region (China, Japan, South Korea, New Zealand, and Australia). RCEP was reached on November 15, 2020, after nearly eight years of tough negotiation. (Note: ASEAN members include Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam. India was an original RCEP member but decided to quit in late 2019 due to concerns about competing with Chinese products, including textiles and apparel.)

So far, RCEP is the world’s largest trading bloc. As of 2019, RCEP members accounted for nearly 26.2% of world GDP, 29.5% of world merchandise exports, and 25.9% of world merchandise imports.

As of November 1, 2021, Lao, Burnei, Cambodia, Singapore and Thailand (ASEAN members), as well as China, Japan, New Zealand and Australia have ratified the agreement. This has met the minimum criteria for RCEP to enter into force (i.e., six members, including at least three ASEAN members and three non-ASEAN members).

Why RCEP matters to the textile and apparel industry?

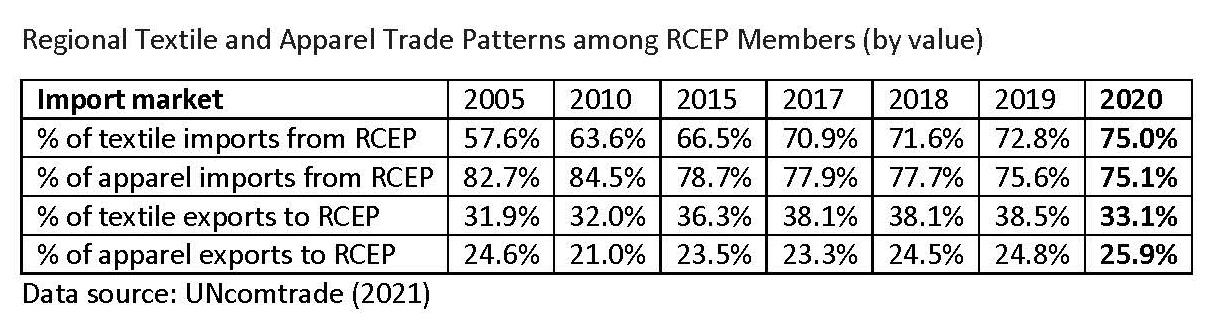

RCEP matters significantly for the textile and apparel (T&A) sector. According to statistics from the United Nations, in 2019, the fifteen RCEP members altogether exported US$374 billion worth of T&A (or 50% of the world share) and imported US$139 billion (or 20% of the world share).

In particular, RCEP members serve as critical apparel-sourcing bases for many US and EU fashion brands. For example, in 2019, close to 60% of US apparel imports came from RCEP members, up from 45% in 2005. Likewise, in 2019, 32% of EU apparel imports also came from RCEP members, up from 28.1% in 2005.

Notably, RCEP members have been developing and forming a regional textile and apparel supply chain. More economically advanced RCEP members (such as Japan, South Korea, and China) supply textile raw materials to the less economically developed countries in the region within this regional supply chain. Based on relatively lower wages, the less developed countries typically undertake the most labor-intensive processes of apparel manufacturing and then export finished apparel to major consumption markets worldwide.

As a reflection of an ever more integrated regional supply chain, in 2019, as much as 72.8% of RCEP members’ textile imports came from other RCEP members, a substantial increase from only 57.6% in 2005. Nearly 40% of RCEP members’ textile exports also went to other RCEP members in 2019, up from 31.9% in 2005.

What are the key provisions in RCEP related to textiles and apparel?

