With the public’s increasing demand, fashion companies are making more significant efforts to improve their apparel supply chains’ transparency, i.e., mapping where the product is made and knowing suppliers’ compliance with social and environmental regulations.

Recently, VF Corporation, one of the most historical and largest US apparel corporations, released the entire supply chain of its 20 popular apparel items, such as Authentic Chino Stretch, Men’s Merino Long Sleeve Crewe, and Women’s Down Sierra Parka. VF Corporation used more than 300 factories worldwide to make these apparel items and related textile raw materials.

We conducted a statistical analysis (Multivariate analysis of variance, MANOVA) of these factories, aiming to evaluate the state of VF Corporation’s apparel supply chain transparency, including its strengths and areas that can be improved further. The findings of this study will fulfill a critical research gap and significantly enhance our understanding of the nature of today’s apparel supply chain and the opportunities and challenges to improve its transparency.

The results show that VF Corporation’s suppliers in different segments of the apparel supply chain had different transparency performances overall:

While more than 92% of tier 1 & 2 suppliers shared their environmental or social compliance information with VF Corporation, less than 60% of VF Corporation’s tier 3 & 4 suppliers did so (note: statistically significant).

A higher percentage of VF Corporation’s tier 2 & 3 suppliers (i.e., mills making fabrics, yarns, or accessories) received environmental compliance-related certification than tier 1 suppliers (i.e., garment factories) (note: statistically significant).

Meanwhile, VF Corporation’s tier 1 suppliers were more active in pursuing social compliance-related certification than suppliers in other levels (note: statistically significant)

However, no evidence suggests that whether from a developed or developing country will statistically affect a vendor’s transparency performance.

The study’s findings have several important implications:

First, more work can be done to strengthen fashion companies’ transparency of tier 3 & 4 suppliers (i.e., textile mills making yarns and fibers). Despite the significant efforts to know their garment factories (i.e., tier 1 suppliers), fashion companies like VF Corporation still have limited knowledge about vendors upper in the supply chain. Notably, even VF Corporation doesn’t have much leverage to request environmental and social compliance-related information from these vendors. According to VF Corporation, often “Supplier was unresponsive to VF’s request for information.”

Second, the results suggest that vendors at different supply chain levels have their respective transparency priorities. However, it is debatable whether tier 1 & 2 suppliers also need to care about environmental and sustainability-related compliance, and if tier 3 & 4 suppliers should be more transparent about their social compliance record. The growing concerns about forced labor involved in cotton production (i.e., tier 4 suppliers) make the debate even more relevant.

Additionally, different from the public perception and previous studies, the findings call for equal treatment of suppliers from developed and developing countries when vetting their environmental and social compliance-related transparency.

Because this case study looked at VF Corporation only, future research can continue to investigate other fashion companies’ supply chain transparency based on data availability. It will also be meaningful to hear directly from tier 3 & 4 suppliers to understand their perception about improving the apparel supply chain’s transparency and related opportunities and challenges.

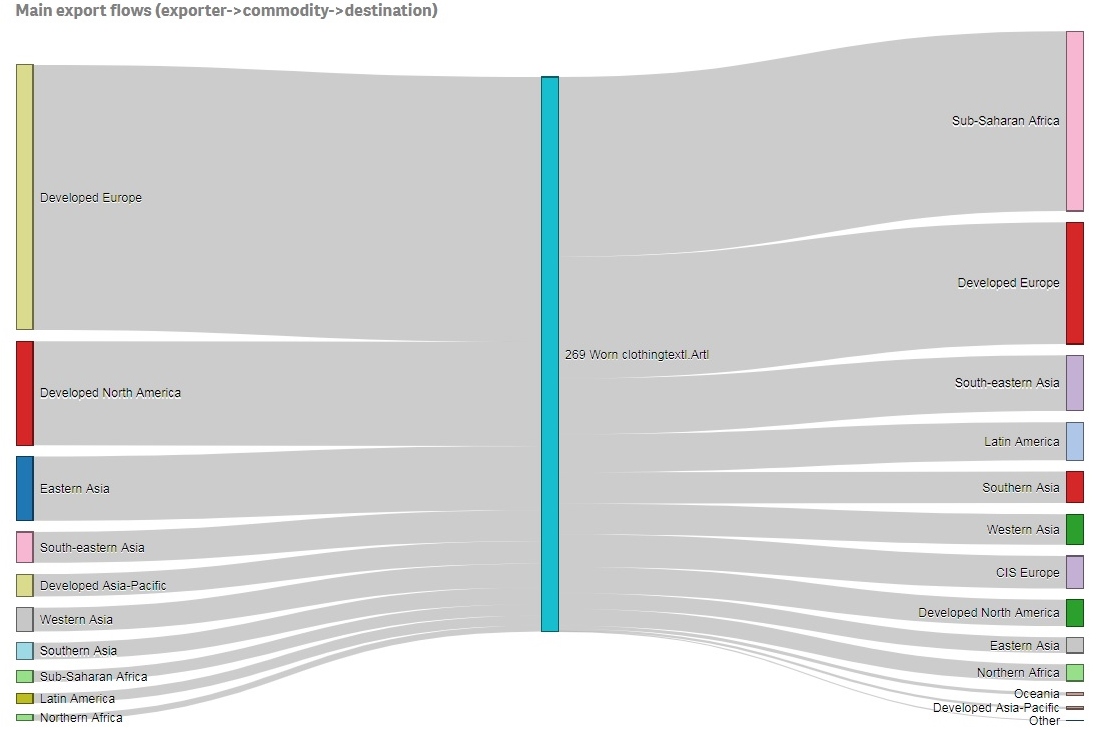

Used clothing trade patterns (data source: UNComtrade (2021)

This study intends to explore the key factors that affect the volume of a country’s used clothing exports. Notably, the world’s used clothing exports (defined as the Harmonized System code 6309) substantially increased from only $2.5 billion in 2009 to over $4.2 billion in 2019, or up 63.4% (UNComtrade, 2021). While numerous studies have explored the patterns of used clothing imports and their social-economic impacts on the importing countries, what drives a country’s used clothing exports remains largely unknown.

In the study, we conducted a regression analysis of 37 countries’ used clothing exports in 2019 (or over 90% of the value of the world’s used clothing exports that year) (UNComtrade, 2021). The explanatory factors we considered include new clothing sales (2018-2019), new clothing retail price (2018-2019), population (2019), and country classification (developed or developing in 2019). The results show that:

First, there is a strong positive relationship between a country’s new clothing sales and its used clothing exports. On average, a 1% increase in new clothing sales would result in a 0.85% increase in used clothing exports when holding other factors constant.

Second, as new clothing gets cheaper in the retail market, a country would export more used clothing and vice versa. Specifically, when the retail price for new clothing decreases by 1%, the value of used clothing export could increase by 1.2% on average when holding other factors constant.

Third, when holding other factors constant, used clothing exports from developed countries were 56% higher than in developing economies. Lower-income levels and various other social-economic factors (such as the awareness of sustainability and used clothing collection mechanism) could be the factors behind the phenomenon.

Fourth, the size of the population has NO significant impact on a country’s used clothing exports. This explains why a developed economy with a relatively small population (such as the Netherlands and Canada) exported far more used clothing than a populous developing one (such as India and Indonesia) in 2019 (Uncomtrade, 2021).

The study’s findings create new knowledge about the primary factors affecting the patterns of used clothing exports and have several important implications. First, the results suggest that we can do more on the supply side to curb the surge of used clothing exports, given the rising concerns about its controversial impacts on the developing world and the environment. Particularly, encouraging consumers to purchase fewer new clothing and shop more “slowly” can be among the most effective ways to reduce the supply of used clothing. Second, echoing the finding of existing studies, the results confirm the significant price impact on the generation of used clothing exports. Notably, the result reminds us about the enormous social-economic and environmental “cost” of selling new clothing too cheaply. Additionally, the findings suggest that developed countries have a crucial role in addressing the used clothing export problem, even those with a relatively small population.

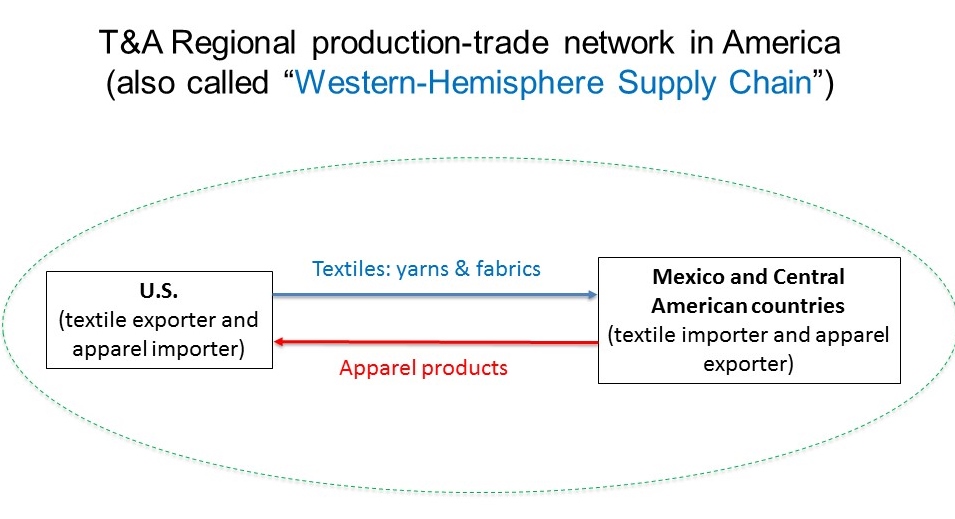

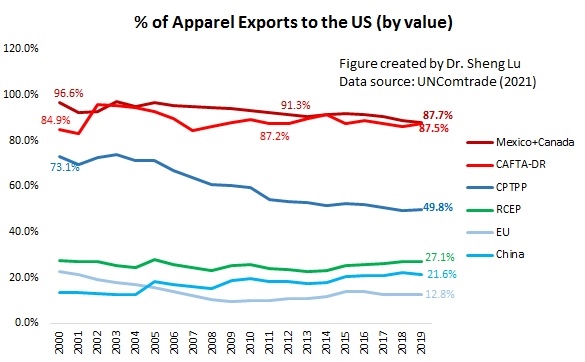

Within the Western-Hemisphere (WH) textile and apparel supply chain, the United States serves as the leading textile supplier, whereas developing countries in North, Central, and South America (such as Mexico and countries in the Caribbean region) assemble imported textiles from the United States or elsewhere into apparel. The majority of clothing produced in the area is eventually exported to the United States or Canada.

WH countries still form a close supply chain partnership in textile and apparel production. For example, close to 70% of US textile exports went to WH members in 2020, a pattern that has stayed stable over the past decades (OTEXA, 2021). Meanwhile, the United States serves as the single largest export market for most apparel exporting countries in the WH For example, in 2019, close to 89% of apparel exports from CAFTA-DR and USMCA (NAFTA) members went to the US.

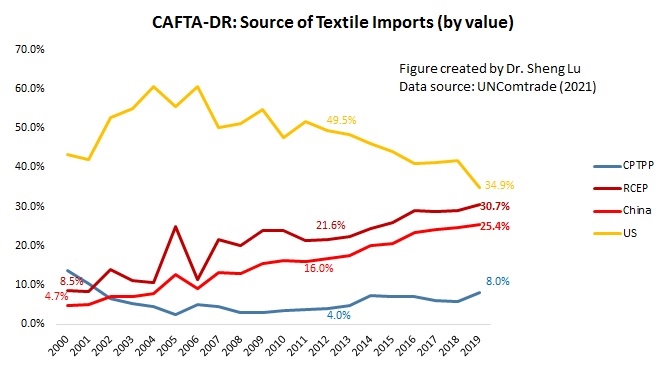

However, the WH textile and apparel supply chain is not without significant challenges. For example, CAFTA-DR and Mexico are increasingly using textiles inputs from outside the WH region, which weakens the US role as a dominant textile supplier. Notably, most of the market shares lost by US textile suppliers are fulfilled by Asian countries, including China and other members of the RCEP (Regional Comprehensive Economic Partnership). Theoretically, using cheaper textile inputs from Asia may help apparel producing countries in the WH improve the price competitiveness of their finished garments and diversify their export markets beyond the US.

Meanwhile, despite the apparent popularity of “near-sourcing”, no evidence suggests that US fashion brands and retailers are sourcing more from WH countries, including CAFTA-DR and USMCA (NAFTA) members. Neither the US-China trade war nor COVID-19 seems to have shifted the trends. Instead, close to 75%-80% of US apparel imports still come from Asian countries (OTEXA, 2021). Studies further show that a vast majority of US apparel imports from WH concentrate on a limited category of products, such as tops and bottoms, which is far from sufficient to meet retailers’ sourcing needs.

On the other hand, technical textiles and industrial textiles account for a growing share in the total US textile exports, and Asia is a particularly fast-growing market. However, there is few US free trade agreement with Asian countries, making it a disadvantage to promote “Made in the USA” products in these markets. It is debatable what should be the priority for the US textile and apparel trade policy: to continue to protect the exports of yarn and fabrics to the WH or open new export markets for technical and industrial textiles outside the WH region?

The EU region as a whole remains one of the world’s leading producers of textile and apparel (T&A). The value of EU’s T&A production totaled EUR137.3 bn in 2019, down around 2% from a year ago (Note: Statistical Classification of Economic Activities or NACE, sectors C13, and C14). The value of EU’s T&A output was divided almost equally between textile manufacturing (EUR68.7bn) and apparel manufacturing (EUR68.6bn).

Regarding textile production, Southern and Western EU, where most developed EU members are located such as Germany, France, and Italy, accounted for nearly 75% of EU’s textile manufacturing in 2019. Further, of EU countries’ total textile output, the share of non-woven and other technical textile products (NACE sectors C1395 and C1396) has increased from 19.2% in 2011 to 23.0% in 2017, which reflects the on-going structural change of the sector.

Apparel manufacturing in the EU includes two primary categories: one is the medium-priced products for consumption in the mass market, which are produced primarily by developing countries in Eastern and Southern Europe, such as Poland, Hungary, and Romania, where cheap labor is relatively abundant. The other category is the high-end luxury apparel produced by developed Western EU countries, such as Italy, UK, France, and Germany.