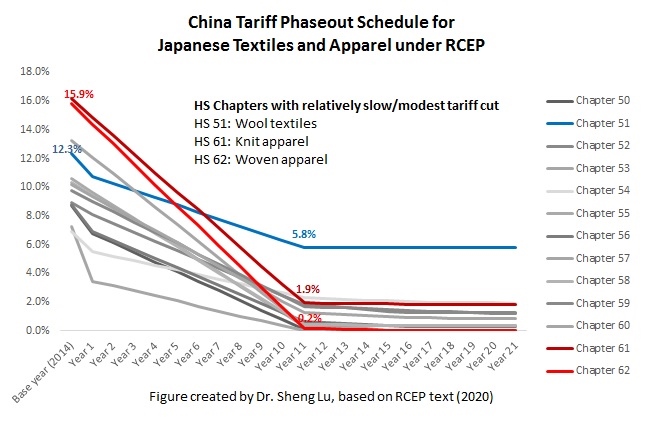

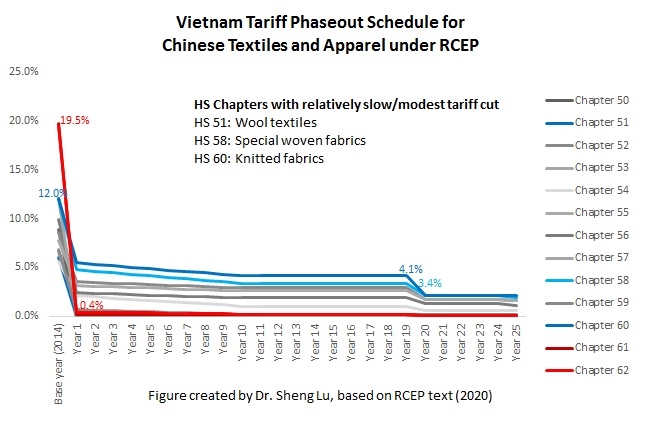

First, RCEP members have committed to reducing the tariff rates to zero for most textile and apparel traded between RCEP members on day one after the agreement enters into force. That being said, the detailed tariff phaseout schedule for textile and apparel products under RCEP is very complicated. Each RCEP member sets their own tariff phaseout schedule, which can last more than 20 years (for example, 34 years for South Korea and 21 years for Japan.) Also, different from U.S. or EU-based free trade agreements, the RCEP phaseout schedule is country-specific. For example, South Korea sets different tariff phaseout schedules for textile and apparel products from ASEAN, China, Australia, Japan, and New Zealand. Japan’s tariff cut for apparel products is more generous toward ASEAN members and less so for China and South Korea (see the graph above). Companies interested in taking advantage of the duty-free benefits under RCEP need to study the “rules of the game” in detail.

Second, in general, RCEP adopts very liberal rules of origin for apparel products. It only requires that all non-originating materials used in the production of the good have undergone a tariff shift at the 2-digit HS code level (say a change from any chapters from chapters 50-60 to chapter 61). In other words, RCEP members are allowed to source yarns and fabrics from anywhere in the world, and the finished garments will still qualify for duty-free benefits. Most garment factories in RCEP member countries can immediately enjoy the RCEP benefits without adjusting their current supply chains.

What are the potential economic impacts of RCEP on the textile and apparel sector?

On the one hand, the implementation of RCEP is likely to further strengthen the regional textile and apparel supply chain among RCEP members. Particularly, RCEP will likely strengthen Japan, South Korea, and China as the primary textile suppliers for the regional T&A supply chain. Meanwhile, RCEP will also enlarge the role of ASEAN as the leading apparel producer in the region.

On the other hand, as a trading bloc, RCEP could make it even harder for non-RCEP members to get involved in the regional textile and apparel supply chain formed by RCEP members. Because an entire regional textile and apparel supply chain already exists among RCEP members, plus the factor of speed to market, few incentives are out there for RCEP members to partner with suppliers from outside the region in textile and apparel production. The tariff elimination under the RCEP will put textile and apparel producers that are not members of the agreement at a more significant disadvantage in the competition. Not surprisingly, according to a recent study, measured by value, only around 21.5% of RCEP members’ textile imports will come from outside the area after the implementation of the agreement, down from the base-year level of 29.9% in 2015.

Further, the reaching of RCEP could accelerate the negotiation of other trade agreements in the Asia-Pacific region, such as the China-South Korea-Japan Free Trade Agreement. We might also see growing pressures on the Biden administration to join the Comprehensive and Progressive Agreement of the Trans-Pacific Partnership (CPTPP) to strengthen the US economic ties with countries in the Asia-Pacific region. The economic competition between the United States and China in the area could also intensify as the combined effects of RCEP and CPTPP begin to shape new supply chains and test the impacts of the two countries on the regional trade patterns.

The virus is here to stay. What steps the companies must take to mitigate its impact?

Sheng: Earlier this year, I, together with the US Fashion Industry Association, surveyed about 30 leading US fashion brands and retailers to understand COVID-19’s impact on their sourcing practices. Respondents emphasized two major strategies they adopted in response to the current market environment. One is to strengthen the relationship with key vendors, and the other is to improve flexibility and agility in sourcing. These two strategies are also highly connected. As one respondent told us “We’re adjusting our sourcing model mix (direct vs. indirect) & establishing stronger strategic supplier relationships across entire matrix continue to build flexibility and dual sourcing options.” Many respondents, especially those large-scale fashion brands and retailers, also say they plan to reduce the number of vendors in the next few years to improve operational efficiency and obtain greater leverage in sourcing.

Which are the countries benefitting out of the US-China tariff war and why?

Sheng:The trade war benefits nobody, period. Today, textiles and apparel are produced through a highly integrated supply chain, meaning the US-China tariff war could increase everyone’s production and sourcing costs. Back in 2018, when the tariff war initially started, the unit price of US apparel imports from Vietnam, Bangladesh, and India all experienced a notable increase. Whereas companies tried to switch their sourcing orders, the production capacity was limited outside China. Meanwhile, China plays an increasingly significant role as a leading textile supplier for many apparel exporting countries in Asia. Despite the trade war, removing China from the textile and apparel supply chain is impossible and unrealistic.

How do you compare the African and Asian markets when it comes to sourcing and manufacturing? Which are the advantages both offer?

Sheng: Asia as a whole remains the world’s dominant textile and apparel sourcing base. According to statistics from the United Nations (i.e., UNComtrade), Asian countries as a whole contributed about 65% of the world’s total textile and apparel exports in 2020. In the same year, Asian countries altogether imported around 31% of the world’s textiles and 19% of apparel. Asian countries have also established a highly efficient and integrated regional supply chain by leveraging regional free trade agreements or arrangements. For example, as much as 85% of Asian countries’ textile imports came from other Asian countries in 2019, a substantial increase from only 70% in the 2000s. With the recent reaching of several mega free trade agreements among countries in the Asia-Pacific region, such as the Regional Comprehensive Economic Partnership (RCEP), the pattern of “Made in Asia for Asia” is likely to strengthen further.