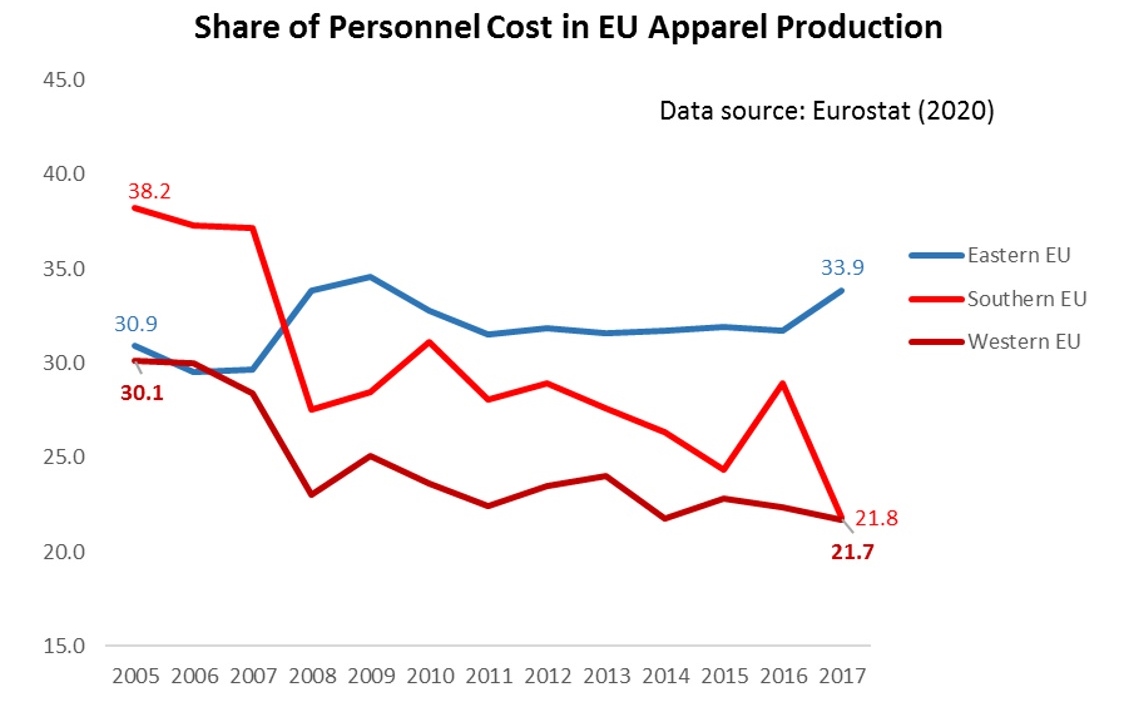

It is also interesting to note that in Western EU countries, labor only accounted for 21.7% of the total apparel production cost in 2017, which was substantially lower than 30.1% back in 2006. This change suggests that apparel manufacturing is becoming capital and technology-intensive in some developed Western EU countries—as companies are actively adopting automation technology in garment production.

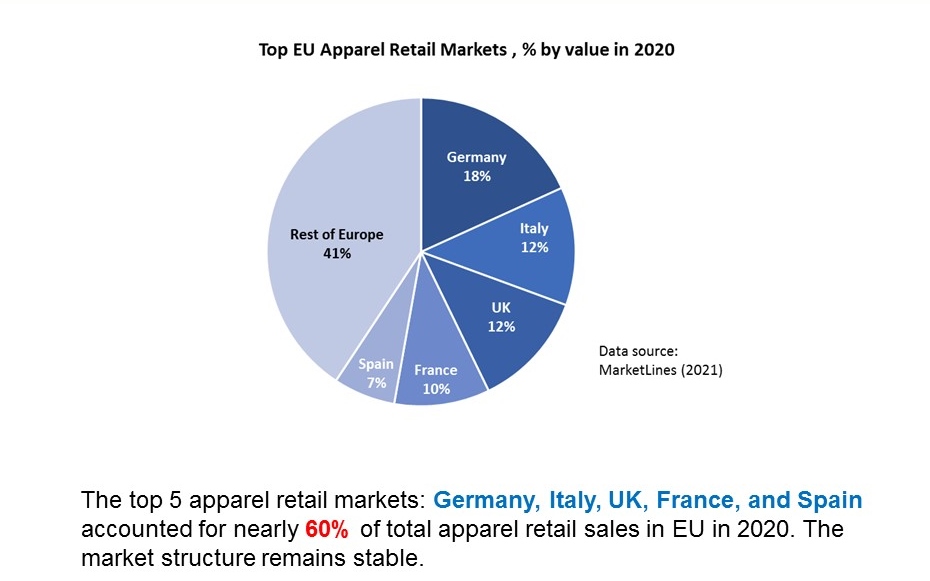

Because of their relatively high GDP per capita and size of the population, Germany, Italy, UK, France, and Spain accounted for nearly 60% of total apparel retail sales in the EU in 2020. Such a market structure has stayed stable over the past decade.

Data source: UNcomtrade (2021)

Intra-region trade is an important feature of the EU’s textile and apparel industry. Despite the increasing pressure from cost-competitive Asian suppliers, statistics from UNComtrade show that of the EU region’s total US$73.8bn textile imports in 2019, as much as 54.6% were in the category of intra-region trade. Similarly, of EU countries’ total US$204.0bn apparel imports in 2019, as much as 37.4% also came from other EU members. In comparison, close to 98% of apparel consumed in the United States are imported in 2019, of which more than 75% came from Asia (Eurostat, 2021; UNComtrade, 2021).

Regarding EU countries’ textile and apparel trade with non-EU members (i.e., extra-region trade), the United States remained one of the EU’s top export markets and a vital textile supplier (mainly for technical and industrial textiles). Meanwhile, Asian countries served as the dominant apparel sourcing base outside the EU region for EU fashion brands and retailers.

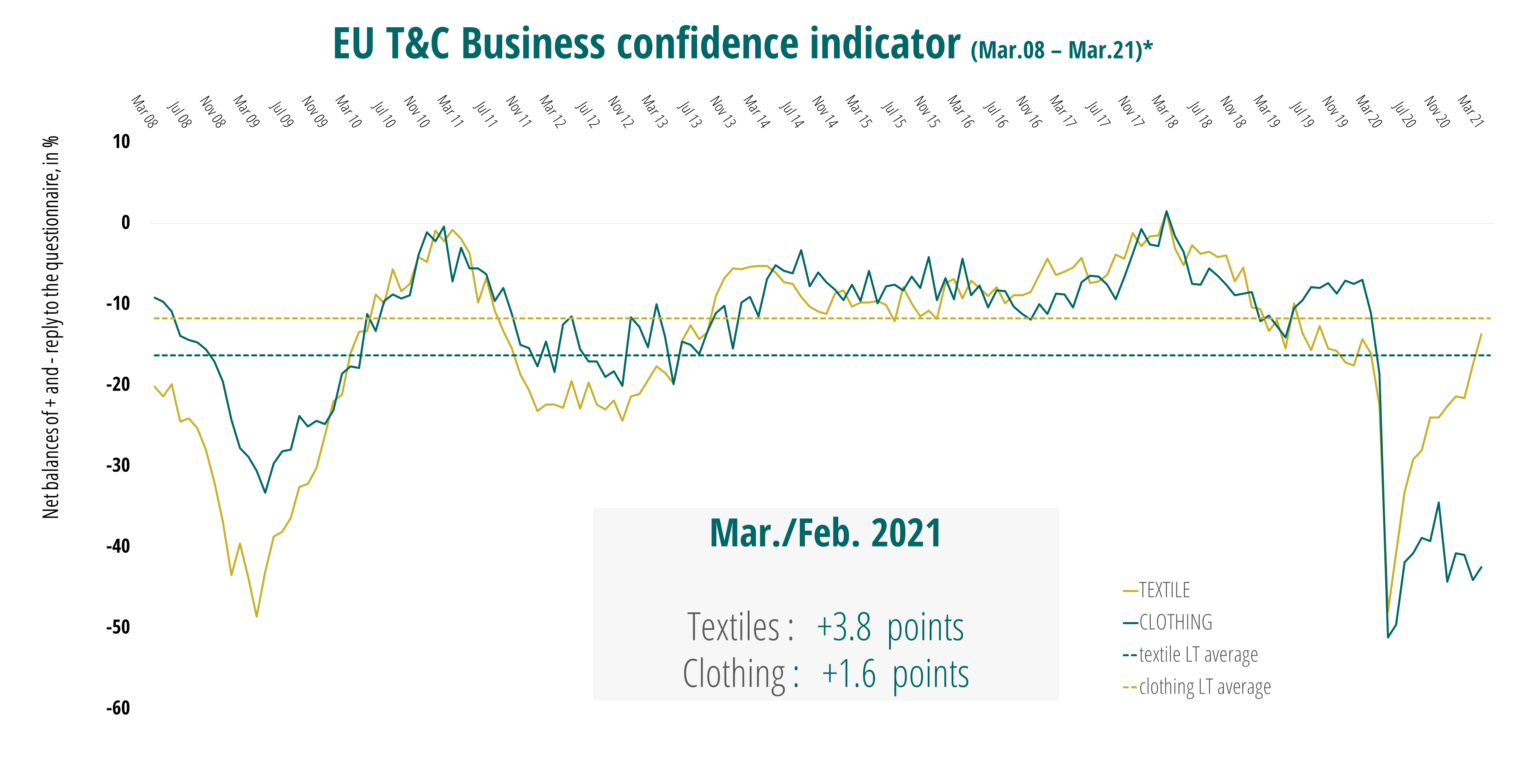

2021 hopefully will be a year of recovery and growthfor the EU textile and apparel industry. According to Euratex, the EU Business Confidence indicator of March 2021 gained momentum, with a confirmed upward trend in the textile industry (+3.8 points), and a modest recovery in the clothing industry (+1.6 points). However, Euratex also noted that EU textile and apparel companies still face daunting challenges and uncertainties in 2021, ranging from the rising raw material price, increasing transportation cost, to political instability in some key sourcing destinations (such as China and Myanmar).

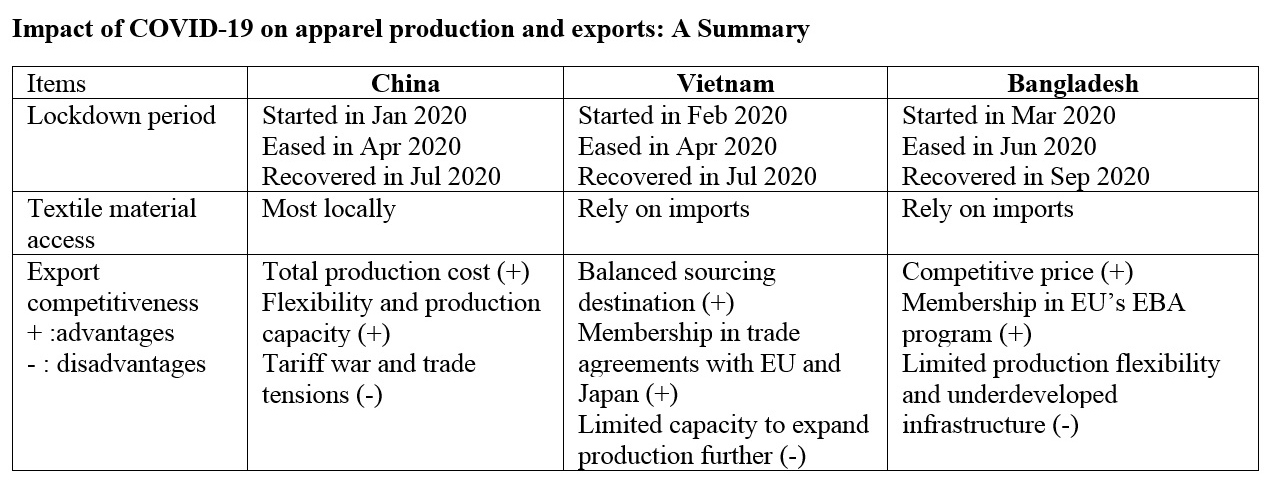

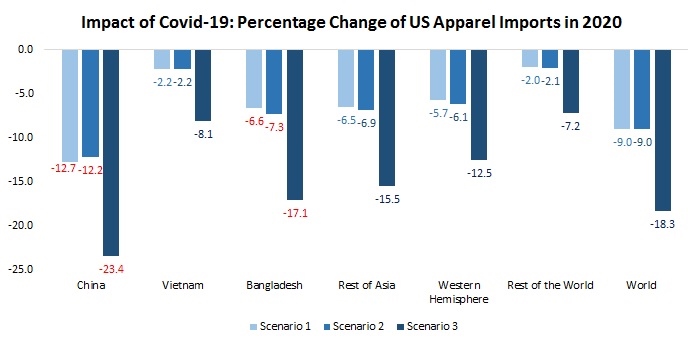

During the pandemic, three factors are most relevant to a country’s apparel export performance: government lockdown measures, textile raw material access, and comprehensive export competitiveness. Against these three factors, apparel producers and exporters in China, Vietnam, and Bangladesh face common but differentiated business challenges and opportunities during the pandemic (see the table above).

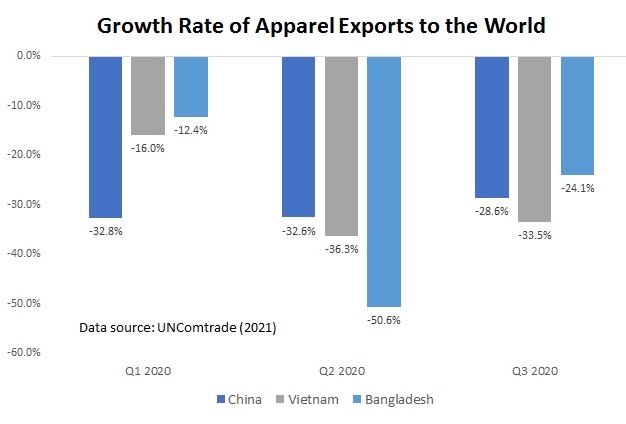

China, Vietnam, and Bangladesh all suffered an unprecedented (nearly 30% year over year) drop in their apparel exports to the world in 2020 (Q1-Q3) due to COVID-19. This result mirrored the reduced import demand in the world’s major apparel consumer markets, where the local economies were also hit hard by the pandemic, including the US (down 2.3%), the EU (down 4.3%), and Japan (down 4.8%).