In comparison, only about 1% of the world’s apparel imports come from Africa today. And this percentage has barely changed over the past decades. Many western fashion brands and retailers have expressed interest in expanding more apparel sourcing from Africa. However, the tricky part is that these fashion companies are hesitant to invest directly in Africa, without which it is highly challenging to expand African countries’ production and export capacity. Political instability is another primary concern that discourages more investment and sourcing from Africa. For example, because of the recent political turmoil, Ethiopia, one of Africa’s leading apparel sourcing bases, could be suspended for its eligibility for the African Growth and Opportunity Act (AGOA). Without AGOA’s critical support, Ethiopia’s apparel exports to the US market could see a detrimental decline. On the other hand, while these trade preference programs are crucial in supporting Africa’s apparel exports, they haven’t effectively solved the structural issues hindering the long-term development of the textile and apparel industry in the region. More work needs to be done to help African apparel producers improve their genuine export competitiveness.

Another issue is Brexit. Is that having any significant impact on the sourcing scenario of the world or is it just limited to the European nations?

Sheng: Despite Brexit, the trade and business ties between the UK and the rest of the EU for textile and apparel products continue to strengthen. Thanks to the regional supply chain, EU countries remain a critical source of apparel imports for UK fashion brands and apparel retailers. Nearly 35% of the UK’s apparel imports came from the EU region in 2019, a record high since 2010. Meanwhile, the EU region also is the single largest export market for UK fashion companies—about 79% of the UK’s apparel exports went to the EU region in 2019 before the pandemic.

However, trade statistics in the short run may not fully illustrate the impacts of Brexit. For example, some recent studies suggest that Brexit has increased fashion companies’ logistics costs, delayed customs clearance, and made talent-hiring more inconvenient. Meanwhile, Brexit provides more freedom and flexibility for the UK to reach trade deals based on its national interests. For example, the UK recently submitted its application to join the Comprehensive Progressive Agreement of the Trans-Pacific Partnership (CPTPP). The UK is also negotiating a bilateral trade agreement with the United States. The reaching of these new trade agreements, particularly with non-EU countries, could significantly promote the UK’s luxury apparel exports and help the UK diversity its source of imports.

How do you think the power shortages happening across Europe, China, and other nations, are going to impact the apparel supply chains?

Sheng: One of my primary concerns is that the new power shortage could exacerbate inflation further and result in a more severe price hike throughout the entire textile and apparel supply chain. When Chinese factories are forced to cease production because of power shortage, the impact could be far worse than recent COVID-related lockdowns in Vietnam and Bangladesh. As mentioned earlier, more than half of many leading Asian apparel exporting countries’ textile supplies come from China today. Also, no country can still compete with China in terms of the variety of apparel products to offer. In other words, for many western fashion brands and retailers, their stores and shelves could look more empty (i.e., having less variety of products to sell) because of China’s power shortage problem.

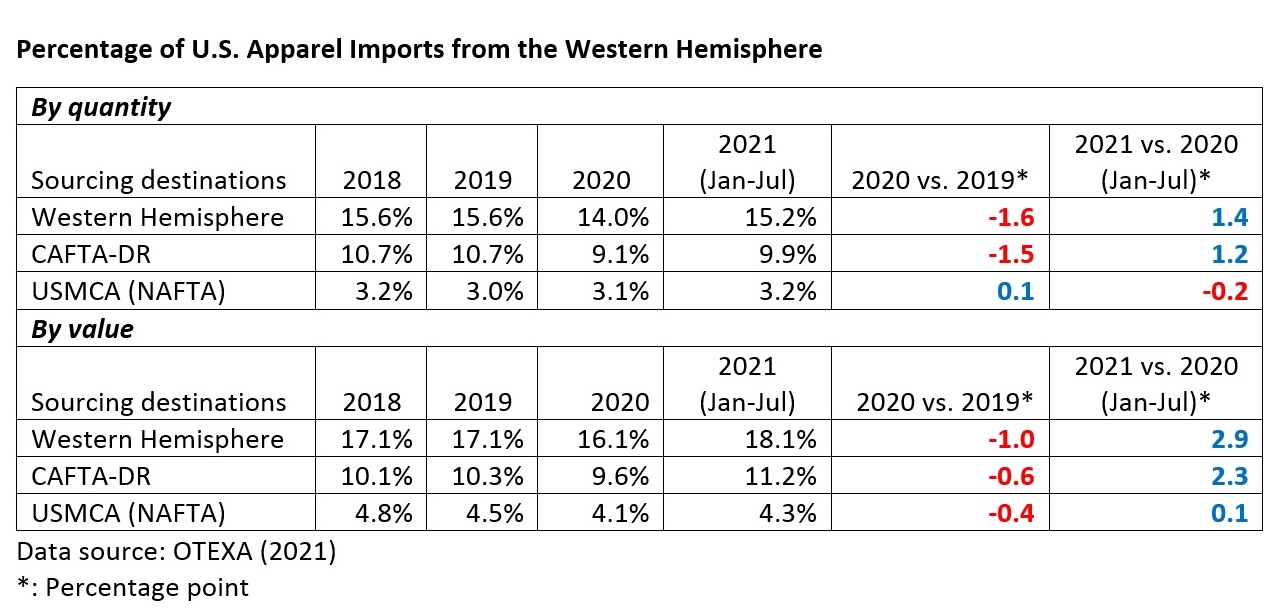

Data shows that 15.2% of US apparel imports came from USMCA and CAFTA-DR members YTD in 2021 (January-August), higher than 13.7% in 2020 and about 14.7% before the pandemic (2018-2019). Notably, CAFTA-DR members’ market shares increased to 11% in 2021 (January to Aug) from 9.6% in 2020. The value of US apparel imports from CAFTA-DR also enjoyed a 54% growth in 2021 (January—Aug) from a year ago, faster than 25% of the world’s average.

#2 Sourcing apparel from USCMA and CAFTA-DR members helps US fashion brands and retailers save around $1.6-1.7 billion tariff duties annually. (note: the estimation considers the value of US apparel imports from USMCA and CAFTA-DR members at the 6-digit HTS code level and the applied MFN tariff rates for these products; we didn’t consider the additional Section 301 tariffs US companies paid for imports from China). Official trade statistics also show that measured by value, about 73% of US apparel imports under free trade agreements came through USMCA (25%) and CAFTA-DR (48%) from 2019 to 2020.

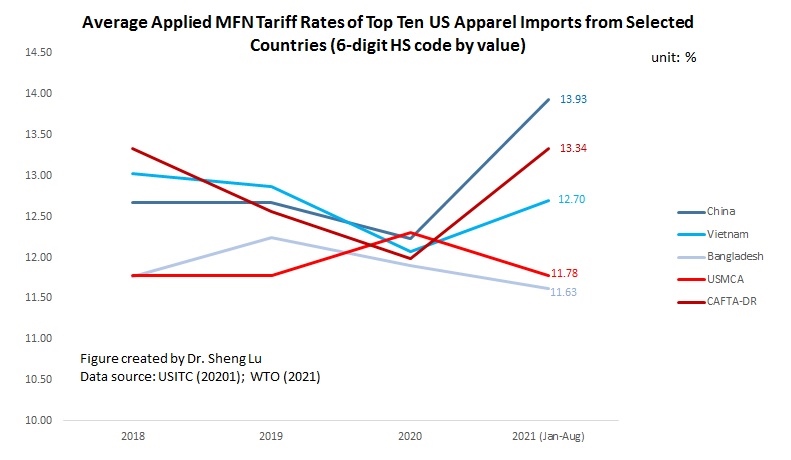

#3 US apparel imports from USMCA and CAFTA-DR members do NOT necessarily focus on items subject to a high tariff rate. Measured at the 6-digit HS code level, apparel items subject to a high tariff rate (i.e., applied MFN tariff rate >17%) only accounted for about 8-9% of US apparel imports from USMCA members and 7-8% imports from CAFTA-DR members. In comparison, even having to pay a significant amount of import duties, around 17% of US apparel imports from Vietnam and 10% of imports from China were subject to a high tariff rate (see table below).

The phenomenon suggests that USCMA and CAFTA-DR members still have limited production capacity for many man-made fibers(MMF) clothing categories (such as jackets, swimwear, dresses, and suits), typically facing a higher tariff rate. This result also implies that expanding production capacity and diversifying the export product structure could make USMCA and CAFTA-DR more attractive sourcing destinations.

#4 US apparel imports from USMCA and CAFTA-DR members tend to focus on large-volume items subject to a medium tariff rate. Specifically, from 2017 to 2021 (Jan-Aug), ten products (at the 6-digit HTS code level) typically contributed around half of the US tariff revenues collected from apparel items (HS chapters 61-62). However, the average applied MFN tariff rates for these items were only about 13%. Meanwhile, these top tariff-revenue-contributing apparel items accounted for about 50% of US apparel imports from USMCA members and nearly 64%-69% of imports from CAFTA-DR members.

Likewise, the top ten products (at the 6-digit HTS code level) typically accounted for 65%-68% of US apparel imports from USMCA members and nearly 73-75% of US apparel imports from CAFTA-DR members. These products also had a medium average applied MFN rate at 11-12% for USMCA and 12-13% in the case of CAFTA-DR.

Given the duty-saving incentives, expanding “near-sourcing” from USMCA and CAFTA-DR members could prioritize these large-volume apparel items with a medium tariff rate in short to medium terms. However, in the long run, a shortcoming of this strategy is that many such items are basic fashion clothing that primarily competes on price (such as T-shirts and trousers) and cannot leverage the unique competitive edge of near-sourcing (such as speed to market). When the US reaches new free trade agreements, particularly those involving leading apparel-producing countries in Asia, it could offset the tariff advantages enjoyed by USMCA and CAFTA-DR members and quickly result in trade diversion.

#1: As of June 2021, US textile production had resumed about 98.8% of its production capacity at the pre-COVID level. Based on the readings, why or why not do you think the industry is already “out of the woods”? How to understand the impact of COVID-19 on the international competitiveness of US textile production?

#2: To which extent do you think the state of the US textile and apparel industry and its performance during the pandemic challenge the conclusions of the classic trade and economic development theories we learned in the class (e.g., comparative advantage, factor proportion, the international division of labor, and stage of development theories)? Do you find any trade or production patterns that existing theories cannot fully explain?