However, the three countries’ export performance is most different in the US market—China’s apparel exports dropped by 31.6%, much steeper than Vietnam (down 6.9%) and Bangladesh (down 12.6%). It seems that even though COVID-19 may favor China as an apparel sourcing base from an economic perspective, US fashion companies have given more weight to non-economic factors, such as the outlook of the trade war, in their sourcing decisions involving China.

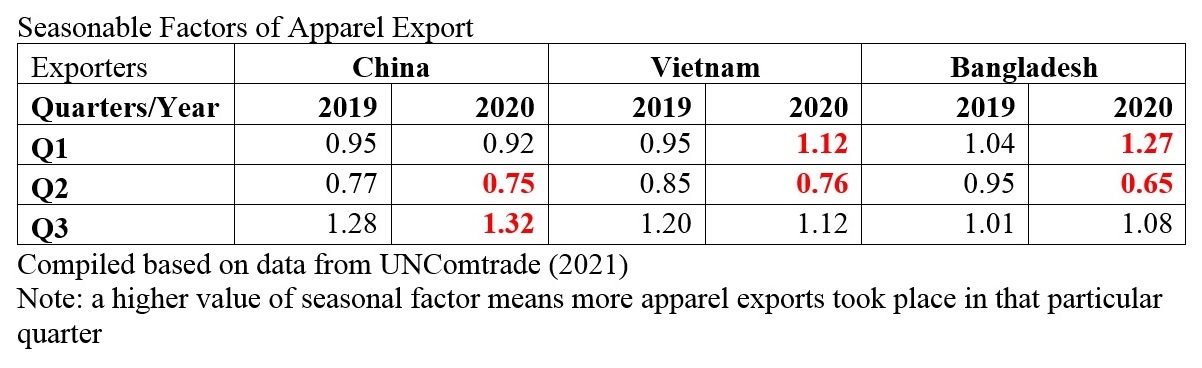

COVID-19 had disrupted apparel exporters’ regular production and export schedule in 2020. The lockdown measures in these three countries seem to affect their export seasonal pattern most significantly. For example, as the first country hit by COVID-19, China’s apparel exports were at the bottom from February to April 2020; however, China’s apparel exports recovered quickly since May 2020 when factories resumed production. In comparison, apparel exports from Vietnam and Bangladesh were at their lowest level from April to May and May to June 2020, respectively, when their factories had to close.

Additionally, Bangladesh’s apparel export seasonality had experienced a more dramatic change in 2020 than in China and Vietnam. A possible reason behind the phenomenon is the export product structure. Notably, China and Vietnam export a more diverse range of products, whereas apparel exports from Bangladesh concentrate on basic fashion items.

Industry sources also indicate that between February 2020 and February 2021, US apparel imports from China and Vietnam see a significant structural change—they include more COVID-popular items such as sweaters, smock dresses, and sweatpants, and fewer dresses, shirts, and suits. However, over the same period, the product structure of US apparel imports from Bangladesh barely changed, and they also included few COVID-popular categories mentioned above. In other words, despite order cancellations, garment factories in China and Vietnam seem more likely to receive new sourcing orders than their counterparts in Bangladesh because of advantages in production flexibility and agility.

Further, China, Vietnam, and Bangladesh all turned less diversified in their apparel export market during the pandemic. Notably, the US, EU, and Japan have become more critical export markets ever. Compared with fashion companies’ efforts in sourcing diversification, it could be more challenging for garment-producing countries to diversify their export market during the pandemic.

[for FASH455 in spring 2022: If you comment on this blog post, please respond to this question: as we are 2 years into the pandemic, why or why not do you think the study’s findings are still valid?]

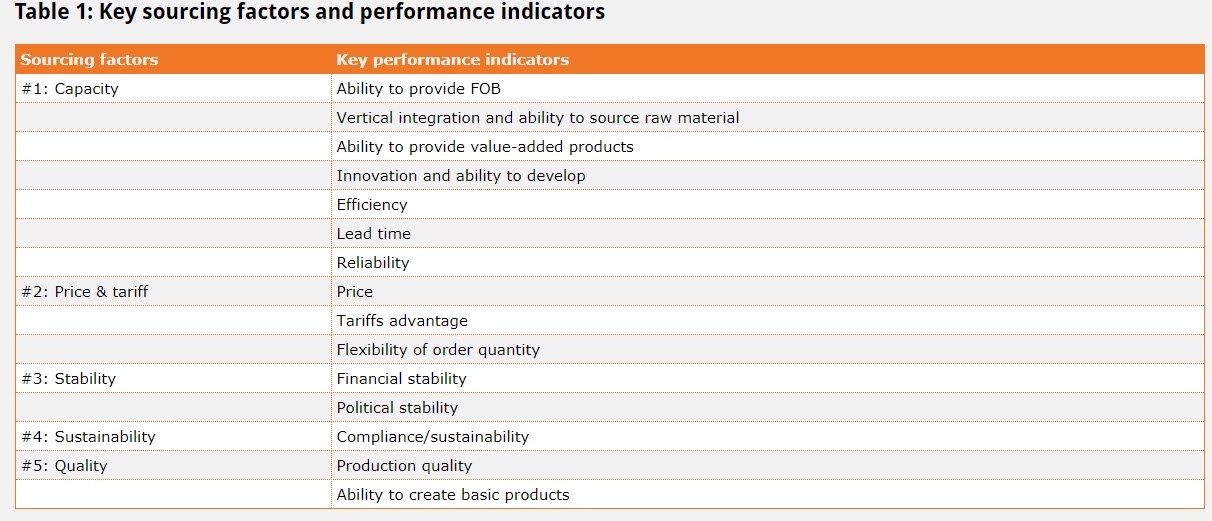

The apparel sourcing formula is getting ever more sophisticated today. US fashion brands and retailers consider a wide range of factors when deciding where to source their products. The long list of sourcing factors includes #1 Capacity, #2 Price & tariff, #3 Stability, #4 Sustainability, and #5 Quality (see the table below).

When evaluating the world’s top 27 largest apparel supplying countries’ performance, no souring destination appears to be perfect. In general, fashion brands and retailers have many choices for sourcing destinations that can meet their demand for production capacity, price point, and quality. However, fashion companies face much more limited options when seeking an apparel sourcing destination with a stable financial and political environment and a strong sustainability record.

When we compare the trade volume and the performance against the five primary sourcing factors:

Apparel sourcing today is no longer a “winner takes all” game. Notably, the factor “Capacity” is suggested to have limited impacts on the value of apparel imports from a particular sourcing destination.

Apparel sourcing is not merely about “competing on price” either--the impact of the factor “Price & tariff” on the pattern of apparel imports statistically is not significant.

Improving financial and political stability as well as product quality can help a country enhance its attractiveness as an apparel sourcing base. In particular, American and Asia-based fashion companies seem to give substantial weight to the factors of “Stability” and “Product quality” in their sourcing decisions.

Fashion companies’ current sourcing model does not always provide strong financial rewards for sustainability. Interestingly, the result indicates that a higher score for the factor “sustainability” does NOT result in more sourcing orders at the country level. Behind the result, fashion companies today likely consider sustainability and compliance at the vendor level rather than at the country level in their sourcing decisions. It is also likely that sustainability and compliance are treated more as pre-requisite or “bottom-line” criteria instead of a factor to determine the volume of the sourcing orders.

In conclusion, fashion companies’ sourcing decisions seem to be more complicated and subtle than what is often described in public.

While textile and apparel is well-known as a global sector, the latest statistics show that world textile and apparel trade patterns remain largely regional-based. Three particular regional textile and apparel trade flows are critical to watch:

First, Asian countries are increasingly sourcing textile raw material from within the region. As much as 85% of Asian countries’ textile imports came from other Asian countries in 2019, a substantial increase from only 70% in the 2000s. This result reflects the formation of an ever more integrated regional textile and apparel supply chain in Asia. However, as Asian countries become more economically integrated, textile and apparel producers in other parts of the world could find it more challenging to get involved in the region. With the recent reaching of several mega free trade agreements among countries in the Asia-Pacific region, such as the Regional Comprehensive Economic Partnership (RCEP), the pattern of “Made in Asia for Asia” is likely to strengthen further.

Second, the EU intra-region trade pattern for textile and apparel stays relatively strong and stable. Intra-region trade refers to trade flows between EU members. Statistics show that 54.6% of EU(27) members’ textile imports and 37.4% of their apparel imports came from within the EU(27) region in 2019. This pattern only slightly changed over the past decade. In other words, despite the reported increasing competition from Asian suppliers, many of which even enjoy duty-free market access to the EU market (such as through the EU Everything But Arms program), a substantial share of apparel sold in the EU markets are still locally made.

EU consumers’ preferences for “slow fashion” (i.e., purchasing less but for more durable products with higher quality) may contribute to the stable EU intra-region trade pattern. Many EU consumers also see textile and apparel as cultural products and do NOT shop simply for the price. This explains why Western EU countries such as Italy, Germany, and France rank the top apparel producers and exporters in the EU region despite their high wage and production costs.

Third, the Western Hemisphere (WH) supply chain faces significant challenges despite the seemingly growing popularity of “near-sourcing.” On the one hand, textile and apparel exporters in the Western-Hemisphere still rely heavily on the regional market. In 2019, respectively, as much as 79% of textiles and 86% of apparel exports from countries in the Western Hemisphere went to the same region.

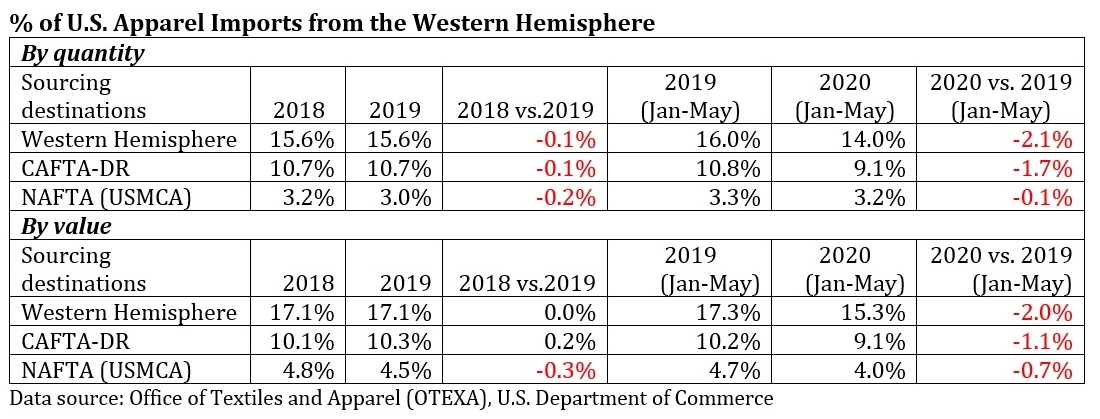

However, on the other hand, the Western-Hemisphere supply chain is facing increasing competition from Asian suppliers. For example, in 2019, only 22% of North, South, and Central American countries’ textile imports and 15% of their apparel imports came from within the Western Hemisphere, a new record low in ten years. Similarly, in the first eleven months of 2020, only 15.7% of US apparel imports came from the Western Hemisphere, down from 17.1% in 2019 before the pandemic. The limited local textile production capacity and the high production cost are the two notable factors that discourage US fashion brands and retailers from committing to more “near-sourcing” from the Western Hemisphere.

In comparison, Asian countries supplied a new record high of 62.2% of textiles and 75% apparel to countries in the Western Hemisphere in 2019, up from 49.1% and 71.1% ten years ago. This trend suggests that as the competitiveness of “Factory Asia” continues to improve, even regional trade agreements (such as USMCA and CAFTA-DR) and their restrictive “yarn-forward” rules of origin have limits to protect the Western Hemisphere supply chain.

In comparison, Asian countries supplied a new record high of 62.2% of textiles and 75% apparel to countries in the Western Hemisphere in 2019, up from 49.1% and 71.1% ten years ago. This trend suggests that as the competitiveness of “Factory Asia” continues to improve, even regional trade agreements (such as USMCA and CAFTA-DR) and their restrictive “yarn-forward” rules of origin have limits to protect the Western Hemisphere supply chain.

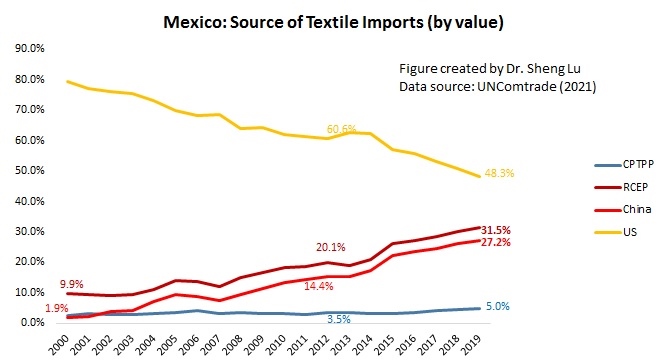

Additionally, many say that the reaching of RCEP creates new pressure for the new Biden administration to consider joining the CPTPP and strengthening economic ties with countries in the Asia-Pacific region. Notably, several USMCA and CAFTA-DR members, such as Mexico, also have RCEP or CPTPP membership. Apparel producers in these Western Hemisphere countries may find it more rewarding to access the cheaper textile raw material from Asia through CPTPP or RCEP rather than claiming the duty-saving benefits for finished garments under USMCA or CAFTA-DR. Like it or not, the Biden administration’s inaction will also have consequences.