#3 Many US fashion companies’ strategies to “consolidate existing sourcing base and strengthen the relationship with key vendors” during the pandemic. What is your evaluation of this strategy—is it a short-term reaction toward COVID-19 or a long-term trend likely to stay? What does this strategy mean for vendors in the apparel supplying countries?

#4: What are the notable changes in fashion companies’ sourcing criteria during the pandemic? How to explain such changes? Who are the winners and losers? Why?

#5: It is of concern that sustainability and social responsibility become a lower priority for the apparel industry during the pandemic, given the unprecedented operational and financial challenges companies face. What is your assessment based on the readings?

#6: What is your vision for the US textile and apparel industry in the post-COVID world? What are the key issues/questions/development trends we shall watch?

(Welcome to our online discussion. For students in FASH455, please address at least two questions and mention the question number (#) in your reply)

By leveraging theGlobalData Apparel Intelligence Center’s “Company Filing Analytics” tool, we took a detailed look at apparel companies’ latest efforts on addressing climate change. Specifically, we conducted a content analysis of annual and quarterly filings (e.g., 10-Q report and corporate annual report) submitted by over a hundred leading apparel companies worldwide from June 2020 to September 2021.

Key findings:

First, addressing climate change has become a more critical topic for apparel companies over the past five years. The percentage of apparel companies that mention “climate change” in their corporate filings nearly doubled from 43% in 2016 to 80% in 2020. Notably, different from the public perception, fast fashion brands like Inditex and H&M were among apparel companies that most frequently mentioned “climate change” in their corporate reports over that period.

Second, many apparel companies see their business risks associated with climate change growing. Results from GlobalData show that apparel companies are particularly concerned about potential supply chain disruption caused by climate change. Apparel companies are also concerned that climate change could increase their sourcing and production costs and hurt financials. As a leading fashion brand noted, “Disasters, climate change…may cause escalating prices or difficulty in procuring the raw materials (such as cotton, cashmere, down, etc.)”. Another added, “In the long term, the broader impacts of climate change may impact the cost and accessibility of materials used to manufacture products or other resources needed to operate business.”

Third, an increasing number of apparel companies have incorporated climate change into their corporate strategies or long-term business visions. Some apparel companies also established a dedicated office or governance structure to address climate change.

Further, apparel companies call for more detailed and transparent regulatory guidelines that can help them combat climate change. As one leading fashion brand commented, “Any assessment of the potential impact of future climate change legislation, regulations or industry standards, as well as any international treaties and accords, is uncertain given the wide scope of potential regulatory change in the countries in which we operate… As a result, the effects of climate change could have a long-term adverse impact on our business and the results of operations.”

In conclusion, addressing climate change is no longer a topic apparel companies can only ignore or treat as a marketing slogan. Instead, we are likely to see companies allocate more dedicated resources to this area in the long run, from human resources to research & development (R&D) spendings. Meanwhile, apparel companies may find it necessary and beneficial to effectively communicate their efforts and needs to address climate change with key stakeholders like consumers and public policymakers.

Victoria Langro is an Honors Marketing & Operations Management Majors and Fashion Management Minor (class of 2022). She is also a 2020 UD Summer Scholar. In summer 2021, Victoria worked with Tapestry, which owns Coach, as a global trade compliance intern.

Julia Hughes, President, United States Fashion Industry Association

Matthias Knappe, Senior Officer and Program Manager for Cotton, Fibers and Textiles, International Trade Centre

Avedis Seferian, President & CEO, Worldwide Responsible Accredited Production (WRAP).

Anna Walker, Vice President of Public Policy, Levi’s Strauss Co.

Dr. Sheng Lu, Associate Professor, Department of Fashion & Apparel Studies, University of Delaware

Event summary:

Apparel is a $2.5 trillion global business, involving over 120 million workers worldwide and playing a uniquely critical role in the post-COVID economic recovery. The session intends to facilitate constructive dialogue regarding the progress, challenges, and opportunities of building a more sustainable and transparent apparel supply chain in the Post-COVID world, which matters significantly to ALL stakeholders, from fashion brands, garment workers, policymakers to ordinary consumers.

The panel shared their valuable insights about the impacts of COVID on the world apparel trade patterns and how to make the apparel supply chain more sustainable and transparent in the post-COVID world. Specifically:

First, panelists agree that COVID-19 has resulted in unpresented challenges for apparel sourcing and trade, from supply chain disruptions, cost increases to market uncertainties.

Second, despite the mounting challenges and financial pressures caused by COVID-19, the apparel industry as a whole is NOT ignoring sustainability and social responsibility. Some leading fashion brands and retailers allocate more resources to strengthen their relationships with key vendors during the pandemic. The shifting business environment and the adoption of digital technologies also allow apparel companies to explore new business models and achieve more sustainable and socially responsible apparel production and trade.

Third, the apparel industry is attaching greater importance to supply chain transparency. Today, fashion brands and retailers typically track their tier 1 and tier 2 suppliers. A growing number of companies also start to understand who is making the textile raw materials (i.e., fibers and yarns). To improve supply chain transparency further, panelists suggest more traceability technologies, building trust between importers and suppliers and creating a clearer regulatory framework. Trade policy can also have a crucial role to play in the process.

The new law bans the long-standing piece-rate system — 5 cents to sew a side seam, for instance, or 10 cents to sew a neck — that often adds up to less than $6 an hour (source: LA times). From now on, garment workers in California will get a minimum wage of $14 per hour for employers with 26 or more employees.

The new law’s “brand guarantor” provision would extend the liability for wage theft from the factories themselves to the brands and retailers that sell the clothes, as well as any subcontractors in between. In other words, the bill creates new liabilities across California’s clothing supply chain from factory subcontractors to retailers. (source: San Francisco Examiner)

Concerns about Senate Bill 62

According to the American Apparel and Footwear Association (AAFA), the California Garment Worker Protection Act “does not recognize that brands or buyers may have little to no control over how a particular garment factory employer manages their payroll or enterprise finances.” AAFA explains why this new law in actuality could punish good actors:

“Brand Good contracts with Manufacturer Y to manufacture their clothes, paying a good price, more than enough to pay required wages to Manufacturer Y’s employees. However, in an effort to generate more business, Manufacturer Y also takes a low-bid contract from Brand Bad, so low that both Manufacturer Y and Brand Bad know Manufacturer Y will not be able to pay required wages to its employees. Under this bill, Brand Good would be liable for any wage claims resulting from Manufacturer Y’s acceptance of a low-bid contract completely unrelated to its operations.

The legislation would make responsible brands like Brand Good legally liable to pay for wage claims resulting from Manufacturer Y’s and Brand Bad’s unlawful or irresponsible activity. SB 62 will not deter bad actors like Brand Bad from operating in California’s garment manufacturing industry. Instead, it will penalize responsible companies like Brand Good, even though Brand Good did the right thing. As a result, Brand Good, and other responsible brands, will no longer allow their branded garments to be manufactured in California out of fear that they will acquire additional liabilities over activities they don’t control.”

More than 60% of garment factories in the US are based in California.

Discussion question:Based on the video and the readings, what is your view on the California Garment Worker Protection Act? What changes could it bring to the fashion apparel industry and why?

(Disclaimer: All posts on this site are for FASH455 educational and academic research purposes only, and they are nonpolitical and nonpartisan. No blog post intends to either favor or oppose any particular political party/public policy, nor shall be interpreted that way)

As one breaking news, on 16 September 2021, China officially presented its application to join the 11-member Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). While the approval of China’s membership in CPTPP remains a long shot and won’t happen anytime soon, the debate on the potential impact of China’s accession to the trade agreement already starts to heat up.

Like many other sectors, textile and apparel companies are on the alert. Notably, China plus current CPTPP members accounted for nearly half of the world’s textile and apparel exports in 2020. Many non-CPTPP countries are also critical stakeholders of China’s membership in the agreement. In particular, the Western Hemisphere textile and apparel supply chain, which involves the US textile industry, could face unrepresented challenges once China joins CPTPP.

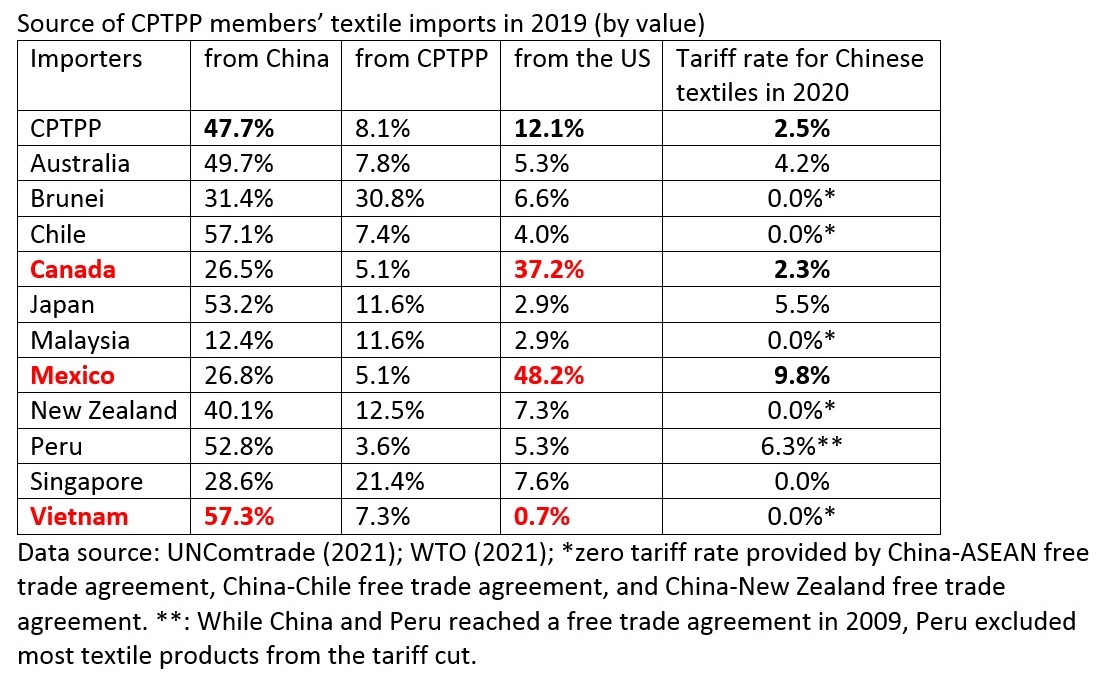

First, once China joins CPTPP, the tariff cut could provide strong financial incentives for Mexico and Canada to use more Chinese textiles. China is already a leading textile supplier for many CPTPP members. In 2019, as much as 47.7% of CPTPP countries’ textile imports (i.e., yarns, fabrics, and accessories) came from China, far more than the United States (12.1%), the other leading textile exporter in the region.