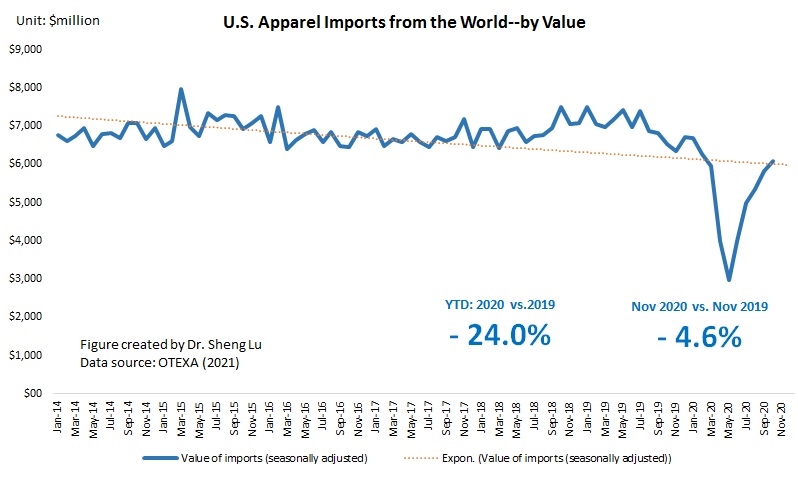

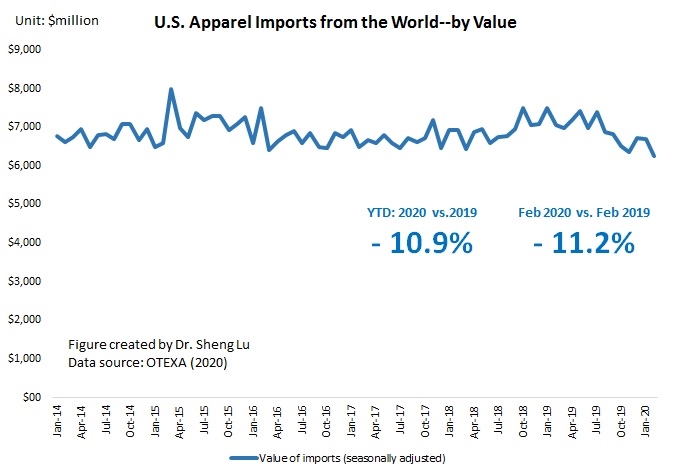

First, affected by the surge of COVID cases and consumers’ slowed spending, the value of U.S. apparel imports decreased by 15.7% in December 2020, the worst performance since September 2020. Specifically, the value of U.S. apparel imports in December 2020 shrank by 6.4% from November 2020 (seasonally adjusted), compared with an 8.8% growth from Aug to September, a 4.6% growth from September to October (seasonally adjusted), and a slight 0.3% decline from October to November (seasonally adjusted).

The substantial drop of U.S. apparel imports in December 2020 also altered the recovery trajectory. Overall, the outlook of US apparel imports in 2021 is hopeful but remains far from uncertain.

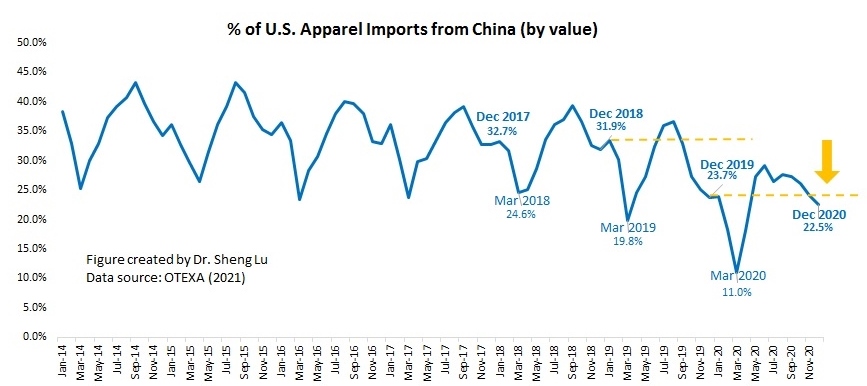

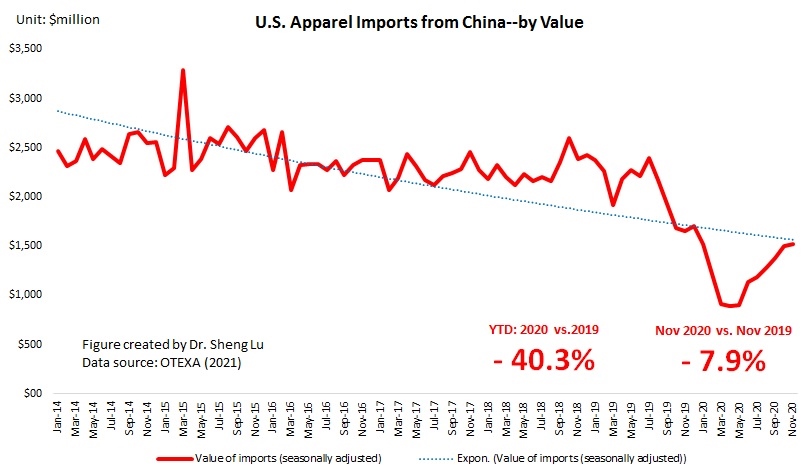

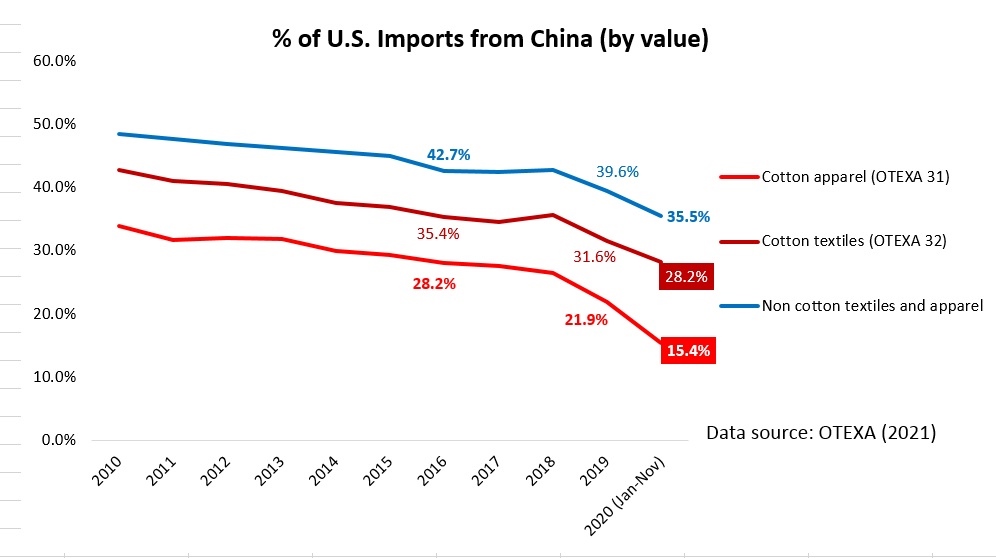

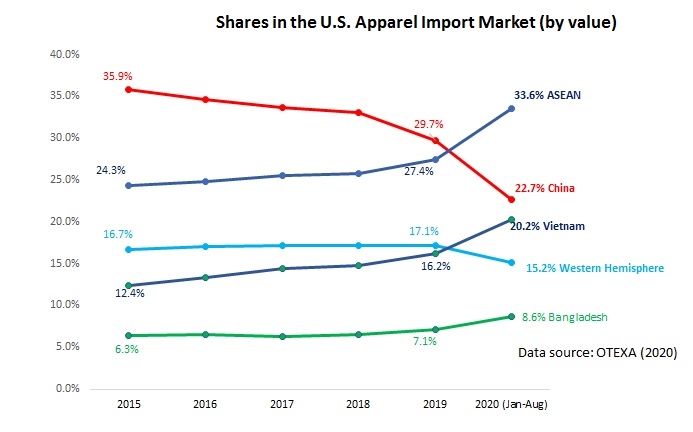

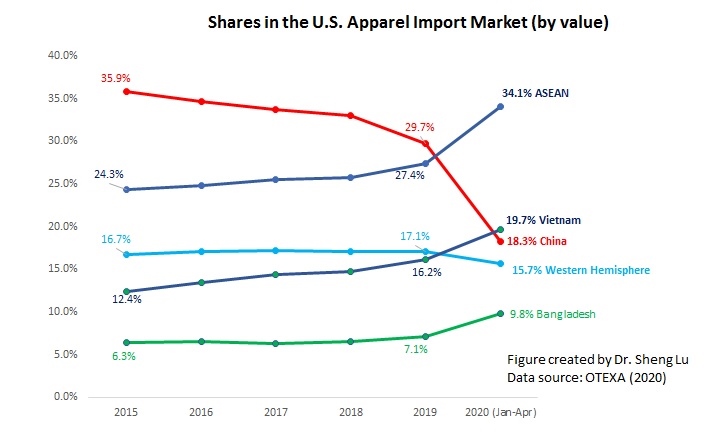

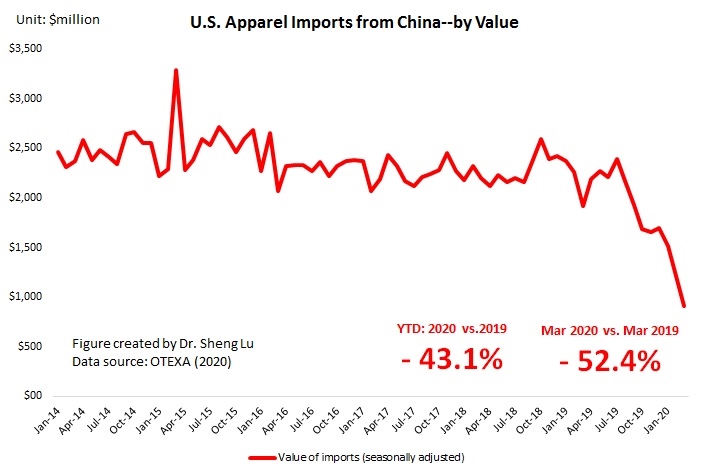

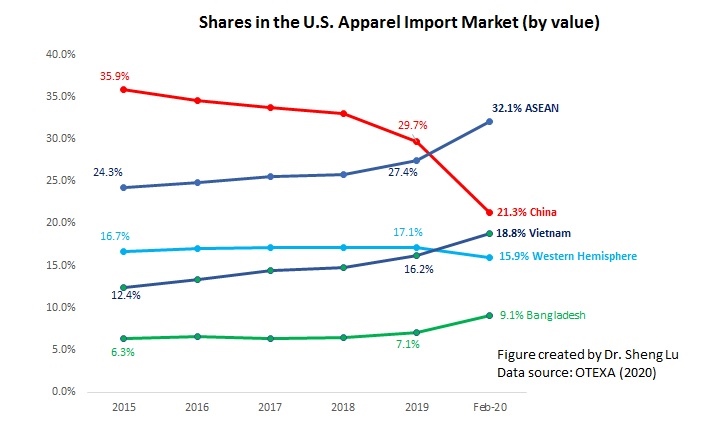

Second, supporting the findings of some recent studies, data suggests that U.S. fashion brands and retailers continue to reduce their “China exposure” in 2020. For example, both the HHI index and market concentration ratios (CR3 and CR5) suggest that apparel sourcing orders are gradually moving from China to other Asian countries. Measured by value, only 23.7% of U.S. apparel imports came from China in 2020, a new record low in the past ten years (was 29.7% in 2019 and 33% in 2018).

However, China’s apparel exports to the US lost more market shares from 2018-2019 than 2019-2020–it seems the impact of the trade war is more significant than the COVID.

The latest data confirms the concerns that some non-economic factors negatively affect China’s prospect as an apparel sourcing destination. For example, the reported forced labor issue related to Xinjiang, China, and a series of actions taken by the U.S. government (such as the CBP withhold release orders) have significantly affected U.S. cotton apparel imports from China. Measured by value, only 15.4% of U.S. cotton apparel came from China in 2020, compared with 22.2% in 2019 and 28% back in 2017. While China’s total textile and apparel exports to the US dropped by 30.7% in 2020, China’s cotton textiles and cotton apparel exports to the US went down more sharply by nearly 40%.

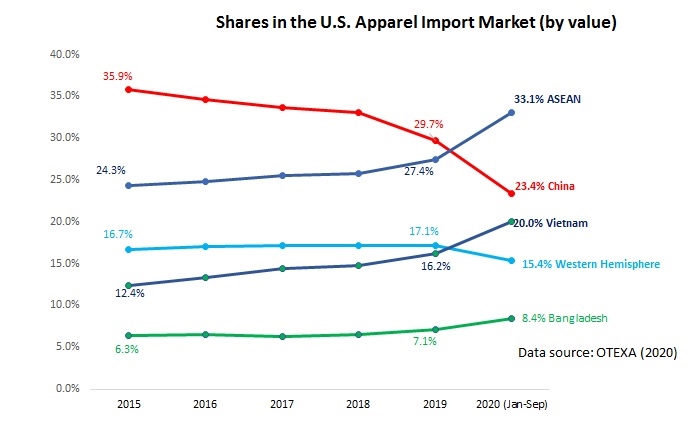

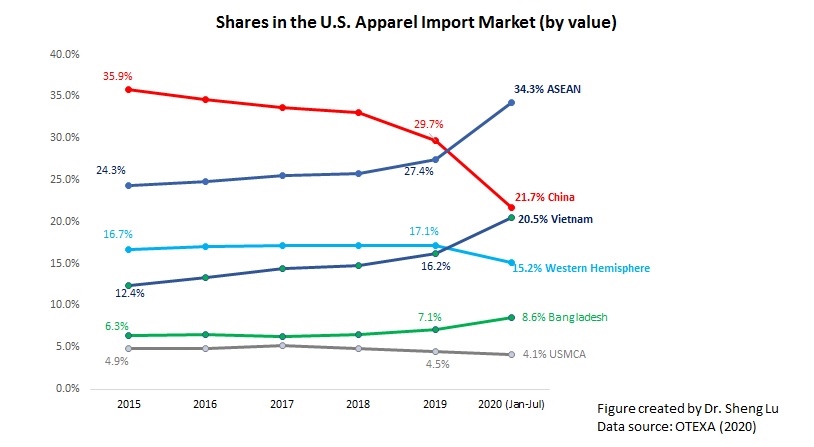

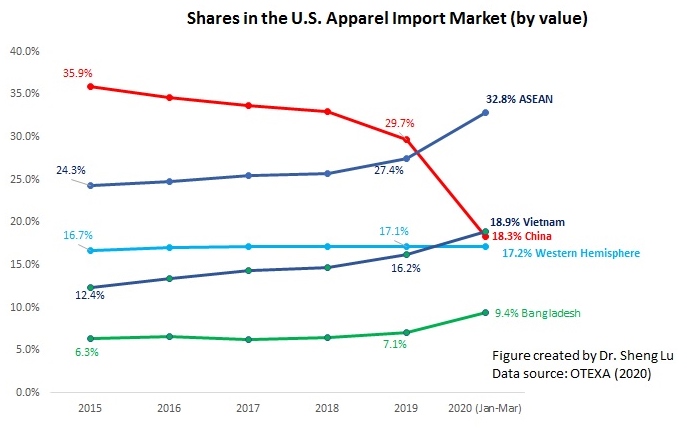

Third, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (19.6% in 2020 vs. 16.2% in 2019), ASEAN (32.3% in 2020 and vs. 27.4% in 2019), Bangladesh (8.2% in 2020 vs.7.1% in 2019), and Cambodia (4.4% in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

Fourth, due to seasonal factors, around 21% of U.S. apparel imports came from the Western Hemisphere in December 2020. Notably, to fulfill consumers’ last-minute holiday orders, which require faster speed to market, U.S. fashion companies typically do relatively more near-sourcing from September to December. In comparison, U.S. fashion companies place more sourcing orders with Asian suppliers from June to late September/early October.

However, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the U.S.-China tariff war. In 2020, 9.6% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from USMCA members (down from 4.5% in 2019).

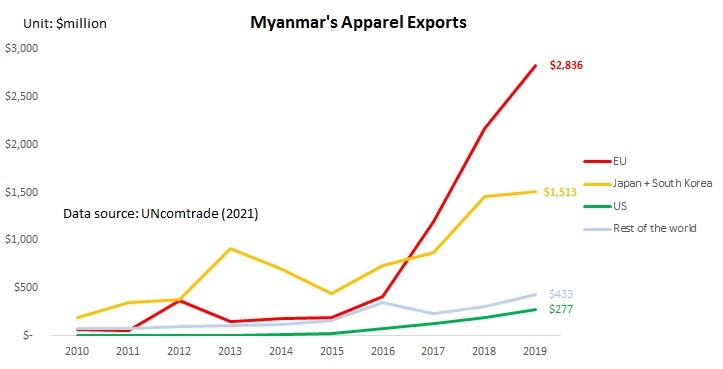

First, the textile and apparel industry plays a significant role in Myanmar’s economy, particularly the export sector. Data from the UNComtrade shows that textile and apparel accounted for nearly 30% of Myanmar’s total merchandise exports in 2019, followed by footwear and luggage. Industry data also indicates that the textile, apparel, and footwear industry employed more than 1.1 million workers in Myanmar in 2018, up from only 0.3 million in 2016.

On the other hand, as a developing country, Myanmar highly depends on the imported textile raw material. As of 2019, nearly 83% of Myanmar’s textile imports came from China.

Second, since the United States lifted the import ban on Myanmar and the EU reinstated the Everything But Arms (EBA) trade preferences for the country in 2013, Myanmar has been one of the most popular emerging apparel sourcing bases among fashion companies. From 2015 to 2019, Myanmar’s apparel exports to the world enjoyed an impressive 57% annual growth. Myanmar’s apparel exports to the EU (97% annual growth) and the United States (78% annual growth) have been growing particularly fast.

From 2019 to 2020, some of the top fashion brands that carry apparel items “Made in Myanmar” include United Colors of Benetton, Next, Only, Guess, Jack & Jones, and Mango.

Second, the reasons why fashion companies source apparel from Myanmar are multiple:

Thanks to foreign investment (e.g., nearly half of Myanmar’s garment factories are foreign-owned), Myanmar specializes in making relatively higher-quality functional/technical clothing (i.e., outwear like jackets and coats). This is different from many other apparel exporting countries like Bangladesh, Vietnam, and Cambodia, mostly exporting low-cost tops and bottoms.

Myanmar’s apparel exports were able to enjoy duty-free market access in the EU, Japan, and South Korea. Myanmar was also a beneficiary of the US Generalized System of Preferences (GSP) program. This explains why Myanmar’s apparel exports mostly go to the EU (56%), Japan and South Korea (30%), and the US (5.5%).

Relatively low production cost—garment workers earn around $85/month in 2019.

However, Myanmar still accounts for a tiny share in fashion companies’ total sourcing portfolio because of the size effect. For example, as of 2019, less than 0.1% of US and EU countries’ apparel imports came from Myanmar.

Third, western fashion brands could reevaluate their sourcing strategy from Myanmar because of its recent coup. Notably, in a new study, we find that apparel sourcing is not merely about “competing on price.” Instead, fashion companies give substantial weight to the factors of “political stability” and “financial stability” in their sourcing decisions—reputation risk matters. The country’s latest political instability will hurt Myanmar’s attractiveness as an apparel sourcing base, given many other alternatives out there.

Further, the international community, including the US and the EU, is considering new sanctions against Myanmar. Should Myanmar lose its EU’s EBA eligibility or no longer enjoy duty-free access to its key apparel export markets, the country’s apparel exports could be among the biggest losers. Notably, it could be challenging for Myanmar to find an alternative apparel export market during the pandemic. (for example, only 1.3% of Myanmar’s apparel exports went to China in 2019).

What do you see as the biggest challenges – and opportunities – facing the apparel industry in 2021?

I see COVID-19 and market uncertainties caused by the contentious US-China relations as the two most significant challenges facing the apparel industry in 2021.

The difficulties imposed by COVID-19 on fashion businesses are twofold. First, with the resurgence of COVID cases worldwide, when and how quickly apparel consumption can rebound to the pre-COVID level remain hard to tell, particularly in leading consumption markets, including the United States and Europe. As the apparel business is buyer-driven, the industry’s full recovery is impossible without a strong return of consumers’ demand. Numerous studies also show that switching to making and selling PPE won’t be sufficient to make up for losses from regular businesses for most fashion companies.

Second, COVID-19 will also continue to post tremendous pressures on the supply side. In the 2020 Fashion Industry Benchmarking Study, which I conducted in collaboration with the US Fashion Industry Association (USFIA), the surveyed sourcing executives reported severe supply chain disruption during the pandemic. These disruptions come from multiple aspects, ranging from a labor shortage, a lack of textile raw materials, and a substantial cost increase in shipping and logistics. Even more concerning, many small and medium-sized (SME) vendors, particularly in the developing countries, are near the tipping point of bankruptcy after months of struggle with the order cancellation, mandatory lockdown measures, and a lack of financial support. The post-covid recovery of the apparel business relies on a capable, stable, and efficient textile and apparel supply chain, in which these SME vendors play a critical role.

In 2021, fashion companies also have to continue to deal with the ramifications of contentious US-China relations. On the one hand, the chance is slim that the punitive tariffs imposed on Chinese products, which affect most textiles and apparel, will soon go away. On the other hand, we cannot rule out the possibility that the US-China commercial relationship will deteriorate further in 2021, as more sensitive, complicated, and structural issues began to get involved, such as national security, forced labor, and human rights. Compared with President Trump’s unilateral trade actions, the new Biden administration may adopt a multilateral approach to pressure China. However, it also means more countries could be “dragged into” the US-China trade tensions, making it even more challenging for fashion companies to mitigate the trade war’s supply chain impacts.

Meanwhile, I see digitalization as a big opportunity for the apparel industry, not only in 2021 but also in the years to come. Fashion brands and retailers will increasingly find digitalization ubiquitous to their businesses—like air and electricity. In 2021, I expect fashion companies will make more efforts to creatively use digital technologies to interact with consumers, make transactions, develop products, and improve consumers’ online shopping experiences. Thanks to the adoption of digital tools, apparel companies may also find new opportunities to improve sustainability, better understand their customers through leveraging data science, and develop a more agile and nimble supply chain.

What’s happening with supply chains? How is the sourcing landscape likely to shift in 2021, and what can apparel firms and their suppliers do to stay ahead, remain competitive and build resilience for the future?

Apparel companies’ sourcing and supply chain strategies will continue to evolve in response to consumers’ shifting demand, COVID-19, and the new policy environment. Several trends are worth watching in 2021:

First, fashion companies’ sourcing bases at the country level will stay relatively stable in 2021 overall. For example, although it sounds a little contradictory, fashion companies will continue to treat China as an essential sourcing base and reduce their “China exposure” further, a process that has started years before the tariff war. Most apparel sourcing orders left China will go to China’s competitors in Asia, such as Vietnam, Bangladesh, and Cambodia. This also means that Asia, as a whole, will remain the single largest source of apparel imports, particularly for US and Asia-based fashion companies. In comparison, still, “near-sourcing” is NOT likely to happen on a large scale, mainly because “near-sourcing” requires enormous new investments to rebuild the supply chain, and most fashion companies do not have the resources to do so during the pandemic.

Second, sourcing diversification is slowing down at the firm level, and more apparel companies are switching to consolidate their existing sourcing base. For example, as the 2020 USFIA benchmarking study found, close to half of the respondents say they plan to “source from the same number of countries, but work with fewer vendors” through 2022. Another 20 percent of respondents say they would “source from fewer countries and work with fewer vendors.” The results are understandable– competition in the apparel industry is becoming supply chain-based. Building a strategic partnership with high-quality vendors will play an ever more critical role in supporting fashion brands and retailers’ efforts to achieve speed to market, flexibility and agility, sourcing cost control, and low compliance risk. Thus, apparel companies find it more urgent and rewarding to consolidate the existing sourcing base and resources and strengthen their key vendors’ relations.

Third, apparel sourcing executives still need to keep a close watch on trade policy in 2021. However, we may see fewer news headlines about trade and more “behind the door” advocacy and diplomacy. Specifically:

US Section 301 actions: While the punitive tariffs on Chinese goods may not go away anytime soon, there could be a fight over whether the new Biden administration should continue granting certain companies exclusions from those tariffs. Further, in October 2020, the Trump Administration launched two new Section 301 investigations on Vietnam regarding its import and use of timber and reported “undervaluation currency.” The case is pending, but the stakes are high for fashion companies —Vietnam is often treated as the best alternative to sourcing from China and already accounting for nearly 20% of total US apparel imports.

The US-China relationship: We all know the relationship is at its low-point, but the fact is many US fashion companies still treat China as one of their most promising markets to explore. China continues to expand its role in the Asia-based textile and apparel supply chain also. In a nutshell, more than ever, apparel executives need to care about what is going on in geopolitics. Hopefully, “tough times can breed positive outcomes.”

CPTPP and RCEP: With the reaching of the Regional Comprehensive Economic Partnership (RCEP) in November 2020, there are growing calls for the new Biden administration to consider rejoining the Trans-Pacific Partnership (TPP) in some format to showcase the US presence in the Asia-Pacific region. To make the situation even more complicated, China has openly expressed its interest in joining the Comprehensive Progressive Agreement of the Trans-Pacific Partnership (CPTPP), commonly known as “the TPP without the US.” 2021 will be a critical time window for all stakeholders, including the apparel sector, to debate various trade policy options that could shape the future trade architecture in the Asia-Pacific region.

Brexit: Brexit will enter a new phase in 2021 as the transition period ends on 31 December 2020. On the positive side, we have a playbook to follow—the UK has announced its new tariff schedules for various scenarios, which provide critical market predictability. We might also see the reaching of a new US-UK free trade agreement in the first half of the year, which will be exciting news for the apparel sector, particularly those in the luxury segment. However, as the US Trade Promotion Authority (TPA) is set to expire in July 2021, when and how soon such an agreement will enter into force will be another story. By no means trade policy in 2021 will go boring.

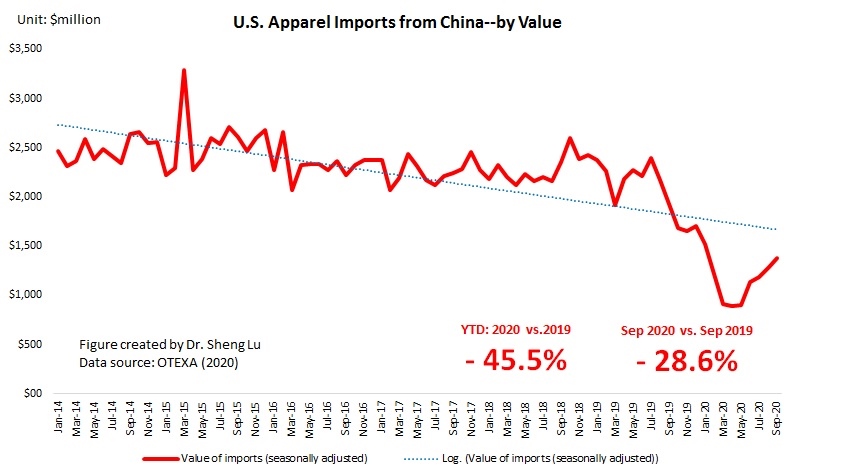

First, U.S. apparel imports continue to rebound thanks to consumers’ robust demand. However, the speed of recovery slowed. Specifically, The value of U.S. apparel imports in November 2020 marginally went down by 0.3% from October 2020 (seasonally adjusted), compared with an 8.8% growth from Aug to September and a 4.6% growth from September to October (seasonally adjusted).

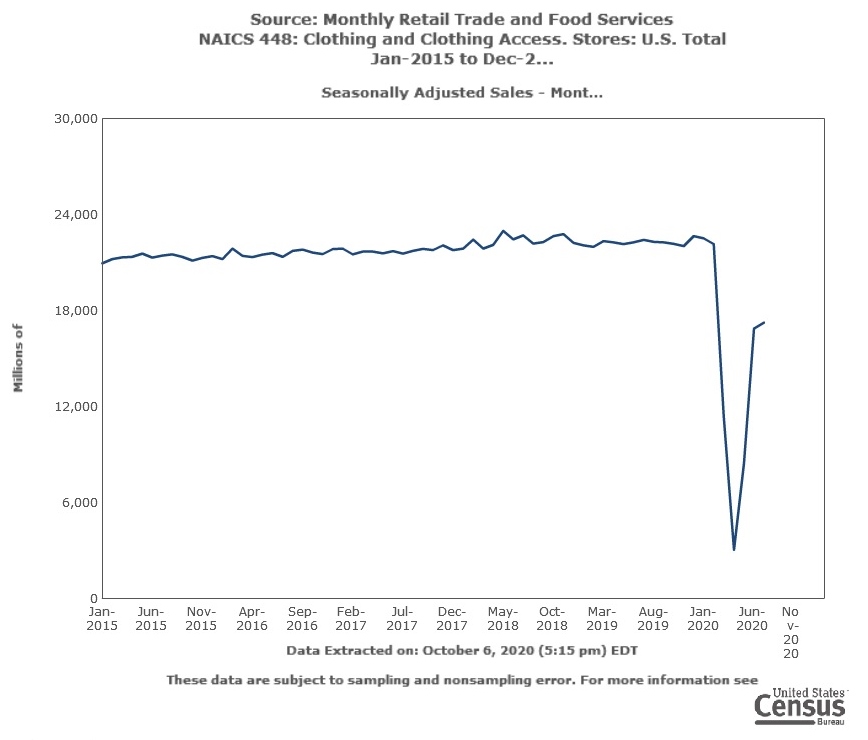

As of November 2020, the volume of U.S. apparel imports has recovered to around 85-90% of the pre-coronavirus level. This result echoes the trend of U.S. apparel retail sales (NAICS 4481), which also indicates a “V-shape” rebound since May 2020.