Notably, thanks to the Western Hemisphere supply chain and the US-Mexico-Canada Trade Agreement (USMCA, previously NAFTA), the United States remains the largest textile supplier for Mexico (48.2%) and Canada (37.2%). Mexico and Canada also serve as the largest export market for US textile producers, accounting for as many as 46.4% of total US yarn and fabric exports in 2020.

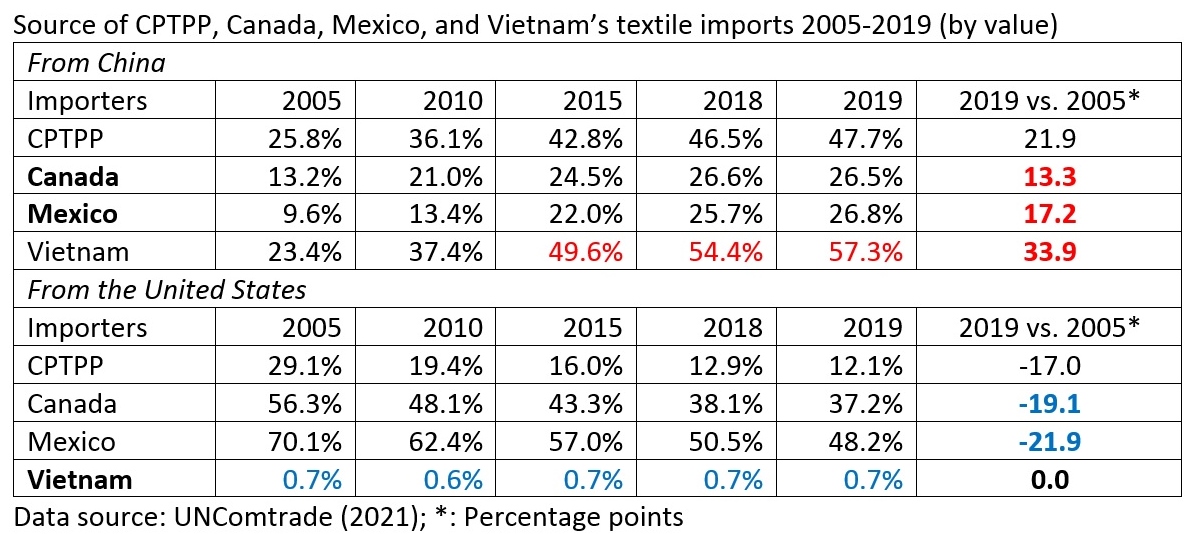

However, US textile exporters face growing competition from China, offering more choices of textile products at a more competitive price (e.g., knitted fabrics and man-made fiber woven fabrics). From 2005 to 2019, US textile suppliers lost nearly 20 percentage points of market shares in Mexico and Canada, equivalent to what China gained in these two markets over the same period.

Further, China’s membership in CPTPP means its textile exports to Mexico and Canada could eventually enjoy duty-free market access. The significant tariff cut (e.g., from 9.8% to zero in Mexico) could make Chinese textiles even more price-competitive and less so for US products. This also means the US textile industry could lose its most critical export market in Mexico and Canada even if the Biden administration stays away from the agreement.

Second, if both China and the US become CPTPP members, the situation would be even worse for the US textile industry. In such a case, even the most restrictive rules of origin would NOT prevent Mexico and Canada from using more textiles from China and then export the finished garments to the US duty-free. Considering its heavy reliance on exporting to Mexico and Canada, this will be a devastating scenario for the US textile industry.

Even worse, the US textile exports to CAFTA-DR members, another critical export market, would drop significantly when China and the US became CPTPP members. Under the so-called Western-Hemisphere textile and apparel supply chain, how much textiles (i.e., yarns and fabrics) US exports to CAFTA-DR countries depends on how much garments CAFTA-DR members can export to the US. In comparison, US apparel imports from Asia mostly use Asian-made textiles. For example, as a developing country, Vietnam relies on imported yarns and fabrics for its apparel production. However, over 97% of Vietnam’s textile imports come from Asian countries, led by China (57.1%), South Korea, Taiwan, and Japan (about 25%), as opposed to less than 1% from the United States.