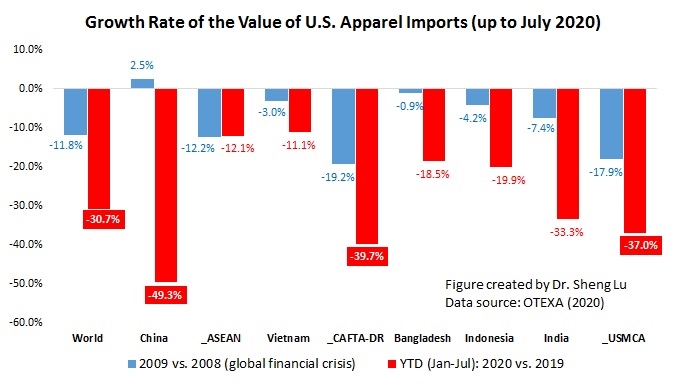

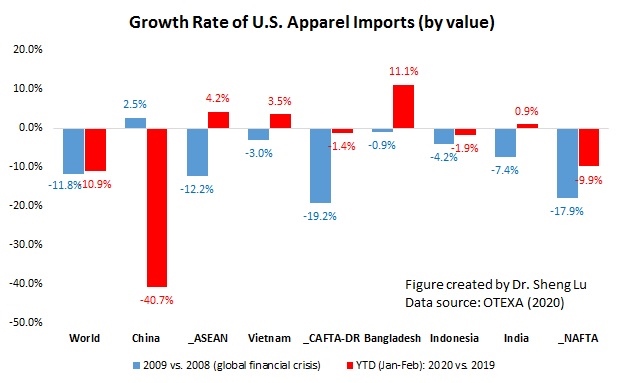

Data further shows that compared with the 2008 world financial crisis, Covid-19 has caused a more significant drop in the value of U.S. apparel imports. However, it seems the post-Covid recovery process has been more robust than the 2009 financial crisis. The Auto Regressive Integrated Moving Average (ARIMA) model forecasts that at the current speed of recovery, the value of U.S. apparel imports (seasonally adjusted) could start to enjoy a positive year over year (YoY) growth by February 2021 (or around 11 months after the outbreak of Covid-19 in March 2020). In comparison, when recovering from the 2008 world financial crisis, it took almost 15 months to turn the YoY growth rate from negative to positive).

With the new lockdown measures taken in response to the resurgence of the Covid cases, the outlook of US apparel imports remains uncertain. It should also be noted that the period from December to April usually is the light season for apparel imports.

Second, supporting the findings of some recent studies, data suggests that U.S. fashion brands and retailers continue to reduce their “China exposure” in 2020. For example, both the HHI index and market concentration ratios (CR3 and CR5) suggest that apparel sourcing orders are gradually moving from China to other Asian countries. Related, since August 2020, China’s market shares in total U.S. apparel imports have been sliding both in quantity and in value.

We should NOT ignore the impact of non-economic factors on China’s prospect as an apparel sourcing destination. For example, the reported forced labor issue related to Xinjiang, China, and a series of actions taken by the U.S. government (such as the CBP withhold release orders) have significantly affected U.S. cotton apparel imports from China. Measured by value, from January to November 2020, only 15.4% of U.S. cotton apparel came from China, compared with 22.2% in 2019 and 28% back in 2017. While China’s total textile and apparel exports to the US dropped by 32% in 2020 (Jan to Nov), China’s cotton textiles and cotton apparel exports to the US went down more sharply by 41.1% and 47.2%, respectively.

Third, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (19.8% YTD in 2020 vs. 16.2% in 2019), ASEAN (32.6% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.2% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.4% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 (Jan to Nov) from a year ago.

Fourth, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the U.S.-China tariff war. In the first eleven months of 2020, 9.4% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.4% from USMCA members (down from 4.5% in 2019). The limited local textile production capacity and the high production cost are the two notable disadvantages of sourcing from the region.

Suggested citation: Lu, Sheng. (2020). Textile and Apparel Products Covered by the U.S.-China Tariff War Reference List (updated December 2020). Retrieved from http://www.shenglufashion.com

The latest data collected from industry sources show that the monthly minimum wages for garment workers vary significantly in the world, ranging from as low as USD $26 in Ethiopia to USD $1,764 in Belgium in 2019. The world average stood at USD $470/month that year.

These figures echo the findings of a 2017 study by Public Radio International, which also shows a significant variation of the minimum wage level among garment workers worldwide. Meanwhile, there was no clear evidence that the minimum wage level in 2019 was notably higher than in 2017 in many countries we examined.

On the other hand, we need to interpret the minimum wage level in the context of the local living wage. According to the International Labor Organization (ILO), a living wage is defined as the theoretical income level that an individual must earn to pay for basic essentials such as shelter, food, and water in the country where a person resides. As shown in the figure above, a high minimum wage in absolute terms does not always guarantee a high standard of living and vice versa. For example, while the United States offers one of the world’s highest minimum wages for garment workers (USD $1,160/month), that minimum wage level was only about 70% of the living wage (USD $1,660/month) 2018-2019. In comparison, garment workers in Indonesia earned a much lower nominal minimum wage of USD $181/month. That wage level, however, was much higher than the reported USD $103/month living wage over the same period.

Additionally, the results suggest that fashion companies’ sourcing decision today is far more than just about “chasing the lowest wage or price.” For example, while China and Vietnam are the two largest apparel suppliers for the U.S. market, the minimum wage level for garment workers in the two countries have exceeded most of their competitors in Asia.

By Emma Davis (Research Assistant, Fashion and Apparel Studies, University of Delaware) and Dr. Sheng Lu

First, U.S. apparel imports continue to rebound thanks to consumers’ robust demand. The value of U.S. apparel imports in September 2020 went up by 8.8% from August 2020 (seasonally adjusted), a new record high since March 2020 when COVID-19 broke out in the States. As of September 2020, the volume of U.S. apparel imports has recovered to around 84-85% of the pre-coronavirus level. This result echoes the trend of U.S. apparel retail sales (NAICS 4481), which also indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports hopefully will last for another 1-2 months.

Data also shows that compared with the 2008 world financial crisis, Covid-19 has caused a more significant drop in the value of U.S. apparel imports. However, it seems the post-Covid recovery process has been more robust than the 2008 financial crisis. Notably, the Auto Regressive Integrated Moving Average (ARIMA) model forecasts that at the current speed of recovery, the value of U.S. apparel imports (seasonally adjusted) could start to enjoy a positive year over year (YoY) growth by February 2021 (or around 11 months after the outbreak of Covid-19 in March 2020). In comparison, when recovering from the 2008 world financial crisis, it took almost 15 months to turn the YoY growth rate from negative to positive.

Second, still, no evidence suggests that U.S. fashion companies are giving up China as one of their essential apparel-sourcing bases. Notably, since May 2020, China had quickly regained its position as the top apparel supplier to the U.S. market. From June to September 2020, China’s market shares have stably stayed at around 27-28% in value and 40-42% in quantity.

According to the media, some sourcing orders are returning to China as China’s competitors in Asia are struggling with more limited production capacity, shortage of raw material and supply chain disruption caused by Covid-19.

CR5 (exclude China) includes Vietnam, Bangladesh, Indonesia, India and Cambodia

That being said, trade data suggests that U.S. fashion companies continue to reduce their “China exposure” overall. For example, both the HHI index and the market concentration ratios (CR3–total market shares of top 3 suppliers and CR5–total market shares of top 5 suppliers) indicate that apparel sourcing orders are gradually moving from China to other Asian countries–it is interesting to see HHI, CR3 and CR5 all suggest a more diversified apparel sourcing base in 2020 (Jan-Sep) than in 2018 and 2019; however, the value of CR5 (exclude China) reached a new record high in 2020 (Jan-Sep).

Third, related to the point above, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.0% YTD in 2020 vs. 16.2% in 2019), ASEAN (33.1% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.4% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.4% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

Fourth, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first nine months of 2020, only 9.1% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.4% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first nine months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 26% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the major contributing factors.

Just an anecdote–according to some industry insiders, the booming of E-commerce during the pandemic may also possibly explain why “near sourcing” is not reflected in trade data despite its reported growing popularity. Specifically, US fashion retailers would:1) import products from Asia and stock them in the bonded warehouses in Mexico (note: bonded warehouse means dutiable goods may be stored, manipulated, or undergo manufacturing operations without payment of duty). 2) When US consumers place orders, the retailer will ship products directly from these bonded warehouses in Mexico to the final destination. Most importantly, retailers could take advantage of the US de minimis rule (i.e., goods valued at $800 or less could enter the U.S. duty-free one person one day) and avoid paying tariffs– even though these products are counted as imports from Asian countries that do not have a free trade agreement with the United States. In other words, these products are not officially treated as imports from Mexico even though they are shipped from bonded warehouse in Mexico.

The surveyed U.S. fashion companies demonstrate more readiness and interest in using the US-Mexico-Canada Trade Agreement (USMCA) for apparel sourcing purposes in 2020 than a year ago:

For companies that were already using NAFTA for sourcing, the vast majority (77.8 percent) say they are “ready to achieve any USMCA benefits immediately,” up more than 31 percent from 2019.

Even for respondents who were not using NAFTA or sourcing from the region, about half of them this year say they may “consider North American sourcing in the future” and explore the USMCA benefits.

Nevertheless, when asked about the potential impact of USMCA on companies’ apparel sourcing practices, some respondents expressed concerns about the rules of origin changes. These worries seem to concentrate on denim products in particular. For example, one respondent says, “USMCA changes negatively affects our denim jeans sourcing particularly with the new pocketing rules of origin.” Another adds, “Denim pocketing ROO change is a concern but manageable.”

It also remains to be seen whether USMCA will boost “Made in the USA” fibers, yarns, and fabrics by limiting the use of non-USMCA textile inputs. For example, while the new agreement expands the Tariff Preference Level (TPL) for U.S. cotton/man-made fiber apparel exports to Canada (typically with a 100 percent utilization rate), these apparel products are NOT required to use U.S.-made yarns and fabrics.

First, U.S. apparel imports continue to rebound thanks to consumers’ robust demand. The value of U.S. apparel imports in August 2020 went up by 7.6% from July 2020 (seasonally adjusted), a new record high since March 2020 when COVID-19 broke out in the States. As of August 2020, the volume of U.S. apparel imports has recovered to around 80% of the pre-coronavirus level. This result echoes the trend of U.S. apparel retail sales (NAICS 448), which also indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports hopefully will last for another 1-2 months.

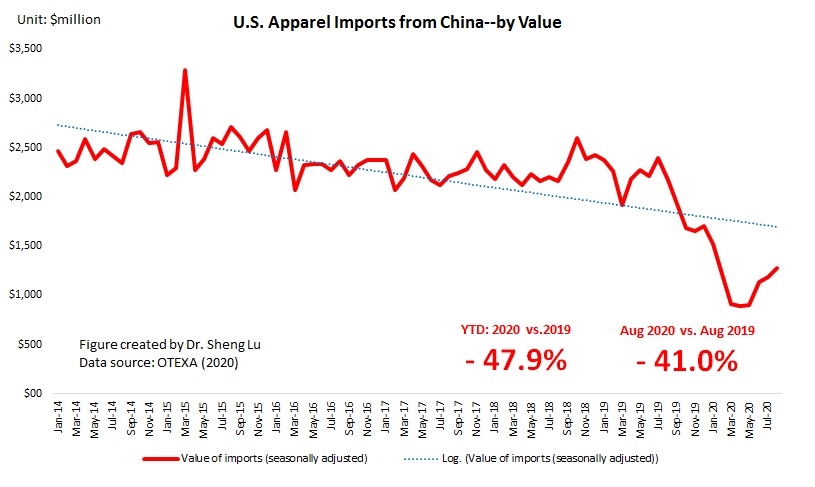

Nevertheless, between January and August 2020, the value of U.S. apparel imports decreased by almost 30% year over year, which has been MUCH worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

Second, no evidence suggests that U.S. fashion companies are giving up China as one of their essential apparel-sourcing bases. Notably, since May 2020, China had quickly regained its position as the top apparel supplier to the U.S. market. From June to August 2020, China’s market shares have stably stayed at around 27-28% in value and 40-42% in quantity.

Some industry sources show that “Made in China” enjoys two notable advantages that other apparel supplying countries cannot catch up in the short term. 1) unparalleled production capacity, meaning importers can source almost all products in any quantity from China vs. more limited production capacity (both in terms of variety and volume) in other alternative sourcing destinations. 2) China can mostly produce textile raw material locally vs. many apparel exporting countries still rely heavily on imported yarns and fabrics (supplied by China).

However, non-economic factors, particularly the reported Xinjiang forced labor issue, are complicating fashion companies’ sourcing decisions. Notably, US cotton apparel imports from China year-to-date (YTD) in 2020 (Jan to August) significantly decreased by 54% from a year ago, much higher than the 22% drop in US imports from the rest of the world. As a result, China’s market share in the US cotton apparel import market sharply declined from 22% in 2019 to only 15.1% in 2020 (Jan-Aug), a record low in the past ten years. This unusual trade pattern suggests that the concerns about social compliance risk are holding US fashion companies back from sourcing cotton apparel products from China. As the forced labor issue continues to evolve and become ever more sensitive and high profile, it is not unlikely that US fashion companies may substantially cut their China sourcing further, even if it is not a preferred choice economically.

Third, despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.2% YTD in 2020 vs. 16.2% in 2019), ASEAN (33.6% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.6% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.5% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

Likewise, thanks to a highly integrated regional textile and apparel supply chain, Asian countries all together were able to maintain fairly stable market shares on the world stage over the past decade despite all market disruptions, from the financial crisis, trade war to the wage increase.

Fourth, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first seven months of 2020, only 8.9% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first eight months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 28.0% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the contributing factors.

Further, industry sources show that the apparel products U.S. fashion companies import from members of USMCA and CAFTA-DR predominantly are tops and bottoms. The lack of production capacity for other product categories significantly limits the growth potential of these countries playing the role as a leading sourcing base.

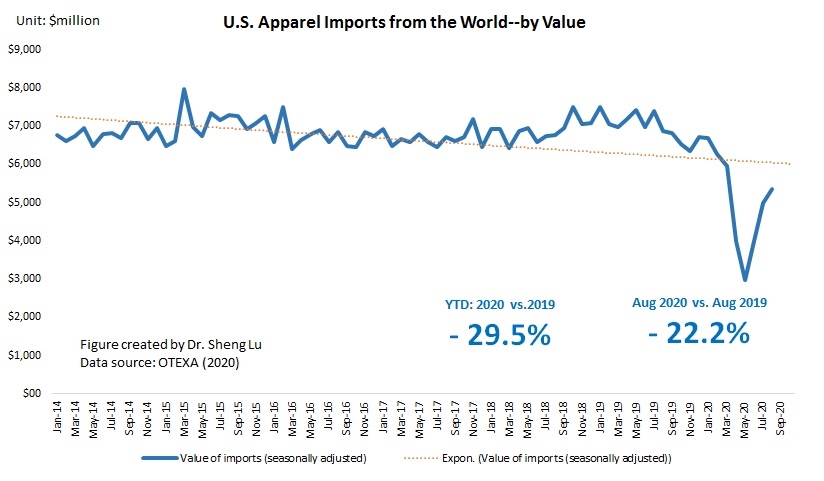

The latest statistics from the Office of Textiles and Apparel (OTEXA) show that the patterns of U.S. apparel imports continue to involve because of COVID-19 and the escalating US-China tensions. Meanwhile, there appeared to be more potent signs of gradual economic recovery in the U.S. driven by consumers’ robust demand. Specifically:

While the value of U.S. apparel imports decreased by 32.0% in July 2020 from a year ago, the speed of the decline has significantly slowed (was down 60% and 42.8% year over year in May and June 2020, respectively). This result echoes the trend of U.S. apparel retail sales (NAICS 448), which indicates a “V-shape” rebound since May 2020. As fashion brands and retailers typically build their inventory for holiday sales (such as back to school, Thanksgiving, and Christmas) from July to October, the upward trend of U.S. apparel imports could continue in the next two to three months.

Nevertheless, between January and July 2020, the value of U.S. apparel imports decreased by 30.7% year over year, which has been much worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

The latest trade statistics suggest that based on economic factors, U.S. fashion companies would like to continue to treat China as an essential apparel-sourcing base. As the first country hit by COVID-19, China’s apparel exports to the U.S. dropped by as much as 49.3% from January to July 2020 year over year. In February 2020, China’s market shares slipped to only 11%, and both in March and April 2020, U.S. fashion companies imported more apparel from Vietnam than from China. However, China had quickly regained its position as the top apparel supplier to the U.S., with a 26.3% market share in value and a 38.8% share in quantity in July 2020.

Different from the impact of the trade war, COVID-19 could benefit China as an apparel sourcing base as fashion companies have to “do more with fewer resources.” In general, China still enjoyed two notable advantages that other apparel supplying countries are unable to catch up in the short term. 1) unparalleled production capacity, meaning importers can source almost all products in any quantity from China vs. more limited production capacity (both in terms of variety and volume) in other alternative sourcing destinations. 2) China can mostly produce textile raw material locally vs. many apparel exporting countries still rely heavily on imported yarns and fabrics (supplied by China).

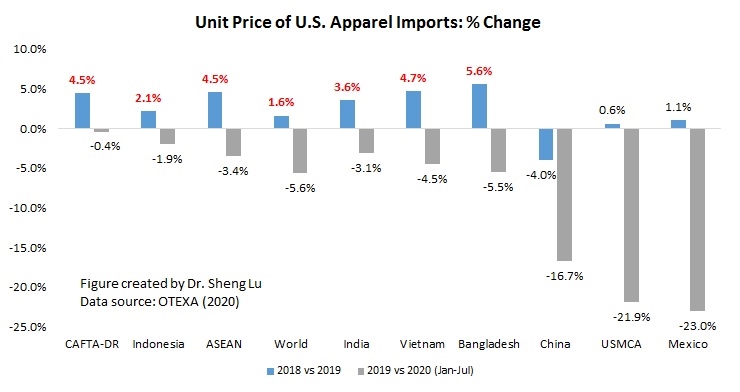

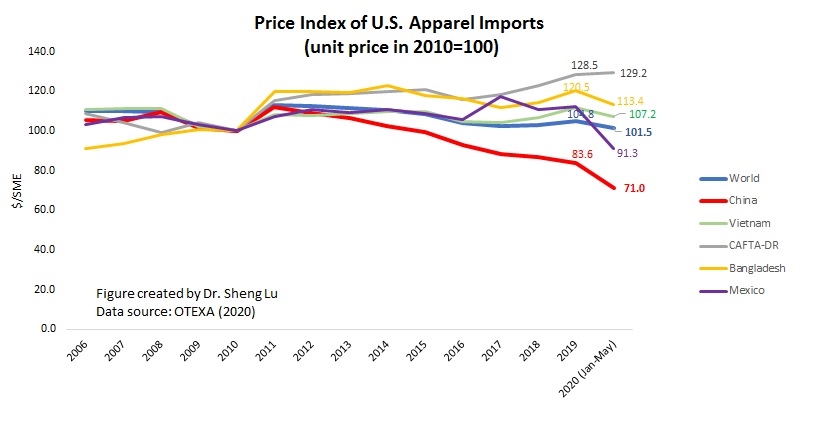

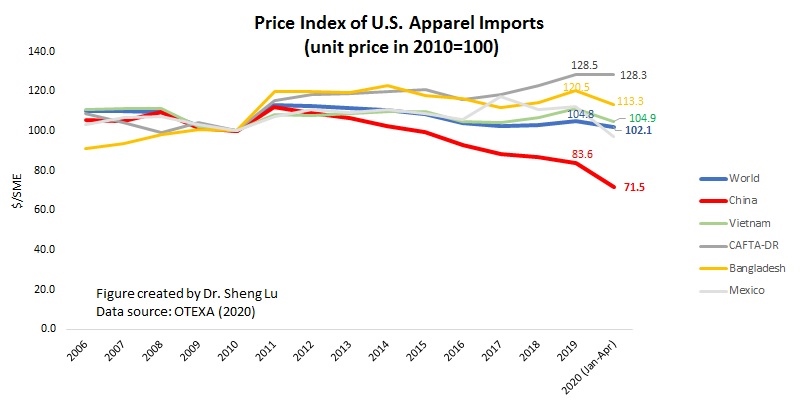

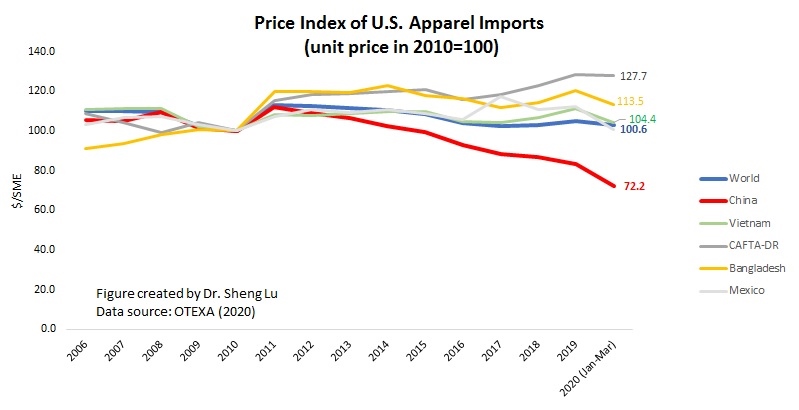

Contrary to common perceptions, apparel “Made in China” apparently are also becoming more price-competitive–the unit price slipped from $2.25/Square meters equivalent (SME) in 2019 to $1.88/SME in 2020 (January to July), or down more than 16.7% (compared with a 5.6% price drop of the world average). As of July 2020, the unit price of U.S. apparel import from China was only 65.7% of the world average, and around 25—35 percent lower than those imported from other Asian countries.

That being said, non-economic factors, from the deteriorating US-China relations to the reported Xinjiang forced labor issue, are increasingly complicating fashion companies’ sourcing decisions. Somehow as a warning sign, China’s market shares in the U.S. apparel import market slipped in both quantity and value terms in July 2020 compared with a month ago.

Despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.5% YTD in 2020 vs. 16.2% in 2019), ASEAN (34.3% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.6% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.5% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

However, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first seven months of 2020, only 8.8% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.1% from USMCA members (down from 4.5% in 2019). Confirming the trend, in the first seven months of 2020, the value of U.S. yarns and fabrics exports to USMCA and CAFTA-DR members also suffered a 28.9% decline from a year ago. The heavy reliance on textile supply from the U.S. (implying more vulnerability to the Covid-19 supply chain disruptions) and the price disadvantage could be among the contributing factors why near sourcing has been stagnant.

As a reflection of weak demand, the unit price of U.S. apparel imports was lower in the first six months of 2020. The price index declined from 104.7 in 2019 to 99.0 YTD (Jan to Jul) in 2020 (Year 2010 =100). The imports from Mexico (price index =86.4 YTD in 2020 vs. 112.1 in 2019) and China (price index = 69.7 YTD in 2020 vs. 83.5 in 2019) have seen the most notable price decrease so far.

By Victoria Langro(2020 UD Summer Scholar) and Dr. Sheng Lu (advisor)

Key findings:

US-UK bilateral apparel trade

Over the past decade, the US and UK bilateral trade in apparel enjoyed steady growth, reflecting ever closer business ties of fashion companies in the two countries. While US apparel exports still predominantly go to geographically nearby countries such as Mexico and Canada, the UK has emerged to become the single largest export market for “Made in the USA” apparel outside the Western Hemisphere. Similarly, the United States has always been the UK’s single largest export market outside the EU region.

On the other hand, the apparel products that the US and the UK export to each other target different segments of the market. Industry sources indicate that the clothing exported from the US to the UK primarily focuses on the premium market. Garments “Made in the USA” in the UK are mostly carried by premium brands and retailers such as Free People, J. Crew, and Moda Operandi. However, due to a lack of brand power, clothing “Made in the USA” is typically priced 30%-50% lower than similar products locally made in the UK or elsewhere in Western EU, such as France and Italy.

In comparison, approximately 70% of apparel exported from the UK to the US are luxury goods. With a relatively clear-cut market position, luxury and high-end designer UK brands, such as Burberry, Roland Mouret, and Victoria Beckham, can effectively reach out to their target markets.

How Might the US-UK FTA Affect the Bilateral Apparel Trade

According to the released negotiation objectives, both the US and the UK seem to be willing to consider a substantial cut or even a full elimination of the apparel tariff rate as part of the trade deal. Should this happen, fashion companies across the Atlantic could benefit from a proportional reduction of their sourcing cost, resulting in a considerable expansion of the US-UK bilateral apparel trade flows.

On the other hand, to enjoy the preferential duty benefit under a free trade agreement, rules of origin will always be a requirement. Notably, most US trade agreements currently adopt the so-called “yarn-forward” rules of origin. In contrast, most EU-based trade deals adopt a more liberal “fabric-forward” rule.

While it is hard to predict which specific rules of origin the proposed US-UK trade agreement will adopt, it seems the result will have a more significant impact on the US apparel exports to the UK than the other way around. Restrained by the limited domestic supply and high cost, a substantial proportion of US apparel exports contain imported textile raw materials. This means US apparel producers may have to either switch to use more expensive domestic textile inputs or forgo the FTA duty-saving benefits should restrictive rules of origin are adopted. Meanwhile, the UK apparel exports to the US will be less sensitive to the rules of origin in the proposed FTA, as most of these luxury items are already 100% “Made in the UK” to meet customers’ expectations.

Uncertainties associated with the US-UK FTA

The US-UK trade negotiations have to deal with an evolving Brexit. Given the EU’s economic cloud, understandably, some argue that the UK may have to reach a comprehensive trade agreement with the EU before it can consider a trade deal with the US. Additionally, several US domestic politics and policy factors may further slow down the progress of the US-UK trade negotiation, from the US presidential election to the upcoming expiration of the trade promotion authority (TPA).

Impact of COVID19 on Fashion Companies’ Businesses

The overwhelming majority of respondents report “economic and business impacts of the coronavirus (COVID-19)” as their top business challenge in 2020. The business difficulties caused by COVID-19 will not go away anytime soon, and U.S. fashion companies have to prepare for a medium to the long-term impact of the pandemic.

COVID-19 has caused severe supply chain disruptions to U.S. fashion companies. The disruptions come from multiple aspects, ranging from a labor shortage, shortages of textile raw materials, and a substantial cost increase in shipping and logistics.

COVID-19 has resulted in a widespread sales decline and order cancellation among U.S. fashion companies. Almost all respondents (96 percent) expect their companies’ sales revenue to decrease in 2020.

As sales drop and business operations are significantly disrupted, not surprisingly, all respondents (100 percent) say they more or less have postponed or canceled sourcing orders. Nearly half of self-identified retailers say the sourcing orders they canceled or postponed go beyond the 2nd quarter of 2020. Another 40 percent expect order cancellation and postponement could extend further to the fourth quarter of 2020 or even beyond. The order cancellation or postponement has affected vendors in China, Bangladesh, and India the most.

Impact of COVID-19 and US-China Trade War on Fashion Companies’ Sourcing

As high as 90 percent of respondents explicitly say, the U.S. Section 301 action against China has increased their company’s sourcing cost in 2020, up from 63 percent last year.