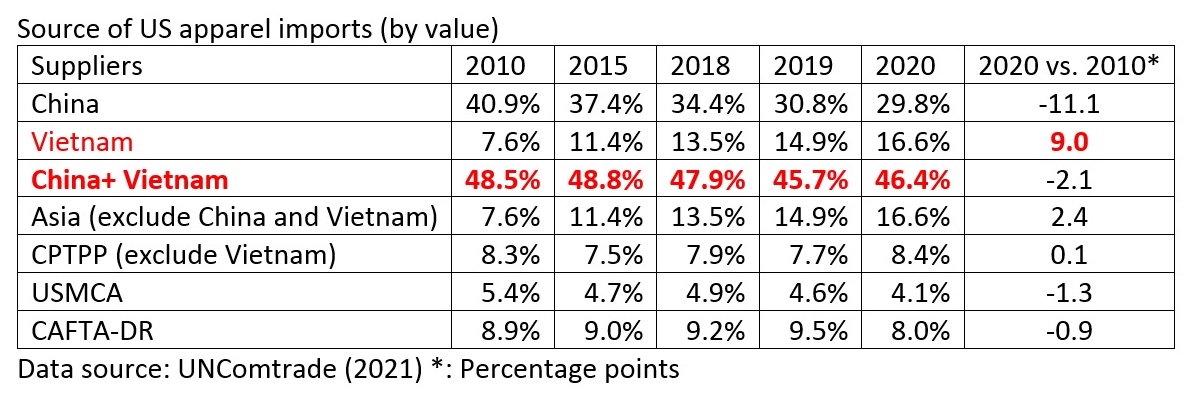

The US textile industry also deeply worries about Vietnam becoming a more competitive apparel exporter with the help of China under CPTPP. Notably, among the CPTPP members, Vietnam is already the second-largest apparel exporter to the United States, next only to China. Despite the high tariff rate, the value of US apparel imports from Vietnam increased by 131% between 2010 and 2020, much higher than 17% of the world average. Vietnam’s US apparel import market shares quickly increased from only 7.6% in 2010 to 16.6% in 2020 (and reached 19.3% in the first half of 2021). The lowered non-tariff and investment barriers provided by CPTPP could encourage more Chinese investments to come to Vietnam and further strengthen Vietnam’s competitiveness in apparel exports.

Understandably, when apparel exports from China and Vietnam became more price-competitive thanks to their CPTPP memberships, more sourcing orders could be moved away from CAFTA-DR countries, resulting in their declined demand for US textiles. Notably, a substantial portion of US apparel imports from CAFTA-DR countries focuses on relatively simple products like T-shirts, polo shirts, and trousers, which primarily compete on price. Losing both the USMCA and CAFTA-DR export markets, which currently account for nearly 70% of total US yarns and fabrics exports, could directly threaten the survival of the US textile industry.

#1: Is the sole benefit of globalization helping us get cheaper products? How to convince US garment workers who lost their jobs because of increased import competition that they benefit from globalization also?

#2 How to explain the phenomenon that US apparel imports from China continue to rise despite the tariff war? Do you think the tariff war is a wrong strategy or a good strategy implemented at the wrong time given COVID?

#2: In the class, we mentioned that major driving forces of globalization include economic growth, lowered trade and investment barriers, and technology advancement. What will be the primary driving forces of globalization or deglobalization in the post-COVID world, and why?

#3: Based on the reading “U.S.-China Trade War Still Hurting Ohio Family-Owned Business,” what results of the US-China tariff war are expected and unexpected? What is your recommendation for the Biden administration regarding the Section 301 tariff exclusion process and why?

#4: We say textile and apparel is a global sector. How does the US-China tariff war affect textile and apparel producers and companies in other parts of the world? Why?

#5: From this week’s readings, why do we say textile and apparel trade and sourcing involve economic, social, and political factors and implications? Please provide 1-2 specific examples from the articles to support your viewpoints.

(Welcome to our online discussion. For students in FASH455, please address at least two questions and mention the question number (#) in your reply)

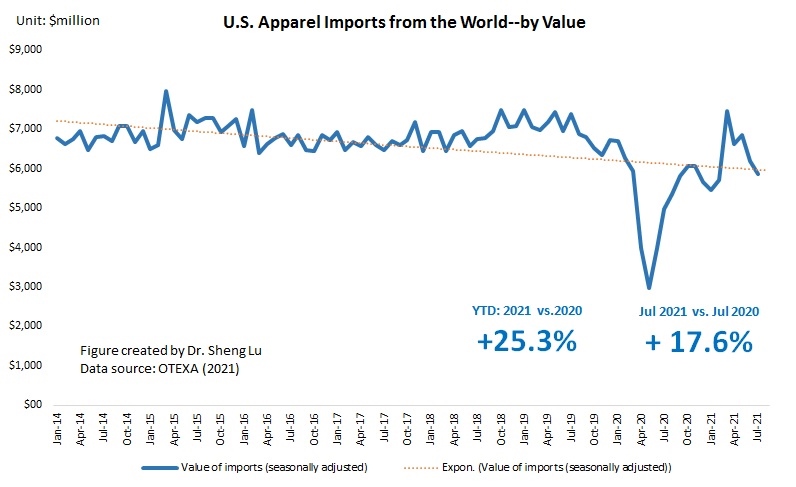

First, the shipping crisis and new wave of COVID cases start to affect US apparel imports negatively. While US consumers’ demand for clothing overall remains strong, for the second month in a row, the value of US apparel imports (seasonally adjusted) in July 2021 decreased by 5.5% from a month ago and down 9.7% from May to June. The absolute value of US apparel imports year to date (YTD) in 2021 (January—July) was 25.3% higher than in 2020 and around 87% of the pre-COVID level (benchmark: January-July, 2019). However, the year-over-year growth in July 2021 was only 15.4%, compared with 60.0% in May 2021 and 29.1% in June 2021. Overall, the results remind us that the market environment is far from stable yet as the COVID situation in the US and other parts of the world continues to evolve.