COVID-19 and the trade war are pushing U.S. fashion companies to reduce their “China exposure” further. While “China plus Vietnam plus Many” remains the most popular sourcing model among respondents, around 29 percent of respondents indicate that they source MORE from Vietnam than from China in 2020, up further from 25 percent in 2019.

As U.S. fashion companies are sourcing relatively less from China, they are moving orders mostly to China’s competitors in Asia. All respondents (100 percent) say they have “moved some sourcing orders from China to other Asian suppliers” this year, up from 77 percent in 2019.

However, no clear evidence suggests that U.S. fashion companies are sourcing more from the Western Hemisphere because of COVID-19 and the U.S.-China trade war.

Emerging Sourcing Trends

Sourcing diversification is slowing down, and more U.S. fashion companies are switching to consolidate their existing sourcing base. Close to half of the respondents say they plan to “source from the same number of countries, but work with fewer vendors,” up from 40 percent in last year’s survey.

China most likely will remain a critical sourcing base for U.S. fashion companies. However, non-economic factors could complicate companies’ sourcing decisions. Benefiting from U.S. fashion companies’ reduced sourcing from China, Vietnam and Bangladesh are expected to play a more significant role as primary apparel suppliers for the U.S. market.

Given the supply chain disruptions experienced during the pandemic, U.S. fashion companies are more actively exploring “Made in the USA” sourcing opportunities to improve agility and flexibility and reduce sourcing risks. Around 25 percent of respondents expect to somewhat increase sourcing locally from the U.S. in the next two years, which is the highest level since 2016.

US-Mexico-Canada Trade Agreement (USMCA)

For companies that were already using NAFTA for sourcing, the vast majority (77.8 percent) say they are “ready to achieve any USMCA benefits immediately,” up more than 31 percent from 2019. Even for respondents who were not using NAFTA or sourcing from the region, about half of them this year say they may “consider North American sourcing in the future” and explore the USMCA benefits. Some respondents expressed concerns about the rules of origin changes. These worries seem to concentrate on denim products in particular.

African Growth and Opportunity Act (AGOA)

Close to 37 percent of respondents say they have been sourcing MORE textile and apparel from sub-Saharan Africa (SSA) since the latest AGOA renewal in 2015, a substantial increase from 27 percent in the 2019 survey. More than 40 percent of respondents say AGOA and its “third-country fabric provision” are critical for their sourcing from the SSA region. More than 40 percent of respondents say AGOA and its “third-country fabric provision” are critical for their sourcing from the SSA region.

However, respondents still demonstrate a low level of interest in investing in the SSA region directly. Around 27 percent of respondents say the temporary nature of AGOA and the uncertainty associated with the future of the agreement have discouraged them.

With AGOA’s expiration date quickly approaching, the discussions on the future of the agreement and the prospect of sourcing from SSA begin to intensify. Among the various policy options to consider, “Renew AGOA for another ten years with no major change of its current provisions” and “Replace AGOA with a permanent free trade agreement that requires reciprocal tariff cut and continues to allow the third-country fabric provision” are the most preferred by respondents.

The latest statistics from the Office of Textiles and Apparel (OTEXA) show that while the negative impacts of COVID-19 on U.S. apparel imports continued in June 2020, there appeared to be early signs of economic recovery. Specifically:

While the value of U.S. apparel imports decreased by 42.8% in June 2020 from a year ago, the speed of the decline has slowed (was down 60% year over year in May 2020). Nevertheless, between January and June 2020, the value of U.S. apparel imports decreased by 30.4% year over year, which has been much worse than the performance during the 2008-2009 global financial crisis (down 11.8%).

The latest trade statistics support the view that U.S. fashion companies continue to treat China as an essential apparel-sourcing base, despite COVID-19, the trade war, and companies’ sourcing diversification strategy. As the first country hit by COVID-19, China’s apparel exports to the U.S. dropped by as much as 49.0% from January to June 2020 year over year. In February 2020, China’s market shares slipped to only 11%, and both in March and April 2020, U.S. fashion companies imported more apparel from Vietnam than from China. However, China’s apparel exports to the U.S. are experiencing a “V-shape” recovery: as of June 2020, China had quickly regained its position as the top apparel supplier to the U.S., with a 29.1% market share in value and 43.4% share in quantity.

Moreover, U.S. apparel imports from China are also becoming more price-competitive—the unit price slipped from $2.25/Square meters equivalent (SME) in 2019 to $1.88/SME in 2020 (January to June), or down more than 16% (compared with a 4.6% price drop of the world average). As of June 2020, the unit price of U.S. apparel import from China was only 65% of the world average, and around 25—35 percent lower than those imported from other Asian countries. On the other hand, the official Chinese statistics report a 19.4% drop in China’s apparel exports to the world in the first half of 2020.

Despite Covid-19, Asia as a whole remains the single largest source of apparel for the U.S. market. Other than China, Vietnam (20.3% YTD in 2020 vs. 16.2% in 2019), ASEAN (34.4% YTD in 2020 and vs. 27.4% in 2019), Bangladesh (8.9% YTD in 2020 vs.7.1% in 2019), and Cambodia (4.5% YTD in 2020 vs. 3.2% in 2019) all gain additional market shares in 2020 from a year ago.

However, still, no clear evidence suggests that U.S. fashion brands and retailers have been giving more apparel sourcing orders to suppliers from the Western Hemisphere because of COVID-19 and the trade war. In the first six months of 2020, only 8.8% of U.S. apparel imports came from CAFTA-DR members (down from 10.3% in 2019) and 4.2% from NAFTA members (down from 4.5% in 2019).

Notably, U.S. fashion companies source products from Asia (including China) and the Western Hemisphere for different purposes. In general, US companies tend to source either price-sensitive or more sophisticated items from Asia, where factories overall have higher productivity and more advanced production techniques. Meanwhile, the Western Hemisphere is typically used to source products that require faster speed-to-market or more frequent replenishments during the selling season. Some studies further show that there is more divergence in the products imported into the United States from Asian countries and the Western Hemisphere from 2015 to 2019. In contrast, over the same period, China, ASEAN, and Bangladesh appear to be exporting increasingly similar products to the United States.

That being said, as USMCA enters into force on July 1, 2020, a more stable trading environment could encourage more U.S. apparel sourcing from Mexico down the road (assuming garment factories there can gradually resume production and no further COVID-19 related shutdown).

As a reflection of weak demand, the unit price of U.S. apparel imports dropped in the first six months of 2020 (price index =100, meaning the same nominal price as in 2010). The price index was 104.7 in 2019. The imports from Mexico (price index =87.1 YTD in 2020 vs. 112.1 in 2019) and China (price index = 69.9 YTD in 2020 vs. 83.5 in 2019) have seen the most notable price decrease so far.

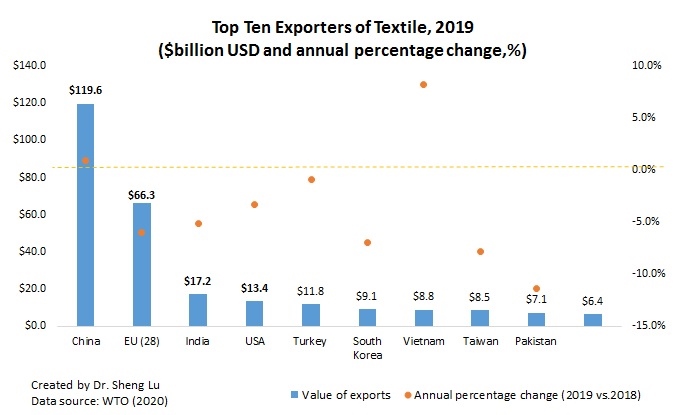

First, the volume of world textiles and apparel trade reduced in 2019 due to weakened demand and the negative impacts of trade tensions. According to the WTO, the value of the world textiles (SITC 65) and apparel (SITC 84) exports totaled $305bn and $492bn in 2019, respectively, decreased by 2.4% and 0.4% from a year ago. The world merchandise trade also fell by nearly 3% measured by value and 0.1% measured by volume 2018-2019, in contrast with a positive 2.8% growth 2017-2018. Put these numbers in context, the year 2019 was the first time that world merchandise trade fell since the 2008 global financial crisis, and the decline happened even before the pandemic. As noted by the WTO, the economic slowdown and the escalating trade tensions, particularly the tariff war between the United States and China, were among the major contributing factors for the contraction of trade flows.

Second, the pattern of world textile exports overall stays stable in 2019; Meanwhile, China and Vietnam continue to gain momentum. China, European Union (EU28), and India remained the world’s top three exporters of textiles in 2019. Altogether, these top three accounted for 66.9% of the value of world textile exports in 2019, almost no change from two years ago. Notably, despite the headwinds, China and Vietnam stilled enjoy the positive growth of their textile exports in 2019, up 0.9%, and 8.3%, respectively. In particular, Vietnam exceeded Taiwan and ranked the world’s seventh-largest textile exporter in 2019 ($8.8bn of exports, up 8.3% from a year earlier), the first time in history. The change also reflects Vietnam’s efforts to continuously upgrade its textile and apparel industry and strengthen the local textile production capacity are paying off.

Third, the pattern of world apparel exports reflects fashion companies’ shifting strategies to reduce sourcing from China. China, the European Union (EU28), Bangladesh, and Vietnam unshakably remained the world’s top four exporters of apparel in 2019. Altogether, these top four accounted for as much as 71.4% of world market shares in 2019, which, however, was lower than 74% from 2016 to 2018—primarily due to China’s reduced market shares.

China is exporting less apparel and more textiles to the world. Notably, China’s market shares in world apparel exports fell from its peak of 38.8% in 2014 to a record low of 30.8% in 2019 (was 31.3% in 2018). Meanwhile, China accounted for 39.2% of world textile exports in 2019, which was a new record high. It is important to recognize that China is playing an increasingly critical role as a textile supplier for many apparel-exporting countries in Asia.

On the other hand, even though apparel exports from Vietnam (up 7.7%) and Bangladesh (up 2.1%) enjoyed fast growth in absolute terms in 2019, their gains in market shares were quite limited (i.e., no change for Vietnam and marginally up 0.3 percentage point from 6.8% to 6.5% for Bangladesh). This result indicates that due to capacity limits, no single country has yet emerged to become the “Next China.” Instead, China’s lost market shares in apparel exports were fulfilled by a group of Asian countries altogether.

Fourth, associated with the shifting pattern of world apparel production, the world textile import is increasingly driven by apparel-exporting countries in the developing world. Notably, 2019 marks the first time that Vietnam emerged to become one of the world’s top three largest importers of textiles, primarily due to its expanded apparel production and heavy dependence on imported textile raw materials. In comparison, although the US and the EU remain the world’s top two largest textile importers, their total market shares had declined from nearly 40% in 2010 to only 31.2% in 2019, the lowest in the past ten years. Furthermore, both the US and the EU have been importing more finished textile products (such as home furnishings and carpets) as well as highly specialized technical textiles, rather than conventional yarns and fabrics for apparel production purposes. The weakening import demand for intermediary textile raw materials also suggests that reshoring (i.e., making apparel locally rather than sourcing from overseas) has NOT become a mainstream industry practice in the developed economies like the US and the EU.

Fifth, the world apparel import market is becoming ever more diversified as import demand is increasingly coming from emerging economies with a booming middle class. Affected by consumers’ purchasing power (often measured by GDP per capita) and size of the population, the European Union (EU28), US, and Japan remained the world’s top three importers of apparel in 2019. This pattern has lasted for decades. Altogether, these top three absorbed 58.1% of world apparel in 2019, which, however, was a new historic low (was 84% back in 2005). Behind the numbers, it is not the case that consumers in the EU, US, and Japan are necessarily purchasing less clothing. Instead, several emerging economies are becoming fast-growing apparel consumption markets and starting to import more. For example, China’s apparel imports totaled $8.9bn in 2019, up 8.1% from a year earlier. From 2010 to 2019, China’s apparel imports enjoyed a nearly 15% annual growth, compared with only 1.9% of the traditional top three.

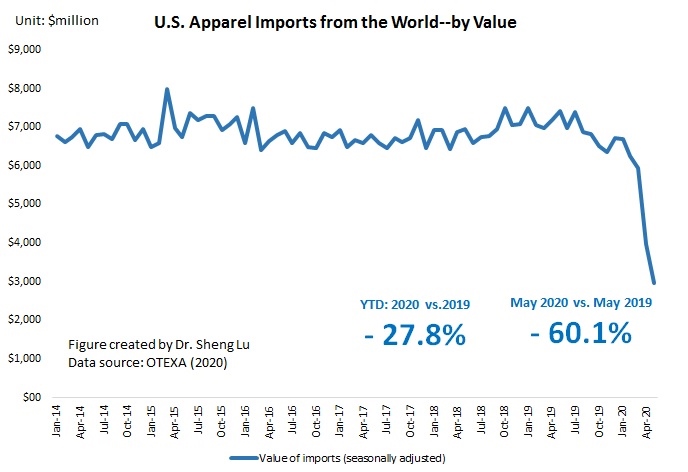

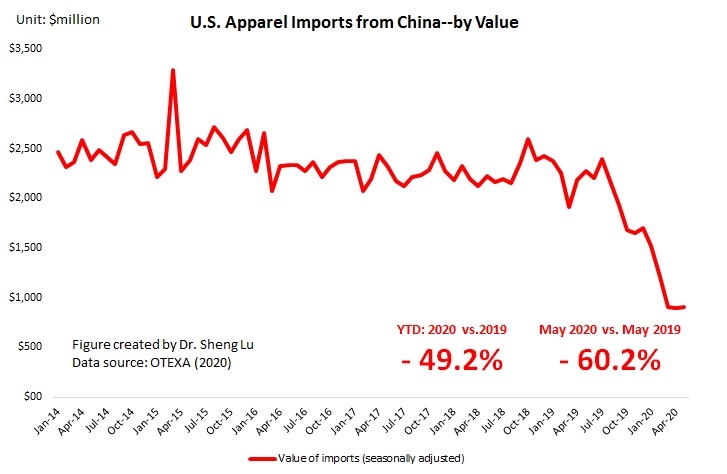

The latest statistics from the Office of Textiles and Apparel (OTEXA) show that COVID-19 continued to enlarge its negative impact on U.S. apparel imports in May 2020, and the path to recovery will NOT be straightforward and quick. Specifically: